Live Comments

Japan PMI Manufacturing Finalized at 54.5, AI Demand Offsets Middle East Headwinds

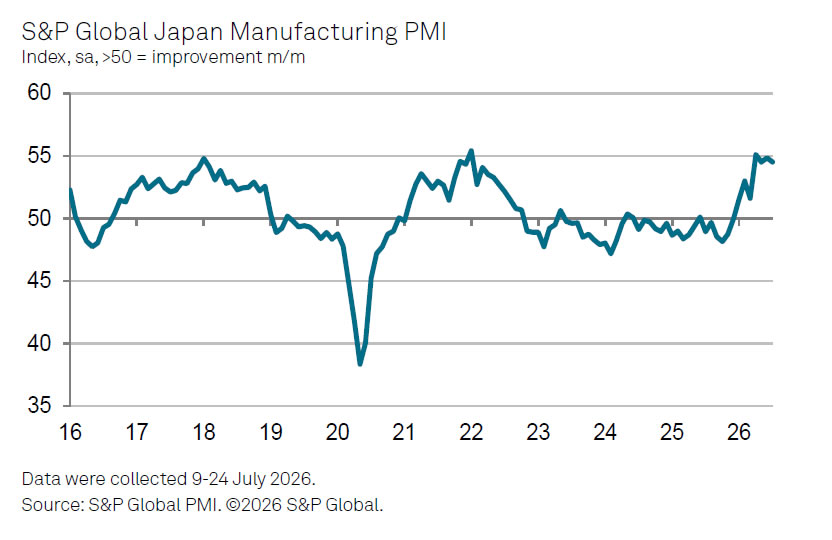

Japan's manufacturing sector remained firmly in expansion territory in July, with the final S&P Global Manufacturing PMI edging down slightly to 54.5 from 54.8 in June. While the headline index eased marginally, it still pointed to a seventh consecutive month of improving business conditions as the sector entered the second half of the year with robust momentum.

The survey highlighted broad-based strength beneath the headline figure. Manufacturing output posted its strongest increase in nearly 12-and-a-half years as firms responded to the steepest rise in new orders in four-and-a-half years. According to S&P Global, many companies linked the improvement to stronger global demand for semiconductors and expanding AI-related manufacturing activity. Firms also stepped up hiring, but the surge in production and order inflows led to mounting capacity pressures, prompting a sharp increase in purchasing activity and inventory accumulation.

At the same time, geopolitical risks continued to shape business conditions. Companies reported building inventories in response to the conflict in the Middle East, driving the fastest increase in input stocks in more than two years. Although input cost inflation moderated from June, it remained elevated and continued to feed through to higher selling prices. The survey therefore points to a manufacturing sector benefiting from powerful structural demand drivers, while still contending with supply-chain and inflation risks stemming from geopolitical uncertainty.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Manufacturing PMI | 54.5 | 54.8 |

| Production | Strongest growth in nearly 12½ years | Expanded |

| New Orders | Strongest rise in 4½ years | Expanded |

| Employment | Solid increase | Increased |

| Input Costs | Rose at a marked but softer pace | Sharper increase |

| Selling Prices | Rose substantially | Increased |

Market Takeaways

- Manufacturing PMI eased only marginally from 54.8 to 54.5, remaining firmly in expansion territory for a seventh consecutive month.

- Output recorded its strongest increase since early 2014, supported by the steepest rise in new orders in four-and-a-half years, pointing to robust underlying demand.

- Survey respondents highlighted stronger global demand for semiconductors and AI-related manufacturing as key drivers of the rebound.

- Firms continued to hire, but rapid growth in production and orders intensified capacity pressures, prompting the fastest increase in purchasing activity since April 2022 and the quickest inventory build-up in more than two years.

- While input cost inflation moderated from June, cost pressures remained elevated due in part to the Middle East conflict, allowing manufacturers to continue raising selling prices.

Australia Manufacturing PMI Finalizes at Six-Month High, Yet Inflation and Supply Risks Limit Confidence

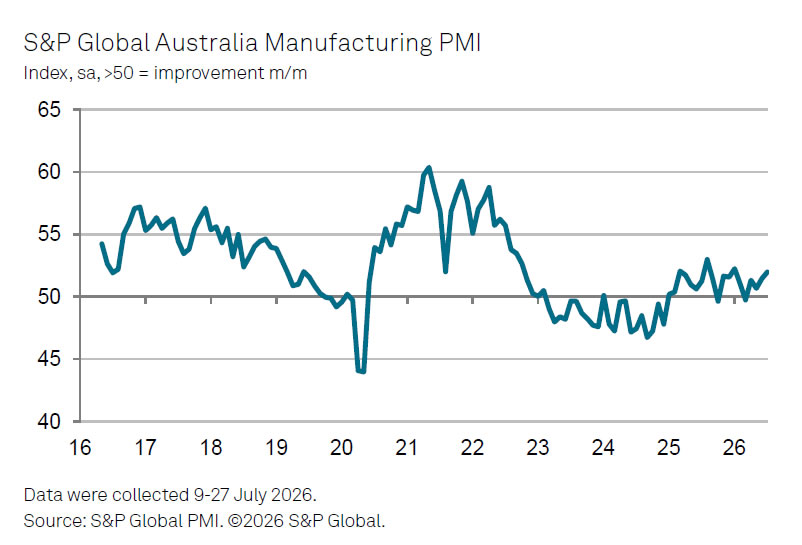

Australia's manufacturing sector showed further signs of recovery in July, with S&P Global Australia Manufacturing PMI finalized at 52.0, up from 51.5 in June and the strongest reading since January. The sector has now remained in expansion territory for four consecutive months, supported by renewed growth in both production and new orders as business conditions improved at the start of the second half of the year.

The details of the survey suggest the recovery is beginning to broaden, albeit only gradually. Factory output expanded for the first time in six months, while new orders returned to growth for the first time since February. However, both increases were only marginal, indicating that underlying demand remains subdued. Manufacturers also continued to face elevated input costs and supply-side pressures, preventing a stronger rebound despite the improvement in headline activity.

S&P Global's Economics Director Andrew Harker said the latest data offered reassurance that the sector was recovering from the disruption caused by the Middle East conflict, but stressed that the improvement remained tentative. He warned that renewed deterioration in the region could quickly rekindle inflationary and supply pressures, leaving the nascent recovery vulnerable. The survey therefore points to improving business conditions, but also underscores that manufacturers remain highly exposed to geopolitical developments that could influence both inflation and the broader economic outlook.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Manufacturing PMI | 52.0 | 51.5 |

| Output | Returned to growth | Contracted |

| New Orders | Returned to growth | Contracted |

| Business Conditions | Improved at fastest pace since January | Improved |

Market Takeaways

- Manufacturing PMI rose from 51.5 to 52.0, marking the strongest expansion since January and extending the sector's expansion streak to four months.

- Output increased for the first time in six months, while new orders returned to growth for the first time since February, suggesting the manufacturing downturn linked to the Middle East conflict is easing.

- Despite the stronger headline reading, both output and demand expanded only marginally, indicating the recovery remains fragile rather than broad-based.

- Persistent price and supply-chain pressures continue to weigh on manufacturers, leaving the sector vulnerable to renewed geopolitical disruptions.

- The survey reinforces the view that Australia's manufacturing sector is stabilizing, but the durability of the recovery will depend heavily on whether inflation and supply pressures ease further.

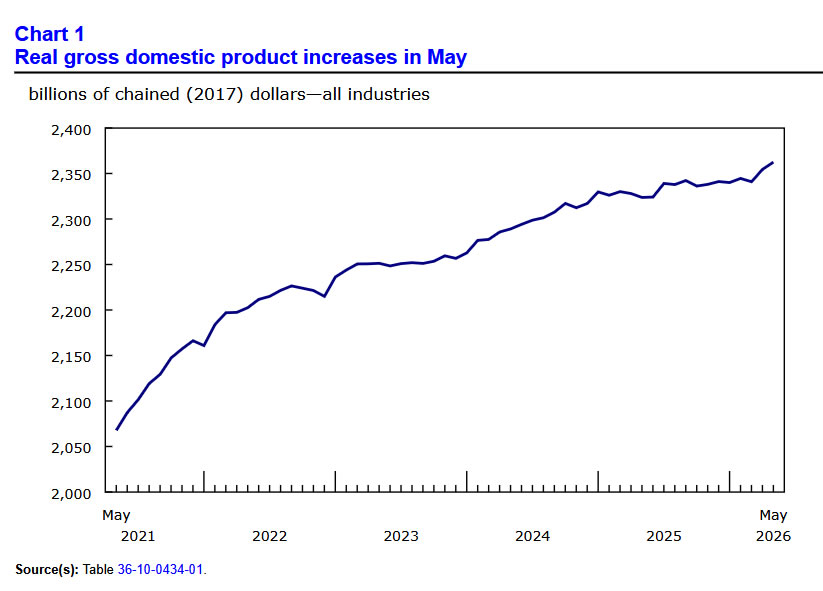

Canada GDP Beats Expectations, June Estimate Points to Strong Q2 Growth

Canada's economy expanded 0.3% month-over-month in May, beating expectations of 0.2% and marking a second consecutive monthly increase. Growth was broad-based, with 13 of 20 industrial sectors posting gains as both goods-producing and services-producing industries contributed to the expansion. Statistics Canada also estimated that real GDP rose a further 0.2% in June, pointing to annualized growth of 0.8% for the second quarter based on industry data.

The goods-producing sector led the way with a 0.6% increase in May, supported by widespread gains across most industries. Mining, quarrying and oil and gas extraction advanced 1.0%, extending April's recovery as two of its three subsectors posted a second straight monthly increase. Manufacturing also grew 0.3%, with most subsectors expanding during the month. On the services side, output rose 0.2%, driven primarily by gains in real estate and rental and leasing as well as public administration. Real estate activity increased 0.4%, with all subsectors contributing to the advance.

The latest figures suggest the Canadian economy maintained solid momentum through the second quarter despite an uncertain external backdrop. The advance estimate for June indicates growth remained supported by wholesale trade, finance and insurance, and retail trade, although weaker utilities and agriculture partially offset those gains. With domestic activity continuing to broaden across both goods and services sectors, the data point to an economy that has proved more resilient than expected heading into the second half of the year.

Economic Data Summary

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| GDP M/M (May) | 0.3% | 0.2% | 0.5% |

| GDP M/M (June Advance) | 0.2% | — | — |

| Q2 2026 GDP (Industry-Based Estimate) | 0.8% | — | — |

Sector Breakdown

| Component | Current | Trend |

|---|---|---|

| Goods-producing industries | 0.6% | ↑ Broad-based growth |

| Services-producing industries | 0.2% | ↑ Continued expansion |

| Mining, quarrying & oil and gas | 1.0% | ↑ Second consecutive gain |

| Manufacturing | 0.3% | ↑ Majority of subsectors higher |

| Real estate & rental and leasing | 0.4% | ↑ Broad-based gains |

Key Takeaways

- Canada's economy outperformed expectations in May. Real GDP rose 0.3% month-over-month, beating the 0.2% consensus forecast and marking a second consecutive monthly increase.

- Growth was broad-based. Thirteen of twenty industrial sectors expanded, with both goods-producing and services-producing industries contributing to the overall gain.

- Goods production led the expansion. Goods-producing industries grew 0.6%, supported by stronger mining, oil and gas extraction, and manufacturing output.

- Mining and energy remained key drivers. The mining, quarrying and oil and gas extraction sector increased 1.0%, posting a second straight monthly gain.

- Services continued to provide support. Services-producing industries rose 0.2%, led by real estate and rental and leasing (0.4%) together with public administration.

- June appears to have maintained the momentum. Statistics Canada's advance estimate points to another 0.2% increase in June, driven by wholesale trade, finance and insurance, and retail trade.

- Second-quarter growth looks solid. Based on May data and the June advance estimate, real GDP by industry is on track to have expanded 0.8% in Q2, suggesting the Canadian economy entered the second half of the year with steady momentum.