Sample Category Title

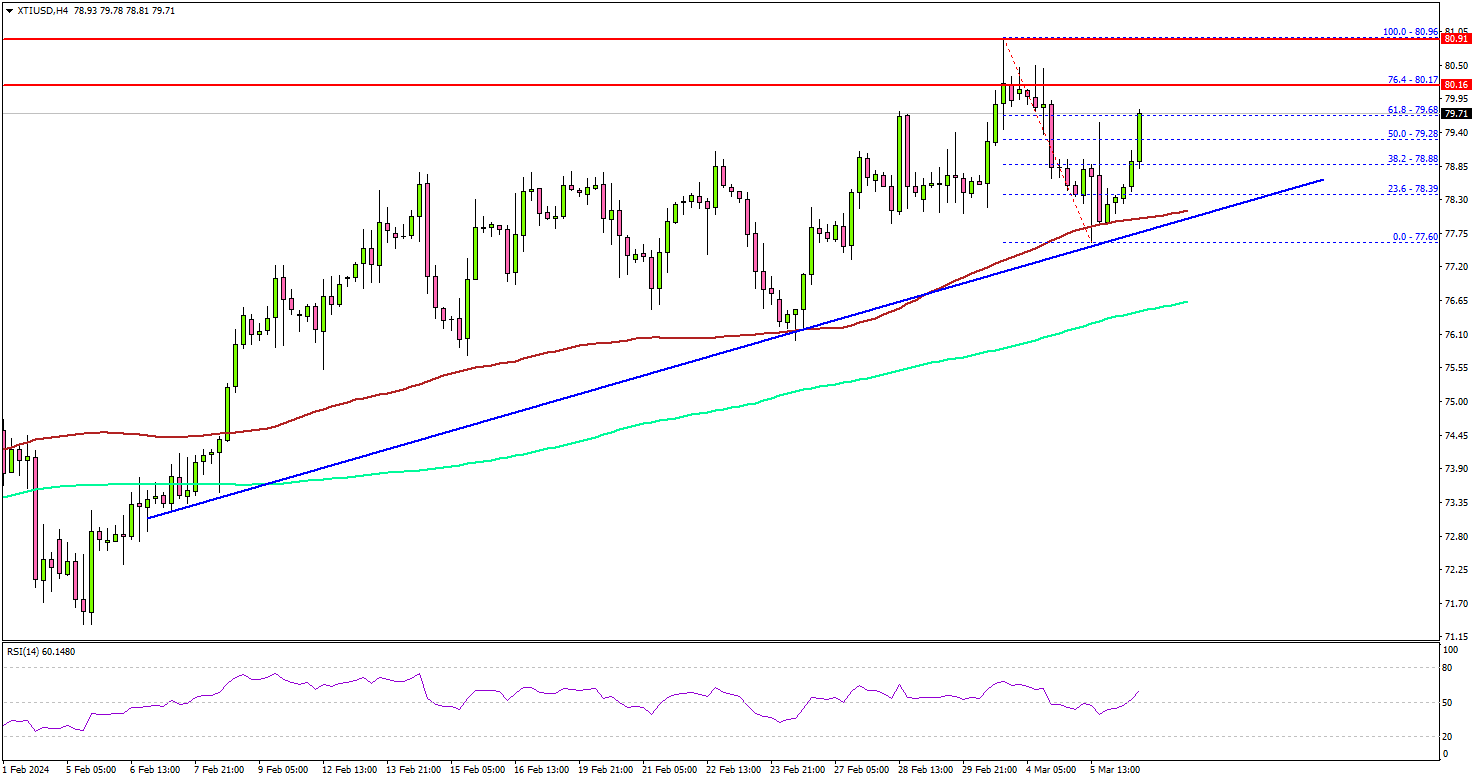

Crude Oil Price Aims Higher As Dollar Takes Hit

Key Highlights

- Crude oil bulls are eyeing an upside break above the $81.00 resistance.

- A major bullish trend line is forming with support at $78.40 on the 4-hour chart.

- Gold prices extended gains above the $2,032 resistance.

- Bitcoin trimmed most losses and could extend its increase above $70,000.

Crude Oil Price Technical Analysis

After struggling above $80.00, Crude oil prices saw a downside correction. However, the bulls were active near the $77.50 zone and protected more downsides.

Looking at the 4-hour chart of XTI/USD, the price remained stable above the $78.00 level, the 200 simple moving average (green, 4-hour), and the 100 simple moving average (red, 4-hour).

It started a fresh increase above the $78.80 resistance. There was a move above the 50% Fib retracement level of the downward move from the $80.96 swing high to the $77.60 low. The current price action suggests a high chance of more upsides above $80.00.

On the upside, the price is facing hurdles near the $80.20 level. The next major resistance is near the $81.00 zone, above which the price may perhaps accelerate higher. In the stated case, it could even visit the $84.00 resistance.

If not, the price might decline and test the $78.80 support. The first major support on the downside is near the $78.40 level or the 100 simple moving average (red, 4-hour).

There is also a major bullish trend line forming with support at $78.40 on the same chart. The next major support is at $77.60, below which the price might test $76.60. Any more losses might send oil prices toward $75.00.

Looking at Bitcoin, there was a strong bearish reaction from the $69,200 zone but the bulls were active and pushed the price back above $65,000. The main hurdle now sits at $68,000.

Economic Releases to Watch Today

- US Initial Jobless Claims - Forecast 243K, versus 244K previous.

- Fed's Chair Powell testimony.

BoJ’s Nakagawa: Promising cycle of wages and inflation on the horizon

BoJ board member Junko Nakagawa highlighted a promising outlook for wage growth, expressed confidence in the emergence of a positive cycle between inflation and wages, a prerequisite for the central bank to exit negative interest rate.

"We can say that prospects for the economy to achieve a positive cycle of inflation and wages are in sight," she stated, pointing to a shift in the wage-setting behavior of companies as a sign of economic optimism.

According to Nakagawa, there are "clear signs of change in how companies set wages," with businesses increasingly inclined to offer annual pay raises in response to the ongoing labor shortages. This adjustment marks a significant departure from previous practices and suggests that companies are prepared to propose wage increases surpassing those of the previous year.

"Japan is moving steadily towards sustainably and stably achieving our 2% inflation target," she remarked.

Japan’s nominal wage growth hits seven-month high, real wages still in decline

Japan's nominal wage growth surged by 2.0% yoy in January, surpassing expectations of 1.3%, and marking the most substantial growth since last June. This also represents a notable acceleration from the revised 0.8% increase observed in December.

The surge in wages largely stems from a significant 16.2% yoy advance in special payments, which include winter bonuses. Regular or base salaries maintained steady growth rate of 1.4% yoy, consistent with the previous month's performance. Meanwhile, overtime pay, a key indicator of labor demand and economic activity, showed slight improvement of 0.4% yoy, recovering from revised decline of -1.2% yoy in the prior period.

Real wages declined by 0.6% yoy, marking a continued decrease in purchasing power for Japanese workers. However, the pace of decline was the joint-slowest since December 2022, indicating stabilization in the erosion of real earnings.

Fed’s Kashkari sees two, or maybe just one rate cut this year

Minneapolis Fed President Neel Kashkari has refined his expectations for interest rate cuts in 2024, now leaning towards possibility of fewer reductions due to robust economic data emerging since the year's start.

Initially forecasting two rate cuts for the year, Kashkari expressed in a WSJ Live interview that current economic indicators might necessitate only a single cut. "I was at two in December," he remarked. "It's hard to see, with the data that's come in, that I'd be saying more cuts than I had in December, or potentially one fewer, but I haven't decided."

Kashkari emphasized that Fed's "base case scenario" no longer includes further rate hikes. He suggested that should inflation persist beyond current projections, Fed's immediate response would be to maintain the existing interest rates for "an extended period of time." rather than implementing additional increases.

Fed’s Beige Book reveals modest economic growth and easing labor market tightness

Fed's Beige Book report noted "slight to modest" increase in economic activity across various districts. Specifically, eight districts reported slight to modest growth, three observed no change, and one experienced slight softening in economic conditions.

In the realm of consumer spending, the report indicates slight downturn, especially concerning retail goods. This trend is attributed to a "heightened price sensitivity" among consumers, who are increasingly opting to trade down and shift their spending away from discretionary goods. Manufacturing activity remained "largely unchanged", with disruptions in shipping through the Red Sea and Panama Canal reportedly having minimal overall impact.

The report also highlights persistent price pressures, although some districts observed moderation in inflation. Businesses are finding it increasingly difficult to pass higher costs onto customers, who are becoming more resistant to price increases. Labor market conditions have shown further signs of improvement, with nearly all districts reporting increased labor availability and enhanced employee retention.

BoC Holds Rates Steady in March With Dovish Lean

The Bank of Canada held the overnight rate unchanged for a fifth consecutive meeting, extending a pause that started after the last hike in July last year.

Softer inflation data in January made sure that no hiking bias (dropped in January) would reappear. BoC’s key messaging remains that we’re on the right path to target inflation, but just not there yet.

The BoC highlighted weak final domestic demand in Q4 last year and easing wage pressures as evidence that high interest rates are working to restrict economic activities, but not enough to stamp upside inflationary risks yet.

Progress in lowering the BoC’s preferred core inflation measures, including CPI trim and CPI median has been slow and choppy - both measures dropped in latest data for January but were also above 3% that is the top end of the inflation target range in Canada.

Later in the press conference (that was the first for a non-MPR meeting), Governor Macklem once again confirmed that the focus of discussions at the BoC have shifted to how long rates will stay high, but also said explicitly that "It’s still too early to consider lowering the policy interest rate."

Still, persistently softer macro backdrop and the assessment that the economy is in “modest excess supply” should mean that inflation pressures are much more likely to recede than to reaccelerate – the BoC expected inflation to stay around 3% before gradually easing below that during the second half of this year.

As expected, there was no announcement on the ending of the QT program. Guidance is likely to come in Gravelle’s speech on March 21 about balance sheet normalization.

We’ll look forward to releases of the bank’s quarterly surveys on Canadian businesses and consumers, scheduled ahead of the meeting in April for more forward-looking information on inflation and wage expectations as well as corporate price setting behaviour.

Bottom line: The BoC’s decision to hold the overnight rate steady again in March confirmed that interest rates are already at levels that are high enough to restrict economic activity and further slow price pressure. We expect the BoC to start gradually lowering the policy rate by mid-year, after allowing for clearer signs of easing in core inflation readings to come through.

Bank of Canada Maintains Interest Rate, No New Guidance on Cuts

The Bank of Canada maintained the overnight rate at 5.0%, while stating that it will continue with Quantitative Tightening (QT).

The Bank highlighted the slowing in economic momentum, stating that growth "remained weak and below potential", while emphasizing that "final domestic demand contracted with a large decline in business investment". It also stated that "employment continues to grow more slowly than the population, and there are now some signs that wage pressures may be easing".

On the inflation outlook, the BoC mentioned that inflationary pressures have eased. But in spite of shelter being the driver of overall inflation, it has focused on the fact that "the share of CPI components growing above 3% declined but is still above the historical average". It expects that inflation will "remain close to 3% during the first half of this year".

On the future path of policy, the Bank is still concerned about the "persistence in underlying inflation (and the) Governing Council wants to see further and sustained easing in core inflation."

A press conference is forthcoming at 10:30.

Key Implications

The song remains the same. The BoC came out today to reinforce its view that more time is needed to make sure that inflation is headed to the 2% target. We get it. With core rates of inflation tracking around the mid-3% level, the Bank can justify waiting longer. Luckily the central bank has been gifted a little more time to wait. Economic growth eked out small, but positive, growth to end 2023. With effectively no pressure for the BoC to respond, it can sit back and wait for a couple more inflation reports to roll in.

Markets don't think the BoC can get too comfortable. A June cut is nearly 90% priced, and we agree with that timing. In spite of the economy having avoided recession, consumers are feeling the pain of higher rates. Spending per capita has contracted over the better part of the last 18 months. And it is not as if rate hikes aren't impacting inflation. Sure, the BoC's core measures are still elevated, but they are being driven by shelter prices. Indeed, inflation excluding shelter is running below the BoC's 2% target, at only 1.6% year-on-year. While the BoC isn't ready to adjust course just yet, we think that the time for rate cuts is quickly approaching.

Sunset Market Commentary

Markets

Yesterday’s risk correction on Wall Street didn’t spill to European dealings with key indices adding up to 0.5%. January EMU retail sales barely grew (0.1% M/M vs 0.2% consensus), but obviously didn’t impact trading ahead of tomorrow’s ECB gathering. Employment indices in US manufacturing ISM last Friday (45.9 from 47.1) and non-manufacturing ISM yesterday (48 from 50.5) suggested the worst for today’s ADP employment report and Friday’s payrolls. Downside risks in any case didn’t materialize today with net job growth clocking at 140k (vs 150k consensus) from a marginally upwardly revised 111k in January. Details showed mainly medium (+69k) and large companies (+61k) responsible for job gains. Sector and regional-wise, job creation was broad-based, led by leisure and hospitality, construction and trade & transportation. Wage growth accelerated for the first time in over a year for job changers (7.6% Y/Y from 7.2% Y/Y) while slowing further for job stayers (5.1% Y/Y from 5.3% Y/Y). Remarks of Fed Chair Powell’s semi-annual testimony before US Congress sounded very familiar. Rate cuts are coming “at some point this year” but “the committee does not expect that it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2%”. Most Fed members recently closed ranks around December forecasts, suggesting a cumulative 75 bps of rate cuts is still the valid scenario with a first move coming as soon as June. Ahead of rate cuts, the Fed is likely to sort out how the quantitative tightening process will continue in coming months. They want to avoid draining too much liquidity from the system like they did back in 2018. Markets didn’t respond to the outcome. US Treasuries outperform German Bunds in a daily basis, pushing EUR/USD for a test of the upper bound of the broad 1.07-1.09 range in place since mid-January. Higher oil prices can’t help the greenback while the euro doesn’t suffer from French comments that last year’s budget deficit would even be bigger than the upwardly revised 4.9% of GDP.

UK Chancellor Hunt announced that the main national insurance payroll tax will be cut from 10% to 8% as he delivered the annual budget. The ONR also upgraded growth forecast for this year and next from 0.7% to 0.8% and from 1.4% to 1.9% respectively. The UK debt management office separately announced that it will issue £265.3bn of gilts this fiscal year (up from £237bn) with long term bonds making up less of the issuance compared to last year (18.5% vs 21.1%). UK Gilts slightly outperform today, with yields dropping up to 4 bps.

News & Views

The Egyptian pound slumped against the US dollar today. USD/EGP shot up from 30.85 to 50. After the central bank at an unscheduled meeting today jacked up interest rates by a whopping 600 bps to 27.25%, investors felt something else was coming too. Indeed, authorities later announced the long-awaited 35%+ devaluation of EGP. Doing so brought the pound to levels for which it is changing hands on the black market. Egypt is suffering from a severe currency crisis and rampant inflation (30%). It has struck a $3bn deal with the IMF but little of that has been disbursed yet as the Washington-based lender wanted Egypt to take additional crisis measures first. These include tighter monetary policy and a more flexible official exchange rate. Today’s announcement paves the way not only for the IMF loan to be disbursed but also to be increased to more than $10bn. Last month, Cairo also struck a mega $35bn deal with the UAE to develop parts of Egypt’s coast and elsewhere and authorities claimed it as the biggest foreign investment ever. In a sign of investors gaining some confidence back, Egyptian dollar bonds since the UAE deal rallied sharply, pushing double digit yields several percentage points lower.

The European Union is closing in on imposing additional tariffs on imported Chinese electric vehicles. Launching an inquiry into illegal financial support for the industry in October last year, the bloc this week said it has now found “sufficient evidence” of Chinese direct transfers of funds to producers, tax breaks or public provision of goods and services below market prices. It noted a “substantial increase” of Chinese imports in a relatively short period of time, adding that the damage for local EV producers may have started to materialize even before the end of the investigation (which may last no longer than 13 months). For this reason, the EU is taking the appropriate steps to make it possible to collect import duties retroactively should it decide to impose them. Provisional tariffs could be introduced in July with definitive ones in place by November.

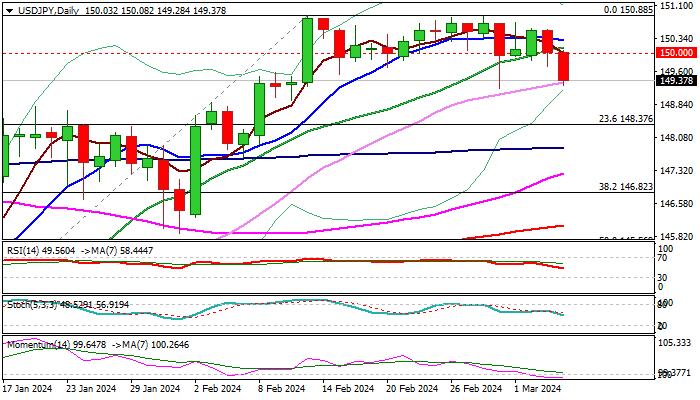

USD/JPY: Falls Below 150.00 on Growing Expectations for BoJ Rate Hike in March

USDJPY dips below 150 support and is on track for clear break lower after the pair was hanging above this level for more than two weeks.

Yen gained traction on signals may decide to start raising interest rates, with the most optimistic BOJ policymakers seeing chances for the first hike this month.

On the other hand, the US dollar came under pressure from weaker than expected US Fed ADP private sector payrolls, while prospects for the first Fed rate cut in June remain in play, despite remarks from Fed Chair Powell, who pointed to uncertain economic outlook and still not assured progress towards inflation 2% target.

The US central bank remains very cautious as too early rate cuts that would allow inflation to re-accelerate, but keeping too high interest rates for too long period would hurt economic growth, pointing to balanced approach to the monetary policy in coming months.

Daily close below 150 level (also 20DMA) will generate initial bearish signal, which will look for reinforcement on extension below 149.20 (Feb 29 spike low) and expose first Fibo support at 148.37 (23.6% of 140.25/150.88, reinforced by daily Kijun-sen).

Near-term bias is expected to remain with bears while the price stays below 150 level, while break here and falling 10DMA (150.29) would sideline bears.

Res: 150.00; 150.29; 150.88; 151.43.

Sup: 149.20; 148.80; 148.37; 147.83.