Sample Category Title

Guide to FOMC Statement and September SEP: Key Takeaways and What to Watch

The most important day in a few trading months is coming up fast (two days left!).

The September FOMC rate decision is part of four quarterly meetings where key economic projections (SEP or Summary of Economic Projections) are published (don't forget the 4 other meetings). They take place in March, June, September and December.

These quarterly meetings tend to hold higher weight on potential changes to the FED's tone. With Wednesday's meeting in focus, markets are preparing for a change in tone and changing SEPs.

While the decision itself may not surprise (25 bps is heavily priced in and should be the basis except for any surprise), the details in the projections and Powell’s tone at the press conference will dictate the market reaction.

One good thing to do is to also follow any pre-FOMC post from Wall Street Journal's Nick Timiraos who re-guided wrongly priced markets during the 2022 hike cycle and is considered as an insider. The FED "leaks" their own info that way to avoid shaking markets too suddenly, with the US dollar's central role in the global economy – As a reminder, FED members cannot speak on the Economic or financial outlook two weeks before the FOMC meeting in what is called the "Blackout period".

Don't forget to also check out our freshly released Podcast with discussions on the upcoming FOMC.

(and Too Long, Didn't Read recap further down if needed).

What to take from the previous meeting

At the previous meeting (July 30, 2025), Powell struck a balanced but cautious tone amid still high tariff uncertainty.

He acknowledged progress on disinflation but highlighted tariff-driven risks to the inflation outlook. His remarks left the door open to cuts later in the year, but the Fed emphasized it would remain data-dependent.

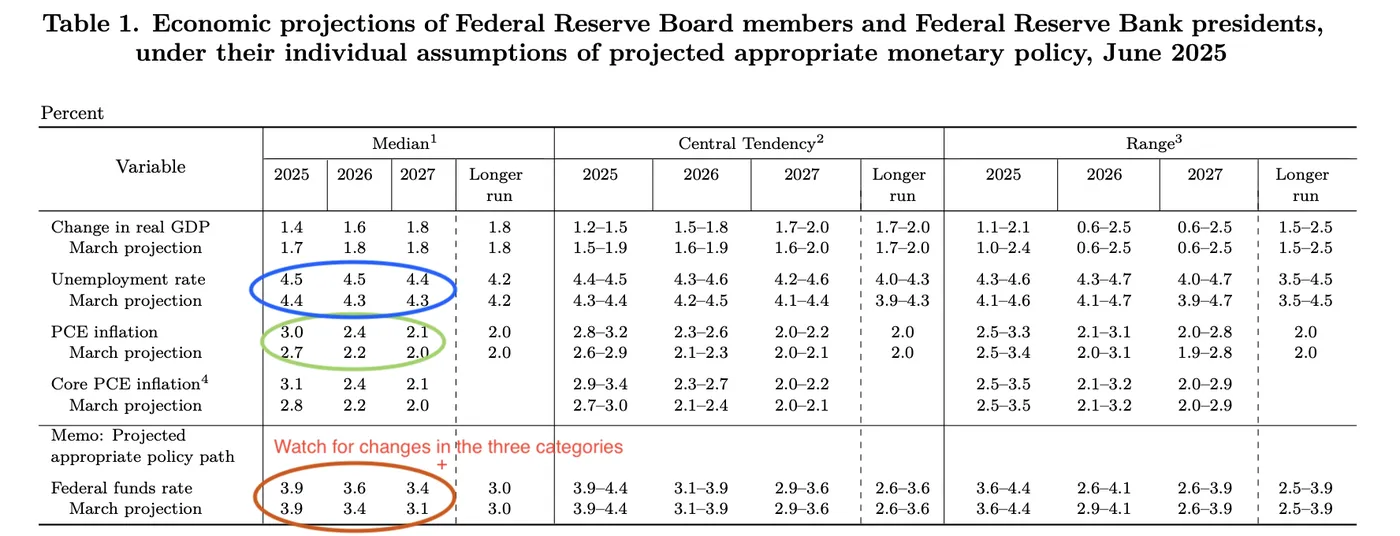

The June last SEP reflected this stance: inflation forecasts were nudged slightly lower, growth remained resilient, and the famous dot plot still suggested two cuts before year-end — a point markets have since debated heavily.

June 2025 SEP, source: Federal Reserve

What to watch in the September SEP

- Dot Plot: The median projection for rate cuts will be the market’s first checkpoint. A shift from two cuts to one would reinforce a hawkish narrative, while holding steady would keep the Fed aligned with current pricing.

- Inflation forecasts (Core PCE, PCE): Expect markets to scrutinize whether tariffs are raising the Fed’s inflation expectations. Any upward revision would challenge the softening CPI and PPI figures released this week and the change in tone from Powell's Jackson Hole speech. The inflation projections might be revised upward in 2025 and down in later year: Major key is to watch 2026 PCE projections and onwards to get a glimpse of 2026 cut pricing (currently 140 bps are priced in).

- Unemployment rate: A move higher would confirm the gradual softening already seen in recent jobs reports – A sudden rise in this could shift the pace of cuts priced in.

What was said in Powell's previous FOMC speech?

You can access Powell's July FOMC speech right here. I also invite you to balance these comments with what was said in his Jackson Hole speech (link available just above).

Through his July speech, Powell emphasized the FED's dual mandate (inflation and maximum employment) and could be expected to put an extra emphasis on the employment mandate with the Labor market data degrading.

He also emphasized a moderating economic activity with tariff uncertainty (uncertainty should be expected to get less mentions).

Reading Jerome Powell’s speech.

Markets know by now that Powell’s tone matters as much as the text. Expect sharp reactions to how he balances:

- Confidence in inflation trending lower vs. caution about tariff pass-through.

- Reassurance on labor market strength vs. acknowledgment of weakness in recent payrolls.

- Whether he hints at future financial stability concerns, particularly with equities and crypto markets surging.

Analysts tend to highlight the number of mentions for elements like: Employment/unemployment, inflation, tariffs etc to spot what the FED will focus on looking forward.

Market dynamics

Current state of Markets, September 15, 2025 – Source: TradingView

Bond yields have already been retreating, with the 2Y at its lowest since April’s “Liberation Day” trough. Don't forget to take a look at the 2-10s curve: Currently very steep due to higher short-term cut expectations but higher inflation (= higher long term rates)

Risk assets are at all-time highs, therefore the Markets hold high expectations for a dovish tone, watch out for disappointments !

FX markets remain rangebound, leaving the Dollar Index exposed to any surprises in the dot plot or Powell’s tone – One of the thesis I had been holding is the Seller's inability to reach new lows in a hesitant Dollar, but its reaction is still binary.

With high expectations of a dovish speech, Powell could balance out recent dovish pricing with a more hawkish stance which would strengthen the US Dollar and hurt Equities a bit.

TLDR conclusion: What to focus on for the upcoming FOMC

TL,DR:

- For now a bit less than 75 bps priced in through 25 bps at every meeting.

- SEP: Particularly expected Fed Funds rate in end 2025 and 2026 (Neutral rate should be priced in until then for now) and Core PCE projections.

- More or less mentions of tariffs: Any hints of one time price hikes could bring more cuts in the future. More mentions of uncertainty = less hikes in 2026.

- Labor market and unemployment rate: If see more mentions of degrading employment, it could add more rate cuts more suddenly – Particularly if the FED balances out its dual mandate more towards employment.

- Any hawkishness to balance out the most recent dovish comments and give back some credibility to the FED's independence

Safe trades and a successful FOMC week!

Dollar Falls Which Takes EUR to August Highs – EURUSD and DXY Outlooks

The US dollar finally breaks its range ahead of Wednesday's FOMC as market participants keep placing their pre-Meeting bets.

After holding between 97.50 to 98.50 since August 11th, the Dollar Index has failed to hold support to start this week to regain lows reached in the previous week's downward fakeout.

With Equities rallying to their continued highs, hopes for a dovish cut are extremely optimistic which could lead to some furious reactions.

This move notably weakening the US Dollar also assisted majors like the British Pound and the Aussie to reach new highs.

As a matter of fact, despite the odds for 50 bps retracting from 10% to 4% since Thursday, the US dollar still broke support which could be due to position closing or hedging (more on this in the EURUSD analysis) – Some mean-reversion buying is happening as I write this piece which deserves a close look.

The Euro is also getting close to its August 22 peak which got reached right after Jerome Powell's Jackson Hole speech – As the FOMC approaches, let's have a look at levels for the EURUSD and the Dollar Index.

EURUSD 4H Chart – close to new monthly highs but forms a convergence

EURUSD 4H Chart, September 15, 2025 – Source: TradingView

Buyers took the most traded currency pair to about 120 pips from its Monthly highs and will have to do more work to reach new highs.

A short-term bearish convergence (where a lower high in price = lower high in RSI) could prevent further movement – Don't forget that even if Market had to retrace from here, rangebound consolidation could impede much movement before.

Nonetheless, the action is still evolving in an upward channel which should be monitored for breakout/continuation scenarios.

A dovish cut from the FED could easily propulse the pair to new yearly highs (currently 1.1830) and vice-versa, but looking at the charts and recent price action, downside reactions could be heavier on a hawkish FED (which would also trigger many other Markets to revert).

Keep a close eye on pre-FOMC trading in the pair, the highest it goes, the more dovish the expectations for Wednesday.

Levels of interest for EURUSD trading:

Resistance Levels:

- 1.1780 September 9th highs

- Main resistance 1.18 to 1.1830 (yearly highs)

- 1.20 psychological level and 2021 highs

Support Levels:

- 1.1750 Intermediate Pivot (+/- 150 pips)

- 1.1650 Key support

- 1.16 Main support

- 1.1470 Pivotal Support (bearish below this)

Dollar Index (DXY) breaks its range support, what next?

It is surprising to see that the range that held so strongly amid many dovish data points (dovish NFPs, last week's CPI and PPI) just before breaking at the weekly open.

These days, everything can happen in Markets but in the past, action tended to stay more rangebound throughout the first few days of the week before the Wednesday meetings. However, everything is possible!

A test of the past week fakeout-lows is approaching and breaching it could lead to further technical downside.

However, the fundamentals of players putting more positions right before the FOMC are not adding up too much, so my guess would be that participants are currently hedging for a potential 50 bps cut, leading to the current moves.

Watch the 97.25 lows, buyers are currently mean-reverting right just above these lows.

Levels to watch for the Dollar Index:

Support Levels:

- 97.40 to 97.80 Range Support (currently getting broken, fakeout?)

- Last Pivot before run-higher 97.15 Zone acting as Key Support

- 2025 Lows Major support 96.50 to 97.00

Resistance Levels:

- 98.00 Mid-Range pivot

- 98.50 to 98.80 Resistance Zone

- Mid-line of the ascending channel and psychological level 99.50

- 100.00 Main resistance zone

Safe trades and a successful FOMC week!

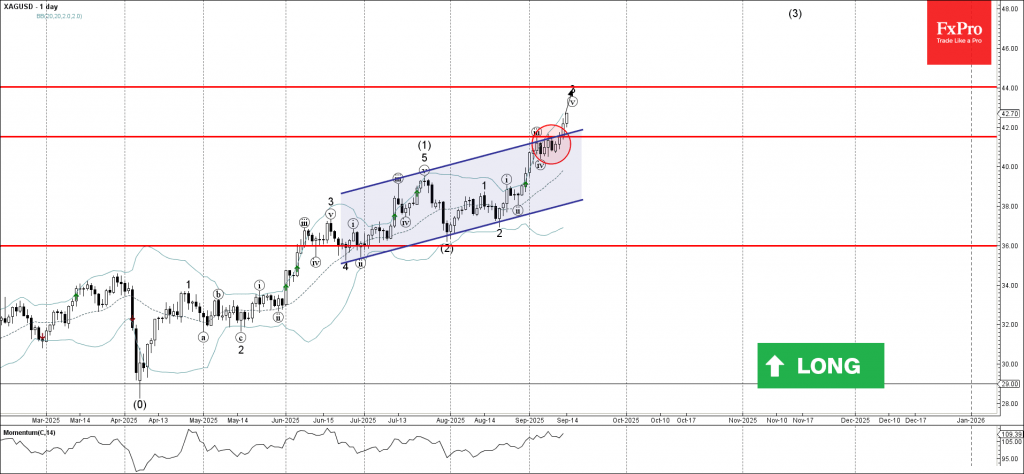

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver broke the resistance area

- Likely to rise to resistance level 44.00

Silver recently broke the resistance area between the key resistance level 41.50 (which stopped the previous impulse wave iii) coinciding with the resistance trendline of the daily up channel from June.

The breakout of this resistance area accelerated the active impulse wave v of the higher-order impulse waves 3 and (3).

Given the clear daily uptrend, Silver can be expected to rise to the next resistance level 44.00, target for the completion of the active impulse wave 3.

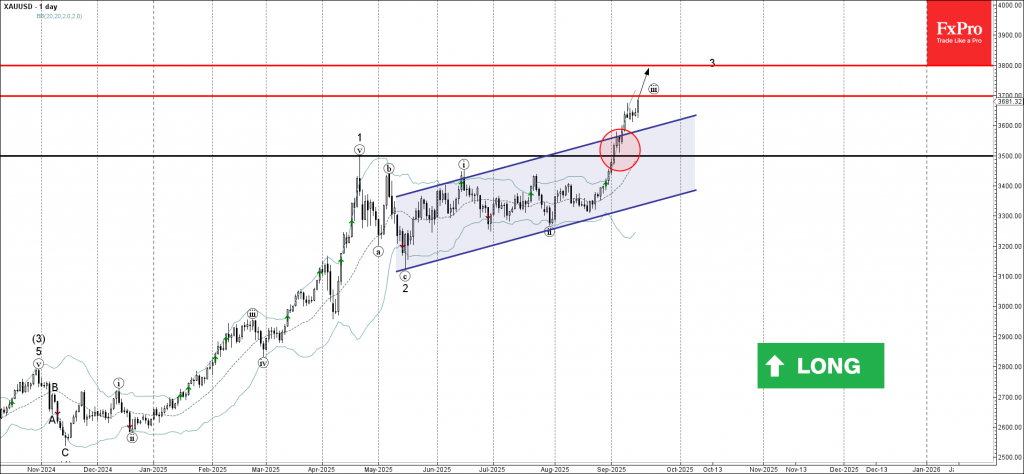

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold broke resistance area

- Likely to rise to resistance levels 3700.00 and 3800.00

Gold recently broke the resistance area between the key resistance level 3500.00 (which stopped the sharp impulse wave 1 in April) and the resistance trendline of the daily up channel from May.

The breakout of this resistance area accelerated the active impulse wave iii of the medium-term impulse wave 3 from the start of May.

Given the clear daily uptrend, Gold can be expected to rise to the next resistance level 3700.00 – followed by 3800.00 (target for the completion of the active impulse wave 3).

Nasdaq-100 Wave Analysis

Nasdaq-100: ⬆️ Buy

- Nasdaq-100 broke key resistance level 24000.00

- Likely to rise to resistance level 25000.00

Nasdaq-100 index recently broke above the key resistance level 24000.00 (upper border of the narrow sideways price range inside which the index has been trading from July).

The breakout of the resistance level 24000.00 accelerated the active impulse wave v of the higher order impulse wave 5 from June.

Given the clear daily uptrend, Nasdaq-100 index can be expected to rise to the next resistance level 25000.00, target for the completion of the active impulse wave v.

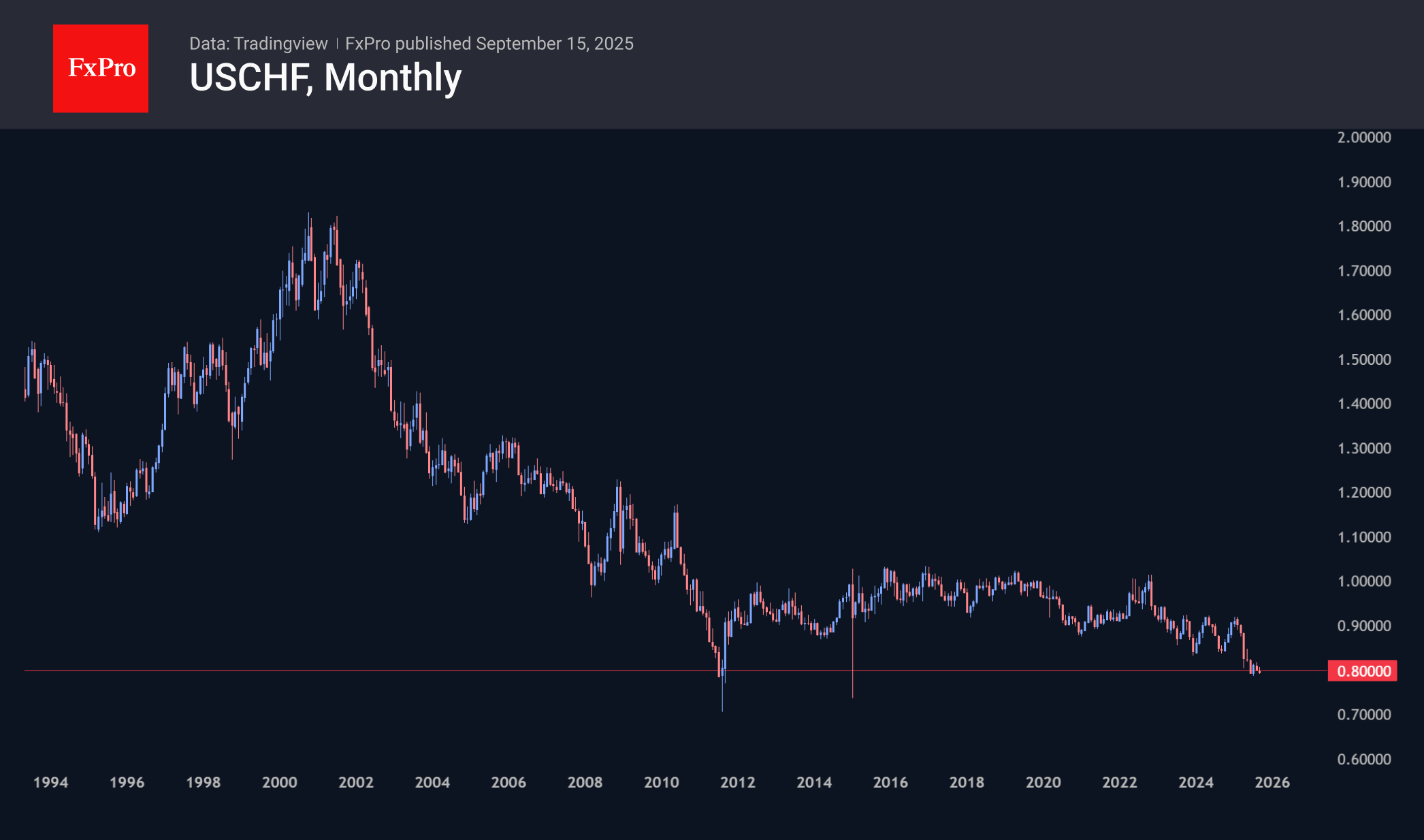

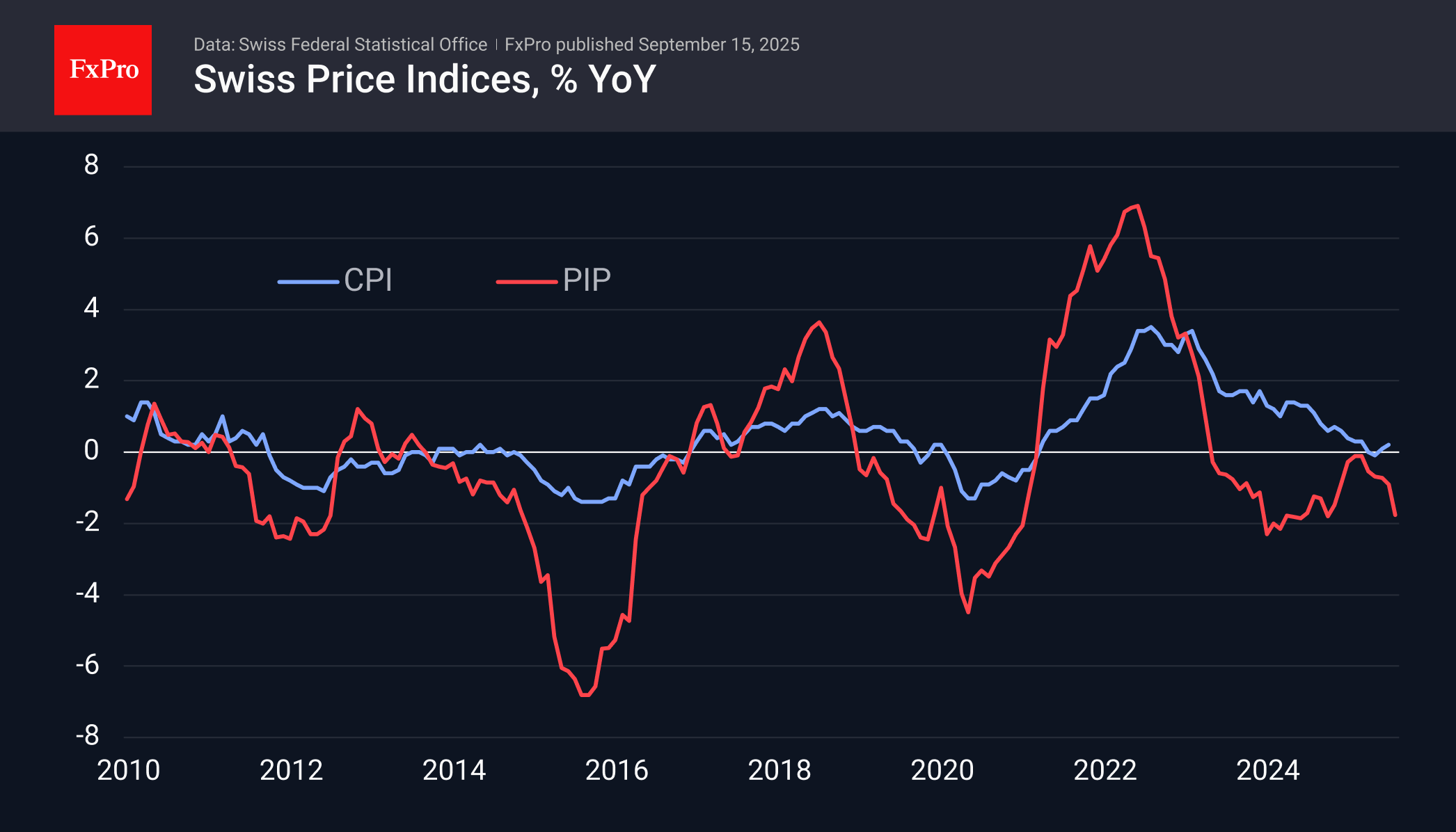

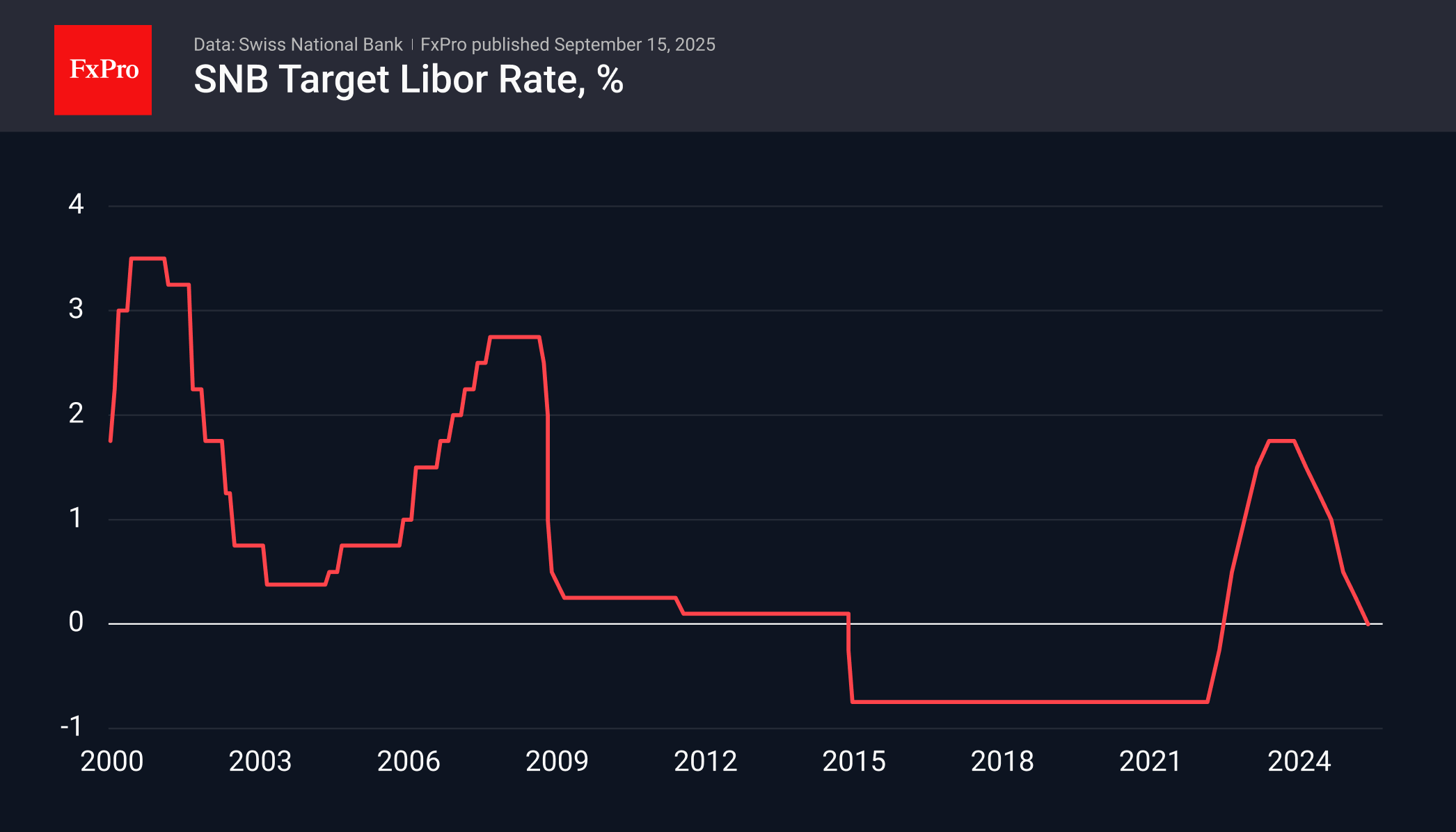

Franc Entered Turbulence Zone, Ball on the Side of SNB

USDCHF is trading below 0.8000, returning to the area of 14-year lows after rebounding from these levels in July. Earlier, in 2010 and 2014, the pair traded lower only in free-fall mode, forcing the central bank to intervene and reverse the trend. Although the Swiss National Bank has cut its key rate twice this year, and the Fed did so most recently in December last year, the dynamics of the currency market clearly show how the market values policy predictability and trade surplus this year.

At its quarterly meeting on 25 September, the SNB has every opportunity to increase pressure on the currency by easing monetary policy, as other competitors (the ECB, the Bank of England and colleagues from New Zealand and Australia) have implemented more easing measures this year.

Inflation needs support, not restraint. A recent report on 15 September noted the fourth consecutive month of decline in the producer and import price index, totalling 1.3%, with August accounting for almost half of this decline. From August last year, the decline had accelerated to 1.8%, the largest since June 2024, remaining in negative territory for the last 28 months. Annual consumer price inflation is close to zero, and the sharp decline in PIP increases the risks of deflation in the coming months.

Foreign trade is also showing the first signs of problems amid the strong franc. July estimates showed exports falling by almost a quarter compared to March’s peak, with imports down more than 22%.

The consumer climate index also resumed its decline in August, which should help strengthen the position of doves in the central bank.

The SNB already lowered its target rate to 0% in June, returning to zero or negative rates for the first time. The bank has previously indicated that it is prepared to go lower. Still, we also believe that further steps carry the risk of a resumption of forex interventions involving the printing of francs to buy foreign currency. These measures are designed to increase the supply of CHF on the global market. Such measures could halt the franc’s appreciation against key global currencies, which is beginning to harm the national economy.

If these assumptions are confirmed, current levels could prove to be a turning point for USDCHF and other crosses with the franc.

WTI Oil Rallies 1% After Ukrainian Attacks on Russian Oil Facilities, Russia Sanction Calls Grow

Oil prices have risen as much as 1.17% at the start of the week following claims by Ukrainian forces that their recent drone attacks have hit two major Russian oil centers in the Baltic Sea.

According to reports, these strikes temporarily halted crude oil shipments at Primorsk, Russia's biggest oil port, late last week. There are also claims that three pumping stations that send oil to another port, Ust-Luga, were also attacked.

Russia Sanction Calls Grow

Add to this growing calls for harsher sanctions on countries and entities which are still purchasing Russian Oil.

Pressure is increasing on Russia after a statement from the U.S. President. On Saturday, he said the U.S. is ready to place new sanctions on Russia's energy sector. However, this would only happen if all NATO member countries agree to stop buying Russian oil and enforce similar actions.

Markets appear cautious in this regard and thus oil prices remain supported.

China Oil Demand Robust Despite Poor Industrial Production Data

Based on data from this morning, Chinese oil refiners processed almost 15 million barrels of crude oil per day in August. This is a 7.6% increase from the same time last year, thanks to a combination of strong oil imports and more oil being produced within China.

Additionally, the apparent demand for oil in China—the amount of oil being used—rose to 14.53 million barrels per day last month, which is a 4.9% increase compared to August of the previous year.

This comes as Chinese data off late have shown signs of deterioration which may be a concern moving forward. For now though, Oil demand and refining remains at impressive levels which will also support oil prices as it mitigates any fears around a demand slowdown for now.

Outlook Moving Forward

Despite the rally we are seeing today Oil prices upside potential may remain limited. The reason for this is largely down to growing expectations of a potential slowdown in global growth for the rest of the year.

OPEC + output hike has also added to the dilemma which is keeping Oil prices relatively rangebound.

Later in the week, the Federal Reserve interest rate decision could have a knock-on impact on oil prices as well. We will also get updated inventories data as markets brace for a potential inventory build-up in Q4 2025.

![]()

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Technical Analysis - WTI

From a technical analysis standpoint, Oil is eyeing a move toward the 100-day MA which rests at 64.65.

Oil has failed to break above the 64.00 a barrel mark since September 4.

Any attempt to break above this level has been met with significant selling pressure.

However, a close around the current price would provide some hope for bulls, as it would be seen as a morningstar candlestick pattern which hints at further upside.

Any move will depend on developments around Russia/Ukraine which for the moment seems to be the major driving force of Oil price moves.

Immediate resistance rests at 64.00 before the psychological 65.00 mark and the 200-day MA at 67.15 come into focus.

Looking at support to the downside and the first point of interest will be the recent swing low at 62.19 before the 60.77 and psychological 60.00 handle come into focus.

WTI Oil Daily Chart, September 15, 2025

Source: TradingView (click to enlarge)

British Pound Hits Two-Month High, UK Job Data Next

The British pound has started the new trading week in positive territory. In the European session, GBP/USD is trading at 1.3591, up 0.26% on the day. Earlier, the pound hit a daily high of 1.3620, its highest level since July 10.

UK claimant count change expected to jump

The UK releases employment data on Tuesday. Claimant counts is expected to jump to 20.3 thousand in August, after a rare decline in July which saw claimant counts decline by 6.2 thousand. The unemployment rate is expected to remain at 4.7% for a third straight time, its highest level in four years.

Wage growth including bonuses is expected to rise to 4.7%, up from 4.6% in the previous release, which was the lowest pace in nine months.

It's a busy week in the UK, with the inflation report on Wednesday and the Bank of England rate decision on Thursday. The BoE is expected to maintain rates at 4.0% after last month's narrow 5-4 decision to lower rates. Governor Bailey has said rates would move "downwards gradually over time" but hasn't provided any details as to the timing or extent of cuts.

The new danger - stagflation

The UK may have already entered stagflation, which is a toxic mix of persistently high inflation, weak growth and rising unemployment. This presents a major headache for the BoE, as weak growth supports a rate cut while high inflation could get worse if the BoE reduces rates.

The central bank is hesitant to lower rates with inflation close to 4%, but may have to cut before the end of the year if the labor market continues to deteriorate. Tuesday's job report is unlikely to change minds at the BoE, which is expected to hold rates. Still, it could be a factor in the November rate decision.

GBP/USD Technical

- GBPUSD has pushed above resistance at 1.3564 and is testing 1.3589 Above, there is resistance at 1.3605

- There is support at 1.3548

GBPUSD 1-Day September 15, 2025

Sunset Market Commentary

Markets

A slow start to the new trading week. Multiple Chinese data (including production, retail sales, investment and a higher than expected jobless rate) all came in weaker than expected this morning. The Chinese economy struggles as the US and China still are trying to make progress in talks on tariffs and economic policy in Madrid currently. This kind of underperformance as usual raised market talk on potential additional (fiscal) stimulus. Question remains whether it will be enough to overcome multiple uncertainties that consumers and corporates are facing. Poor data at least had little impact on the yuan. After a new upleg in August, the yuan this morning is holding recent gains (USD/CNY 7.122). Regarding developed markets, eco data were few in EMU and the US. Even so, an unexpectedly sharp decline in the US empire manufacturing survey (-8.7 , from 11.9) solidified the case for the Fed to restart scaling back policy restriction on Wednesday. Aside from poor activity sub-indices (orders and shipments sharply down), also the pay component eased further. US yields currently decline between 2.2 bps (30-y) and 3.5 bps (5-y). Key technical levels in the 2-y (3.43/3.5% area) and the 10-y (4% area) are nearby but not really challenged yet. EMU (short-term) yields have found a new equilibrium after chair Lagarde last week indicated that the disinflation process is over and that risks to growth are balanced rather than skewed to the downside. ECB board member Isabel Schnabel in a presentation today also guided that interest rates are in a good place as inflation stabilizes around 2%. She even sees the economy expanding above potential while the pass-through of a stronger exchange rate is likely to be limited. In this respect, she even warned that upside inflation risks again dominate, referring to tariffs, services inflation, food inflation and fiscal policy as potential drivers. Earlier today, ECB’s Kazimir indicated that there is no need for the ECB to act to tiny deviations from the 2% target and that it would be a mistake to neglect upside inflation risks. The bar for an additional ECB rate cut has been put quite high. No additional damage from the Fitch rating downgrade of France to the ‘single-A’ category. The 10-y French-German spread even narrows marginally (78 bps).

On FX markets the dollar underperforms as markets anticipate on protracted further Fed normalization. This hoped for easing of (global) financial conditions supports smaller, cyclically sensitive currencies. The euro slightly outperforms the dollar (EUR/USD 1.1765) and trades in line with the yen (USD/JPY 147.3; EUR/JPY 173.25) and sterling (EUR/GBP 0.8646) as investors also look forward to the BoE (Thursday) and BoJ (Friday) policy decision (both expected unchanged). On Central European markets, the forint still outperforms other regional FX with EUR/HUF testing the 390 barrier for the first time since July last year.

News & Views

Eurostat released EMU trade data for the month of July. First estimate showed a €12.4bn surplus in trade in goods with the rest of the world (non-seasonally adjusted), up from €7bn a month ago, but down from €18.5bn in July of last year (mainly attributed to chemicals and related products). EMU exports of goods to the rest of the world in July 2025 were €251.5 bn (+0.4% Y/Y). Imports from the rest of the world stood at €239.1 bn (+3.1% Y/Y). The EU trade surplus with the US declined from €18bn in July of last year to €13bn in July 2025 (€10.7bn seasonally-adjusted). Exports fell by 4.4% Y/Y to €44.2bn with imports growing by 10.7% to €31.2bn. Among major trading partners, the EU had the biggest trade surplus with the UK (€16.7bn from €15.9bn in July 2024) and the largest deficit with China (-€30.7bn from -€27.6bn in July 2024). On a seasonally-adjusted base, the EMU trade surplus rose from €3.7bn to €5.3bn with exports decreasing by 0.1% M/M and imports by 0.8% M/M.

According to statics Poland, inflation rose by 0.1% M/M and 2.9% Y/Y (up from flash estimate at 2.8% Y/Y). Goods prices fell by 0.3% M/M to be up 1.7% Y/Y (from 1.9%) while services prices increased 0.7% M/M to 6% Y/Y (from 6.2%). The highest monthly contribution came from communication prices (+1.4% M/M), alcoholic beverages and tobacco (0.4% M/M) and restaurants and hotels (0.3% M/M). Lower prices related, among others, to clothing and footwear (-1.5% M/M), transport (-0.4% M/M) and food (-0.1% M/M). Today’s data should keep the National Bank Poland sidelined at its next, October, policy meeting, but keep the door slightly open for another rate cut in November when a new Monetary Policy Report is available and when there will be more clarity on extending (or not) the current electricity price freeze..