Sample Category Title

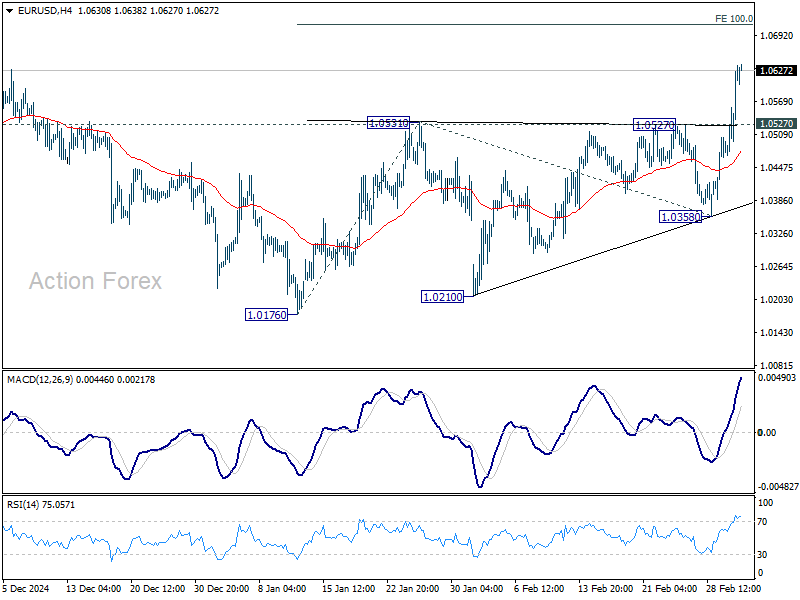

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0522; (P) 1.0575; (R1) 1.0679; More...

EUR/USD's current upside acceleration argues that bullish trend reversal is probably already underway. Intraday bias stays on the upside for 100% projection of 1.0176 to 1.0531 from 1.0358 at 1.0173. Decisive break there will solidify this bullish case and target 161.8% projection at 1.0932 next. On the downside, below 1.0527 resistance turned support will turn intraday bias neutral again first.

In the bigger picture, the strong rebound from 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199 argues that fall from 1.1274 might be a correction only. Sustained trading above 55 W EMA (now at 1.0668) should indicate that this correction has already completed with three waves down to 1.0176. Rise from 0.9534 (2022 low) might then be ready to resume through 1.1274. Nevertheless, rejection by 55 W EMA would keep outlook bearish for another fall through 1.0176 at a later stage.

Euro Stays Strong, While Markets Stabilize on China’s Stimulus and Hopes for Trump’s Tariff Compromise

Despite the steep selloff on Wall Street overnight, sentiment appears to have improved somewhat in Asia. Investors found reasons for optimism as China set a 2025 GDP growth target of around 5% and announced stimulus measures to counter escalating tensions with the U.S. In a notable shift, Beijing raised its budget deficit target to roughly 4% of GDP, marking the highest level since at least 2010. Stocks in Hong Kong led regional gains, reflecting hopes that China’s commitment to boosting domestic growth will help offset some global headwinds.

In the US, there is cautious optimism following remarks from Commerce Secretary Howard Lutnick, who revealed that President Donald Trump may unveil a compromise deal with Canada and Mexico as early as Wednesday. Such a pact could potentially scale back the recently enacted 25% tariffs. However, any progress on that front may be overshadowed by the looming threat of reciprocal tariffs, particularly on the EU, set to be announced in early April.

While US equity futures received a minor lift from Lutnick’s comments, investors remain wary that ongoing protectionist policies could still drive the economy toward recession. Upcoming US ISM services data will be a crucial test for investor confidence, as weak results could deepen economic concerns and overshadow any positive developments on trade negotiations.

Meanwhile, Euro is lifted by Europe’s increasing focus on rearmament. The European Commission has proposed borrowing up to EUR 150B to lend to EU governments under a new defense initiative, citing growing threats from Russia and diminishing confidence in US security commitments. The package, championed by Commission President Ursula von der Leyen, could mobilize up to EUR 800B for European defense priorities, including air defense, missile systems, and drone technology.

Germany is also making significant moves, with the prospective coalition between the CDU/CSU and SPD pledging to loosen the country’s debt brake. This reform would allow higher defense spending and facilitate the creation of a EUR 500B infrastructure fund over the next decade. By exempting defense spending above 1% of GDP from debt limits, Berlin is positioning itself for a substantial boost in military expenditure—a development viewed positively by market participants anticipating a multi-year European rearmament cycle.

In the currency markets, Dollar remains the worst performer for the week, despite some respite today. Canadian Dollar and Japanese Yen are also under pressure. Conversely, Euro continues to top the leader board, bolstered by optimism around Europe’s defense plans, while Sterling and Swiss Franc follow. Caught in the middle are the Australian and New Zealand Dollars, which face mixed prospects. On one hand, they remain vulnerable to US-China trade friction, but on the other, they could gain support if China’s stimulus measures help stabilize demand for commodities.

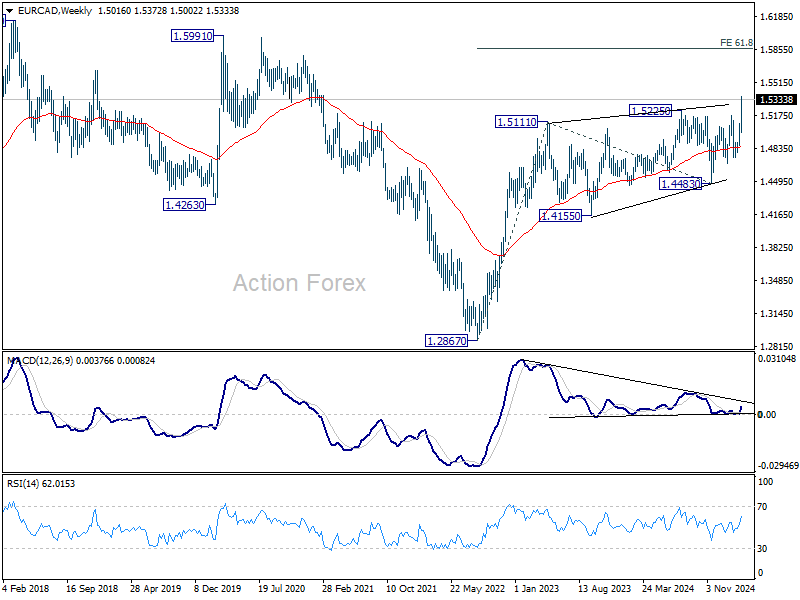

Technically, EUR/CAD's strong break of 1.5225 resistance this week confirms resumption of long term up trend from 1.2867 (2022 low). Further rise is now expected to 61.8% projection of 1.2867 to 1.5111 from 1.4483 at 1.5870 in the medium term. This will now remain the favored case as long as this week's low at 1.5002 holds.

In Asia, at the time of writing, Nikkei is up 0.44%. Hong Kong HSI is up 2.27%. China Shanghai SSE is up 0.44%. Singapore Strait Times is up 0.30%. Japan 10-year JGB yield is up 0.017 at 1.443. Overnight, DOW fell -1.55%. S&P 500 fell -1.22%. NASDAQ fell -0.35%. 10-year yield rose 0.030 to 4.210.

BoJ's Uchida: Interest rate to gradually approach neutral by late FY 2025 to FY 2026

BoJ Deputy Governor Shinichi Uchida reinforced today that interest rates will continue to rise if the bank’s economic projections hold. He highlighted in a speech that BoJ expects inflation to stabilize around the 2% target in the second half of fiscal 2025 to fiscal 2026, with "effects of the cost-push wane" while underlying inflation strengthens with wages growth.

"The policy interest rate at that time is considered to approach an interest rate level that is neutral to economic activity and prices," he added.

However, Uchida acknowledged that determining the "neutral" interest rate level remains uncertain. While in theory, it should be around 2% plus Japan’s natural rate of interest, estimates for the latter vary significantly from -1% to +0.5%.

Given this wide range and estimation errors, BoJ will avoid relying solely on theoretical models and instead "examine the response of economic activity and prices as it raises the policy interest rate"

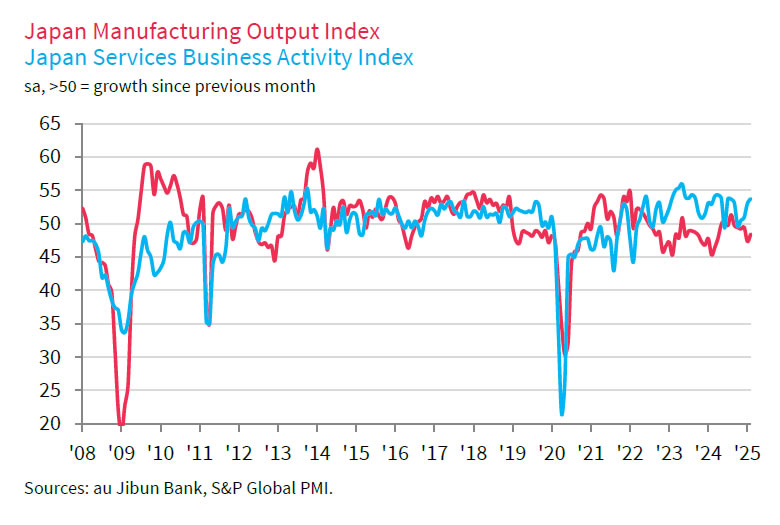

Japan's PMI service finalized at 53.7, sector strengthens but confidence wanes on labor shortages and trade risks

Japan's PMI Services was finalized at 53.7 in February, up from January's 53.0, marking a six-month high. PMI Composite also improved from 51.1 to 52.0, the strongest reading since September 2024.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence, service sector businesses saw higher sales volumes, with export demand contributing to the expansion. Meanwhile, the broader private sector recorded its steepest rise in activity in five months, supported by a milder contraction in manufacturing.

Despite the growth, overall business confidence showed signs of softening. Bhatti noted Firms expressed concerns over labor shortages and uncertainty stemming from US trade policies, leading to the weakest sentiment since January 2021.

RBA’s Hauser: Uncertain on further easing disputes market’s rate-cut outlook

RBA Deputy Governor Andrew Hauser emphasized in a speech today that monetary policy is set to ensure inflation returns to the midpoint of the target range, which is crucial for maintaining price stability over the long run.

He justified the February rate cut, stating that it “reduces the risks of inflation undershooting that midpoint.”

However, Hauser pushed back against market expectations of a sustained easing cycle, saying the "Board does not currently share the market’s confidence that a sequence of further cuts will be required".

While Hauser acknowledged that interest rates will go where they need to go to balance inflation control with full employment, he made it clear that progress so far does not warrant complacency.

He stressed that RBA will continue to assess economic developments on a “meeting by meeting” basis.

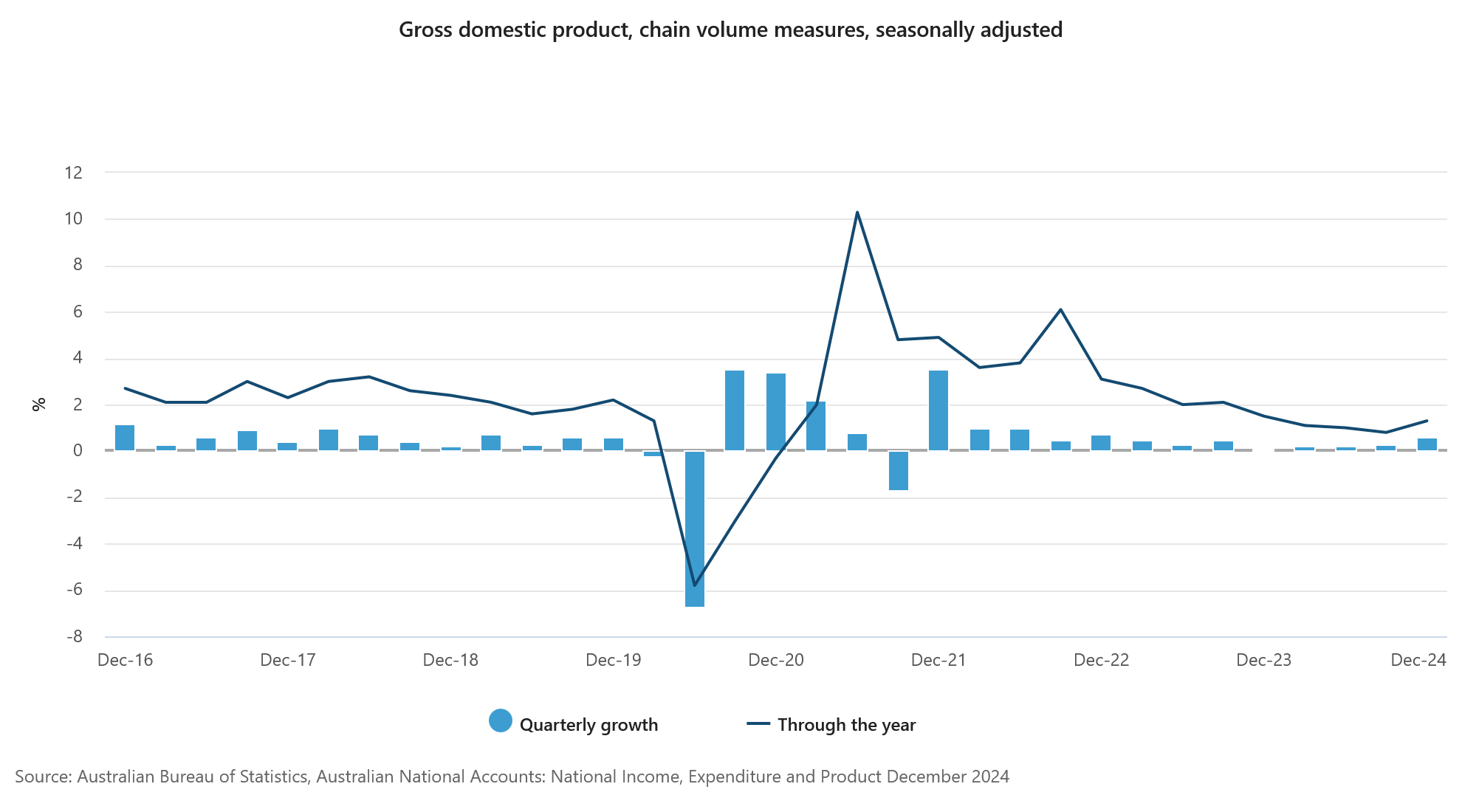

Australia’s GDP grows 0.6% qoq in Q4, ending per capita contraction streak

Australia’s GDP grew by 0.6% qoq in Q4, exceeding expectations of 0.5% qoq, while annual growth stood at 1.3% yoy. A key highlight was the 0.1% qoq per capita GDP growth, marking the first increase after seven consecutive quarters of contraction.

According to Katherine Keenan, head of national accounts at the ABS, "Modest growth was seen broadly across the economy this quarter." She noted that both public and private spending contributed positively, alongside a rise in exports of goods and services.

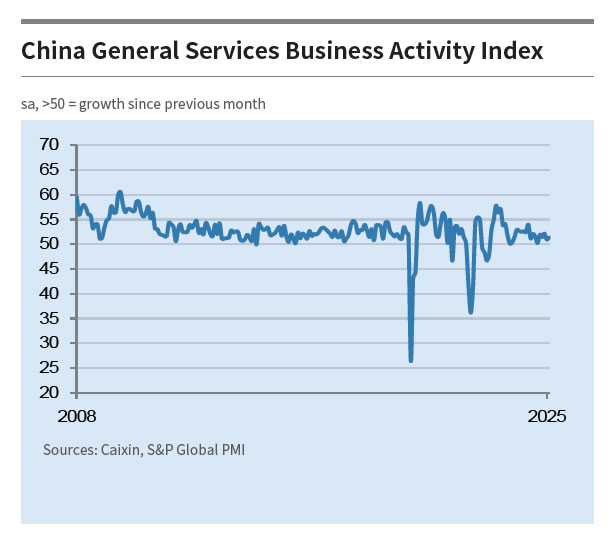

China’s Caixin PMI services rises to 5.14, but uncertainties rising in employment and income

China’s Caixin Services PMI climbed to 51.4 in February, up from 51.0, beating market expectations of 50.8. Composite PMI also improved slightly to 51.5, signaling steady expansion across both manufacturing and services for the 16th consecutive month.

According to Wang Zhe, Senior Economist at Caixin Insight Group, supply and demand showed improvement in both sectors, supported by robust consumption during the Chinese New Year holiday and technological innovations in select industries. However, "employment saw a slight contraction", mainly due to weakness in the manufacturing sector.

Concerns remain over China’s broader economic recovery. Wang noted that overall price levels "remained subdued", with declining sales prices in both manufacturing and services. "Rising uncertainties in employment and household income constraining efforts to boost domestic demand and stabilize the economy," he added.

Fed’s Williams: Tariff adds to inflation risks, no rush for rate cuts

New York Fed President John Williams acknowledged that tariffs could contribute to inflation pressures later this year, noting that consumer goods could likely see immediate price increases while other sectors may experience a more gradual impact.

However, he emphasized the high level of uncertainty surrounding trade policies, stating, “We don’t know how long the tariffs will apply. We don’t know what other countries may do in response to this.”

Beyond tariffs, Williams pointed out that fiscal and regulatory policies under the Trump administration would also play a key role in shaping the economic outlook and monetary policy decisions.

Williams also reiterated that the current policy stance remains appropriate. “I think the current place for policy is good. I don’t see any need to change it right away," he noted.

While acknowledging that rate cuts could be a possibility later this year, he was noncommittal, adding that it’s “really hard to know” if further easing will be necessary.

Looking ahead

Swiss CPI, Eurozone PMI services final and PPI, UK PMI services final will be released in European session. Later in the day, main focus will be on US ADP private employment and ISM services. Fed will also publish Beige Book economic report.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0522; (P) 1.0575; (R1) 1.0679; More...

EUR/USD's current upside acceleration argues that bullish trend reversal is probably already underway. Intraday bias stays on the upside for 100% projection of 1.0176 to 1.0531 from 1.0358 at 1.0173. Decisive break there will solidify this bullish case and target 161.8% projection at 1.0932 next. On the downside, below 1.0527 resistance turned support will turn intraday bias neutral again first.

In the bigger picture, the strong rebound from 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199 argues that fall from 1.1274 might be a correction only. Sustained trading above 55 W EMA (now at 1.0668) should indicate that this correction has already completed with three waves down to 1.0176. Rise from 0.9534 (2022 low) might then be ready to resume through 1.1274. Nevertheless, rejection by 55 W EMA would keep outlook bearish for another fall through 1.0176 at a later stage.

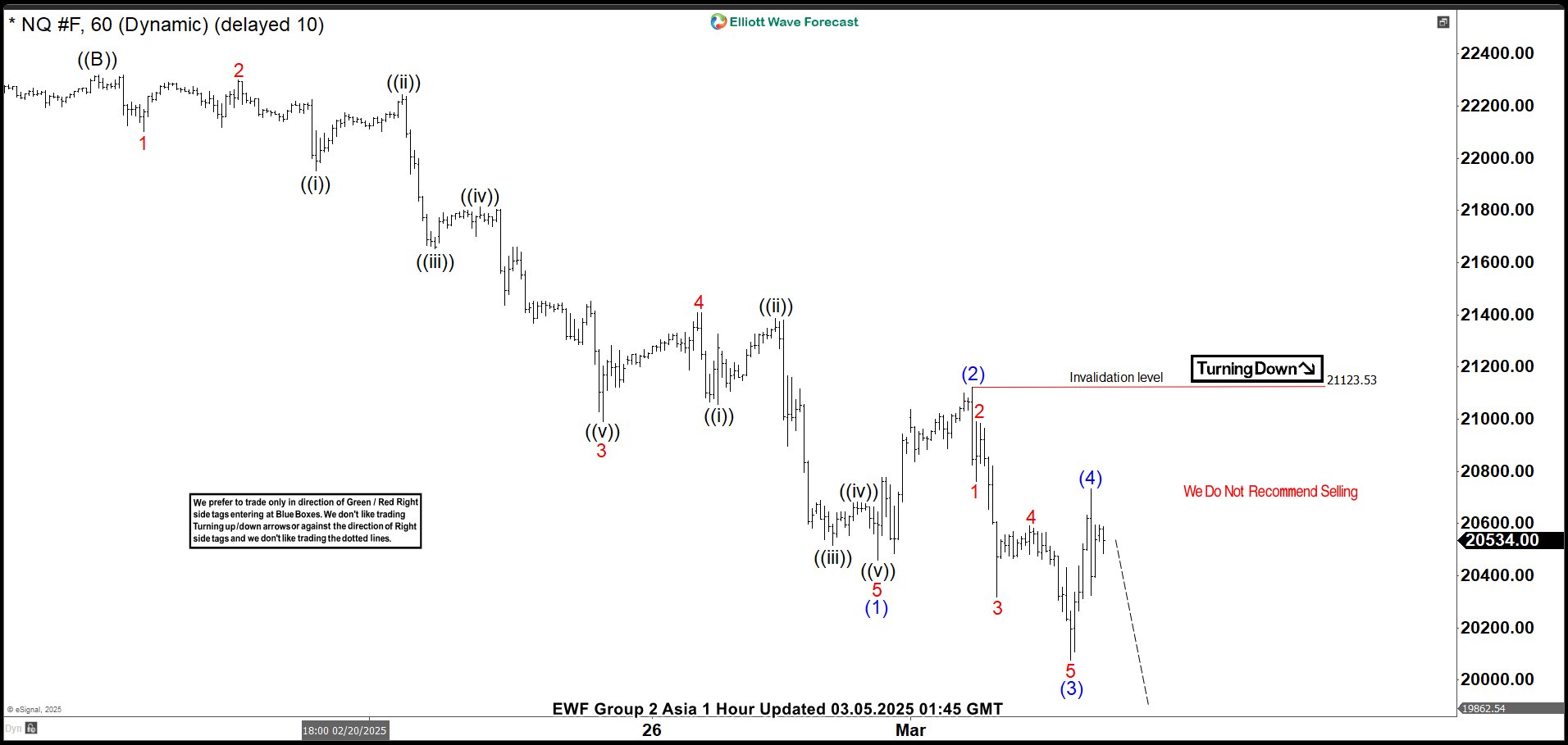

Elliott Wave View: Nasdaq (NQ) Has Reached Support Area

Nasdaq (NQ) has reached the extreme area from 12.16.2024 peak and thus the Index may see support soon for a 3 waves rally at least. Near term, decline from 2.18.2025 peak is in progress as a 5 waves diagonal. Down from 2.18.2025 peak, wave 1 ended at 22102.75 and wave 2 rally ended at 22299.75. The Index then nested lower in wave 3. Down from wave 2, wave ((i)) ended at 21951 and wave ((ii)) ended at 22245.5. The Index extended lower in wave ((iii)) towards 21652.75 and wave ((iv)) ended at 21813. Final wave ((v)) lower ended at 20990 which completed wave 3 in higher degree.

Wave 4 rally ended at 21409.25. Final wave 5 lower ended at 20460.5 which completed wave (1) of ((C)) in higher degree. Rally in wave (2) ended at 21123.53 and wave (3) lower ended at 20075.25. Rally in wave (4) is proposed complete at 20732.5. Near term, as far as pivot at 21123.53 high stays intact, expect the Index to extend lower in wave (5). The extreme area from 12.16.2024 peak comes at 19452 – 20543 where the current decline can end and the Index can see support.

Nasdaq (NQ) 60 Minutes Elliott Wave Chart

NQ Video

https://www.youtube.com/watch?v=K2K5EYK5XdE

WTI Crude Oil Price Slump Deepens—What’s Next For The Market?

Key Highlights

- WTI Crude Oil prices started a fresh decline below the $70.00 support.

- It traded below a key contracting triangle at $67.85 on the 4-hour chart.

- Gold prices started another increase and surpassed the $2,895 resistance.

- Bitcoin restarted its decrease and traded below $88,000.

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price failed to clear the $71.20 resistance. The price started a fresh decline below $70.20 and $70.00 to enter a bearish zone.

Looking at the 4-hour chart of XTI/USD, the price settled below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). It traded below a key contracting triangle at $67.85.

The bears seem to be in action below the $68.80 pivot level. On the upside, the price is facing hurdles near the $68.40 level. The main hurdle is now near the $69.20 zone, above which the price may perhaps accelerate higher.

In the stated case, it could even visit the $70.80 resistance and the 100 simple moving average (red, 4-hour). Any more gains might call for a test of the $72.00 resistance zone in the near term.

On the downside, the first major support sits near the $67.00 zone. A daily close below $67.00 could open the doors for a larger decline. The next major support is $65.80. Any more losses might send oil prices toward $65.00 in the coming days.

Looking at Gold, there was a strong increase above the $2,895 level and the price could extend gains in the near term.

Economic Releases to Watch Today

- Euro Zone Services PMI for Feb 2025 – Forecast 50.7, versus 50.7 previous.

- UK Services PMI for Feb 2025 – Forecast 51.1, versus 51.1 previous.

- US Services PMI for Feb 2025 – Forecast 49.7, versus 49.7 previous.

- US ISM Services Index for Feb 2025 – Forecast 52.9, versus 52.8 previous.

China’s Caixin PMI services rises to 5.14, but uncertainties rising in employment and income

China’s Caixin Services PMI climbed to 51.4 in February, up from 51.0, beating market expectations of 50.8. Composite PMI also improved slightly to 51.5, signaling steady expansion across both manufacturing and services for the 16th consecutive month.

According to Wang Zhe, Senior Economist at Caixin Insight Group, supply and demand showed improvement in both sectors, supported by robust consumption during the Chinese New Year holiday and technological innovations in select industries. However, "employment saw a slight contraction", mainly due to weakness in the manufacturing sector.

Concerns remain over China’s broader economic recovery. Wang noted that overall price levels "remained subdued", with declining sales prices in both manufacturing and services. "Rising uncertainties in employment and household income constraining efforts to boost domestic demand and stabilize the economy," he added.

BoJ’s Uchida: Interest rate to gradually approach neutral by late FY 2025 to FY 2026

BoJ Deputy Governor Shinichi Uchida reinforced today that interest rates will continue to rise if the bank’s economic projections hold. He highlighted in a speech that BoJ expects inflation to stabilize around the 2% target in the second half of fiscal 2025 to fiscal 2026, with "effects of the cost-push wane" while underlying inflation strengthens with wages growth.

"The policy interest rate at that time is considered to approach an interest rate level that is neutral to economic activity and prices," he added.

However, Uchida acknowledged that determining the "neutral" interest rate level remains uncertain. While in theory, it should be around 2% plus Japan’s natural rate of interest, estimates for the latter vary significantly from -1% to +0.5%.

Given this wide range and estimation errors, BoJ will avoid relying solely on theoretical models and instead "examine the response of economic activity and prices as it raises the policy interest rate"

Japan’s PMI service finalized at 53.7, sector strengthens but confidence wanes on labor shortages and trade risks

Japan's PMI Services was finalized at 53.7 in February, up from January's 53.0, marking a six-month high. PMI Composite also improved from 51.1 to 52.0, the strongest reading since September 2024.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence, service sector businesses saw higher sales volumes, with export demand contributing to the expansion. Meanwhile, the broader private sector recorded its steepest rise in activity in five months, supported by a milder contraction in manufacturing.

Despite the growth, overall business confidence showed signs of softening. Bhatti noted Firms expressed concerns over labor shortages and uncertainty stemming from US trade policies, leading to the weakest sentiment since January 2021.

RBA’s Hauser: Uncertain on further easing disputes market’s rate-cut outlook

RBA Deputy Governor Andrew Hauser emphasized in a speech today that monetary policy is set to ensure inflation returns to the midpoint of the target range, which is crucial for maintaining price stability over the long run.

He justified the February rate cut, stating that it “reduces the risks of inflation undershooting that midpoint.”

However, Hauser pushed back against market expectations of a sustained easing cycle, saying the "Board does not currently share the market’s confidence that a sequence of further cuts will be required".

While Hauser acknowledged that interest rates will go where they need to go to balance inflation control with full employment, he made it clear that progress so far does not warrant complacency.

He stressed that RBA will continue to assess economic developments on a “meeting by meeting” basis.

Australia’s GDP grows 0.6% qoq in Q4, ending per capita contraction streak

Australia’s GDP grew by 0.6% qoq in Q4, exceeding expectations of 0.5% qoq, while annual growth stood at 1.3% yoy. A key highlight was the 0.1% qoq per capita GDP growth, marking the first increase after seven consecutive quarters of contraction.

According to Katherine Keenan, head of national accounts at the ABS, "Modest growth was seen broadly across the economy this quarter." She noted that both public and private spending contributed positively, alongside a rise in exports of goods and services.

Fed’s Williams: Tariff adds to inflation risks, no rush for rate cuts

New York Fed President John Williams acknowledged that tariffs could contribute to inflation pressures later this year, noting that consumer goods could likely see immediate price increases while other sectors may experience a more gradual impact.

However, he emphasized the high level of uncertainty surrounding trade policies, stating, “We don’t know how long the tariffs will apply. We don’t know what other countries may do in response to this.”

Beyond tariffs, Williams pointed out that fiscal and regulatory policies under the Trump administration would also play a key role in shaping the economic outlook and monetary policy decisions.

Williams also reiterated that the current policy stance remains appropriate. “I think the current place for policy is good. I don’t see any need to change it right away," he noted.

While acknowledging that rate cuts could be a possibility later this year, he was noncommittal, adding that it’s “really hard to know” if further easing will be necessary.