Sample Category Title

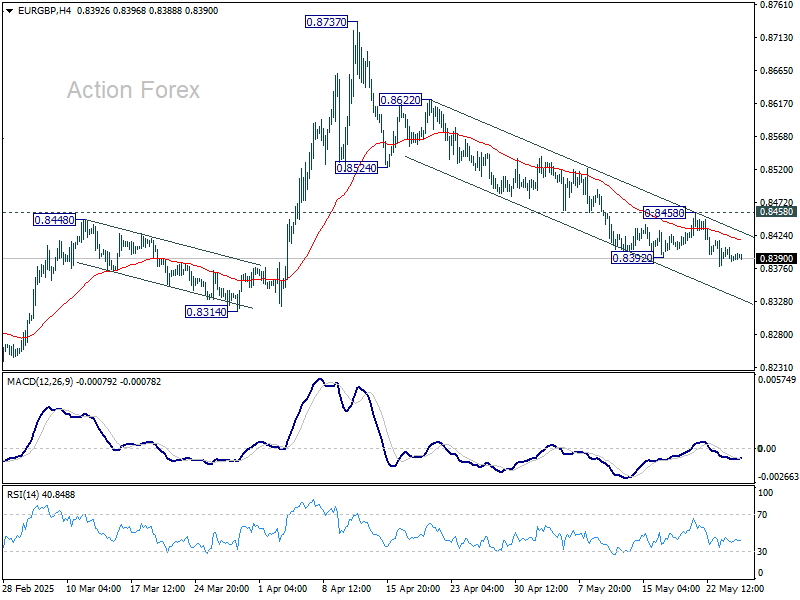

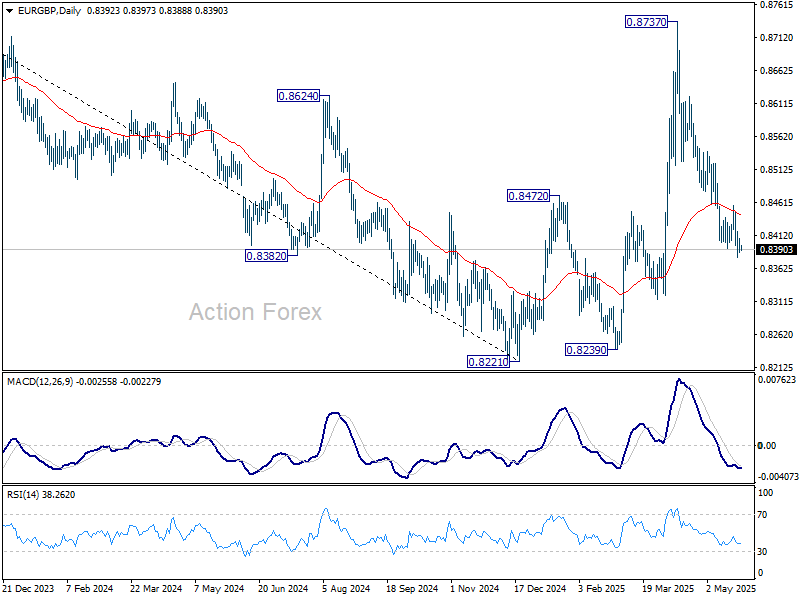

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8386; (P) 0.8397; (R1) 0.8407; More...

Intraday bias in EUR/GBP remains on the downside at this point. Decline from 0.8737 should target 0.8314 support first, and then 0.8239 low. On the upside, above 0.8458 resistance should indicate short term bottoming, likely with bullish convergence condition in 4H MACD, and turn bias back to the upside for stronger rebound.

In the bigger picture, current development suggests that price actions from 0.8221 medium term bottom are merely forming a corrective pattern. However, there is no clear momentum to break through 0.8201 key support (2022 low) yet. Hence, range trading is expected between 0.8221/8737 for now.

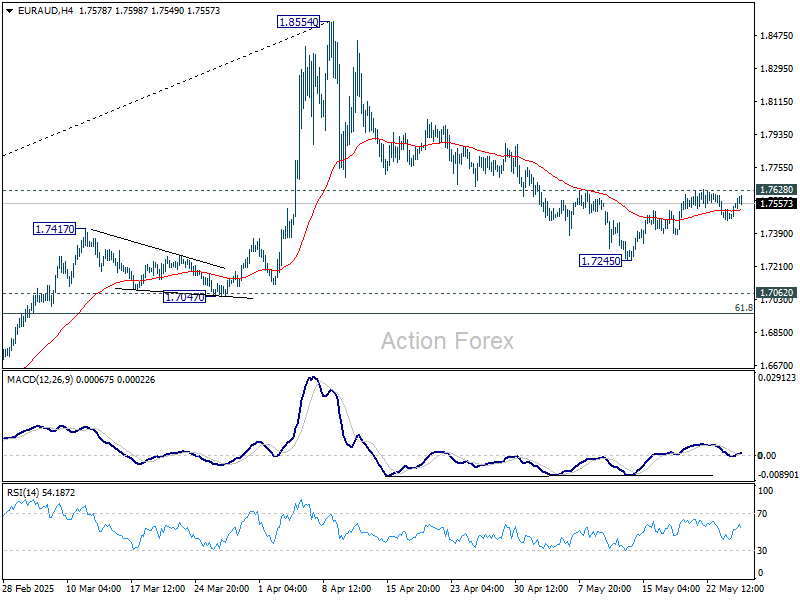

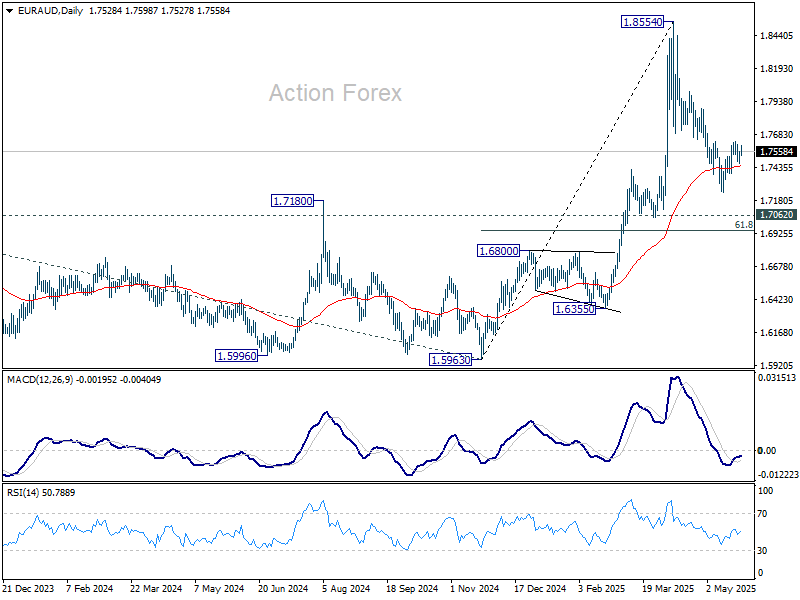

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7491; (P) 1.7525; (R1) 1.7585; More...

Intraday bias in EUR/AUD remains neutral for the moment. On the upside, firm break of 1.7628 resistance will suggest that fall from 1.8554 as completed as a correction, and retain larger bullishness. Intraday bias will be back on the upside for stronger rebound. However, below 1.7245 will resume the fall to 61.8% retracement of 1.5963 to 1.8554 at 1.6953.

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from 1.4281 (2022 low) should still be in progress. Break of 1.8554 will target 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. However, sustained break of 1.7062 will confirm medium term topping and bring deeper fall back to 1.5963 support.

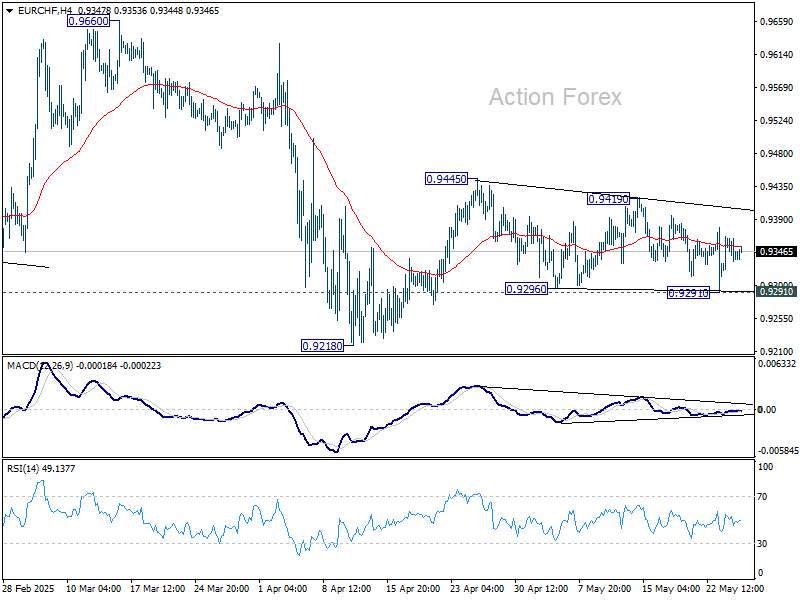

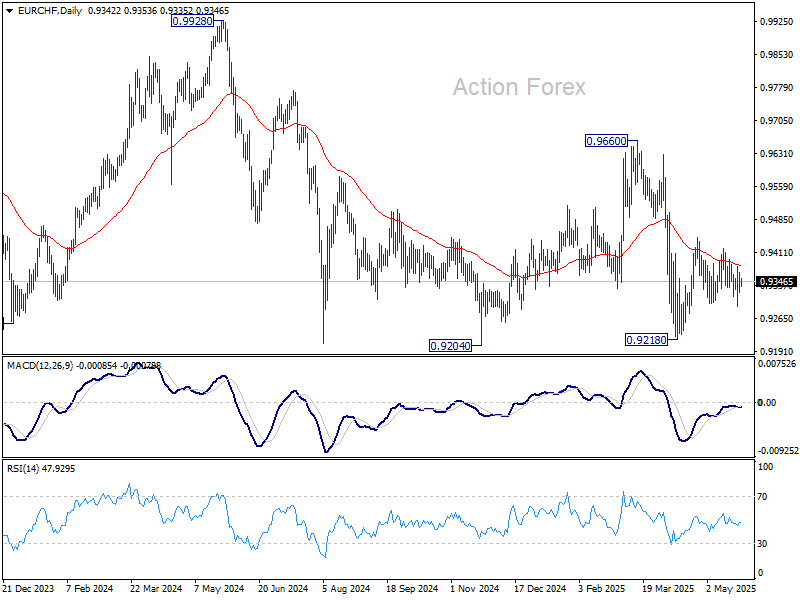

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9326; (P) 0.9347; (R1) 0.9369; More....

Sideway trading continues in EUR/CHF and intraday bias remains neutral. Price actions from 0.9218 are seen as either a corrective move or the third leg of the pattern from 0.9204. On the upside, break of 0.9419 will resume the rise from 0.9218 through 0.9445 resistance. However, firm break of 0.9291 support will bring retest of 0.9218 low.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9548) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

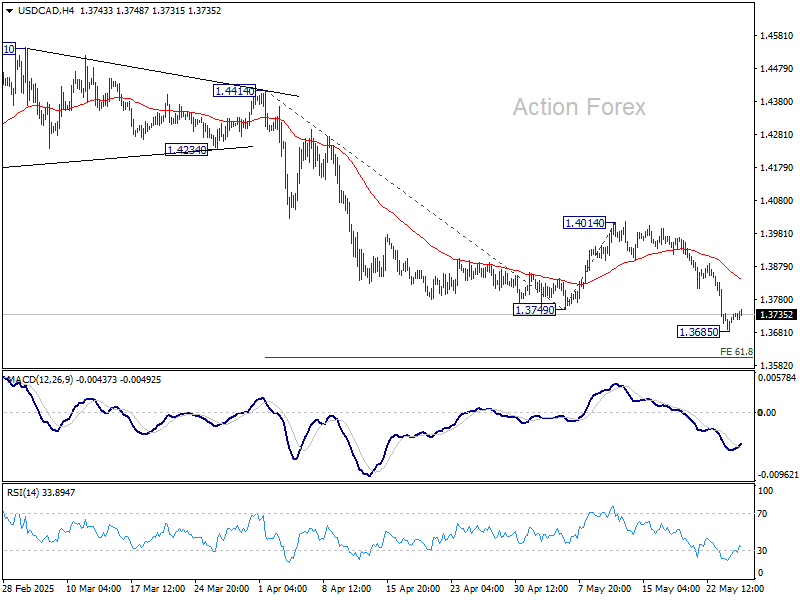

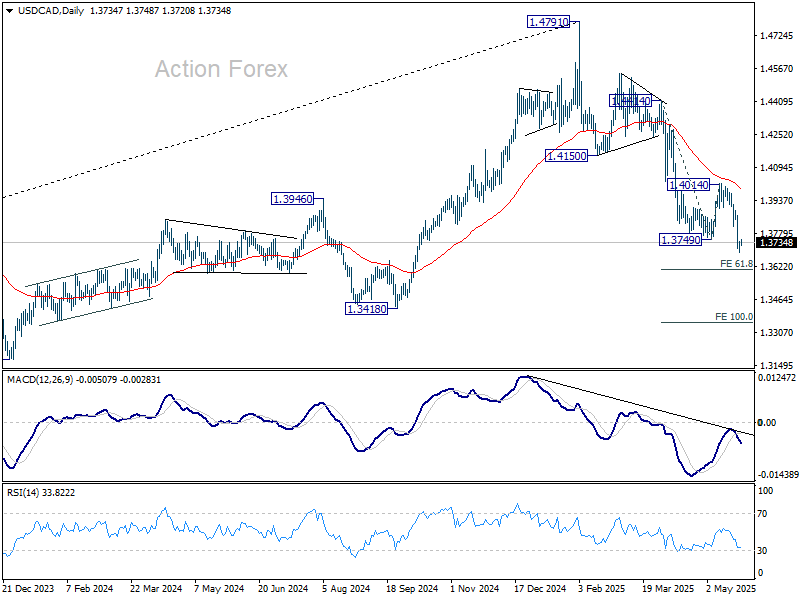

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3673; (P) 1.3771; (R1) 1.3832; More...

Intraday bias in USD/CAD Is turned neutral first with current recovery, and some consolidations would be seen above 1.3685 temporary low. Upside should be limited well below 1.4014 resistance to bring another fall. Below 1.3685 will resume the decline from 1.4791 and target 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

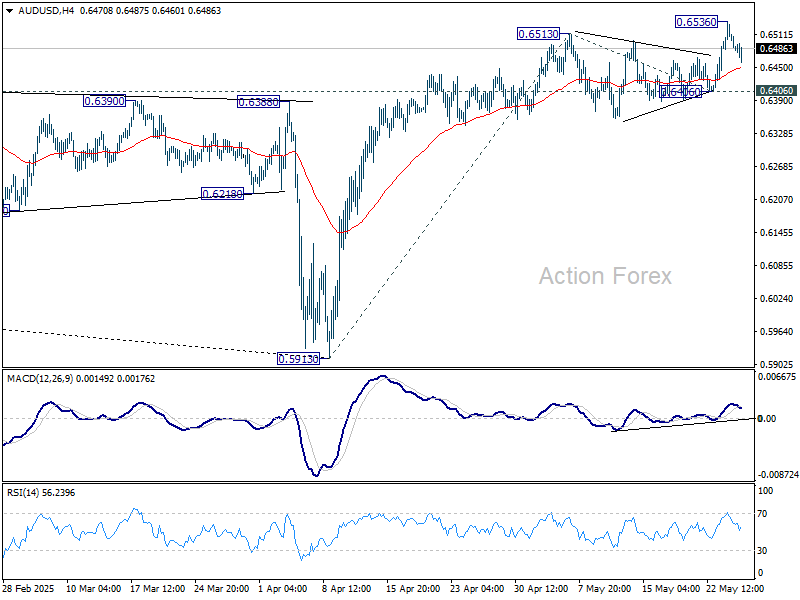

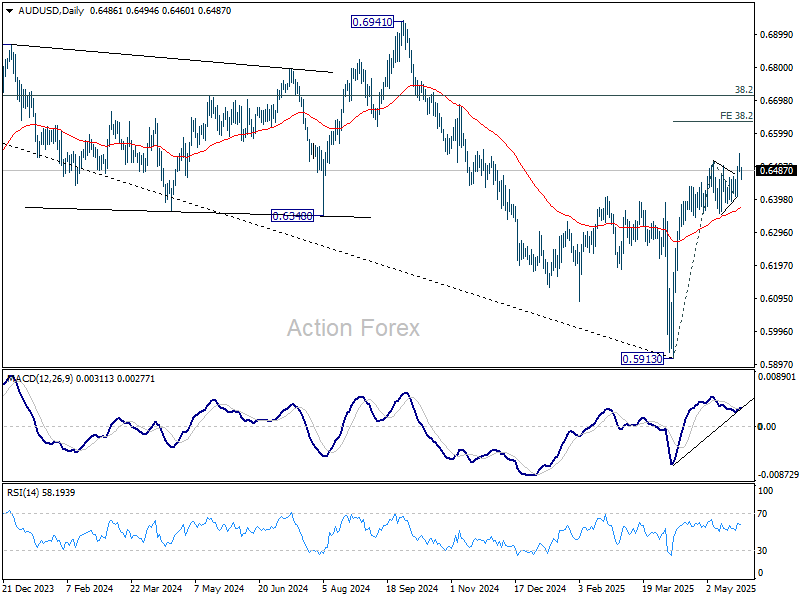

AUD/USD Daily Report

Daily Pivots: (S1) 0.6468; (P) 0.6502; (R1) 0.6523; More...

AUD/USD retreated after edging higher to 0.6536 and intraday bias is turned neutral again first. Outlook will stay bullish as long as 0.6406 support holds. Break of 0.6536 will resume the rally from 0.5913 to 38.2% projection of 0.5913 to 0.6513 from 0.6406 at 0.6635.

In the bigger picture, 55 W EMA (now at 0.6439) is considered taken out. A medium term bottom should already be in place at 0.5913. Rise from there could either be a corrective move, or reversing whole down trend from 0.8006 (2021 high). In either case, further rise is now expected as long as 55 D EMA (now at 0.6372) holds. Next target is 38.2% retracement of 0.8006 to 0.5913 at 0.6713.

The Single Currency Has a New Poster Girl

Markets

The single currency has a new poster girl. ECB President Lagarde picked her moment. In absence of UK and US investors, she pulled maximum attention with a speech on Europe’s role in a fragmented world. Foundations that seemed unshakeable begin to shift and create the opening for “a global euro moment”. Which has to be earned of course. Current fracturing of the global order caused by the US trade strategy poses short-term economic risks for Europe with exports accounting for close to one fifth of added value. Long term, there could be opportunities with the change landscape questioning the dominant role of the dollar, opening the door for the euro to play a greater international role. In past experiences of shifts in the global FX landscape (suspension of gold convertibility or ending Bretton Woods), a decline in the standing of the dollar pushed investors into gold as on neither occasion, there was a robust alternative currency to take over at short notice. Lagarde points out that things are different now with the euro currently already accounting for 20% of global FX reserves compared with 58% (lowest since 1994) in the case of the US dollar. Investors aren’t convinced yet though, as the share of gold in global FX reserves recently started increasing again, also reaching 20%. For the euro to become cornerstone of the financial system, Europe must first ensure it has a solid and credible geopolitical foundation by maintaining a steadfast commitment to open trade and underpinning it with security capabilities. Lagarde sports the EU’s largest network of trade agreements in the world with the single currency used as invoice currency in around 40% of global trade. The ECB can help the euro’s attractiveness by working on a potential digital euro, pursuing initiatives to enhance cross-border payments in euro And by extending swap and repo lines to key partners. Usage in trade needs to go hand in hand with robust military partnerships. The current USD dominance is not just a product of economic fundamentals, but it is powerfully reinforced by US security guarantees. Investors like assets in regions that can honour alliances with hard power. A major shift on this military part is currently under way in Europe. Second, Europe must reinforce its economic foundation to make Europe a top destination for global capital, enabled by deeper and more liquid capital markets. Simply put: Europe needs a more liquid supply of safe assets to invest in. Lagarde refers to the competitiveness report from her predecessor, Draghi, and warns for self-defeating fragmentation. Economic logic tells us that public goods need to be jointly financed. And this joint financing could provide the basis for Europe to gradually increase its supply of safe assets. Finally, Europe must bolster its legal foundation by defending the rule of law – and by uniting politically so that we can resist external pressures. While Europe can improve by dropping single veto voting systems, she especially takes a swing at the US here by pointing out that investors have significant doubts on the stability of the US legal and institutional framework as witnessed by the highly unusual simulataneaous sell-off in USD, US treasuries and US stocks after “Liberation Day”. Increasing the international role of the euro can have several positive implications for the euro area. It would allow EU governments and businesses to borrow at lower cost, helping boost internal demand when external demand is becoming less certain. It would insulate from FX fluctuations, protecting Europe from more volatile capital flows and it would protect Europe from sanctions or other coercive measures.

News & Views

The head of the UK’s Debt Management Office (DMO) told the Financial Times that the agency is shifting to shorter-term borrowing. The average maturity of UK debt is around 14 years. That’s significantly higher than the US’ +/- 6 years and longer than most other government bond markets. But UK (and global) long-term bond yields are at elevated levels over fiscal concerns and amid waning demand from institutional investors, the pension industry in particular. The UK 30-yr yield hit the highest level since 1998 last week. This is threatening the government compliance to its self-imposed fiscal rules. Chancellor Reeves resultingly tweaked them in the autumn budget of 2024, was forced to cut spending and raise taxes in the spring update of 2025 and will most likely face the issue again in the 2025 autumn budget.

Rallies on Thin Ice

The week started on a slow but hopeful note for European markets, with expectations that Trump’s latest 50% tariff threat on European imports would accelerate negotiations. And that’s what the latest headlines suggest. As a result, the Stoxx 600 rebounded around 1% yesterday, the DAX led gains with a 1.68% advance, the CAC added 1.21%, while the Swiss SMI index also gained 1.21%—on echoes that Switzerland could also ink a deal with the US in the coming weeks – a deal that would bring the 30% tariff rate down to 10%

So, yes, that market optimism fascinates me! European markets are flirting with ATH levels, US futures were also up yesterday, but the reality is that with every piece of incoming information, the collective welfare deteriorates. Today, we are in a worse position than we were a month ago. And a month ago, we were in a worse position than we were three months ago. The global trade negotiation period was supposed to last 90 days, and now, it ends all of a sudden. The tariffs won’t be brought below the 10% ‘universal’ level and market rallies are triggered not by good news, but by the least bad of the options, once Trump or his administration softens a previously crazy stance. Oh well...

Moving forward, fresh deals between the US and major trade partners could further boost market sentiment and send indices on both sides of the Atlantic to fresh ATH levels—but whether that optimism lasts is yet to be seen. The economic data, especially the inflation metrics, will be crucial.

FX rates are crucial for equity valuations, as well, provided that they have a direct impact on companies’ costs and revenues. They reflect monetary policy, and/or they influence policy decisions—hence borrowing costs. As such, European Central Bank (ECB) Chief Lagarde believes that the turmoil in the US dollar and US bonds could strengthen the euro’s position as a reserve currency. The latter would increase sovereign bond demand for the euro area. That additional demand could help lower borrowing costs on top of the ECB’s supportive policy, and help European companies secure cheaper funding. Then, it will be up to the European companies to move and innovate, and up to the European regulators to let them do so.

The US dollar, on the other hand, is better bid this morning, but remains under pressure from trade tensions and the worsening perception of the US’s ballooning debt.

The debt issues are also making the headlines in Japan. The 30- and 40-year JGB yields have recently spiked to the highest levels on record, and the 10-year yield hit the highest since 2009. Political pushes for tax cuts and spending hikes are refocusing investor attention on fiscal cracks, just as the Bank of Japan (BoJ) looks willing to slow purchases and tighten monetary policy. And when you think that the BoJ holds almost half of the outstanding 10-year debt, the fallout could hurt.

On the other hand, higher yields will attract Japanese investors, especially the institutional ones, back to Japanese markets, partly by dumping their UST holdings. That could put further pressure on US debt and weigh further on the dollar. The USDJPY rebounded near 142 on the back of a sudden retreat in Japanese yields before a 40-year auction and a certain rebound in the US dollar—but the trend remains in favour of the Japanese yen.

As per the Japanese bonds, liquidity remains poor in the JGB space, and I’d rather prefer German bonds for diversifying US exposure.

Still in Asia, the latest data revealed that Chinese industrial profits rose 1.4% y/y in the first four months of the year—up from a 0.8% advance in Jan–Mar, thanks to policy support. On the trade front, there’s no fresh news about the US-China trade negotiations, but there is progress on the China-EU front, as policymakers are willing to respond and tame the impact of the deterioration of their relations with the US. The CSI 300 is breaking below the 50-DMA despite encouraging data, while the HSI is retreating from the May peak. On the individual front, BYD dropped almost 15% since last Friday’s peak following reports of significant price cuts in a promotional campaign, raising concerns about margin pressure. But the move showcases the strength of demand as BYD sales accelerate at an impressive speed globally. Therefore, price pullbacks are interesting opportunities to enter—or to strengthen—existing positions.

All Eyes on US Consumer Confidence

In focus today

From the US, Conference Board's May consumer confidence survey is due for release in the afternoon. Another preliminary survey from the University of Michigan released earlier pointed towards further weakening in consumer sentiment in early May. That said, Conference Board's surveys' cut-off date is typically around a week later, so we will follow if the US-China trade deal managed to improve consumers' mood.

In the euro area, focus turns to the French inflation data for May. As French inflation has been very low since February due to a publicly related lowering of electricity prices, focus will mainly be on the m/m increases as predictors of the euro area data.

In Sweden, the NIER survey released at 09:00 CET may shed further light on both household sentiment (which we expect to recover) and companies' price plans. While price plans have mainly been elevated due to retail trade and especially by non-durables, it still poses as an upside risk to inflation and should be a concern for the Riksbank. A clear easing in the price plans would be needed to make the case a bit stronger for the Riksbank to ease policy. Additionally, Riksbank board member Per Jansson gives a speech at 08:30-09:30 CET, potentially commenting on the fresh data.

In Hungary, the central bank will announce its policy rate. The market consensus is a for an unchanged decision, with the policy rate kept at 6.50%.

Overnight, the Reserve Bank of New Zealand will have a monetary policy meeting. In line with markets, we expect a 25bp cut to the Official Cash Rate (to 3.25%).

Economic and market news

What happened overnight

In China, industrial profit for the January-April period ticked up 1.4% y/y (January-March: 0.8% y/y), reflecting economic resilience in the face of pressure from trade tensions with the US and lingering deflationary pressures domestically. In isolation, April alone was up 3.0% y/y compared to 2.6% y/y in March. The increase in profits was driven by a government trade-in program that boosted demand for manufactured products.

In Japan, while the BoJ projects that the effects of food inflation will wane, BoJ Governor Ueda emphasized that the central bank should be "careful about how food price inflation will impact underlying inflation" with underlying inflation nearing 2%. Ueda also added that the BoJ continues to expect underlying inflation to gradually move toward 2% over the second half of its forecast horizon, and that the BoJ will "adjust the degree of monetary easing as needed." Currently, the BoJ is expected to stay on hold at its meeting on 17 June. We believe the next BoJ hike is most likely to occur in October this year, followed by a potential additional hike in Q1 2026.

What happened yesterday

In Sweden, PPI for April stood at -1.6% m/m (-2.4% y/y), compared to -3.0% m/m and -0.3% y/y in March, marking the largest decline yearly in 16 months. Electricity prices served as the main driver behind the decrease.

Equities: The tariff induced round trips in equities are truly remarkable. Equities recouped most of the tariff threat losses already Friday and amid the tariff pause on Sunday, equities rallied yesterday. This means that European equities have fully recovered to where they were before the 50% tariff threat. For the stock market, nothing has really happened. After multiple threats by the US administration that have ultimately not been carried out, markets are no longer taking them at face value.

European markets were in risk-on yesterday while the US market was closed for holiday, with Stoxx 600 up 1% (German DAX up 1.7%). Unlike past sessions, this was not a large cap cyclical rally. Instead, investors looked outside the usual bets for new sources of risk: Growth stocks and small-cap stocks. It is a long time since we saw such preference in equity markets. While interesting to observe after years of underperformance, we do not style mix it to be particularly long lasting, given the upward pressure on long-end yields.

FI & FX: EUR/USD continue to experience upwards pressure and traded close to 1.14 yesterday. SEK and NOK held on to recent gains vis-à-vis the EUR on an otherwise quiet day in FX markets. Long-end EUR yields dropped slightly yesterday despite some relief on the tariff front as the market digested the decision by US to postpone the 50% tariff on the EU announced on Friday. Oil market did not react on OPEC+'s call to move its coming meeting, where it will decide on another output hike, forward one day to 31 May.

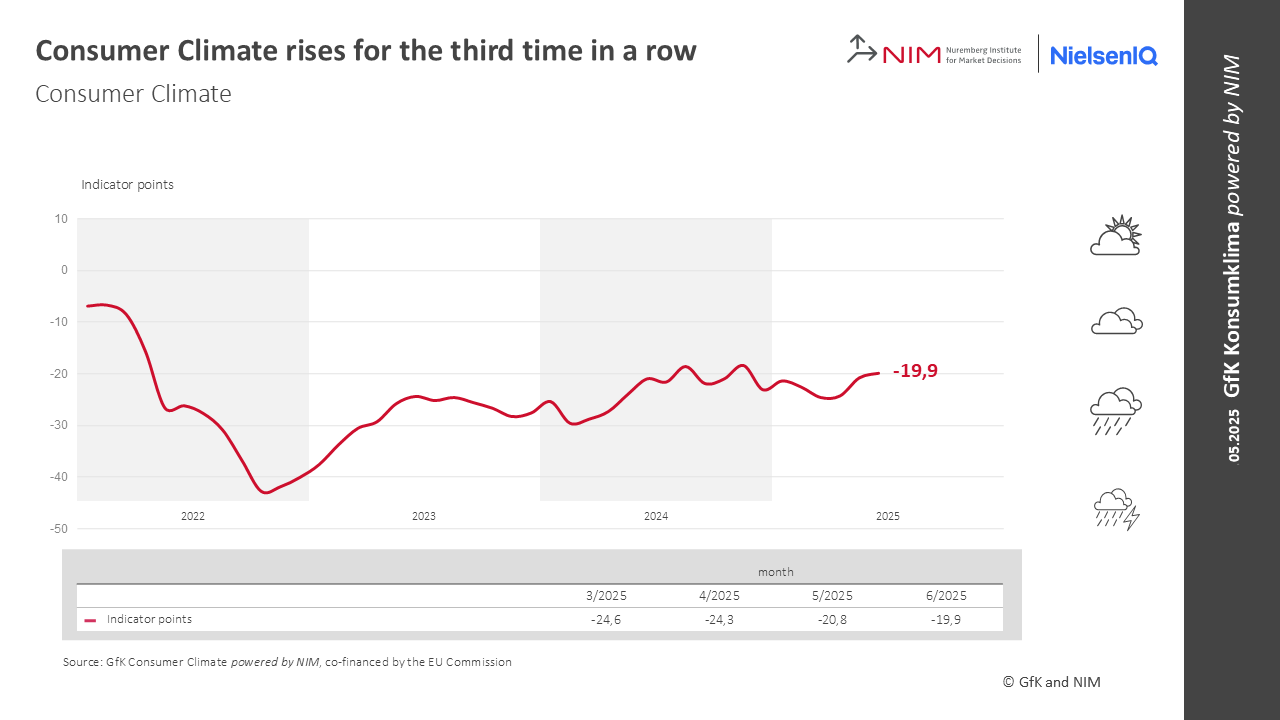

German Gfk consumer sentiment edges higher to -19.9, mood remains extremely low

Germany’s GfK Consumer Sentiment rose for the third straight month, reaching -19.9 in June, its highest reading since November 2024, but slightly below expectations of -19.7. In May, income expectations surged 6.1 pts to 10.4, the best since October last year. Economic expectations climbed 2.9 pts to 13.1, their highest since April 2023.

According to Rolf Bürkl of the NIM, the mood remains "extremely low," with uncertainty still elevated due to global trade tensions, stock market volatility, and persistent fears of another year of economic "stagnation". These concerns are encouraging households to prioritize saving over spending.

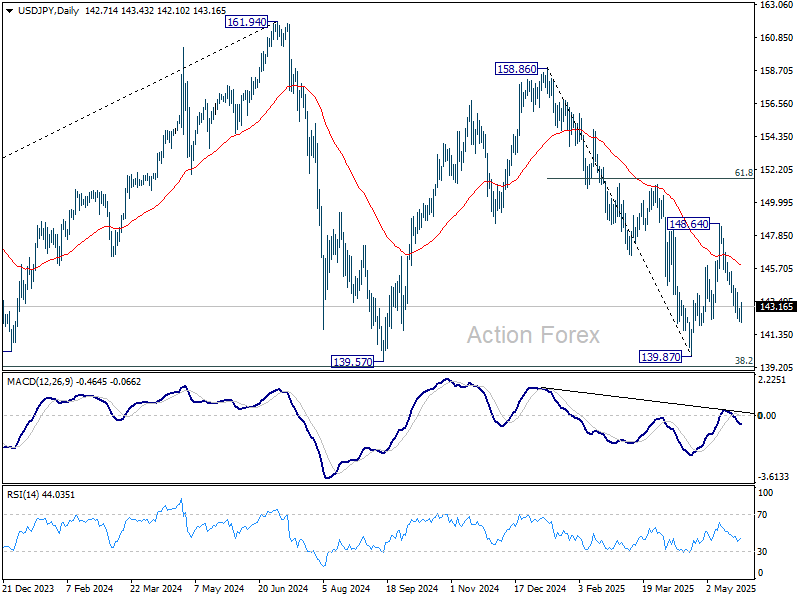

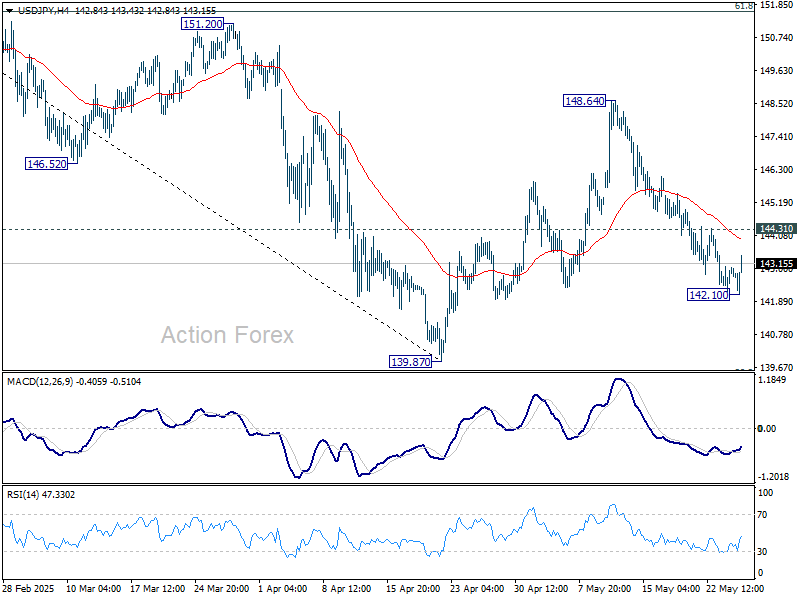

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.35; (P) 142.72; (R1) 143.20; More...

Intraday bias in USD/JPY is turned neutral with current recovery. Some consolidations would be seen above 142.10 temporary low. Further decline is expected as long as 55 D EMA (now at 145.85) holds. Below 142.10 will resume the fall from 146.64 to retest 139.87 low.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.