Sample Category Title

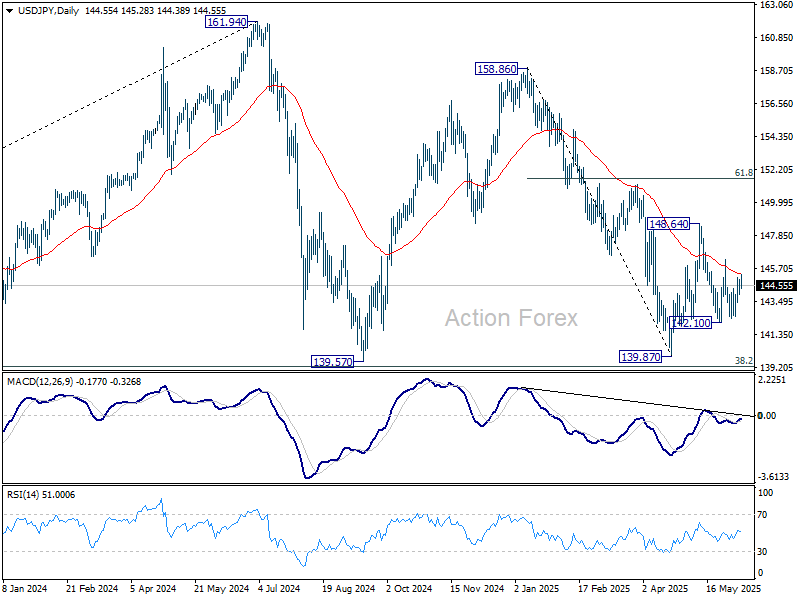

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.06; (P) 144.51; (R1) 145.04; More...

Intraday bias in USD/JPY remains neutral for the moment. On the upside, above 146.27 resistance will argue that price actions from 148.64 has completed as a corrective pattern. Intraday bias will be back on the upside for 148.64 resistance and above to resume the rebound from 139.87 low. However, firm break of 142.10 will bring retest of 139.87 instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

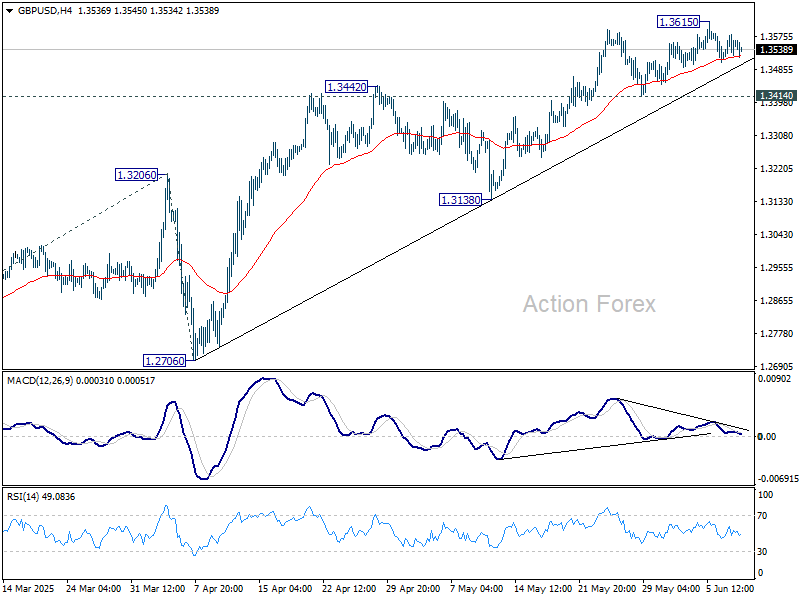

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3514; (P) 1.3547; (R1) 1.3586; More...

Intraday bias in GBP/USD remains neutral as consolidations continues below 1.3615. Further rise will remain in favor as long as 1.3414 support holds. Above 1.3615 will target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. Considering bearish divergence condition in 4H MACD, break of 1.3414 support should confirm short term topping, and bring deeper correction to 1.3138 support instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2913) holds, even in case of deep pullback.

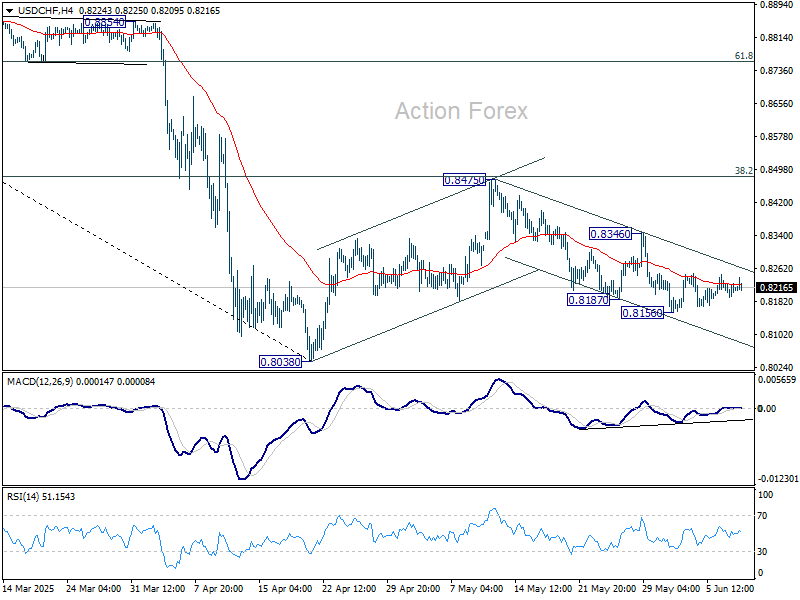

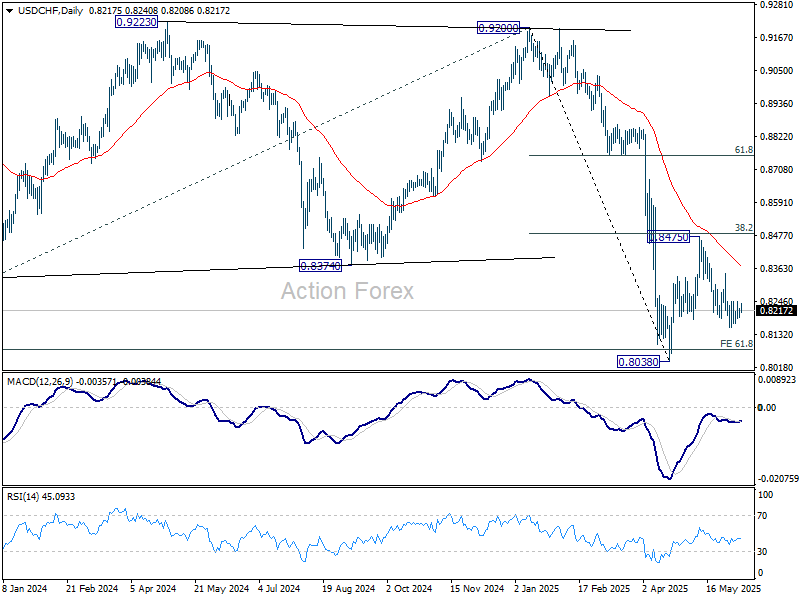

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8197; (P) 0.8213; (R1) 0.8234; More….

Intraday bias in USD/CHF stays neutral as range trading continues above 0.8156. Price actions from 0.8038 are seen as a corrective pattern to decline from 0.9200. While fall from 0.8475 might extend lower, downside should be contained by 0.8038 to bring rebound. Break of 0.8436 resistance will suggest that it's already in the third leg of the correction, and target 0.8475.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8696) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

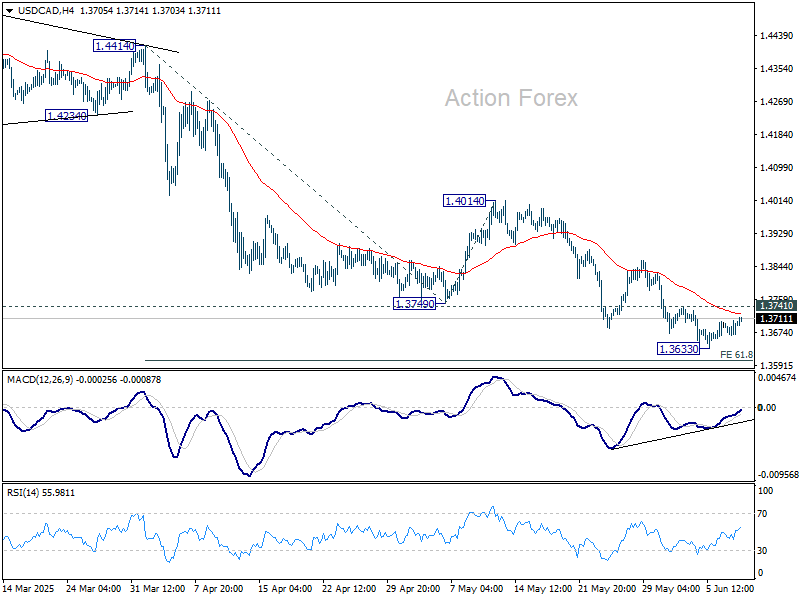

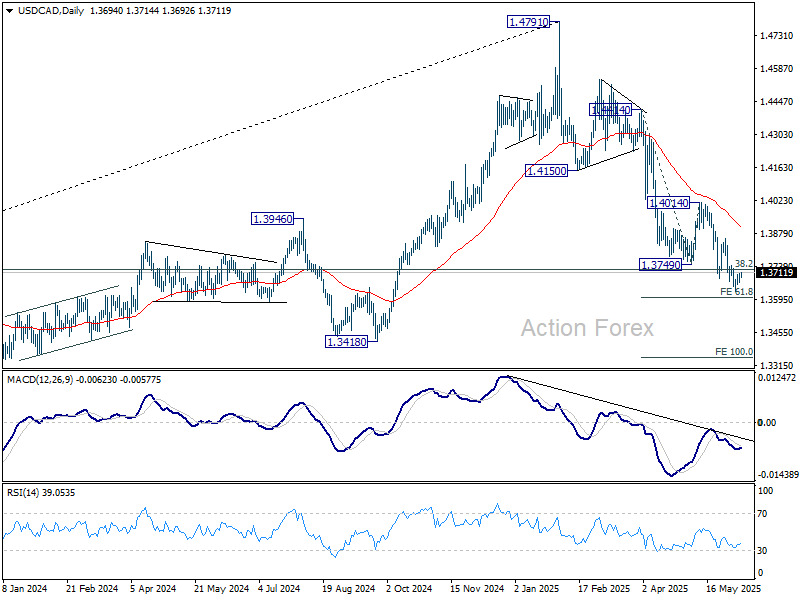

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3677; (P) 1.3692; (R1) 1.3715; More...

USD/CAD is staying in tight range above 1.3633 and intraday bias remains neutral. Considering bullish convergence condition in 4H MACD, firm break of 1.3741 will indicate short term bottoming at 1.3633. Intraday bias will turn back to the upside for stronger rebound to 1.4014 resistance, as a correction to fall from 1.4791. Nevertheless, decisive break of 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603 will pave the way to 100% projection at 1.3349.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

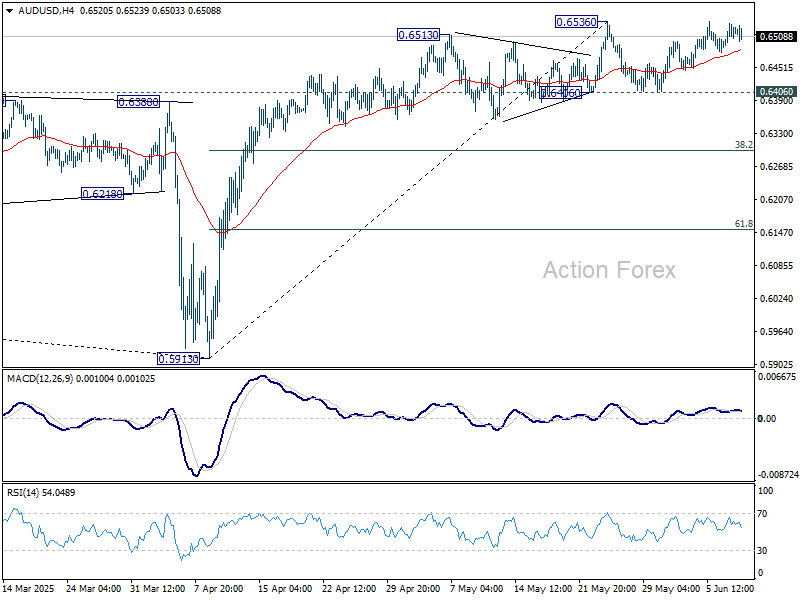

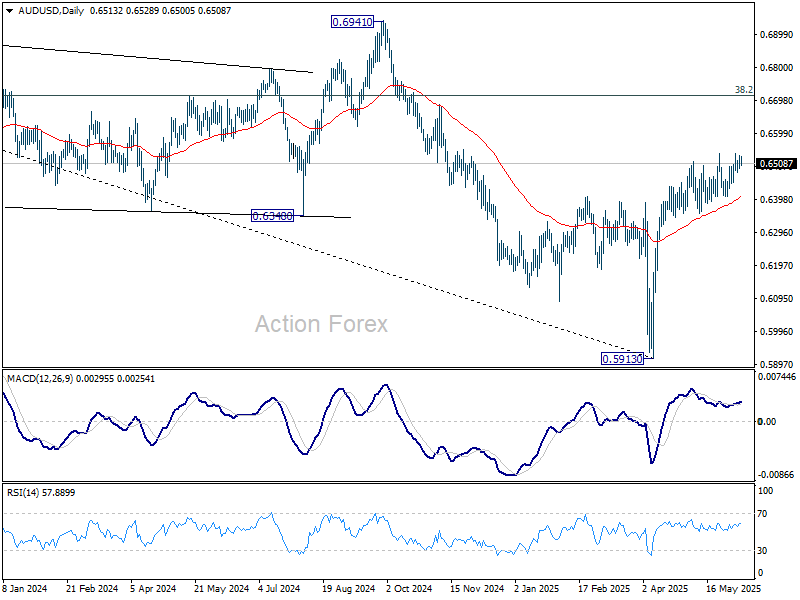

AUD/USD Daily Report

Daily Pivots: (S1) 0.6496; (P) 0.6515; (R1) 0.6536; More...

Intraday bias in AUD/USD remains neutral as it's still staying below 0.6536 resistance. More consolidations could be seen, but even in case of another dip, further rise is in favor favor as long as 0.6406 support holds. On the upside, decisive break of 0.6536 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, firm break of 0.6406 will turn bias to the downside for 38.2% retracement of 0.5913 to 0.6536 at 0.6298.

In the bigger picture, AUD/USD is still struggling to sustain above 55 W EMA (now at 0.6443) cleanly, and outlook is mixed. Sustained trading above 55 W EMA will indicate that rise from 0.5913 is at least correcting the down trend from 0.8006 (2021 high), with risk of trend reversal. Further rise should be seen to 38.2% retracement of 0.8006 to 0.5913 at 0.6713. However, rejection by 55 W EMA will revive medium term bearishness for another fall through 0.5913 at a later stage.

Aussie Firmer in Quiet Markets as US-China Trade Talks Continue

Global markets remain in a state of cautious anticipation as high-level trade negotiations between the US and China continue for a second day in London. While there’s no definitive outcome yet, mild optimism lingers. Asian equities reflected that mood, with Japan’s Nikkei and Hong Kong’s Hang Seng Index both trading slightly higher. Yet the prevailing sense is one of hesitation, with limited conviction behind the moves. Investors are still waiting for substantive developments before making bolder positioning decisions.

In the currency markets, Kiwi and Aussie continue to outperform for the week so far, buoyed by broad risk resilience and perhaps early hopes that renewed dialogue could reduce global trade frictions. However, upside momentum in both currencies has been sluggish. At the other end, Loonie is trading as the weakest, followed by Swiss Franc and Japanese Yen. Dollar, Euro, and British Pound are largely directionless, trading in the middle of the weekly performance board.

The London meetings between US and Chinese officials mark the second day of high-stakes negotiations aimed at resolving the fallout from earlier tariff escalations. While Monday’s talks yielded no breakthrough, the inclusion of Commerce Secretary Howard Lutnick in this round is notable. His agency oversees export controls, signaling the centrality of rare earths in the ongoing discussions. These magnets, vital to EV production and defense equipment, have become a leverage point for Beijing as it holds a near-monopoly over global supply.

Markets are not pricing in a full resolution just yet. Most expectations center around a tentative agreement on technical issues or interim concessions, such as expanded export licenses. However, structural divisions persist, particularly over technology and national security. Without more substantive signs of compromise, the fragile sentiment boost from the talks could quickly fade, especially if either side issues a combative post-meeting statement.

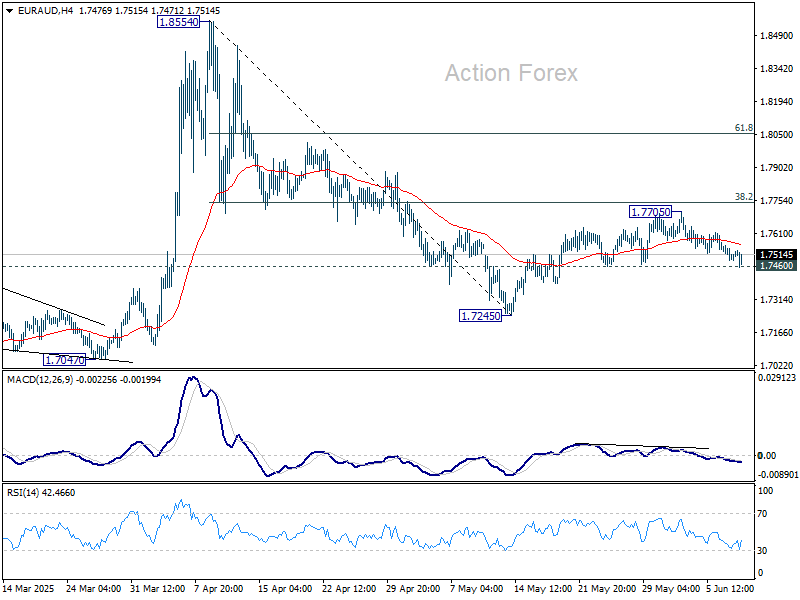

Technically, EUR/AUD is now pressing 1.7460 support as the decline from 1.7705 extends. Firm break there will argue that choppy recovery from 1.7245 has completed as a correction, ahead of 38.2% retracement of 1.8554 to 1.7245. That would also suggest that fall from 1.8854 is ready to resume through 1.7245 low.

In Asia, at the time of writing, Nikkei is up 0.89%. Hong Kong HSI is up 0.15%. China Shanghai SSE is down -0.13%. Singapore Strait Times is down -0.13%. Japan 10-year JGB yield is down -0.002 at 1.476. Overnight, DOW closed down -0.00%. S&P 500 rose 0.09%. NASDAQ rose 0.31%. 10-year yield fell -0.028 to 4.482.

BoJ’s Ueda reaffirms gradual tightening path, cites limited room for rate cuts

BoJ Governor Kazuo Ueda reiterated to parliament today that interest rate hikes will continue, though cautiously, once the central bank gains "more conviction that underlying inflation will approach 2% or hover around that level".

Ueda explained that BoJ still maintains negative real interest rates to support inflation momentum and ensure price growth remains both stable and sustained.

However, Ueda also flagged a significant limitation in policy space should economic conditions deteriorate. With the short-term policy rate still only at 0.5%, the BoJ has "limited room" to cut rates in response to any sharp downturn in growth.

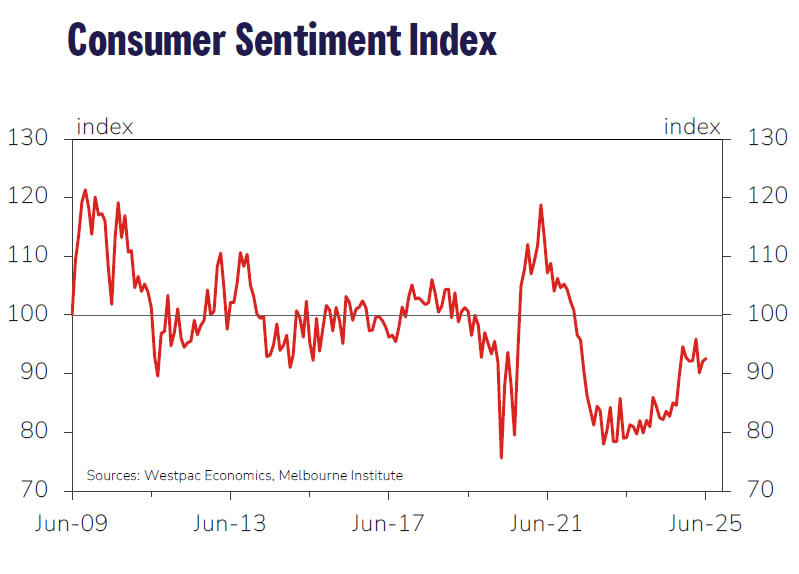

Australia's Westpac consumer sentiment edges higher as rate cuts clash with growth worries

Australia's Westpac Consumer Sentiment index rose a modest 0.5% mom in June to 92.6, reflecting a population still mired in what Westpac called a “holding pattern of cautious pessimism.”

The data reveal "two clear opposing forces" shaping household attitudes: easing inflation and RBA’s May rate cut have improved perceptions around major purchases. On the other hand, sluggish domestic growth and global trade uncertainties continue to weigh heavily on expectations.

Looking ahead, attention turns to the RBA’s next meeting on July 7–8. With economic data remaining mixed and labor market tightness still evident, Westpac expects the central bank to proceed with caution and keep the cash rate on hold. Nonetheless, a fresh round of economic projections in August could pave the way for another 25 basis point cut, as RBA recalibrates its stance amid still-sluggish growth.

Australia’s NAB business confidence lifts to 2, but employment conditions erode

Australia’s NAB Business Confidence index turned positive in May, rising from -1 to 2. However, the improvement in confidence was not matched by underlying business conditions, which weakened further. Business Conditions index slipped from 2 to 0, with trading conditions dipping slightly from 6 to 5, profitability remaining in the red at -4, and employment conditions dropping from 4 to 0 — all pointing to a stagnating environment.

On the inflation front, cost indicators presented a mixed picture. Labor cost growth remained firm at a quarterly equivalent pace of 1.7%. Purchase cost and final product price growth eased to 1.1% and 0.5%, respectively. Retail price growth held steady at 1.2%, suggesting persistent margin pressures.

NAB Chief Economist Sally Auld emphasized that business conditions are still weak and warned that continued softness could cap any recovery in confidence. She also flagged the labor market as a key area to monitor, with the employment index now below average.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6496; (P) 0.6515; (R1) 0.6536; More...

Intraday bias in AUD/USD remains neutral as it's still staying below 0.6536 resistance. More consolidations could be seen, but even in case of another dip, further rise is in favor favor as long as 0.6406 support holds. On the upside, decisive break of 0.6536 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, firm break of 0.6406 will turn bias to the downside for 38.2% retracement of 0.5913 to 0.6536 at 0.6298.

In the bigger picture, AUD/USD is still struggling to sustain above 55 W EMA (now at 0.6443) cleanly, and outlook is mixed. Sustained trading above 55 W EMA will indicate that rise from 0.5913 is at least correcting the down trend from 0.8006 (2021 high), with risk of trend reversal. Further rise should be seen to 38.2% retracement of 0.8006 to 0.5913 at 0.6713. However, rejection by 55 W EMA will revive medium term bearishness for another fall through 0.5913 at a later stage.

Elliott Wave Perspective: S&P 500 (SPX) Set to Finish Wave 3

Since reaching its low on April 7, 2025, the S&P 500 (SPX) has embarked on an impulsive rally. From that bottom, the index progressed through distinct waves, as defined by Elliott Wave theory. Wave 1 concluded at 5246.57, followed by a corrective pullback in wave 2, which found support at 4910.42. Currently, wave 3 is underway, unfolding as a strong impulse with subdivisions in a lesser degree.

From the wave 2 low, the rally continued with wave ((i)) peaking at 5481.34. A brief retracement in wave ((ii)) then followed which ended at 5101.63. The index then surged higher in wave ((iii)), reaching 5968.61. A subsequent pullback in wave ((iv)) found support at 5767.41, setting the stage for further gains. The index should push to a few more highs to complete wave ((v)) of 3. This will mark the culmination of this upward phase.

Looking ahead, once wave 3 concludes, a corrective wave 4 should follow, retracing part of the rally from the April 7, 2025 low. This correction could unfold in a 3, 7, or 11-swing pattern before the index resumes its upward trajectory. In the near term, as long as the pivot low at 5765.74 holds, the S&P 500 is poised to achieve additional highs to finalize wave ((v)) of 3. However, if this critical support at 5765.74 is breached, it would signal the end of wave 3, prompting a larger wave 4 pullback, potentially in a 3, 7, or 11-swing structure.

S&P 500 (SPX) 60-Minute Elliott Wave Technical Chart

SPX Elliott Wave Technical Video

https://www.youtube.com/watch?v=IXbLsoD2zbg

BoJ’s Ueda reaffirms gradual tightening path, cites limited room for rate cuts

BoJ Governor Kazuo Ueda reiterated to parliament today that interest rate hikes will continue, though cautiously, once the central bank gains "more conviction that underlying inflation will approach 2% or hover around that level".

Ueda explained that BoJ still maintains negative real interest rates to support inflation momentum and ensure price growth remains both stable and sustained.

However, Ueda also flagged a significant limitation in policy space should economic conditions deteriorate. With the short-term policy rate still only at 0.5%, the BoJ has "limited room" to cut rates in response to any sharp downturn in growth.

Australia’s NAB business confidence lifts to 2, but employment conditions erode

Australia’s NAB Business Confidence index turned positive in May, rising from -1 to 2. However, the improvement in confidence was not matched by underlying business conditions, which weakened further. Business Conditions index slipped from 2 to 0, with trading conditions dipping slightly from 6 to 5, profitability remaining in the red at -4, and employment conditions dropping from 4 to 0 — all pointing to a stagnating environment.

On the inflation front, cost indicators presented a mixed picture. Labor cost growth remained firm at a quarterly equivalent pace of 1.7%. Purchase cost and final product price growth eased to 1.1% and 0.5%, respectively. Retail price growth held steady at 1.2%, suggesting persistent margin pressures.

NAB Chief Economist Sally Auld emphasized that business conditions are still weak and warned that continued softness could cap any recovery in confidence. She also flagged the labor market as a key area to monitor, with the employment index now below average.

Australia’s Westpac consumer sentiment edges higher as rate cuts clash with growth worries

Australia's Westpac Consumer Sentiment index rose a modest 0.5% mom in June to 92.6, reflecting a population still mired in what Westpac called a “holding pattern of cautious pessimism.”

The data reveal "two clear opposing forces" shaping household attitudes: easing inflation and RBA’s May rate cut have improved perceptions around major purchases. On the other hand, sluggish domestic growth and global trade uncertainties continue to weigh heavily on expectations.

Looking ahead, attention turns to the RBA’s next meeting on July 7–8. With economic data remaining mixed and labor market tightness still evident, Westpac expects the central bank to proceed with caution and keep the cash rate on hold. Nonetheless, a fresh round of economic projections in August could pave the way for another 25 basis point cut, as RBA recalibrates its stance amid still-sluggish growth.