After initial jitters, Dollar rose broadly overnight as Fed Chair Jerome Powell indicated the possibility of higher terminal rate in the current tightening cycle. US stocks ended notably lower and risk-off sentiment carried on in Asian session. Yen is also rising on risk aversion. Nevertheless, markets are taking a breather for now, with focus firstly turned to BoE rate decision today. Besides, ISM services in US session, as well as non-farm payroll employment data tomorrow has the potential to trigger more volatility.

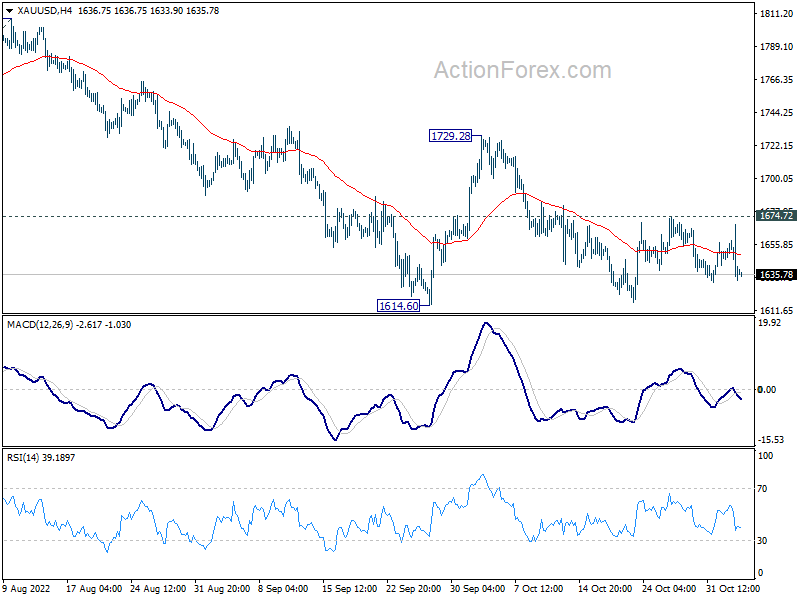

Technically, the breaks of 0.9847 minor support in EUR/USD, 0.6355 minor support in AUD/USD, and 1.0030 minor resistance in USD/CHF suggest Dollar buying in coming back. Gold, too, might be heading back to 1614.60 low as recovery faltered at 1674.72, and even a break there, if Dollar builds up more upside momentum.

In Asia, at the time of writing, Hong Kong HSI is down -2.70%. Chin Shanghai SSE is down -0.10%. Singapore Strait Times is down -1.24%. Japan is on holiday. Overnight, DOW dropped -1.55%. S&P 500 dropped -2.50%. NASDAQ dropped -3.36%. 10-year yield rose 0.007 to 4.059, after dipping to 3.976.

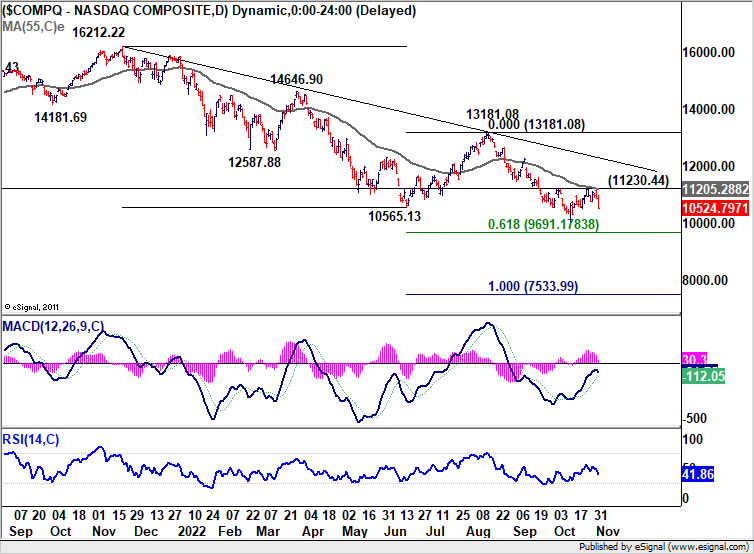

NASDAQ ready for down trend resumption after hawkish Fed Powell

US stocks initially jumped after Fed hinted in the statement that pace of tightening could slow ahead. But sentiment reversed after Fed chair Jerome Powell indicated that slower pace of hikes might come soon, Fed could end up at a higher terminal rate.

In short, comparing to last statement, Fed added, “in determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” This is clearly an indication that Fed is going to consider adjusting the pace of interest rate increases.

In the post-meeting press conference, Powell acknowledged, “As we come closer to that level and move further into restrictive territory, the question of speed becomes less important. … And that’s why I’ve said at the last two press conferences that at some point it will be important to slow the pace of increases. So that time is coming, and it may come as soon as the next meeting or the one after that. No decision has been made.”

However, “incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected,” indicating the possibility of higher terminal rate. Also, Powell noted, “It is very premature to be thinking about pausing. People when they hear ‘lags’ think about a pause. It is very premature, in my view, to think about or be talking about pausing our rate hikes. We have a ways to go.”

More on Fed:

- Fed Review: Another Hawkish 75bp Hike – We Now Expect 50bp also in February

- FOMC Signals a Slower Pace of Tightening Ahead, Although It Is Not Yet Done

- FOMC Short: Dovish Statement, Hawkish Powell

Major US stock indexes closed lower, with development of NASDAQ particularly bearish. Yesterday’s decline suggests rejection by 11230.44 resistance, as well ass 55 day EMA. The fall could be setting up resumption of the whole down trend from 16212.22. Next target will be 61.8% projection of 16212.22 to 10565.13 from 13181.08 at 9691.17. Reaction from there, which is close to 10000 psychological level, will be crucial for the development in the early half of next year.

BoE to hike 75bps, some previews

BoE is widely expected to raise interest rate by 75bps to 3.00% today. That would be the eighth consecutive rate rise, and the largest since 1989.

Governor Andrew Andrew Bailey had already indicated earlier that “inflationary pressures will require a stronger response than we perhaps thought in August.” Additionally, Deputy Governor Ben Broadbent also indicated that “the government’s Energy Price Guarantee has the effect of limiting headline inflation and, to that extent, any related strengthening of second-round (and more persistent) effects on domestic inflation.”

There are talks that the Bank Rate would hit 3.50% in December, and tightening will continue to 4.75% next May. Yet, the path forward remains complicated by the uncertainty over the new government’s new budget. Prime Minister Rishi Sunak’s plan on spending cut and tax hike won’t be revealed until a fiscal statement later on November 17. While the new economic projections by BoE may not matter much, the voting today could at least show the bias among MPC members.

Some previews on BoE:

- Bank of England Might Disappoint Amid Uncertainties about the Budget

- BoE Preview: A Dovish 75bp Hike

- Bank of England Preview

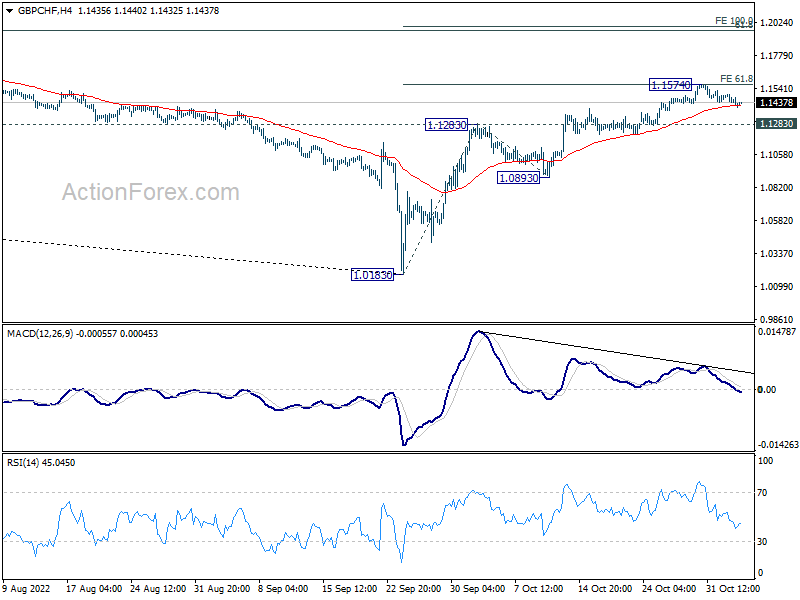

As per market reaction, GBP/CHF would be one to watch. Rise from 1.0183 stalled after hitting 61.8% projection of 1.0183 to 1.1283 from 1.0893 at 1.1574. For now, further rise is expected as long as 1.1283 resistance turned support holds. Firm break of 1.1574 will target 100% projection at 1.1993.

However, sustained break of 1.1283 will argue that whole rebound has completed, and bring deeper fall back to 1.0893 support and possibly below. If happens, that could be a signal of return of Sterling selloff elsewhere.

RBNZ Orr: Significant shocks still arriving through the global economy

RBNZ Governor Adrian Orr told a parliamentary committee that the central bank has “laser-like focus” on bringing inflation down to target. Yet, he admitted that, “the (inflationary) shocks still arriving through the global economy are significant and this is where people need to think about their own ability to weather an enormous amount of unanticipated activities.”

“Meanwhile around our confidence of having inflation under control – that is very high, because we control the end outcome through the interest rate environment. So, that’s a guessing game. That’s about the things we will have to do to achieve low and stable inflation, subject to the continuing buffering of shocks left right and centre. Resilience and humility,” he added.

China Caixin PMI services dropped to 48.4, lowest since May

China Caixin PMI Services dropped from 49.3 to 48.4 in October, below expectation of 49.2. PMI Composite dropped from 48.5 to 48.3. Both were the lowest readings since May.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Both supply and demand contracted to different degrees. The overall employment level increased slightly thanks to an expansion in employment of the services sector. Input costs for all surveyed enterprises rose slightly, while prices charged remained stable. Market sentiment improved but was still below the long-term average.

“Overall, the negative impact of Covid controls on the economy lingered, and the economy was faced with increasing downward pressure. In October, activities in the manufacturing and services sectors continued to shrink, while supply and both domestic and overseas demand contracted. Business costs increased. Service providers were in a better position than manufacturers in terms of prices charged and employment.”

Looking ahead

Swiss CPI, UK services PMI final, and Eurozone unemployment rate will be released in European session. Canada will release building permits and trade balance. US will release trade balance, jobless claims ISM services and factory orders.

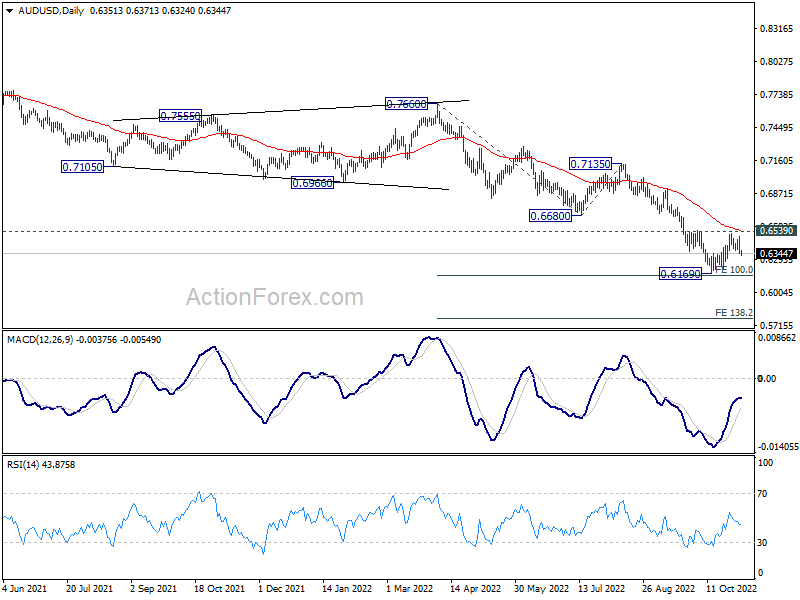

AUD/USD Daily Report

Daily Pivots: (S1) 0.6301; (P) 0.6396; (R1) 0.6446; More…

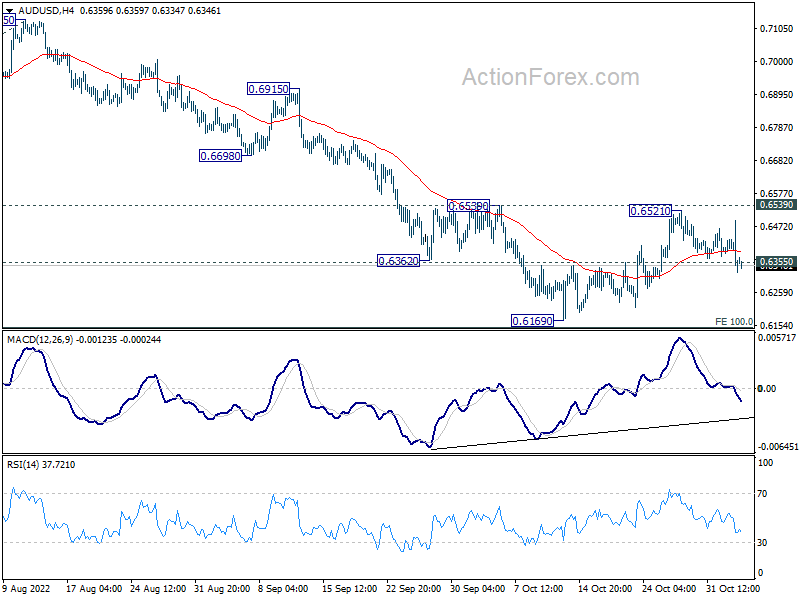

AUD/USD’s break of 0.6355 minor support suggests that corrective recovery from 0.6169 has completed at 0.6521, missing 0.6539 resistance. Rejection by falling 55 day EMA maintains near term bearishness. Intraday bias is back on the downside for retesting 0.6169. Firm break there will resume larger down trend to 138.2% projection of 0.7660 to 0.6680 from 0.7135 at 0.5781.For now, risk will stay on the downside as long as 0.6539 resistance holds.

In the bigger picture, down trend form 0.8006 (2021 high) is expected to continue as long as 0.6680 support turned resistance holds. Medium term momentum remains strong and retest of 0.5506 (2020 low) cannot be ruled out. But firm break of 0.6680 will be the first sign of reversal, and bring stronger rebound back to 0.7135 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Sep | 12.44B | 9.00B | 8.32B | 8.66B |

| 01:45 | CNY | Caixin Services PMI Oct | 48.4 | 49.2 | 49.3 | |

| 07:30 | CHF | CPI M/M Oct | 0.20% | -0.20% | ||

| 07:30 | CHF | CPI Y/Y Oct | 3.20% | 3.30% | ||

| 09:30 | GBP | Services PMI Oct F | 47.5 | 47.5 | ||

| 10:00 | EUR | Eurozone Unemployment Rate Sep | 6.60% | 6.60% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | 67.60% | |||

| 12:00 | GBP | BoE Interest Rate Decision | 3.00% | 2.25% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 9–0–0 | 9–0–0 | ||

| 12:30 | CAD | Building Permits M/M Sep | -4.90% | 11.90% | ||

| 12:30 | CAD | Trade Balance (CAD) Sep | 1.1B | 1.5B | ||

| 12:30 | USD | Trade Balance (EU) Sep | -70.3B | -67.4B | ||

| 12:30 | USD | Initial Jobless Claims (Oct 28) | 215K | 217K | ||

| 12:30 | USD | Nonfarm Productivity Q3 P | -0.10% | -4.10% | ||

| 12:30 | USD | Unit Labor Costs Q3 P | 4.00% | 10.20% | ||

| 13:45 | USD | Services PMI Oct F | 46.6 | 46.6 | ||

| 14:00 | USD | ISM Services PMI Oct | 55.2 | 56.7 | ||

| 14:00 | USD | Factory Orders M/M Sep | 0.30% | 0.00% | ||

| 14:30 | USD | Natural Gas Storage | 99B | 52B |

{kind=link}