Sample Category Title

AUD/USD Weekly Report

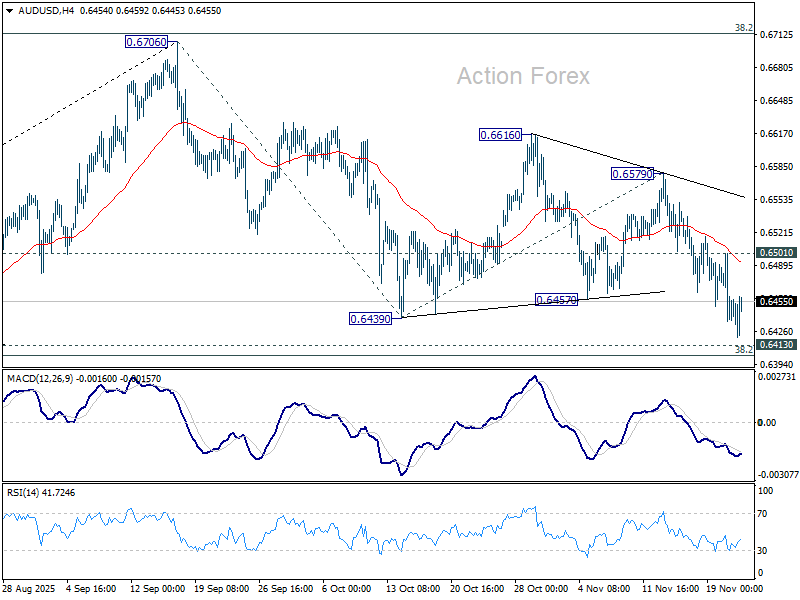

AUD/USD's fall from 0.6706 resumed by breaking through 0.6439 support last week. Initial bias stays on the downside for 0.6413 cluster (38.2% retracement of 0.5913 to 0.6706 at 0.6403). Decisive break there should confirm near term bearish reversal. Next target is 100% projection of 0.6706 to 0.6439 from 0.6579 at 0.6312. ON the upside, though, above 0.6501 minor resistance will turn intraday bias neutral first.

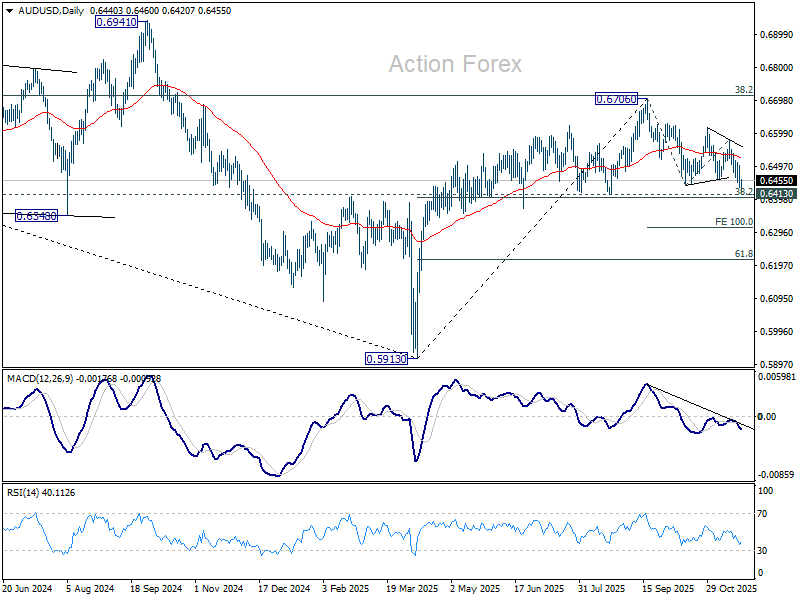

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Break of 0.6413 support will suggest rejection by 0.6713 and solidify this bearish case. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

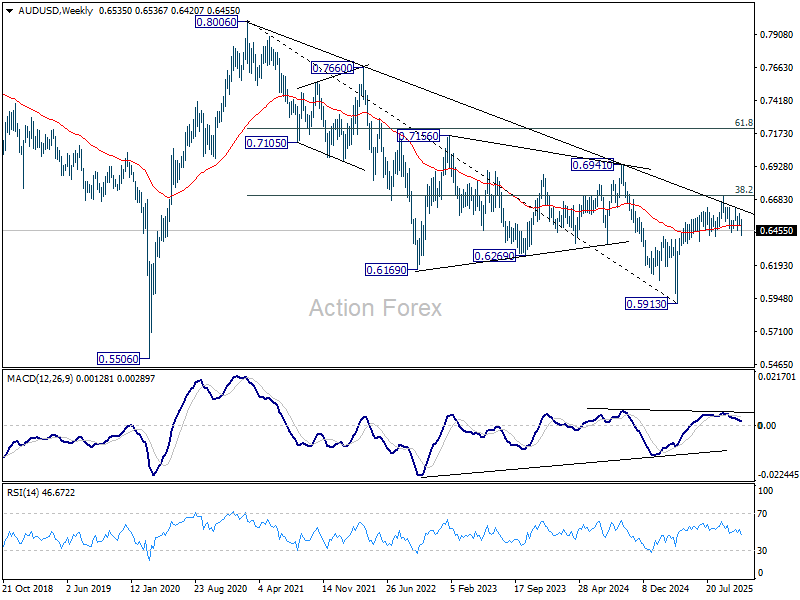

In the long term picture, fall from 0.8006 is seen as the second leg of the corrective pattern from 0.5506 long term bottom (2020 low). Hence, in case of deeper decline, strong support should emerge above 0.5506 to contain downside to bring reversal. On the upside, firm break of 0.6941 will argue that the third leg has already started back to 0.8006.

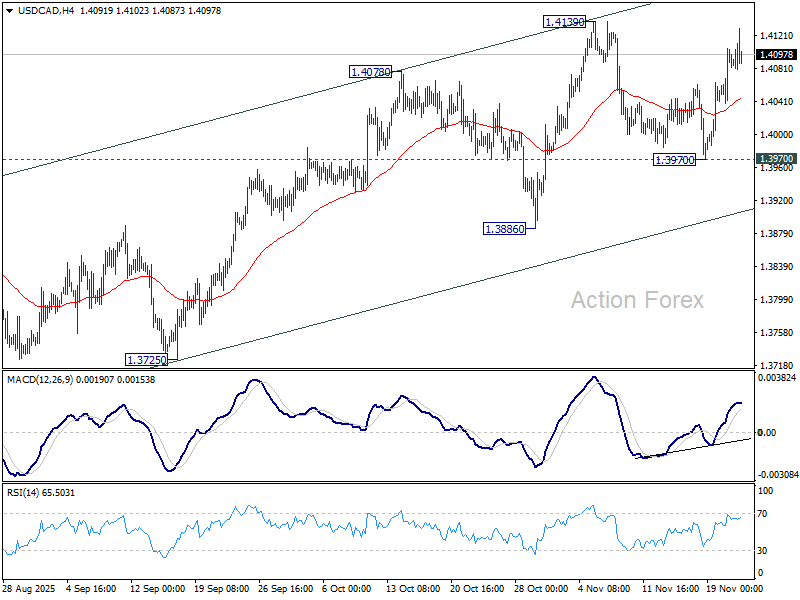

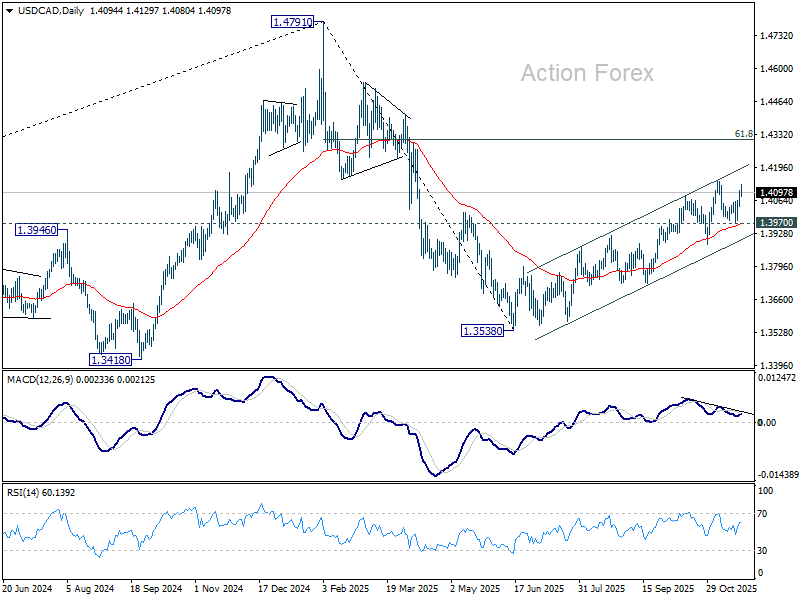

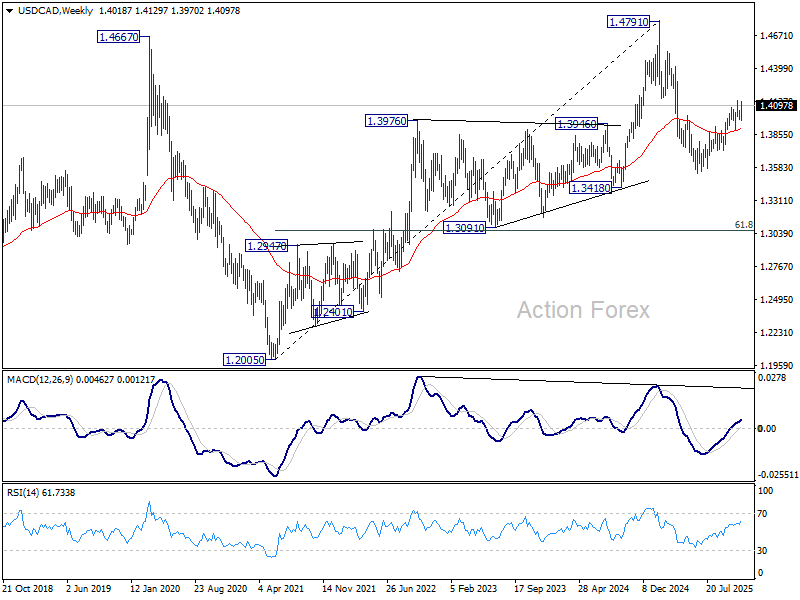

USD/CAD Weekly Outlook

USD/CAD rebounded strongly after initial dip to 1.3970 last week, but upside is capped below 1.4139 resistance for now. Initial bias remains neutral this week first. Outlook stays bullish as rally from 1.3538 is in progress. Break of 1.4139 will confirm resumption and target 61.8% retracement of 1.4791 to 1.3538 at 1.4312. Risk will stay on the upside as long as 1.3970 support holds, in case of retreat.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low), with rise from 1.3538 as the second leg. A third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.

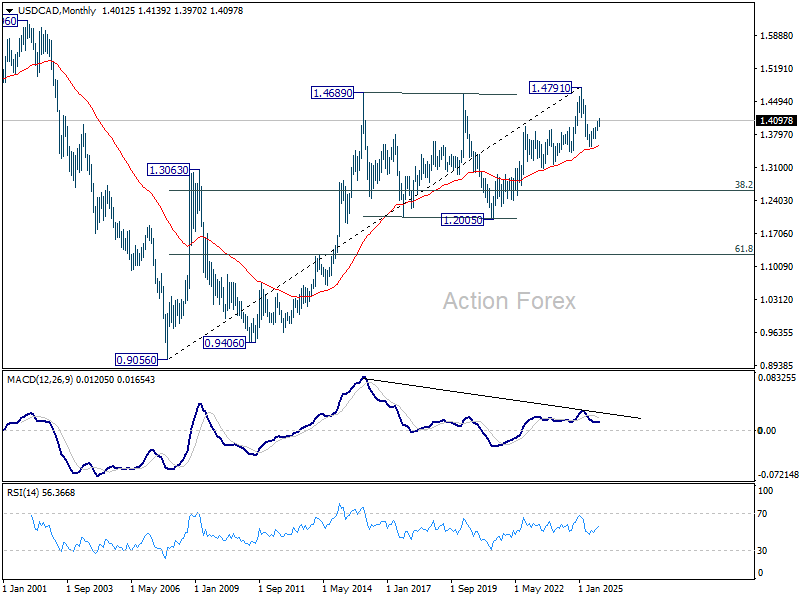

In the long term picture, rising 55 M EMA (now at 1.3562) remains intact. Thus, up trend from 0.90567 (2007 low) should still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction.

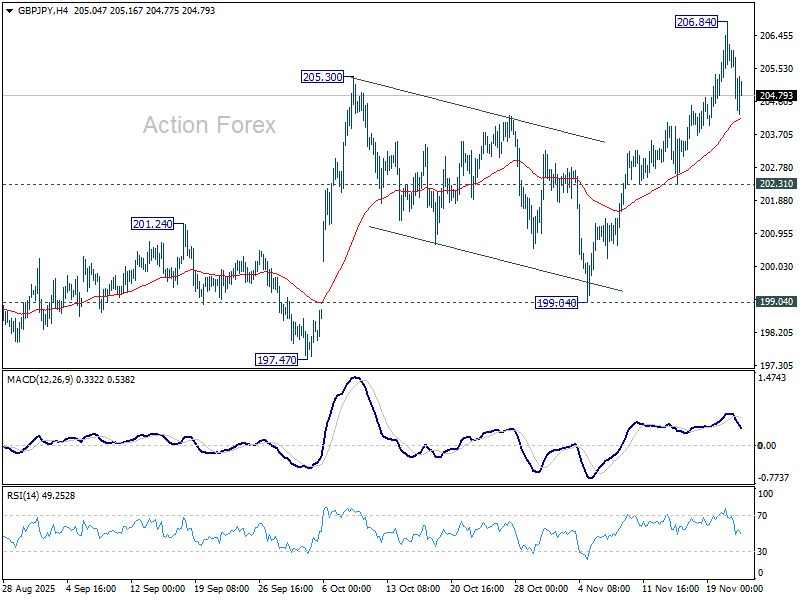

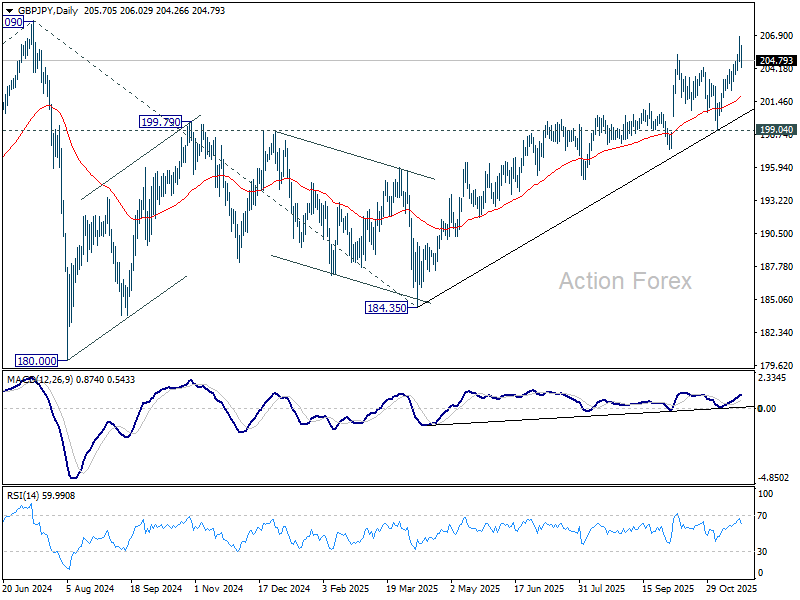

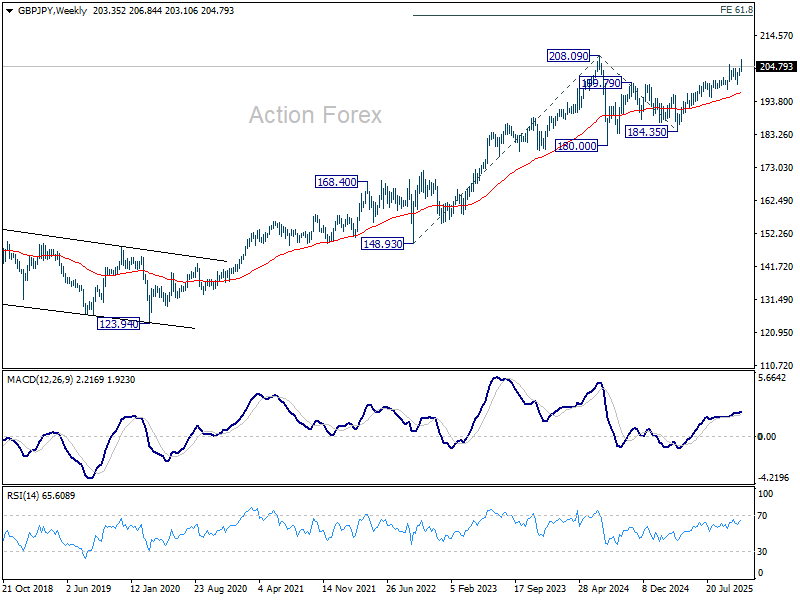

GBP/JPY Weekly Outlook

GBP/JPY's rally from 184.35 resumed last week but lost momentum after hitting 206.84. Initial bias remains neutral this week for some consolidations. Downside of retreat should be contained by 202.31 support to bring another rise. Break of 206..84 will target 208.09 high. Decisive break there will confirm long term up trend resumption.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.

In the long term picture, there is no sign that the long term up trend from 122.75 (2016 low) has concluded. But firm break of 208.09 is needed to confirm resumption. Otherwise, more medium term range trading could still be seen.

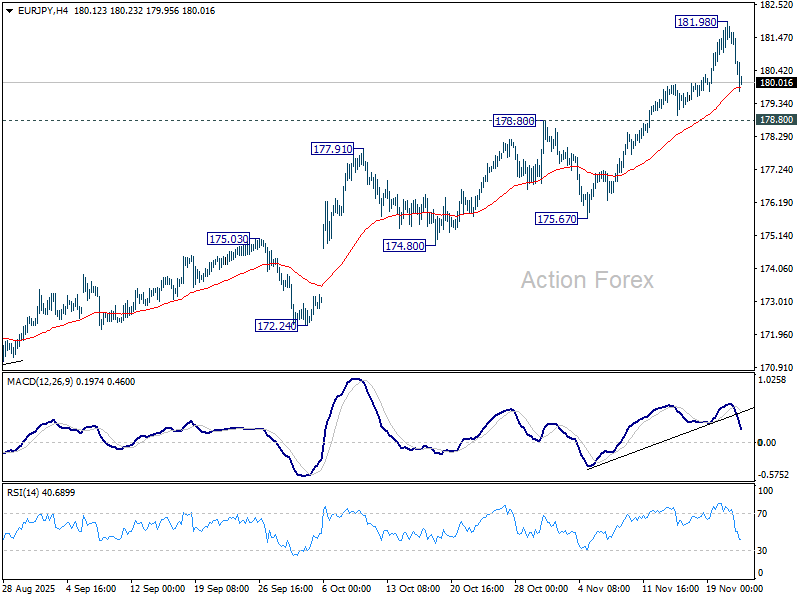

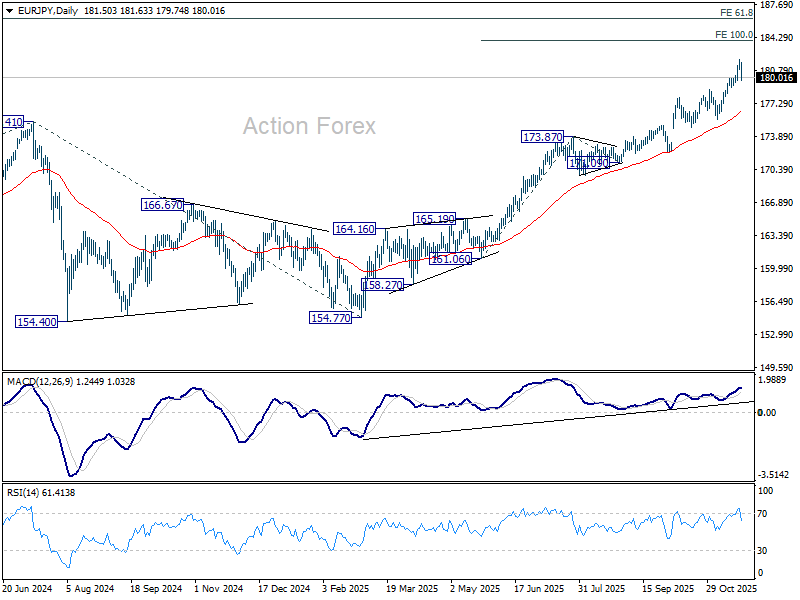

EUR/JPY Weekly Outlook

EUR/JPY jumped further to 181.98 last week but retreated from there. Initial bias remains neutral this week for consolidations. Downside should be contained by 178.80 resistance turned support to bring another rally. On the upside, break of 181.98 will target 100% projection of 161.06 to 173.87 from 171.09 at 183.90 next. However, firm break of 178.80 will argue that deeper correction is already underway towards 55 D EMA (now at 176.36).

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Outlook will continue to stay bullish as long as 55 W EMA (now at 169.00) holds, even in case of deep pullback.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

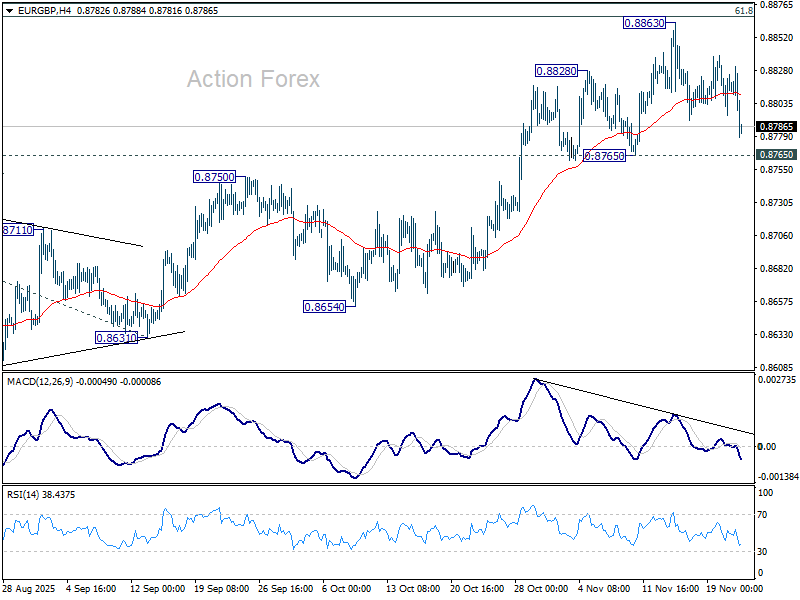

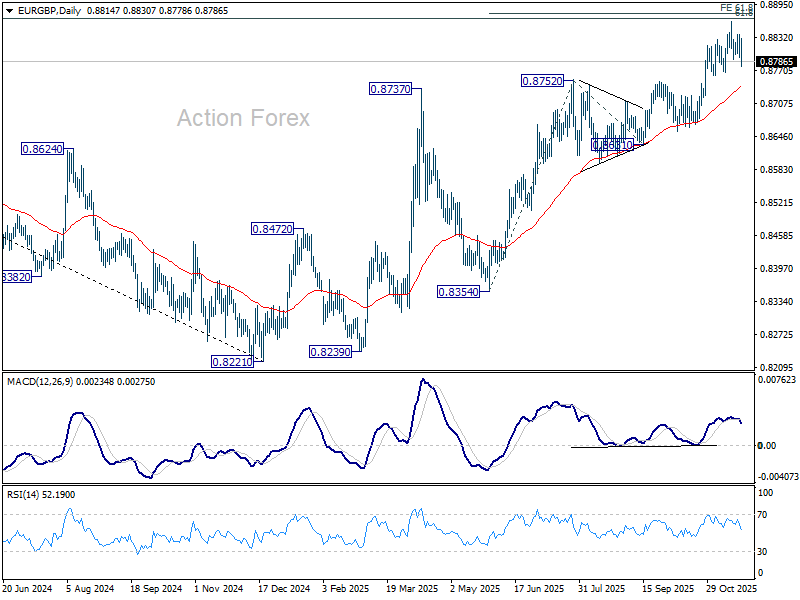

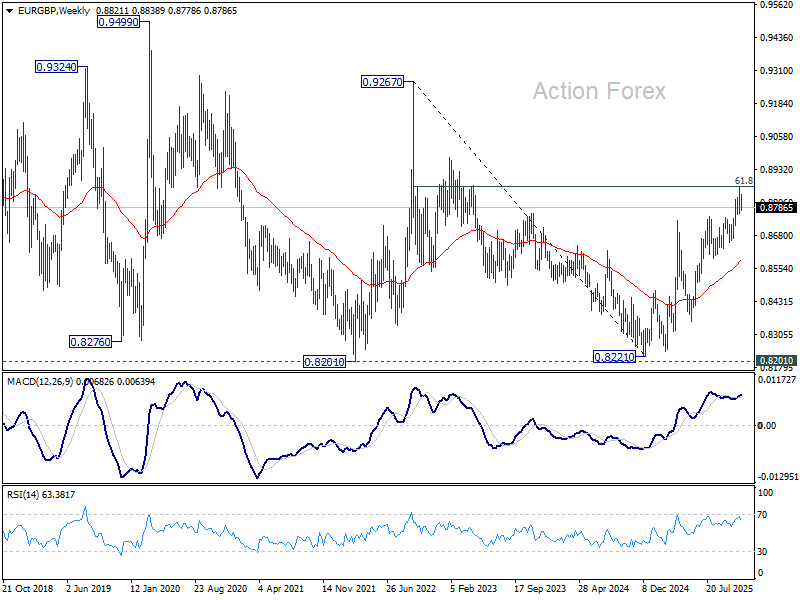

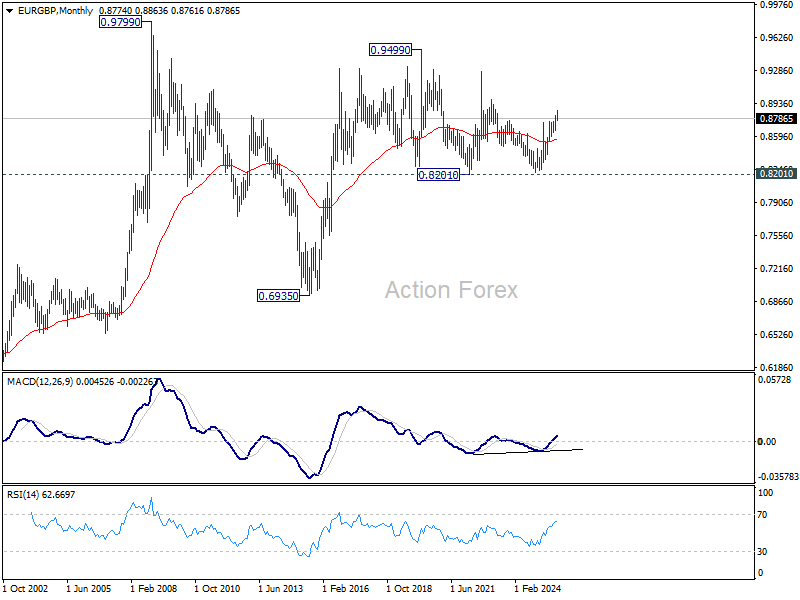

EUR/GBP Weekly Outlook

EUR/GBP's pullback from 0.8863 extended lower last week but downside is still contained above 0.8765 support. Initial bias remains neutral this week first. Considering bearish divergence condition in 4H MACD, firm break of 0.8765 will confirm short term topping. Intraday bias will be back to the downside for 55 D EMA (now at 0.8739). Sustained break there will be an early sign of bearish trend reversal. Nevertheless, decisive break of 0.8867 fibonacci level will carry larger bullish implications.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8589) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

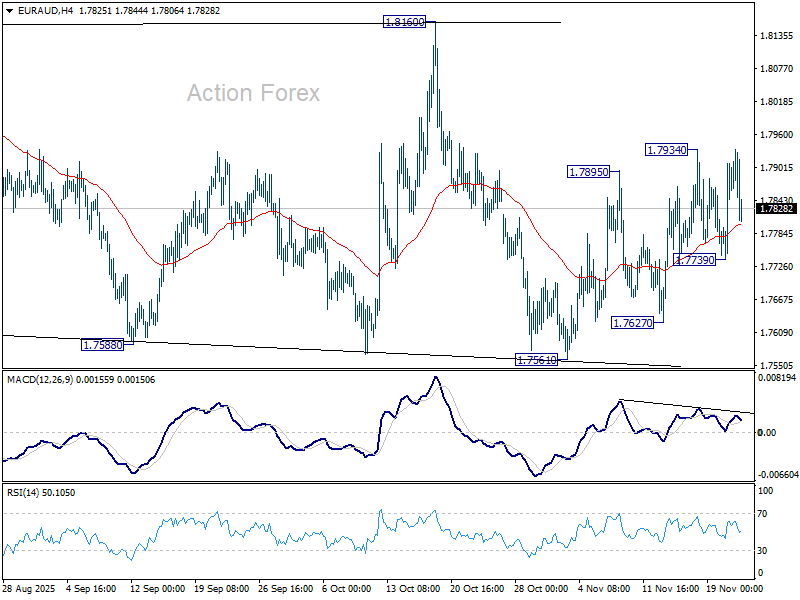

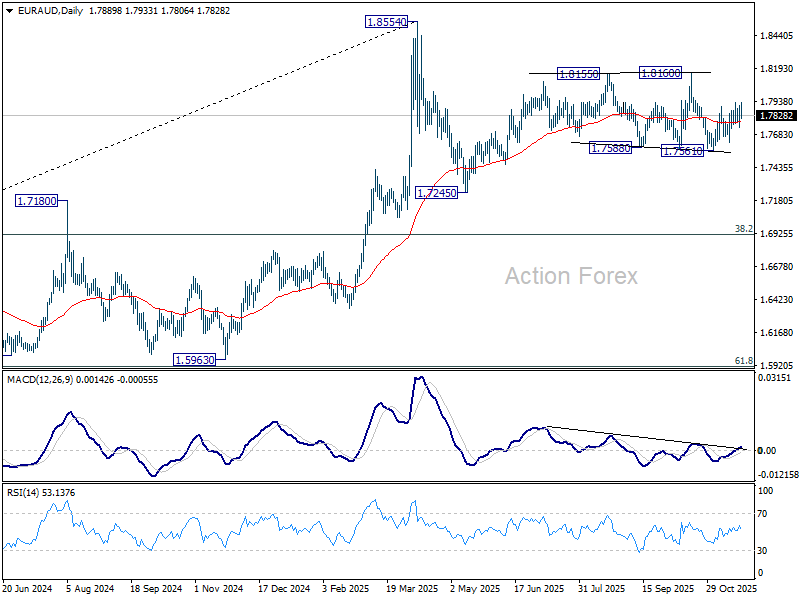

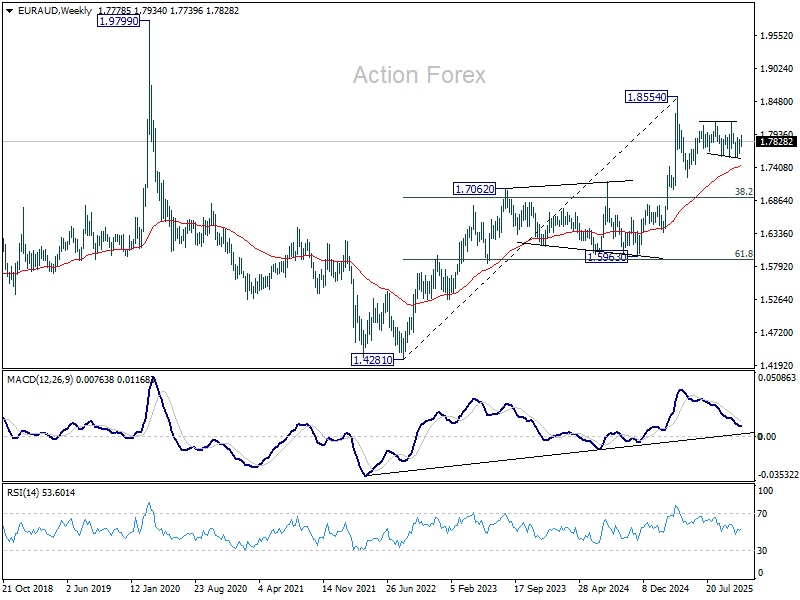

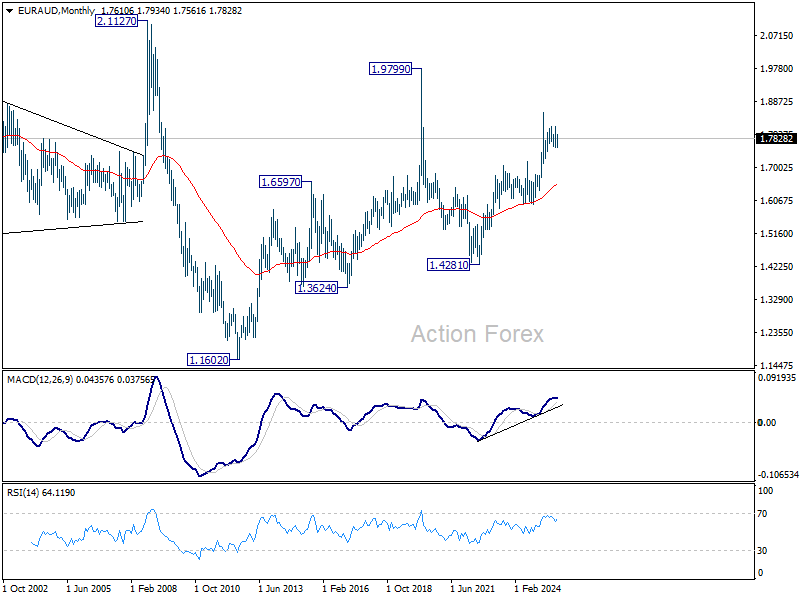

EUR/AUD Weekly Outlook

EUR/JPY gyrated higher last week but lost momentum again after hitting 1.7934. Initial bias remains neutral this week first. On the upside, above 1.7934 will resume the rebound from 1.7561 towards 0.8160 resistance. On the downside, however, break of 1.7739 support will argue that the rebound has completed and turn bias back to the downside for 1.756.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Sustained break of 55 W EMA (now at 1.7440) will suggest that it's correcting the whole rally from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922. Nevertheless, strong rebound from 55 W EMA will likely bring resumption of the up trend sooner.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6548) holds, this second leg could still extend higher.

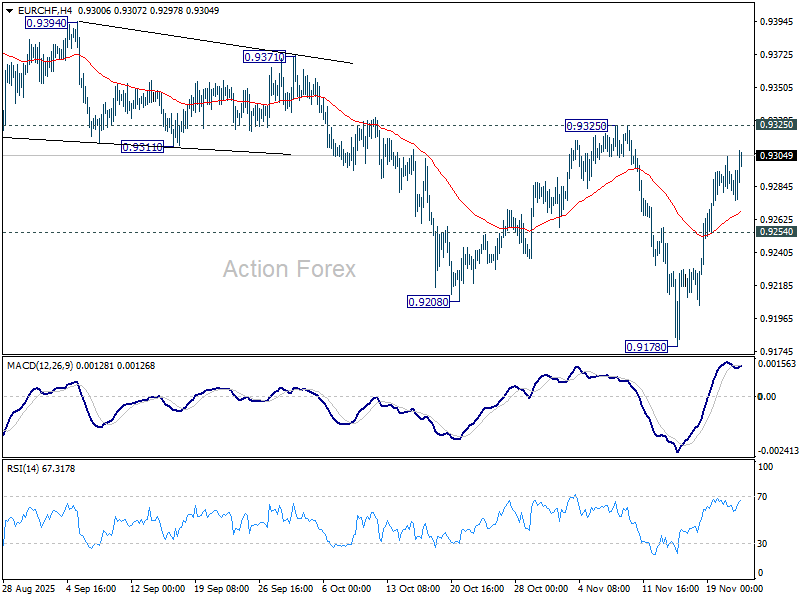

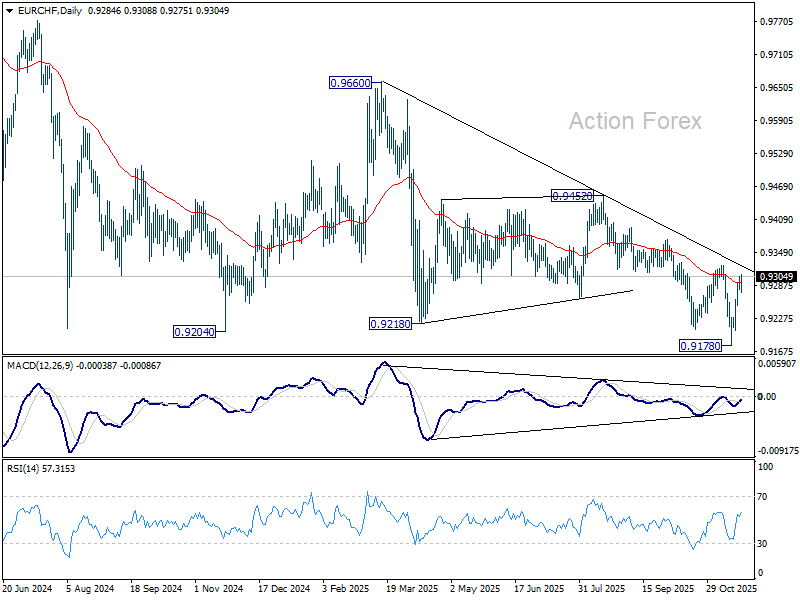

EUR/CHF Weekly Outlook

EUR/CHF's strong rebound last week indicates short term bottoming at 0.9178. Still, with 0.9325 resistance intact, outlook remains bearish and another fall is still in favor. On the downside, below 0.9254 minor support will bring retest 0.9178 support. However, considering bullish convergence condition in D MACD, decisive break of 0.9325 will argue that whole fall from 0.9660 has completed. Strong rally should then be seen towards 0.9452 resistance.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9377). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish in case of strong rebound.

In the long term picture, overall long term down trend is still in progress in EUR/CHF. Outlook will continue to stay bearish as long as falling 55 M EMA (now at 0.9800) holds.

Markets Weekly Outlook – UK Budget in Focus as Global Equities Eye Recovery

Week in review

The week draws to a close on a positive note after a significant selloff in risk assets as US rate cut bets continued to decline from the Federal Reserve's December meeting.

US jobs data for September was finally released but came with a caveat, the October and November data will not be released until after the Fed's December meeting. This is one of the main contributing factors to the decline in rate cut probabilities which dropped to a low of around 25%.

However, Friday saw a significant change once more with markets once again favoring a rate cut at the December meeting and this may continue to change as the Fed meeting in December draws closer.

Source: CME FedWatch Tool

Risk assets faced a difficult week with the three major US indices trading 5.5-8.5% below their recent peaks at one point. The concern for markets came as a surprise given the positive earnings report by chip giant NVIDIA as valuation concerns linger.

Investors are beginning to doubt the rising stock prices of leading AI companies. They are worried that these companies are announcing big plans that they don't actually have the money or the factory capacity to handle right now. If these worries continue, it will be very hard for the stock market to go up significantly. Interesting times ahead indeed especially after the positive end to the week.

All major US stock indexes rose on Friday as investors became more confident that the Federal Reserve will cut interest rates next month. This optimism grew after John Williams, a key central bank official, stated that rates could be lowered soon without causing inflation to rise again. Despite this positive end to the week, the main market indexes are still expected to finish with a total loss of about 2% for the week.

Technology stocks also stabilized after suffering a sharp drop the previous day. Most large companies saw their values go up, led by Google’s parent company, Alphabet, which rose by 3%. Meanwhile, shares of AI chipmaker Nvidia remained flat; this follows a very unstable day on Thursday where the stock price swung wildly after the company released its quarterly financial results.

How has the US Dollar and FX Performed?

The US dollar weakened against the Japanese yen on Friday after Japanese officials warned they might take action to stop the yen from losing too much value. The Finance Minister stated that the government is ready to step in if currency prices swing too wildly, which alerted traders that Japan might start buying yen soon to support it.

Despite this specific drop against the yen, the dollar had a very strong week overall. It reached its highest level since May against other major currencies and is on track for its best weekly performance in six weeks.

Meanwhile, other major currencies and assets struggled. The Euro dropped slightly and is set to lose roughly 1% for the week. The British Pound also fell, trading around $1.31, as investors wait for the UK government's new budget plan while facing signs of a weak economy.

In the cryptocurrency market, Bitcoin had a difficult day, falling nearly 5% to around $82,900, its lowest price in seven months.

In the week ahead,keep an eye on the Japanese Yen as the case for FX intervention continues to grow.

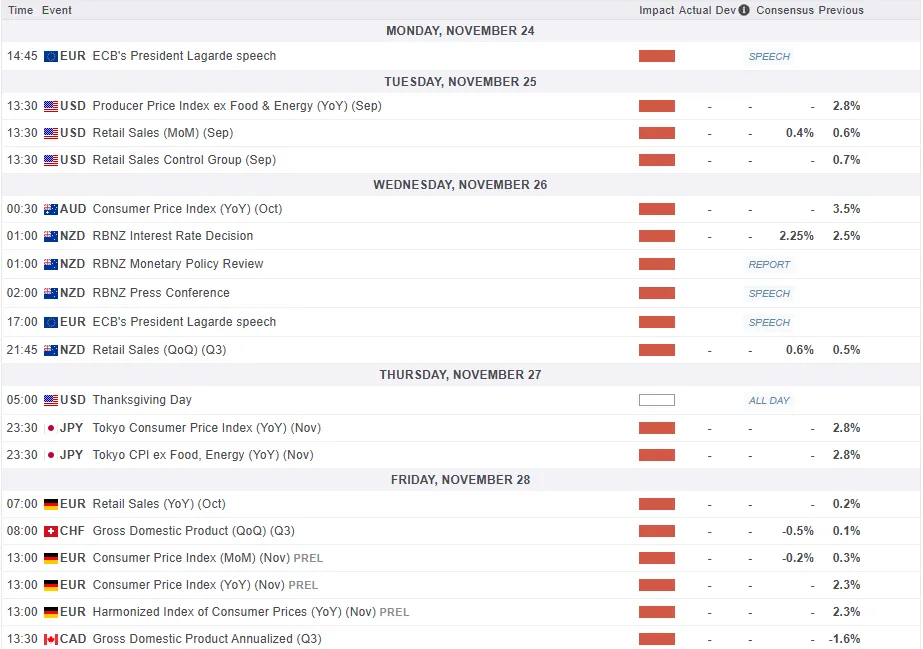

The Week Ahead

The week ahead will not be as busy for the US given that it is Thanksgiving, which means data will be packed in the first three days of the week.

There are still some high impact data releases from Asia and of course the highly anticipated UK budget, where Chancellor Rachel Reeves faces an unenviable task.

Asia Pacific Markets

China is set to release its industrial profit figures on Thursday, which will complete the economic data for the month. Profits have been improving recently, showing a 3.2% increase for the year so far, driven largely by very strong growth of over 20% in both August and September. Part of this jump is because last year's numbers were low, and while that statistical advantage will fade in the fourth quarter, profits for October are still expected to look healthy.

The strongest industries this year have been those that sell goods abroad, specifically trains, ships, aerospace equipment, and electronics and this positive trend is likely to continue.

In Japan, inflation in Tokyo is expected to rise to 2.7% in November, fueled by higher worker wages and a weaker Yen, which pushes prices up. Factory output remains steady following a trade agreement with the US.

Although the economy shrank in the third quarter, recent signs of recovery support the Bank of Japan's plan to return to standard economic policies. While fewer investors now expect interest rates to rise in December, based on innuendo and comments, it appears at least three central bank members support the move. I still lean toward a rate hike next month, though there is a growing chance it could be delayed until January.

Thanksgiving Week in the US as the UK Budget Comes Into Focus

Because of Thanksgiving, economic reports are coming out early this week, but they may be unreliable due to the government shutdown. Key jobs and inflation data have been delayed until after the Federal Reserve's December meeting.

Since officials were already planning to keep interest rates steady, the lack of new data means they likely won't cut rates unless the economy faces a sudden crisis. However, we still predict interest rates will eventually drop by 0.75% by the middle of 2026.

The main event to watch in the week ahead is the "Beige Book," a general survey of the economy.

On Wednesday, the UK Chancellor faces a £30 billion gap in the budget. Markets are watching to see if she raises taxes to fix this, as her decision will affect future interest rates and government borrowing. Regardless of what happens, the country's deficit is expected to shrink next year.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week - US Dollar Index

This week's Chart of the week is the US Dollar Index (DXY)

From a technical perspective, the DXY has broken above the 100.00 psychological level.

This is the third time since the end of July that this has happened and each time thus far a selloff has taken place. Will we see similar price action again or will the DXY finally gain acceptance above this key psychological level?

This will be the major test in the days ahead.

US Dollar Index (DXY) Daily Chart - November 21, 2025

Source:TradingView.Com (click to enlarge)

The Weekly Bottom Line: Data – In, December’s Rate Cut – Out?

Canadian Highlights

- Canada’s economy is showing signs of slowing momentum, but inflation persists.

- Upcoming GDP figures have an additional layer of uncertainty due to delayed trade data.

- Tepid growth and slowly softening underlying inflation are in line with the Bank of Canada’s projections, suggesting no upcoming changes to the policy rate.

U.S. Highlights

- Equity markets sold off this week as investors continued to worry about the valuations of AI companies.

- Although the data fog has started to clear, it did little to resolve differences among FOMC members, with a rate cut in December now looking less likely.

- The delayed September payrolls report was better than expected, rising by 119,000 jobs. However, the unemployment rate increased to a new cyclical high of 4.4%.

Canada – Waning Momentum and Stubborn Inflation

An absolute data dump of a week, with updates on housing, inflation and retail sales. The overall story was one of waning economic momentum, and some disappointingly stubborn underlying inflation. That is basically in line with the Bank of Canada’s (BoC) and our expectations – tepid growth and gradually weakening price pressures. With trade policy still prone to large changes, things could swing rapidly, but the new information this week suggests the BoC will remain on the sidelines for the time being.

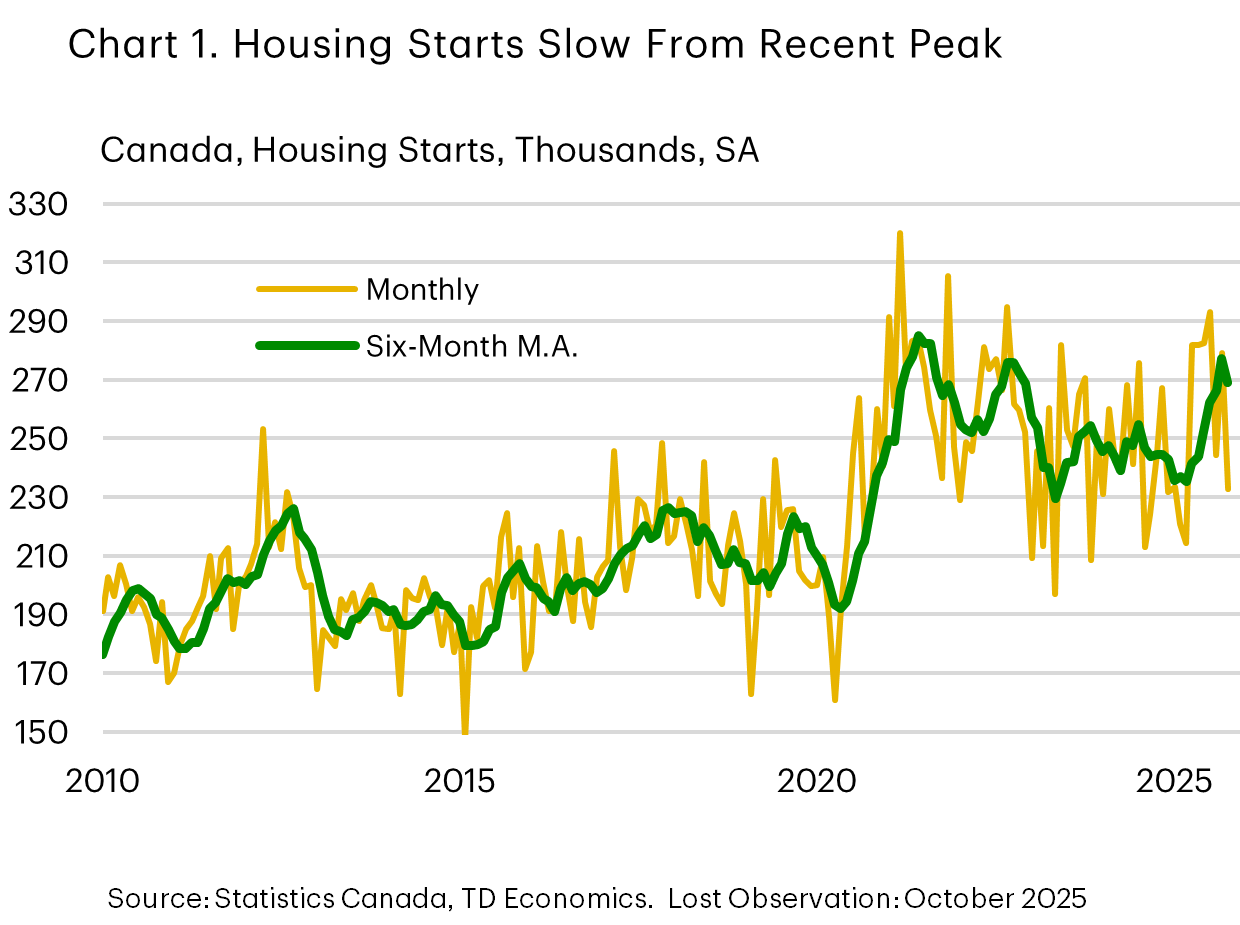

The Canadian housing market continues to trudge along, with monthly starts dipping 3% on a six-month moving average basis. The figure isn’t all that surprising given that new housing construction has been running at a healthy clip well ahead of anything registered before the pandemic (Chart 1). This has been supported by healthy activity in the multifamily space, with purpose-built rental construction offsetting the drag from the owner-occupied segment. Nonetheless, with building permits trending downward the sector’s contribution to growth is likely to fade.

Fading momentum was the story in September’s retail sales figures as well, with sales tumbling 0.8% in real terms on the month, essentially reversing August’s gains. This leaves real retail sales up only 1.2% versus a year ago. October’s flash estimate is for no growth – although with goods CPI falling last month there is hope for some small gains in volume terms. Nonetheless, real retail spending contracting in the third quarter and trending below 2% for the year are not the hallmarks of robust consumer activity.

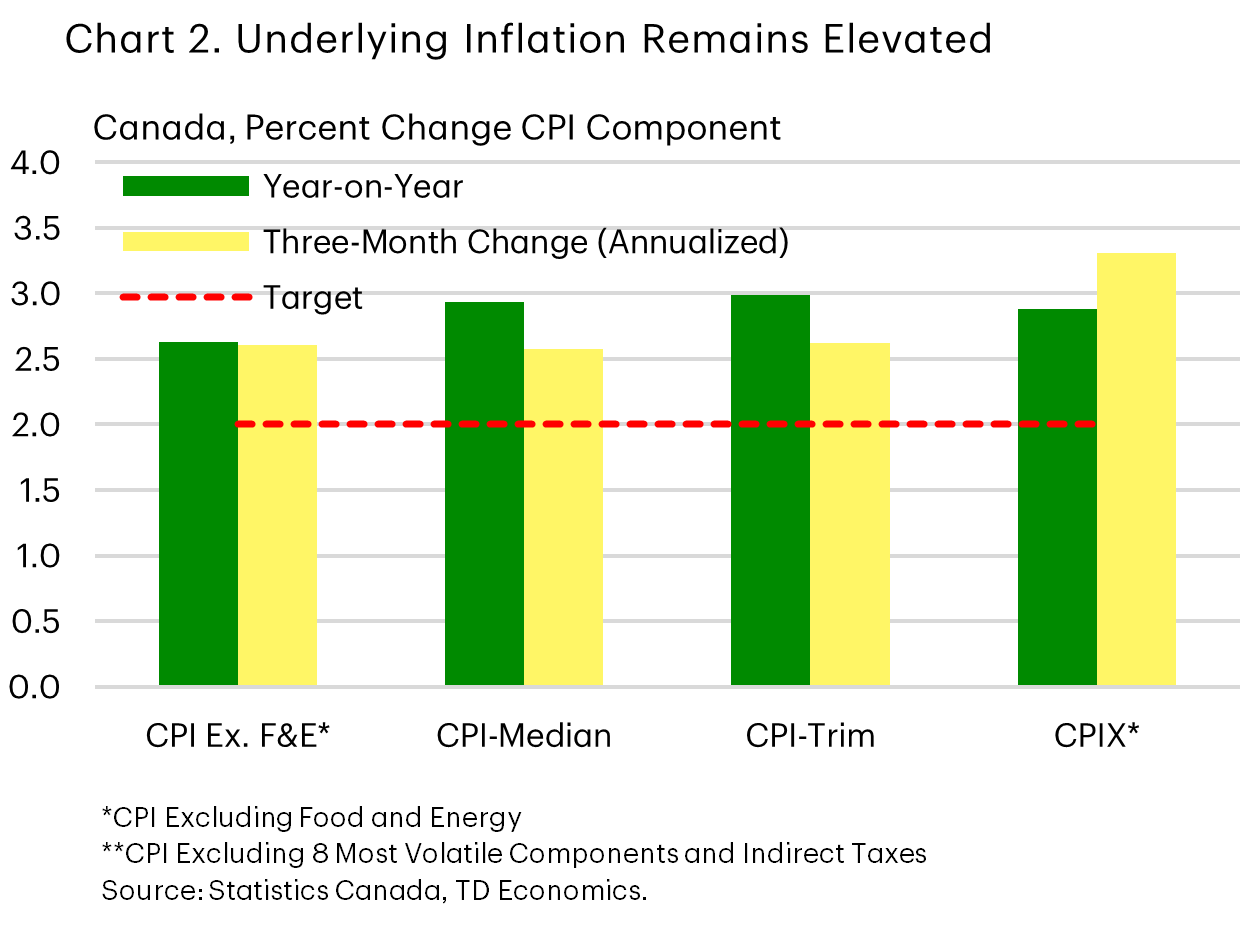

Domestic activity data suggest that some of the healthy momentum in late-2024 and the second quarter of this year has begun to fade amid an elevated unemployment rate. This is consistent with our view that inflation should remain contained in the coming months as domestic excess supply helps to offset inflationary pressure from global trade disruptions. And there are inflationary pressures to be offset. Measures of core inflation remain close to 3% on an annual basis, and near-term trends have also flipped higher, with three-month rates of change above 2.5% for the four most-prominent indicators (Chart 2).

This sets the stage for next week’s third quarter GDP report. Our expectation is that growth will register somewhere between 0.5% and 1.0% on a quarterly (annualized) basis. This forecast, however, has an additional layer of uncertainty embedded in it as the U.S. government shut down delayed the release of Canadian trade data. Given the swings in trade in the second quarter, this forms a vital input into the projection – so its absence is adding uncertainty. We await clarity on when the information will be released and whether Statistics Canada’s estimates of third quarter GDP will incorporate the information or rely on their own estimates of the figure.

All told, signs point to slow growth for Canada in Q3, with some stubbornness in inflation. All in line with what the BoC outlines in their most recent projection and suggesting that change in policy is not in the offing.

U.S. – Data – In, December’s Rate Cut – Out?

Equity markets sold off this week amid concerns about high tech-stock valuations and aggressive AI capital spending. As of writing, the tech-focused Nasdaq Composite was down 2.5% on the week, while the S&P 500 had declined 1.9%.

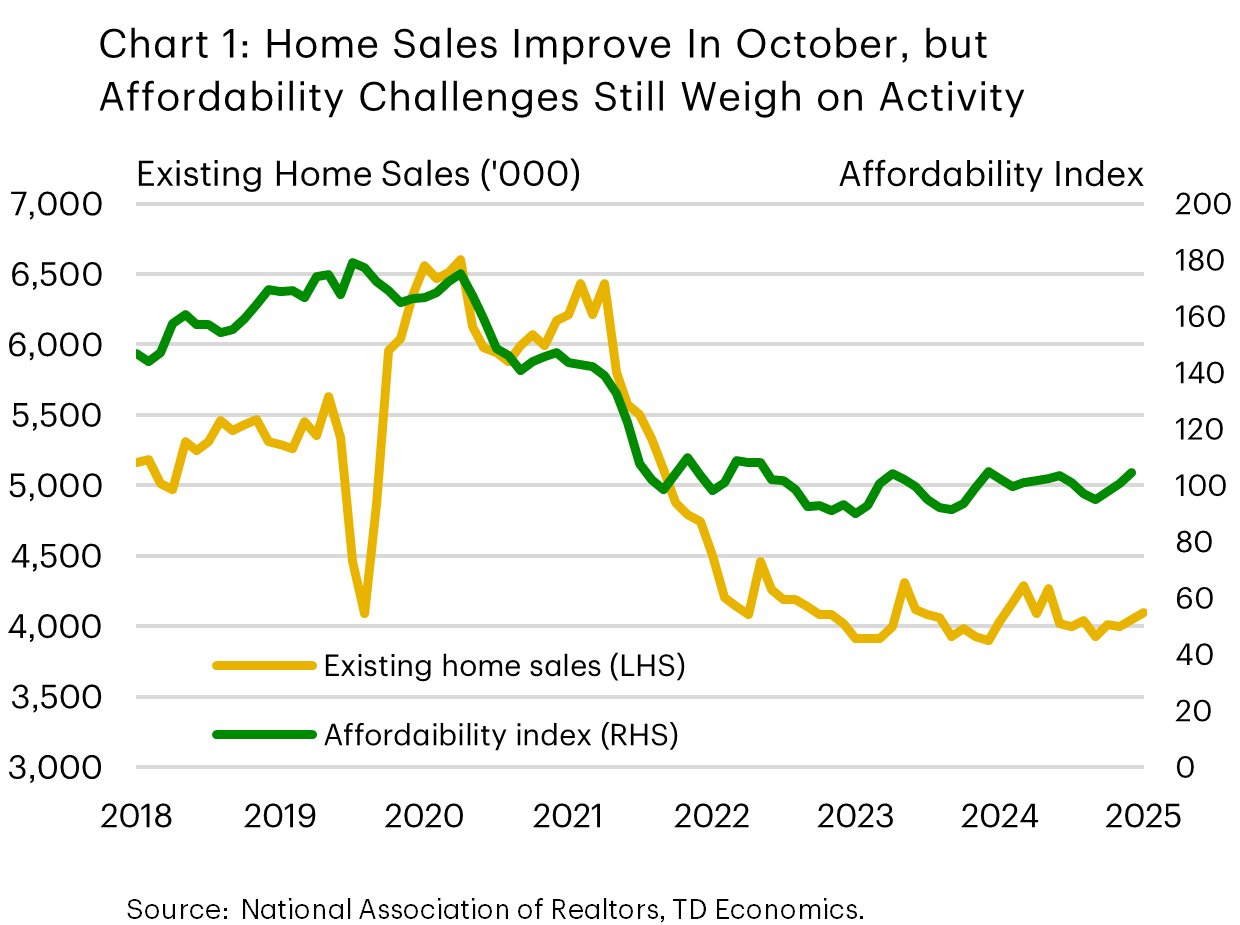

Official economic data began to trickle in, with September’s payroll report being the most notable. However, reporting backlogs are expected to persist. October payrolls will be released with November’s figures on December 16, not in time for the FOMC’s next meeting on December 9–10. Other data points, like October CPI, will not be released. On the housing side, existing home sales edged higher in October, supported by falling mortgage rates. Still, the housing market continues to tread water as affordability remains stretched, despite some modest improvement in recent months (Chart 1).

A busy slate of Fed speakers reaffirmed the lack of consensus among FOMC members for another rate cut in December. Some, like Governor Jefferson (voter), advocated for a cautious, “meeting-by-meeting approach,” as the policy rate moves closer to neutral. Chicago Fed President Goolsbee (voter) joined the hawkish camp, downplaying the recent labour-market weakness and emphasizing the lack of progress on inflation.

Minutes from the October FOMC meeting also highlighted the growing divide, with many participants seeing no case for easing in December. This contributed to market pricing shifting towards the next cut coming in January rather than December. After that meeting, Chair Powell stated that a December cut “is not a foregone conclusion, far from it.”

But policy doves like Governor Waller (voter), argued that another rate cut in December is warranted, given his assessment that the labor market remains weak, longer-term inflation expectations are anchored, and the impact of tariffs on inflation are likely to be transitory. Echoing this view, FOMC Vice Chair Williams emphasized that inflation expectations remain “very well anchored” and noted room for further cuts over the ‘near-term’. These remarks helped to tip market odds back in favour of a December cut on Friday morning.

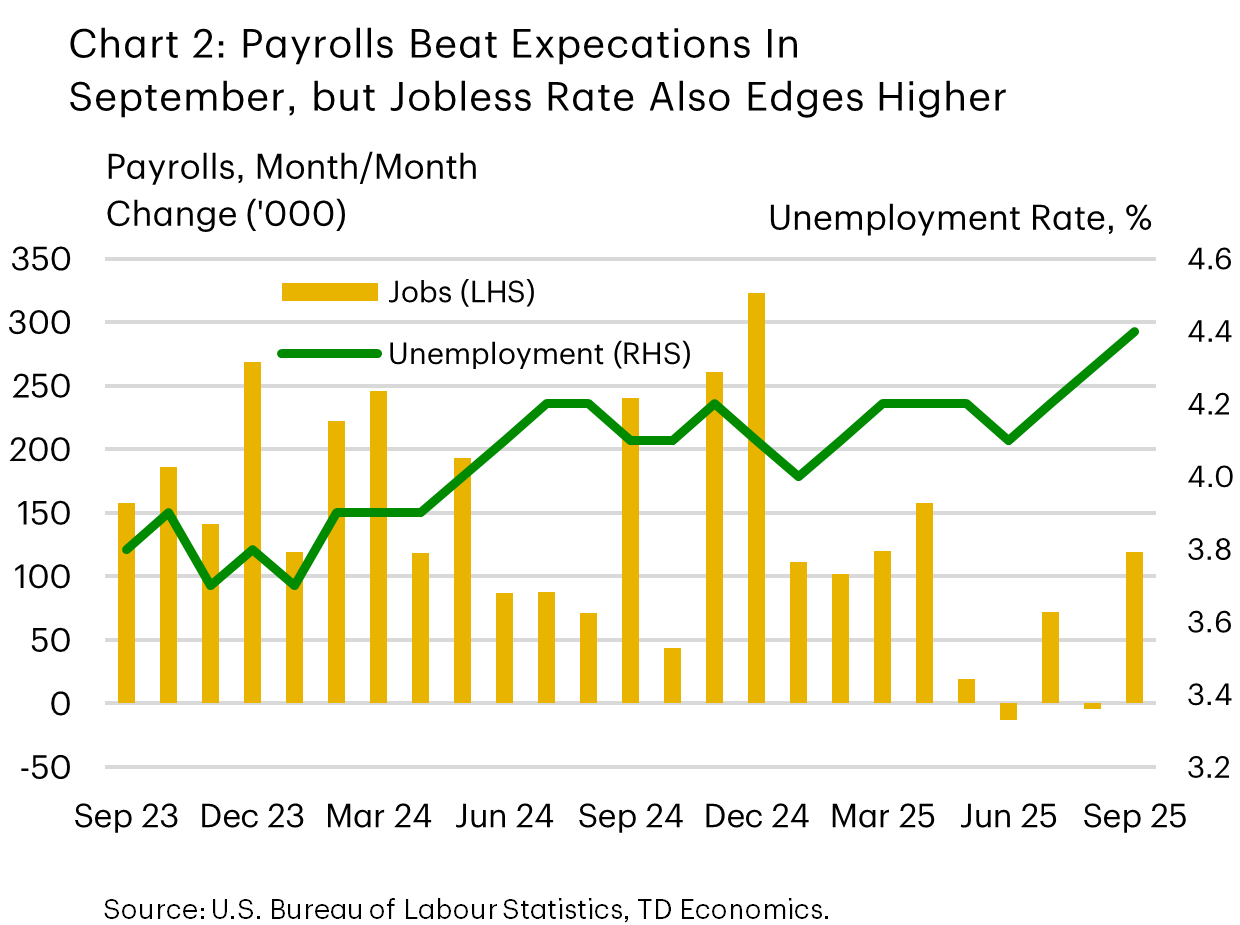

The delayed September payrolls report did little to reconcile the divide among policymakers. Hawks were likely reassured by the better-than-expected job gains: payrolls rose by 119k—the strongest reading since April (Chart 2). However, policy doves are likely to point to the negative revisions to prior months, the narrow concentration of job gains, and the uptick in the unemployment rate.

All in all, hawkish voters appear to outnumber the doves on the FOMC for now, and there is no official jobs or inflation data before the next meeting to shift views. Therefore, we expect the slow-and-steady approach to carry the day and for the Fed to hold rates steady in December. Chair Powell perhaps said it best: “when you’re driving in the fog, you slowdown”. That said, the door for a cut in January remains open.

Weekly Economic & Financial Commentary: Tariffs on the Table

Summary

United States: Should They Stay or Should They Go?

- Delayed data started to trickle in this week, adding to the debate over the Fed's course of action at its December meeting. The September jobs report painted the picture of a cooling but not rapidly deteriorating jobs market. We believe the data are supportive of a December cut, but it's not a done deal.

- Next week: Consumer Confidence (Tue.), Retail Sales (Tue.), Durable Goods (Wed.)

International: Sluggish Yet Resilient

- Japan’s economy contracted in Q3 while prices accelerated in October. In contrast, inflation eased in the UK and Canada, reinforcing expectations for policy adjustments. Eurozone PMIs signaled mixed momentum—sluggish but positive growth—while UK PMIs disappointed, highlighting stalled activity.

- Next week: RBNZ Policy Rate (Wed.), Canada GDP (Fri.), India GDP (Fri.)

Topic of the Week: Tariffs on the Table

- As consumers gear up for the holiday season, they are contending with stubborn inflation. The trend decline in inflation stalled this year, with the Consumer Price Index (CPI) increasing 3.0% year-over-year in September—its highest reading since January. Though services prices have been gradually slowing, goods prices have experienced a pickup, and food categories have not been immune.