Sample Category Title

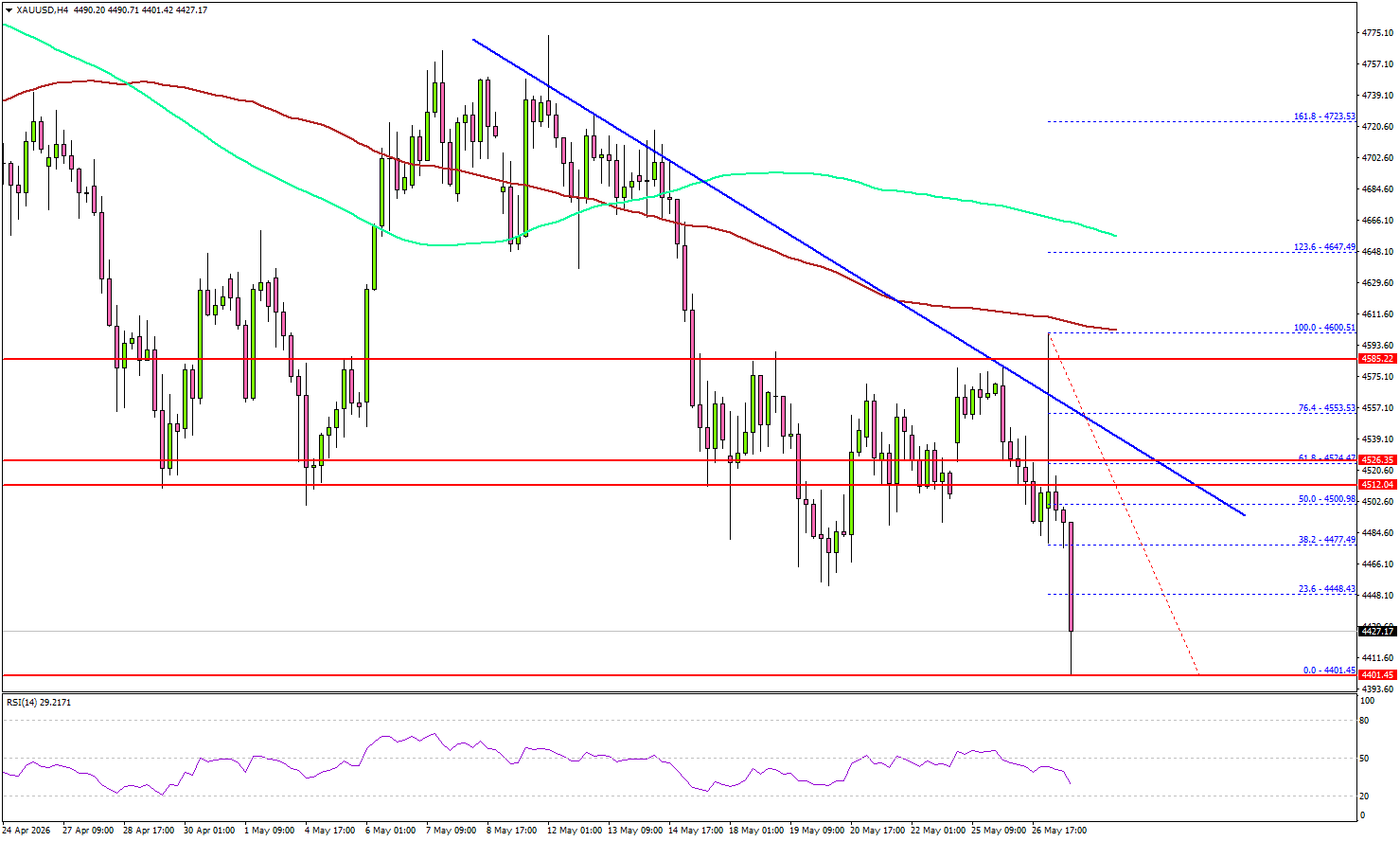

Gold Weakens Further, Downside Momentum Starts Accelerating

Key Highlights

- Gold started a fresh decline below the $4,550 support.

- A major bearish trend line is forming with resistance at $4,525 on the 4-hour chart.

- WTI Crude Oil extended losses and traded below $95.

- EUR/USD started a minor recovery wave above 1.1620.

Gold Price Technical Analysis

Gold failed to surpass $4,650 and trimmed gains against the US Dollar. The price dipped below $4,600 and $4,550 to enter a bearish zone.

The 4-hour chart of XAU/USD indicates that the price even declined below $4,500, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours). A low was formed at $4,401, and the price is now consolidating losses.

On the upside, immediate resistance is $4,475. The next major resistance sits near $4,500 and the 50% Fib retracement level of the downward move from the $4,600 swing high to the $4,401 low.

The main resistance could be near $4,525 and the 61.8% Fib retracement level. There is also a major bearish trend line forming with resistance at $4,525. A clear move above $4,525 could open the doors for more upside. In the stated case, the bulls could aim for a move toward $4,600 or even $4,620.

If there is another decline, Gold might find bids near the $4,400 level. The first major support sits at $4,365. The next support could be $4,320, below which the price might slide to $4,300. The main support sits at $4,200. Any more losses might call for a test of $4,065 or even $4,000 in the coming days.

Looking at WTI Crude Oil, the price started a fresh decline and there are chances of more losses below the $90 zone.

Economic Releases to Watch Today

- US Initial Jobless Claims - Forecast 243K, versus 244K previous.

- US Gross Domestic Product Q1 2026 (Preliminary) – Forecast 1.3% versus previous 2.1%.

Fed’s Jefferson Says Policy Well Positioned Despite Rising Inflation Risks

Federal Reserve Vice Chair Philip Jefferson said the current stance of US monetary policy remains appropriate despite ongoing upside risks to inflation tied to the Middle East conflict and energy disruptions. Speaking at the Bank of Japan-IMES Conference in Tokyo, Jefferson said the current federal funds rate range leaves the Fed “well positioned to respond to economic developments based on the incoming data, the evolving outlook, and the balance of risks.”

Jefferson acknowledged that inflation pressures are expected to ease later this year, but warned that risks to the outlook remain skewed higher. He noted that while the United States is a major energy producer, it is “not fully insulated from the energy disruptions the war has created.”

At the same time, Jefferson avoided signaling any predetermined move for the June FOMC meeting, stressing that he had “not prejudged the next meeting.”

He described the US economy as still delivering a “solid performance,” while characterizing the labor market as stable with low hiring and firing. However, Jefferson added that job-market risks are “tilted to the downside,” underscoring the delicate balancing act facing the Fed as policymakers weigh persistent inflation pressures against softer growth risks.

Fed’s Cook Says Inflation Risks Rising, Prepared to Hike if Needed

Federal Reserve Governor Lisa Cook warned that inflation risks are increasingly tilted to the upside, even though she currently favors keeping interest rates unchanged. Speaking at a policy forum at Stanford University, Cook said the Fed should continue holding rates steady “from a risk-management perspective,” but stressed that policymakers must remain prepared to tighten further if inflation fails to ease in a timely manner.

Cook acknowledged that inflation is “clearly moving in the wrong direction,” citing tariffs, the Iran conflict, rising oil prices, and surging AI-related investment as major drivers of renewed price pressures. She pointed specifically to rising energy and fertilizer costs, as well as stronger demand for chips, software, and construction workers linked to the rapid expansion of AI data centers.

Importantly, Cook warned that after more than five years of inflation running above the Fed’s 2% target, the danger of inflation expectations becoming embedded is increasing. “The risks remain tilted toward higher inflation,” she said, adding: “I am prepared to raise rates, if the expected disinflation does not appear in a timely manner.” While she still expects inflation to moderate without additional tightening, her remarks reinforce a broader shift among Fed officials toward greater caution about persistent second-round inflation pressures.

Fed’s Kashkari Says Inflation Still “Much Too High” as Energy Shock Spreads

Federal Reserve Bank of Minneapolis President Neel Kashkari warned that inflation remains the Fed’s primary concern despite growing uncertainty surrounding the global economy and Middle East conflict. Speaking at the Bank of Japan-IMES Conference in Tokyo, Kashkari said inflation in the United States is still “much too high,” while the labor market remains in “decent shape.”

Kashkari emphasized that the Fed must continue taking a “balanced approach” toward its dual mandate, but acknowledged that inflation persistence is becoming increasingly worrying after more than five years of elevated price pressures. “The longer inflation remains elevated, the greater the risk that inflation expectations become unanchored and move higher,” he warned. Kashkari added that if inflation expectations were to drift higher, policymakers “would have to respond even more aggressively”.

The Minneapolis Fed President also pointed directly to the Iran conflict as an important inflation driver, alongside the pandemic, tariffs, and the war in Ukraine. He said rising energy and fertilizer prices are now feeding broader inflation pressures across the global economy. “One of the things I’m going to be looking for is, when do we see energy prices affecting the broader economy,” Kashkari said, highlighting growing concern inside the Fed about second-round inflation effects spreading beyond oil markets alone.

ECB’s Lane Warns Iran Energy Shock Could Keep Inflation Elevated Even After Peace Deal

European Central Bank Chief Economist Philip Lane warned that the inflation impact from the Middle East conflict is likely to persist even if a quick diplomatic resolution is reached. Speaking at a conference hosted by the Bank of Japan and its think tank in Tokyo, Lane said policymakers are concerned that energy-driven price pressures may continue feeding through the broader economy long after the initial oil shock fades.

“Even if the initial energy shock starts to reverse, the second round effect will be with us for a while,” Lane said. He argued that the conflict could leave lasting structural effects on supply chains and global energy strategy, warning that “even if Iran war sees resolution, prolonged conflict could prompt shifts in optimal diversification strategy.”

Lane’s remarks add to increasingly hawkish messaging from senior European Central Bank officials this week as markets prepare for a likely June rate hike. Policymakers are becoming more focused on preventing higher energy costs from feeding into wages, pricing behavior, and broader inflation expectations across the Eurozone economy. The comments also suggest that even a reopening of the Strait of Hormuz may not quickly reverse the inflation pressures already embedded into Europe’s economic outlook.

Traders Are Desperate for More News, but the Status Quo Is Positive

Global financial markets are on edge as traders wait for clear details about the new US-Iran peace plan.

After two months of intense tension and repeated ceasefire extensions, a concrete framework is finally being discussed.

Both sides know what is at stake: the US wants the Strait of Hormuz reopened without conditions and Iran’s nuclear program dismantled, while Iran wants a full regional ceasefire and a withdrawal of US troops.

The big question for markets now is whether negotiators can bring some still-contradicting demands together in the next 60 days.

Even with uncertainty still in the air, the current situation is giving strong support to risk assets.

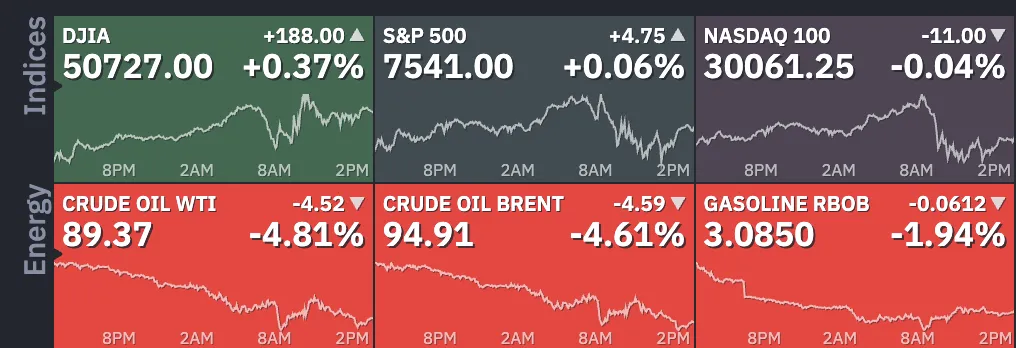

The fact that tensions are not turning into a wider war is a major positive change. This relief has pushed the tech-focused Nasdaq to new record highs above 30,000 this morning, up 4% since last week.

The Dow Jones Industrial Average also broke records on Monday’s holiday and is trying to move higher, though today’s trading has been slower and steadier.

This particularly reflects the large change seen in crude oil prices, down just shy of 10% since the weekly open.

Daily FX Performance (15:56), May 27, 2026 – Courtesy of Finviz.

Still, there is some caution in the market because the White House has not shown much excitement about the final details of the deal.

President Trump made it clear that Iran will not get immediate sanctions relief for giving up its highly enriched uranium.

This firm position shows that, even though there is a Memorandum of Understanding, reaching a full treaty remains very complicated and faces many diplomatic challenges.

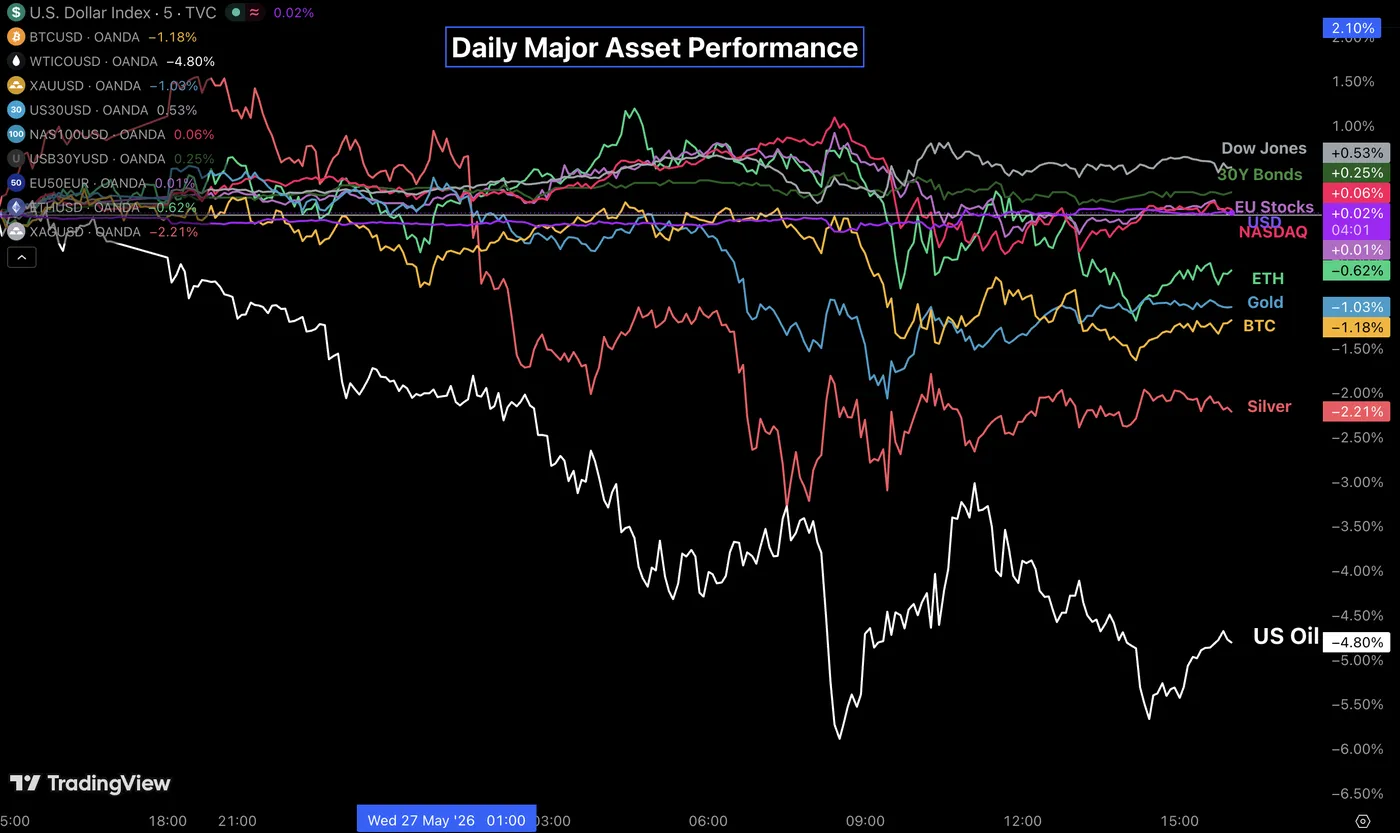

Cross-Asset Daily Performance, May 27, 2026 – Source: TradingView.

Even if the risk of re-escalation has eased, many details are still unclear and traders are turning their attention back to economic data while awaiting further headlines.

With few major events early this week, big investors are waiting for tomorrow’s important Core PCE report.

This key inflation number will show if the recent oil-driven supply shocks have hurt the US economy more than expected, which could make things harder for the Federal Reserve’s next moves (the next FOMC meeting is on June 17).

These are my final pieces on MarketPulse, so thank you to everyone who enjoyed the posts over the past year. I wish you success in the world of trading and a long life in markets.

With time, resistance and resilience, things will fall in order.

Don't forget to follow me on X, send me messages for any questions, and you can check out my website if you want to stay in contact.

Safe trades and keep your eyes on the news!

Buyers Likely to Support Nikkei Futures (NKD) Pullback, Eyeing 72,870 Extension

Nikkei Futures (NKD) continues to demonstrate remarkable strength as it extends into new all‑time highs, reinforcing the bullish sequence that began from the March 23, 2026 low. This upward momentum favors additional gains in the near term. From the March 23 low, wave 1 concluded at 63,880, followed by a corrective pullback in wave 2 that ended at 59,352. The internal subdivision of wave 2 unfolded as a zigzag, a common corrective structure, before the Index resumed higher. The decisive break above the wave 1 peak confirmed that wave 3 had begun, signaling continuation of the impulsive advance.

From wave 2, the initial leg wave (i) ended at 62,075, while the subsequent pullback in wave (ii) found support at 61,040. The rally extended further, with wave (iii) reaching 65,695, before a modest dip in wave (iv) concluded at 64,650. The final leg, wave (v), advanced to 66,520, completing wave ((i)) of a higher degree. At present, a corrective phase in wave ((ii)) is unfolding, designed to retrace the cycle from the May 20, 2026 low. This correction is expected to provide a healthy consolidation before the broader rally resumes.

In the near term, as long as the pivotal support at 59,352 remains intact, the pullback should ultimately find support within the typical 3, 7, or 11 swing sequence. Consequently, the broader outlook continues to favor further upside once the current consolidation completes, maintaining the bullish trajectory established since March.

Nikkei Futures (NKD) 60-Minute Elliott Wave Chart

NKD_F Elliott Wave Video:

https://www.youtube.com/watch?v=mffic6woNVU

Eco Data 5/28/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Private Capital Expenditure Q1 | 6.50% | 1.00% | 0.40% | 0.70% |

| 09:00 | EUR | Eurozone Economic Sentiment May | 93.5 | 92 | 93 | 93.2 |

| 09:00 | EUR | Eurozone Services Sentiment May | 2.2 | 0.1 | 0.9 | |

| 09:00 | EUR | Eurozone Industrial Confidence May | -8 | -7.8 | -7.7 | |

| 09:00 | EUR | Eurozone Consumer Confidence May F | -19 | -19 | -19 | |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | CAD | Current Account (CAD) Q1 | -1.9B | -0.7B | ||

| 12:30 | USD | Initial Jobless Claims (May 22) | 215K | 210K | 209K | 210K |

| 12:30 | USD | Personal Income M/M Apr | 0.00% | 0.40% | 0.60% | 0.50% |

| 12:30 | USD | Personal Spending M/M Apr | 0.50% | 0.50% | 0.90% | 1.00% |

| 12:30 | USD | PCE Price Index M/M Apr | 0.40% | 0.50% | 0.70% | |

| 12:30 | USD | PCE Price Index Y/Y Apr | 3.80% | 3.80% | 3.50% | |

| 12:30 | USD | Core PCE Price Index M/M Apr | 0.20% | 0.30% | 0.30% | |

| 12:30 | USD | Core PCE Price Index Y/Y Apr | 3.30% | 3.30% | 3.20% | |

| 12:30 | USD | Durable Goods Orders Apr | 7.90% | 3.30% | 0.80% | 1.30% |

| 12:30 | USD | Durable Goods Orders ex Transport Apr | 1.10% | 0.50% | 0.90% | 1.10% |

| 12:30 | USD | GDP Annualized Q1 P | 1.60% | 2% | 2% | |

| 14:00 | USD | New Home Sales Apr | 622K | 661K | 682K | 663K |

| 14:30 | USD | Natural Gas Storage (May 22) | 92B | 96B | 101B | |

| 16:00 | USD | Crude Oil Inventories (May 22) | -3.8M | -7.9M |

| 01:30 | AUD |

| Private Capital Expenditure Q1 | |

| Actual | 6.50% |

| Consensus | 1.00% |

| Previous | 0.40% |

| Revised | 0.70% |

| 09:00 | EUR |

| Eurozone Economic Sentiment May | |

| Actual | 93.5 |

| Consensus | 92 |

| Previous | 93 |

| Revised | 93.2 |

| 09:00 | EUR |

| Eurozone Services Sentiment May | |

| Actual | 2.2 |

| Consensus | 0.1 |

| Previous | 0.9 |

| 09:00 | EUR |

| Eurozone Industrial Confidence May | |

| Actual | -8 |

| Consensus | -7.8 |

| Previous | -7.7 |

| 09:00 | EUR |

| Eurozone Consumer Confidence May F | |

| Actual | -19 |

| Consensus | -19 |

| Previous | -19 |

| 11:30 | EUR |

| ECB Monetary Policy Meeting Accounts | |

| Actual | |

| Consensus | |

| Previous | |

| 12:30 | CAD |

| Current Account (CAD) Q1 | |

| Actual | |

| Consensus | -1.9B |

| Previous | -0.7B |

| 12:30 | USD |

| Initial Jobless Claims (May 22) | |

| Actual | 215K |

| Consensus | 210K |

| Previous | 209K |

| Revised | 210K |

| 12:30 | USD |

| Personal Income M/M Apr | |

| Actual | 0.00% |

| Consensus | 0.40% |

| Previous | 0.60% |

| Revised | 0.50% |

| 12:30 | USD |

| Personal Spending M/M Apr | |

| Actual | 0.50% |

| Consensus | 0.50% |

| Previous | 0.90% |

| Revised | 1.00% |

| 12:30 | USD |

| PCE Price Index M/M Apr | |

| Actual | 0.40% |

| Consensus | 0.50% |

| Previous | 0.70% |

| 12:30 | USD |

| PCE Price Index Y/Y Apr | |

| Actual | 3.80% |

| Consensus | 3.80% |

| Previous | 3.50% |

| 12:30 | USD |

| Core PCE Price Index M/M Apr | |

| Actual | 0.20% |

| Consensus | 0.30% |

| Previous | 0.30% |

| 12:30 | USD |

| Core PCE Price Index Y/Y Apr | |

| Actual | 3.30% |

| Consensus | 3.30% |

| Previous | 3.20% |

| 12:30 | USD |

| Durable Goods Orders Apr | |

| Actual | 7.90% |

| Consensus | 3.30% |

| Previous | 0.80% |

| Revised | 1.30% |

| 12:30 | USD |

| Durable Goods Orders ex Transport Apr | |

| Actual | 1.10% |

| Consensus | 0.50% |

| Previous | 0.90% |

| Revised | 1.10% |

| 12:30 | USD |

| GDP Annualized Q1 P | |

| Actual | 1.60% |

| Consensus | 2% |

| Previous | 2% |

| 14:00 | USD |

| New Home Sales Apr | |

| Actual | 622K |

| Consensus | 661K |

| Previous | 682K |

| Revised | 663K |

| 14:30 | USD |

| Natural Gas Storage (May 22) | |

| Actual | 92B |

| Consensus | 96B |

| Previous | 101B |

| 16:00 | USD |

| Crude Oil Inventories (May 22) | |

| Actual | |

| Consensus | -3.8M |

| Previous | -7.9M |

Sunset Market Commentary

Markets

Oil prices erased yesterday’s bounce back towards the $100 barrel. There’s little news to report on the ongoing talks between the US and Iran. Markets take it as a positive sign. Iran’s state TV did say it obtained a draft of the initial unofficial MoU framework which included the withdrawal of US military forces and lifting the naval blockade. Iran in return would commits to allow commercial transit through the Strait of Hormuz to pre-war levels within one month. Future management of the Strait will be handled by Iran in cooperation with Oman, the draft stated. Brent crude fell to currently trade around $96. Core bonds benefit slightly from these lower oil prices. US changes are limited to <2 bps though. German yields ease a similar amount with the front end slightly outperforming (-2.0 bps) but that didn’t weigh on money market bets for an ECB June hike, on the contrary. The market implied probability grew from +/- 92% yesterday to 95% today as ECB heavyweight Schnabel’s comments from yesterday continue to linger. Stock markets march higher again. The EuroStoxx50 recoups part of yesterday’s losses and the likes of the S&P500 hold near record highs. Economic data was limited to the weekly ADP employment estimate but came with zero impact on markets. Coming in at nearly 36k (on a four-week moving average basis), weekly job growth remains among the quickest in the series, be it still short, history.

Currency markets show little movement. The kiwi dollar is the exception to the rule after the central bank barely kept the policy rate at 2.25% during this morning’s decision. The status quo came with strong messaging that hikes were imminent though and “most likely more and sooner”. Markets upped tightening bets with a first move fully priced in for September, to be followed several more through March next year. The 3.25% currently expected puts it in line with the Reserve Bank of New Zealand’s own view. NZD/USD sprints towards the 0.59 barrier. Most other dollar pairs hold a tight range with EUR/USD treading water around 1.165. USD/JPY sticks around 159.4, unfazed by Bank of Japan governor Ueda’s veiled hint for near-term hike(s) this morning. Sterling loses ground to EUR/GPB 0.866 amid Gilt outperformance.

News & Views

New EU car registrations increased by 4.2% YtD in April 2026 (to 3794k). The market continued to benefit from strong consumer demand for a range of electrified technologies, supported by new and revised tax benefits and incentive schemes across major European countries. In absolute terms, new battery-electric car registrations (BEV’s) rose by 33.8% when comparing April YtD 2025 with April YtD 2026 (747k). BEV’s accounted for 19.7% of the EU market, an increase from 15.3% a year earlier. Hybrid-electric (HEV’s) car registrations captured 38.2% of the market (from 35.3%), remaining the preferred choice among consumers in the EU. Moreover, the combined market share of petrol and diesel cars declined to 30.2%, down from 38.1%. In Belgium, new car registrations are 4.5% lower (151.6k) YtD compared to 2025. Petrol cars remain the dominant choice (43.8% from 42.2%), ahead of BEV’s (35.2% from 33.3%) and HEV’s (12.2% from 12%). Compared with the first four months of 2025, only new registrations of BEV’s increased (+1.1%).

UK energy regulator Ofgem today announced a 13% increase of the energy price cap for the third quarter of this year. Customers will see a smaller price increase of around 5% on their electricity bills compared to gas bills which are rising by 24%. The current price cap for a typical household paying by direct debit for gas and electricity is £1,641. In practice, the increase will be much smaller than an increase to £1,862 though as Ofgem updated its Typical Domestic Consumption Review. That’s how much energy a typical household uses. From 1 July, the figures will be updated to reflect the fact that households are using less energy than before - around 7% less electricity and 17% less gas compared to the last review. As a result, the price cap level from 1 July will be £1,663 per year - reflective of these updated values. At the height of the energy crisis, the government stepped in to cap bills at £2500. Currently, 40% (22 mn) of accounts are fixed tariffs and are therefore unaffected by this price rise.

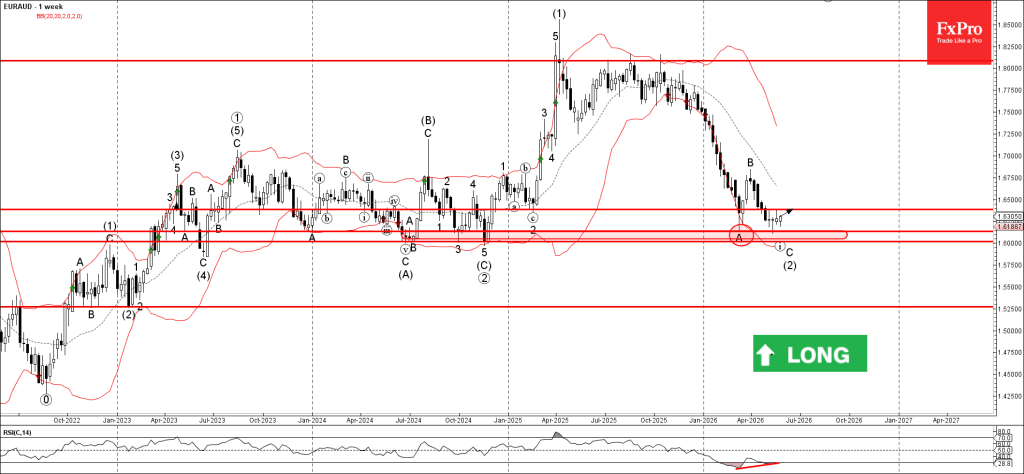

EURAUD Wave Analysis

EURAUD: ⬆️ Buy

- EURAUD reversed from multi-month support level 1.6130

- Likely to rise to resistance level 1.6385

EURAUD currency pair recently reversed up from the strong multi-month support level 1.6130 (upper border of the narrow support zone, which has been reversing the price from the middle of 2024).

The upward reversal from the support level 1.6130 stopped the previous weekly impulse wave C of the weekly downward ABC correction (2) from the start of 2025.

Given the strength of the support level 1.6130 and the bullish divergence on the weekly RSI indicator, EURAUD currency pair can be expected to rise to the next resistance level 1.6385.