Sample Category Title

Forward Guidance: Canada’s Economy Steadied in Q3 After Trade-Led Contraction in Q2

We expect the Canadian economy grew an annualized 0.5% in Q3—a partial reversal of the 1.6% decline in Q2 when international trade disruptions plunged exports lower.

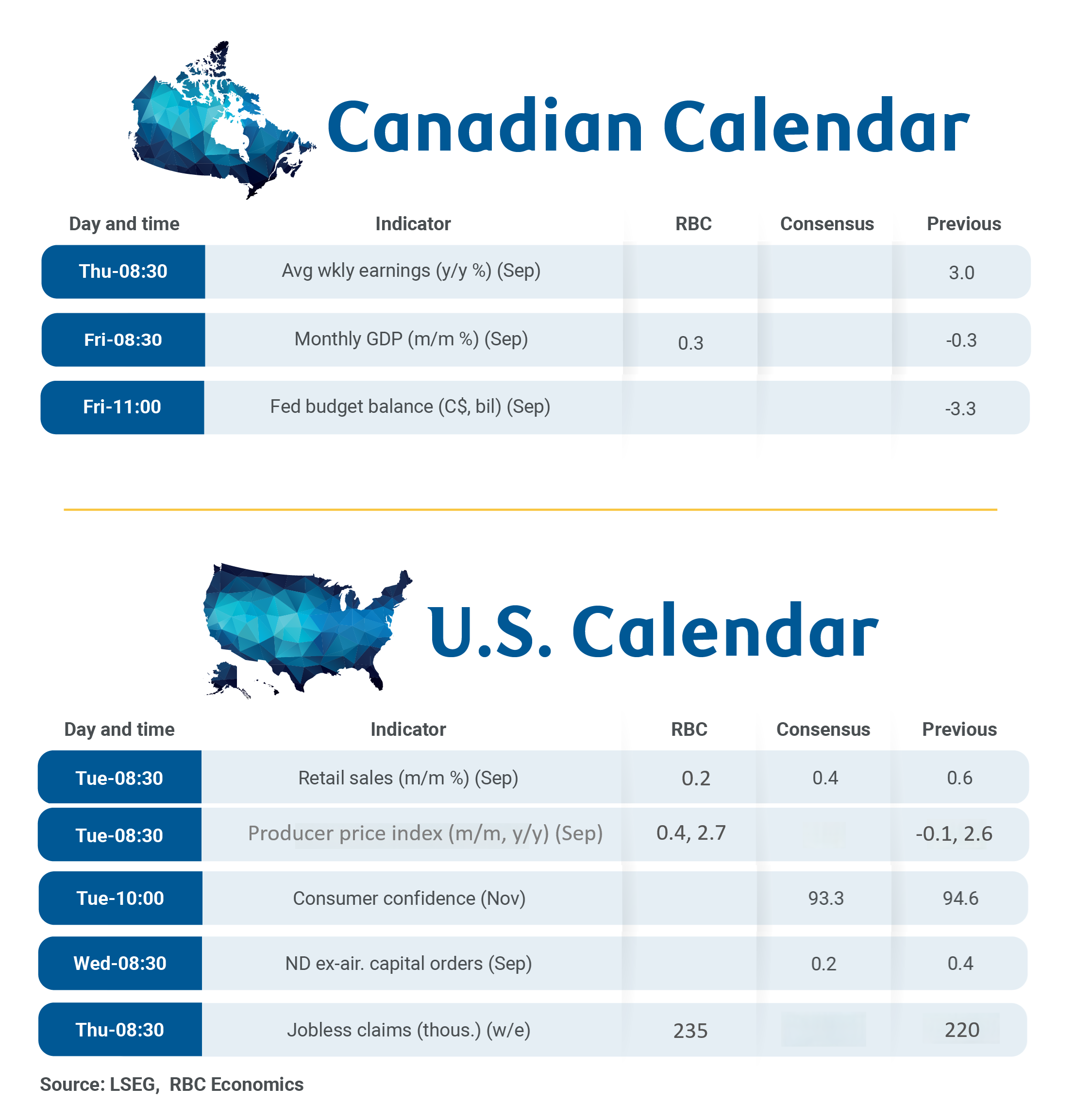

Next Friday’s Q3 gross domestic product appears backloaded with (what we expect will be) a 0.3% bounce-back in September after a surprise 0.3% contraction in August. That is firmer than the 0.1% preliminary estimate from Statistics Canada, but consistent with further acceleration in growth in Q4.

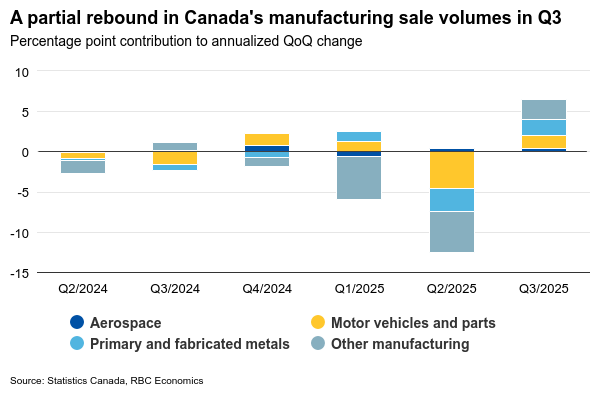

Heavily trade exposed industries continued to broadly underperform in Q3, but have shown further signs of stabilization. Manufacturing and wholesale sales volumes rebounded by an annualized 6 ½ % in Q3 to partially reverse large declines (-11.7% and -9%, respectively) in Q2.

Offsetting weakness in the trade exposed sectors is domestic Canadian demand that has remained relatively resilient so far. Business investment likely contracted in Q3, but our tracking of RBC card transactions points to further, albeit slower growth in consumer spending after a large increase in Q2. Residential investment is expected to have risen again in Q3 as well, following a gradual pick-up in home resales since March.

Net international trade data through August is on pace to add slightly to growth in Q3 after record subtraction from Q2 GDP (outside 2020 pandemic lockdowns) when exports plunged on lower shipments to the United States.

Missing September trade data could lead to revisions

Canadian international trade data for September is still missing. Statistics Canada relies on U.S. Census Bureau for information on Canadian exports to the U.S. that has been delayed by the six-week U.S. government shutdown. It’s, therefore, likely the quarterly Canadian trade data in the GDP add-up will include imputations, and could see larger-than-normal revisions in the future.

Overall, early indicators for monthly September GDP have been positive. Manufacturing sales volume jumped 2.7%—the largest one-month increase since January 2023. Oil production increased almost 3% in September by our estimates, and is on track to add positively to Q3 GDP growth after wildfires and maintenance related disruptions dampened oil sands production in Q2.

Air transportation also contributed to GDP growth in September after a strike in August temporarily weighed on output. Soft spots for growth in September include retail sales volume which pulled back 0.8%, and mining output (ex-oil & gas) that by our count edged lower for a second straight month.

Week ahead data watch:

September Survey of Employment, Payrolls and Hours data on Thursday should show moderation in declining job vacancies, following recent stabilization in timelier Indeed job openings data. Wage growth is expected to have further unwound, and the employment details will be closely watched for more signs of tariff impact among most targeted Canadian manufacturing sub-industries.

The end of the U.S. government shutdown will see a gradual return of economic data releases in the coming weeks. We expect next week’s retail sales will show a 0.2% in September and a smaller 0.1% rise in core sales. Producer price index is expected to have risen 0.4% in September, led by goods as tariff impact continue to flow through gradually. Core PPI is expected to have risen 0.3% in the same month.

Summary 11/24 – 11/28

Monday, Nov 24, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 09:00 | EUR | Germany IFO Business Climate Nov | 88.5 | 88.4 |

| 09:00 | EUR | Germany IFO Current Assessment Nov | 85.3 | |

| 09:00 | EUR | Germany IFO Expectations Nov | 91.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 09:00 | EUR | Germany IFO Business Climate Nov | |

| Forecast: 88.5 | Previous: 88.4 | ||

| 09:00 | EUR | Germany IFO Current Assessment Nov | |

| Forecast: | Previous: 85.3 | ||

| 09:00 | EUR | Germany IFO Expectations Nov | |

| Forecast: | Previous: 91.6 | ||

Tuesday, Nov 25, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | EUR | Germany GDP Q/Q Q3 F | 0.00% | 0.00% |

| 13:30 | USD | Retail Sales M/M Sep | 0.40% | 0.60% |

| 13:30 | USD | Retail Sales ex Autos M/M Sep | 0.30% | 0.70% |

| 13:30 | USD | PPI M/M Sep | 0.30% | -0.10% |

| 13:30 | USD | PPI Y/Y Sep | 2.70% | 2.60% |

| 13:30 | USD | PPI Core M/M Sep | -0.10% | |

| 13:30 | USD | PPI Core Y/Y Sep | 2.80% | |

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Sep | 1.60% | |

| 14:00 | USD | Housing Price Index M/M Sep | 0.40% | |

| 15:00 | USD | Consumer Confidence Nov | 93.4 | 94.6 |

| 15:00 | USD | Pending Homeles M/M Oct | 0% | |

| 15:00 | USD | Business Inventories Aug | 0.10% | 0.20% |

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | 2.70% | 3.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | EUR | Germany GDP Q/Q Q3 F | |

| Forecast: 0.00% | Previous: 0.00% | ||

| 13:30 | USD | Retail Sales M/M Sep | |

| Forecast: 0.40% | Previous: 0.60% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Sep | |

| Forecast: 0.30% | Previous: 0.70% | ||

| 13:30 | USD | PPI M/M Sep | |

| Forecast: 0.30% | Previous: -0.10% | ||

| 13:30 | USD | PPI Y/Y Sep | |

| Forecast: 2.70% | Previous: 2.60% | ||

| 13:30 | USD | PPI Core M/M Sep | |

| Forecast: | Previous: -0.10% | ||

| 13:30 | USD | PPI Core Y/Y Sep | |

| Forecast: | Previous: 2.80% | ||

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Sep | |

| Forecast: | Previous: 1.60% | ||

| 14:00 | USD | Housing Price Index M/M Sep | |

| Forecast: | Previous: 0.40% | ||

| 15:00 | USD | Consumer Confidence Nov | |

| Forecast: 93.4 | Previous: 94.6 | ||

| 15:00 | USD | Pending Homeles M/M Oct | |

| Forecast: | Previous: 0% | ||

| 15:00 | USD | Business Inventories Aug | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | |

| Forecast: 2.70% | Previous: 3.00% | ||

Wednesday, Nov 26, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Oct | 3.60% | 3.50% |

| 01:00 | NZD | RBNZ Interest Rate Decision | 2.25% | 2.50% |

| 09:00 | CHF | UBS Economic Expectations Nov | -7.7 | |

| 13:30 | USD | Initial Jobless Claims (Nov 21) | 226K | 220K |

| 13:30 | USD | Durable Goods Orders Sep | 0.20% | 2.90% |

| 13:30 | USD | Durable Goods Orders ex Transport Sep | 0.20% | 0.30% |

| 14:45 | USD | Chicago PMI Nov | 43.9 | 43.8 |

| 15:30 | USD | Crude Oil Inventories (Nov 21) | -3.4M | |

| 17:00 | USD | Natural Gas Storage (Nov 21) | -14B | |

| 19:00 | USD | Fed's Beige Book | ||

| 21:45 | NZD | Retail Sales Q/Q Q3 | 0.60% | 0.50% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q3 | 0.80% | 0.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Oct | |

| Forecast: 3.60% | Previous: 3.50% | ||

| 01:00 | NZD | RBNZ Interest Rate Decision | |

| Forecast: 2.25% | Previous: 2.50% | ||

| 09:00 | CHF | UBS Economic Expectations Nov | |

| Forecast: | Previous: -7.7 | ||

| 13:30 | USD | Initial Jobless Claims (Nov 21) | |

| Forecast: 226K | Previous: 220K | ||

| 13:30 | USD | Durable Goods Orders Sep | |

| Forecast: 0.20% | Previous: 2.90% | ||

| 13:30 | USD | Durable Goods Orders ex Transport Sep | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 14:45 | USD | Chicago PMI Nov | |

| Forecast: 43.9 | Previous: 43.8 | ||

| 15:30 | USD | Crude Oil Inventories (Nov 21) | |

| Forecast: | Previous: -3.4M | ||

| 17:00 | USD | Natural Gas Storage (Nov 21) | |

| Forecast: | Previous: -14B | ||

| 19:00 | USD | Fed's Beige Book | |

| Forecast: | Previous: | ||

| 21:45 | NZD | Retail Sales Q/Q Q3 | |

| Forecast: 0.60% | Previous: 0.50% | ||

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q3 | |

| Forecast: 0.80% | Previous: 0.70% | ||

Thursday, Nov 27, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Nov | 58.1 | |

| 00:30 | AUD | Private Capital Expenditure Q3 | 0.60% | 0.20% |

| 07:00 | EUR | Germany GfK Consumer Confidence Dec | -23.4 | -24.1 |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | 2.80% | 2.80% |

| 10:00 | EUR | Eurozone Economic Sentiment Nov | 96.8 | |

| 10:00 | EUR | Eurozone Industrial Confidence Nov | -8.2 | |

| 10:00 | EUR | Eurozone Services Sentiment Nov | 4 | |

| 10:00 | EUR | Eurozone Consumer Confidence Nov F | -14.2 | -14.2 |

| 12:30 | EUR | ECB Meeting Accounts | ||

| 13:30 | CAD | Current Account (CAD) Q3 | -14.4B | -21.2B |

| 23:30 | JPY | Tokyo CPI Y/Y Nov | 2.80% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Nov | 2.70% | 2.80% |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Nov | 2.80% | |

| 23:30 | JPY | Unemployment Rate Oct | 2.50% | 2.60% |

| 23:50 | JPY | Industrial Production M/M Oct P | -0.60% | 2.60% |

| 23:50 | JPY | Retail Trade Y/Y Oct | 0.80% | 0.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Nov | |

| Forecast: | Previous: 58.1 | ||

| 00:30 | AUD | Private Capital Expenditure Q3 | |

| Forecast: 0.60% | Previous: 0.20% | ||

| 07:00 | EUR | Germany GfK Consumer Confidence Dec | |

| Forecast: -23.4 | Previous: -24.1 | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Nov | |

| Forecast: | Previous: 96.8 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Nov | |

| Forecast: | Previous: -8.2 | ||

| 10:00 | EUR | Eurozone Services Sentiment Nov | |

| Forecast: | Previous: 4 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Nov F | |

| Forecast: -14.2 | Previous: -14.2 | ||

| 12:30 | EUR | ECB Meeting Accounts | |

| Forecast: | Previous: | ||

| 13:30 | CAD | Current Account (CAD) Q3 | |

| Forecast: -14.4B | Previous: -21.2B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Nov | |

| Forecast: | Previous: 2.80% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Nov | |

| Forecast: 2.70% | Previous: 2.80% | ||

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Nov | |

| Forecast: | Previous: 2.80% | ||

| 23:30 | JPY | Unemployment Rate Oct | |

| Forecast: 2.50% | Previous: 2.60% | ||

| 23:50 | JPY | Industrial Production M/M Oct P | |

| Forecast: -0.60% | Previous: 2.60% | ||

| 23:50 | JPY | Retail Trade Y/Y Oct | |

| Forecast: 0.80% | Previous: 0.50% | ||

Friday, Nov 28, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Private Sector Credit M/M Oct | 0.60% | 0.60% |

| 05:00 | JPY | Housing Starts Y/Y Oct | -4.90% | -7.30% |

| 07:00 | EUR | Germany Import Price Index M/M Oct | 0.30% | 0.20% |

| 07:00 | EUR | Germany Retail Sales M/M Oct | 0.30% | 0.20% |

| 07:45 | EUR | France GDP Q/Q Q3 | 0.50% | 0.50% |

| 08:00 | CHF | KOF Leading Indicator Nov | 100.8 | 101.3 |

| 08:00 | CHF | GDP Q/Q Q3 | -0.50% | 0.10% |

| 08:55 | EUR | Germany Unemployment Rate Oct | 6.30% | |

| 08:55 | EUR | Germany Unemployment Change Oct | 6K | -1K |

| 13:00 | EUR | Germany CPI M/M Nov P | -0.20% | 0.30% |

| 13:00 | EUR | Germany CPI Y/Y Nov P | 2.30% | |

| 13:30 | CAD | GDP M/M Sep | 0.20% | -0.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Private Sector Credit M/M Oct | |

| Forecast: 0.60% | Previous: 0.60% | ||

| 05:00 | JPY | Housing Starts Y/Y Oct | |

| Forecast: -4.90% | Previous: -7.30% | ||

| 07:00 | EUR | Germany Import Price Index M/M Oct | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 07:00 | EUR | Germany Retail Sales M/M Oct | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 07:45 | EUR | France GDP Q/Q Q3 | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 08:00 | CHF | KOF Leading Indicator Nov | |

| Forecast: 100.8 | Previous: 101.3 | ||

| 08:00 | CHF | GDP Q/Q Q3 | |

| Forecast: -0.50% | Previous: 0.10% | ||

| 08:55 | EUR | Germany Unemployment Rate Oct | |

| Forecast: | Previous: 6.30% | ||

| 08:55 | EUR | Germany Unemployment Change Oct | |

| Forecast: 6K | Previous: -1K | ||

| 13:00 | EUR | Germany CPI M/M Nov P | |

| Forecast: -0.20% | Previous: 0.30% | ||

| 13:00 | EUR | Germany CPI Y/Y Nov P | |

| Forecast: | Previous: 2.30% | ||

| 13:30 | CAD | GDP M/M Sep | |

| Forecast: 0.20% | Previous: -0.30% | ||

Week Ahead – Could US Data Revive Risk Appetite Amidst a Low Liquidity Week?

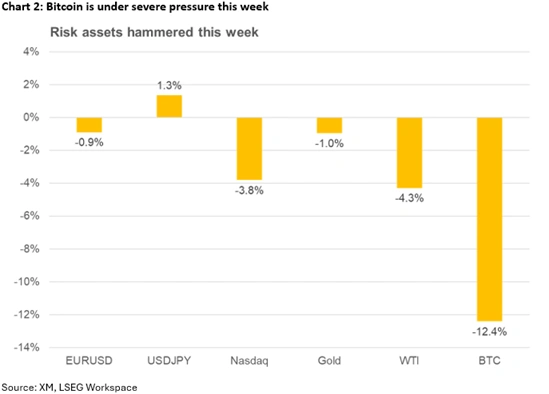

- Risk assets sell off on AI valuation concerns and hawkish Fedspeak.

- US data in focus amidst a holiday-shortened week with low liquidity available.

- Dollar weakness hinges on improved risk appetite and weak data releases.

- Fresh Ukraine-Russia peace deal pushes both oil and gold lower.

- Intervention risk heightens for yen; pound traders await Wednesday’s Budget.

Risk appetite falters this week, Nvidia fails to reverse sentiment

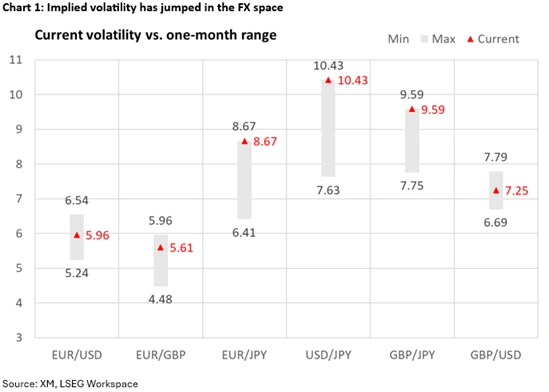

It has been a very difficult period for risk assets, with equities feeling the pressure throughout the week. At some stage, the three major US indices were 5.5-8.5% below their recent peaks, with technical analysis generating very bearish short-term signals. This market nervousness is clearly depicted in one-month implied volatility rising to new monthly highs.

Interestingly, Wednesday’s strong Nvidia earnings report and the upbeat commentary from its CEO failed to sustainably reverse the negative momentum. Investors continue to question the rallies posted by firms seen as AI leaders, and their investment announcements, which go beyond their current financial and manufacturing capabilities. Should AI-related concerns linger, it would be difficult to risk assets to meaningfully rally.

The situation is even worse in cryptocurrencies. Bitcoin is trading around $83k at the time of writing, 35% below its all-time high of $126k, almost fully erasing its post-April gains. The king of cryptos is down 18% this week – the strongest weekly drop since mid-November 2022 – with November primed to post the worst monthly performance since the June 2022 correction.

Hawkish Fedspeak also dampens risk sentiment

Beyond AI, hawkish Fedspeak has been branded as the main culprit for the negative risk appetite. Chances of the December rate cut have crashed to 27% from 90% before the October meeting, as the hawks have been extremely vocal lately, highlighting the lack of clean data posing the greatest obstacle for further rate cuts. The minutes from the latest FOMC meeting confirmed this hawkish stance, with the Fed doves scrambling to gather enough evidence to convince the board of the need for further easing.

Data in focus but shortened week implies minimal moves

Next week’s focus will probably be on the amended US data calendar. With the October CPI report missing, next week’s PCE print is critical for Fedspeak; a soft report may revive the current low December expectations, supporting risk appetite.

That said, consumer confidence could play an even greater role going forward. Persistent weakening in spending appetite could result in significantly weak Q4 GDP growth, highlighting the damage done by the shutdown. As a reminder, the recently approved bill funds the federal government until January 30, so the risk of another shutdown cannot be understated.

Notably, next week will be shortened due to Thursday’s US Thanksgiving holiday and Black Friday, when US markets will observe an early close, with noticeably lower liquidity available.

Trade tensions and geopolitics are wildcards for next week

Amidst this mixed environment, there are a couple of wildcards that could materially change market sentiment.

While trade tensions have abated, there are issues in the background that could result in flare-ups. Specifically, there is uncertainty about the US administration’s stance regarding foreign made chips – will Trump impose hefty tariffs? – and the currently debated ‘Gain AI’ bill in Congress. This bill requires US chip companies such as Nvidia to limit their exports, giving priority to domestic clients, potentially drawing China’s ire.

The second wildcard is the fresh US-brokered peace deal between Ukraine and Russia. Despite the plan appearing to favour Russia, and the initial negative reaction from Ukrainian officials, the current deal might be the only way to restart the negotiations between the two sides.

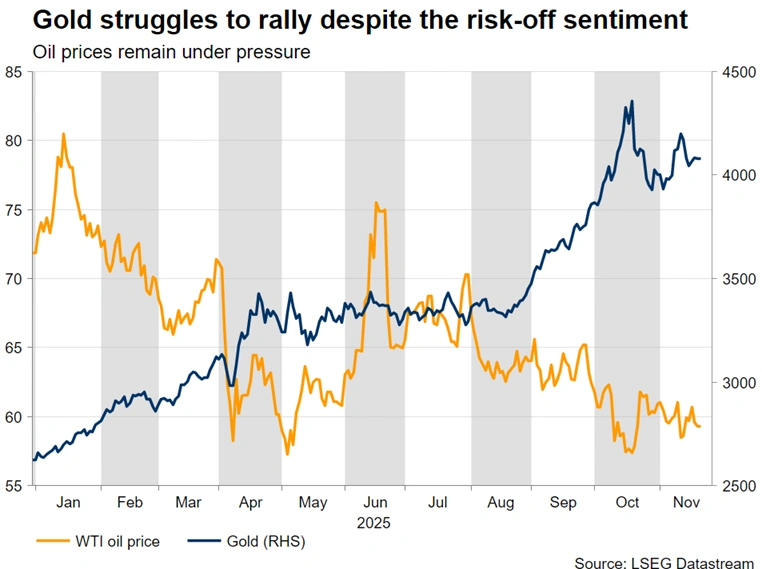

Concrete progress toward a resolution would support risk appetite, but dent gold’s current appeal. The precious metal has been dropping toward $4,000, unable to capitalize on the stock market weakness, potentially revealing its own weaknesses such as the overstretched 2025 rally. A move towards the late October low of $3,886 may challenge the prevailing long-term bullish trend.

Persistent risk-off sentiment could boost the Dollar

While both the US government reopening and the hawkish Fedspeak failed to boost the US dollar, the current stock market weakness is a different story. The greenback is posting gains this week, with euro/dollar testing the 1.1500 area once again. A boost in December Fed cut expectations, an improvement in risk appetite and positive news on the geopolitical stage could dent the dollar’s current appeal next week.

In the meantime, the newsflow from the euro area remains subdued, as most of the ECB members are content with the current monetary policy stance. Thursday’s minutes from the last ECB meeting are expected to confirm the current rates pause, with the focus quickly shifting to Friday’s preliminary Germany inflation report. The absence of a major downside surprise in this data print should make the final ECB meeting for 2025 more a formality than something that could capture the market’s attention.

UK budget in focus, pound in agony

Following months of speculation, Chancellor Reeves will present the 2026 Budget in Parliament on Wednesday, November 26. The market’s attention will be on the magnitude of tax increases, as Reeves attempts to close the current £20bn fiscal gap to remain on course to meet her own fiscal rules, and increase the fiscal headroom. Plans for higher personal taxes have been abandoned, but other revenue sources will be explored, with higher property taxes potentially in the frame.

With gilt yields climbing lately and the pound weakening aggressively, the budget could prove a make-or-break moment. Aggressive tax increases might initially please the market but could open the door to a severe government crisis, challenging PM Starmer’s ability to govern. The result will probably be higher gilt yields and a weaker pound.

A tax-light budget might also result in a negative market reaction as the Labour government would be then seen as lacking the resolve to take difficult decisions. Higher yields will not benefit the pound, with pound bears eyeing a decline towards the April 7, 2005 low of 1.2707 in pound/dollar.

The BoE will be left to pick up the pieces of the Budget, with an 82% probability currently assigned to a December rate cut following the softer October CPI report. An acute market reaction following the budget could further support current cut expectations and bring forward the next 25bps rate cut – after December’s meeting – currently fully priced in for July.

Yen weakness persists as BoJ fails to provide a lifeline

With Governor Ueda still sending mixed messages about the timing of the next rate hike, and PM Takaichi announcing a new stimulus plan of ¥21.3tr ($135bn) – the largest since 2022 – the yen remains under pressure. Next Friday’s critical Tokyo CPI might surprise on the upside, somewhat boosting the yen, but this might not prove enough to turn the tide.

Meanwhile, verbal interventions have intensified as dollar/yen reached 157.88 on Thursday. Should this move persist, with dollar/yen surpassing the 2025 high of 158.66 and getting close to the key 160 level, chances of an actual intervention would heighten. Notably, given the low liquidity market conditions expected for the latter part of next week, it might be the best opportunity for the BoJ to intervene and produce a meaningful drop in dollar/yen, should the need arise.

Likely peace deal pushes Oil lower

The latest developments regarding the Ukraine-Russia conflict have come into the spotlight, with a possible ceasefire agreement heavily influencing the outlook for the oil market, adding to the current bearish setup of unspectacular growth and oversupply. The bears crave a retest of the October lows, not far from the five-year low of $55.60 posted in early May.

On the other hand, failed Ukraine-Russia negotiations and renewed escalation on the battlefield – with Ukraine potentially targeting Russian oil and gas infrastructure – could result in a jump in oil prices, reversing the current bearish oil trend.

Could peripheral currencies react to this week’s underperformance against the Dollar?

With the aussie, the kiwi and the loonie posting sizeable losses against the dollar, next week’s calendar might offer them a chance for redemption. The Australian CPI report, the RBNZ meeting and the Canadian Q3 GDP could set the tone for the remainder of the year. Notably, the aussie appears to be best suited to take advantage of the greenback’s renewed weakness, while the kiwi remains the weakest of the bunch, as the RBNZ remains on an aggressive easing path.

Weekly Focus – Fears of AI Bubble Top the Agenda

Global stocks are heading towards their worst week since April with tech stocks under pressure. Despite Nvidia delivering yet another strong result and an upbeat revenue forecast, investor concerns regarding an AI bubble remain. The fears are not baseless. Investment growth in the US largely rests upon AI-related and high-tech investments, and at the same time, there is still a great level of uncertainty regarding AI-driven productivity gains. In addition, the market is increasingly concentrated. Nvidia's valuation alone exceeds the entire equity markets of most countries, and the rising number of interrelated deals in the tech sector has further fuelled investor concerns recently.

Understandably then, investors are looking for a hedge against AI risk. This has led to a rapidly rising demand for credit default swaps for companies like Oracle Corp, the software company that has borrowed massively to finance the AI-related spending spree. The company's 5-year CDS price has tripled since summer. Such price moves can hardly be explained by investors actually expecting Oracle, an investment-graded company, to default. Instead, investors probably anticipate the CDS price to rise further, should the AI concerns escalate.

This week, we also started receiving the US data delayed because of the government shutdown. The long-awaited September Jobs Report was released with mixed signals, as nonfarm payrolls growth recovered to +119k but the unemployment rate still rose to 4.4%. The uptick was driven by an increase in native-born labour supply rather than weak demand. As we do not expect labour supply to continue growing, we also do not see this as a dovish signal for Fed. Fed minutes, released earlier in the week, appeared slightly hawkish on the margin with "many participants" suggesting that rates could be kept unchanged in December. Hence, we still like our call for the next rate cut in January. Read more on US Labour Market Monitor - Calm before the storm?, 20 November.

In FX market, dollar was king this week. In the near term, risks remain tilted toward USD strength, but we continue to see EUR/USD at 1.22 in 12 months. Read more on FX forecast update - USD to weather AI valuation woes, 18 November. Japanese authorities are concerned about weak yen on the back of the expected fiscal easing, and on Friday, the authorities again flagged the possibility of FX intervention.

The US and Russian authorities have drafted a new peace plan for Ukraine, and Ukraine's President Zelensky has received the proposal. The new 28-point plan outlines that Ukraine would have to concede the whole of the Donbas region and cut down the number of reservists. Ukraine would not be allowed in NATO, but doors to the EU would be kept open. Although the 28-point plan clearly favours Russia, there is a separate document regarding security guarantees and those seem strong, NATO-like (see e.g. Axios reporting). Zelensky has been given time until next week Thursday to accept the deal.

The euro area preliminary PMI for November came in close to expectations with the composite index falling marginally to 52.4 from 52.5. On Monday, we will see how the German Ifo index aligns with the German PMI softening. Otherwise, next week is rather quiet in terms of data but watch out for US September retail sales and PPI due on Tuesday.

Sunset Market Commentary

Markets

The November PMIs stood in the shadow of a much more important market driver today: risk sentiment. Stocks continued to slide with European equities catching up with the US yesterday where strong Nvidia results did little to address growing market concerns about elevated AI-valuations. The EuroStoxx50 at some point shed 1.4%, piercing through three key levels that created a strong support zone between the 5568.19 pre Liberation Day peak, the 5522.42 Dot Com high in 2000 and the 5516.5 23.6% retracement on the April-Nov rally. Enter Fed Williams. NY Fed boss said he still sees room for another rate cut “in the near term”. As a confidant to chair Powell and following a string of more hawkish signals from other policymakers (including today), Williams’ comments drew attention and lifted sentiment somewhat. The turnaround lacks conviction but for now it’s enough for the Stoxx50 cut losses to 0.8%. Wall Street opens with minor gains. Investors similarly kept puking out crypto before Williams lured dip buyers from the sidelines. BTC came to close to the 80k mark before recovering to 84k currently. Core bonds attract safe haven flows. US yields decline 1.7-3.1 bps, led by the front end – which is now pricing a 70% December Fed cut probability. German rates ease 2.2-3.1 bps across the curve. UK gilts actually outperform core peers with the long end of the curve erasing an earlier rise this week (-5.5 bps). This tentative calm risks being upended short-term by the upcoming Autumn Budget due November 26 though. The stakes are incredibly high for both gilts and the pound. The latter trades a tad stronger on the day around but above EUR/GBP 0.88, ignoring weak retail sales and a sub-par November PMI. The services sector (53.1) in the European edition kept powering economic activity, with a pullback in Germany counterbalanced by a French catch-up move and the rest of the EU. The manufacturing sector (49.7) remains mired around the 50 neutral level. Rising new orders in services offset a renewed fall in manufacturing. Employment stagnated. Input costs rose sharply and across sectors but didn’t feed through one on one in selling prices. Their rise slowed to the weakest in just over a year. Business confidence for the year ahead ticked higher and was above the running 2025 average. The PMIs mattered not for EUR/USD though, which instead had more attention for the risk off and a drop in Q3 negotiated wage growth to sub 2% for the first time since 2021Q1. The pair is struggling north of the 1.15 big figure.

News & Views

The Hungarian 10-y swap yield suddenly rose 6 bps (to 6.83%) and the forint weakened from the EUR/HUF 382.4 area to EUR/HUF 385.5. The Hungarian currency later recovered a bit to currently near EUR/HUF 384. The move might at least partially be due to an overall negative risk sentiment. However domestic headlines also might have been in play. Deputy governor Barnabas Virag, responsible for research, money circulation and central bank programs quit the monetary policy committee early. The MNB indicates that the Hungarian Parliament will hear Peter Banai as a nominee to take over the role of Virag. Virag in the future will still serve as an adviser to MNB governor Varga. The move as seen as driven by political considerations as it allows the current government to fill the function for the next six year mandate, ahead of parliamentary elections that are expected to rake place in April next year. Even as the move isn’t expected to change the MNB monetary policy stance anytime soon, markets apparently might feel discomfort with political uncertainty/unexpected decisions for current government in the run-up to the elections.

The UK PMI indicates a softer expansion of private business activity during November. The composite index decreased from 52.2 to 50.5. Services slowed from 52.3 to 50.5. Output in manufacturing equally eased from 51.6 to 50.6. New services orders declined for the first time since July amid heightened client caution ahead of the November Budget. Manufacturing registered a first increase in total new orders in over a year. Average output prices rose at their slowest rate in nearly five years but input price pressures accelerated, putting margins under pressure. In a context of tight margins and heightened policy uncertainty, firms reduced their headcounts more aggressively than in October. Business activity expectations also moderated from October's 12-month peak. The PMI suggests no growth this month and corresponds with a meagre 0.1% Q4 quarterly pace. S&P assesses that “The PMI data therefore suggest the policy debate will shift further away from inflation worries toward the need to support the struggling economy, hence adding to the chances of interest rates being cut in December”, a view we endorse.

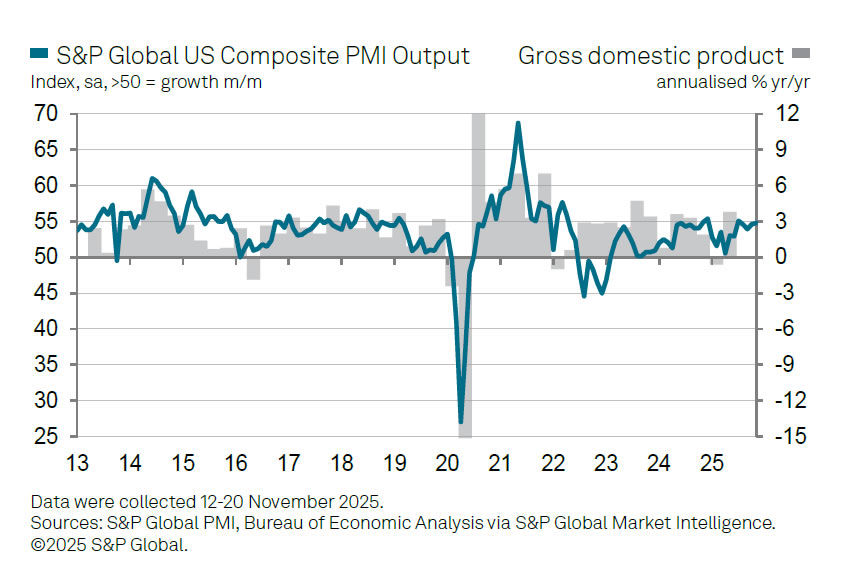

US PMI composite rises to 54.8, solid Q4 momentum but inflation pressures re-emerge

US business activity held firm in November, with the PMI Composite edging up from 54.6 to 54.8. The manufacturing index slipped from 52.5 to 51.9, while services climbed from 54.8 to 55.0. According to S&P Global’s Chris Williamson, the readings point to a “relatively buoyant” economy tracking around 2.5% annualized GDP growth so far in Q4, with the upturn "encouragingly broad-based".

Business confidence has also improved meaningfully, helped by expectations of further Fed rate cuts and relief following the reopening of the federal government. Williamson noted that optimism for the year ahead has strengthened as uncertainty surrounding policy and political risks recedes. Hiring continued in November, though firms remained cautious as tariffs and higher operating costs restrained labor demand.

Still, the PMI report highlighted pockets of concern. Manufacturers saw slower new orders growth while reporting a record rise in finished goods inventories. Price pressures also re-accelerated: both input costs and selling prices rose at faster rates, keeping the inflation debate alive within the Fed.

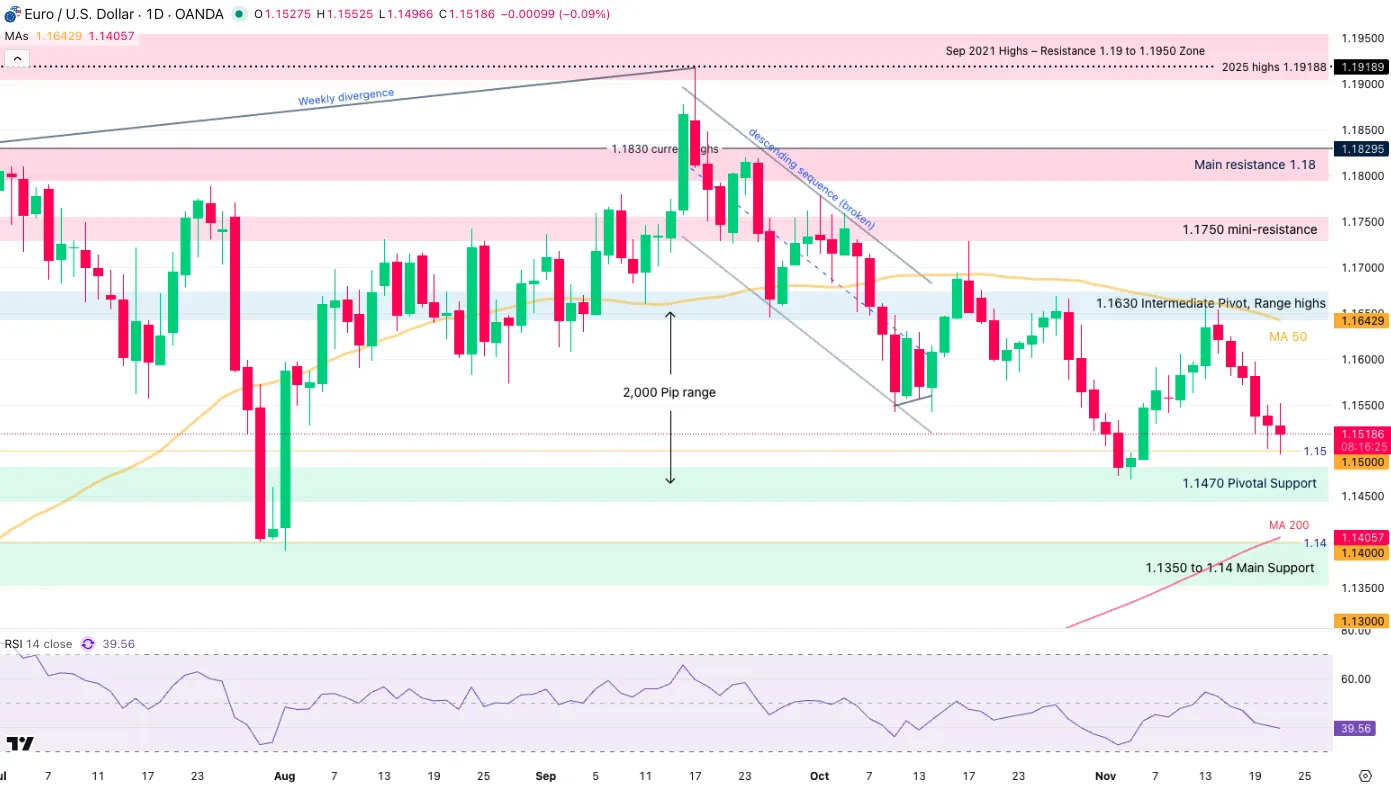

EUR/USD Technical Analysis: Spotting Mean Reversion in the 2,000 pip Range

After rebounding well through the past week, what was initially thought to be a broader trading range is actively contracting into a tight consolidation pattern.

Currently stuck between 1.15 and 1.17 (+/- 150 pips), the most popular FX pair hasn't been able to find a concrete direction since reaching its peak back in July.

The US Dollar made its point again earlier, fueled by the Fed's hawkish repricing as fears of a December "non-cut" created sudden demand for the Greenback, leading to a series of lower price action in the pair.

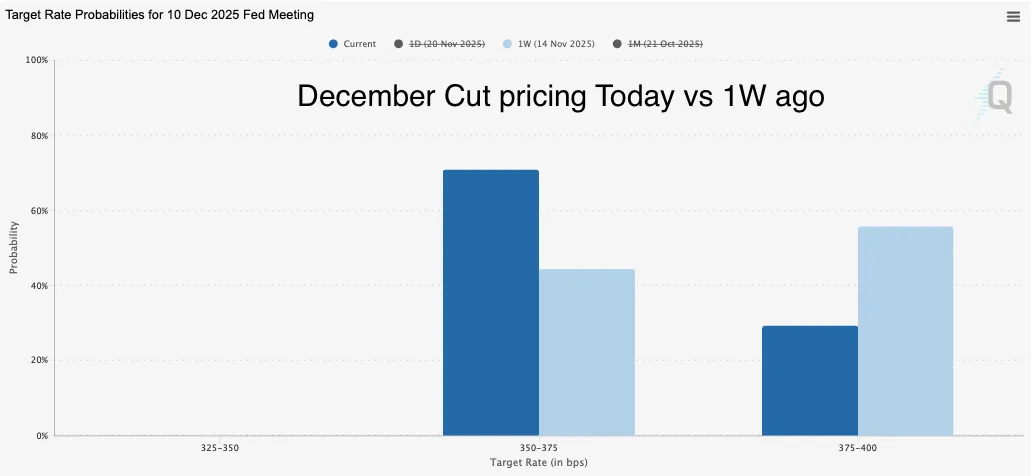

December Cut pricing, November 21, 2025 – Source: FedWatchTool

However, Fed member communication continues to heavily influence flows. Comments from NY Fed President John Williams—a very influential voice—have put the December cut back firmly on the table, bringing pricing right back around 70% from 20% just yesterday morning.

As cuts are typically negative for a currency, this shift has applied fresh pressure on the Dollar, potentially boosting the pair as it tests its range lows.

Meanwhile, Christine Lagarde mentioned in a recent speech that Europe is "increasingly vulnerable to shocks," noting that the AI boom has further amplified the volatility seen in EU stocks throughout 2025. In the context of EUR/USD, both economies remain highly vulnerable to such market developments.

Let's dive in EUR/USD multi-timeframe analysis.

EUR/USD Multi-timeframe Technical Analysis

Daily Chart

EUR/USD Daily Chart, November 21, 2025 – Source: TradingView

Oscillating between the 1.1470 Pivot Support zone and the 1.1650 Pivot Zone, the pair provides strong support and resistance levels to base analysis on.

2025 has been a trending year, but rangebound action takes place around 70% of the time in Markets and particularly in FX.

Hence, spotting ranges like these early can provide opportunities.

With the RSI also flattening, playing mean-reversion has high probabilities of functioning.

However, spot trends in the US Dollar: Strong numbers before the December 10 meeting can add further USD strength and break the 1.1470 Support. Let's take a closer look.

4H Chart and Technical Levels

EUR/USD 4H Chart, November 21, 2025 – Source: TradingView

EUR/USD responds well to overbought and oversold RSI levels, a good indicator of rangebound action.

Levels to place on your EUR/USD charts:

Resistance Levels

- 1.1630 to 1.1670 Pivot zone (range Highs)

- 1.1750 mini-resistance

- Resistance Zone around 1.18 (+/- 150 pips)

- Sep 2021 Highs – Resistance 1.19 to 1.1950 Zone

- Weekly highs 1.1656

Support Levels

- 1.1470 to 1.15 range support

- 4H MA 200 Mini-support 1.16190

- 1.1475 to 1.15 Support Zone

- 1.1350 to 1.14 Support

- Session lows 1.14966

1H Chart

EUR/USD 1H Chart, November 21, 2025 – Source: TradingView

Adding to the up-and-down price action, the key moving averages, particularly the longer 200-H MA is starting to flatten, indicating a non-trending environment.

Still, Traders will have to closely monitor the past week lows (1.1470) and highs (1.1656) to check for potential breakouts:

A daily close above or below such levels would be indicative of a potential breakout

Data can also have an influence on such trading ranges, therefore it is very important to keep track of releases.

Safe Trades!

Canada: Retail Sales Decline in September, Signal a Weak Start to the Holiday Season

Retail sales declined 0.7% month-on-month (m/m) in September, matching Statistics Canada's advanced estimate.

After adjusting for inflation, the volume of retail sales dropped 0.8% m/m.

Auto sales were the key swing factor in September, falling 2.9% m/m.

Receipts at gas stations and fuel vendors rose for the first time in three months, up 1.9% m/m, though this was driven by higher gasoline prices - volumes were down 1.0% m/m.

Core sales – excluding auto sales and receipts at gas stations – were flat on the month. Softness was concentrated in building material & garden equipment dealers (-2.0% m/m) and general merchandise retailers (-0.5% m/m), which pulled sales lower. Gains at food and beverage stores (+0.8% m/m) and miscellaneous store retailers (+1.8% m/m) offset the weakness.

E-commerce sales declined by 3.5% m/m in September, but August was revised up to +0.6% from -0.1% m/m.

Statistics Canada's advanced estimate points to a flat reading in October.

Key Implications

Retail sales are heading into the holiday season on shaky footing. September recorded a renewed decline, and early signals point to a flat reading in October. Despite recent volatility, the underlying trend is weaker real spending with major categories now in outright contraction. Some good news comes from our internal credit and debit card data, which continues to point to relatively healthy gains in services spending, especially travel and recreation.

We expect real personal spending growth to drift to a below-trend pace in the second half of 2025, with Q3 consumption tracking in a flat to 0.5% range. At this stage, the Bank of Canada has largely priced in this softer demand profile, giving policymakers sufficient justification to remain on hold.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.93; (P) 157.41; (R1) 157.94; More...

Intraday bias in USD/JPY remains neutral and some consolidations could be seen. Downside of retreat should be contained above 154.47 resistance turned support to bring another rally. Above 157.88 temporary top will resume larger rise to 161.8% projection of 146.58 to 153.26 from 149.37 at 160.17.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 restiveness turned support will dampen this bullish view and extend the corrective pattern with another falling leg.

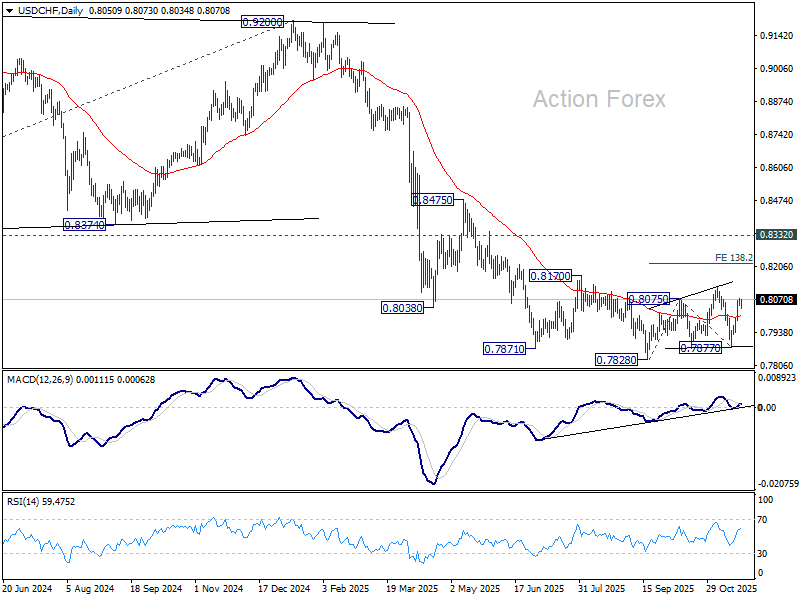

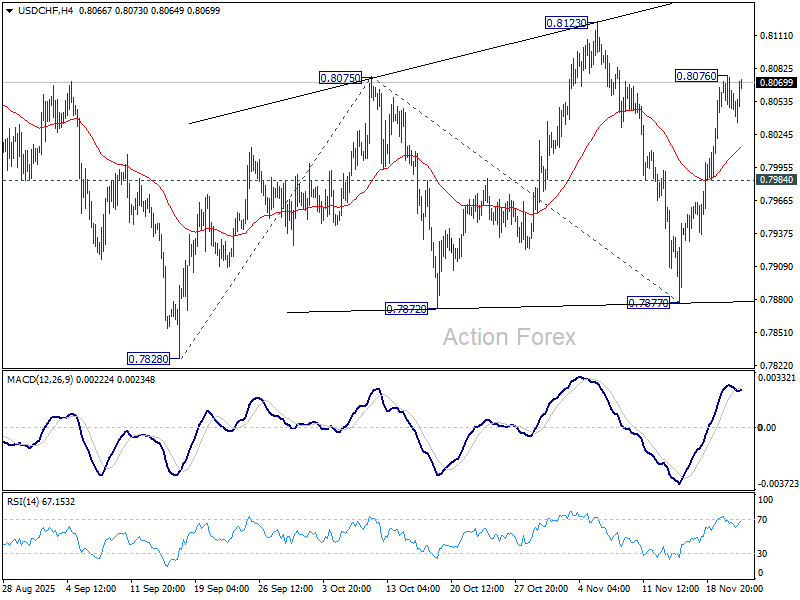

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8047; (P) 0.8062; (R1) 0.8076; More…

Intraday bias in USD/CHF remains neutral and more consolidations could be seen. Overall, corrective pattern from 0.7828 is still extending. Above 0.8076 will target 0.8123 resistance next. On the downside, though, break of 0.7984 support will bring deeper fall back to 0.7877 support.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).