Sample Category Title

EUR/USD Trims Gains—Can Bulls Save The Day?

Key Highlights

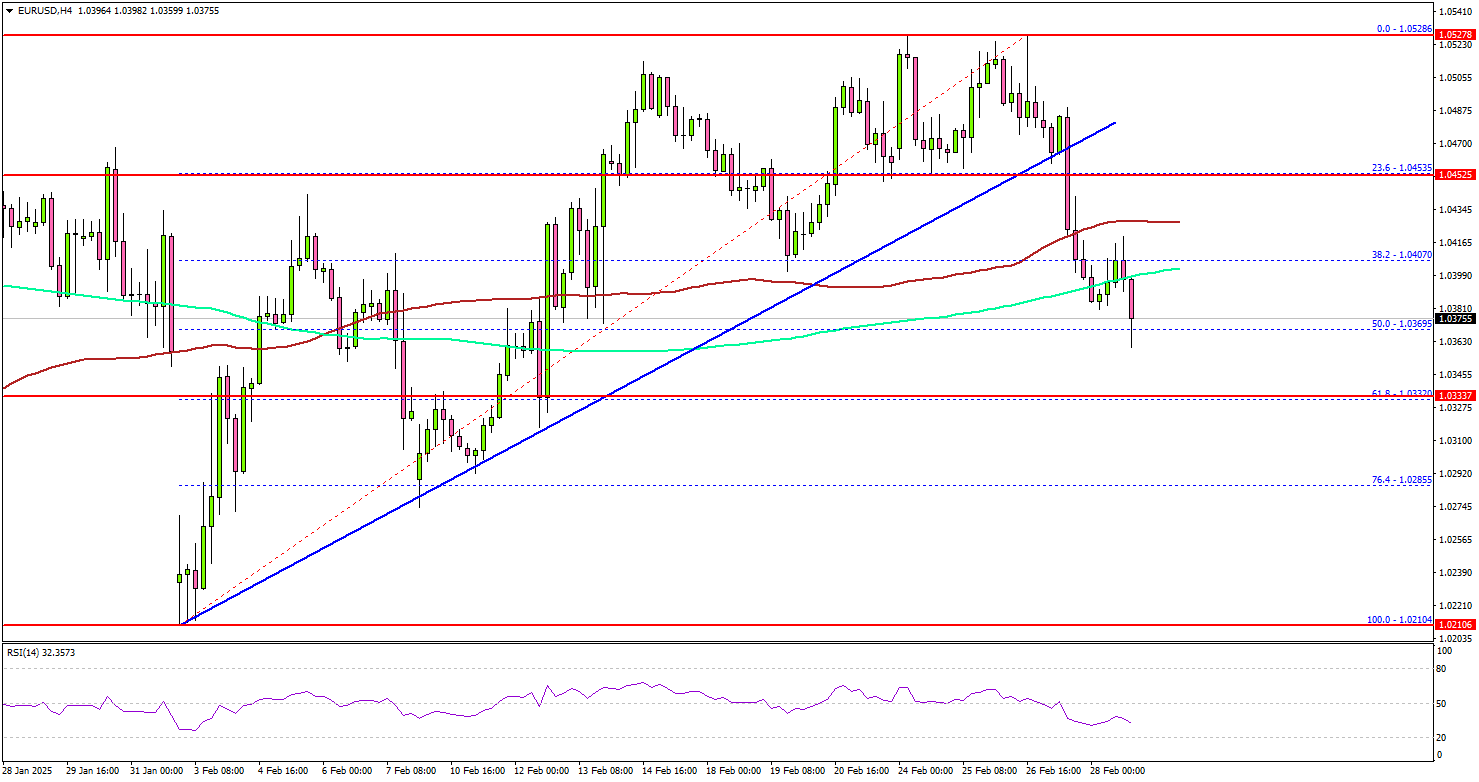

- EUR/USD started a fresh decline from the 1.0530 resistance.

- It traded below a major bullish trend line with support at 1.0470 on the 4-hour chart.

- GBP/USD also corrected gains and traded below 1.2640.

- The US ISM Manufacturing Index could dip from 50.9 to 50.8 in Feb 2025.

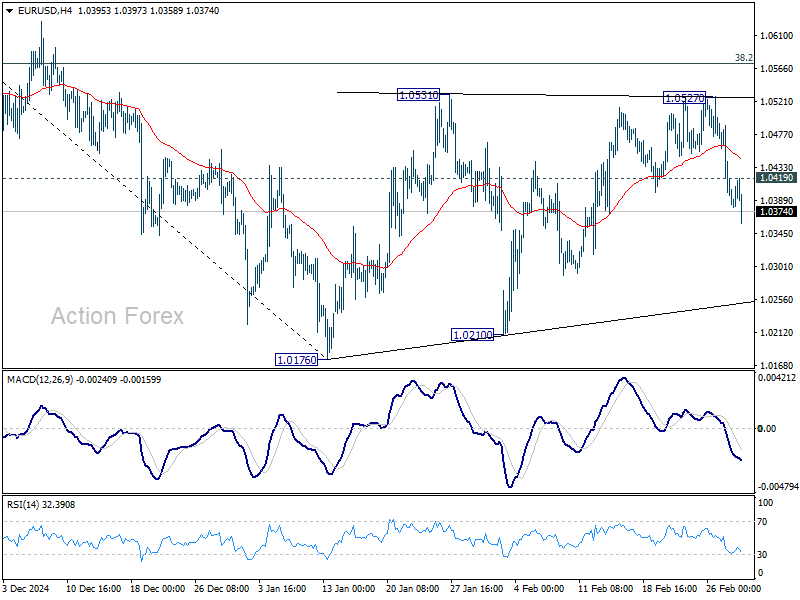

EUR/USD Technical Analysis

The Euro started a fresh increase above the 1.0450 and 1.0500 levels against the US Dollar. However, EUR/USD failed to clear 1.0535.

Looking at the 4-hour chart, the pair formed a top near 1.0530 and started a fresh decline. There was a move below the 1.0500 and 1.0480 levels. The pair dipped below a major bullish trend line with support at 1.0470.

The pair settled below the 100 simple moving average (red, 4-hour) and spiked below the 200 simple moving average (green, 4-hour). There was a test of the 50% Fib retracement level of the upward move from the 1.0210 swing low to the 1.0528 high.

On the upside, the pair seems to be facing hurdles near the 1.0420 level. The next major resistance is near the 1.0450 level. The main resistance is now forming near the 1.0465 zone.

A close above the 1.0465 level could set the tone for another increase. In the stated case, the pair could even clear the 1.0500 resistance.

On the downside, immediate support sits near the 1.0365 level. The next key support sits near the 1.0350 level. Any more losses could send the pair toward the 1.0320 level.

Looking at GBP/USD, the pair failed to gain pace for a move above the 1.02700 resistance and corrected some gains.

Upcoming Economic Events:

- Euro Zone Manufacturing PMI for Feb 2025 – Forecast 47.3, versus 47.3 previous.

- UK Manufacturing PMI for Feb 2025 – Forecast 46.4, versus 46.4 previous.

- US ISM Manufacturing Index for Feb 2025 – Forecast 50.8, versus 50.9 previous.

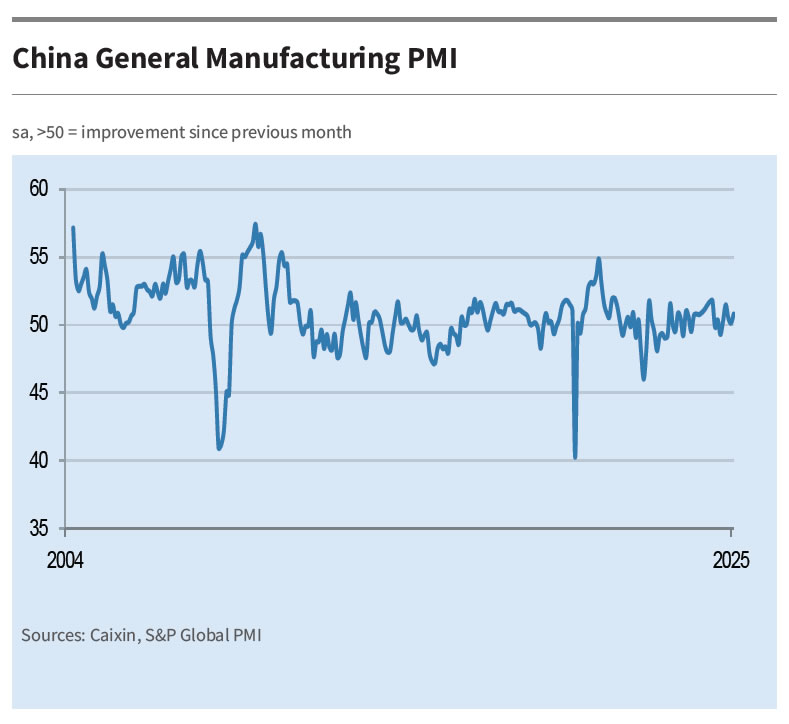

China’s Caixin PMI manufacturing rises to 50.8, but employment remains a concern

China’s Caixin PMI Manufacturing climbed to 50.8 in February, up from 50.1, exceeding expectations of 50.3.

Wang Zhe, Senior Economist at Caixin Insight Group, noted that new export orders rebounded, corporate purchasing increased, and logistics remained smooth. However, employment continued to decline, and output prices stayed weak.

Additionally, official PMI data released over the weekend further reinforced signs of recovery. The official PMI Manufacturing rebounded from 49.1 to 50.2, marking its highest level since November and moving back into expansionary territory. Additionally, the non-manufacturing PMI, which covers services and construction, ticked up to 50.4 from 50.2.

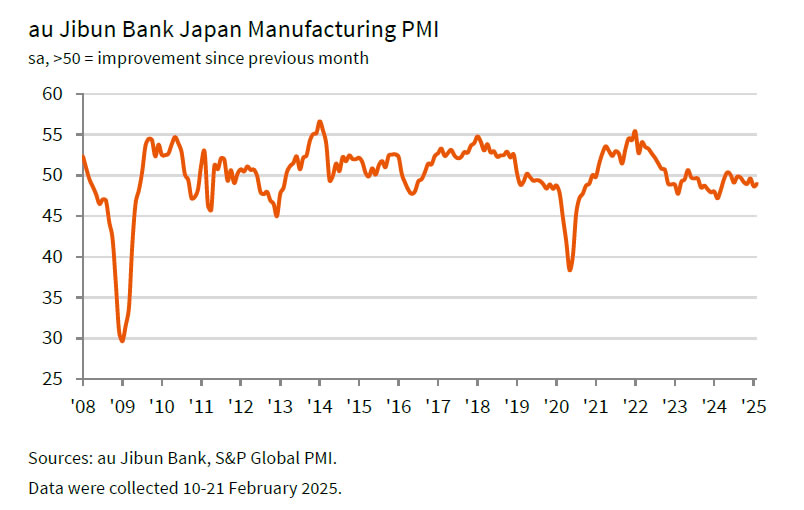

Japan’s PMI manufacturing finalized at 49 in Feb, modest improvement but outlook remains weak

Japan’s manufacturing sector showed slight improvement in February, with PMI finalized at 49.0, up from 48.7 in January. However, the sector remains in contraction territory, reflecting ongoing struggles with weak demand.

According to Usamah Bhatti at S&P Global Market Intelligence, manufacturers cited soft global and domestic demand, with "muted conditions" in key markets such as the US, Europe, and China. Additionally, purchasing activity saw a solid and sustained decline.

The "near-term outlook remains clouded". Business confidence fell to its lowest level since mid-2020, driven by growing concerns over the impact of US trade policies and a slower-than-expected global economic recovery.

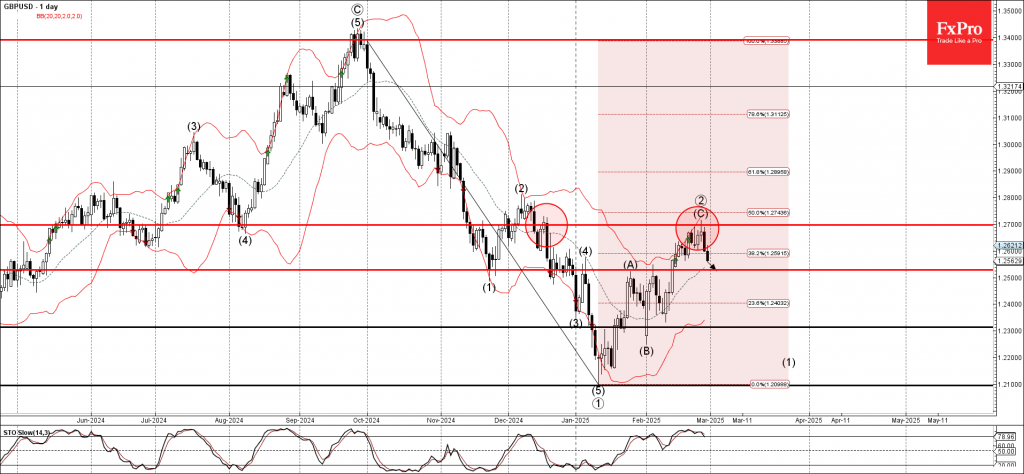

GBPUSD Wave Analysis

- GBPUSD reversed from the resistance zone

- Likely to fall to support level 1.2530

GBPUSD currency pair recently reversed from the resistance zone between the resistance level 1.2700, the upper daily Bollinger Band and the 50% Fibonacci correction of the downward impulse from September.

The downward reversal from this resistance zone created the daily Japanese candlesticks reversal pattern Evening Star which ended the previous impulse wave (3).

Given the overbought daily Stochastic, GBPUSD can be expected to fall to the next support level 1.2530 (former resistance from the end of January).

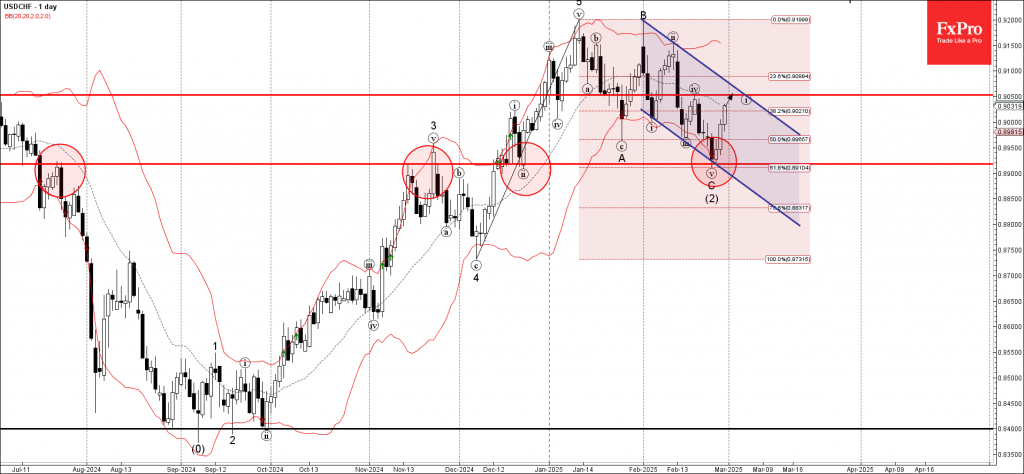

USDCHF Wave Analysis

- USDCHF reversed from support zone

- Likely to rise to resistance level 0.9050

USDCHF currency pair recently reversed from the support zone between the support level 0.8920 (which has been reversing the price from November), support trendline of the daily down channel from January and the lower daily Bollinger Band.

The upward reversal from this support zone created the daily Japanese candlesticks reversal pattern Morning Star which started the active impulse wave (3).

Given the clear daily uptrend, USDCHF can be expected to rise to the next resistance level 0.9050 (top of the previous minor correction iv).

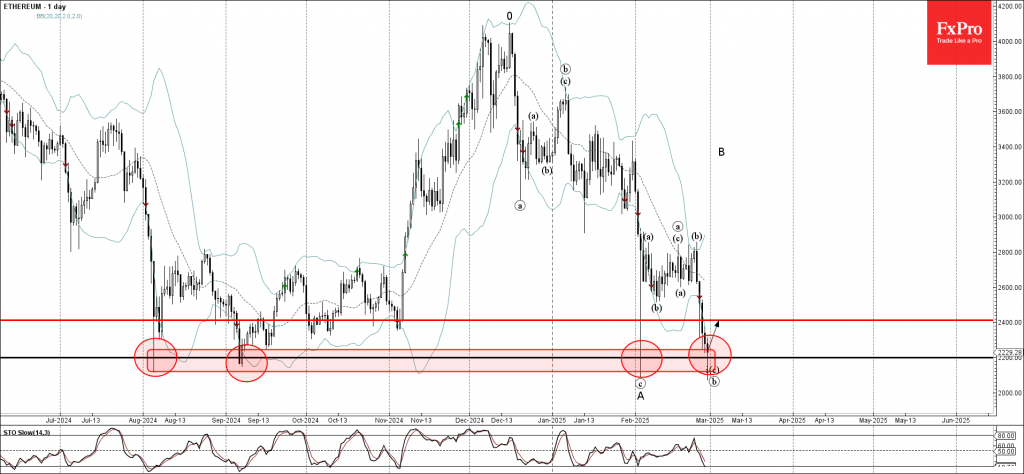

Ethereum Wave Analysis

- Ethereum reversed from support zone

- Likely to rise to resistance level 2400.00

Ethereum recently reversed from the support zone between the major long-term support level 2200.00 (which has been reversing the price from August) and the lower daily Bollinger Band.

The upward reversal from this support zone is currently forming the daily Japanese candlesticks reversal pattern Hammer – a strong buy signal for Ethereum.

Given the strength of the nearby support level 2200.00 and the oversold daily Stochastic, Ethereum can be expected to rise to the next resistance level 2400.00.

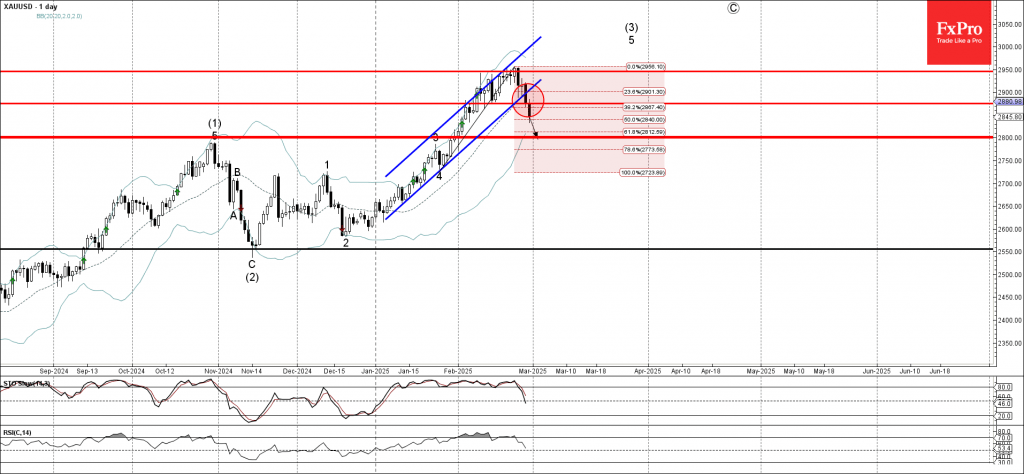

Gold Wave Analysis

- Gold broke the support zone

- Likely to fall support level 2800.00

Gold recently broke the support zone between the key support level 2875.00 (which has been reversing the price from the start of February), the support trendline of the daily up channel from January and the 38.2% Fibonacci correction of the upward impulse from January.

The breakout of this support zone strengthened the bearish pressure on gold accelerating the active downward correction.

Gold can be expected to fall to the next support level 2800.00 (a former multi-month high from last October and the 61.8% Fibonacci correction of the upward impulse from January).

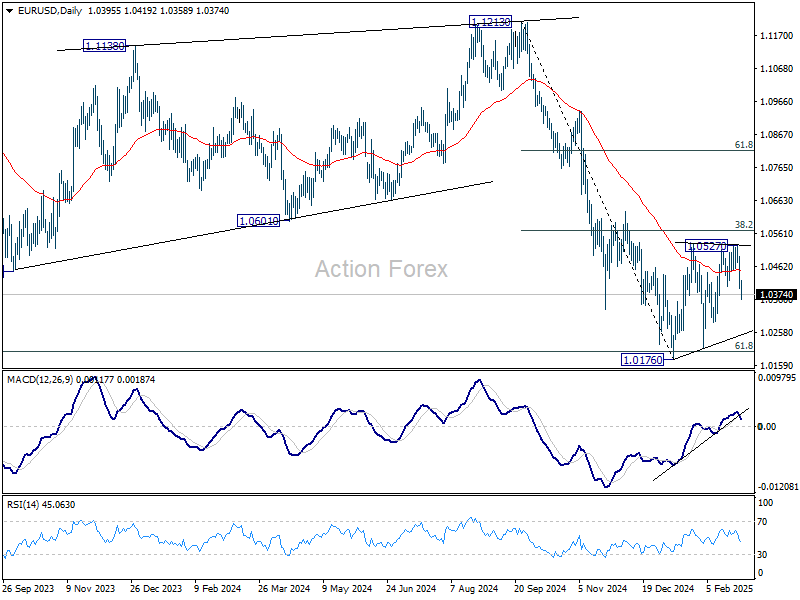

EUR/USD Weekly Outlook

EUR/USD reversed after edging higher to 1.0527 last week, and the development suggests that consolidation from from 1.0176 has already completed. Initial bias stays on the downside this week for retesting 1.0176/0210 support zone first. Firm break there will resume whole fall from 1.1213, and carry larger bearish implications. On the upside, above 1.0419 minor resistance will turn intraday bias neutral. But outlook will stay bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

In the long term picture, down trend from 1.6039 remains in force with EUR/USD staying well inside falling channel, and upside of rebound capped by 55 M EMA (now at 1.0929). Consolidation from 0.9534 could extend further and another rising leg might be seem. But as long as 1.1274 resistance holds, eventual downside breakout would be mildly in favor.

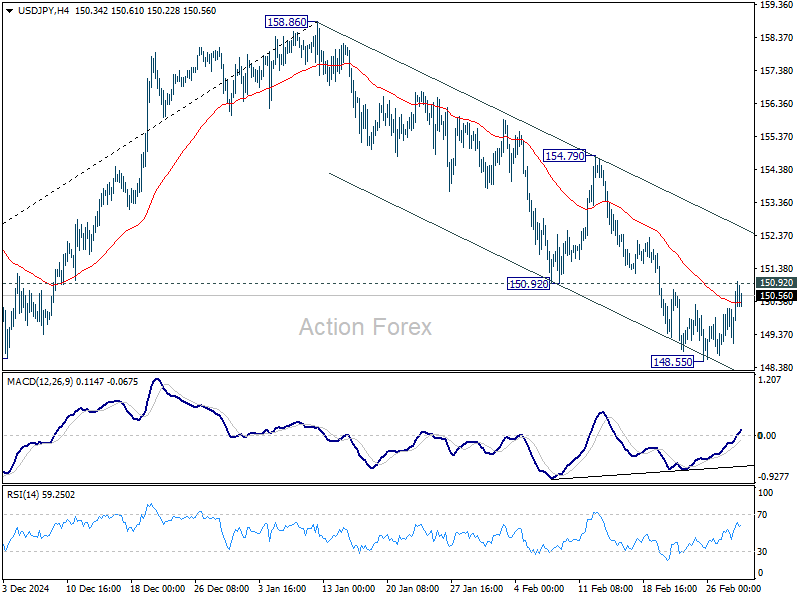

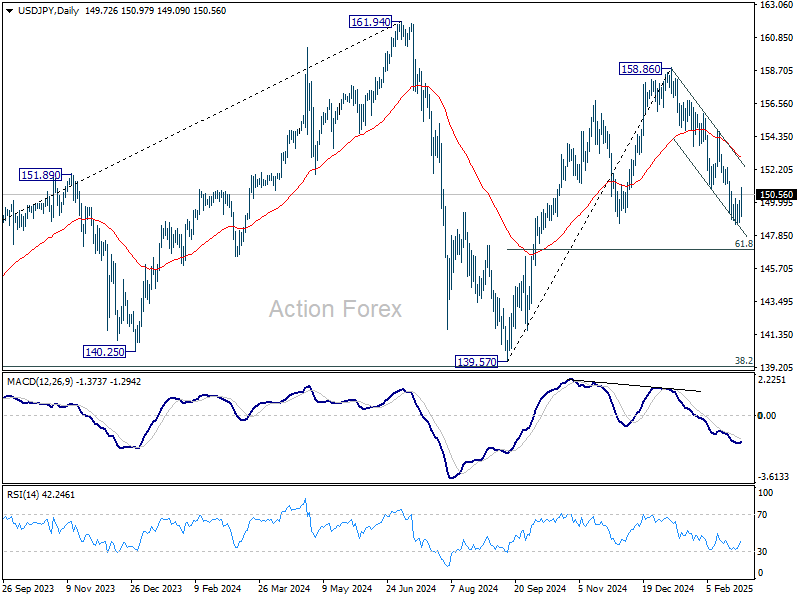

USD/JPY Weekly Outlook

USD/JPY's fall from 158.86 continued last week but recovered after hitting 148.55. Initial bias remains neutral this week first. This decline is seen as the third leg of the corrective pattern from 161.94 high. Break of 148.55 will target 61.8% retracement of 139.57 to 158.86 at 146.32 next. On the upside, however, break of 150.92 will indicate short term bottoming and bring stronger rebound.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. A medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 136.50).