Sample Category Title

Eurozone PMI signals 0.4% Q3 GDP growth, backs ECB hold

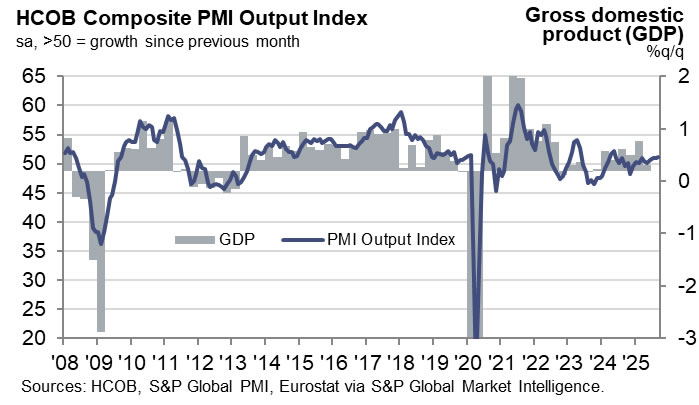

Eurozone services activity strengthened in September, with PMI Services finalized at 51.3, up from 50.5 in August and marking an eight-month high. Composite PMI also edged higher to 51.2, the best in 16 months.

Country breakdowns in Composite highlighted broad-based improvement. Spain led with a 53.8 reading, while Germany and Ireland both came in at 52.0, representing multi-month highs. Italy held at 51.7, while France lagged with a decline to 48.1, its weakest in five months.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that business activity “picked up more strongly” in September, and that the rebound was “broad-based geographically.” The uptick in new business suggests expansion could continue into October, though backlogs have yet to recover.

Crucially, price pressures eased but remained slightly above average. De la Rubia said the data support policymakers who resist further cuts, as inflation in services is still sticky. With the composite PMI holding in expansionary territory throughout Q3, HCOB’s nowcast points to quarterly GDP growth of around 0.4%.

GBP/USD Snaps Four-Day Winning Streak, Hovers Around 1.34500 – Potential Targets and Price Forecast

Having rallied substantially from lows made last week, the GBP/USD broke a four-day winning streak in yesterday's trading, falling by 0.28%.

Today, and at the London open, GBP/USD currently trades at ~1.34521, up 0.10%.

GBP/USD: Key takeaways 03/10/2025

- The most significant catalyst of GBP/USD movement currently, the US government shutdown is weighing heavily on the dollar, as markets readjust confidence in American governance

- Otherwise, and following Wednesday’s worse-than-expected UK manufacturing PMIs, signifying five-month lows, the Bank of England is under increasing pressure to consider further rate cuts, although inflation remains somewhat sticky

- Recent GBP/USD upside is almost exclusively due to dollar weakness, as opposed to pound strength

Dollar Strength Index (DXY) vs. British Strength Index (BXY). TVC, TradingView, 02/10/2025

GBP/USD: US government shutdown adds to cable upside

In a return to a word oh-so-familiar in this year’s trading, the latest wave of market uncertainty has come by way of the US government shutdown, announced on Tuesday evening, as the US Senate failed to reach an agreement on government funding.

@realDonaldTrump, Truth Social, 02/10/2025

With the majority of US Democrats voting against a funding bill proposed by the Republican Party, the shutdown is the first in almost seven years, the last having occurred during Trump’s first presidency in 2018.

While at first glance, the notion of a governmental shutdown seems purely political, some knock-on effects are already being felt within currency markets, with the release of many key economic indicators expected to be delayed, since reporting agencies are considered ‘non-essential’ during times of government shutdown.

This is especially relevant considering that, under normal market conditions, nonfarm payrolls were scheduled to be released this week.

Considering the importance of these figures, especially their implications for upcoming monetary policy, the market understandably remains somewhat uneasy, which has introduced some short-term dollar weakness.

Should a resolution to the shutdown be found, either by a temporary bill or a Democrat concession in accepting the most recent Republican suggestion, we can expect dollar weakness to reverse course, at least in the short term.

GBP/USD: UK manufacturing PMIs fall short of market expectations

To touch quickly on recent data, Wednesday’s report revealed that manufacturing conditions in the UK not only continue to worsen but have fallen to five-month lows, at 46.2.

At least in part, these conditions are adding pressure to the Bank of England to consider further rate cuts, although this will prove difficult if inflation remains sticky.

As such, and considering not only a non-flattering reflection of the UK economy, but also implications for Bank of England monetary policy, we can expect some short-term pound downside as seen in yesterday’s session.

GBP/USD: Technical Analysis 03/10/2025

GBP/USD: Daily (D1) chart analysis

GBP/USD, D1, OANDA, TradingView, 03/10/2025

While cable performance in the first half of 2025 was remarkable, mainly owing to a downbeat dollar, since June, the tune has somewhat changed.

Of late, we’ve entered into a period of consolidation, best visible on the daily timeframe, with price moving sideways and yet to challenge the highs of 1.37710 made earlier this year.

Currently, price trades close to the trendline, with some short-term downside on the table unless the trendline can be broken.

Should this happen, here are some key levels to be watching:

- Price target 1 (T1): 78.6% Fib: $1.33887

- Price target 2 (T2): 61.8% Fib: $1.33498

- Price target 3 (T3): 50% Fib: $1.3322

- Resistance 1 (R1): $1.35745

- Resistance 2 (R2): $1.36550

It should be considered, however, that while some downside is possible in the immediate, price remains in a sideways channel, with longer-term direction unclear.

Until the fundamental analysis picture becomes clearer, traders are advised to approach with at least some caution.

Bitcoin Enters a Favourable Period

Statistically, September has a poor reputation for the cryptocurrency market, whereas October and November are the most favourable months, during which Bitcoin’s price has traditionally risen, as history shows. October has even earned the nickname “Uptober” within the crypto community.

The drop in BTC/USD at the end of September 2025 and the steady growth this week underline this established “tradition.”

Why is Bitcoin rising?

Fundamentally, demand for Bitcoin is strengthening:

→ due to growing uncertainty linked to the US government shutdown and increased appeal of safe-haven assets, as evidenced by capital inflows into Bitcoin‑related ETFs;

→ thanks to expectations of a Federal Reserve interest rate cut amid signs of a slowdown in the labour market.

At the same time:

→ JP Morgan analysts forecast that Bitcoin could rise to $165,000 by year‑end;

→ Cardano founder Charles Hoskinson suggested that by mid‑2026 BTC could reach $250,000, pointing to geopolitical shocks as a potential catalyst for growth.

Technical Analysis of the BTC/USD Chart

Analysing the drop in Bitcoin’s price on 22 September, we updated the long‑term ascending channel and suggested that:

→ bulls are retreating towards its lower boundary (on today’s Bitcoin chart, the channel is constructed using the regression method);

→ BTC/USD may consolidate within a broad zone forming an S–R triangle.

Indeed, between 25 and 28 September the lower boundary acted as support. Furthermore, note the price behaviour below the $110,000 level — there appeared to be few willing to sell the coin below this psychological threshold, creating initial momentum for a rally (highlighted by the black arrow). However, fluctuations within the S–R zone were not sustained.

Along the way, BTC/USD broke through:

→ the upper boundary of the red descending channel around $115,000 (which could act as support in the future). This marks a breakout of a corrective “bull flag” pattern and an attempt to resume the long‑term upward trend;

→ the psychological $120,000 level, reaching today a one‑and‑a‑half‑month high.

From a bearish perspective, selling pressure intensified around the $122,000 level, pushing the price down twice this summer (as shown by the red arrows). It is possible we could see a similar reversal for a third time. However, if October and November confirm their bullish reputation for the cryptocurrency market in 2025, this could drive Bitcoin’s price to the upper boundary of the channel, validating analysts’ positive forecasts.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

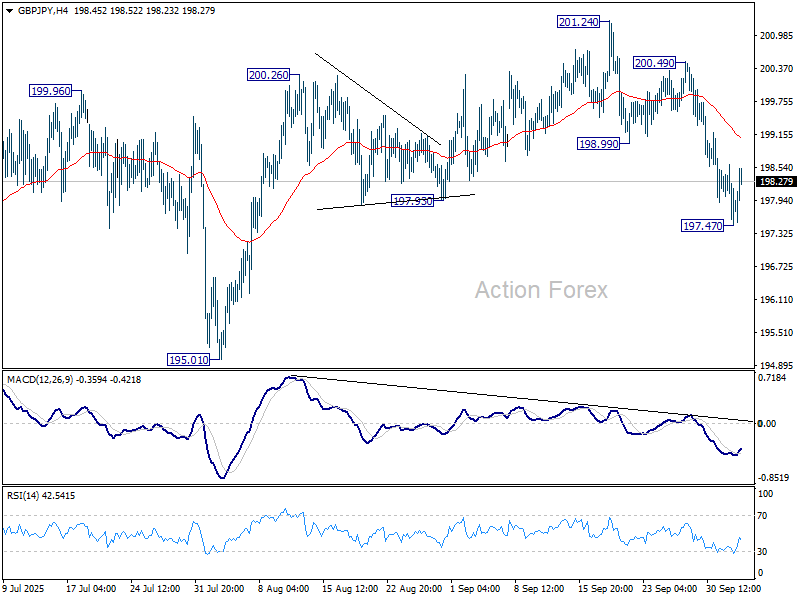

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.39; (P) 198.01; (R1) 198.52; More...

Intraday bias in GBP/JPY is turned neutral first with current recovery. Some consolidations would be seen above 197.47 but further decline is expected as long as 200.49 resistance holds. Below 197.47 will resume the fall from 201.24 to 195.01 support next. Firm break there will confirm near term bearish reversal.

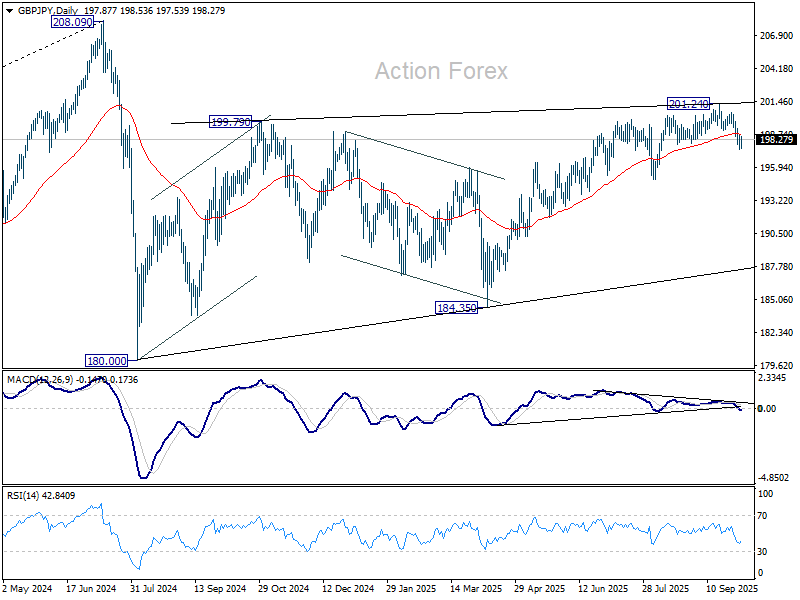

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

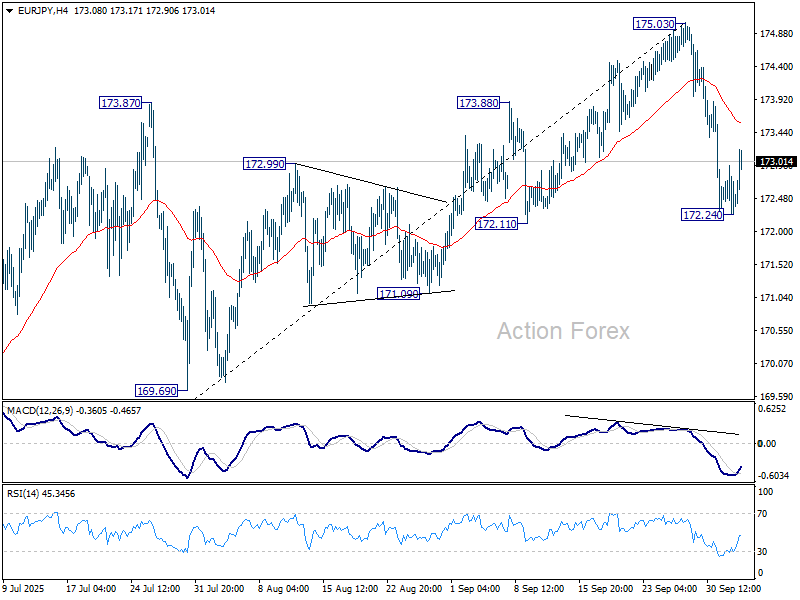

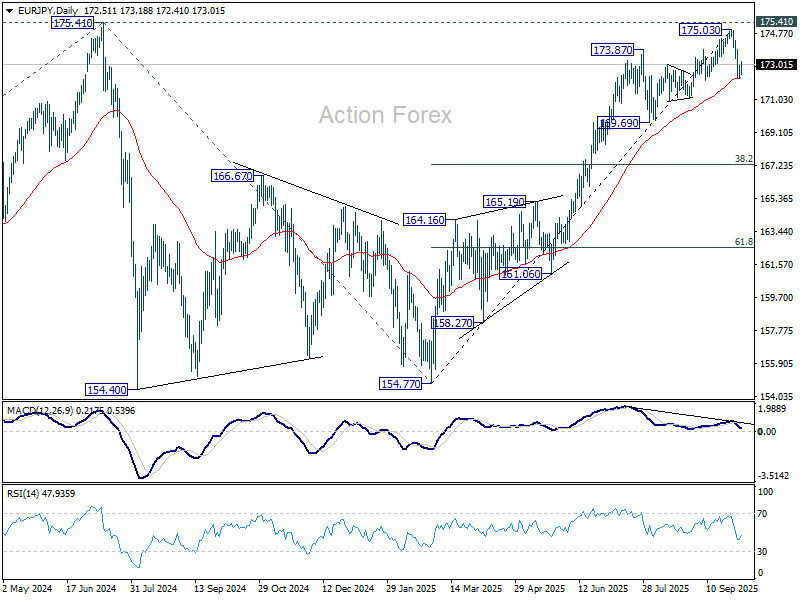

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.92; (P) 172.92; (R1) 173.53; More...

EUR/JPY recovered after drawing support fro 55 D EMA (now at 172.25) and intraday bias is turned neutral first. Risk will stay on the downside as long as 175.03 resistance holds. On the downside, sustained trading below 55 D EMA will argue that whole five-wave rally from 154.77 has completed. Further fall should then be seen to 169.69 support next.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 (2022 low) to 175.41 from 154.77 (2025 low) at 186.31. However, sustained break of 55 D EMA will delay this bullish case, bring deeper pullback to 169.69 support first.

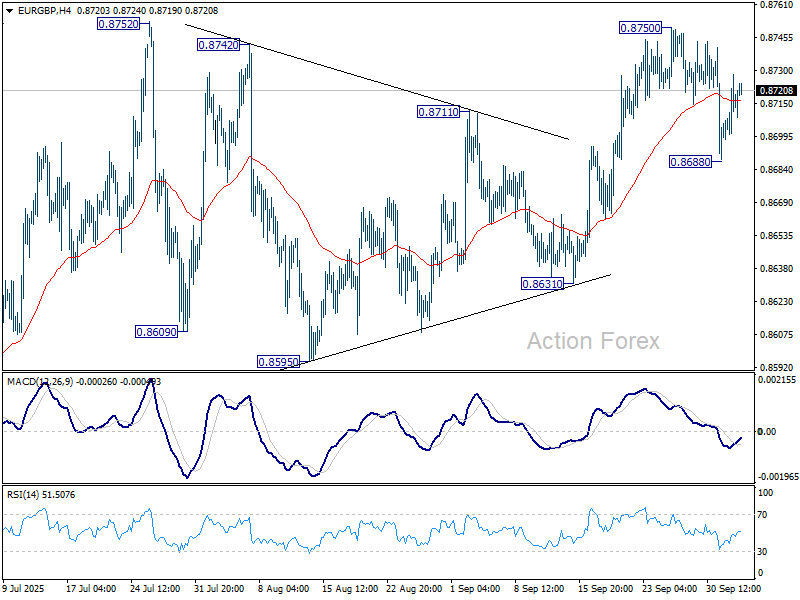

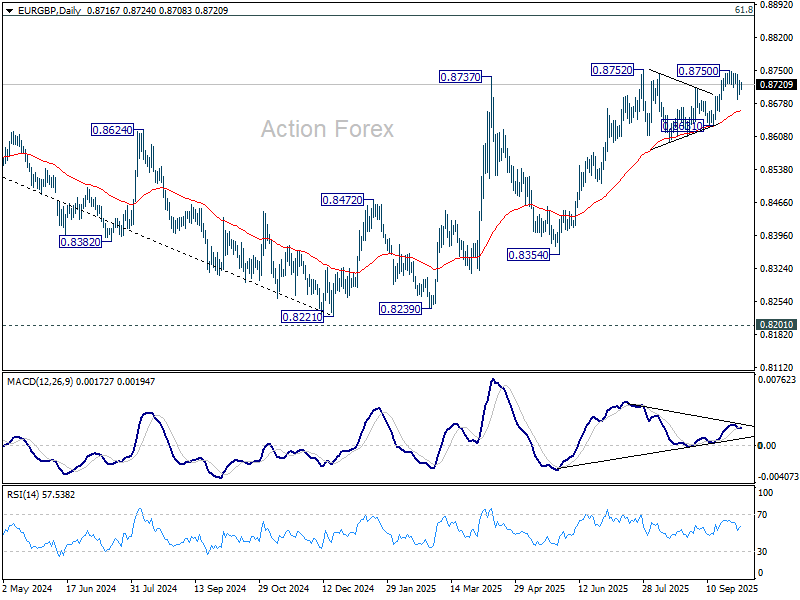

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8699; (P) 0.8715; (R1) 0.8734; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the upside, firm break of 0.8750 will resume larger rise to 0.8867 fibonacci level. However, decisive break of 0.8688 will turn bias back to the downside for 0.8631 support. Firm break there will indicate near term bearish reversal.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8533) will argue that the pattern has completed and bring retest of 0.8221 low.

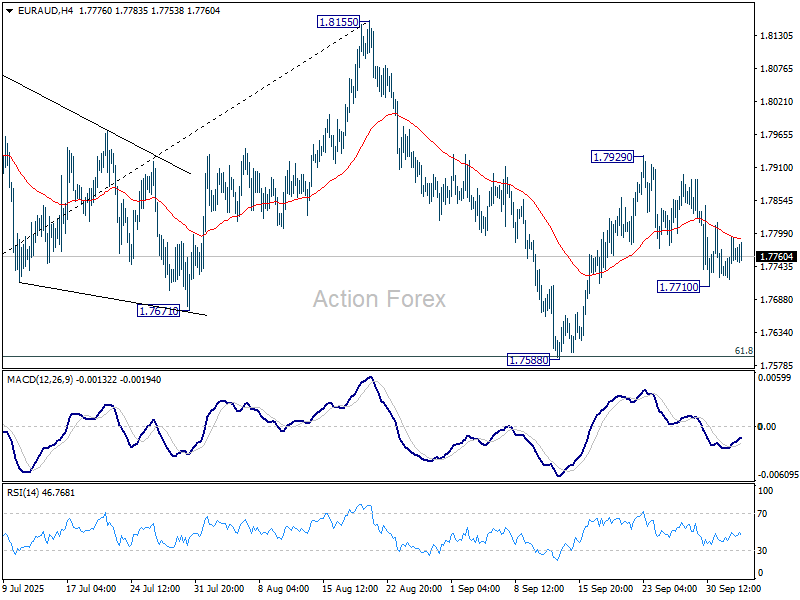

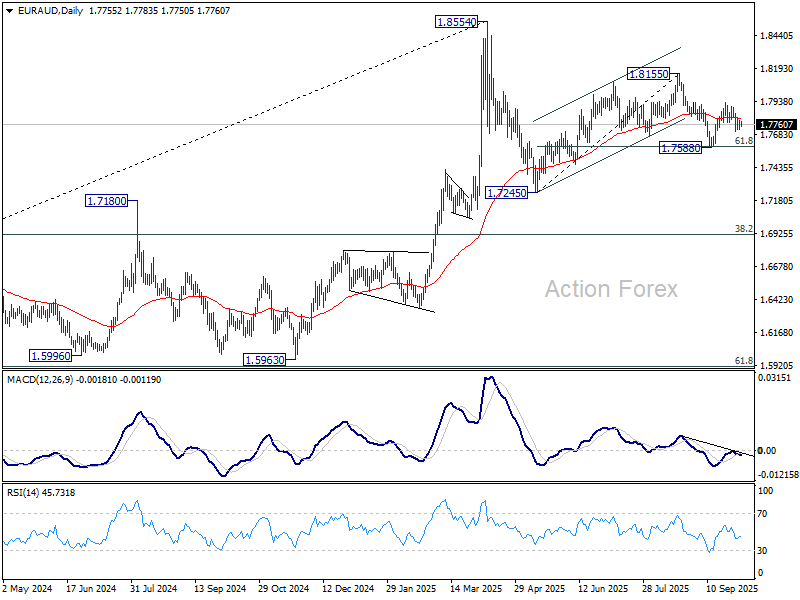

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7725; (P) 1.7760; (R1) 1.7796; More...

Intraday bias in EUR/AUD stays neutral and outlook is unchanged. On the upside, above 1.7929 will resume the rebound from 1.7588 to retest 1.8155. However, sustained break of 61.8% retracement of 1.7245 to 1.8155 at 1.7593, will resume the fall from 1.8155 to 1.7245 resistance, as part of the corrective pattern from 1.8554 high.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

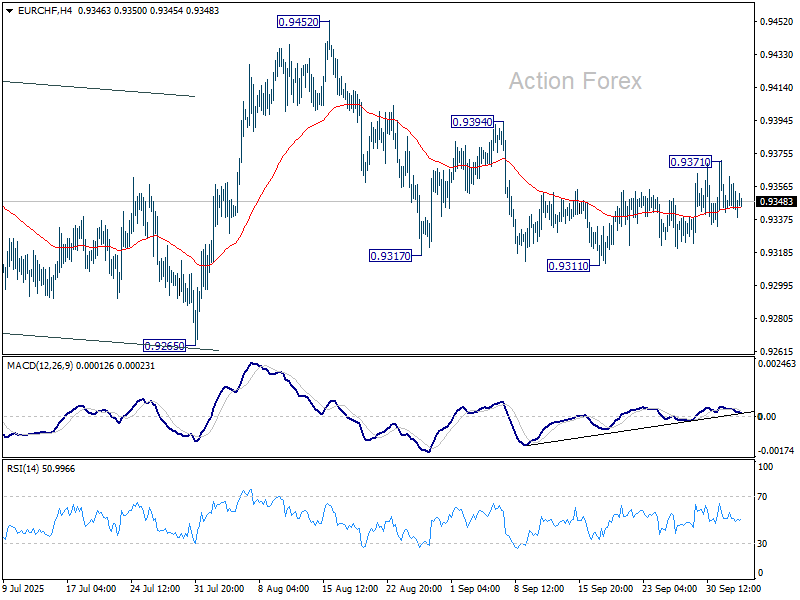

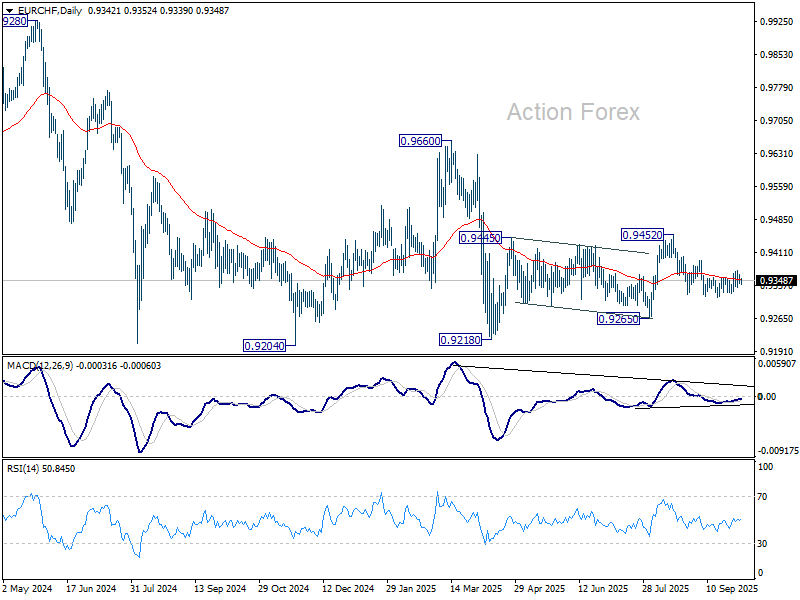

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9337; (P) 0.9351; (R1) 0.9362; More...

Range trading continues in EUR/CHF and intraday bias remains neutral. On the upside, above 0.9371 will target 0.9394 resistance. Firm break there should confirm that the pullback from 0.9452 has completed, and bring retest of this resistance. Nevertheless, break of 0.9311 will resume the fall from 0.9452 to 0.9265 support.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

Yen Underperforming After ‘Balanced’ Comments from BOJ Ueda

Markets

The US government shutdown to a large degree translated into a ‘market info shutdown’. US data releases including jobless claims and factory orders were delayed, depriving investors of some potential drivers. Especially jobless claims over the previous weeks showed some (intraday) market moving potential. With no key data in other developed economies like the EMU or the UK, this only reinforced the low volatility environment. This not only applies to US equity markets but also to interest rate markets and FX. A measures of US bond market volatility has dropped to the lowest level since end 2021! As a point in case. US yields yesterday changed between + 0.4 bp (2y) and -2.1 bps (30-y). German yields in similar directionless trading eased between 0.3 bps (2-y) and -2.5 bps (30-y). For now, the adagio ‘no news is good news’ reigns. The S&P 500 closed at a marginal new all-time record. The EuroStoxx 50 decisively confirmed Wednesday’s break into uncharted territory (+1.15%). A similar low-volatility narrative also plays in the major dollar cross rates. The dollar didn’t budge despite a positive risk sentiment and the prospect/hope of Fed easing. DXY gained marginally (97.85) but perfectly holds in the 96.21/98.83 short-term consolidation range. Idem for EUR/USD (close 1.1715 from 1.1732). Even the yen, one of the more outspoken directional trades in major FX this week, wasn’t able to maintain its momentum. After a failed test of the 150 area end last week, the yen rebounded yesterday after running into resistance in the USD/JPY 146.60 area. Comments supportive of a (potential) rate hike at the end of this month from deputy government Uchida, didn’t help further yen gains.

Most Asian equity markets continue a (tech-driven) rally this morning with Japan one of the outperformers. China and South Korea are closed. Still the dollar gains marginally, with the yen this time underperforming after ‘balanced’ comments from BOJ governor Ueda (see below). An unexpected rise in the Japanese unemployment rate in this respect probably also doesn’t help (2.6% from 2.3%). Later today, the US labour market data won’t be published due to the shutdown, but markets at least have the US services ISM as one of the few remain guides in the run-up to the October 29 Fed decision. US confidence indicators recently suggested a further loss of momentum including softer labour market conditions. Today’s services ISM is expected at 51.7 (from 52) with the employment index near 46.5. With two follow-up 25 bps Fed rate cuts almost fully discounted, there is far less room for a similar reaction compared to this week’s ADP miss. Maybe it might still have some limited impact on the dollar, more than on US interest rates, with USD/JPY most sensitive even as Japanese domestic factors (LDP leadership vote) are in play.

News & Views

Bank of Japan governor Ueda kept options open for the end-of-the month policy meeting. In a speech for local business leaders, he didn’t extend market momentum endorsing a 25 bps rate hike instead sticking to official guidance. “If the baseline scenario for economic activity and prices outlined so far is realized, the bank, in accordance with improvement in economic activity and prices, will continue to raise the policy rate”. On the economic front, the central bank monitors the global economy and the impact of US tariffs on Japan’s corporate profits. On the price front, wage and food inflation require attention. Ueda made no reference to domestic political uncertainty, but for sure keeps a close eye on local LDP leadership elections this weekend. The risk of snap parliamentary elections ahead of the next BoJ meeting is still a tail risk.

Bank of Canada deputy governor Mendes indicated that markets are too focused on the central bank’s “preferred” core inflation measures. They were introduced in 2016 under former governor Poloz with two of the three original ones remaining (trimmed mean and median). They show annual price pressures around 3%, but the BoC sees underlying inflation in the vicinity of 2.5%. Mendes argued that the way the central bank measures inflation will be part of next year’s framework renewal. As an example, he suggested revising inflation gauges so they all “pre-exclude mortgage interest costs”. The BoC revamped its cutting cycle in September after a six-month pause with money markets 50/50-split over the possibility of a new rate cut (to 2.25%) at the end of this month.

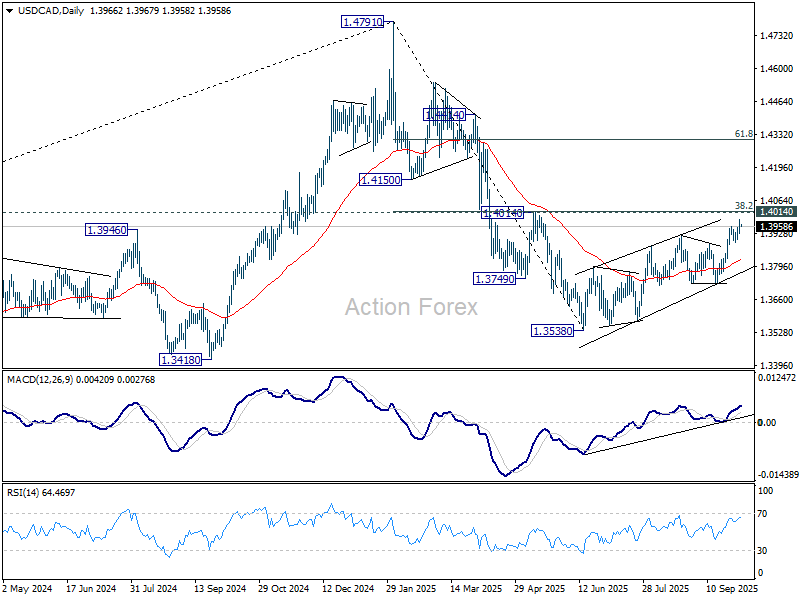

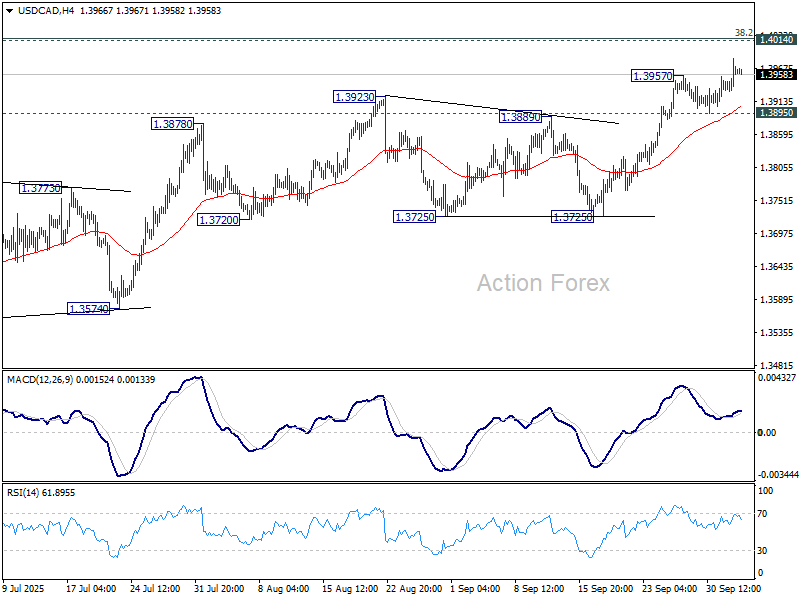

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3938; (P) 1.3962; (R1) 1.3991; More...

USD/CAD's rally resumed by breaking through 1.3957 and intraday bias is back on the upside. Strong resistance is expected from 1.4014 cluster to complete the corrective rebound from 1.3538. On the downside, break of 1.3895 support will turn bias back to the downside for 1.3725. However, sustained break of 1.4014 will carry larger bullish implications.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069. However, sustained break of 1.4014 will argue that fall from 1.4791 has completed, and bring stronger rally to 61.8% retracement at 1.4312.