Sample Category Title

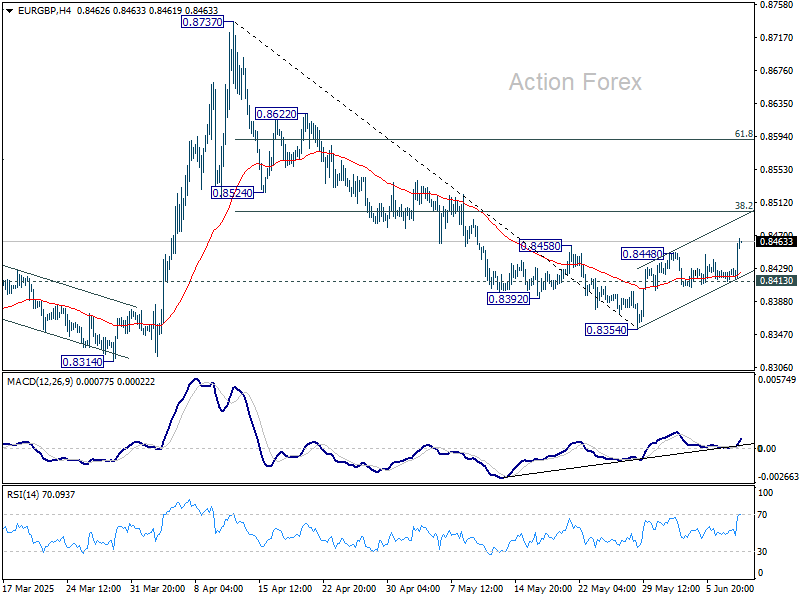

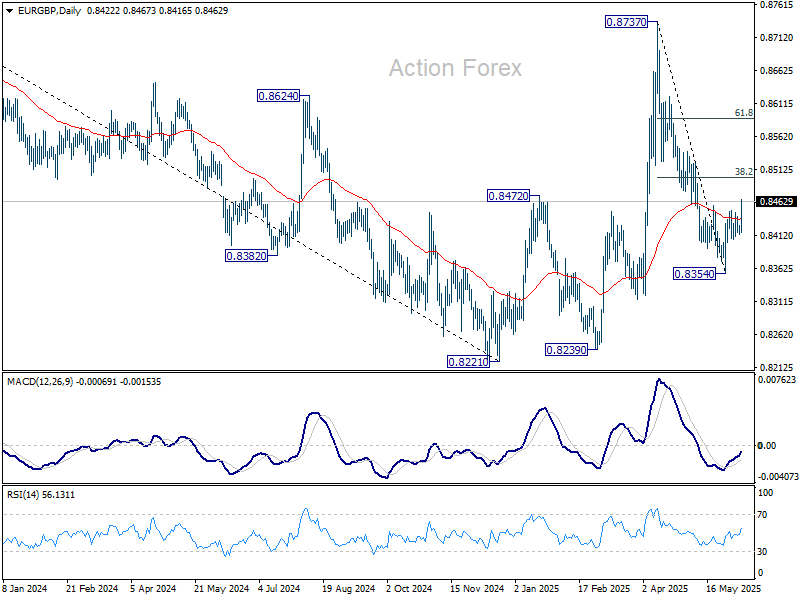

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8419; (P) 0.8424; (R1) 0.8433; More...

EUR/GBP's rebound from resumed by breaking through 0.8448 resistance, and intraday bias is back on the upside for 38.2% retracement of 0.8737 to 0.8354 at 0.8500. Strong resistance could be seen from 0.8500 to complete the corrective bounce. On the downside, break of 0.8413 support will bring retest of 0.8354 low. However, firm break of 0.8500 will pave the way to 61.8% retracement at 0.8591 instead.

In the bigger picture, price actions from 0.8221 medium term bottom are merely forming a corrective pattern. Nevertheless, there is no clear momentum to break through 0.8201 key support (2022 low) yet. Hence, range trading is expected between 0.8221/8737 for now.

Sterling Slumps as UK Jobs Data Fuels August BoE Rate Cut Bets

Sterling is sold off notably today after dismal UK labor market data intensified expectations of a BoE rate cut in August. The most striking element was the -109k drop in payrolled employment—the largest non-pandemic decline since records began in 2014—coupled with a rise in the unemployment rate to its highest level since mid-2023.

While wage growth remains elevated, its slowdown reinforces the view that inflationary pressures are easing. With signs that labour market cooling is gaining momentum, markets are increasingly pricing in not just an August rate cut, but a follow-up move in November. Traders will, however, closely monitor Chancellor Rachel Reeves’ fiscal statement tomorrow, which may influence expectations depending on the scale and orientation of policy shifts.

Elsewhere, markets are also eyeing the second day of US-China trade talks in London. Ahead of the meeting, U.S. Commerce Secretary Howard Lutnick said that he expected a full day meeting today, while the negotiations are "going well". Both sides are expected to issue updates later in the day.

Overall in the currency markets, Sterling is currently the worst performer, followed by Swiss Franc, and then Dollar. Loonie is the best, followed by Aussie, and then Euro. Yen and Aussie are positioning in the middle.

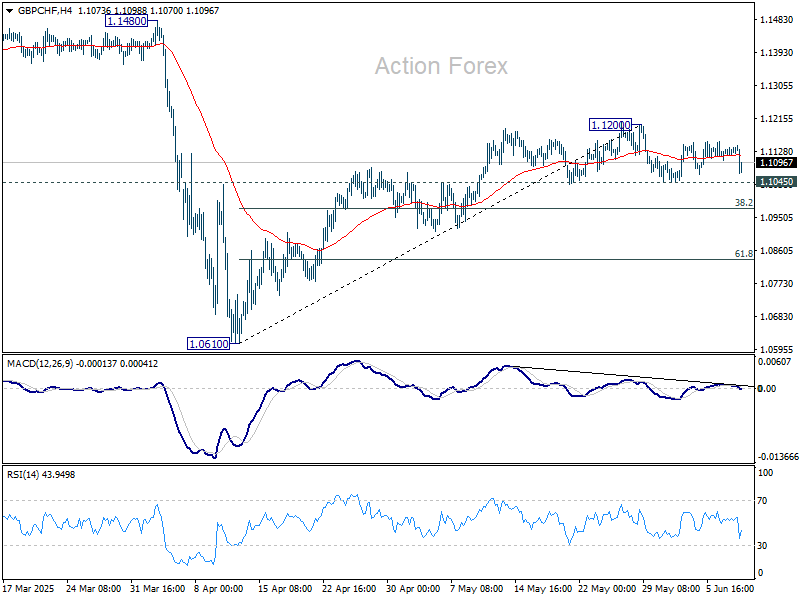

Technically, focus is now on 1.1045 support in GBP/CHF with today's dip. Firm break there will complete a head and shoulder top pattern, which suggest that rise from 1.0610 has completed, at 1.1200. Deeper decline should then be seen to 38.2% retracement of 1.0610 to 1.1200 at 1.0975, and possibly further to 61.8% retracement at 1.0835.

In Europe, at the time of writing, FTSE is up 0.53%. DAX is down -0.40%. CAC is up 0.01%. UK 10-year yield is down -0.094 at 4.543. Germany 10-year yield is down -0.035 at 2.535. Earlier in Asia, Nikkei rose 0.32%. Hong Kong HSI fell -0.08%. China Shanghai SSE fell -0.44%. Singapore Strait Times fell -0.06%. Japan 10-year JGB yield rose 0.002 to 1.480.

ECB's Villeroy: Favorable 2 and 2 zone is not static

French ECB Governing Council member Francois Villeroy de Galhau said in a conference today that ECB is now in a favorable "2 and 2 zone. That means, inflation is forecast at 2% this year, while deposit rate is also at 2%.

Nevertheless, he warned that with current uncertainties, this zone "does not mean a comfortable zone or a static zone". "We will remain pragmatic and data-driven, and as agile as necessary," Villeroy added.

Separately, Finnish ECB policymaker Olli Rehn warned that as inflation is projected to stay below 2% this year, the central must be mind of "not slipping towards the zero lower bound."

“We must not grow overconfident — instead we must stay vigilant and monitor the risks in both directions,” Rehn said. “The ECB team must remain alert and ready to act with agility as and if needed.”

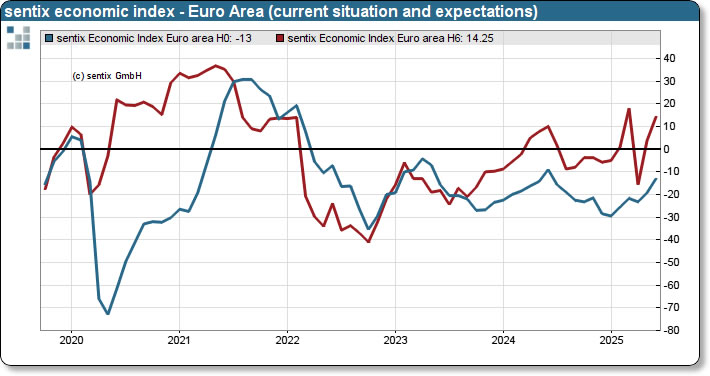

Eurozone Sentix surges back into positive territory, recession fears recede

Investor sentiment in the Eurozone turned notably upbeat in June, as Sentix Investor Confidence index climbed from -8.1 to +0.2—its first positive reading since June 2024 and well above expectations of -6. Current Situation Index also improved markedly from -19.3 to -13.0, while Expectations Index jumped from 3.8 to 14.3.

Germany led the improvement, with its overall Sentix index rising to -5.9, the highest since March 2022. Expectations climbed by 12 points to 17.5, while current conditions advanced for the fourth consecutive month to -26.8.

According to Sentix, fears of a recession triggered by the US tariff shock in April have largely dissipated, and the economic outlook for the Eurozone is now tilted toward a cyclical upswing.

With economic momentum building and the Sentix inflation barometer showing signs of easing price pressures, ECB may view its policy as being in a “comfort zone.” While another rate cut isn’t off the table, any such move could be delayed if the upswing continues to solidify over the summer.

UK labor market softens as unemployment rises to 4.6% and wage growth slows

UK labor market data released today point to gradual cooling. In May, payrolled employment dropped by -109k, or -0.4% mom. Claimant count rose sharply by 33.1k, well above the expected 4.5k increase. Wage pressures are also easing, with median monthly pay rising by 5.8% yoy, down from 6.2% previously, though still within a relatively tight band seen this year.

For the three months to April, unemployment rate ticked up to 4.6% as expected, while both average earnings measures came in softer than forecast. Regular pay (excluding bonuses) rose 5.2% yoy, and total pay increased 5.3% yoy, both under the 5.5% consensus.

BoJ’s Ueda reaffirms gradual tightening path, cites limited room for rate cuts

BoJ Governor Kazuo Ueda reiterated to parliament today that interest rate hikes will continue, though cautiously, once the central bank gains "more conviction that underlying inflation will approach 2% or hover around that level".

Ueda explained that BoJ still maintains negative real interest rates to support inflation momentum and ensure price growth remains both stable and sustained.

However, Ueda also flagged a significant limitation in policy space should economic conditions deteriorate. With the short-term policy rate still only at 0.5%, the BoJ has "limited room" to cut rates in response to any sharp downturn in growth.

Australia's Westpac consumer sentiment edges higher as rate cuts clash with growth worries

Australia's Westpac Consumer Sentiment index rose a modest 0.5% mom in June to 92.6, reflecting a population still mired in what Westpac called a “holding pattern of cautious pessimism.”

The data reveal "two clear opposing forces" shaping household attitudes: easing inflation and RBA’s May rate cut have improved perceptions around major purchases. On the other hand, sluggish domestic growth and global trade uncertainties continue to weigh heavily on expectations.

Looking ahead, attention turns to the RBA’s next meeting on July 7–8. With economic data remaining mixed and labor market tightness still evident, Westpac expects the central bank to proceed with caution and keep the cash rate on hold. Nonetheless, a fresh round of economic projections in August could pave the way for another 25 basis point cut, as RBA recalibrates its stance amid still-sluggish growth.

Australia’s NAB business confidence lifts to 2, but employment conditions erode

Australia’s NAB Business Confidence index turned positive in May, rising from -1 to 2. However, the improvement in confidence was not matched by underlying business conditions, which weakened further. Business Conditions index slipped from 2 to 0, with trading conditions dipping slightly from 6 to 5, profitability remaining in the red at -4, and employment conditions dropping from 4 to 0 — all pointing to a stagnating environment.

On the inflation front, cost indicators presented a mixed picture. Labor cost growth remained firm at a quarterly equivalent pace of 1.7%. Purchase cost and final product price growth eased to 1.1% and 0.5%, respectively. Retail price growth held steady at 1.2%, suggesting persistent margin pressures.

NAB Chief Economist Sally Auld emphasized that business conditions are still weak and warned that continued softness could cap any recovery in confidence. She also flagged the labor market as a key area to monitor, with the employment index now below average.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8419; (P) 0.8424; (R1) 0.8433; More...

EUR/GBP's rebound from resumed by breaking through 0.8448 resistance, and intraday bias is back on the upside for 38.2% retracement of 0.8737 to 0.8354 at 0.8500. Strong resistance could be seen from 0.8500 to complete the corrective bounce. On the downside, break of 0.8413 support will bring retest of 0.8354 low. However, firm break of 0.8500 will pave the way to 61.8% retracement at 0.8591 instead.

In the bigger picture, price actions from 0.8221 medium term bottom are merely forming a corrective pattern. Nevertheless, there is no clear momentum to break through 0.8201 key support (2022 low) yet. Hence, range trading is expected between 0.8221/8737 for now.

ECB’s Villeroy: Favorable 2 and 2 zone is not static

French ECB Governing Council member Francois Villeroy de Galhau said in a conference today that ECB is now in a favorable "2 and 2 zone. That means, inflation is forecast at 2% this year, while deposit rate is also at 2%.

Nevertheless, he warned that with current uncertainties, this zone "does not mean a comfortable zone or a static zone". "We will remain pragmatic and data-driven, and as agile as necessary," Villeroy added.

Separately, Finnish ECB policymaker Olli Rehn warned that as inflation is projected to stay below 2% this year, the central must be mind of "not slipping towards the zero lower bound."

“We must not grow overconfident — instead we must stay vigilant and monitor the risks in both directions,” Rehn said. “The ECB team must remain alert and ready to act with agility as and if needed.”

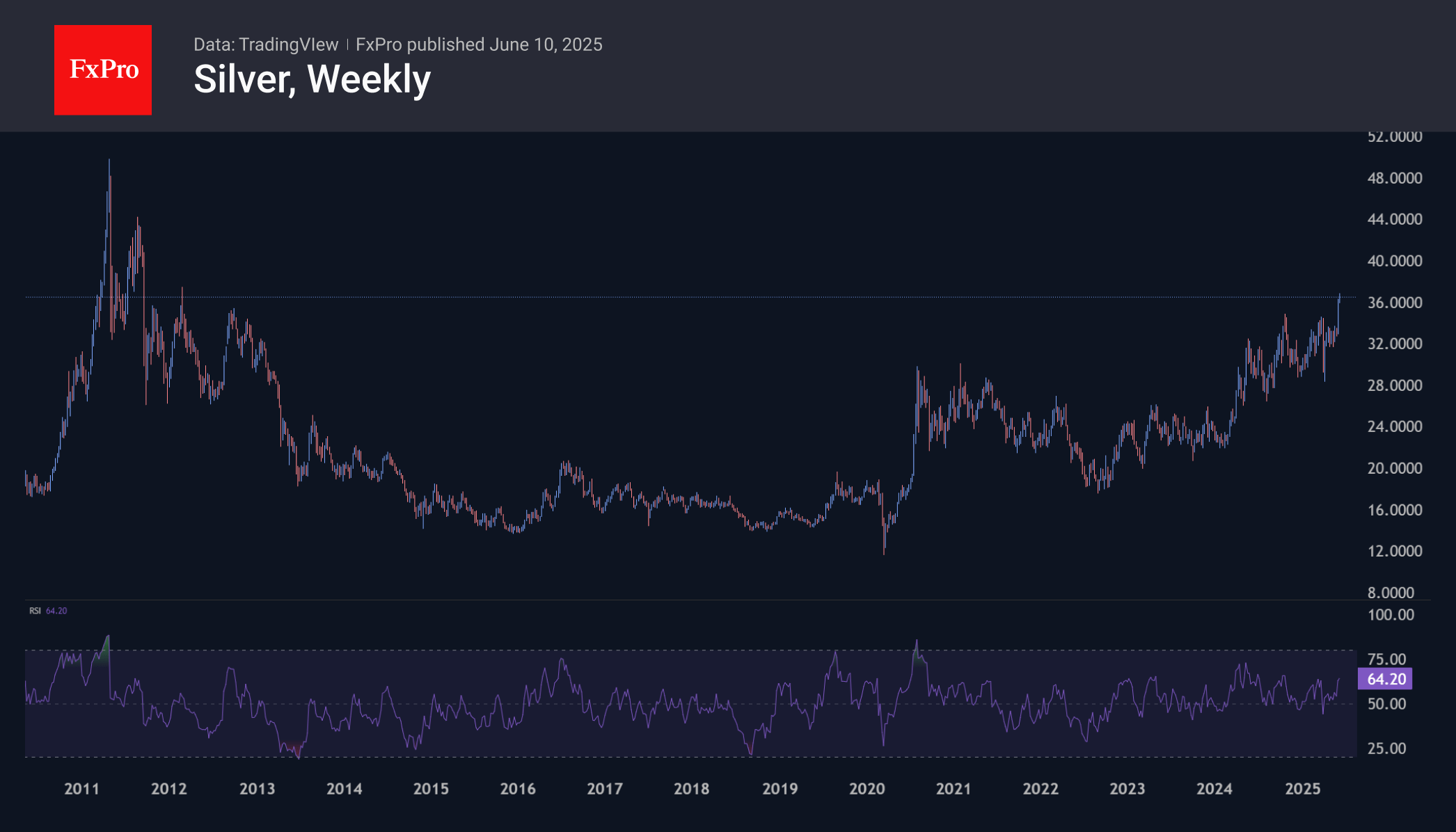

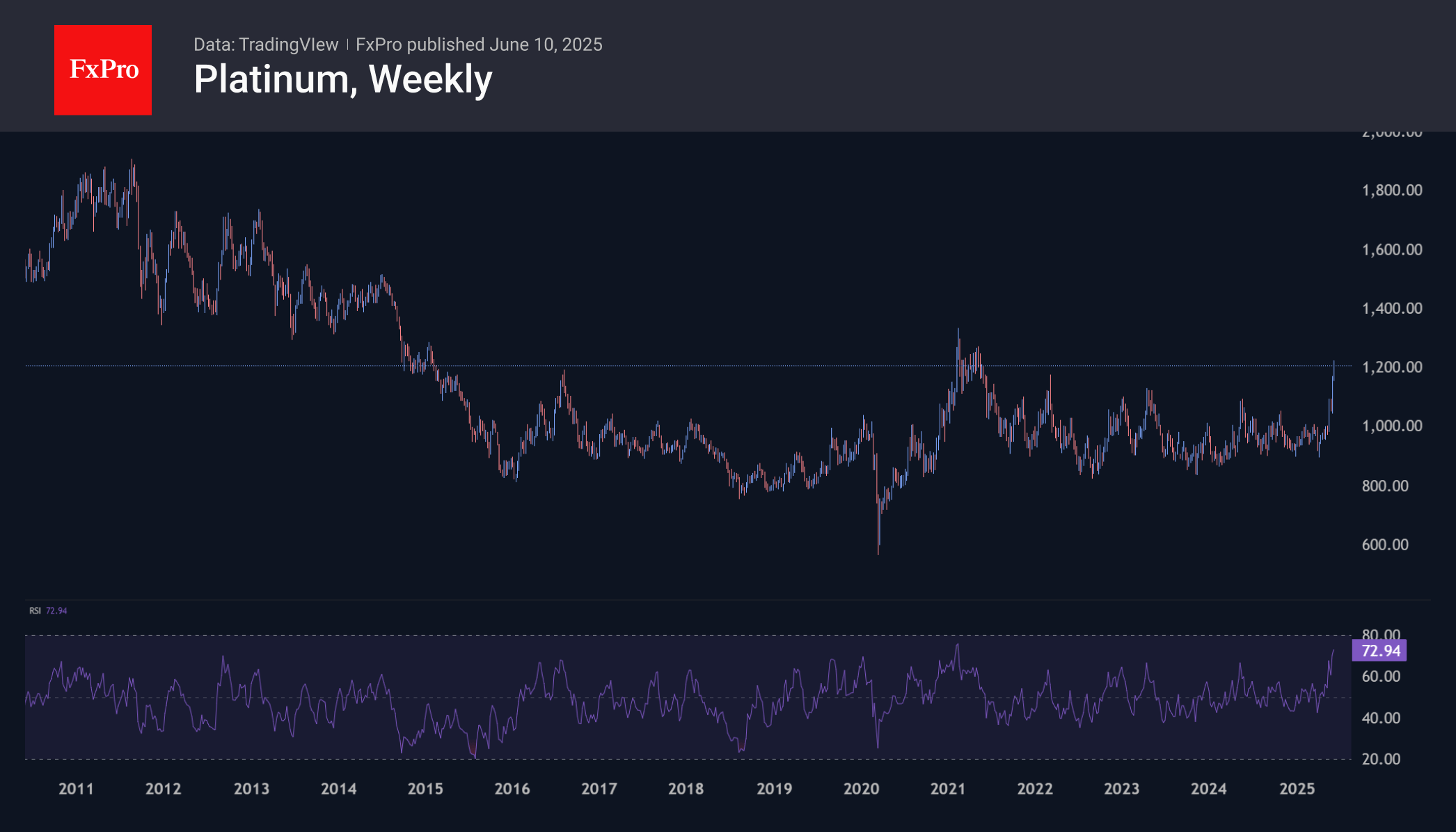

Silver and Platinum Ready to Rally Further

While gold prices remain heated and volatile at the top, its precious counterparts—silver and platinum—are attracting bullish interest and surging toward multi-year highs.

Platinum has gained about 35% from its lows at the beginning of the year at $900, reaching $1,225 at the start of the day on Tuesday. The latest rally brought the price back to the 2021 highs, ending a three-year sideways trend. Bulls intensified their push after successfully breaking through the $1,000 level in the middle of last month.

Silver is up 27% since the beginning of the year, accelerating its growth in the last couple of weeks after an 18% correction in early April. With the price reaching $36.9 on Monday, silver is trading at its highest level since February 2012.

In both cases, bulls were encouraged by the rapid correction in gold, which did not turn into a prolonged decline. This was a signal that gold was seeing profit-taking rather than a reversal of sentiment. In such conditions, traders look for alternatives. Since the platinum and silver markets are less liquid, price movements here are usually more significant.

In 2011, the silver rally pushed the price from less than $18 to almost $50. If the momentum that has been driving precious metals since the beginning of the year continues, bulls may aim to repeat the peaks of fifteen years ago or even try to exceed them. On weekly timeframes, silver is not overheated, with an RSI of 64. In 2011 and 2018–2019, only an RSI above 80 was a signal for a reversal.

Platinum has fallen sharply in recent years, falling out of focus for investors as the automotive industry has sought to move away from internal combustion engines, where platinum is actively used. In recent weeks, however, platinum has emerged as an alternative to gold as a metal for gold reserves. However, it has yet to prove its potential. The 2021 turning point is in the $1,200–1,300 range. Successfully overcoming this resistance level opens the way to $1,500 and then $1,900, which, in a bullish scenario, could well be reached by the end of the year.

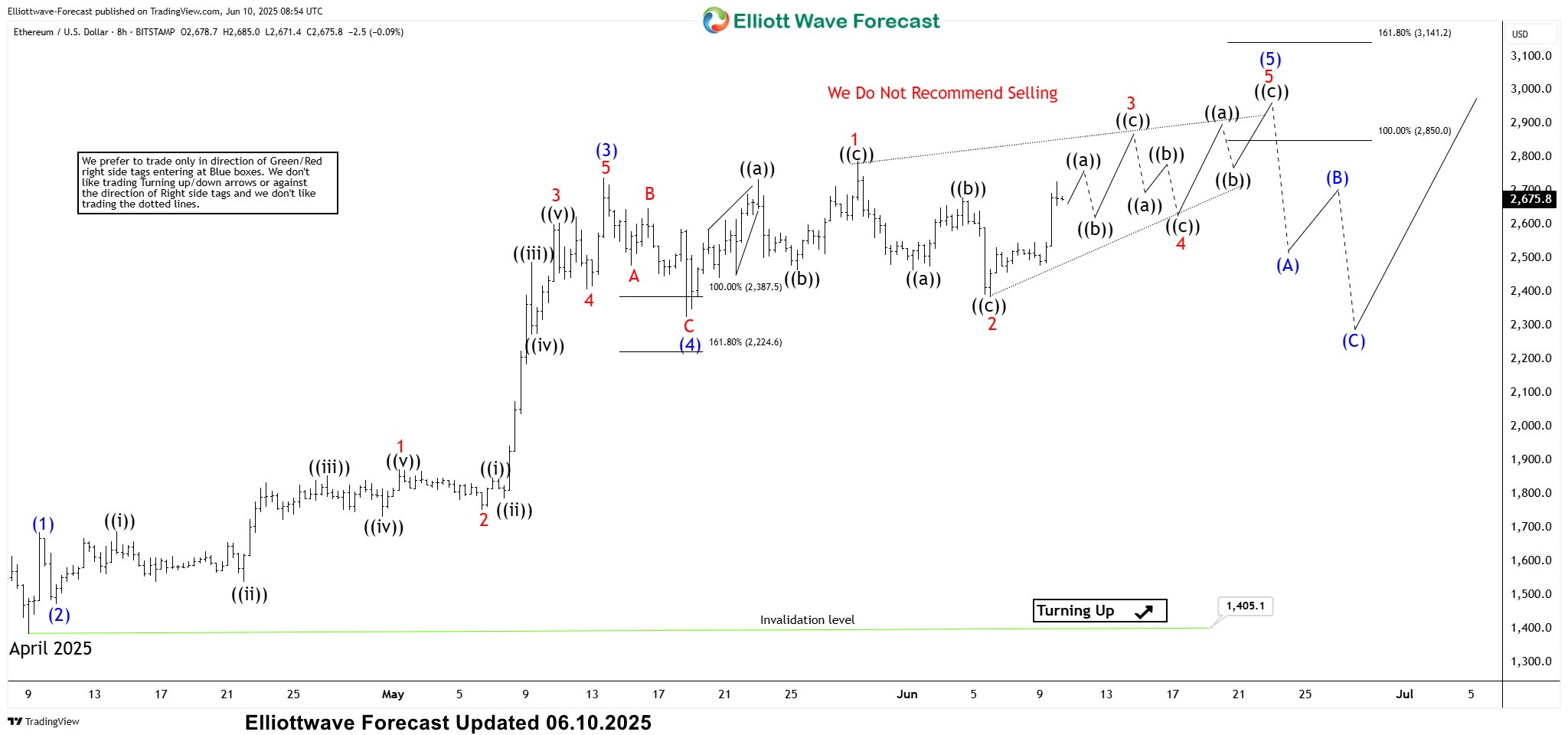

Ethereum Showing An Impulsive Rally Since April 2025 Low

In this article, we will take a look at Ethereum. We can see that Cryptocurrencies formed a major low back in April 2025 and have been rallying since then. Some have rallied more than others and we see Bitcoin even made a new all time high already. ETHUSD, on the other hand, has not yet made a new high above it’s December 2024 peak but it has nearly doubled since forming a low back on April 7, 2025 rallying from $1385 to $2789. It is currently trading at $2674 and is attempting to break above the earlier peak of $2789. Today, we will take a look at the structure of the rally from April 7, 2025 low and try to determine the next move in the cryptocurrency.

Ethereum (ETHUSD) 8 Hour Elliott Wave Chart June 10, 2025

Above chart shows current rally is clearly impulsive with clear separation and extension in wave 3. Wave (1) ended at $1687.2, wave (2) completed at $1473. Wave 1 of 3 completed at $1873.2 wave 2 of (3) completed at $1753.2, this followed by a strong rally in wave 3 which ended at $2606.5, this was followed by an irregular wave 4 which ended at $2407.5 and then a new high in wave 5 to $2738.9 which completed wave (3) of the on-going impulse Elliott wave structure. Then, we saw a 3 waves pull back in wave (4) which was expected to complete between $2387.5 – $2224.6 which was 100 – 161.8 fib extension area of wave A related to wave B. Wave (4) competed at $2325 and the rally resumed in wave (5). We have already seen a new high above wave (3) peak but the new high was in 3 waves which is part of a corrective sequence. Since wave (5) should be an impulse so it can’t have a corrective sequence. We considered the possibility of a FLAT in wave (4) but the decline was also left in 3 waves and Ethereum rally is getting closer to the previous peak due to which we are considering the possibility of an Ending diagonal structure in wave (5) when we are currently in wave 3 of (5). 100 – 161.8 fibonacci extension area of wave 1 related to wave 2 comes between $2850 – $3141 from where we can see a pull back in wave 4 followed by another 3 swings higher to complete the ending diagonal wave (5) and impulsive rally from April 7, 2025 low. Afterwards, expect a larger 3 waves pull back to correct the cycle from April 7, 2025 low before the rally resumes.

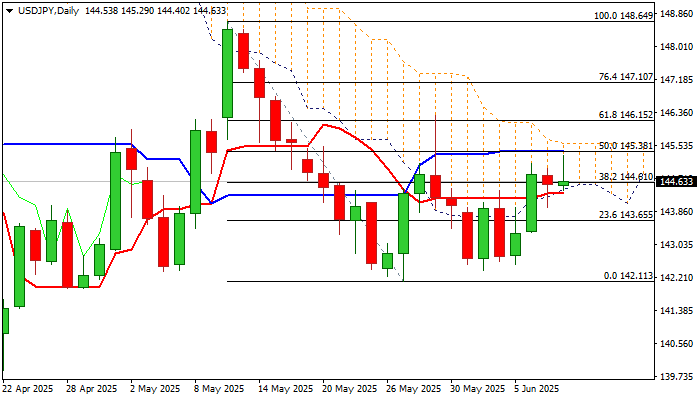

USD/JPY: Near Term Action Looks for Direction Signals on Break of Either Daily Cloud Boundary

USD/JPY ranges within daily cloud (144.43/145.59) also between daily Tenkan and Kijun-sen lines, with Kijun-sen (145.38) capping the action today.

Near term technical structure is slightly bullishly aligned, with growing positive momentum and repeated close above Tenkan-sen supporting the notion.

On the other hand, overbought stochastic might be limiting factor that partially offsets positive signals.

Sideways near-term mode to be expected as long as price holds within the cloud, as strong downside rejection on Monday and upside rejection today supports scenario.

Firmer direction signals to be expected on clear break of either boundary of daily cloud, with dollar being underpinned by optimism on US China trade talks, though support was so far insufficient for stronger movements.

Markets await release of US inflation data this week, to get more clues about Fed’s action in the near future.

Signals that Bank of Japan will keep its monetary policy unchanged in the meeting next week, could be initial negative signal for yen.

Sustained break below cloud base / daily Tenkan to weaken near term structure and risk test of supports at 143.65/00 and 142.40 on stronger acceleration.

Conversely, firm break of cloud top to generate bullish signal and expose targets at 146.15/38 (Fibo 61.8% of 148.64/142.11 / May 29 spike high).

Res: 145.29; 145.59; 146.15; 146.38.

Sup: 144.33; 143.65; 143.00; 142.40.

Gold Under Pressure Again as Risk Appetite Improves

The price of gold declined to 3,307 USD per troy ounce on Tuesday as investor appetite for risk increased amid growing optimism over a potential de-escalation in US-China trade tensions.

Trade optimism weakens demand for safe-haven assets

The improvement in market sentiment stems from the high-level trade talks between the US and China, which began in London on Monday and continue today. Both sides are working to stabilise a fragile truce, with discussions now extending beyond tariffs to include strategic materials such as rare earth elements.

US Treasury Secretary Scott Bessent described Monday’s session as “a good meeting”, while Commerce Secretary Howard Lutnick called the talks “fruitful”. These positive signals are fuelling hopes for a normalisation of relations between the world’s two largest economies, thereby reducing the appeal of defensive assets like gold.

Investors are also closely watching upcoming US inflation reports, which will include both consumer and producer price indices. These data points could provide crucial insight into the Federal Reserve’s future monetary policy stance.

Meanwhile, a survey by the Federal Reserve Bank of New York, released on Monday, showed that Americans’ inflation expectations declined in May while confidence in personal finances improved, adding to the overall risk-on sentiment.

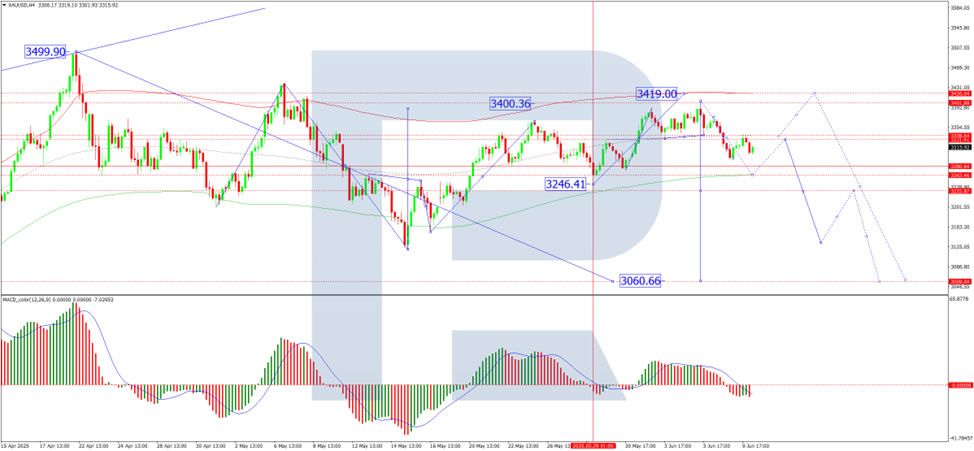

Technical analysis of XAU/USD

On the H4 chart, XAU/USD is developing a corrective structure targeting 3,263 USD. Once this correction is complete, a new upward wave towards 3,419 USD is expected. The MACD indicator supports this view, with its signal line positioned below zero and pointing sharply downwards, indicating a short-term bearish phase within a broader bullish setup.

On the H1 chart, the market formed a consolidation range around 3,331 USD, then broke downwards, reaching the local target at 3,294 USD. A subsequent correction to 3,333 USD has now been fulfilled. Today, the development of a fifth-wave structure is anticipated to reach 3,263 USD. Following this move, gold is expected to resume its growth towards 3,419 USD. The Stochastic oscillator confirms the current outlook, with its signal line below 50 and heading sharply towards 20, signalling continued downward momentum in the short term.

Conclusion

Gold remains under pressure as improving geopolitical sentiment and a better economic outlook dampen demand for safe-haven assets. Near-term technicals indicate further downside towards 3,263 USD, followed by a potential bullish reversal targeting 3,419 USD. Key drivers in the coming sessions will include US inflation data and progress in the US-China trade negotiations.

Eurozone Sentix surges back into positive territory, recession fears recede

Investor sentiment in the Eurozone turned notably upbeat in June, as Sentix Investor Confidence index climbed from -8.1 to +0.2—its first positive reading since June 2024 and well above expectations of -6. Current Situation Index also improved markedly from -19.3 to -13.0, while Expectations Index jumped from 3.8 to 14.3.

Germany led the improvement, with its overall Sentix index rising to -5.9, the highest since March 2022. Expectations climbed by 12 points to 17.5, while current conditions advanced for the fourth consecutive month to -26.8.

According to Sentix, fears of a recession triggered by the US tariff shock in April have largely dissipated, and the economic outlook for the Eurozone is now tilted toward a cyclical upswing.

With economic momentum building and the Sentix inflation barometer showing signs of easing price pressures, ECB may view its policy as being in a “comfort zone.” While another rate cut isn’t off the table, any such move could be delayed if the upswing continues to solidify over the summer.

FTSE 100 Surges Towards Record High

Today saw the release of new data on the UK labour market.

According to official statistics, the number of payrolled employees in the UK fell by 55,000 (0.2%) between March and April 2025. Over the broader period from February to April 2025, the number declined by 78,000 (0.3%).

In response to the drop in employment, the UK’s FTSE 100 index (UK 100 on FXOpen) jumped sharply, rising close to the 8,900 mark — near its all-time high reached in early March this year.

Market participants likely interpreted the weakening labour market as an additional argument in favour of interest rate cuts by the Bank of England. Such a move would be seen as supportive of the economy and a bullish factor for equities.

Technical Analysis of the FTSE 100 (UK 100 on FXOpen)

From a technical perspective:

→ The FTSE 100 continues to trade within an ascending channel (shown in blue);

→ Today’s bullish momentum broke through the resistance line from below — a level that had previously capped the upward movement within the channel.

If the bulls can maintain the price above the 8,860 level, the likelihood increases for a continued uptrend and a potential new all-time high for the FTSE 100 index.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

XBR/USD Chart Analysis: Brent Crude Reaches 1.5-Month High

In our analysis of Brent crude oil six days ago, we identified a large contracting triangle and a local ascending channel. We also outlined a potential scenario involving a bullish breakout above the upper boundary of the triangle.

Although this was not the base-case scenario, the XBR/USD chart now suggests it has played out: yesterday, the price climbed to nearly $67 per barrel — its highest level since the end of April.

The main bullish catalyst appears to be ongoing trade talks between the United States and China, which have raised hopes of a resolution to tariff-related tensions between the world’s two largest economies.

At the same time, rising oil prices may exacerbate geopolitical tensions, particularly amid Israeli threats to strike ports in Yemen — a risk that could disrupt supply chains across the Middle East.

Technical Analysis of the XBR/USD Chart

From a technical perspective:

→ Brent crude continues to move within an ascending channel (marked in blue);

→ the upper boundary may now act as a support level.

The fact that the price is holding in the upper half of the channel indicates strong demand-side pressure. Based on this, it is reasonable to assume that as long as Brent remains above the $65.75 level (the retest zone of the breakout), the technical outlook will remain predominantly bullish.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.