Sample Category Title

S&P 500 Nabs Records on US-Iran Ceasefire Extension Amid Hot PCE Inflation Shock

Key takeaways

- Global equities climbed to fresh record highs after the US and Iran agreed to extend their ceasefire, boosting risk appetite and driving strong gains in technology and AI-related stocks.

- Hotter-than-expected US core PCE inflation at 3.3% y/y reinforced the “higher for longer” interest rate narrative, further reducing expectations for Federal Reserve rate cuts under new Fed Chair Kevin Warsh.

- AI infrastructure and enterprise technology spending remain the dominant market driver, with blockbuster developments from Anthropic, Snowflake, Amazon, and Dell reinforcing the ongoing AI capex supercycle despite growing concerns over potential overcapacity.

- Chart of the day: Nasdaq 100 minor bullish trend intact, en route to another potential fresh all-time high at 30,728/795 with key short-term support at 29,700.

Top macro headlines

- US and Iran agree to extend ceasefire: The S&P 500 and Nasdaq bounced back to hit fresh record highs on Thursday after the United States and Iran officially agreed to extend their ceasefire. US Treasury Secretary Scott Bessent confirmed that a permanent agreement to completely wind down the three-month-old war is within reach, provided Iran satisfies key conditions, including uranium disposal and fully reopening the Strait of Hormuz.

- US core PCE inflation jumps to 3.3% y/y, creating policy “wedge”: The Bureau of Economic Analysis released April's Personal Consumption Expenditures (PCE) report, revealing that headline PCE inflation rose to 3.8% y/y (up from 3.5% in March). More critically, core PCE inflation (excluding food and energy) climbed to 3.3% y/y, creating a rare inflationary "wedge" by running significantly hotter than core CPI (2.8% y/y), further squashing hopes for Federal Reserve interest rate cuts.

- Anthropic secures staggering $965 Billion valuation: Artificial intelligence startup Anthropic closed a massive $65 billion funding round, vaulting its private valuation to $965 billion and rocketing past OpenAI. The firm is tracking to hit a $50 billion annualized revenue run-rate next month after Q1 sales expanded 80-fold.

- Snowflake inks $6B Amazon deal as tech earnings explode: Defying fears that AI automation would kill traditional enterprise software providers, Snowflake surged up to 35% after signing a landmark $6 billion deal with Amazon and upgrading its full-year sales forecast. Concurrently, Dell Technologies skyrocketed 40% in after-hours trading, following blowout quarterly results.

Key macro themes

- The rare PCE-CPI inflation wedge: A significant structural challenge has emerged for newly confirmed Federal Reserve Chair Kevin Warsh. The Fed's preferred price barometer, the core PCE index, has broken higher to 3.3%, creating an unusual divergence from the 2.8% CPI benchmark. Because this underlying inflation spike stems directly from the Strait of Hormuz conflict choking global energy supplies, traditional monetary policy tools are constrained, and higher interest rates cannot lower oil transit costs but run the risk of severely bruising an already slowing economy.

- The K-shaped bifurcation of Wall Street vs. Main Street: The latest macro data dump exposes a profound macroeconomic split. Corporate profit margins remain near record highs as companies exploit structural supply shortages and the ongoing AI capex boom to drive revenues. Conversely, Main Street consumers are under acute duress; the U.S. personal savings rate plummeted to a near-historic low of just 2.6% in April, a level eclipsed in weakness only once in the past 18 years, as soaring gas prices near $5 a gallon erode real wage growth.

- AI Infrastructure overcapacity skepticism: Despite record-breaking stock market indices, a distinct undercurrent of institutional skepticism is building regarding the trillions of dollars pouring into AI capital expenditures. Several portfolio managers are warning of near-term overcapacity as commercial entities experience budget fatigue; for instance, Microsoft has begun cutting internal Claude code licenses due to prohibitive costs, while Uber has already entirely exhausted its 2026 AI coding capital allocation.

Global market impact (last 24 hours)

Equities: Wall Street rallied forcefully, with the S&P 500 gaining 0.6% to close at 7,563, while the tech-heavy Nasdaq 100 outperformed, hitting a fresh all-time high with a gain of 0.8%. Overall, Technology (1.4%) and Healthcare (1.3%) led, while defensive sectors, Consumer Staples (-0.6%) and Utilities (-1%) underperformed. Conversely, European bourses fell, with the FTSE 100 shedding 0.7% and DAX dropping 0.3%.

Fixed Income: Sovereign bond yields edged lower following the extension of the Middle East truce. The benchmark U.S. 10-year Treasury yield fell by roughly 3 basis points to anchor at 4.45% as the sovereign yield curve bull-flattened.

FX: The U.S. Dollar Index weakened by 0.2%, pulling the USD/JPY pair away from the critical 160.00 intervention line. Risk-sensitive currencies, the New Zealand Dollar (NZD) and Australian Dollar (AUD), led the G10 currencies higher with gains of 0.6% and 0.3% against the USD, while the South African Rand (ZAR) outperformed across emerging markets.

Commodities: Crude oil prices extended losses, with Brent and WTI crude hitting close to six-week lows of $92.41/bbl and $88.52. In contrast, precious metals rebounded, supported by a pull-back in longer-term US Treasury yields, with spot gold surging 0.9% to settle at $4,496/oz, still below the 20-day moving average at $4,585/oz.

Asia Pacific impact

- Equity and currency volatility: Before the late-session Wall Street ceasefire bounce, regular-hour Asian equity benchmarks fell by up to 1% as they digested sticky global yields. Currencies stabilized slightly following the 0.2% drop in the greenback, relieving pressure on the Japanese yen near the 160 psychological threshold. Asia Pacific benchmark stock indices recovered sharply in today’s Asia opening session; Nikkei 225 (+1.9% to record high), Hang Seng Index (+0.4%), China A50 (+0.5%), KOSPI (+2.2% to record high), ASX 200 (+1%), and STI (+ 0.7%).

- Corporate labour and tech supply chains: Highlighting an immense structural divergence, Samsung Electronics' advanced chip workers secured a historic 10-year corporate pay package including bonuses of up to $416,000. These massive wins by a regional bellwether are expected to significantly harden the bargaining positions of other domestic unions, introducing structural wage inflation into the region.

- Derivative infrastructure race: Financial localization is accelerating. While U.S. exchanges prepare to launch futures contracts tied to raw computing rental power, China is actively designing a brand-new futures market for AI tokens used to price localized AI services, sparking a structural derivatives race with Washington.

Top 4 events to watch today

- Japan Consumer Confidence (May) - 1:00 pm SGT (consensus:32, Apr:32.2) Impact: USD/JPY, JPY crosses, Nikkei 225

- Germany Harmonised Inflation Rate Prelim (May) - 8:00 pm SGT (consensus: 2.8% y/y, Apr: 2.9%) Impact: EUR/USD, EUR crosses, DAX

- Fed Speak - Bowman (9.10 pm SGT), Paulson (9.15 pm SGT) Impact: Short-end US Treasuries, USD, US stock indices

- US-Iran peace deal news flows Impact: All asset classes

Chart of the Day - Nasdaq 100 Bullish Trend Intact

Fig. 1: US Nasdaq 100 CFD minor trend as of 29 May 2026 (Source: TradingView).

The intraday decline of 2% seen in the US Nasdaq 100 CFD (a proxy of the Nasdaq 100 E-mini futures) measured from Wednesday, 27 May US session high to Thursday, 28 May Asia session low has hit an inflection level at 29,700.

Thereafter, it staged a bullish reversal, which suggests that its minor uptrend phase from the 19 May 2026 low remains intact.

Watch the 29,700 key short-term pivotal support, and a clearance above 30,425 sees the next intermediate resistances coming in at 30,728/795 (upper boundary of the ascending channel & Fibonacci extension cluster) and 31,050 (Fibonacci extension).

On the other hand, a break and an hourly close below 29,700 negates the bullish tone for a minor corrective decline to expose the next intermediate supports at 29,433 and 29,110 (also the 20-day moving average).

RBNZ Hints at Bigger Hikes as Kiwi Surge Accelerates: NZD/JPY and AUD/NZD Analysis

The New Zealand Dollar extended its powerful rally on Friday as investors interpreted the latest comments from Reserve Bank of New Zealand officials as a signal that the tightening cycle could restart sooner — and perhaps more aggressively — than previously expected. Markets had already viewed July as a live meeting after this week's dramatic hawkish hold, but subsequent remarks from policymakers today have raised a more important question: not whether rates will rise, but how large future hikes may ultimately be.

Governor Anna Breman delivered the strongest signal, stating that "on balance, the OCR is likely to increase sooner and by more than previously signaled." Meanwhile, MPC member Hayley Gourley argued that acting earlier offered the best chance to keep inflation expectations anchored and later emphasized that the data received before July would determine "the speed and the magnitude of change." Those remarks have encouraged traders to consider the possibility that the RBNZ may eventually need to move more aggressively if the inflationary effects of the Middle East energy shock become increasingly embedded in the economy. Even policymakers who voted to hold rates this week continue to argue that OCR increases will be needed.

Currency markets have responded quickly to the evolving policy outlook. NZD/JPY has emerged as one of the clearest beneficiaries as investors contrast a hawkish RBNZ with the cautious Bank of Japan. Japan's latest inflation figures showed further moderation in Tokyo CPI, reinforcing expectations that the BoJ is unlikely to rush into additional tightening.

That widening policy gap has pushed NZD/JPY to the verge of a major breakout. Sustained move above 94.96 would mark the highest level since 2024 and confirm continuation of the broader uptrend from last year's low at 79.79. Next target will be 61.8% projection of 85.33 to 94.96 from 90.55 at 96.50. Near term outlook will stay bullish as long as 92.89 support holds, in case of retreat.

The same divergence theme is driving AUD/NZD sharply lower. Earlier this year, the Reserve Bank of Australia was widely seen as the more aggressive central bank after delivering three rate hikes. However, weaker Australian inflation data this week and recent signs of labor-market cooling have reduced expectations for further near-term tightening. With a June hold effectively locked in and August no longer certain, attention has shifted toward the possibility that the RBNZ may now be the central bank playing catch-up.

Technically, 1.2283 is seen as a medium term top in AUD/NZD, on bearish divergence condition in D MACD. Risk will stay on the downside as long as 1.2132 support turned resistance holds. Deeper fall would be seen to 1.1922 (38.2% retracement of 1.1412 to 1.2283 at 1.1950).

Strong rebound from 1.1922 will keep the corrective pattern from 1.2283 a sideway consolidations pattern only. However, firm break of 1.1922 will argue that it's already correcting the whole five wave rally from 1.0649, and set up deeper fall to 38.2% retracement of 1.0649 to 1.2283 at 1.1659 in the medium term.

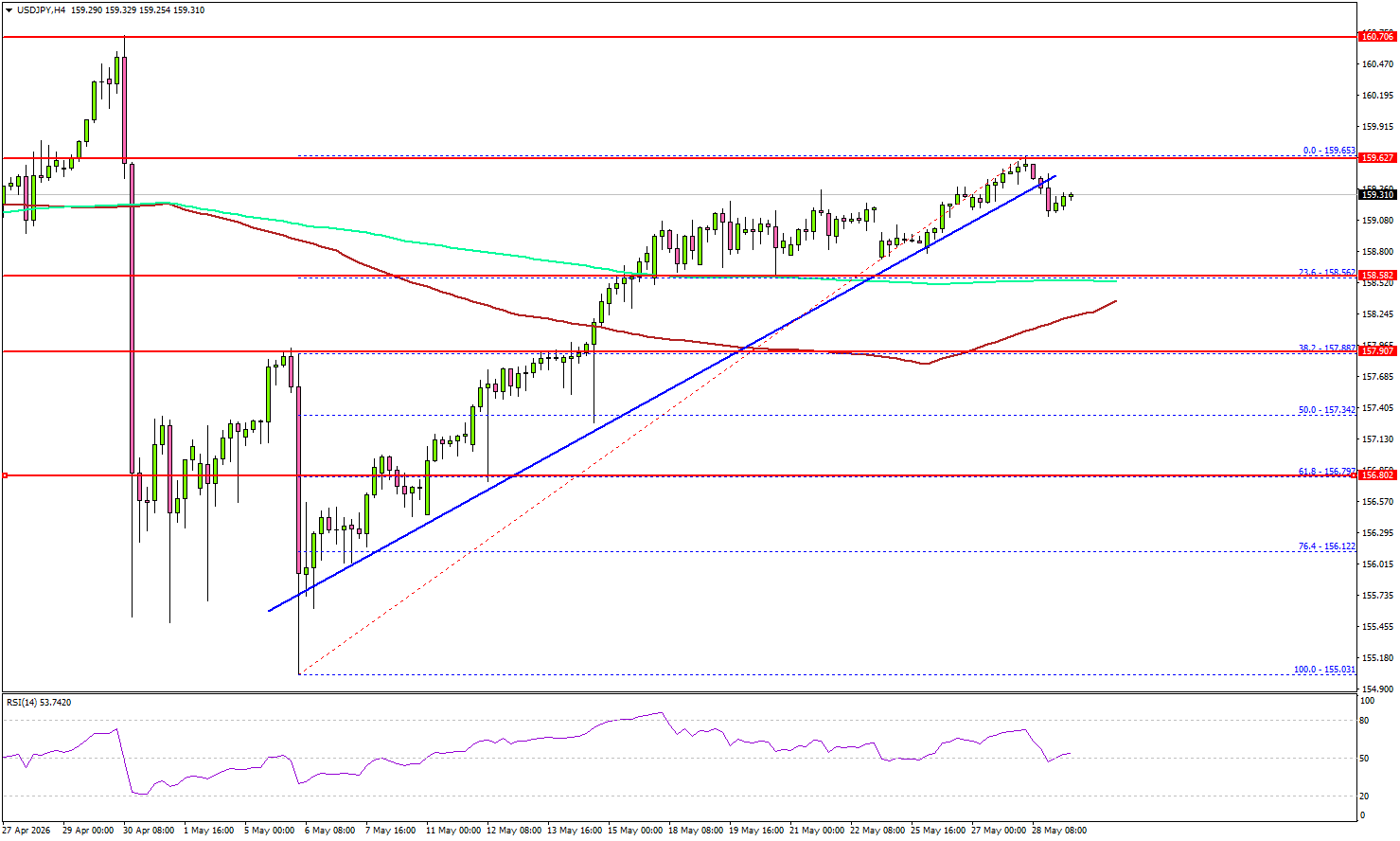

USD/JPY Upside Exhaustion Signals Raise Pullback Concerns

Key Highlights

- USD/JPY seems to be struggling to clear the 159.65 resistance.

- It traded below a bullish trend line with support at 159.40 on the 4-hour chart.

- EUR/USD is still struggling to clear the 1.1675 resistance zone.

- Gold corrected some losses and tested the $4,525 resistance.

USD/JPY Technical Analysis

The US Dollar climbed above 158.50 and 158.80 against the Japanese Yen. USD/JPY even surpassed 159.20 before the bears appeared.

Looking at the 4-hour chart, the pair settled above the 158.50 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). However, it faced resistance near the 159.65 zone.

A high was formed at 159.65, and the pair is now correcting some gains. There was a move below a bullish trend line with support at 159.40. If the pair extends losses, it could test the 23.6% Fib retracement level of the upward move from the 155.03 swing low to the 159.65 high.

The first major support sits near the 158.50 level and the 100 simple moving average (red, 4-hour). The next support could be 157.85. A close below 157.85 might initiate a drop to the 61.8% Fib retracement level of the upward move from the 155.03 swing low to the 159.65 high at 156.80.

Any more losses might open the doors for a drop toward the 156.00 zone. On the upside, the pair could face resistance at 159.65. The next major resistance could be 160.00. A close above 160.00 could open doors for gains above 160.50. In the stated case, the bulls could aim for a move to 162.00.

Looking at EUR/USD, the pair is attempting to recover some losses, but it faces a major hurdle near the 1.1675 region.

Upcoming Key Economic Events:

- Fed's Bowman speech.

- Fed's Paulson speech.

- Chicago PMI for May 2026 – Forecast 49.7, versus 49.2 previous.

RBNZ Hawks Signal Rate Hikes Are Coming, July Meeting Now Live

Fresh comments from senior Reserve Bank of New Zealand officials today reinforced the hawkish message delivered at this week's policy meeting, strengthening the case that interest rate hikes are approaching and putting the July meeting firmly in play. While the RBNZ left the Official Cash Rate unchanged at 2.25%, the decision was split 3-3, with Governor Anna Breman casting the deciding vote to hold. The subsequent commentary suggests policymakers are no longer debating whether rates need to rise, but rather when the tightening cycle should resume.

Among the most hawkish voices was Monetary Policy Committee member Hayley Gourley, who voted for an immediate rate increase. Gourley told Reuters that the policy path points to change "sooner rather than later" and argued that acting early would provide the best opportunity to keep inflation expectations anchored.

"My view was that by increasing sooner rather than later, we had the best opportunity to keep inflation expectations anchored and therefore minimize the negative impact inflation may have for the economy," Gourley said. She also stressed that incoming data over the next five to six weeks would determine "the speed and the magnitude of change," effectively confirming that July is a live meeting.

Even officials who supported holding rates signaled that higher borrowing costs are likely ahead. Assistant Governor Karen Silk acknowledged that higher oil prices from the Middle East conflict will inevitably flow through to broader inflation pressures. "We can't have the oil price shock that we've had without it having some flow through further down the line," Silk said, adding that "you do need to have an increasing OCR to lean against that." Importantly, she rejected the idea that policymakers should simply wait for more quarterly inflation data before acting, stating that "we have always got to be forward looking."

Governor Anna Breman reinforced the shift in guidance, stating that "the OCR is likely to increase sooner and by more than previously signalled." Taken together, the comments suggest the RBNZ is increasingly concerned that the energy shock could become embedded in inflation expectations even as economic growth slows. While policymakers remain divided on timing, there now appears to be broad agreement that higher rates will be required.

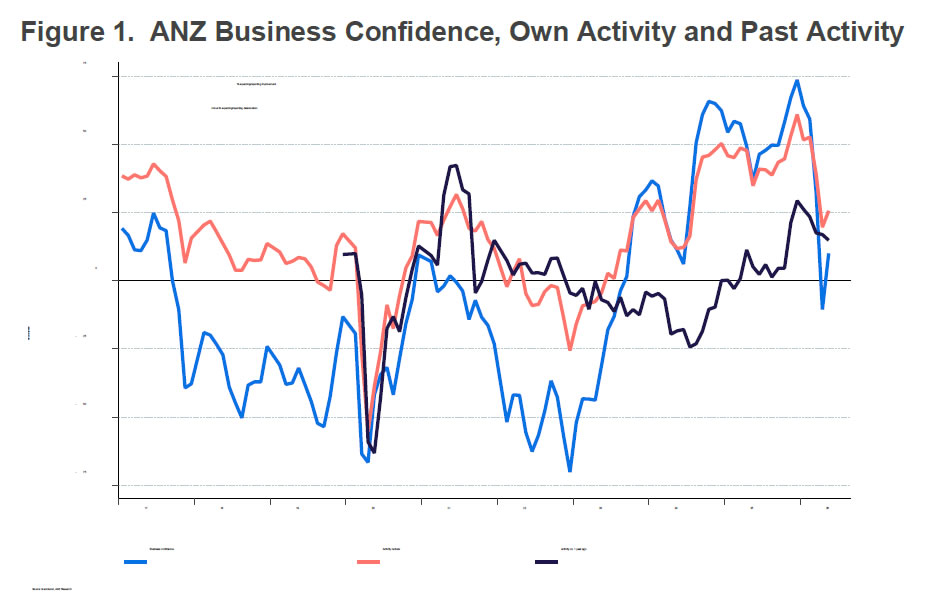

New Zealand ANZ Business Confidence Turns Positive, Inflation Pressures Stay Contained

New Zealand business sentiment improved sharply in May, suggesting firms are gradually adapting to the economic shock created by the Middle East conflict. ANZ Business Confidence jumped from -10.6 to 10.0, returning to positive territory, while firms' Own Activity Outlook rose from 19.6 to 25.6. The rebound indicates that some of the initial pessimism triggered by surging energy prices and global uncertainty has faded, although confidence remains well below levels seen before the conflict began.

Beneath the headline improvement, however, the survey painted a more mixed picture. Inflation expectations one year ahead eased from 3.81% to 3.63%, while wage expectations edged down from 2.53% to 2.48%. Employment intentions also improved notably, rising from -2.7 to 3.4, suggesting firms have become somewhat more optimistic about hiring.

ANZ noted that activity indicators remain considerably weaker than before the conflict, with retail and construction sectors continuing to struggle while agriculture and manufacturing have proven more resilient.

For the Reserve Bank of New Zealand, the survey may offer some reassurance that medium-term inflation pressures remain contained despite elevated headline inflation. ANZ emphasized that wage intentions provide a better guide to underlying inflation than short-term inflation expectations, and both measures remain below pre-conflict levels.

According to the ANZ, firms continue facing rising costs and profitability pressures but have limited ability to pass those costs on to customers in a soft demand environment. That dynamic may help contain broader inflation pressures even as the RBNZ continues preparing markets for likely OCR hikes later this year.

| Indicator | Previous | Actual |

|---|---|---|

| ANZ Business Confidence | -10.6 | 10.0 |

| Own Activity Outlook | 19.6 | 25.6 |

| Inflation Expectations (1-Year) | 3.81% | 3.63% |

| Employment Intentions | -2.7 | 3.4 |

| Wage Expectations (1-Year) | 2.53% | 2.48% |

Tokyo Inflation Cools Further, But Strong Growth Data Keeps BoJ Normalization on Track

Japan's inflation picture softened further in May, but the broader economy continued showing surprising resilience. Tokyo CPI core (excluding fresh food), widely viewed as a leading indicator of nationwide inflation trends, slowed from 1.5% yoy to 1.3% yoy, below expectations and marking the sixth consecutive month of deceleration. Headline inflation eased from 1.5% yoy to 1.4% yoy, while the closely watched core-core measure, excluding both fresh food and energy, slowed from 1.9% yoy to 1.6% yoy.

The decline in inflation was largely driven by government subsidies aimed at reducing utility, water, and tuition costs. However, policymakers are unlikely to take too much comfort from the softer readings. Analysts generally expect inflation to reaccelerate later this year as the impact of surging oil prices and a weak Yen feeds through to import costs. The persistence of Middle East-related energy risks remains particularly important for Japan, which remains heavily dependent on imported energy.

At the same time, activity indicators released for April painted a considerably stronger picture of the economy than expected. Industrial production rose 0.8% mom, sharply outperforming forecasts for a contraction. Manufacturers surveyed by the government expect output to surge another 5.1% in May. Retail sales also surprised to the upside with a 2.1% yoy increase, suggesting consumer demand remains relatively healthy despite higher living costs. The labor market also strengthened, with the unemployment rate falling from 2.7% to 2.5%, its lowest level in several months.

Taken together, the data reinforces that underlying economic conditions remain firm even as inflation temporarily cools. While softer CPI may reduce pressure for immediate tightening, resilient growth, a tight labor market, and expectations of renewed energy-driven inflation should keep policy normalization firmly on the table in coming months.

| Indicator | Previous | Forecast | Actual |

|---|---|---|---|

| Tokyo CPI Core (YoY) | 1.5% | 1.5% | 1.3% |

| Tokyo CPI Core-Core (YoY) | 1.9% | 1.6% | |

| Tokyo CPI Headline (YoY) | 1.5% | 1.4% | |

| Industrial Production (MoM) | -0.4% | 0.8% | |

| Industrial Production Outlook (May) | 5.1% | ||

| Industrial Production Outlook (June) | -0.4% | ||

| Retail Sales (YoY) | 1.4% | 1.3% | 2.1% |

| Unemployment Rate | 2.7% | 2.7% | 2.5% |

Gold (XAUUSD) Price Action Strong Elliott Wave Impulsive Reaction from Key Support Zone

The short‑term Elliott Wave view in Gold (XAUUSD) shows that the yellow metal has completed a three‑swing correction from the April 17, 2026 high. The pullback unfolded as a zigzag, with wave A ending at $4499.92 and wave B at $4773.58. Gold then declined in wave C to $4365.13, completing wave (2) as seen on the one‑hour chart. This level sits inside the key support zone, where wave C equals the 100%–161.8% Fibonacci extension of wave A. The broader support area spans $4137–$4380.

After testing this zone, Gold began a strong impulsive rally. The advance signals renewed momentum, but confirmation requires a break above the April 17 peak at $4890.97, which marked the end of wave (1). In the near term, wave (i) of the new cycle should finish soon. A corrective pullback in wave (ii) is expected, addressing the cycle from the May 28, 2026 low before the rally resumes. As long as the pivot at $4365.13 holds, pullbacks should attract buyers. These retracements are likely to form in three or seven swings, supporting further upside. The structure suggests Gold has shifted from correction to impulsive advance, with the support zone providing the base for the next bullish phase.

Spot Gold (XAUUSD) 60-Minute Elliott Wave Chart

XAUUSD Elliott Wave Video:

https://www.youtube.com/watch?v=aOmnScRdvPw

Cliff Notes: AI Goes From Strength to Strength

Key insights from the week that was.

Australia’s main market event this week was the April CPI which came in slightly below consensus on a headline basis (0.4%, 4.2%yr). Volatile, policy-driven components related to travel drove the outcome – the Federal Government’s temporary halving of fuel excise and some state governments offering free public transport, while cancelled flights and refunds for holiday travel provided a partial offset. These dynamics were also the main factors behind household spending's April decline.

Trimmed mean inflation meanwhile met expectations (0.3%, 3.4%yr). Pass-through of higher fuel costs is evident in some areas – home-building costs registered its strongest monthly gain since November 2023. However, the pass-through is not unfolding as rapidly as we initially feared. While April’s outcome will give the RBA space to pause and assess in June, the risk of a larger and faster pass-through in coming months is material. We believe the RBA will feel compelled to resume raising the cash rate in the second half of the year as these risks crystalise.

In the run-up to Q1 GDP next Wednesday, we also received two partial indicators for investment.

Construction activity rose 3.4% in Q1, pushing annual growth to 6.3%yr. This outsized gain was mostly driven by a large mining infrastructure installation in WA – lumpy completions like these have a much smaller impact on National Accounts estimates which are reported on an accrual basis. Activity was weak elsewhere, residential construction dipping 0.6% despite a solid project pipeline, and public infrastructure works trending lower, down –3.2%.

Private CAPEX subsequently surprised to the upside, surging 6.5% in Q1 to be up 14.6% over the year. Data centres were responsible for almost all the increase: machinery and equipment spending in the information and telecommunications sector almost tripling (+196%) in Q1 alone. It should be noted that the net impact on GDP will be limited given the high import component of the data centre build-out. The second estimate of 2026/27 CAPEX plans provided an upgrade; adjusting for inflation, real investment intentions remained resilient as the Middle East conflict began.

While these headline estimates have their caveats, the underlying detail suggests there is some modest upside risk to Q1 GDP. Our preview will be published later today on Westpac IQ.

This week’s offshore data provided little fresh signal and, for the market, paled in significance to perceived progress towards a truce in the Middle East. Intermediated negotiations between the US and Iran continued throughout the week despite several US strikes on Iranian military assets in the Strait, which were perceived to be active threats to shipping and dealt with. The successful transiting of several ships was instead focused upon as evidence to an end to the conflict was near. Having tested the top of 2026’s range early last week, circa US$110 per barrel, the price of Brent crude has since fallen to around US$94.

As we go to press, reports suggest a 60-day ceasefire has been agreed to by the US and Iran, but this time it includes a full resumption of shipping through the Strait within a month. The intent is to allow supply of energy and other goods to resume, alleviating stress on the Iranian and global economy, while negotiations continue over Tehran’s nuclear program. President Trump still needs to agree to the deal, however. And, further ahead, while November’s US mid-term elections will, if necessary, arguably warrant an extension of the ceasefire to year end, the complexity and significance of the nuclear negotiations could see the conflict flare again in 2027. For the foreseeable future, the price of oil and downstream margins are likely to depend not only on the current balance of physical demand and supply, but also a heightened awareness of political risk.

Of this week’s US data, releases related to the consumer were most notable. The second estimate for US GDP was revised down from 2.0% annualised to 1.6%, in large part due to weaker consumption growth. At 1.4% annualised, the current consumer pulse is well below the historic trend circa 2.5% and looks to be entrenched – real personal consumption up just 0.1% in April as wage growth failed to keep pace with inflation (0.2%). Housing is also clearly under pressure, S&P Cotality house prices falling for a second consecutive month (-0.2%, +0.8%yr), and new home sales down 6.2% in April after March’s gain was halved from 7.4% to 3.4%.

FOMC members prioritising inflation risks is notable given the subdued pulse for housing demand. While market participants have been debating the probability of a fed funds rate hike(s) over the coming year, for activity it is the implications for the long end of the yield curve that matter most. The FOMC may find they do not need to hike, as we currently forecast, because inflation risks and fiscal uncertainty result in a modest uptrend in the US 10-year yield. Since mid-April, the US 10-year has risen as much as 40bps to 4.67% because of these factors. Now at 4.44%, we see it rising to 4.75% by mid-2028.

Peering Below the Surface

Topline data, on their own, can mislead. It pays to look below the surface to see the underlying trend.

- Headline data can sometimes mislead. One needs to delve into the detail to get the full story. Headline inflation was softer than expected in April, but underlying trends told a different story. Likewise, employment growth was weak in the month, but this was mostly seasonal and hours worked told a different story. Productivity growth is also likely to have been weak in Q1; again, business investment data give reason not to despair about the trend.

- The RBA has the knowledge and resources to delve into the detail and not be misled by the surface figures. It is clearly concerned about the possibility that the energy price shock will pass through to other prices at scale, keeping inflation high. New detailed datasets have become available that allow its staff to quantify some important relationships more accurately.

- The economy is a complicated thing, though, and it is possible that the RBA’s analysis of the outlook is missing some important trends and relationships. Structural change is especially hard to grapple with. Shifts in labour market trends and the consequences of the data centre boom might be being misunderstood, though hopefully not for long.

Recent data have tended to tell a different story than the headline figures would suggest. Headline inflation was soft in April, but underlying measures were still too high and, if anything, still drifting up. Employment was even weaker than seasonal patterns implied in the month, but the hours worked data told the opposite story. And productivity growth is likely to be reported to have been weak in the March quarter, but this is partly because much data centre investment is in the build phase, and will only add to GDP and productivity later.

These contrasts are all examples of why one can be misled by focusing on a few headline figures. Accurately assessing the state of the economy requires a considered view of the whole picture. There is no substitute for delving into all the data detail.

In doing so, one must also guard against seizing on the data detail that fits your preferred narrative. For example, we remain concerned that pass-through of fuel prices to the prices of other goods and services will be extensive, and we are seeing some evidence of pass-through in homebuilding costs and hospitality already in the April CPI. It is nonetheless also true that pass-through has so far been a bit less than we feared.

The RBA understands the subtleties of Australia’s economic data and has the resources to look below the surface properly. It will not jump to rash conclusions based on headline numbers. It will, however, want to take a pause to assess how dominant and lasting these below-the-surface trends will be.

To the extent that we can glean anything from the RBA’s latest communications, it is that – like us – they are worried about second-stage pass-through of energy costs. Recent research, which was presented to the May meeting of the Monetary Policy Board and discussed in a subsequent speech by the RBA’s chief economist, highlights that pass-through is larger and faster following a large shock than after a small one.

This is not exactly a new result. The RBA has known that the “Phillips curve” relationship between inflation and labour market slack is nonlinear for about three decades. Their main whole-economy model incorporates this nonlinearity, though it does not seem to be in the model used in the speech to highlight the different behaviour of inflation that it implies. And the linkage of this nonlinear relationship to the size of the shock is an implication of so-called “menu cost” models that has been known to other central banks for at least 20 years, both in theory and in other countries’ data, though this link wasn’t recognised when the original RBA nonlinearity paper was published.

Quantifying this effect accurately arguably had to wait until the dataset used in the recent research paper became available. The 1990s-era empirical result means it is nonetheless unlikely that the RBA’s existing forecasting framework would have entirely missed faster pass-through of larger supply shocks, even if the theory behind it was not fully recognised at the time. But the recent communication does speak to the balance of risks that the RBA perceives.

It is possible, though, that the RBA’s current analysis misses some other trends under the surface.

As highlighted by Westpac Economics colleague Ryan Wells’ note yesterday, as best as we can tell, official family forecasters’ views about the outlook for labour supply have diverged. Commonwealth Treasury shares our view that the underlying trend in the participation rate is up. This is a departure from its longstanding assumption that population ageing shrinks the workforce. As we have been highlighting for a while, the opposite is true in Australia and most other advanced economies. By contrast, the RBA’s forecast is for a flat participation rate this year and a decline next year as job opportunities diminish. The labour demand effect is assumed to dominate.

To be fair, Assistant Governor Hunter’s speech did acknowledge that extra labour supply is a possible response to cost-of-living pressures, citing a recent IMF working paper that used Australian data to show this. But they acknowledge it only as a risk, not as their base case. It is also a cyclical factor, not the underlying trend discussed above. Past RBA communication has acknowledged this upward trend, but the latest Statement on Monetary Policy did not mention it. As Ryan commented in his note, the labour demand effect will have to work hard to offset this trend and generate the decline the RBA assumes.

(As an aside, I find it interesting that this paper was released as an IMF Working Paper and not an RBA Research Discussion Paper. Yes, three of the authors are from the IMF, but one is the deputy head of the RBA’s Economic Research department and likely the only one authorised to access the detailed tax and Census linked dataset directly. Likewise, it is interesting that the speech cited the paper in the context of cost-of-living pressures, not the – admittedly small at a macro level – positive labour supply response to monetary policy that the paper focused on.)

It is also possible that the RBA’s forecasting framework has not fully absorbed the implications of the build phase of the AI boom. Capex data released recently shows a huge contribution from data centres and IT investment more broadly – bigger than even our top-of-market expectation. Business investment will be strong, but as Westpac Economics colleague Pat Bustamante points out today, the imported component is very large, especially in the fit-out stage. A fixed view of potential growth in supply capacity will interpret this growth as adding to capacity pressures, even though it is literally building capacity. And like the mining investment boom, the build phase actually drags on measured productivity, as workers labour to build capital stock that is not yet producing anything.

Will a weak outcome for measured labour productivity in Q1 nudge the RBA to become even gloomier about ongoing productivity trends, even though it is likely a temporary lag?

Let’s hope the team at the RBA remember to look below the surface.

Memorandum Is Finalized but Its Agreement Is Still Pending – Dow Jones, Nasdaq and S&P 500 Intraday Levels

- Markets are rallying due to the finalization of the Peace Memorandum, but final agreement by Trump and Khamenei are still awaited

- While Nasdaq continues to price heaven and shoot for it, the DJIA is surprisingly unchanged

- Exploring Technical Levels for the Dow Jones, Nasdaq and S&P 500

Stock Markets are rallying after major diplomatic progress, as negotiators have finalized the draft of the much-anticipated US-Iran Peace Memorandum. Still, the deal is not yet official.

Axios reports that while the main framework is set, final approval is needed from both President Trump, who has asked for a few more days to review the terms, and Supreme Leader Khamenei, before the agreement is signed.

The draft shows a more balanced agreement, still tilting towards the US. The main points include keeping the Strait of Hormuz open and gradually lifting the US naval blockade over the next 30 days.

The draft also calls for Iran to get rid of its highly enriched nuclear material and allows for free commercial transit in the region.

In return, Iran will have key financial assets unfrozen, some economic sanctions lifted, and new systems set up for more humanitarian aid.

Even with this major diplomatic breakthrough, energy markets are reacting quietly today. WTI Crude Oil is almost unchanged and remains below $90 as traders wait for clear signs that the strait will reopen. Brent crude fell sharply and is now trading close to WTI, as the international risk premium has disappeared.

Daily Market Performance (14:28). May 28, 2026 – Courtesy of Finviz

The tech-focused Nasdaq is rising quickly, led by gains in semiconductor and large tech companies, running for yet another all-time high, but the rise isn’t uniform, with the Dow Jones Industrial Average mostly flat.

Outside of the tech sector, most of the market is quiet, as big investors wait for the final diplomatic approvals by the respective US and Iran leaders.

Now, let’s take a look at the intraday charts and trading levels for the Dow Jones Industrial Average, Nasdaq Composite, and S&P 500.

Current Session's Stock Heatmap

Current picture for the Stock Market (14:32) – Source: TradingView – May 28, 2026

Dow Jones 4H Chart and Trading Levels

Dow Jones (CFD) 4H Chart – May 28, 2026 – Source: TradingView

Bulls are actually struggling to push the DJIA above the 50,750 major momentum pivot, despite a strong morning candle.

This indicates a potential for a wider pullback, particularly if sellers push the action below the 4H 50-period MA (50,291).

Dow Jones technical levels for trading:

Resistance Levels

- Intraday Pivot 50,750 to 50,900 (morning highs)

- Memorial Day resistance 51,100 to 51,200

Support Levels

- February ATH Pivot 50,400 to 50,500 (Short-term Bearish below)

- Pivotal Support – 49,000 to 49,100 (mid-term bearish below)

- Momentum Support 48,500

- Pivotal Support at 48,000

- Mini Support 47,400 to 47,600

Nasdaq 4H Chart and Trading Levels

Nasdaq (CFD) 4H Chart – May 28, 2026 – Source: TradingView

Nasdaq is attempting a run to new record highs but the action is stalling as we speak right around the previous 30,300 ATH.

Forming a bearish divergence, bulls will actually want to see a clean break in order to push for more price discovery – A rejection however would lead to at least a 29,535 retest (4H 50-Period MA)

Nasdaq technical levels of interest:

Resistance Levels

- 30,300 Daily Top and ATH

- Current ATH 30,327 on the CFD

Support Levels

- 29,535 retest (4H 50-Period MA)

- 29,500 - 29,650 Pivot

- 29,100 - 29,250 momentum support (short-term bearish below)

- 28,000 minor support

- Prior ATH Support 26,200 to 26,300

S&P 500 4H Chart and Trading Levels

S&P 500 (CFD) 4H Chart – May 28, 2026 – Source: TradingView

The S&P 500 is actually the only index reaching new record highs in today's session, but also forming a bearish divergence at the same time.

This indicates that despite the new record, momentum is not as strong as indicated – This could precede a larger pullback to 7,500.

If the bullish action continues however, 7,600 is the next step.

S&P 500 technical levels of interest:

Resistance Levels

- 7,550 - 5,770 Memorial Day ATH Resistance (double top!)

- current ATH 7,575

Support Levels

- 7,525 Past week's ATH Resistance now pivot

- 7,450 - 7,460 Minor Support (Short-term bearish below – 4H 50-period MA (7,448)

- 7,400 Key support

- Pivotal Support 7,250 to 7,260

- Prior ATH Pivot 7,000 to 7,020

Keep track of WTI Crude and the latest headlines throughout the week to stay ahead of the game.

These are my final pieces on MarketPulse, so thank you for all who enjoyed the posts since a bit more than a year – I wish you success in the World of Trading and a long life in Markets.