Sample Category Title

European Central Bank Pauses Again, Further Easing Still Possible

Summary

- The European Central Bank (ECB) held its Deposit Rate steady at 2.00% at today's monetary policy announcement, keeping its monetary policy stance on hold for the second meeting in a row. The accompanying statement was neutral in tone and offered little in the way of forward guidance on future policy moves.

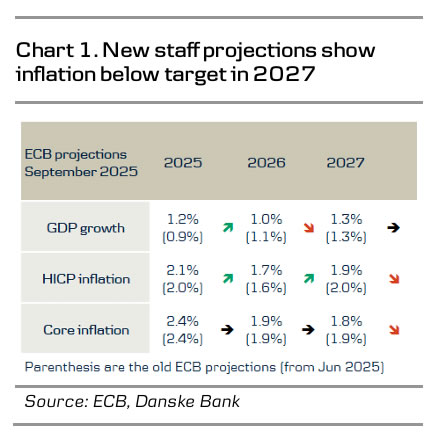

- The ECB made only modest revisions to its economic projections, raising its economic growth outlook modestly, while lowering its forecast for underlying inflation very slightly. The ECB projects underlying inflation at 2.4% for 2025, 1.9% for 2026, and 1.8% for 2027. The fact that the central bank's medium-term inflation forecasts are below the 2% inflation target, and the 2027 forecast was revised lower, are modestly dovish signals in our view. The dovish signal from the economic projections was largely offset however by comments from ECB President Lagarde. She said that growth risks were balanced, and suggested the disinflationary process for the Eurozone is now over.

- Despite the overall neutral tone of today's announcement, we expect the evolving growth, wage and inflation trends will still see the ECB deliver one final 25 bps rate cut, to 1.75%, at its December meeting. We expect growth to soften in the coming quarters, reflecting slower employment and income growth, and still subdued sentiment and confidence. Meanwhile, wage and labor cost pressures continue to show a gradual deceleration, which we view as consistent with core inflation converging to target and leading to modest further monetary easing.

European Central Bank Pauses For a Second Meeting

The European Central Bank (ECB) held its Deposit Rate steady at 2.00% at today's monetary policy announcement, keeping its monetary policy on hold for the second meeting in a row. The ECB offered little in the way of new guidance, while making only marginal changes to its economic projections. Overall, our outlook for ECB monetary policy remains unchanged, and we still see potential for modest further monetary easing.

Today's announcement was perhaps even more concise than usual, with the ECB simply saying its "assessment of the inflation outlook is broadly unchanged." That is reflected in the ECB's updated economic projections, which saw a modest upgrade to the growth outlook, and a very mild downgrade to the underlying inflation outlook. The central bank forecasts GDP growth of 1.2% for 2025 (previously 0.9%), 1.0% for 2026 (previously 1.1%) and 1.3% for 2027 (unchanged). With regard to underlying inflation (CPI excluding food and energy), the ECB forecasts underlying inflation of 2.4% in 2025 and 1.9% in 2026 (both unchanged) and 1.8% in 2027 (previously 1.9%). Despite only minor changes, we view the updated inflation forecasts in particular as noteworthy. The minor downward revision to the 2027 inflation forecast is, in our view, a modestly dovish signal. Moreover, with both the 2026 and 2027 underlying inflation forecasts below the ECB's 2% inflation target, it leaves open the possibility of further easing, without guaranteeing it. The dovish signal from the economic projections was largely offset however by comments from ECB President Lagarde. She said that growth risks were balanced, and suggested the disinflationary process for the Eurozone is now over.

The ECB also said it is determined to ensure that inflation stabilizes at its 2% target and, in a familiar refrain, said it "will follow a data-dependent and meeting-by-meeting approach" and that it is “not pre-committing to a particular rate path.” The importance of the underlying inflation outlook was also reinforced by the ECB's comment that its decision will be based, among other things, by "the dynamics of underlying inflation and the strength of monetary policy transmission."

We Still Expect a Final ECB Rate Cut Later This Year

While the ECB held rates steady at today's meeting, we believe the evolving growth, wage and inflation trends could still see the central bank deliver one final 25 bps rate cut, to 1.75%, at its December meeting. That would take the ECB's policy rate towards the "accommodative end" of what view as the neutral range, of between 1.75% to 2.25%. We expect a slower pace of economic growth over the second half of 2025 and still see some downside risks to the growth outlook, while we also think wage and price fundamentals remain consistent with a gradual disinflationary trend toward the 2% inflation target.

Eurozone Q2 GDP grew by just 0.1% quarter-over-quarter, after a 0.6% gain in Q1. While that headline result might overstate the degree of weakness (our estimate of underlying final domestic demand rose 0.3% in Q2), there are still reasons to expect a slower pace of growth over the next few quarters. Income trends have begun to soften, as Q2 real employee compensation slowed to 2.5% year-over-year, while Q1 real household disposable income rose by even less, with a 0.8% gain. Slow income growth, combined with an overall cautious consumer (as reflected in unusually elevated savings rates in recent quarters) will likely be consistent with only a modest pace of Eurozone consumer spending, at best, in the coming quarters. Reinforcing the slowing income trend is a deceleration in job growth. Eurozone Q2 employment rose by just 0.6% year-over-year, and forward-looking employment indicators suggest a slight further slowing in job growth remains possible.

While increased defense spending could support investment spending over the medium-term, the immediate prospects for investment spending are also mixed. Our measure of core ex-housing investment dipped by 0.1% year-over-year in Q2, and low levels of capacity utilization suggest sluggish investment spending for the time being. While acknowledging that uncertainty, especially surrounding trade and tariff policy, has receded to some extent, a still somewhat unsettled environment is also a limiting factor for the near-term investment outlook. The Eurozone August manufacturing PMI rose to 50.7 while the services PMI slipped to 50.5. Neither index is at a level, however, that suggests upbeat sentiment which would be consistent with stronger investment spending. Moreover, the PMI surveys are also at levels that are historically consistent with only a modest pace of overall economic growth more broadly.

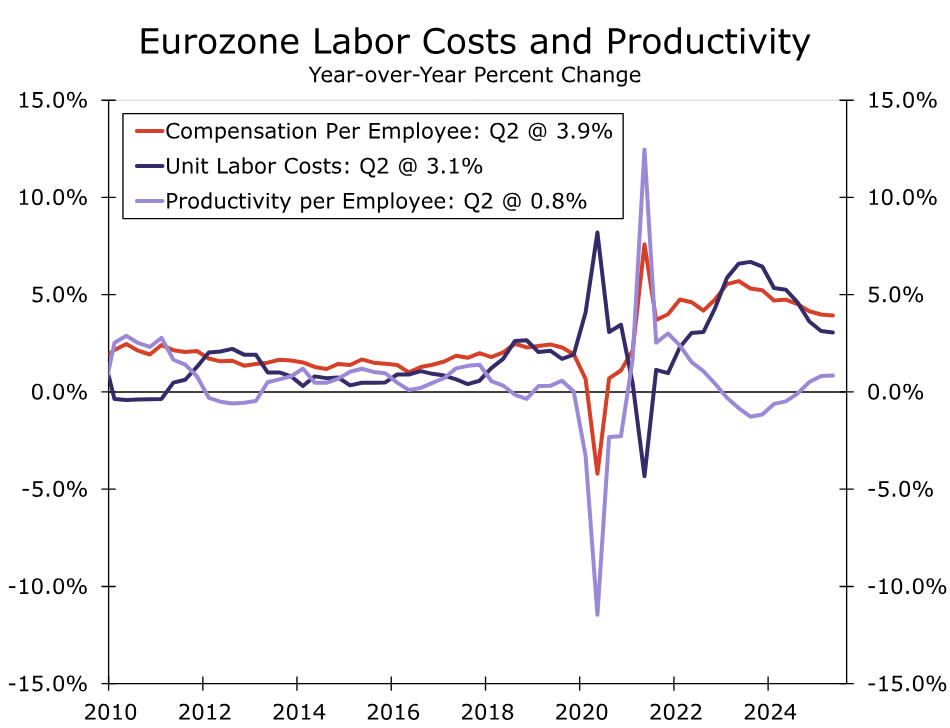

Finally, we still view wage and cost pressures as consistent with some further gradual disinflation in the quarters ahead. To be sure, wage indicators were somewhat mixed in the second quarter, as the ECB Indicator of Negotiated Wages quickened to 4.0% year-over-year, while the Q2 labor cost index also firmed to 3.7%. However, Q2 compensation per employee—the broadest wage measure—eased slightly further to 3.9%. Combined with a moderate improvement in labor productivity to 0.8% year-over-year in Q2, that has also contributed to a deceleration in unit labor cost growth to 3.1%. While the current level of unit labor cost growth remains mildly elevated, a further slowing in wages provides a clear path for unit labor cost growth and underlying inflation to both converge towards 2%, and possibly slightly below.

Overall, with the likelihood of slower economic growth ahead and in our view some potential for further disinflation to come, we lean toward the European Central Bank delivering a final 25 bps rate cut at its December meeting, to 1.75%. We think that benign CPI readings, especially core and services inflation, as well as a further slowing in wage growth, would be the most important contributors to further monetary policy easing. At the same time, wage and price indicators represent the main risk to our call for another ECB rate cut. Should wage growth, and/or core and services inflation fail to slow perceptibly in the months ahead, ECB policymakers may be more comfortable holding the Deposit Rate at the current 2.00% level for an extended period.

ECB Review – Confident Despite Inflation Below Target in 2027

- ECB decided to leave the policy rate unchanged at 2.00% at today's meeting as fully expected by both markets and analyst.

- The staff projections featured a dovish twist as the inflation forecast for 2027 was lowered to 1.9% y/y (from 2.0% y/y) and core inflation to 1.8% (from 1.9%).

- Lagarde downplayed the revisions to inflation and said the growth outlook was balanced for the first time since September 2023 leading to an overall hawkish market reaction.

- We do not expect any policy rate changes from the ECB in 2025 or 2026.

As widely expected, the ECB decided to keep the policy rates unchanged at today's meeting, leaving the deposit rate at 2.00%. The most significant information from the meeting was the new staff projections that lowered the core inflation forecast for 2027 to 1.8% y/y (from 1.9%) and headline to 1.9% y/y (from 2.0%). The forecast for 2027 should be seen as "medium-term inflation" since it is mainly affected by monetary policy and not temporary factors such as swings in global commodity prices. Following an initial dovish market reaction to the new projections, Lagarde struck a hawkish tone at the press conference, fully erasing the previous move. She downplayed the downward revision to the inflation forecast noting that this was primarily due to a stronger euro and that the deviation from 2% was minor. Moreover, the GC now sees the risks to the growth outlook as being balanced after having highlighted downside risks to growth since September 2023. In our view, this adds to the hawkish arguments for the ECB being on hold as they are more confident in the outlook. The risk of a final cut remains as the ECB could be surprised on the downside by data, particularly if domestic demand does not evolve as expected, although this is not our base case.

Otherwise, the staff projections showed a growth forecast that was revised up for 2025 to 1.2% y/y (from 0.9%) due to better-than-expected growth in the first half of the year while the expectation was unchanged for 2027. Core inflation was unchanged in 2025 and 2026 and headline slightly higher in 2025 at 2.1% (from 2.0%) due to previous inflation being higher than expected. Hence, the upward revision in 2025 was expected due to previous data while the downward inflation revision in 2027 came as a surprise. Lastly, the ECB repeated the previous guidance that the GC will "follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance".

We keep our call that the ECB will not make any policy rate changes in 2025 or 2026. With growth holding up better than expected core inflation above the 2% target due to sticky wage growth, and the outlook for fiscal easing in 2026 we do not expect the ECB to deliver a final cut in the coming six months, contrary to market expectations. At the same time, we believe hikes in 2026 are premature due to inflation most likely being below target by then and the German economy having sufficiently room to increase production without fuelling inflation.

A Hesistant FX Market After As-Expected September CPI Release

Forex currencies have been dormant since the beginning of August as Markets haven't found what they want in the latest key data reports.

As previously thought, the latest NFP, PPI, and CPI combo reports would have expected to relieve volatility in FX. But volatility there wasn't.

After receiving all the most influential market data, the next step will be next Wednesday's FOMC rate decision (September 17).

Prior to the CPI release, expectations for a 50 bps cut were priced at 10% and are now closer to 5%. The 25 bps cut, however, is still priced to be a sure thing.

Indeed, when looking at Market reactions in other assets, it seems that the theme that is developing is one of a less prolonged impact of tariffs.

Despite an as expected 0.3% report, participants bidding on Bonds and Gold point toward a repricing of lower long-run inflationary impact of tariffs (while they are just starting to bite now), which is flattening the US Yield curve.

Until now, pricing has been one of lower short-term inflation expectations versus higher ones in the long run.

Despite the immediate US Dollar selloff, FX currencies are hesitant and hang close to unchanged on the session.

Discover major currency pairs charts and levels, after first peaking at reactions to other asset classes.

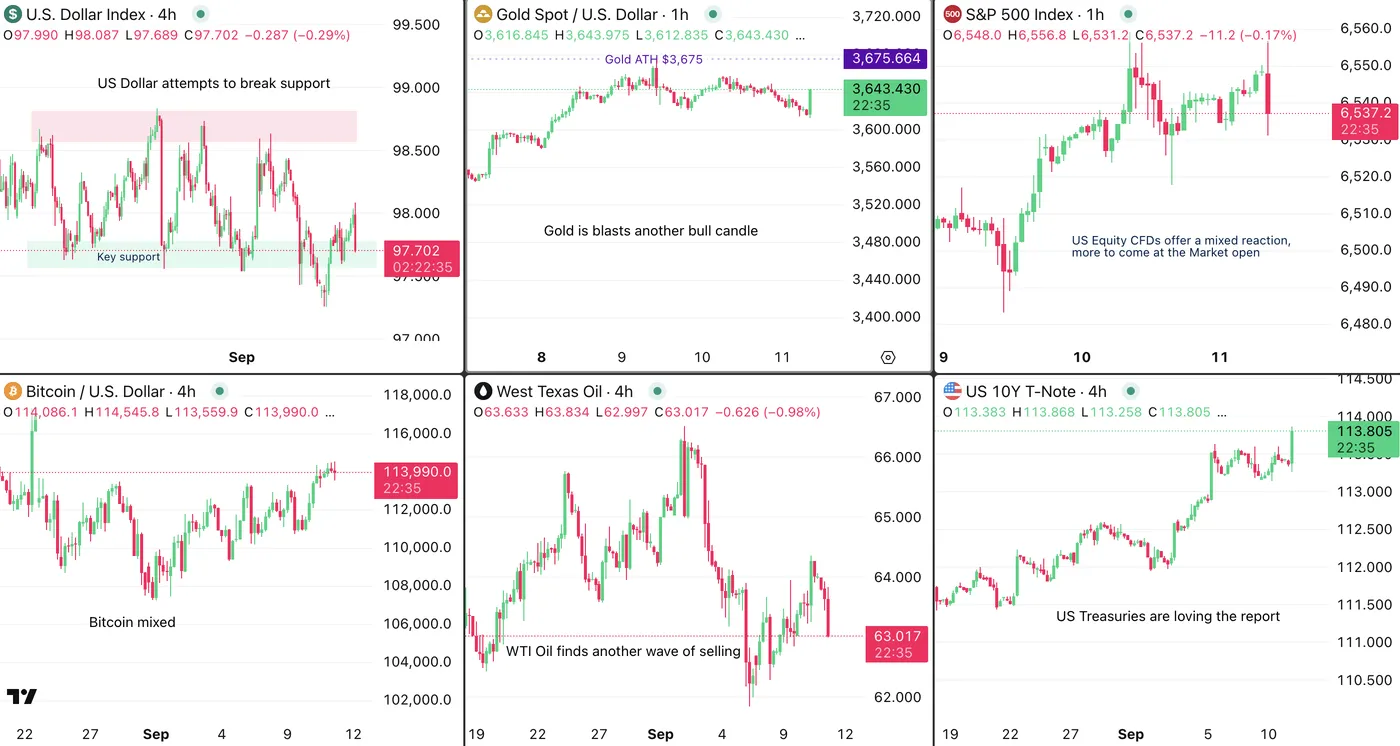

An overlook at cross-assets market reactions: Bonds and Gold are loving it, USD corrects.

Cross-Asset charts post-CPI – September 11, 2025 – Source: TradingView

All FX Majors Charts with the immediate key levels in play

Yen likes the report but still needs more – USDJPY

USDJPY 1H Chart, September 11, 2025, Source: TradingView

The most volatile FX pair is enjoying the ongoing selloff in the US Dollar but has yet to break out of its mid-range pivot zone.

Some ongoing selling might be pushing prices out of this region however this move still has to develop.

Wicky action at the extremes prove that participants are still hesitant on the upcoming direction for currencies.

A 25 bps confirming could still provide some strength to the USD which helps to explain why participants are still looking at each other to see who moves first

Levels to watch for USDJPY:

- Mid-range pivot 147.50 to 148.00 (currently trading – Look for breakouts of this zone)

- May Range Extremes 148.70 to 149.50 (Daily MA 200)

- 146.50 Main range Support

AUDUSD – pushing to retest yearly highs

AUDUSD 1H Chart, September 11, 2025, Source: TradingView

AUDUSD has rebounded significantly since its August 1st lows and by evolving in an intermediate upward channel, heads to retest its yesterday and 2025 highs (0.6535).

Some hesitation at the current levels is forming and will be essential to monitor.

Levels to watch for AUDUSD:

- 2025 Highs Resistance 0.6620 to 0.6650

- 0.6580 to 0.66 Pivot acting as mid-term support

- 0.6550 Pivot turned support and low of intermediate channel.

EURUSD – a wicky retest of its range resistance

EURUSD 2H Chart, September 11, 2025, Source: TradingView

EURUSD still evolves within its August range after a failed upside breakout in yesterday's session.

Buyers have pushed towards a retest of the resistance but seem to be running out of steam.

Levels to watch for EURUSD:

- PPI highs 1.17801

- 1.1750 Immediate Resistance

- Session lows and key range pivot 1.1660

- 1.16 Current main Support

USDCHF – Downfall stalling

USDCHF 2H Chart, September 11, 2025, Source: TradingView

The Swiss franc had strengthened immensely in the beginning of the month which pushed USDCHF towards a retest of its 2025 Main support (0.7916 week lows).

However, despite a selling candle from the data, hesitation comes at the 50-period MA which will also be key to upcoming action: A rejection of the MA could provide a boost to the pair, while a breakdown could also lead to further downside.

Levels to watch for USDCHF:

- 0.8050 Resistance

- 0.80 Immediate Pivot and 50-period MA (action stalling here)

- 0.79 Main Support (latest rebound)

- 2025 Lows 0.78730

GBPUSD – Liked the report, but hesitant at the highs

GBPUSD 2H Chart, September 11, 2025, Source: TradingView

GBPUSD has, like its European neighbor, been stuck in a 2,000 pip range since the middle of August (1.34 to 1.36).

The buying reaction to the CPI report is once again met with some hesitation as prices are meeting the range resistance.

Watch the immediate low-slope downward channel that may shape today's price action.

Levels to watch for GBPUSD:

- 1.36 Main channel Resistance

- Key 1.35 Pivot (daily lows, key for buy/sell momentum)

- 1.34 current Daily pivot (acted as Support)

USDCAD reject its mid-term upward channel

USDCAD 2H Chart, September 11, 2025, Source: TradingView

USDCAD is virtually unchanged after the report – By attaining the upper bound of its upward channel, mean-reversion selling seems to occur but real momentum has yet to materialize.

Levels to watch for USDCAD:

- Immediate resistance at Aug Highs 1.38750

- 1.38 Major resistance turned Pivot

- 1.3740 Support

Safe Trades!

Sunset Market Commentary

Markets

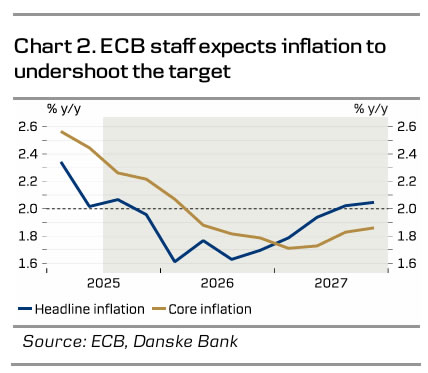

The European Central Bank in a move widely expected kept the policy rate unchanged at 2%. The second no-change outcome straight was unanimous and results from the ECB observing that inflation is currently around the 2% medium target. With the updated forecasts showing inflation to stay there over the policy horizon, there was no need to adjust rates. The ECB penciled in 2.1%-1.7%-1.9% over the 2025-2027 period, to be compared with 2%-1.6%-2% in June. Core inflation expectations stayed pretty much the same as well. Growth for this year was bumped to 1.2% from 0.9%. The first quarter enjoyed a boost from (export) frontloading while domestic consumption remained resilient so far. Current headwinds from a stronger euro, import tariffs and increased competition should fade in 2026. Growth for that year was revised slightly downward to 1% while that for 2027 was kept unchanged at 1.3%. Lagarde noted that risks to growth have become more balanced, an important shift from July when “risks remained tilted to the downside”. Lagarde’s response to the first question in the press conference, whether the easing cycle is over, immediately struck a nerve: “Let me tell you this … the disinflation process is over.” Everything she said afterwards (we’re data dependent, go meeting by meeting …) in the rest of her answer and by extension of the presser can and was easily ignored. Lagarde de facto buried any remaining doubts whether the central bank will lower rates again, barring major shocks. Combined with the upgraded growth risk balance it hurled short-term European rates to intraday highs, leading to net daily changes varying between +1.6 (30-yr) to +4.8 bps (5-yr). The 2-yr swap yield rises to a 5-month high, the German equivalent is on the verge of topping 2%.

In between the statement release and the presser, the US published in-line with consensus August CPI numbers but well-above-consensus jobless claims. The former printed 0.4% on a headline basis, slightly more than the 0.3% expected. The yearly figure matched the anticipated rise to 2.9%. Core CPI came in at 0.3% and 3.1% (same as in July). The core goods excluding new and used vehicles, considered sensitive to tariff-related inflationary pressures, was only up 0.13% m/m, the weakest reading since March and a further deceleration from July’s 0.22%. Other closely watched import-exposed categories such as video & audio products, apparel and household furnishings all showed either a contained price increase, a smaller one than the month before or both. Services inflation added a July-matching 0.3% m/m whereas some feared this category would come in hot. The numbers came together with a significant uptick in jobless claims to 263k, the highest since late 2021 when the numbers were still normalizing from the Covid spike. It’s seen as evidence of a weakening labour market and boosted Fed rate cut expectations. Three 25 bps cuts are now fully priced in for this year with some adding to bets for a 50 bps move next week. The ECB and US data help give the euro the upper hand over the dollar, though given the yield differentials gains could have been larger. EUR/USD bounces of an upward sloping trend line towards 1.172. The 1.1829 July multiyear remains out of reach so far.

News & Views

The Norges Bank today published its Q3 Regional Network report, important input for its policy meeting Thursday next week. According to the report, full capacity utilization (at 35%) was little changed from the previous surveys. Overall, contacts expect output growth to remain fairly stable in the period between Q3 2025 (0.4%) and Q4 2025 (0.4%) Many expect higher household purchasing power to strengthen demand. Some contacts expect growth in residential construction to boost activity. A number of contacts point out that there is still uncertainty related to international trade barriers and some cite greater customer caution. Contacts expect somewhat higher investment in 2025 (1.1% from -0.9% previously) than in 2024 and growth to remain firm in 2026 (1.6%). At 25%, contacts reporting recruitment difficulties rose slightly. They also see further employment growth both in Q3 and Q4 (0.2%). Wage growth is estimated at 4.5% this year and 4% next year. Combined with higher than expected August (core) CPI data published yesterday, the survey outcome poses questions whether the NB will already reduce the policy rate further next week. The Norwegian krone strengths modestly further today (EUR/NOK 11.615).

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.20; (P) 147.42; (R1) 147.69; More...

Intraday bias in USD/JPY remains neutral for the moment. Risk will stay on the upside as long as 149.12 resistance holds. Firm break of 146.20 will target 100% projection of 150.90 to 146.20 from 149.12 at 144.42. Also, sustained trading below 55 D EMA (now at 147.16) will argue that whole rebound from 139.87 has completed with three waves up to 150.90.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

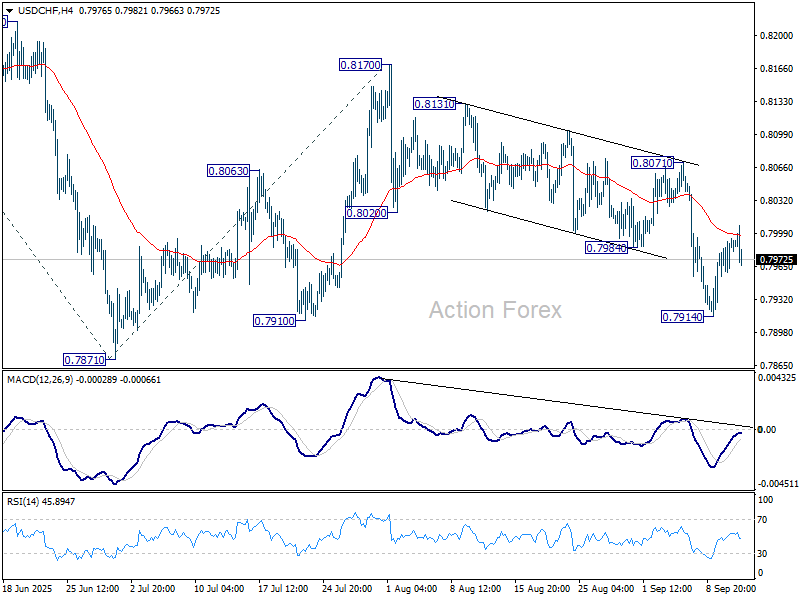

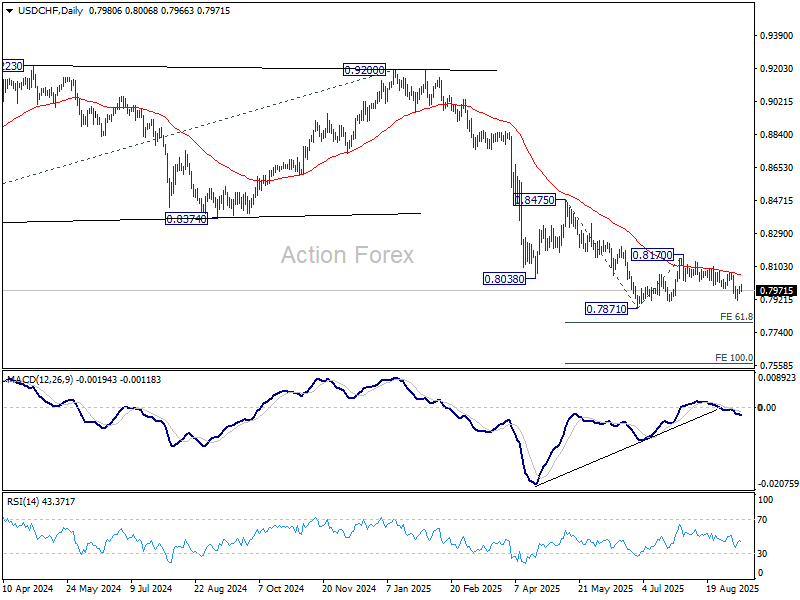

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7970; (P) 0.7982; (R1) 0.8006; More….

USD/CHF is staying in consolidations above 0.7914 temporary low and intraday bias remains neutral. Risk will stay on the downside as long as 0.8071 resistance holds. Below 0.7914 will bring retest of 0.7871 low. Firm break there will resume larger down trend. Next target is 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

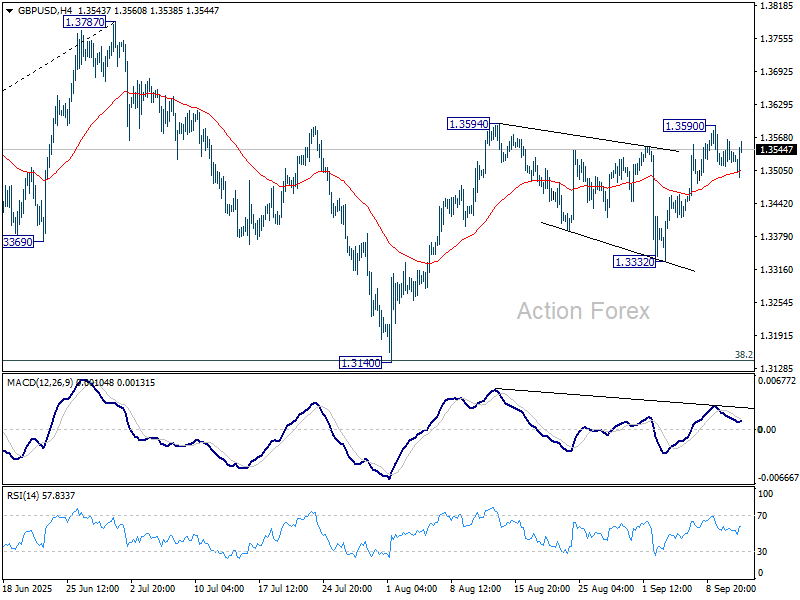

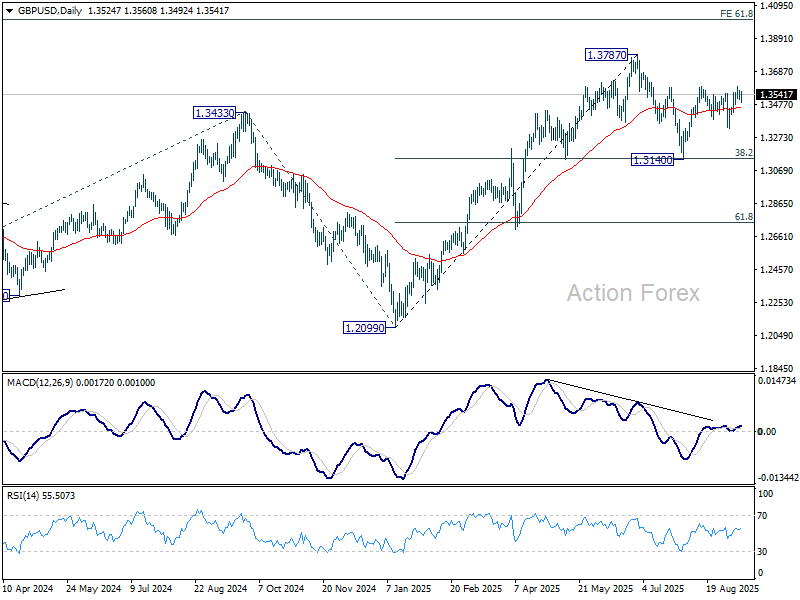

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3508; (P) 1.3534; (R1) 1.3556; More...

GBP/USD is staying in consolidations below 1.3590 temporary top and intraday bias stays neutral. Further rise is expected with 1.3332 support intact. Firm break of 1.3594 will resume the rally from 1.3140 and target a retest on 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3132) holds, even in case of deep pullback.

US: Inflationary Pressures Show Further Signs of Heating Up in August

The Consumer Price Index (CPI) rose 0.4% month-on-month (m/m) in August, a tick ahead of the consensus forecast in Bloomberg and up from the 0.2% m/m gain in July. On a twelve-month basis, CPI was up 2.9% (from 2.7% the month prior).

- Energy costs (+0.7% m/m) turned higher last month, while food prices (+0.5% m/m) also firmed due to higher grocery costs (+0.6% m/m). Price growth for 'food away from home' was up 0.3%m/m - unchanged from July.

Excluding food and energy, core inflation rose 0.3% m/m (0.35% m/m unrounded), largely matching last month's gain and meeting the consensus forecast. The twelve-month change held steady at 3.1%.

Price growth of services continued to come in on the hotter side, rising 0.35% m/m, following a similar gain of 0.36% m/m in July. Primary shelter costs rose at its fastest monthly clip in several months, while price growth of non-housing services (+0.4% m/m) remained firm for a second consecutive month.

- Higher travel costs (+3.0% m/m) were a big driver of price growth in non-housing services, thanks to a sharp uptick in airfares (+5.9% m/m) and hotels (+2.3% m/m).

Tariff passthrough continued to materialize in core goods prices, which were up 0.3% m/m or its fastest monthly gain since January. Price gains were most notable in apparel (+0.5% m/m), appliances (+0.5% m/m), household furniture and bedding (+0.4% m/m) and new vehicle prices (+0.3% m/m). Used vehicle prices also rose 1.0% m/m, which could in part be driven by consumer switching to used models in an effort avoid paying tariff costs.

Key Implications

Inflationary pressures continued to heat up in August, with broad strength in goods and services inflation. Goods prices are likely to continue to drift higher over the coming months as businesses increasingly pass-on more of the tariff costs. However, further upward pressure on services inflation looks limited against the backdrop of a cooling labor market which is likely to limit upward pressure on wage growth and keep a lid on discretionary services spending.

But nothing is a guarantee, and policymakers will need to balance the risks of reducing the policy rate by enough to breathe some life back into the labor market, but not by so much that they risk unnecessarily stoking inflation. We see the Fed delivering on three quarter-point cuts by year-end, with the first coming at next week's meeting. We've long held this view, and following this morning's release, Fed futures are pricing in a similar rate-cut path by year-end.

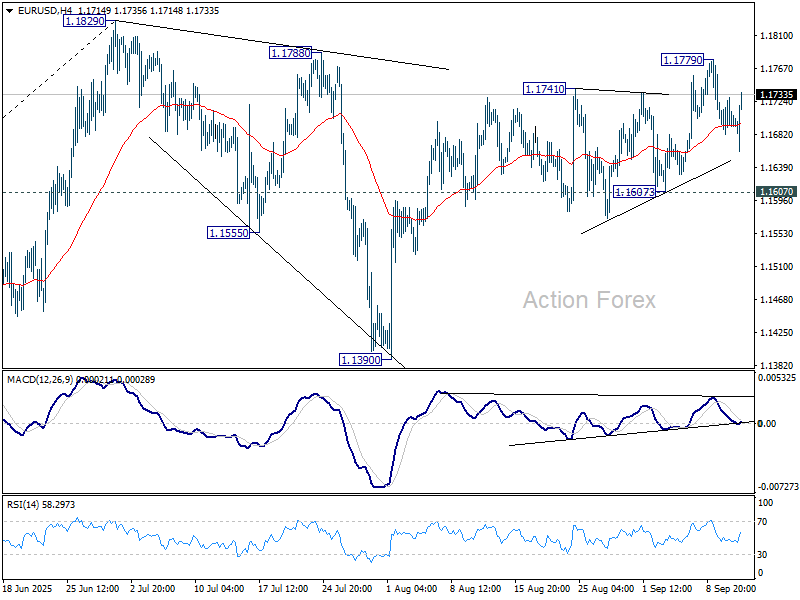

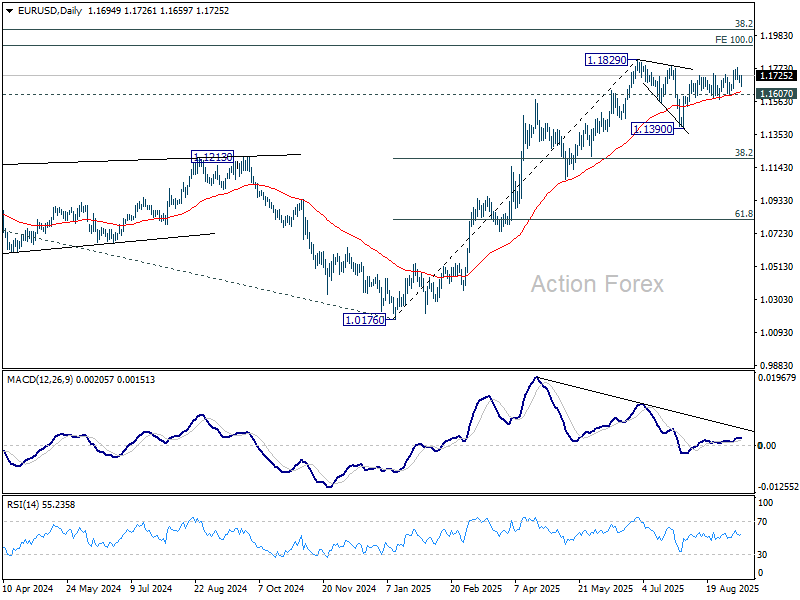

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1674; (P) 1.1703; (R1) 1.1722; More...

EUR/USD is staying in range below 1.1779 temporary top despite today's volatility. Intraday bias remains neutral for the moment. Further rise is expected with 1.1607 support intact. Above 1.1779 will bring retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

ECB and US CPI Underwhelm, Jobless Claims Take Spotlight

Today’s high-profile events turned out to be something of a letdown for traders. Euro dipped after the ECB held its deposit rate steady at 2.00% and published new staff projections, but the move was shallow and short-lived. Markets took note that both headline and core inflation are now projected slightly below the 2% target by 2026 and 2027, hinting at a possible need for further easing down the road.

For now, however, there is no urgency for additional cuts. ECB reiterated the Governing Council’s commitment to a data-dependent stance, and unless incoming figures deteriorate notably, traders see little chance of a near-term move. That kept the euro relatively stable after its initial dip.

In the U.S., CPI data were broadly in line with expectations. Headline inflation’s 0.4% monthly rise was a touch stronger than forecast, but the annual rate of 2.9% and steady core at 3.1% highlights that inflation is not worsening much under tariff pressures.

The bigger surprise came from the weekly jobless claims report. Initial claims jumped to 263k, the highest since 2021, showing a clear softening in the U.S. labor market. With employment one half of the Fed’s dual mandate, the data reinforced expectations that policymakers will have to expedite easing to cushion the economy.

Market pricing for next week’s FOMC remains anchored to a 25bps cut, with odds for a larger 50bps move still low at about 10%. But expectations for a consecutive cut in October have surged to around 95%, showing traders are becoming more convinced of back-to-back easing.

Despite the data, currency markets remain locked in yesterday's ranges. Swiss Franc, Euro, and Sterling are modestly firmer, while Yen and Loonie are weaker alongside Kiwi. Dollar and Aussie sit in the middle of the pack. For now, the highly anticipated breakout in FX markets has yet to materialize.

In Europe, at the time of writing, FTSE is up 0.37%. DAX is up 0.08%. CAC is up 0.67%. UK 10-year yield is down -0.008 at 4.625. Germany 10-year yield is down -0.006 at 2.650. Earlier in Asia, Nikkei rose 1.22%. Hong Kong HSI fell -0.43%. China Shanghai SSE rose 1.65%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield rose 0.01 to 1.578.

US CPI rises to 2.9% in August, core CPI unchanged at 3.1%

U.S. consumer prices rose more than expected on the month in August, with CPI up 0.4% mom versus forecasts of 0.3% mom. Core CPI rose 0.3% mom, matching expectations. Shelter costs climbed 0.4% mom and were the largest contributor to the monthly increase, while food prices rose 0.5% mom and energy gained 0.7% mom.

On a year-over-year basis, headline CPI accelerated to 2.9% from 2.7% in July, in line with forecasts. Core inflation held steady at 3.1%, also as expected. The data show underlying price pressures remain stable even as headline measures edge higher. Food inflation rose 3.2% over the past year, while energy prices were up a modest 0.2%. Overall, the report points to steady but not accelerating inflation.

US initial jobless claims spike to 263k, highest since 2021

U.S. initial jobless claims surged by 27k to 263k in the week ending September 6, well above expectations of 240k and marking the highest level since October 2021. The four-week moving average rose 10k to 241k, pointing to a clear softening trend in labor market conditions.

Continuing claims were steady at 1.939 million for the week ending August 30, with the four-week average slipping slightly to 1.936 million. Still, the rise in new claims highlights a labor market that is starting to cool more decisively, adding pressure on the Fed as it weighs the pace of policy easing.

ECB holds at 2.00% Again, upgrades 2025 growth outlook

The ECB left its deposit rate unchanged at 2.00% as widely expected, marking a second consecutive hold. The Governing Council reiterated its commitment to stabilizing inflation at 2% over the medium term and stressed a "data-dependent and meeting-by-meeting" approach. Policymakers emphasized they are "not pre-committing to a particular rate path", leaving flexibility to respond to incoming data.

Fresh staff projections showed little change from June, with headline inflation expected to average 2.1% (prior 2.0%) in 2025, 1.7% (1.6) in 2026, and 1.9% (2.0%) in 2027.

Core inflation, excluding food and energy, is projected at 2.4% in 2025 before easing to 1.9% in 2026 and 1.8% in 2027. The figures reinforce the view that price pressures are gradually converging toward target.

On growth, the ECB revised up its 2025 forecast to 1.2% from 0.9%, but cut its 2026 estimate slightly to 1.0% (prior 1.1%). The 2027 projection was left unchanged at 1.3%.

Japan CGPI accelerates to 2.7% yoy, import price declines ease

Japan’s producer prices rose modestly in August, with CGPI climbing 2.7% yoy from 2.5% yoy in July, matching market forecasts. The pickup was driven mainly by food and beverage costs, which rose 5.0% yoy versus 4.7% yoy previously. In contrast, utility bills fell -2.9% yoy due to government subsidies, softening the overall inflation impact.

Import price declines eased significantly in the past two months, with yen-based import prices down -3.9% yoy compared with a revised -10.3% fall in July. The data suggest external cost pressures are stabilizing, even as domestic food inflation remains sticky.

RBNZ’s Hawkesby: OCR seen at 2.5% by year-end, data dependent

RBNZ Governor Christian Hawkesby said today the central bank still projects the Official Cash Rate to fall to around 2.50% by year-end, down from current 3.00%. Though, the pace could be "faster or slower" depending on incoming data. He emphasized that the path of policy easing will hinge on the "speed of New Zealand’s economic recovery".

Hawkesby noted the August Monetary Policy Statement highlighted the sharp blow to household and business confidence, with the economy stalling mid-year and creating more slack. He attributed much of the “confidence shock” to uncertainty over U.S. tariff policies, compounded by cost-of-living pressures and a weak housing market.

Still, leading indicators for July were “better” and aligned with the RBNZ’s outlook for a rebound in the second half of the year. Hawkesby said policymakers will keep monitoring spillovers from U.S. tariffs on both global growth and New Zealand firms. The RBNZ resumed rate cuts last month after a July pause.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1674; (P) 1.1703; (R1) 1.1722; More...

EUR/USD is staying in range below 1.1779 temporary top despite today's volatility. Intraday bias remains neutral for the moment. Further rise is expected with 1.1607 support intact. Above 1.1779 will bring retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.