In the new World Economic Outlook released today IMF kept global growth forecast unchanged at 3.9% in 2018 and 3.9% in 2019.

For advanced economies, growth projections for 2018 were generally revised up except Japan and Canada. For 2019, projections were largely unchanged with upward revision in US, France and Spain.

China’s growth projection was kept unchanged at 6.6% in 2018 and 6.4% in 2019.

Here is the summary table.

Full IMF report here

Full IMF report here

In a blog post by Maurice Obstfeld, Economic Counsellor and Director of Research at the IMF, it’s noted that “the world economy continues to show broad-based momentum. Against that positive backdrop, the prospect of a similarly broad-based conflict over trade presents a jarring picture.”

Obstfeld said that “prospect of trade restrictions and counter-restrictions threatens to undermine confidence and derail global growth prematurely.” And, without naming who, he added that “while some governments are pursuing substantial economic reforms, trade disputes risk diverting others from the constructive steps they would need to take now to improve and secure growth prospects.”

Referring to intensification of trade tensions since US announcement of steel and aluminum tariffs, Obstfeld said “these initiatives will do little, however, to change the multilateral or overall U.S. external current account deficit, which owes primarily to a level of aggregate U.S. spending that continues to exceed total income.”

The full blog post can be found here. Global Economy: Good News for Now but Trade Tensions a Threat

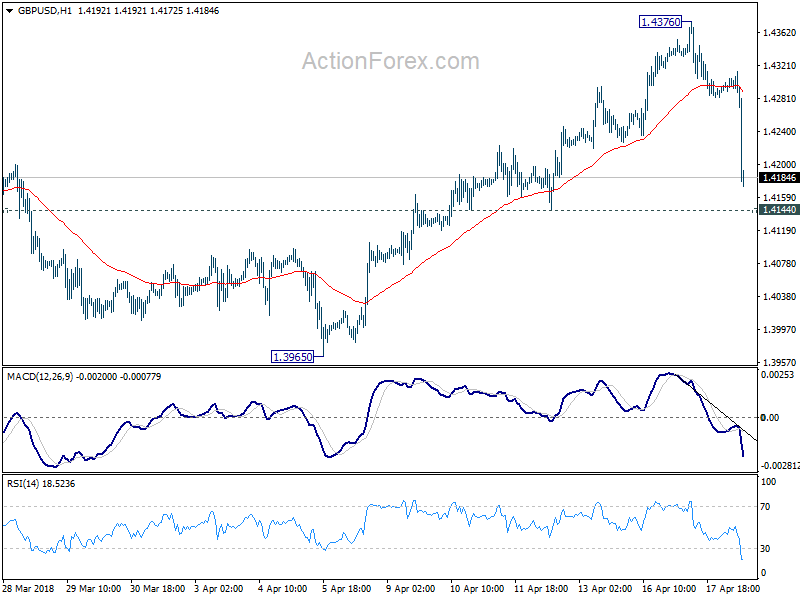

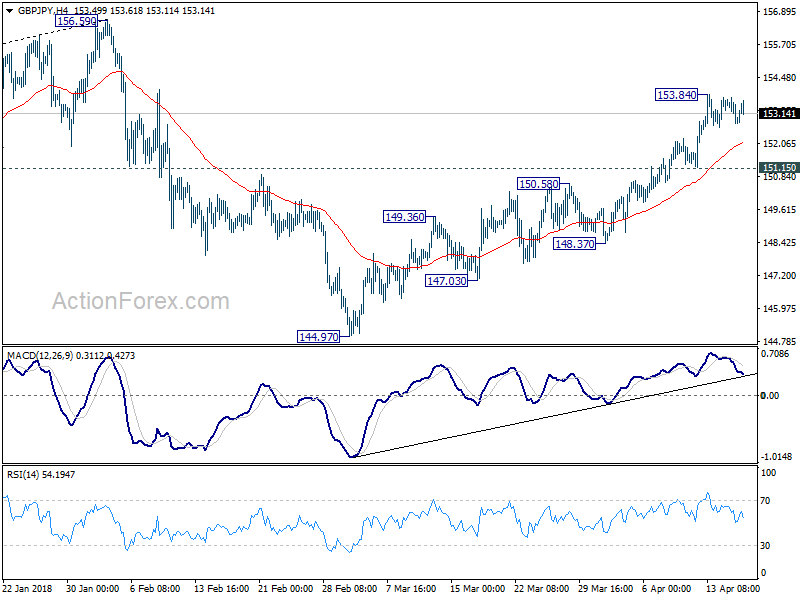

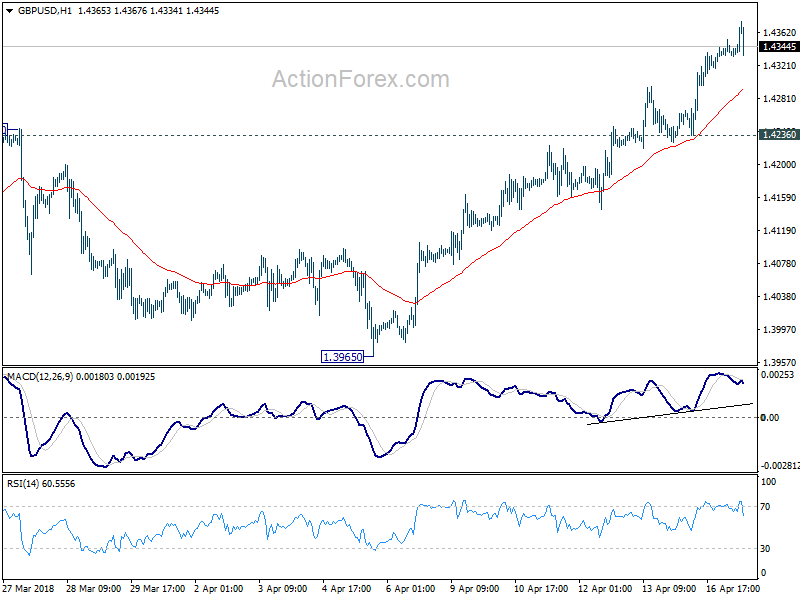

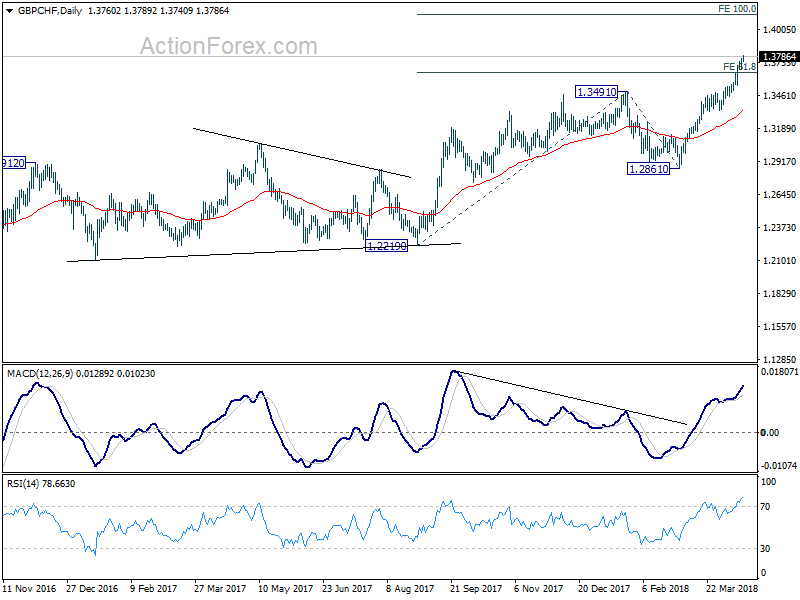

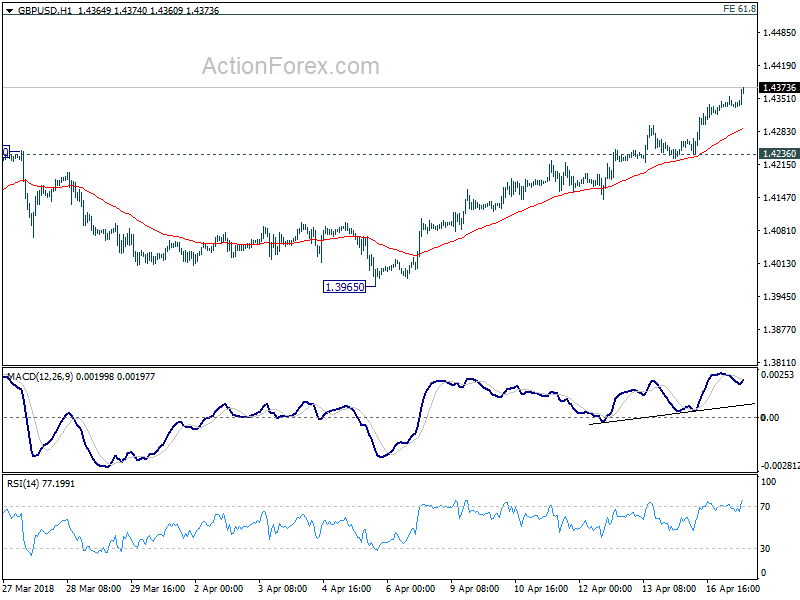

UK Hammond cheers CPI, BoE May hike back on table

After initial post CPI selloff, GBP stabilizes a bit. But it’s still trading as the weakest major currency for today.

Chancellor of Exchequer Philip Hammond surely welcomed the data as he tweeted:

By loading the tweet, you agree to Twitter’s privacy policy.

Learn more

Load tweet

But the data is certainly not that welcomed by BoE hawks like Ian McCafferty and Michael Saunders. They comments will be closely watched to see if they back down from their hawkish stance.

It should be noted that BoE’s February projections were based on market pricing that Bank Rate will rise to 0.7% by 2018 year end. And by 2019 Q1, CPI inflation would drop to 2.3%. Inflation is now already in a clear down trend, diving from 3% in January to 2.5% in March. With Bank Rate staying unchanged at 0.50%. There is much room for BoE to wait through at least another quarter to see how things play out.

November rate decision is now closer to certain, “no”. And May hike is back on the table.