Sample Category Title

ECB officials stress uncertainty, keep options open after rate hold

Several ECB policymakers weighed in after the Governing Council held deposit rate steady at 2.00% yesterday.

Latvian member Martins Kazaks argued the central bank should not provide forward guidance given high geopolitical and economic uncertainty. He said December’s meeting will be crucial, as new staff forecasts will help determine whether inflation is deviating from target in a significant or persistent way.

Kazaks also flagged external factors, including the Euro’s strength— which can suppress import prices— and potentially deflationary Chinese exports as downside risks. “Uncertainty is high,” he said, adding this justifies a cautious, meeting-by-meeting policy stance.

Olli Rehn of Finland struck a similar note, warning about the disinflationary impact of cheaper energy and a stronger currency. He stressed the importance of avoiding inflation moving “too much below or too much above” the 2% objective,.

France’s Francois Villeroy de Galhau left the door open to further easing, saying “another rate cut is entirely possible” in coming meetings.

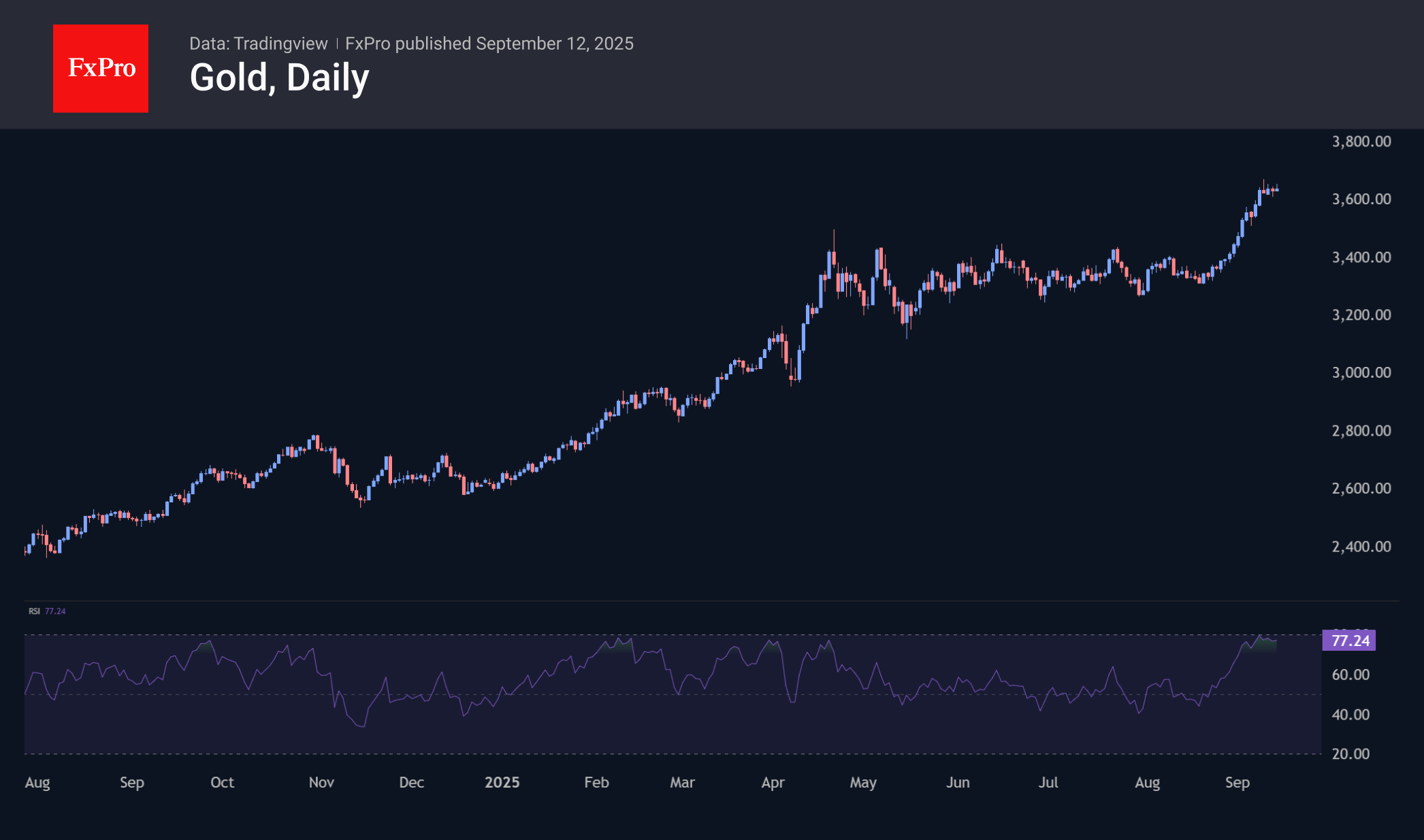

Gold Vulnerable to Sell-the-Fact Pattern Next Week

Gold reacts strongly to geopolitics and has reached another record high, rising for the fourth week in a row. Washington is ready to wage economic war on the Kremlin’s main allies, India and China, if Brussels supports it. As a result, there is an increased risk that central banks will step up their gold purchases as part of their reserve diversification and de-dollarisation processes.

Geopolitics has made the precious metal less sensitive to the Fed’s monetary policy. Even the resurgent US dollar has been unable to put a spoke in gold’s wheel. Neither could the White House’s announcement that it would exclude this asset from the list of potential tariffs.

If Donald Trump manages to drive a wedge between Russia, India, and China, oil prices will rise, and inflation will accelerate. A stagflationary environment and increased central bank purchases of bullion will help gold.

However, in the short term, we note technical overbought conditions after an impressive rise. This was reflected in the stabilisation of prices from Tuesday to Friday, contrary to the continued growth of silver and other precious metals and new highs in stock indices. In daily timeframes, the RSI gradually declines after touching the zone above 80. In 10 out of 11 cases over the past six years, such a signal has been followed by corrective pullbacks, which may well happen again this time.

The expected cut in the key rate on Wednesday risks triggering a “buy the rumours, sell the fact” pattern.

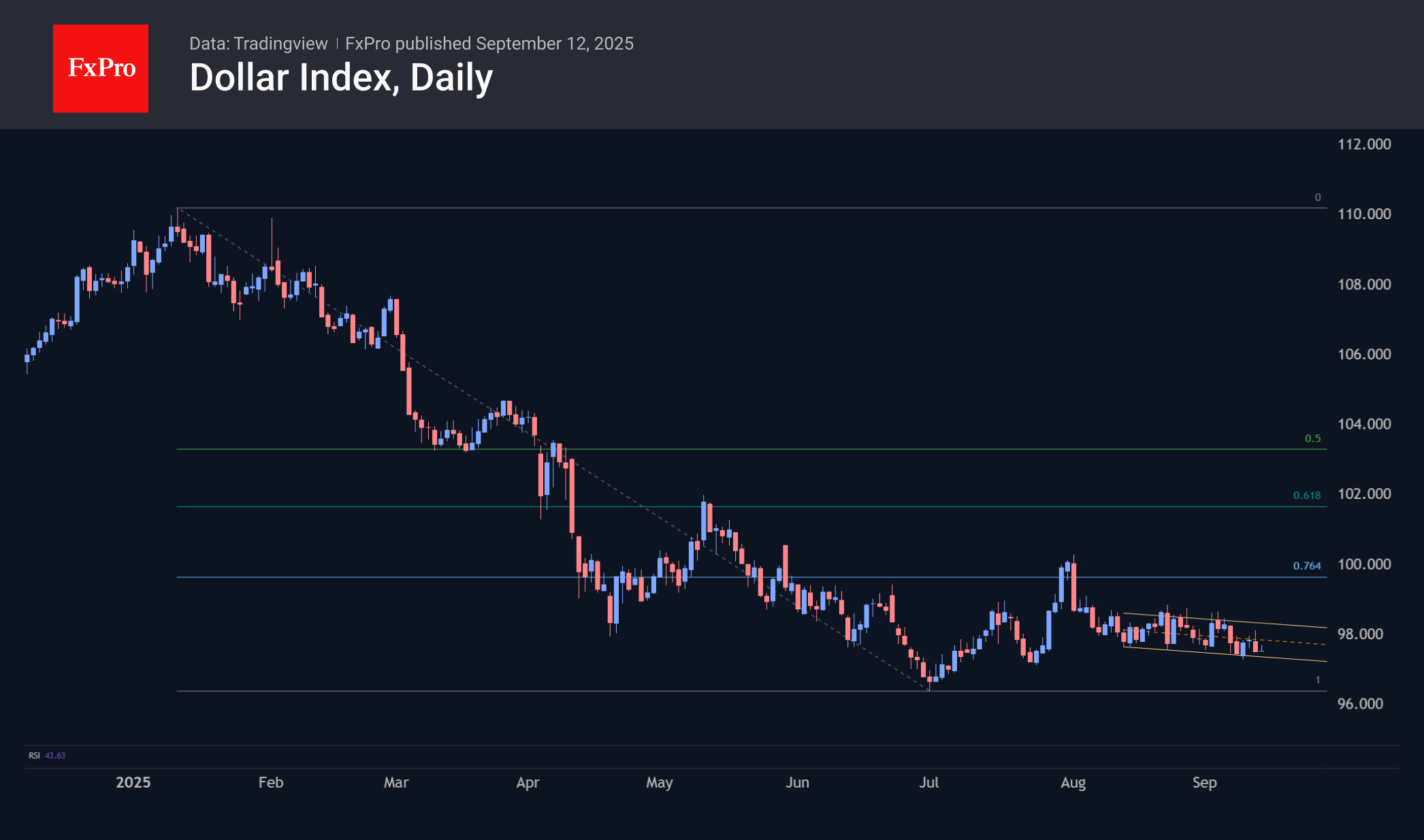

Dollar Needs a Global Shock to Revive

Political crises in France and Japan have undermined the strength of the US dollar’s main competitors, the euro and the yen. The resignations of the French and Japanese prime ministers and Paris’s move towards parliamentary elections are temporarily allowing the dollar to forget about monetary policy. The chances of further steps to ease Fed policy are growing rapidly after a record revision of employment data for the year in March, which took 911K jobs off previous estimates, and an unexpected decline in producer price indices for August.

A federal court ruling allowing Fed member Lisa Cook to attend the September FOMC meeting is helping the US currency. Donald Trump wants to weaken the US dollar, so any failure by the president serves as a signal to buy the US currency. This includes as part of the strategy of trading the Fed’s independence.

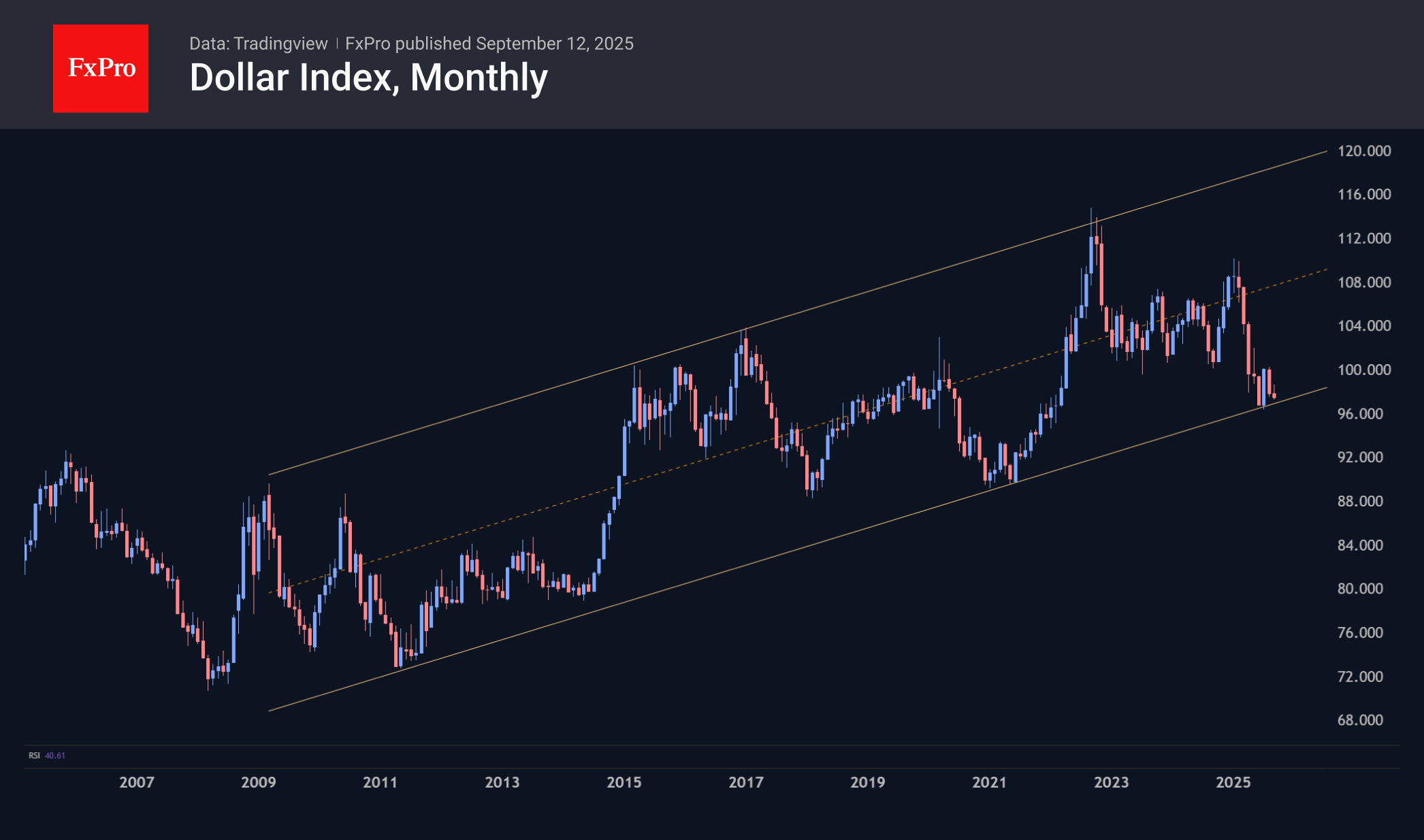

The dollar index has barely moved from the narrow range of 97-98 over the past five weeks. This tug-of-war replaced the six-month downtrend and the subsequent attempt to rebound in July. In this case, the sideways movement is a bearish signal. In the medium term, the current dynamics may turn out to be a corrective rebound, and its insignificant swing, not even reaching the typical 76.4% of the initial decline, is an indication of the strength of sellers. At the same time, the dollar found itself at the support level of the 13-year uptrend line, and even remaining at the same level leads to a fall below this line.

Given the growing expectations that the Fed will conduct a series of 4-5 rate cuts, while other central banks are not expected to follow suit, we have fundamental grounds for the dollar to resume its decline at the beginning of the new financial year.

During periods of global expansion, the US currency is under pressure due to increased demand for risky, higher-yielding assets outside of US government bonds. In similar conditions in the past, unexpected and sudden problems have saved America, including the dollar and government bonds, from a self-sustaining spiral of selling.

These included the more severe consequences for economies outside the US in response to the 2008-2009 financial crisis and the 2010-2011 sovereign debt crisis in Europe, which had repercussions for many years. Later, in 2018, the dollar gained on trade wars and in 2021 on the Fed’s ability to raise rates aggressively.

All these cases have in common the rush to the dollar during periods of acute crisis. Such a crisis would play into the hands of the US government, allowing it not only to legitimise rate cuts but also to simultaneously reduce the cost of borrowing by increasing demand for it.

AUD/USD Technical: Bullish Breakout Above 0.6700 Major Resistance After Minor Pull-back as US Consumer Sentiment Looms

The price actions of the AUD/USD have indeed jumped as expected; it rallied by 1.2% to record an intraday high of 0.6690 on Friday, 12 September, Asia session at the time of writing, and hit the lower limit of the 0.6660/0.6680 major resistance zone mentioned in our publication.

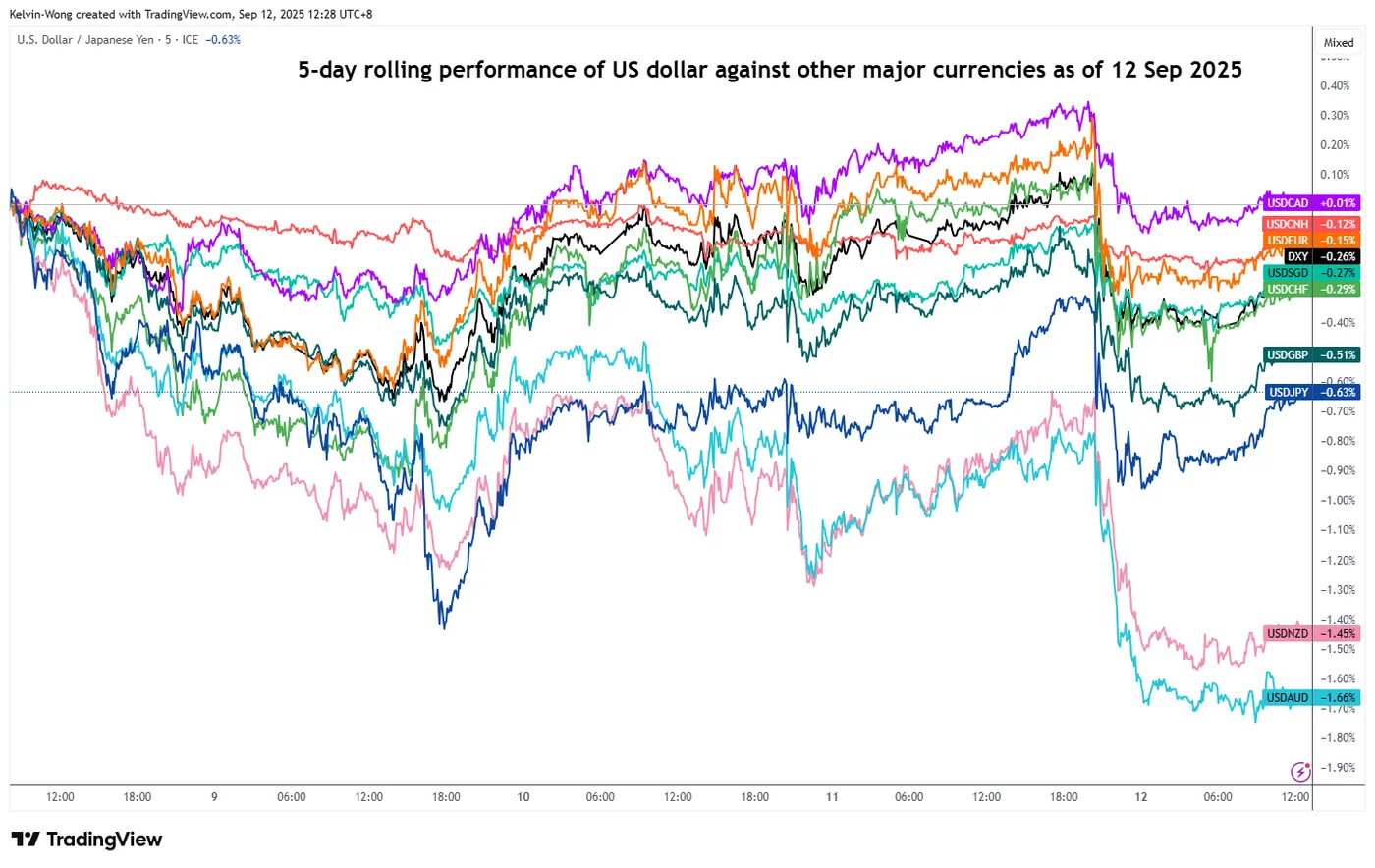

Fig. 1: 5-day rolling performances of major currencies versus the US dollar as of 12 Sep 2025 (Source: TradingView)

Based on the 5-day rolling performances of the US dollar against the major currencies as of Friday, 12 September, the Australian dollar is the strongest performing currency, where the US dollar shed -1.67% against the AUD, a larger magnitude than the loss of -0.3% seen in the US Dollar Index over the same period (see Fig. 1).

What’s next? Let’s break down for you the key fundamental factors and technical elements that are likely to drive forward the movement of the AUD/USD in the near to medium-term time horizon.

Further demand-side weakness in the US economy

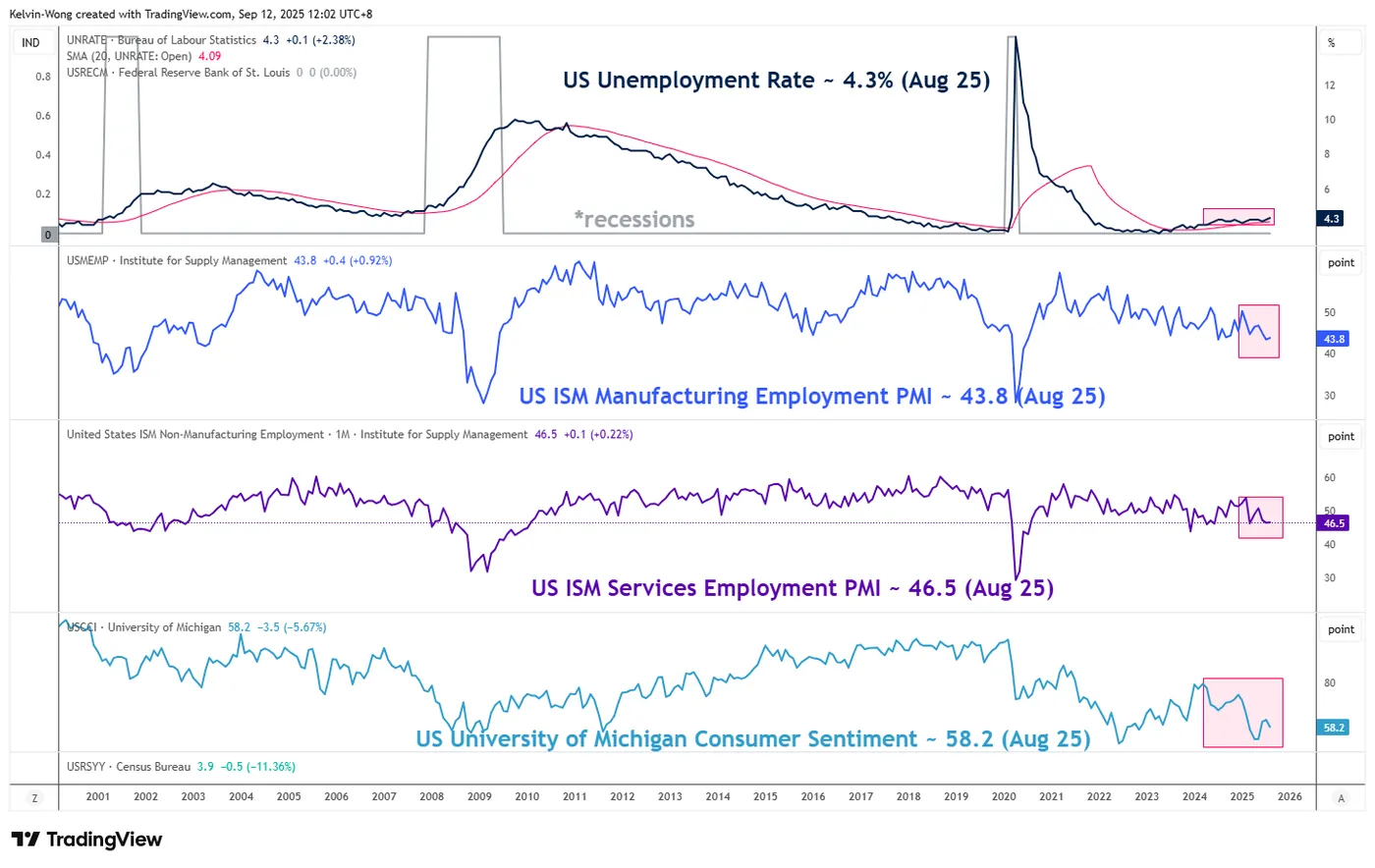

Fig. 2: US Unemployment Rate, ISM Manufacturing/Services Employment & University of Michigan Consumer Sentiment as of Aug 2025 (Source: TradingView)

The rally seen in the Australian dollar in the past two weeks has been more attributed to external economic forces (the US and China).

On the US side of the equation, more evidence that the deterioration of the US labour market (weaker-than-expected non-farm payrolls data for August, unemployment rose to almost a 4-year high of 4.3%, and initial jobless claims for the week ending 6 September increased to 263,000, the highest level since October 2021).

All these latest lackluster US labour market data outweigh the risk of a sticky inflationary trend in the US due to the US White House’s trade tariffs, which have triggered the pricing of a more pronounced Fed dovish pivot that is likely to kickstart next week at the FOMC meeting on 17 September.

Today at 14:00 GMT, the preliminary September reading of the University of Michigan’s consumer sentiment index will be released, a key leading indicator of US demand-side conditions.

According to the Trading Economics website, market forecasts are at 58, a slight dip from August’s print of 58.2.

The major trend of the University of Michigan’s US consumer sentiment has been deteriorating since March 2024’s print of 79/4, and if September’s print is below expectations (below 58), it is likely to trigger higher odds of Fed’s rate cuts bets in 2026, and asserts further downside pressure on the US dollar, in turn, boosting indirect demand for AUD (see Fig. 2).

Higher Iron Ore futures prices trigger a positive feedback loop back into AUD/USD

Fig. 3: Iron Ore CFR China futures with AUD/USD as of 12 Sep 2025 (Source: TradingView)

In our previous publication, we highlighted that the latest core CPI inflation trend in China has reduced the risk of an entrenched deflationary risk spiral.

It will have a trickle-down positive impact on the demand for iron ore, which is one of Australia’s key exports to China.

The forward-looking demand for iron ore can be gauged by examining the trends of the iron ore futures, which have a direct correlation with the movement of the AUD/USD (see Fig. 3).

Recent price actions of the Iron Ore CFR China futures listed on the Singapore Exchange have started to form a major bullish basing formation since September 2024 and traded back up above its 200-day moving average since the week of 4 August 2025.

A further move up in the Iron Ore CFR China futures and a break above 113.75 is likely to trigger a major positive feedback loop back into the AUD/USD (see Fig. 3).

Let’s now dive deeper into the technical analysis aspects of AUD/USD and determine its next near-term trajectory (1 to 3 days), key levels to watch, and key technical elements.

Fig. 4: AUD/USD minor trend as of 12 Sep 2025 (Source: TradingView)

Fig. 5: AUD/USD medium-term & major trends as of 12 Sep 2025 (Source: TradingView)

Preferred trend bias (1-3 days)

The minor bullish trend of AUD/USD from the 4 September 2025 low remains intact, but a risk of a minor pullback first before a potential new impulsive up move sequence materializes.

Maintain bullish bias with an adjusted short-term pivotal support at 0.6620 to contain the potential minor pull-back, and a clearance above 0.6700 adds impetus for the next intermediate resistance to come in at 0.6760 (also a Fibonacci extension) in the first step (see Fig. 4).

Key technical elements

- The major resistance of the AUD/USD stands at 0.6660/0.6700, which is defined by the upper boundary of the medium-term “Expanding Wedge” range configuration and the long-term secular descending trendline from the 25 February 2021 high (see Fig. 5).

- The daily RSI momentum indicator of the AUD/USD has continued to trend higher after its bullish breakout on 5 September 2025 and has not reached its overbought region (above 70). These observations suggest a potential bullish signal for the AUD/USD to break above 0.6700 (see Fig. 5).

- The yield spread between Australia’s 2-year sovereign bond and the US Treasury note has steadily narrowed from -0.55% on 1 August 2025 to -0.19% at the time of writing. This recent breakout above a 5-day descending resistance reinforces the bullish momentum in AUD/USD (see Fig. 4).

Alternative trend bias (1 to 3 days)

A break below 0.6620 key short-term support negates the bullish scenario on the AUD/USD to expose the next intermediate supports at 0.6580 and 0.6550.

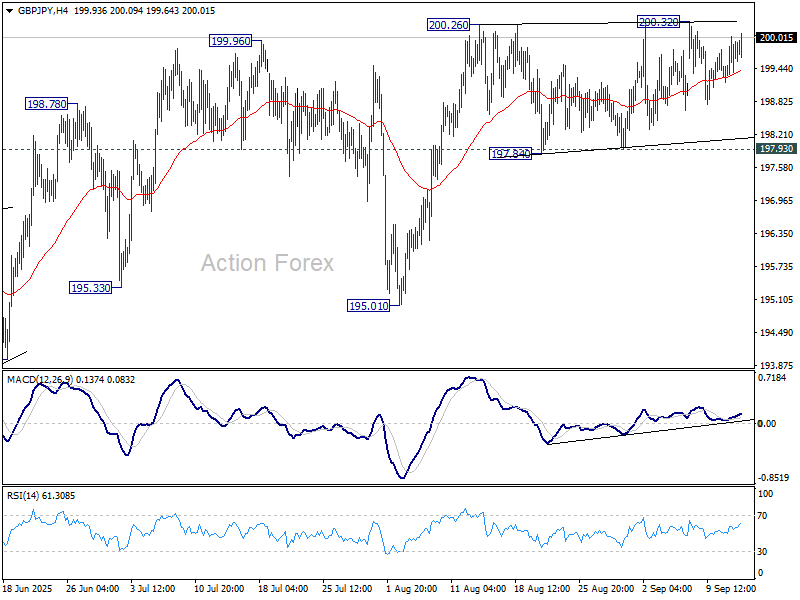

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.30; (P) 199.68; (R1) 200.21; More...

Range trading continues in GBP/JPY and intraday bias stays neutral. Further rise is expected as long as 197.93 support holds. Firm break of 200.26 resistance will resume the rally from 184.35 to 100% projection of 180.00 to 199.79 from 184.35 at 204.14. On the downside, however, break of 197.93 support will turn bias to the downside for 195.01 support next.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

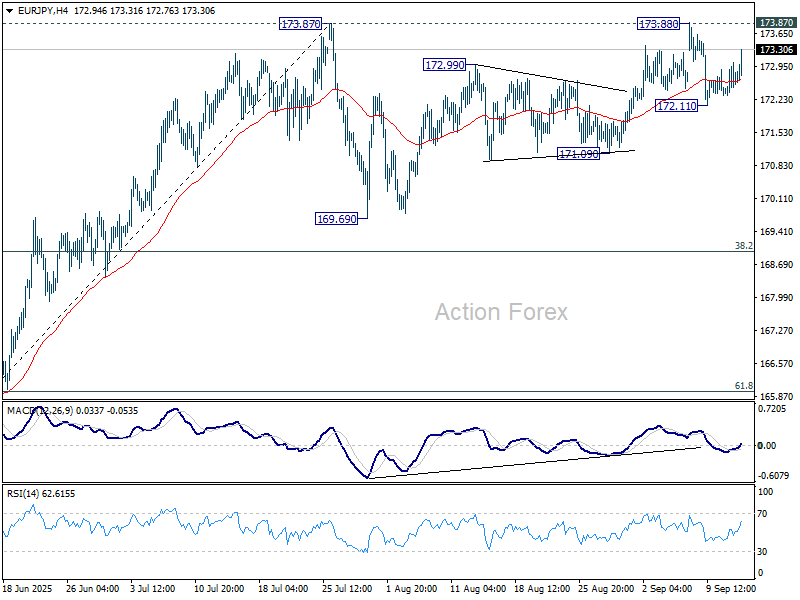

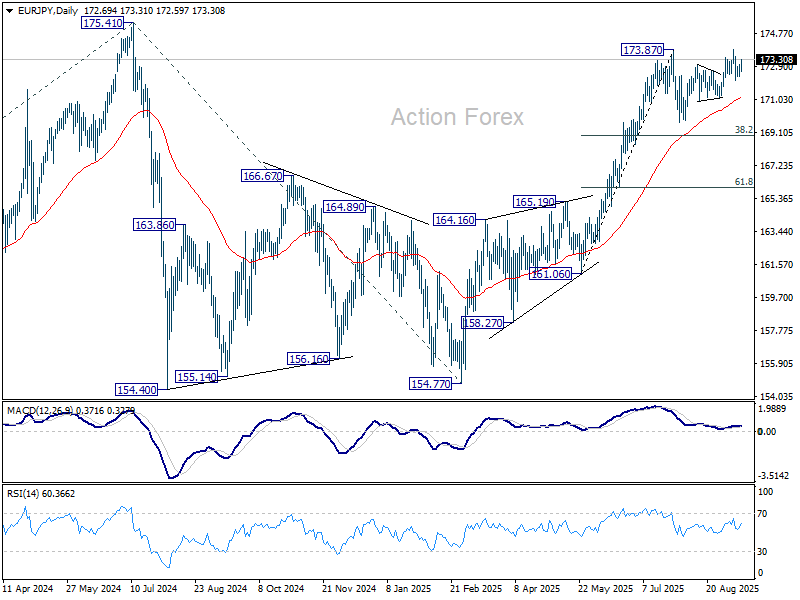

EUR/JPY Daily Outlook

Daily Pivots: (S1) 172.31; (P) 172.69; (R1) 173.17; More...

Intraday bias in EUR/JPY is turned neutral first will current recovery. On the upside, decisive break of 173.87/8 will resume larger rise from 154.77 to retest 175.41 high. On the downside, break of 172.11 will extend the corrective pattern from 173.87 with another leg, and target 171.09 support and below.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, sustained break of 38.2% retracement of 161.06 to 173.87 at 168.97 will delay this bullish case, and probably extend the correction from 175.41 with another fall.

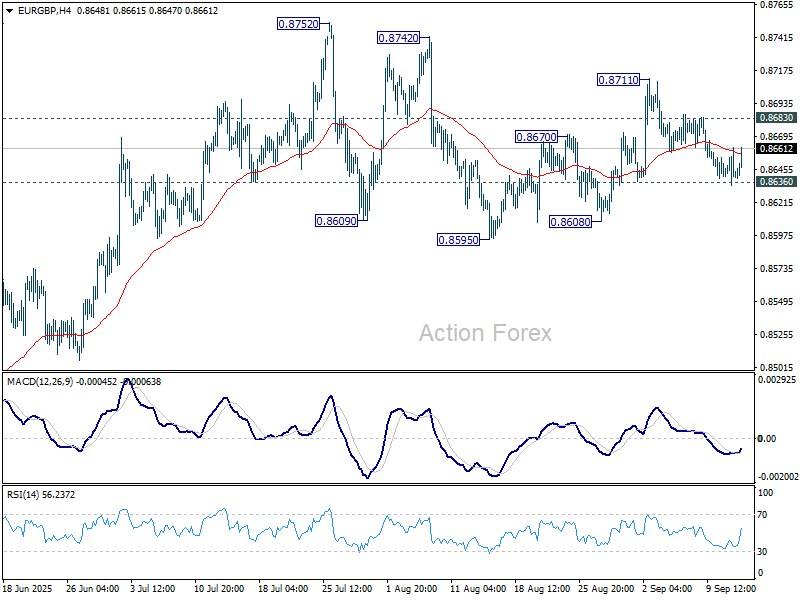

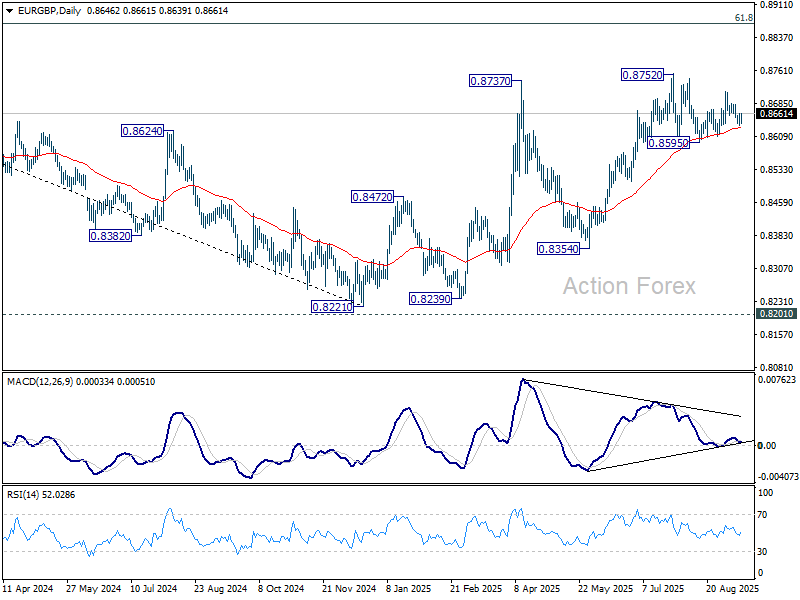

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8634; (P) 0.8648; (R1) 0.8661; More...

Intraday bias in EUR/GBP remains neutral for the moment. As long as 0.8636 minor support holds, further rise is still in favor. Above 0.8683 resistance will turn bias to the upside for 0.8711. Break there will bring retest of 0.8752 high. However, firm break of 0.8636 will extend the pattern from 0.88752 with another falling leg, and target 0.8595 support.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8519) will argue that the pattern has completed and bring retest of 0.8221 low.

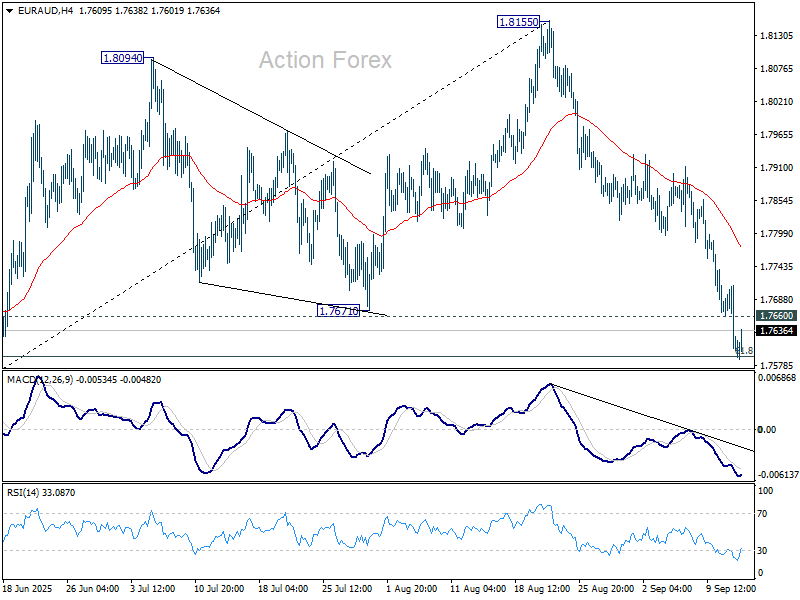

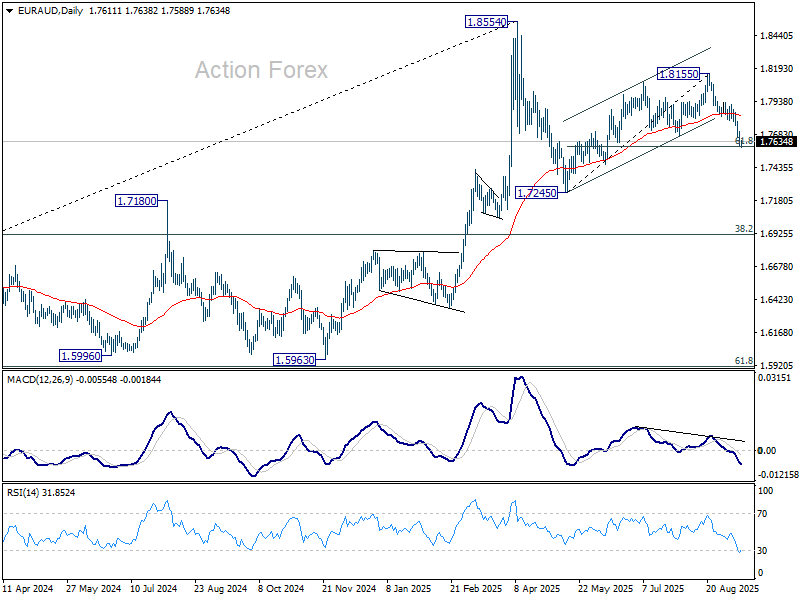

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7578; (P) 1.7647; (R1) 1.7683; More...

EUR/AUD's fall from 1.8155 continued and hit 61.8% retracement of 1.7245 to 1.8155 at 1.7593 already. Intraday bias stays on the downside. The decline is seen as the third leg of the corrective pattern from 1.8554. Sustained break of 1.7593 will pave the way to 1.7245 support next. On the upside, above 1.7660 support turned resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

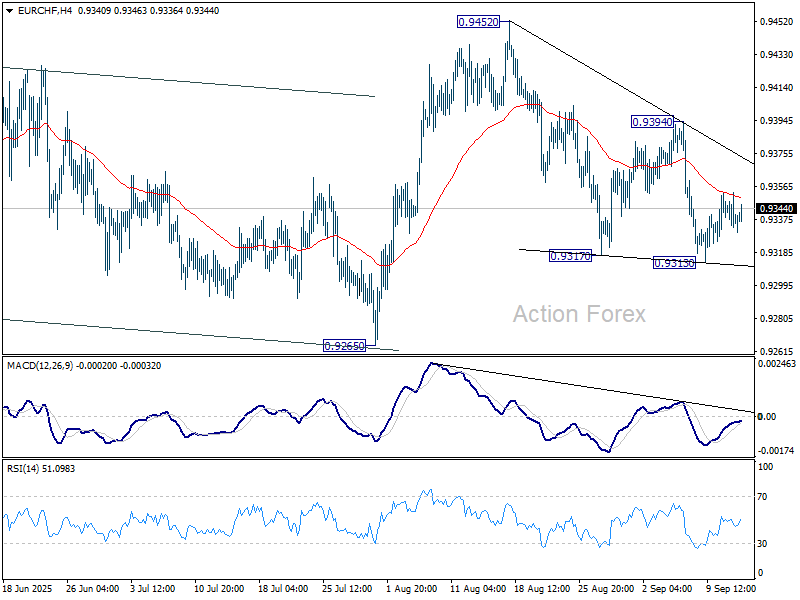

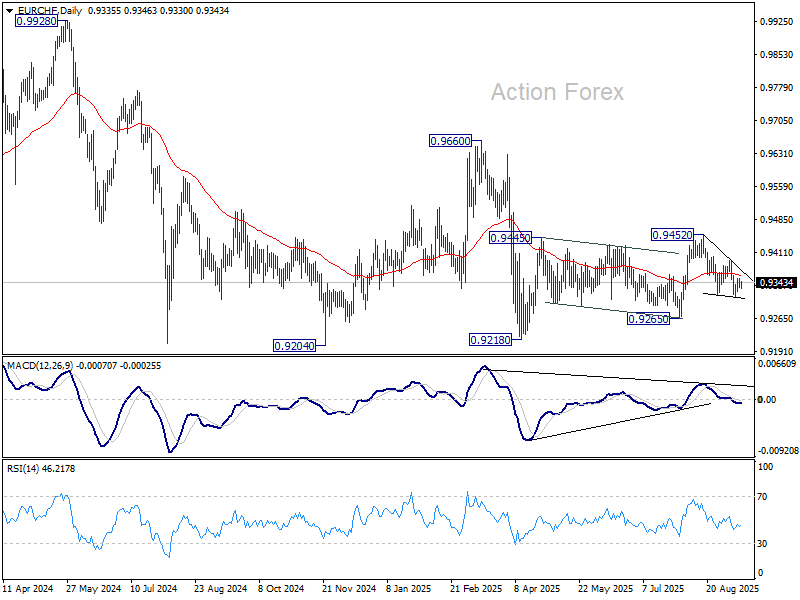

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9330; (P) 0.9343; (R1) 0.9351; More....

Intraday bias in EUR/CHF stays neutral for consolidations above 0.9313. Risk will stay on the downside as long as 0.9394 resistance holds. On the downside, firm break of 0.9313 support will resume the decline from 0.9452. That would also solidify the bearish case that corrective pattern from 0.9218 has completed with three waves up to 0.9452 already. Deeper fall should then be seen to 0.9265 support, and then 0.9204 low.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

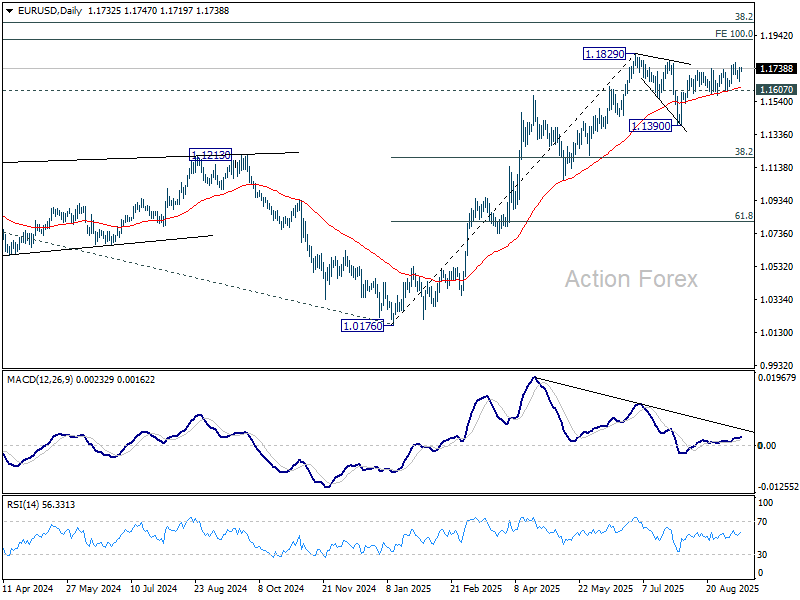

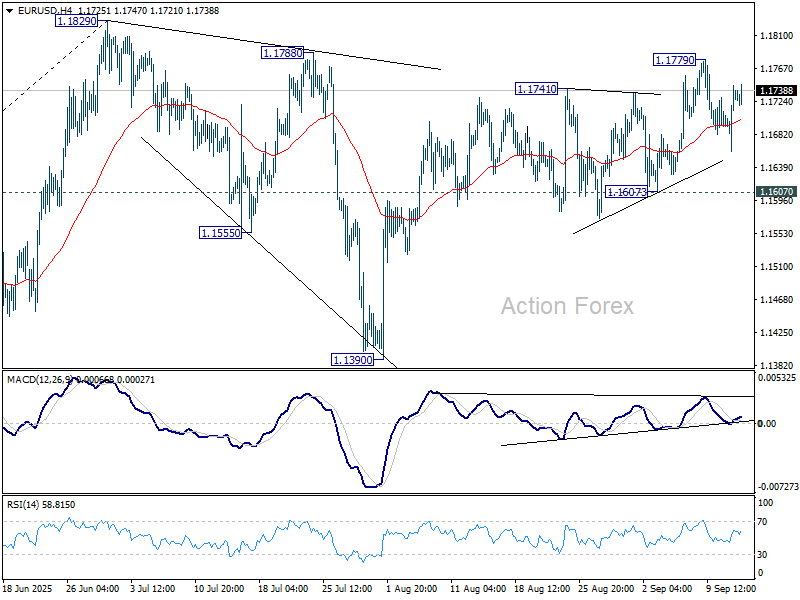

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1682; (P) 1.1714; (R1) 1.1766; More...

Intraday bias in EUR/USD remains neutral as range trading continues below 1.1779. Further rise is expected with 1.1607 support intact. Above 1.1779 will bring retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.