Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 140.18; (P) 141.16; (R1) 141.85; More...

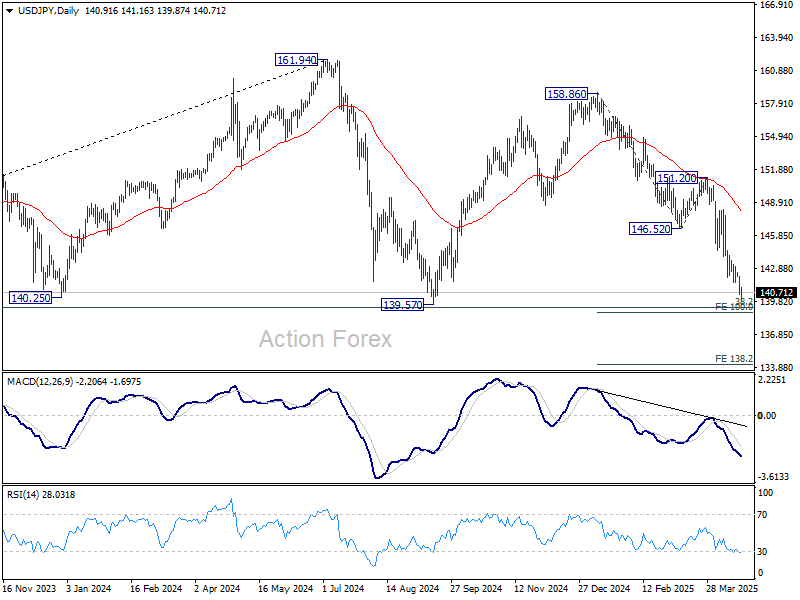

Intraday bias in USD/JPY stays on the downside as fall from 158.86 is in progress for 139.57 support. Strong support could seen from 139.26 fibonacci level to bring rebound. On the upside, above 141.60 minor resistance will turn intraday bias neutral first. However, decisive break of 139.26 will carry larger bearish implications, and target 138.2% projection of 158.86 to 146.52 from 151.20 at 134.14.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8026; (P) 0.8104; (R1) 0.8169; More…

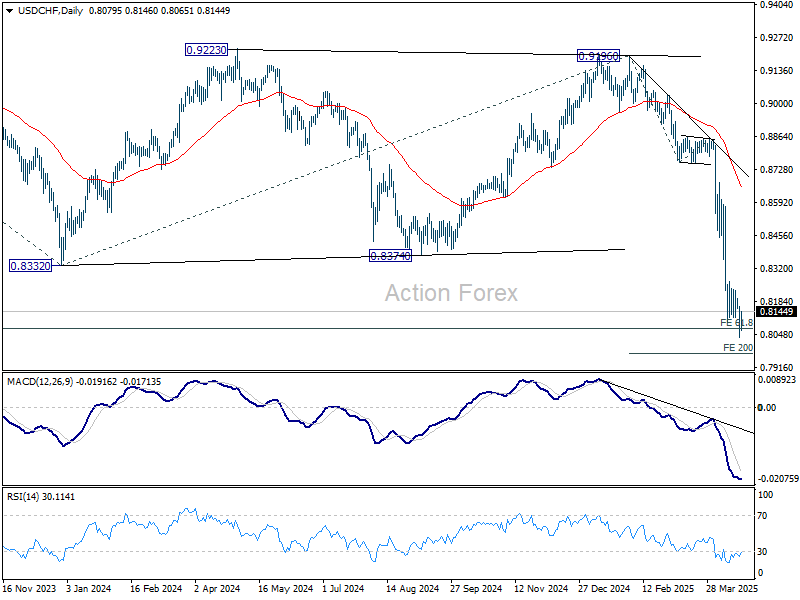

Further decline is expected in USD/CHF with 0.8196 resistance intact. Current down trend should target 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976 next. Nevertheless, considering bullish convergence condition in 4H MACD, break of 0.8196 will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382. In any case, outlook will now stay bearish as long as 55 W EMA (now at 0.8794) holds.

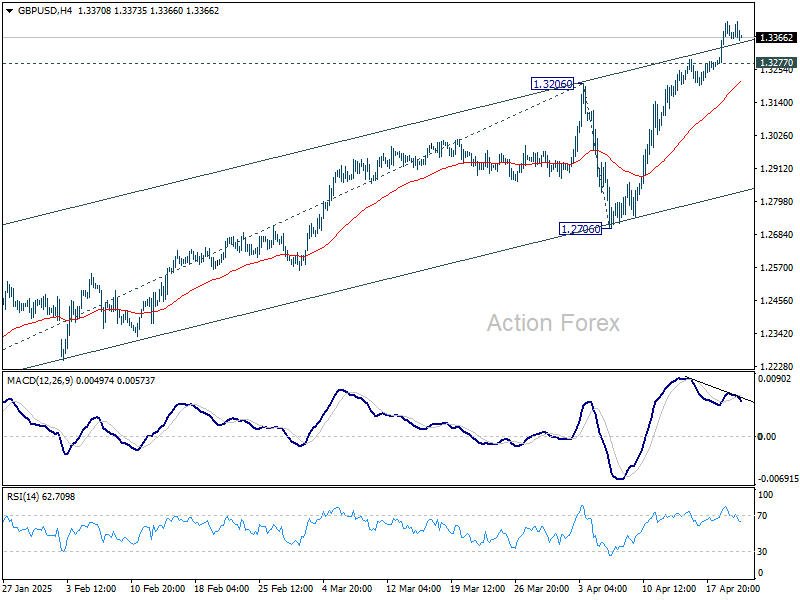

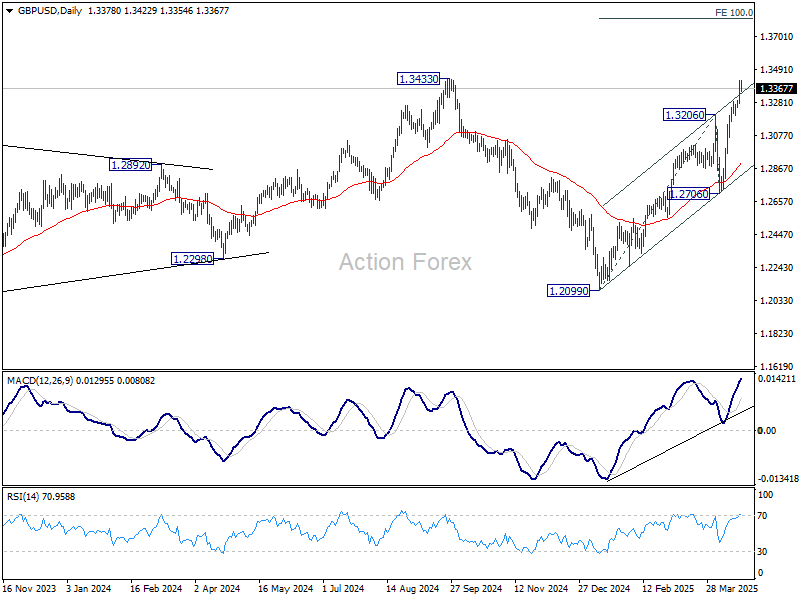

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3297; (P) 1.3359; (R1) 1.3444; More...

Further rally is expected in GBP/USD as long as 1.3277 support holds. Current rise should extend to retest 1.3433 high. Firm break there will confirm larger up trend resumption and target 100% projection of 1.2099 to 1.3206 from 1.2706 at 1.3813. Nevertheless, considering bearish divergence condition in 4H MACD, break of 1.3277 will indicate short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

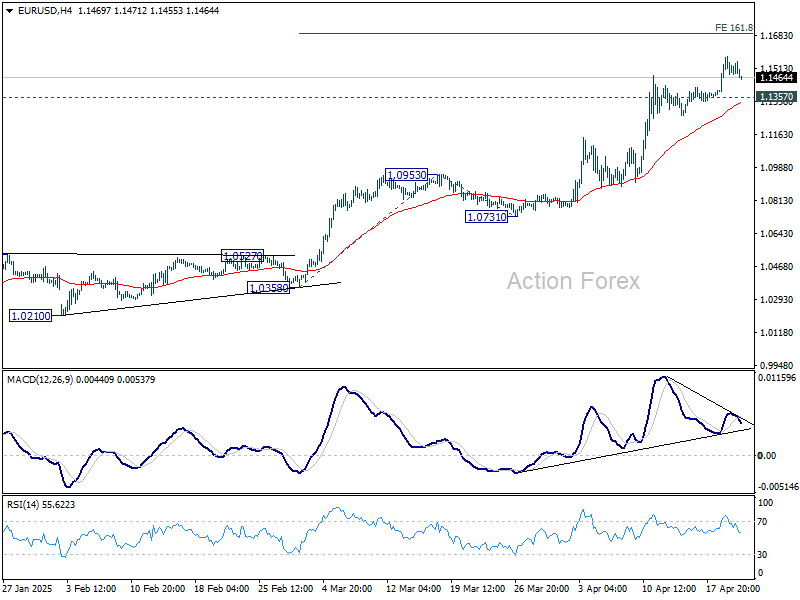

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1414; (P) 1.1494; (R1) 1.1592; More...

Further rally is expected in EUR/USD as long as 1.1357 support holds. Current rise from 1.0176 should target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694 next. Nevertheless, considering bearish divergence condition in 4H MACD, break of 1.1357 should indicate short term topping. Intraday bias will be turned back to the downside for deeper pullback.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

Fragile Calm Returns to Markets as Focus Shifts to Fed Remarks

Global markets saw a modest pause in volatility today as risk sentiment stabilized following yesterday’s US selloff. US futures are pointing to a mild recovery, helping to calm nerves in early trading. Meanwhile, US 10-year Treasury yield dipped slightly but remains elevated around 4.4%, reflecting persistent investor caution. Gold also retreated marginally after coming within striking distance of the 3500 mark earlier in the session, as the appetite for safe havens eased slightly.

Despite today’s calm, market sentiment remains on a knife edge. The political backdrop in the US continues to cast a long shadow over financial markets, with fears about Fed's independence following recent attacks by US President Donald Trump. Any further comments from US officials questioning Fed’s autonomy could quickly reignite volatility. For now, the market is watching closely for signals from a lineup of Fed speakers scheduled for the US session, who are expected to reinforce the central bank’s institutional independence and data-driven approach.

On the trade front, optimism remains scarce. The ongoing 90-day truce on US reciprocal tariffs has so far yielded little tangible progress, with talks reportedly stalling even among close allies like Japan. Uncertainty over what happens when the truce expires continues to weigh on global confidence, limiting the potential for any sustained rebound in risk assets.

In the currency markets, Loonie is underperforming for the week so far, followed by Dollar and Aussie. Yen leads on the stronger side, followed by Kiwi and Euro. Sterling and the Swiss Franc are positioning themselves in the middle of the pack.

Looking ahead, attention will quickly shift to tomorrow’s global flash PMI releases, which will provide a crucial read on business activity, prices and sentiment across major economies. These surveys will be particularly important in gauging the fallout from recent tariff shocks and in setting the tone for monetary policy discussions in the weeks ahead.

Technically, CAD/JPY's fall from 111.55 is now trying to resume through 101.36 support. The key level to watch is 61.8% projection of 110.45 to 101.36 from 105.85 at 100.23. There is prospect of a bounce from there to complete the five wave sequence from 111.55. However, firm break there should bring downside acceleration to 100% projection at 96.76 next.

In Europe, at the time of writing, FTSE is up 0.27%. DAX is down -0.46%. CAC is down -0.31%. UK 10-year yield is up 0.012 at 4.582. Germany 10-year yield is down -0.014 at 2.459. Earlier in Asia, Nikkei fell -0.17%. Hong Kong HSI rose 0.78%. China Shanghai SSE rose 0.25%. Singapore Strait Times rose 0.96%. Japan 10-year JGB yield rose 0.022 to 1.311.

ECB Survey: Inflation expectations tick higher, growth outlook softens

ECB’s latest Survey of Professional Forecasters for Q2 showed a modest upward revision to inflation expectations, signaling persistent price pressures across the Eurozone.

Headline HICP inflation is now expected to average 2.2% in 2025, before easing to 2.0% in both 2026 and 2027. These figures reflect a 0.1% upward revision for 2025 and 2026. Figures for 2027 was left unchanged.

Core inflation, which excludes energy and food, was also revised slightly higher across all horizons, now projected at 2.3% (prior 2.2%) in 2025 and 2.1% (prior 2.0%) for both 2026 and 2027.

Long-term expectations for headline inflation remain anchored at 2.0%, with core inflation expectations edging up from 1.9% to 2.0%.

On the growth front, the outlook was revised slightly lower for the near term. Real GDP is expected to expand by 0.9% in 2025 and 1.2% in 2026—both down -0.1% from the prior survey—before picking up to 1.4% in 2027. Longer-term growth expectations remain unchanged at 1.3%.

ECB's Kazimir sees rate near neutral, emphasize flexibility and agility

Slovak ECB Governing Council member Peter Kazimir said in a blog post today that Eurozone inflation is approaching the 2% target and expressed confidence that it will be reached “within the next few months.”

Following the recent rate cut, Kazimir suggested that ECB’s deposit rate at 2.25% is no longer restrictive and could now be considered close to neutral.

Meanwhile, Kazimir cautioned that the economic backdrop remains highly volatile, with uncertainty continuing to dominate the outlook.

“We are operating in a fast-shifting environment,” he said, pointing to escalating global trade tensions linked to US tariff policies as a key source of instability. He warned that this unpredictability "introduced significant ambiguity into the system, eroding confidence."

Looking ahead to the June meeting, Kazimir emphasized that any decision will depend on incoming data, revised economic forecasts, and a comprehensive risk assessment. His comments reinforce the central bank’s commitment to "flexibility and agility."

BoE’s Greene: US tariffs more of a disinflationary risk for the UK

BoE Monetary Policy Committee member Megan Greene stated today that the US tariffs pose "more of a disinflationary risk than an inflationary risk" for the UK.

However, she emphasized that domestic factors also remain a concern, particularly the UK’s limited supply capacity, which continues to drive underlying inflationary pressures.

Greene highlighted that this supply-side constraint is a key reason behind her cautious stance on interest rate cuts.

Addressing questions on central bank independence amid political scrutiny of the Fed, Greene emphasized the importance of maintaining institutional credibility.

"Credibility is the currency of central banks," she said, adding that independence is a critical component of that credibility.

New Zealand posts surprise NZD 970m trade surplus as exports surge 19%

New Zealand recorded stronger-than-expected trade surplus of NZD 970m in March, far exceeding forecasts of NZD 80m. The surprise was driven by a robust 19% yoy increase in goods exports, which rose by NZD 1.2B to NZD 7.6B. Imports also grew, up 12% yoy to NZD 6.6B.

Export performance was particularly strong across key trading partners. Shipments to China rose by NZD 371m (23% yoy), while exports to the US and the EU grew by 22% yoy and 51% yoy respectively. Exports to Japan also increased 11% yoy, although shipments to Australia dipped slightly, down -0.47% yoy.

On the import side, the largest increases came from the US, with a 48% yoy jump worth NZD 243m. This was followed by China and the EU, which posted 14% yoy and 19% yoy gains respectively. Imports from South Korea bucked the trend, falling -12% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1414; (P) 1.1494; (R1) 1.1592; More...

Further rally is expected in EUR/USD as long as 1.1357 support holds. Current rise from 1.0176 should target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694 next. Nevertheless, considering bearish divergence condition in 4H MACD, break of 1.1357 should indicate short term topping. Intraday bias will be turned back to the downside for deeper pullback.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

ECB’s Kazimir sees rate near neutral, emphasize flexibility and agility

Slovak ECB Governing Council member Peter Kazimir said in a blog post today that Eurozone inflation is approaching the 2% target and expressed confidence that it will be reached “within the next few months.”

Following the recent rate cut, Kazimir suggested that ECB’s deposit rate at 2.25% is no longer restrictive and could now be considered close to neutral.

Meanwhile, Kazimir cautioned that the economic backdrop remains highly volatile, with uncertainty continuing to dominate the outlook.

“We are operating in a fast-shifting environment,” he said, pointing to escalating global trade tensions linked to US tariff policies as a key source of instability. He warned that this unpredictability "introduced significant ambiguity into the system, eroding confidence."

Looking ahead to the June meeting, Kazimir emphasized that any decision will depend on incoming data, revised economic forecasts, and a comprehensive risk assessment. His comments reinforce the central bank’s commitment to "flexibility and agility."

BoE’s Greene: US tariffs more of a disinflationary risk for the UK

BoE Monetary Policy Committee member Megan Greene stated today that the US tariffs pose "more of a disinflationary risk than an inflationary risk" for the UK.

However, she emphasized that domestic factors also remain a concern, particularly the UK’s limited supply capacity, which continues to drive underlying inflationary pressures.

Greene highlighted that this supply-side constraint is a key reason behind her cautious stance on interest rate cuts.

Addressing questions on central bank independence amid political scrutiny of the Fed, Greene emphasized the importance of maintaining institutional credibility.

"Credibility is the currency of central banks," she said, adding that independence is a critical component of that credibility.

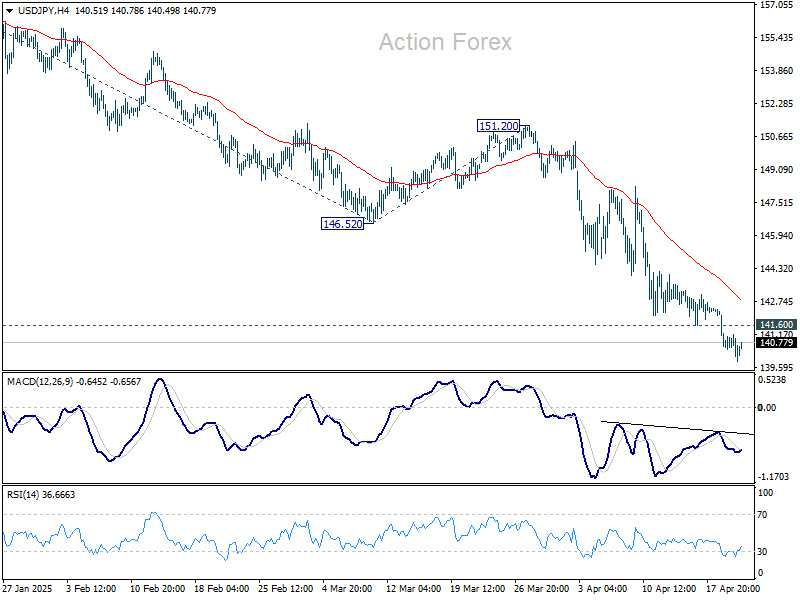

Yen Extends Gains, BOJ Core CPI Lower Than Expected

The Japanese yen has rallied for a third straight day. In the European session, USD/JPY is trading at 140.38, down 0.33% on the day. The yen has climbed 1.3% since Thursday, as the US dollar is under pressure against the major currencies.

BOJ Core CPI remains at 2.2%

BoJ Core CPI, a key inflation indicator, remained at 2.2% for a third consecutive month in March, shy of the forecast of 2.4%. This follows Japan's National Core CPI, which rose 3.2% y/y, matching expectations but higher than the 3.0% gain in February. National CPI eased to 3.6%, down from 3.7% in February and below the market estimate of 3.7%.

The inflation data comes a week before the BoJ's policy meeting next week. The central bank has signaled that it will continue to raise interest rates as wages and inflation have been rising. However, the risks to inflation and growth from US tariffs have muddied the rate outlook and the BoJ may decide to push off another hike until later in the year.

US and Japan meet to de-escalate trade war

The finance ministers of Japan and the US will meet later this week, as Tokyo looks to carve out some tariff exemptions. The BoJ is likely to sit tight and see if the talks lead to a breakthrough. The US is expected to bring up the exchange rate, as President Trump has accused Japan of deliberately keeping the yen weak in order to protect its export sector.

There are no key releases out of the US today, but we'll hear from three FOMC members later today. The markets have priced in a rate cut in May at 10%, with a 62% probability of a rate cut in June.

USD/JPY Technical

- USD/JPY tested support at 140.18 earlier. Below, there is support at 139.49

- There is resistance at 141.16 and 141.85

Dow Jones (DJIA) Technical Outlook: Value Stocks Do Not Provide a Safe Haven Refuge

- The recent sell-off in major US stock indices has been largely driven by broader macroeconomic factors.

- Value stocks may not be able to provide a hedge against undiversifiable risks.

- A further bear steepening of the US Treasury yield (10-year minus 2-year) with rising stagflation risk may trigger a negative feedback loop into the DJIA.

- Watch the 36,300 key intermediate support of the DJIA.

This is a follow-up analysis of our prior report on a related major US stock index, “Nasdaq 100 Technical Outlook: 12% monster rally may be a bull trap” dated 10 April.

Since our last publication, the Nasdaq 100 CFD Index (a proxy for the Nasdaq 100 E-mini futures) has staged a bearish reaction after a retest of its 20-day moving average and shed 8.7% to print an intraday low of 17,592 on Monday, 21 Monday.

In comparison, the US Wall Street 30 CFD Index (a proxy of the Dow Jones Industrial Average futures), which has lesser weightage towards technology and Artificial Intelligence (AI) stocks, has also tumbled over the same period, albeit a slightly smaller loss of 7.7%

Macro factor is now a more significant driver for US stock market performance

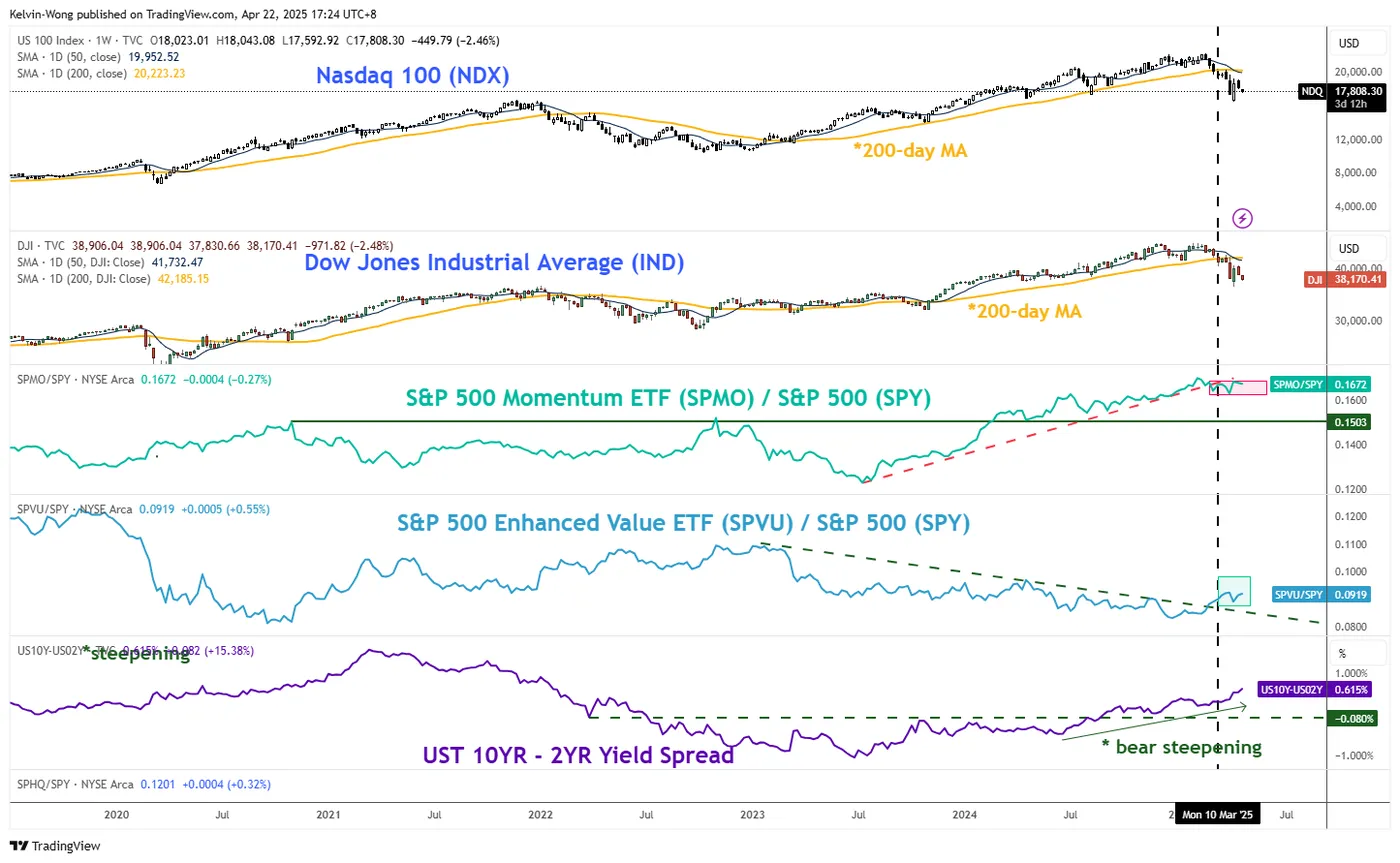

Fig 1: Nasdaq 100, DJIA, momentum, value factors, US Treasury yield curve major trends as of 22 Apr 2025 (Source: TradingView)

The prior medium-term uptrend phase of the Nasdaq 100 from August 2024 to February 2025 has been supported by the momentum factor of the US stock market. This finding can be seen by plotting a relative strength (ratio chart) of the S&P 500 momentum exchange-traded fund (ETF) over the mega-cap weighted S&P 500 ETF

The prior outperformance of the S&P 500 momentum ETF over the S&P 500 ETF was depicted by its rising ratio chart that moved in direct tandem with the Nasdaq 100’s medium-term trend phase from August 2024 to February 2025.

On the week of 10 March 2025, the outperformance of the S&P 500 momentum ETF had started to dwindle as its ratio chart against the S&P 500 ETF had rolled under its former key ascending support, which in turn, saw the Nasdaq 100 tumble below its key 200-day moving average.

In contrast, over the same period (the week of 10 March), the value factor of the US stock market started to outperform, as depicted by the relative strength (ratio chart) of the S&P 500 momentum exchange-traded fund (ETF) over the S&P 500 ETF broke above its former key descending resistance (see Fig 1).

The Dow Jones Industrial Average tends to be viewed as a more “value-oriented” barometer benchmark US stock index due to its higher weightage of value-related sectors, such as Financials and Health, over the Nasdaq 100; these two sectors have a combined weightage of close to 40%.

However, the value factor has failed to propel up the Dow Jones Industrial Average as it has moved in direct synchronisation with the bearish movement inflicted on the Nasdaq 100, as it too broke below its key 200-day moving average on the week of 10 March and continued to trade below it at this time of writing.

The main driver of the Dow Jones Industrial Average at this juncture seems to be dictated by the macro factors (undiversifiable risks), where the US Treasury yield curve (10-year yield minus 2-year yield) has shaped a bear steepening movement.

The steepening of the US Treasury yield has been driven by the 10-year US Treasury yield, which rose by 21 basis points (bps) from the week of 10 March till today, and in comparison, the 2-year US Treasury yield has fallen by 24 bps.

The current bear steepening of the US Treasury yield curve is a negative signal for the broader US stock market, especially when viewed in the context of recent economic indicators. Preliminary data from the University of Michigan’s Consumer Sentiment and Inflation Expectations for April point to rising stagflation risks, characterized by slowing growth alongside persistent inflation. A continued steepening of the yield curve suggests a higher cost of funding, which, combined with weaker growth prospects, could weigh heavily on corporate earnings in the coming quarters.

DJIA at risk of breaking its key support at 36,300

Fig 2: US Wall Street 30 CFD long-term & major trends as of 23 Apr 2025 (Source: TradingView)

In the past week, the price actions of the US Wall Street 30 CFD Index (a proxy of the Dow Jones Industrial Average futures) have almost wiped out 80% of the gains triggered by US President Trump’s early announcement of the 90-day pause on the higher US reciprocal tariffs rates on 9 March.

The US Wall Street 30 CFD Index has slipped by 5.7% since the week of 14 April, coupled with a bearish momentum condition reading seen on its weekly RSI momentum indicator as it shaped a “lower high” below its 50 level and has not reached its oversold region (see Fig 2).

Watch the key intermediate support at 36,300 (also close to the long-term secular ascending channel support from the 23 March 2020 low), a break with a weekly close below it may trigger the start of a potential multi-month major downtrend phase to expose the next medium-term supports at 34,010 and 31,810 in the first step.

On the other hand, a clearance above 42,080 key medium-term pivotal resistance invalidates the bearish scenario to see a squeeze to retest the 45,150/45,475 long-term pivotal resistance zone.

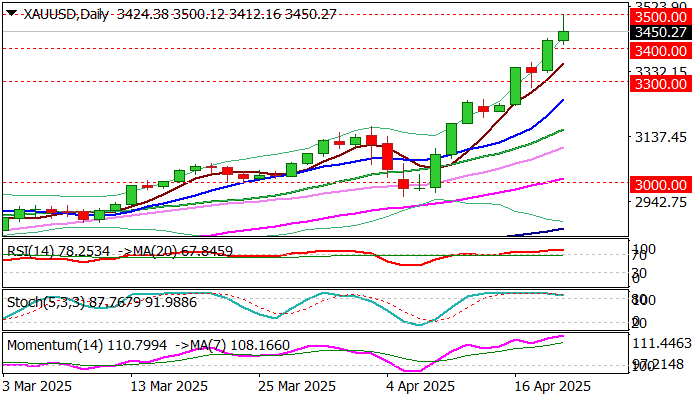

Gold Surges to $3500

Gold skyrocketed since Monday’s opening ($3333) and hit $3500 on Tuesday morning, advancing 5% in slightly more than 24 hours.

It seems that rally since the start of the year is unlikely to slow but continues to accelerate (gold was up around 33% from January 1 until today) as conditions continue to deteriorate that fuels demand for safe-haven yellow metal.

Many analysts saw $3500 level as target for this year and I joined this expectations, anticipating that euphoria over Trump’s radical measures was about to start fading, with expected peace talks in Ukraine, adding to scenario.

However, recent waves of trade tariff stories, particularly on deepening crisis between the US and China, world’s two largest economies, and Trump’s latest attempt to fire the first man of the US Federal Reserve that strongly undermined investors’ confidence in the US economy, sparked further migration into safety, which shows no signs of ending so far.

Touch of $3500 was followed by sharp pullback, partially due to significance of this level, but more due to strongly overbought daily studies which warn that bulls may take a breather for consolidation and positioning for renewed attack at $3500 barrier.

Monday’s high ($3430) and today’s session low ($3412) mark initial support, along with psychological $3400 level, which should ideally contain pullback and keep larger bulls intact, while loss of $3400 handle would signal deeper correction, and expose supports at $3350/$3330 and $3300.

Res: 3466; 3500; 3521; 3535

Sup: 3430; 3412; 3400; 3450