Sample Category Title

ECB Minutes Reveal June Rate Hike Momentum Growing Rapidly

The accounts of the April 29–30 meeting of the European Central Bank revealed that policymakers came significantly closer to raising interest rates than markets may have initially realized. While all members ultimately agreed to leave rates unchanged, the discussion showed growing concern that the Middle East energy shock is becoming more persistent and increasingly incompatible with a passive “looking through” approach. Several policymakers reportedly viewed the decision as a “close call,” and indicated they "would not have opposed raising rates at the current meeting had this been on the table."

A central theme throughout the accounts was that the inflation outlook has materially deteriorated since March. Policymakers acknowledged that the conflict “would last longer than had been expected,” while the energy shock was proving “more persistent and its repercussions broadening.” Officials also noted that the latest oil market developments suggested inflation risks were moving away from the ECB’s baseline scenario. Importantly, the accounts highlighted growing concern that the combination of elevated energy prices, weakening confidence, and slowing growth was creating a classic negative supply shock and increasingly difficult stagflation trade-off for monetary policy.

The debate inside the Governing Council also showed that concerns over second-round inflation effects are intensifying rapidly. Several members warned that the risk of inflation expectations becoming unanchored had “re-emerged,” while pipeline price pressures were beginning to build again. Officials emphasized that firms may increasingly pass higher energy costs through to consumers, especially if the conflict drags on and supply-chain disruptions worsen. The accounts explicitly noted that it was becoming “increasingly unlikely” that a “looking through” approach without monetary tightening would remain appropriate.

Still, policymakers agreed that waiting until June remained the most prudent course because more information on wages, inflation expectations, and the duration of the conflict would become available by then. The ECB also acknowledged that a rapid diplomatic resolution and sharp fall in oil prices could still reverse inflation risks quickly.

Nevertheless, the overall tone of the accounts strongly reinforced expectations that June has effectively become the ECB’s critical tightening decision point. The key debate now increasingly appears to be not whether rates need to rise, but how quickly and how far the ECB may ultimately need to go.

(ECB) Monetary policy accounts

Account of the monetary policy meeting of the Governing Council of the European Central Bank held in Frankfurt am Main on Wednesday and Thursday, 29-30 April 2026

28 May 2026

1. Review of financial, economic and monetary developments and policy options

Financial market developments

Ms Schnabel started her presentation by noting that since the Governing Council's previous monetary policy meeting on 18-19 March 2026, movements in euro area financial markets had continued to be driven by developments in the Middle East and their impact on energy prices. Amid elevated volatility, markets continued to expect the oil price shock to be persistent. Although upside risks had moderated, oil was priced significantly higher, over an extended period of time, than it had been before the start of the war in the Middle East. As a result, markets continued to price in a notable and sustained inflationary impact. Inflation fixings had increased further for both 2026 and 2027. This suggested that investors anticipated some indirect or second-round effects extending beyond the first year of the conflict, before inflation was expected to return to the target of 2% in 2028. At the same time, markets continued to expect the economy to be relatively resilient. Prices of risk assets, including equities, as well as sovereign and corporate bond spreads, and the exchange rate of the euro had moved back towards the levels observed prior to the conflict. Earnings expectations had been revised up since the beginning of the war, which was consistent with the view that the impact on economic growth would be short-lived. At the same time, there had been negative surprises in macroeconomic data for the euro area. Therefore, buoyant risk asset markets, which were hovering near all-time highs, might indicate some investor complacency given the size and persistence of the energy price shock. With inflation still perceived as the dominant risk, investors were pricing in cumulative policy rate hikes by the ECB of 73 basis points in 2026. Overall, financial conditions had eased since the Governing Council’s previous monetary policy meeting, driven mainly by strong risk asset markets, but they remained somewhat tighter than before the war.

Energy prices were unchanged from the levels prevailing at the time of the Governing Council’s previous monetary policy meeting, but remained subject to heightened volatility. Oil prices had been strongly affected by the changing probabilities of a potential reopening of the Strait of Hormuz. The Brent crude oil futures curve had retreated from the peak level reached in late March 2026, but still stood at about the level observed at the time of the Governing Council’s previous monetary policy meeting. Moreover, the curve remained materially above the pre-war level over the next two years, suggesting that market participants assessed the energy price shock to be not only large but also highly persistent.

Energy price developments had been the dominant driver of movements across euro area financial markets. Expectations of persistently higher energy prices had been reflected in inflation compensation, which had increased sharply in response to the energy shock, and higher short and longer-term interest rates. By contrast, riskier market segments had shown less persistent reactions.

A key factor underlying the divergence between the responses of interest rate markets and segments for riskier asset classes was the assessment by investors of the relative impact of the energy shock on inflation and growth. Inflation expectations reported by Consensus Economics had shifted higher for the euro area for both 2026 and 2027, and for the United States they had shifted higher for 2026. By contrast, there had been a more modest adjustment in growth expectations. Both euro area and US growth projections had edged down, while not pointing to a pronounced slowdown. However, recent incoming data had been more favourable in the United States than in the euro area, which was consistent with the different impact of the terms-of-trade shock across the two economies.

Regarding the market’s view of the inflation outlook for the euro area, at the time of the Governing Council’s previous monetary policy meeting, inflation fixings for 2026 and 2027 had already shifted up sharply compared with before the start of the war in the Middle East. The latest fixings had edged up further for 2026, trading at levels of up to 3.6%. For 2027, inflation fixings were even more clearly above their March 2026 levels. This suggested that investors were expecting more persistent inflationary pressures, reflecting some indirect or second-round effects. The balance of risks to inflation over the next two years and also over the next five years remained clearly tilted to the upside, while longer-term risks had started to point more to the upside, but inflation expectations continued to be well anchored.

The shifts in inflation compensation had dominated developments in euro area risk-free rates across all maturities. Since the start of the war in the Middle East, euro area overnight index swap rates had moved up significantly, with the reassessment of inflation prospects pushing rates higher across the curve and leading to a flattening of the nominal yield curve. By contrast, the real overnight index swap curve had steepened, with real rates declining markedly at the front end of the curve relative to pre-war levels and contributing to a loosening of financial conditions.

After the previous monetary policy meeting on 18-19 March, markets had priced in a further tightening of monetary policy. Rate market investors were now fully pricing in one 25 basis point policy rate hike by June 2026, two by September and a 92% probability of a third by December. At the time of the previous meeting, participants in the Survey of Monetary Analysts had expected the ECB to look through the energy supply shock, but their responses had now become more aligned with market pricing and the median expectation was for two hikes in 2026. In the United States, market-based measures of policy rate expectations had remained broadly unchanged since the Governing Council’s previous monetary policy meeting.

The EUR/USD exchange rate had rebounded to close to pre-war levels since the Governing Council’s previous monetary policy meeting. The euro had initially depreciated markedly, both in bilateral and nominal effective terms, as the terms-of-trade shock had been expected to weigh on the currencies of net energy importers. However, it had almost fully recovered its losses over recent weeks. Improved global risk sentiment and expectations of tighter ECB monetary policy relative to US policy had contributed to the euro’s recovery.

Investor optimism regarding the impact on economic growth was most visible in equity markets, which appeared to be largely looking through the energy price shock. The benchmark stock index for the euro area had initially corrected significantly in response to the war, but since the Governing Council’s previous monetary policy meeting it had partly recovered its losses. In the United States, benchmark stock indices had even surpassed pre-war levels and risen towards new all-time highs, supported by renewed optimism about the potential impact of artificial intelligence. Model-based analysis showed that the dominant driver of the initial decline in euro area equity prices had been the rise in risk-free rates. Since the Governing Council’s meeting on 18-19 March, higher longer-term earnings expectations had pushed up euro area equity markets, while higher risk premia had pulled in the opposite direction. Looking at the entire period since the start of the war, earnings expectations had been revised up overall, indicating that analysts did not expect the war to have a lasting impact on corporate profits.

In line with improved risk sentiment, euro area sovereign bond spreads had also narrowed from the peaks recorded in the second half of March. The dispersion of euro area sovereign spreads had remained contained over the entire period since the start of the war. This appeared to reflect not only market perceptions that the real economic fallout from the energy shock would be limited, but also expectations of a prudent fiscal response, as measures taken to shield households and firms from higher energy prices remained limited so far. Another factor supporting euro area government bond markets had been increased inflows of global funds into European sovereign bonds, which pointed to continued confidence in European sovereign debt. In corporate bond markets, pricing had also remained benign. Spreads of high-yield euro area corporate bonds had temporarily widened at the onset of the war, but the increase had remained contained. Overall, financial conditions for the euro area had initially tightened in response to the war, but had eased since the Governing Council’s last monetary policy meeting on the back of buoyant risk assets.

Ms Schnabel concluded by summarising how the rise of tokenised financial markets might affect market functioning and monetary policy implementation. Tokenised finance had expanded rapidly over recent years and was concentrated in three segments: stablecoins, decentralised finance and tokenised traditional assets, with stablecoins dominating. Broader adoption of tokenised finance would take time, as it was being held back by regulatory and structural barriers. From a central bank perspective, the fragmentation of liquidity remained a key concern in relation to tokenised financial markets. On the positive side, tokenisation was expected to give rise to significant efficiency gains, for example by reducing the cost of bond issuance and post-trade processing and by mitigating settlement risk through near-instantaneous settlement of transactions. Given the fast evolution of tokenisation, it was important to foster these developments through the Eurosystem’s own innovation activities, especially in the context of the ongoing Pontes and Appia projects.

The global environment and economic and monetary developments in the euro area

Mr Lane then went through the latest economic, monetary and financial developments in the global economy and the euro area. The incoming information since the March meeting had been broadly consistent with the Governing Council’s previous assessment of the inflation outlook and the risks surrounding it. The war in the Middle East had led to a sharp increase in energy prices, pushing up inflation and weighing on economic sentiment. The implications of the war for medium-term inflation and economic activity would depend on the intensity and duration of the energy price shock and the scale of its indirect and second-round effects.

Starting with inflation developments in the euro area, headline inflation, as measured by the Harmonised Index of Consumer Prices (HICP), had increased to 2.6% in March, from 1.9% in February. The rise had been entirely driven by surging energy prices caused by the war in the Middle East. Energy price inflation had jumped to 5.1% in March, from -3.1% in February, while non-energy inflation had eased further, to 2.3%, from 2.4% in February. Based on the country data available so far, staff expected Eurostat’s flash data release for HICP inflation in April – which was to be published on 30 April – to lie in the range of 3.0% to 3.1%, broadly in line with the March 2026 projections. The projected acceleration in headline inflation from February reflected an expected sharp increase in energy inflation.

Indicators of underlying inflation had changed little over recent months. The ECB’s wage tracker and surveys on wage expectations continued to indicate easing labour costs in the course of 2026. At the same time, surveys indicated an increase in other labour cost components.

Measures of near-term inflation compensation stood at or slightly above 3% for the period until the end of the first quarter of 2027. Markets were pricing in a sharp drop in inflation in the second quarter of 2027 and convergence to target in 2028. At longer horizons, inflation was expected to stabilise at the target. One-year forward inflation compensation two years ahead stood at 2.18% and five-year forward inflation compensation five years ahead stood at 2.15%, which, once corrected for risk premia, was consistent with inflation at target. In the latest rounds of the Survey of Professional Forecasters and the Survey of Monetary Analysts, the median responses to both surveys showed inflation expectations had been revised up for the near term, but remained at target over the medium term. While median consumer expectations for inflation one year ahead and three years ahead had moved up markedly, median expectations for inflation five years ahead had been revised up only slightly, from 2.3% to 2.4%, returning to the level seen at the end of 2025. The latest results of the Survey on the Access to Finance of Enterprises indicated that corporate inflation expectations had been revised up mainly at short horizons, while three‑year ahead and five‑year ahead median expectations had hardly changed. In summary, taken together, the incoming information suggested that longer-term inflation expectations were well anchored at the target. At the same time, market-based, expert-based and survey-based measures of the balance of risk to inflation all pointed to upside risks, especially in the near term.

Global economic activity had remained relatively resilient, but the war in the Middle East was weighing on energy markets, confidence and near-term growth prospects. While remaining in expansionary territory, the global composite Purchasing Managers’ Index (PMI) had declined from 53.5 in February to 50.9 in March. Rising energy prices were beginning to dampen consumer spending, which was likely to weigh increasingly on activity over the coming quarters. Global trade had so far been only moderately affected, while broader shipping disruptions had remained contained and freight costs were generally stable. Survey indicators nevertheless pointed to some weakening of trade in the period ahead.

Turning to commodity prices, movements in energy prices had been driven by developments in the war in the Middle East. The latest oil price futures curve remained elevated and for 2026 it was around 20% above the baseline assumptions for the March 2026 ECB staff projections. Looking ahead, current prices for 2027 were close to the March projections baseline, which was consistent with markets expecting the crisis to be resolved by next year. The latest forward curves for European natural gas prices were well below the baseline assumptions for the March projections. In terms of the profile, futures implied that gas prices would move sideways over the second half of 2026 and then fall quite sharply in 2027 and 2028. The futures curve of the synthetic energy commodity price index (SECPI), which was a weighted average of gas and oil prices, was only slightly above the assumptions for the March baseline projections. Within the SECPI, the upward shift in the oil price futures curve since March had been largely counterbalanced by the downward shift in the gas price futures curve.

The euro had appreciated since the previous Governing Council meeting, increasing by about 1.5% in bilateral terms against the US dollar and by 0.7% in nominal effective terms. Its depreciation at the start of the war in the Middle East had subsequently reversed and it was currently trading close to the levels seen at the start of the year.

The euro area economy had been showing some momentum when the current turbulence started, but early indicators suggested that the conflict in the Middle East was starting to weigh on activity, against the backdrop of a highly uncertain outlook. In the March staff projections, real GDP had been expected to expand by 0.3% and employment by 0.1% in the first quarter of 2026. Eurostat’s flash estimate for these figures was due to be released on 30 April. However, the economic outlook was highly uncertain and would depend on how long the war in the Middle East lasted and how strongly it affected energy and other commodity markets, as well as global supply chains. The composite output PMI had dropped from 50.7 in March to 48.6 in April, indicating a contraction in activity for the first time since December 2024. This had been driven entirely by weaker services activity. Manufacturing had held up on the back of defence spending in Germany and some inventory build-up in anticipation of the impact of the energy shock. Longer delivery times and rising input prices suggested supply chains were coming under pressure. The European Commission’s Economic Sentiment Indicator had declined markedly in April, extending the fall recorded in March. This had been primarily driven by a sharp decline in consumer confidence and clearly pointed to weakening growth momentum.

While unemployment remained close to historical lows – with figures for March due to be published on 30 April – labour demand had cooled further. According to staff estimates, the job vacancy rate was likely to continue to decline, having fallen from 2.2% in the last quarter of 2025 to 2.1% in the first quarter of 2026. The composite employment PMI had stood at 49.8 in April, reflecting increases in both manufacturing, where it remained well in contractionary territory below the threshold of 50, and in services, where it remained just above that threshold.

With respect to fiscal policies, energy price compensation measures recently announced by governments had so far been modest in size and were mainly focused on indirect taxes on energy and targeted subsidies, so that the euro area fiscal stance was likely to be slightly more expansionary in 2026 than previously expected and slightly more contractionary in 2027.

Turning to financing conditions, the war in the Middle East had caused significant volatility in global financial markets. Overall financial conditions remained tighter than before the war. The cost of issuing market-based debt had risen to 3.9% in March, from 3.5% in February. The annual growth rate of bank lending to firms had increased to 3.2% in March, from 3.0% in February, while the growth rate of corporate bond issuance had fallen to 3.9%, from 4.5% in February. Credit standards for loans to firms had tightened in the first quarter of 2026, as reported in the latest bank lending survey for the euro area. This tightening was due to banks becoming more concerned about the economic risks faced by their customers. Demand for loans to firms had decreased slightly in the first quarter, especially for fixed investment. The most recent round of the Survey on the Access to Finance of Enterprises pointed to a further tightening of financing conditions for firms, broadly confirming the signals from the bank lending survey.

Monetary policy considerations and policy options

Mr Lane proposed that the Governing Council keep the three key ECB interest rates unchanged. The incoming information had been broadly consistent with the Governing Council’s previous assessment of the inflation outlook and the risks surrounding it. The Governing Council remained well positioned to navigate the current uncertainty and to gather more information on the implications of the war for inflation and economic activity in the medium term. These would depend on the intensity and duration of the energy price shock and the scale of its indirect and second-round effects. By the next meeting in June, the Governing Council would have additional information – including new projections and some data points for April and May, as well as more clarity on the evolution of the war – that would help it to assess the implications for the monetary policy stance. In this context, the data-dependent, meeting-by-meeting approach, with no pre-commitment to a particular rate path, continued to provide a solid framework for determining the appropriate monetary policy stance.

2. Governing Council’s discussion and monetary policy decisions

Economic, monetary and financial analyses

Regarding the economic analysis, members broadly agreed with the assessment provided by Mr Lane in his introduction.

Starting with the external environment, the war in the Middle East was weighing on energy markets, confidence and near-term growth prospects. At the global level, uncertainty remained elevated, as did volatility in markets. Global economic activity had remained relatively resilient thus far, which was broadly consistent with the March baseline staff projections. However, the longer the conflict persisted and the Strait of Hormuz remained closed, the greater and more persistent the likely unfavourable macroeconomic impact would be. The disruption to energy markets was becoming more protracted and working its way through the economy and global supply chains, with more persistent and broader effects on both inflation and economic growth becoming increasingly likely. The most recent developments in oil markets suggested a shift away from the assumptions underlying the March baseline staff projections.

Although the global economic outlook had weakened somewhat, the global economy had so far displayed resilience. However, the economic impact of the war in the Middle East was not the same everywhere. Asian countries were most affected, in particular countries in South-East Asia, but also China and India, largely owing to their relatively high dependence on energy imports from the Middle East. While the near-term growth outlook for the United States had also weakened, this change was comparatively small, reflecting the fact that the United States was an oil and gas producer. Moreover, artificial intelligence constituted a positive supply shock, and the associated investment was providing a strong counteracting force for the US economy.

Regarding developments in oil markets, spot market prices had lately been considerably higher than prices for futures with the shortest terms, in part reflecting disruptions and strains in the physical market for oil. This raised the question of which prices mattered most for the economic outlook and how this disconnect might play out. The spot price might matter more for the immediate economic impact, as this was the price faced by firms purchasing oil today. Nonetheless, futures prices played a key role in the assumptions for the projections and contained information about the market’s assessment of the outlook, which currently suggested that the energy price shock could be persistent, although some degree of normalisation in energy markets over time was anticipated. The current expectation was that the gap between spot and futures prices was likely to persist over the next few months, with spot prices converging to futures prices thereafter. However, it was recognised that futures prices could move towards spot prices, especially if the conflict was not quickly resolved. In 2022 spot prices had overshot futures prices for an extended period of time – almost one year. Thus, it was cautioned that current oil price futures might be at the lower end of what would eventually materialise, which would have implications for the outlook for both inflation and growth. On the other hand, the recent announcement by the United Arab Emirates of its intention to leave OPEC could have a downward impact on future oil prices, particularly once the conflict was resolved.

Over the next six weeks, the situation in energy markets, and oil markets in particular, could reach a fork in the road. On the one hand, if the flow of energy products through the Strait of Hormuz increased, oil spot and futures prices would likely respond favourably. Yet, even in this case, it would still take some time for oil and gas supplies to normalise, with authorities in Saudi Arabia and Qatar having warned that repairing destroyed facilities would take time. On the other hand, if the conflict persisted or even deteriorated, it was likely that the situation in energy markets would become more critical, with oil spot and futures prices, as well as natural gas prices, increasing further and shortages becoming increasingly likely. The International Energy Agency had recently raised this prospect as a major concern.

One difference in energy price developments between the current situation and 2022 was that, so far, the increase in European natural gas prices had been much more contained. This was due to two main factors: the current crisis was not centred in Europe, and European energy markets, particularly for gas and electricity, had become more resilient, in part owing to an increased use of renewables and the diversification of supply sources, especially liquefied natural gas (LNG) imports. Looking ahead, one reason put forward by analysts for markets being relatively sanguine on gas prices was that even more LNG was likely to become available over the coming years. It was also noted that this time the impact on gas prices was being more keenly felt by Asian economies, in particular China and India. This notwithstanding, it was cautioned that while the increase in gas prices had remained more contained this time, the situation in Europe might deteriorate if gas storage facilities had not been sufficiently replenished by the start of the heating season in the autumn.

The conflict and the ceasefire were continuing, with high uncertainty about the future course of events. Current pricing in oil markets, with a strong backwardation – a negative slope – in the futures curve, could be seen as consistent with the view that the conflict would soon be resolved. However, there was also the possibility that current market pricing was based on an assessment of the situation that was too benign.

With regard to economic activity, members noted that the euro area economy had been showing some, albeit relatively modest, momentum when the current turbulence started. However, since the start of the war in the Middle East, the economic environment had clearly deteriorated and uncertainty was exceptionally high, with the conflict weighing on confidence, energy markets, supply chains and near-term growth prospects. Accordingly, the outlook for euro area economic activity had worsened since the start of the conflict. There were already some indications, particularly in survey data but also some hard data, that the situation was weighing on sentiment and activity. At the same time, it was noted that there was not much in the way of new hard data and that evidence from these data on the effects of the shock remained limited thus far. The first quarter GDP growth outcome of 0.1%, released on the morning of Thursday, 30 April, was lower than anticipated. However, it was observed that the outcome was higher when Ireland was excluded, at 0.2%. Regarding country releases, it was noted that the data for Germany were somewhat better than expected, while for France growth was flat for the first quarter and weaker than expected. A concern was expressed that the more global nature of the shock could mean that the range of future growth outcomes could be wider, particularly to the downside, than currently considered. In terms of soft data available for the second quarter, the composite output PMI for the euro area had fallen in April. This had been driven primarily by weaker services activity. While manufacturing had held up and was still perceived to be expanding, it was unclear how much reassurance could be taken from this, as it might reflect a degree of precautionary frontloading. It was also noted that the European Commission’s Economic Sentiment Indicator had declined markedly in April, extending the fall observed in March, with a particularly pronounced drop in consumer confidence.

Despite the indications of some weakening, it was argued that the euro area had displayed adaptability and resilience over recent years and there were reasons to expect that this could continue. One factor was that the euro area was now less dependent on fossil fuels. In addition, according to information from the Corporate Telephone Survey, government spending on defence and infrastructure, investment in artificial intelligence and continued growth in employment were all factors pointing to some resilience in consumption and investment. At the same time, it was argued that survey signals should be interpreted with caution as they might overstate the change in underlying fundamentals, with information from other sources giving mixed signals as to whether the picture had really changed much from March. Moreover, persistently elevated uncertainty, surging energy costs, the decline in consumer confidence, some signs of weakening in labour markets and tighter financial and lending conditions were all weighing on the economic outlook. Furthermore, it was noted that supply chain disruptions could also have a negative impact on economic activity, in addition to any upward impact on inflation.

Turning to the main components of GDP – consumption, investment and trade – there were mixed signals pointing to both resilience and fragility. There was some concern that private consumption could become weaker than expected owing to the combination of higher energy prices and a drop in consumer confidence. On the other hand, some factors, including the labour market and wage growth, remained broadly supportive of consumption. Signals were mixed for both housing and business investment. While the European Commission’s composite building activity indicator had strengthened, the PMI housing output indicator had ticked down and first quarter data for France also suggested that real estate activity was weakening. Looking ahead, higher expected mortgage rates and tighter credit conditions and lending standards might dampen the outlook for housing. As regards business investment, high uncertainty and tighter financing conditions and lending standards were creating headwinds. However, short-term indicators, such as the European Commission’s confidence indicator (except for the intangibles component) and the PMI for capital goods, had improved further in March. Further support to investment would come from defence and infrastructure spending as well as technology and artificial intelligence-related investment. Meanwhile, export volumes, in particular to the United States, had declined from 2024 levels, while imports had risen, in particular from China and South-East Asia. Looking ahead, the war might result in weaker foreign demand, adding to continued challenges from US tariffs and strong competition from China.

The labour market had remained largely resilient, although there were signs of some easing of labour market tightness, particularly compared with the situation in 2022. On the one hand, the unemployment rate remained close to historical lows and was predicted to remain there, and the employment PMI had remained broadly stable in April. On the other hand, there were indications of some moderation in job vacancies and vacancy rates.

Members discussed the implications of the current shock being more global in nature than the 2022 shock, which had affected Europe the most. It was explained that a global shock in a multi-sector model with production networks generated a more negative hit to economic activity as well as more pressure on import prices than a local shock, as higher energy costs were embedded in the prices of imported intermediate and final goods. However, it was clarified that, while a global shock meant a bigger impact for a given size of shock, this did not mean that the current shock or its impact would necessarily be larger, as this depended on the ultimate size of the shock, its duration and its composition.

In addition to the supply-side nature of the shock, concerns were raised regarding possible generalised supply-side constraints, which would have implications for both activity and inflation. While indications of these had been relatively limited thus far, some signals, such as increasing delivery times, were becoming more evident, and the longer the conflict persisted the more likely it was that these constraints would grow in scope. Physical supply constraints were already apparent in energy markets, affecting quantities, inventory levels and prices. Information from major shipping countries suggested that shipping was being rerouted away from higher-risk corridors and taking the longer route via Cape of Good Hope. This could push up both transportation costs and delivery times, which, in turn, might lead to further price pressures and result in supply bottlenecks. Looking ahead, the risk of broad-based supply chain disruptions was considered a key issue.

Turning to fiscal policy, members highlighted the urgent need to strengthen the euro area economy while maintaining sound public finances. It was underscored that any fiscal responses to the energy price shock should be temporary, targeted and tailored. This was particularly important as fiscal space was currently more limited than in 2022. Furthermore, it was noted that, while the fiscal response had been relatively contained thus far, at less than 0.1% of euro area GDP, pressure for additional measures might grow should the situation deteriorate.

Regarding structural policies, members stressed that reforms to enhance the euro area’s growth potential and accelerate the energy transition to reduce reliance on fossil fuels were more vital than ever. Completing the savings and investments union was key to funding innovation, supporting the green and digital transitions and improving productivity. The digital euro and tokenised wholesale central bank money would enhance Europe’s strategic autonomy, competitiveness and financial integration, and would boost innovation in payments. It was thus essential to swiftly adopt the Regulation on the establishment of the digital euro. Simplifying and harmonising rules across the EU’s Single Market would help European firms grow faster.

Against this background, members assessed that the risks to the growth outlook were to the downside, with risks having intensified since the Governing Council’s previous monetary policy meeting in March. The war in the Middle East remained a downside risk to the euro area economy, adding to the volatile global policy environment. Prolonged disruption of the supply of energy could increase energy prices further and for longer than currently expected. These factors would erode incomes and make firms and households more reluctant to invest and spend. The drag on growth would intensify if the closure of major shipping routes were to cause acute shortages of key inputs that forced euro area firms to curtail output. A worsening of global financial market sentiment could further dampen demand. Additional frictions in international trade could exacerbate supply chain disruptions, reduce exports and weaken consumption and investment. Other geopolitical tensions, in particular Russia’s unjustified war against Ukraine, remained a major source of uncertainty. By contrast, growth could turn out to be higher if the economy proved to be more adaptable to the disruption caused by the war in the Middle East or if the conflict were resolved more quickly than currently expected. Moreover, planned defence and infrastructure spending, reforms to enhance productivity and euro area firms adopting new technologies might drive up growth by more than expected. New trade agreements and a deeper integration of the Single Market could also boost growth beyond current expectations.

With regard to price developments, members concurred with the assessment presented by Mr Lane in his introduction. The incoming information had been broadly consistent with the previous assessment of the inflation outlook and, while upside risks to inflation had intensified, indicators of underlying inflation had changed little over recent months. Although inflation expectations had risen significantly over shorter horizons, most measures of longer-term inflation expectations stood at around 2%, supporting the stabilisation of inflation around target in the medium term.

According to Eurostat’s flash estimate published at 11:00 on 30 April, inflation had risen to 3.0% in April, from 2.6% in March and 1.9% in February. The rise had been driven by higher energy prices caused by the war in the Middle East. Energy price inflation had jumped to 10.9% in April, after 5.1% in March and -3.1% in February. The rise in energy prices was not yet reflected in higher electricity bills, but some increases might materialise over the coming months. Wholesale natural gas prices had eased since March, but there were risks to natural gas supplies, in particular LNG, in the global market, which could push up gas prices later in the year. Food price inflation had edged up to 2.5% in April from 2.4% in March, but was unchanged compared with February. Looking ahead, while there could still be downward pressures from past declines in global food commodity prices, there was upward pressure from fertiliser prices, and firms had increased selling price expectations in food-related sectors, according to the Survey on the Access to Finance of Enterprises. Inflation excluding energy and food had decreased to 2.2% in April, from 2.3% in March, reflecting a fall in services inflation, which had declined to 3.0% from 3.2% in March. Goods inflation had increased to 0.8%, from 0.5% in March.

It was argued that the current shock had so far been more contained than in 2022 and was therefore less likely to trigger non-linear effects. Another possible countervailing factor was that, on this occasion, the impact on gas prices had been much smaller than in 2022, when gas prices in Europe had been particularly affected. Nonetheless, it was recalled that the inflationary impact of a global energy price shock might be amplified via supply chains, including through more expensive imports from China. This could push up non-energy industrial goods inflation, meaning that the previously observed pattern of higher services inflation being offset by lower non-energy industrial goods inflation might fade, posing upside risks to core inflation. At the same time, inflation in China was expected to remain low in relative terms and would therefore continue to have a dampening impact on non-energy industrial goods inflation. It was also questioned whether the current situation should be considered as one shock or rather sequences of shocks – for example, starting with oil before later affecting fertiliser and then food.

Regarding possible indirect and second-round effects of the energy shock, it was noted that some effects, particularly indirect effects, were inevitable and that the key issues would be their extent, magnitude, timing and duration. Regarding their duration, it was noted that the time it took for oil shocks to transmit to HICP items that were identified as being energy-sensitive varied from one month for fuels to more than 15 months for other energy-sensitive items, such as meat products, when measured in terms of the peak impact. The potential for second-round effects was assessed as being dependent mainly on inflation expectations and wage and price-setting behaviour. Regarding wages, there was no evidence of second-round effects so far, and it was suggested that such effects, if any, were unlikely to materialise before 2027. However, the Corporate Telephone Survey and the Survey of Professional Forecasters did already show small upward revisions in expected wage growth.

Survey data indicated an increase in the expectations of firms regarding non-wage cost components and selling prices, suggesting that indirect effects were materialising, although there was limited hard data as yet. The flash PMIs for April had shown the fastest increase in the input costs of firms since 2022 and selling price expectations had increased to their highest level in three years. Pressures were also seen in other surveys, such as the European Commission’s business survey and the Corporate Telephone Survey. In addition to the magnitude of input cost increases, the extent and speed of the pass-through of the energy shock also depended on the price-setting behaviour of firms and especially the frequency of price-setting. It was argued that, during the low-inflation period prior to 2022, firms had had little opportunity to raise prices frequently, whereas the inflation surge in 2022 might have led to an increase in the propensity to change prices. While there was little hard data as yet indicating a change in the price-setting frequency, anecdotal evidence from business economists indicated that the governance of price adjustments had changed, increasing the ability of firms to change prices. It was argued that during the low-inflation period prior to 2022, any price increase would have been a major decision for a company and would have required the approval of the chief financial officer or the chief executive officer. Such decisions could now often be taken at the business line level. However, it was pointed out that the ability to pass through cost increases also depended on the strength of aggregate demand, as well as on the tightness of the labour market. Aggregate demand was weaker at present than in 2022, and the labour market was less tight. Overall, while the direction of price changes was relatively clear, their scale was yet to be seen.

Inflation expectations had moved up significantly over shorter horizons, while most measures of longer-term inflation expectations stood at around 2%, supporting the stabilisation of inflation around target in the medium term. Regarding nearer-term market-based measures of inflation compensation, inflation fixings had moved up sharply for 2026 and, to some degree, for 2027. Beyond the near term, while there had been some increase in inflation-linked swap rates, with the one-year forward rate one year ahead standing at around 2.3%, two considerations had to be borne in mind. First, some spillover into 2027 was to be expected owing to lagged indirect effects. Thus, at the current juncture, forward measures at somewhat longer horizons might provide additional insights, as these would be free from shorter-term effects. Second, it was also important to take into consideration inflation risk premia, with measures of genuine inflation expectations – based on inflation compensation measures corrected for such premia – continuing to stand at around 2%. The April 2026 rounds of the Survey of Professional Forecasters and the Survey of Monetary Analysts showed that, while experts had sharply revised up their inflation expectations for 2026, expectations for the following years were broadly unchanged at levels close to 2%. That said, it was highlighted that the distribution of inflation expectations had shifted to the right, including for core inflation, in the short and medium term. The Consumer Expectations Survey showed that the inflation expectations of households had picked up noticeably beyond the short term. The median of the three-year ahead expectations had risen by 0.5 percentage points and currently stood just below the peak reached during the 2022 inflation surge, while the mean stood at an all-time high. Five-year ahead median expectations had moved up more marginally, although the mean had risen to the highest level on record, indicating movements in the tail of the distribution.

At the same time, it was remarked that survey data should be interpreted with some caution as any deterioration might be driven by sentiment rather than a material change in underlying fundamentals. As regards firms, it was noted that the Survey on the Access to Finance of Enterprises pointed to higher inflation expectations, mainly over the short term, but also showed significant and increasing upside risks over longer horizons.

Turning to labour costs, it was noted that, for now, the ECB’s wage tracker and surveys on wage expectations continued to indicate easing labour costs in the course of 2026. Looking ahead, the reduction in labour market tightness and the weakening economic outlook suggested that labour costs would continue to ease. While it was noted that some surveys, in particular the Corporate Telephone Survey and the Survey of Professional Forecasters, showed small upward revisions in expected wage growth, it remained to be seen whether this would be confirmed more systematically in wage agreements. In this regard, it was noted that wage agreements would likely only reflect the net outcome of the current counteracting trends as of 2027.

Against this background, members assessed that the risks to the inflation outlook were to the upside, with risks having intensified since the Governing Council’s previous monetary policy meeting in March. If energy prices were to rise by more and for longer than currently expected, euro area inflation would increase further. This could be reinforced and become more persistent if higher energy prices were to spill over by more than expected to other prices and to wages, if longer-term inflation expectations were to rise in response, or if global supply chains were disrupted more broadly. Ongoing trade tensions could also give rise to more fragmented global supply chains, curtail the supply of critical raw materials and worsen capacity constraints in the euro area economy. By contrast, inflation could turn out to be lower if the economic effects of the war in the Middle East proved to be more short-lived than currently expected or if indirect and second-round effects proved less pronounced. More volatile and risk-averse financial markets could weigh on demand and thereby lower inflation as well.

Turning to the monetary and financial analysis, members largely concurred with the assessment provided by Ms Schnabel and Mr Lane in their introductions. The war in the Middle East had caused significant volatility in global financial markets. Overall financial conditions had remained tighter than before the war. Nominal risk-free rates had risen and the forward curve had shifted upwards in the run-up to the meeting, with markets now pricing in about three 25 basis point interest rate hikes by the end of the year. Corporate and sovereign bond spreads had remained tight, while equity markets had been buoyant, having gained ground since the previous meeting not only in the United States but also in Europe. Financial market pricing, particularly in US risk asset markets, appeared somewhat complacent. There was a dissonance with the pricing in energy markets, where spot prices had risen substantially since the start of the war, and with the views of political analysts, who expected the closure of the Strait of Hormuz to be prolonged.

Several possible explanations were put forward for the apparent relatively benign pricing in financial markets. On the one hand, it could reflect lower dependence on fossil fuels than in the past pointing to greater economic resilience. Moreover, both hard data on corporate earnings and earnings expectations had been relatively positive. On the other hand, markets might not be sufficiently considering the potential for broad-based and long-lasting supply disruptions and for second-round effects. Equity market valuations, especially in the United States, seemed to be based on the assumption that neither the US Administration nor the Iranian authorities had any interest in a long-lasting conflict. If the assumption that the conflict would be settled in a month or two did not prove correct, there could be a sharp sell-off in equity markets.

Turning to financing conditions, the rise in risk-free rates had pushed up bank funding costs and was expected to lead to a further tightening of bank lending conditions for both firms and households. The cost of issuing market-based debt had risen to 3.9% in March, from 3.5% in February. Bank lending rates for firms – based on data recorded prior to the war – had edged down to 3.5% in February, while mortgage rates had remained at 3.4%. The annual growth rate of bank lending to firms had increased to 3.2% in March, from 3.0% in February, while the growth rate of corporate bond issuance had fallen to 3.9%, from 4.5% in February.

Credit standards for loans to firms had tightened in the first quarter, as reported in the latest bank lending survey for the euro area. Banks were tightening non-price lending conditions to manage risks more effectively, including applying stricter collateral standards, broader margins on high-risk loans and lower maximum loan amounts.

Monetary policy stance and policy considerations

Turning to the monetary policy stance, members assessed the data that had become available since the last monetary policy meeting in accordance with the three main elements that the Governing Council had communicated in 2023, and updated in July 2025, as shaping its reaction function, namely: (i) the implications of the incoming economic and financial data for the inflation outlook and the risks surrounding it; (ii) the dynamics of underlying inflation; and (iii) the strength of monetary policy transmission.

Starting with the inflation outlook, members widely agreed that the incoming information had been broadly consistent with the previous assessment of the inflation outlook, but that upside risks to inflation and downside risks to growth had intensified. Although the short-term outlook had deteriorated somewhat since March, with the latest developments in oil markets suggesting a move away from the baseline projections, the key issue for monetary policy was how significant the impact on inflation would be in the medium term. This depended on the extent to which the shock would lead to second-round effects and raise longer-term inflation expectations.

So far, there was little evidence that the increase in energy prices was generating second-round effects, although the probability of such effects would increase as the duration of the conflict increased, and second-round effects tended to appear with a lag. Their emergence depended on whether firms and consumers would absorb the higher energy prices or whether they would engage in a distributional battle that could lead to inflation becoming entrenched. Although firms had reported higher input prices as well as expectations of increases in their own selling prices, the extent to which they would be able to pass on the higher energy costs to final product prices remained an open question. The pass-through could be limited in view of the weakness of activity in the services sector, while the apparent robustness in manufacturing activity could to some extent be driven by stockpiling. On the consumer side too, it was still too early for second-round effects to be visible, since for this wage negotiations needed to take place.

As regards inflation expectations, the rise that had occurred to date had largely been limited to shorter horizons, with longer-term inflation expectations remaining overall well anchored. Risks were skewed to the upside, however, reflected in a fattening of the right tail of the distribution. While financial markets were pricing in a notable short-term inflationary impact of the conflict in the Middle East, measures of inflation compensation beyond short-term horizons suggested they saw a relatively fast return of inflation to target, in part owing to monetary policy tightening as embedded in market-based interest rate expectations.

At the same time, according to the Consumer Expectations Survey and the Survey on the Access to Finance of Enterprises, inflation expectations of both consumers and corporations had already increased. Inflation expectations of firms and consumers played a significant role, since these economic agents determined price and wage-setting. However, these surveys were relatively new, and the expectations of firms and consumers were more difficult to measure than, for example, market expectations. Moreover, there was evidence that the expectations of consumers and firms were correlated with energy prices, which limited their signalling value at the current juncture. Other indicators of medium and longer-term inflation expectations, based on market pricing and surveys, had remained well anchored at around 2%.

Members assessed that the upside risks surrounding the inflation outlook had intensified. It was now evident that the energy price shock was not only large, but also becoming more persistent, raising the risk of it feeding through into broader inflation dynamics.

There was a risk that oil prices would remain at current levels for a longer period than expected by markets. Supply-side disruptions could spread beyond oil to other products. Moreover, given the global nature of the energy price shock, its inflationary impact could be amplified via supply chains as imported intermediate goods and final consumer goods became more expensive, including imports from China. The extent to which consumers were already reacting to the increase in energy prices could be a sign that people were still keeping in mind the 2022 inflation surge. In the event of a prolonged conflict or an extended period of high energy prices, there was a risk that fiscal support measures would be expanded significantly, further increasing inflationary pressures.

Turning to underlying inflation, members concurred that indicators of underlying inflation had changed little over recent months. Wage growth indicators continued to suggest an easing, and there were no signs as yet that the conflict was leading to an acceleration in wage growth, given also that labour market conditions had been softening. Overall, this suggested a broadly unchanged wage outlook.

The transmission of monetary policy continued to be smooth and effective. The tightening of financial conditions since the onset of the war had already led to credit becoming more expensive and harder to obtain. The rise in the cost of bank funding was pushing banks to tighten financing conditions and credit standards for both firms and households. Tighter credit conditions, in turn, might be expected to further dampen demand for loans, for both consumption and investment. According to the bank lending survey, non-price lending conditions had also tightened, which mainly reflected prudent behaviour on the part of banks, driven by elevated macroeconomic uncertainty. It was nonetheless necessary to remain attentive to such shifts. It was important to monitor the extent to which these factors might constitute a drag on growth and offset some of the inflationary pressures.

Monetary policy decisions and communication

Against this background, all members agreed with the proposal by Mr Lane to keep the three key ECB interest rates unchanged. Members emphasised their collective commitment to setting monetary policy to ensure that inflation stabilised at the 2% target in the medium term.

The war in the Middle East had made the outlook significantly more uncertain, and the key factors determining the medium-term implications for inflation were the intensity and duration of the energy shock and, in particular, of the blockade of the Strait of Hormuz. The situation had evolved in several important ways since the Governing Council’s March meeting. It had now become clear that the conflict would last longer than had been expected, with the energy price shock proving more persistent and its repercussions broadening. The latest developments in oil markets suggested that the inflation outlook was moving away from the baseline scenario. In addition to the upside impact of the energy shock on inflation, the economy had already been weakening, held back by persistent uncertainty, with the decline in sentiment and confidence indicators underscoring the significant downside risks to economic growth. Such weakness could persist well beyond the end of the conflict.

Against this background, the energy price shock and associated supply disruption posed a dilemma for monetary policy. The combination of elevated energy prices, weakening confidence indicators and cooling growth gave rise to a complicated policy trade-off. Maintaining price stability might necessitate tighter monetary policy to prevent inflation expectations from becoming unanchored, even if this exacerbated the shock’s negative impact on the economy. The current situation of a classical negative supply shock was different from the situation in 2022, when the reopening after the pandemic had also led to strong demand forces pushing up inflation.

It was highlighted that the March staff baseline projections were conditional on two rate hikes by year-end. Even under these assumptions, inflation was projected to remain marginally above target in the medium term, and the projections did not take into account the rise in oil prices since the March meeting. So it had become increasingly likely that adopting a “looking through” approach was not appropriate. It was argued that this situation shifted the primary focus to determining the most appropriate timing for a rate increase.

In view of the ongoing uncertainty, it was advisable to adopt the strategy that was most robust across different scenarios. While the inflation outlook could be seen as shifting from the baseline scenario, alongside increasing downside risks to growth, keeping rates stable in April was seen as an appropriate course of action, to be accompanied by communication stressing the Governing Council’s readiness to act as needed.

Given limited signs of second-round effects and broadly anchored inflation expectations, members emphasised that the Governing Council could afford to gather further information before deciding to act. By June, more information on the impact of the energy shock would be available, including new projections featuring updated scenarios and additional data on inflation. This would include evidence on indirect and second-round effects, and on the anchoring of inflation expectations. At the time of the June meeting initial indications of how wages were reacting to the inflation increase would also be available, as well as more insights into the impact of the shock on economic growth, which would only become apparent with a lag.

By the time of the June meeting, there was also likely to be more clarity on the duration of the conflict, especially whether the market view that the situation could settle down in the next few weeks would be vindicated. If this did not happen, the euro short-term rate (€STR) forward curve could have shifted up substantially by the June meeting, and a prolongation of the conflict could activate stronger propagation mechanisms, including interrupted supply chains and actual shortages of energy and bottlenecks.

Finally, it was pointed out that financial markets had increased their rate hike expectations significantly since the start of the war and further over the past few days.

A number of members noted that the decision was a close call and that they would not have opposed raising rates at the current meeting had this been on the table.

Increasing interest rates at the current meeting would have sent an even stronger signal of determination to bring inflation back to target in a timely manner. The option value of waiting to raise policy rates had decreased since the last meeting, and it had become increasingly unlikely that a “looking through” approach without any monetary policy action would be appropriate.

These members viewed the negative supply shock as more pronounced than implied by expectations in the March staff projections and as indicating that supply bottlenecks might worsen, with inflationary pressures becoming more widespread and persistent. They noted that the adverse scenario published in March was becoming increasingly likely. The global nature of the current shock could be expected to amplify its impact on both inflation and growth, and it was emphasised that there was an increased likelihood of firms raising their prices in response to the energy price shock.

These members stressed their concerns regarding indirect and second-round effects, pointing to several surveys that had shown a rightward shift in the distribution of inflation expectations, or increasing upside risks over longer horizons. This suggested that risks of unanchoring had re-emerged, with long-term inflation expectations not being immune to the effects of changes in short-term expectations, highlighting their fragility after a long period of high inflation. Moreover, it was argued that pipeline price pressures had started to build, suggesting that the pass-through of higher input costs to consumer prices could be rapid, with potential for non-linear effects to materialise once again.

It was noted that the euro area economy had proved more resilient than expected over recent years, with a remarkable capacity to adapt to adverse shocks. If this resilience were confirmed in the current circumstance, the expected drag on aggregate demand might be insufficient to eliminate the growing risk of inflation settling above target over the medium term. In addition, it was risky to assume that the impact of the energy price shock on inflation would be limited by its concurrent effect on economic activity, particularly in view of other inflationary forces, such as the ongoing fiscal stimulus and the relatively tight labour market.

In spite of these concerns, all members were willing to rally behind the decision to keep policy rates unchanged, on the grounds that there was no acute urgency for a rate hike at the current meeting, provided that communication stressed the Governing Council’s firm commitment to setting monetary policy to ensure that inflation stabilised at the target in the medium term. Despite some metrics signalling a need for vigilance, the view was broadly shared that there was no evidence yet of strong second-round effects. Markets also seemed to have a good understanding of the Governing Council’s reaction function. Members concluded that while the effects of even a short-lived war might prove to be more enduring than expected, it was too soon to draw firm conclusions about their implications for monetary policy. If a conclusive agreement was reached to end the war, one could not exclude the possibility of a large reduction in the oil price, leading to a quick reversal in the risks to inflation, while damage to the real economy could last longer in light of the effects on confidence. Therefore, given the high degree of uncertainty surrounding the duration and economic impact of the conflict, holding rates at the current meeting was seen as a prudent and appropriate policy response.

Turning to communication aspects, members confirmed the adequacy of the well-established data-dependent and meeting-by-meeting approach, without pre-commitment to a particular rate path. This meant closely monitoring the emergence of possible second-round effects and reassessing all the information available, particularly as summarised in the June projections and scenarios. At the same time, communication should not give the impression that the Governing Council was inclined to look through the supply shock. Members stressed the need to signal vigilance and communicate that upside risks to inflation and downside risks to growth had intensified, while avoiding references to “full” optionality. It was seen as imperative to avoid the perception of being complacent.

It appeared that the ECB’s reaction function was well understood by markets. However, there still seemed to be a need to counter an apparent misperception among market analysts about the relation between policy options and the various scenarios. It was therefore important to clarify that the March baseline was predicated on two rate hikes.

As regards non-monetary elements in the ECB’s communication, it was important to reiterate the call for governments to keep fiscal responses to the energy price shock contained, and to continue undertaking structural reforms while accelerating the energy transition to reduce reliance on fossil fuels, noting that the succession of emergencies and crises posed risks to the medium-term transformation in Europe.

Looking ahead, the Governing Council would closely monitor the ongoing developments and reiterate its determination to set monetary policy to ensure that inflation stabilised at the 2% target in the medium term. The data-dependent and meeting-by-meeting approach meant closely monitoring the emergence of possible second-round effects and reassessing all the information available, particularly as summarised in the June projections and scenarios.

It was emphasised that the baseline and the scenarios needed to be regularly updated in the very uncertain environment, in line with the decisions taken in the 2025 monetary policy strategy assessment.

Taking into account the foregoing discussion among the members, upon a proposal by the President, the Governing Council took the monetary policy decisions as set out in the monetary policy press release. The members of the Governing Council subsequently finalised the monetary policy statement, which the President and the Vice-President would, as usual, deliver at the press conference following the Governing Council meeting.

Monetary policy statement

Monetary policy statement for the press conference of 30 April 2026

Press release

Meeting of the ECB’s Governing Council, 29-30 April 2026

Members

- Ms Lagarde, President

- Mr de Guindos, Vice-President

- Mr Cipollone

- Mr Demarco

- Mr Dolenc

- Mr Elderson

- Mr Escrivá*

- Mr Kazāks*

- Mr Kažimír

- Mr Kocher

- Mr Lane

- Mr Makhlouf

- Mr Müller

- Mr Nagel

- Mr Panetta

- Mr Patsalides*

- Mr Pereira

- Mr Radev

- Mr Rehn

- Mr Reinesch*

- Ms Schnabel

- Mr Šimkus*

- Mr Sleijpen

- Mr Stournaras

- Mr Villeroy de Galhau

- Mr Vujčić*

- Mr Wunsch

* Members not holding a voting right in April 2026 under Article 10.2 of the ESCB Statute.

Other attendees

- Mr Dombrovskis, Commissioner**

- Ms Senkovic, Secretary, Director General Secretariat

- Mr Kamps, Acting Secretary for monetary policy, Acting Director General Monetary Policy

- Ms Baumann, Deputy Head of Division, Directorate General Monetary Policy

- Mr Brand, Head of Section, Directorate General Monetary Policy

** In accordance with Article 284 of the Treaty on the Functioning of the European Union.

Accompanying persons

- Ms Bénassy-Quéré

- Ms Brezigar

- Mr Dewachter

- Mr Kaasik

- Mr Koukoularides

- Mr López

- Mr Lünnemann

- Mr Madouros

- Mr Martin

- Ms Mauderer

- Mr Nicoletti Altimari

- Ms Raposo

- Mr Rutkaste

- Ms Schembri

- Mr Šošić

- Ms Stiftinger

- Ms Tamoševičienė

- Mr Tavlas

- Mr ter Weel

- Mr Välimäki

Other ECB staff

- Mr Proissl, Director General Communications

- Ms Vansteenkiste, Counsellor to the President

- Ms Rahmouni-Rousseau, Director General Market Operations

- Mr Arce, Director General Economics

- Ms Nickel, Deputy Director General Economics

Release of the next monetary policy account foreseen on 9 July 2026.

EUR/USD Daily Outlook

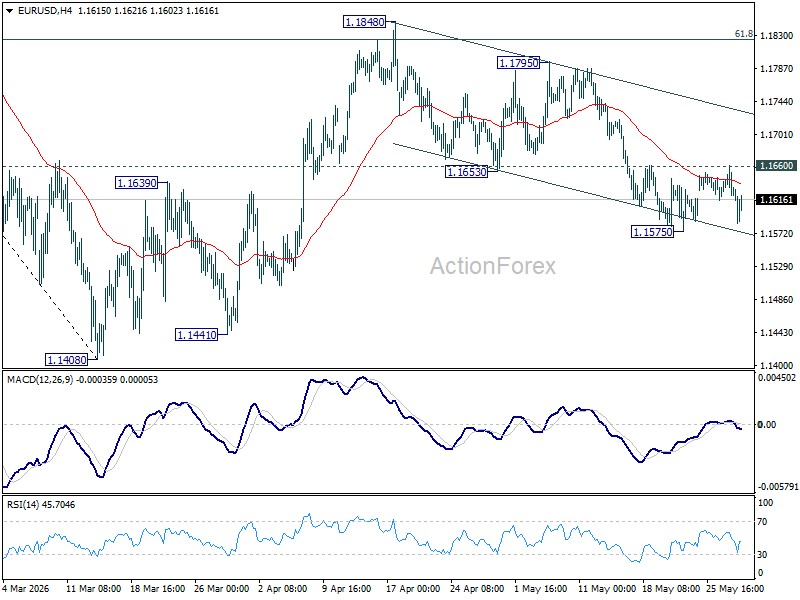

Intraday bias in EUR/USD remains neutral for the moment. On the upside, firm break of 1.1660 resistance will argue that fall from 1.1848 has completed as a correction at 1.1575. Intraday bias will be back on the upside for 1.1795 resistance first. On the downside, break of 1.1575 will solidify the case that rebound from 1.1408 has completed at 1.1848, and bring deeper fall back to retest 1.1408 low.

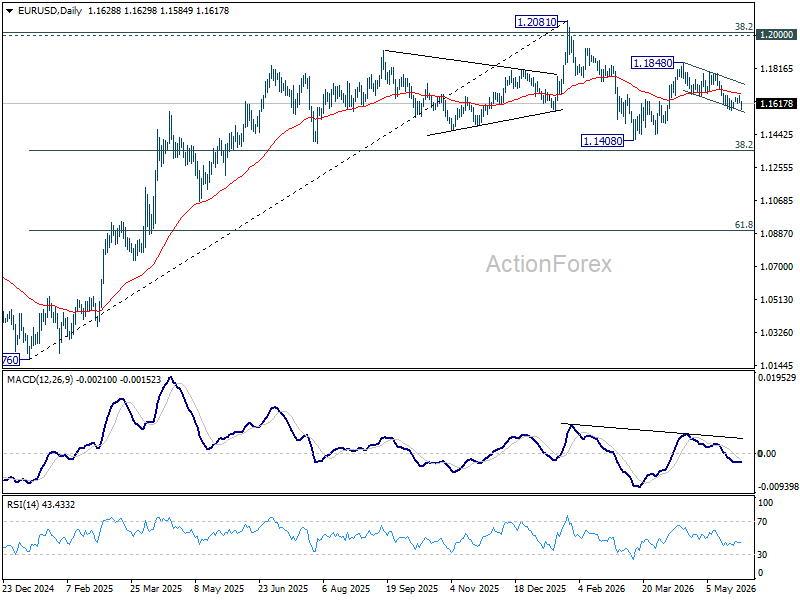

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1544). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

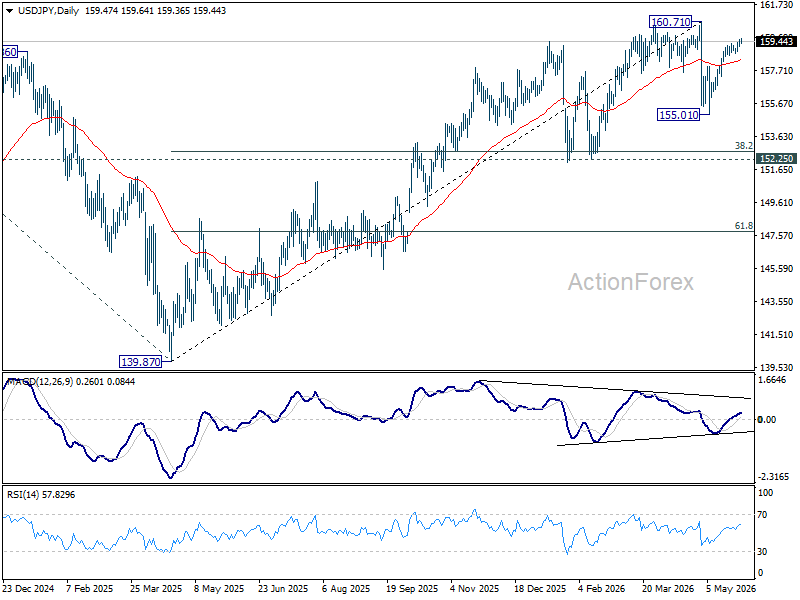

USD/JPY Daily Outlook

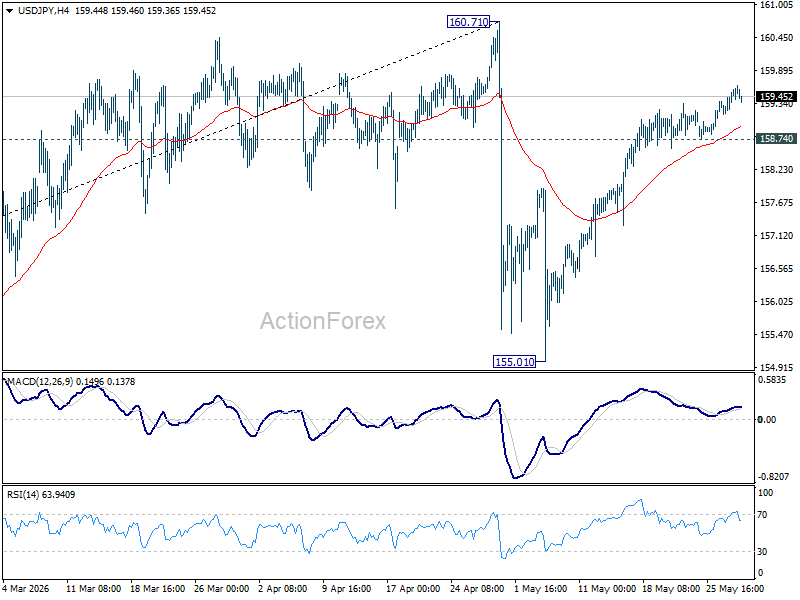

Intraday bias in USD/JPY remains on the upside for the moment. Rise from 155.01 is in progress for retesting 160.71 high. Strong resistance is expected from there to start the third leg of the near term corrective pattern. On the downside, break of 158.74 minor support will turn bias to the downside for 55 D EMA (now at 158.33) and below.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.53) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

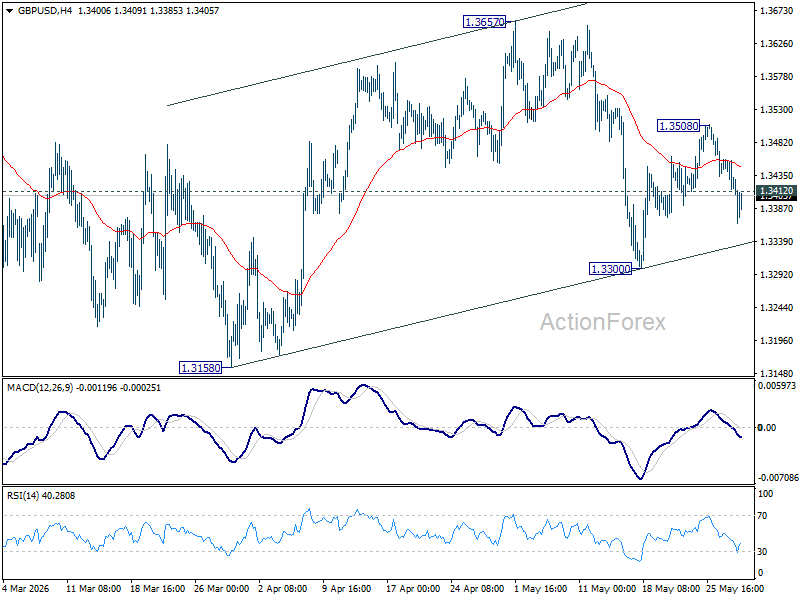

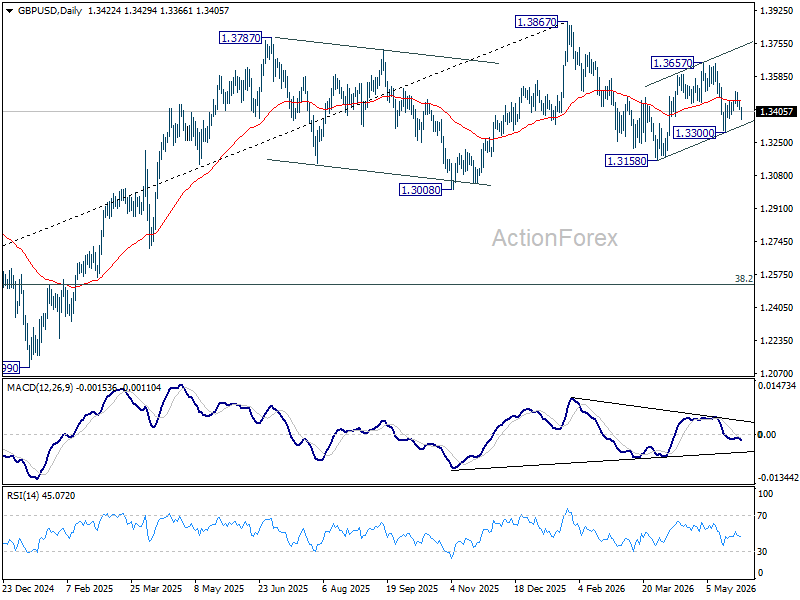

GBP/USD Daily Outlook

GBP/USD's break of 1.3412 suggests that recovery from 1.3300 has completed at 1.3508. Intraday bias is back on the downside. Break of 1.3300 will extend the fall from 1.3657 to 1.3158. On the upside above 1.3508 will extend the rebound from 1.3300 to 1.3657 resistance first.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

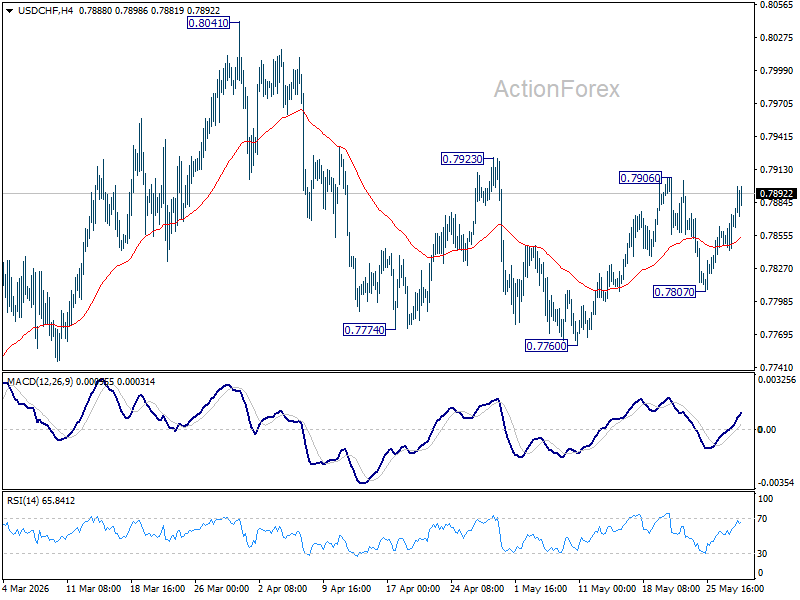

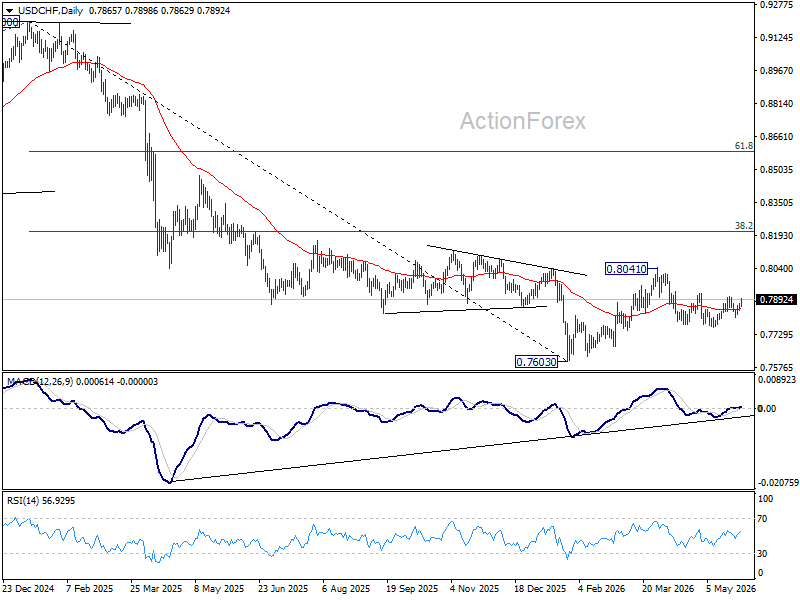

USD/CHF Daily Outlook

Intraday bias in USD/CHF remains neutral first. Firm break of 0.7906/23 will indicate that fall from 0.8041 has already completed as a correction. Further rally should be seen to retest 0.8041. On the downside, though, below 0.7807 will resume the fall from 0.8041 through 0.7760.

In the bigger picture, as long as 55 W EMA (now at 0.8035) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

AUD/USD Daily Report

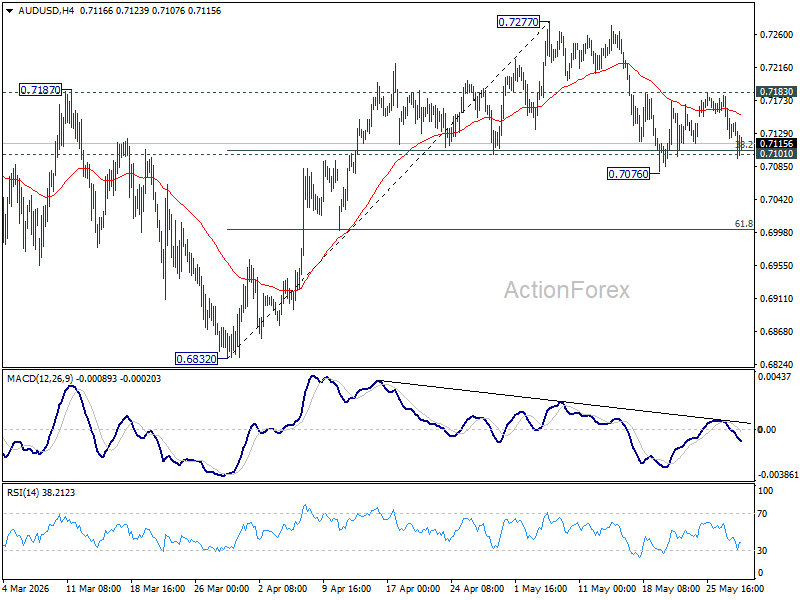

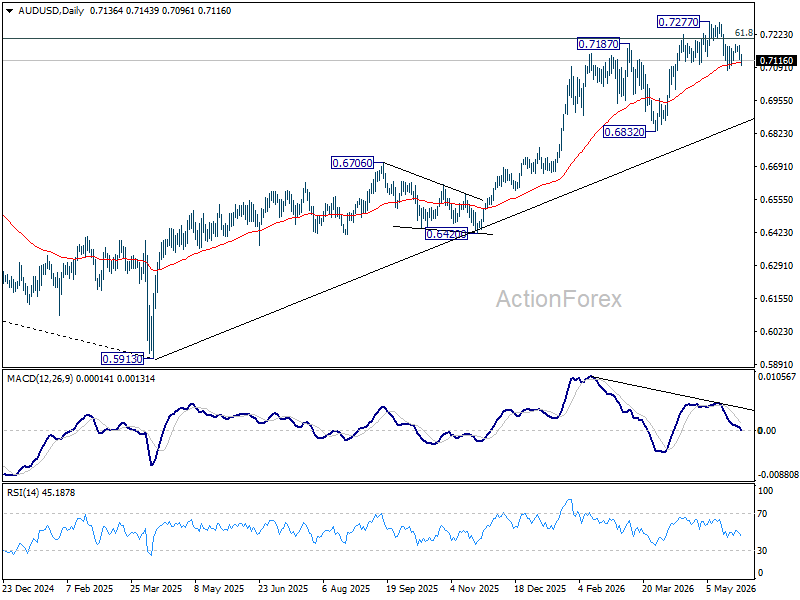

Intraday bias in AUD/USD remains neutral at this point On the upside, firm break of 0.7183 resistance will suggest that pullback from 0.7277 has completed. Stronger rally should then be seen to retest 0.7277 high. However, decisive break of 0.7076 will indicate that larger scale correction is underway and target 0.6832 support instead.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

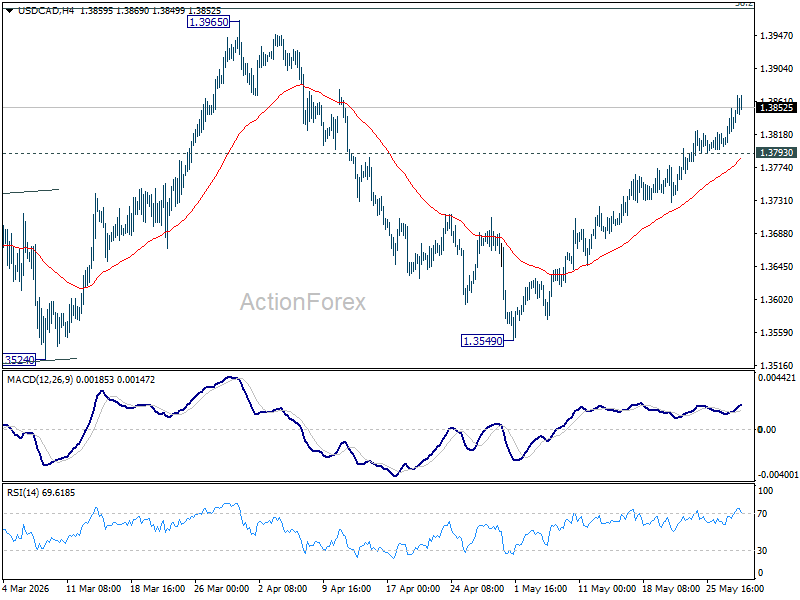

USD/CAD Daily Outlook

Intraday bias in USD/CAD remains on the upside at this point. Rise from 1.3549 is seen and the third leg of the pattern from 1.3480 and should target 1.3965 resistance. On the downside, below 1.3793 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

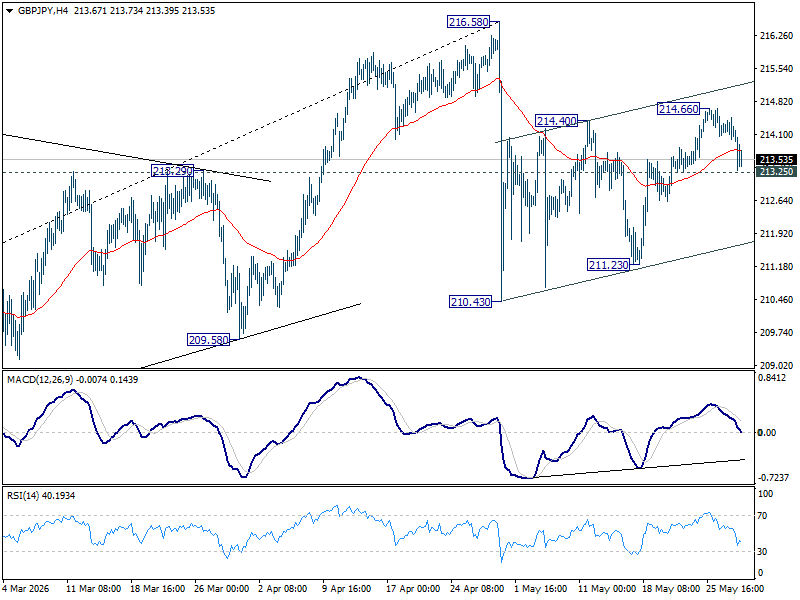

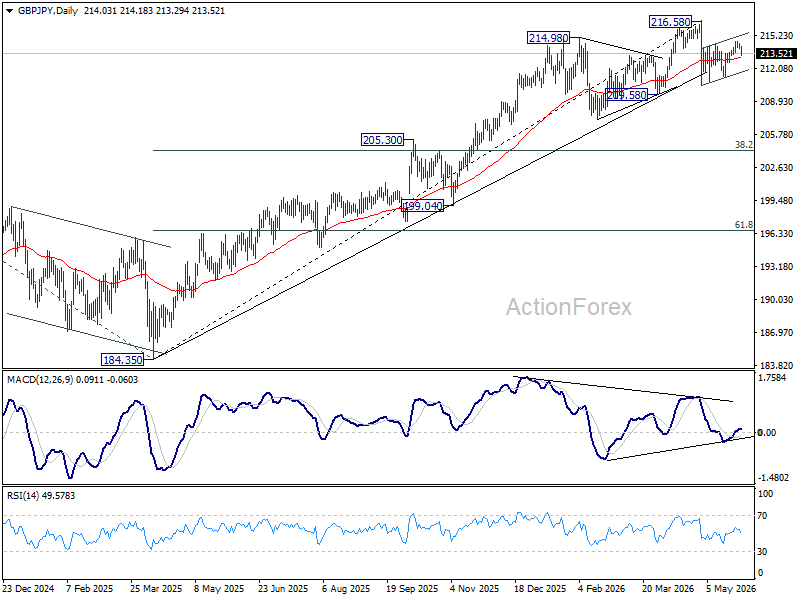

GBP/JPY Daily Outlook

Intraday bias in GBP/JPY remains neutral at this point. On the upside, above 214.66 will extend the rebound from 210.43 to retest 216.58 high. Strong resistance should be seen there to cap upside, at least on first attempt. On the downside, below 213.25 minor support will turn bias back to the downside for 211.23 support instead.

In the bigger picture, while the fall from 216.58 is steep, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 206.27) will argue that it's already in medium term down trend for 184.35 support.

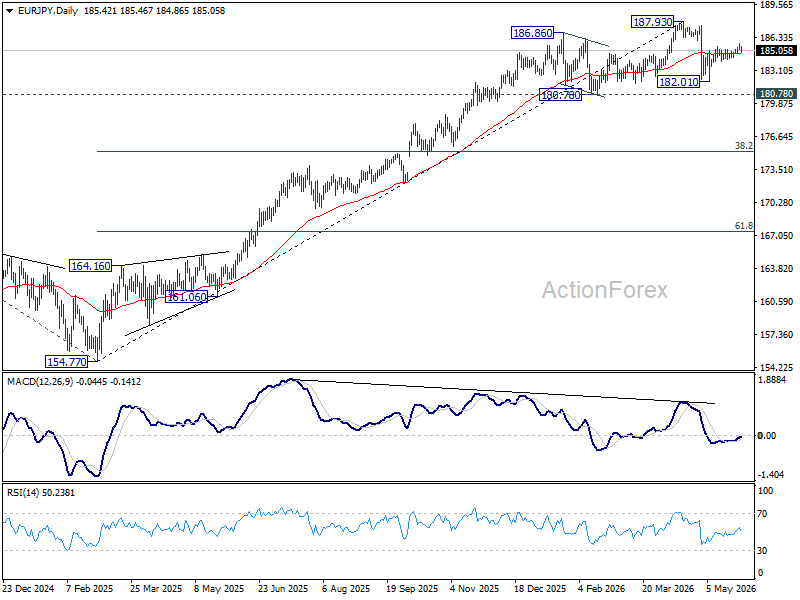

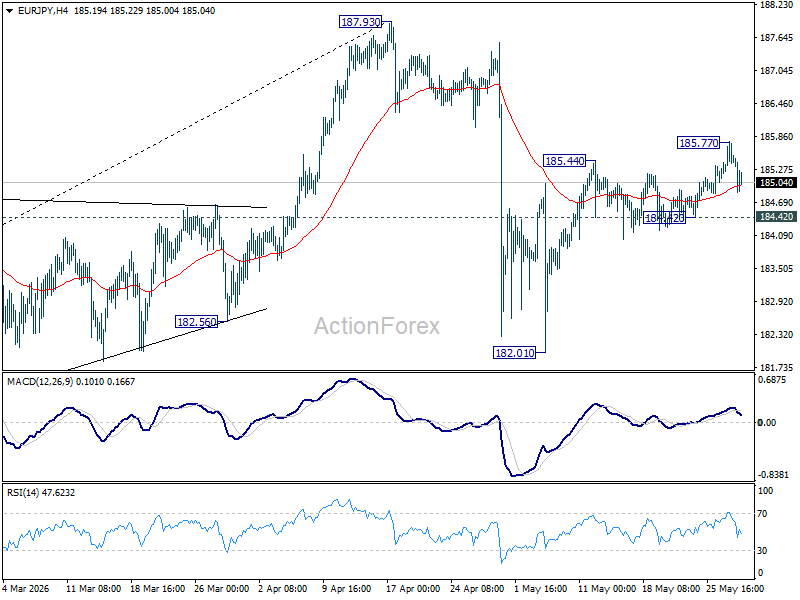

EUR/JPY Daily Outlook

Intraday bias in EUR/JPY is turned neutral again with current retreat. Rebound from 182.01 is seen as the second leg of the corrective pattern from 187.93. Above 185.77 will target a retest on 187.93 high. Nevertheless, firm break of 184.42 will suggest that the rebound has completed, and turn bias back to the downside for 182.01.

In the bigger picture, the pullback from 187.93 is steep, there is no sign of reversal yet. Uptrend from 114.42 (2020 low) is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 178.51) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.