Sample Category Title

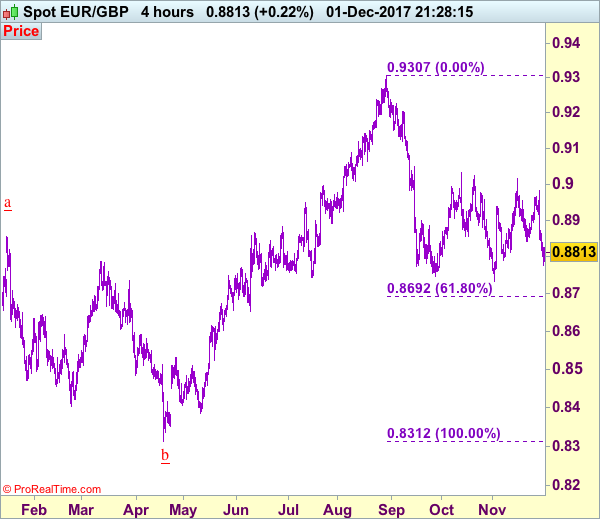

Trade Idea: EUR/GBP – Target met and sell at 0.8885

EUR/GBP - 0.8815

Original strategy :

Sold at 0.8950, met target at 0.8820

Position : - Short at 0.8950

Target : - 0.8820

Stop : -

New strategy :

Sell at 0.8885, Target: 0.8750, Stop: 0.8920

Position : -

Target : -

Stop : -

The single currency did drop after meeting renewed selling interest at 0.8982, our short position entered at 0.8950 met downside target at 0.8820 with 130 points profit, as price has remained under pressure, bearishness remains for the fall from 0.9015 to extend weakness to 0.8770-75, then towards previous support at 0.9733 which is likely to hold on first testing.

In view of this, we are looking to reinstate short on recovery as 0.8880-85 should limit upside. Above previous support at 0.8915 (now resistance) would defer and prolong choppy trading, risk rebound to 0.8935-40, however, still reckon said resistance at 0.8982 would cap upside and bring another retreat later. Only above indicated resistance at 0.9015 would risk test of previous resistance at 0.9033 but only a breach of this level would signal an upside break of recent established broad range has occurred, then subsequent rise to 0.9070-75 would follow.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

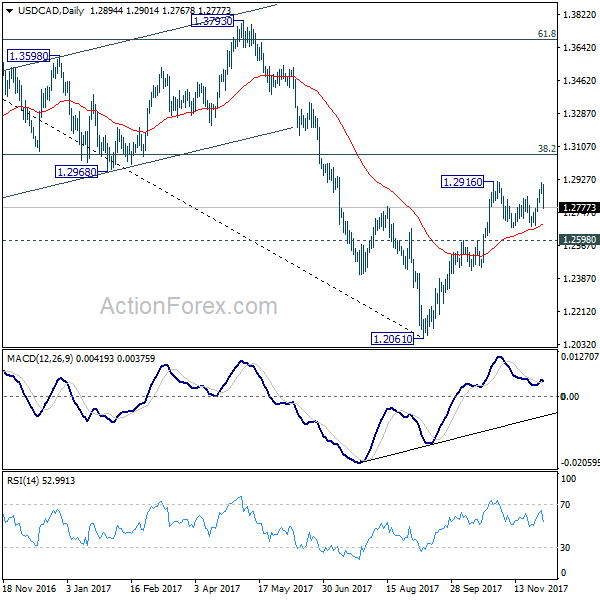

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2822; (P) 1.2847; (R1) 1.2890; More....

USD/CAD's sharp fall and break of 1.2804 support indicates rejection from 1.2916. Consolidation from 1.2916 is extending with another falling leg. Intraday bias is turned back to the downside for 1.2665 support or possibly below. Still, we'd expect downside to be contained by 1.2598 resistance turned support and bring rise resumption. On the upside, decisive break of 1.2916 will confirm resumption of whole rally from 1.2061. In that case, USD/CAD should target 1.3065 medium term fibonacci level next.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Canadian Dollar Surges after Stellar Job Data, Dollar Cautious as Senate Tax Debate Resumes

Canadian Dollar rebound strongly in early US session after stellar economic data. The employment market grew 79.5k in November, more than double of prior month's 35.3k and was well above expectation of 10k. Unemployment rate also dropped to 5.9%, down from 6.3%, way below expectation of 5.9%. USD/CAD reached as high as 1.2908 yesterday on Dollar strength. But the current sharp fall and break of 1.2804 support suggests rejection from 1.2916 key resistance. And consolidation from there is extending with another decline, possibly back to 1.2665 support. Also from Canada, GDP grew 0.2% mom in September, above expectation of 0.1% mom.

The greenback, on the other hand, remains cautiously soft as markets await Senate vote on tax bill. There will be a marathon vote on amendments today. A key focus would be on details of how future deficits would be addressed. The Joint Committee on Taxation found that the Senate's version of the bill could only generate USD 458b in revenue from boosted growth. That's far from being above to cover the USD 1.4T loss. Republicans are expecting to pass the bill finally by tonight. But there are still uncertainties as Republicans can only lose two votes due to slim 52 majority.

UK and Eurozone manufacturing PMIs improved

UK PMI manufacturing jumped to 58.2 in November, up from 56.6 and beat expectation of 56.5. That's also the highest reading in over four years since August 2013. Markit noted that "on its current course, manufacturing production is rising at a quarterly rate approaching 2 percent, providing a real boost to the pace of broader economic expansion". However, "manufacturers have seen supply-chain constraints and rising demand for raw materials overtake exchange rate effects as the primary motivator of price increases."

From Eurozone, Eurozone PMI manufacturing was revised up by 0.1 to 60.1 in November. Germany PMI manufacturing was unrevised at 62.5. France PMI manufacturing was revised up by 0.2 to 57.7. Italy PMI manufacturing rose to 58.3 in November. From Swiss, PMI manufacturing rose to 65.1 in November up from 62.0 and beat expectation of 62.5.

China Caixin PMI manufacturing missed expectations

The Caixin manufacturing PMI for China slipped to 50.8 in November, from 51 in October. The reading also missed expectations of 51. Looking into the details, production and new orders increased at modest rates, while purchasing costs rose sharply. However, confidence towards the business outlook dropped to joint-lowest on record. As the agency noted, the manufacturing sector remained stable for most of November, despite 'some signs of weakness'. It forecast that the economy would remain stable for 4Q17. More in China's November PMIs Helped by 'Double-11'

Released earlier today, Japan national CPI rose to 0.8% yoy in October, Tokyo CPI was unchanged at 0.6% yoy in November. Inflation stays well below the 2% target and justify BoJ's massive stimulus. Also from Japan, unemployment rate was unchanged at 2.8% in October, household spending rose 0.0%. Japan capital spending rose 4.2% in Q3. PMI manufacturing was revised down to 50.8 in November. Also released, New Zealand terms of trade index rose 0.7% qoq in Q3, below expectation of 0.7% qoq.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2822; (P) 1.2847; (R1) 1.2890; More....

USD/CAD's sharp fall and break of 1.2804 support indicates rejection from 1.2916. Consolidation from 1.2916 is extending with another falling leg. Intraday bias is turned back to the downside for 1.2665 support or possibly below. Still, we'd expect downside to be contained by 1.2598 resistance turned support and bring rise resumption. On the upside, decisive break of 1.2916 will confirm resumption of whole rally from 1.2061. In that case, USD/CAD should target 1.3065 medium term fibonacci level next.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q/Q Q3 | 0.70% | 1.30% | 1.50% | 1.40% |

| 23:30 | JPY | Unemployment Rate Oct | 2.80% | 2.80% | 2.80% | |

| 23:30 | JPY | Overall Household Spending Y/Y Oct | 0.00% | -0.30% | -0.30% | |

| 23:30 | JPY | National CPI Core Y/Y Oct | 0.80% | 0.80% | 0.70% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Nov | 0.60% | 0.60% | 0.60% | |

| 23:50 | JPY | Capital Spending Q3 | 4.20% | 3.20% | 1.50% | |

| 00:30 | JPY | PMI Manufacturing Nov F | 53.6 | 53.8 | 53.8 | |

| 01:45 | CNY | Caixin PMI Manufacturing Nov | 50.8 | 51 | 51 | |

| 08:30 | CHF | PMI Manufacturing Nov | 65.1 | 62.5 | 62 | |

| 08:45 | EUR | Italy Manufacturing PMI Nov | 58.3 | 58.3 | 57.8 | |

| 08:50 | EUR | France Manufacturing PMI Nov F | 57.7 | 57.5 | 57.5 | |

| 08:55 | EUR | Germany Manufacturing PMI Nov F | 62.5 | 62.5 | 62.5 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Nov F | 60.1 | 60 | 60 | |

| 09:30 | GBP | PMI Manufacturing Nov | 58.2 | 56.5 | 56.3 | 56.6 |

| 13:30 | CAD | GDP M/M Sep | 0.20% | 0.10% | -0.10% | |

| 13:30 | CAD | Net Change in Employment Nov | 79.5K | 10.0k | 35.3k | |

| 13:30 | CAD | Unemployment Rate Nov | 5.90% | 6.20% | 6.30% | |

| 14:30 | CAD | Manufacturing PMI Nov | 54.3 | |||

| 14:45 | USD | Manufacturing PMI Nov F | 53.8 | 53.8 | ||

| 15:00 | USD | ISM Manufacturing Nov | 58.3 | 58.7 | ||

| 15:00 | USD | ISM Prices Paid Nov | 67.8 | 68.5 | ||

| 15:00 | USD | Construction Spending M/M Oct | 0.50% | 0.30% |

Pound Slips; Stocks Decline; US Tax Vote Awaited; Canada’s GDP Growth Eyed

Here are the latest developments in global markets:

- FOREX: The pound turned to be the worst performer among major currencies despite impressive manufacturing PMI figures, trading below the $1.3500 key level after touching a fresh two-month high of 1.3548 early in the Asian trading (-0.25%). Eurozone's manufacturing PMI stood at multi-year highs, but the euro pared earlier gains, falling back to 1.1900. Dollar/yen remained flat at 112.33, while dollar/loonie was steady at 1.288. The kiwi overperformed its peers, jumping to $0.6550 (+0.22%).

- Stocks: European stocks declined as technology shares dragged the market. The pan-European STOXX 600 fell to a two-week low (- 0.75%), the British FTSE 100 index lost 0.35% and the German DAX 30 index dived by 1.15%. US stock futures were in the red.

- COMMODITIES: Oil prices held onto gains after OPEC and non-OPEC members including Russia compromised to extend supply-cuts until the end of 2018. However, the deal's desired effects are now depending on the US and China. WTI crude was 0.75% up at $57.74 per barrel and Brent gained 0.88% to $63.10. Gold was roughly flat at $1,276.0 per ounce.

Day ahead: US tax story & Brexit in the background; Canada's GDP growth under scrutiny

The loonie and the dollar would attract some caution by investors as economic releases out of Canada and the US during European trading hours might bring some volatility to the currencies. Besides that, markets would be sensitive to any updates in the US tax story after Senate Republicans decided yesterday to postpone voting on the tax bill to Friday over disagreements on the sustainability of the plan.

Statistics Canada will publish readings on GDP growth and employment at 1330GMT. According to the forecasts, the Canadian economy will likely expand by 0.1% m/m in September after a contraction by an equivalent proportion in August. On a quarterly basis, the annualized GDP growth is projected to narrow from 4.5% to 1.6% in the third quarter. That would be the weakest growth posted since the second quarter of 2016.

In another report, Canadian unemployment is said to inch down by 0.1 percentage points to fall back to nine-year lows of 6.2% in November, while the economy is expected to add 10,000 workers in the labor market in November compared to 35,300 in September.

Back in the US, the Institute of Supply Management (ISM) predicts the manufacturing PMI to drop by 0.3 points to 58.4.

In terms of public appearances, the St. Louis Fed President James Bullard will be giving a presentation on the US economy and monetary policy at 1405 GMT and Dallas Fed President Robert Kaplan (an FOMC voting member) will be participating in a Q&A session at 1430 GMT. Philadelphia Fed President Patrick Harker (also an FOMC voting member) will be talking about inclusive economic growth at 1515 GMT.

Brexit news could also shake the pound as Theresa May's deadline on December 4 to propose solutions to three key elements – those being the UK's financial settlement to the EU, the Irish border and the rights of the European citizens – runs out. Note that May will meet the President of the European Commission, Jean-Claude Junker in Brussels on Monday to prepare a breeding ground for the EU summit on December 14.

CAD Data & Senate Vote Next

Four days of gains leaves USD/CAD a handful of pips away from the July highs in a potential breakout with major economic data to come. Sterling was the top performer once again while the New Zealand dollar lagged. Crucial CAD figures are due at 8:30 ET, 13:30 London -- Canada Nov jobs report and Canada's Sep GDP figures. US manuf ISM folows 90 mins later. The Premium FTSE100 short was closed at 7290 for 210 pts.

USD/CAD touched 1.2909 on Thursday, just below the October high of 1.2917. That will be a critical level to watch in the day ahead with Canada releasing the first look at Q3 GDP and November employment. A slight bit of good news for the GDP report on Thursday as the current account deficit for Q3 was about $0.65B below the $20B expected, despite being the third-worst report on record, in large part due to a CAD-driven drop in exports in Q3. The imbalance represented 36 straight quarters of current account deficits in a reminder of the long-term headwinds for Canada and the loonie.

In the US, the Senate hopes to pass the tax bill today as Republicans find difficulty in keeping the number of their Naysayers at no more than 2. The Fed's Mester and Kaplan both said they don't expect it to add to growth but offshore flows returning home could be USD-positive.

The dollar was volatile on the day, dropping early and then storming back as the 10-year Treasury yield climbed above 2.40%. The PCE report was a touch high on overall inflation but in-line on core. Personal income improved more than expected but spending was light.

In other news, OPEC extended production curbs through 2018. The nine-month extension was generally expected. Libya and Nigeria also agreed to cap production at 2017 maximums. The crude market was choppy on the headlines but finished flat on the day.

USDCHF – Backs Off Higher Prices, Weakens

USDCHF - The pair backed off higher prices on Thursday leaving risk to the downside. On the downside, support lies at the 0.9800 level. A turn below here will open the door for more weakness towards the 0.9750 level and then the 0.9700 level. On the upside, resistance resides at the 0.9850 level where a break will clear the way for more strength to occur towards the 0.9900 level. Further out, resistance comes in at the 0.9950 level. Above here if seen will turn attention to 1.0000. All in all, USDCHF faces further upside pressure.

Canadian Dollar Ticks Higher, Canadian GDP, Employment Change Next

The Canadian dollar's slide has paused on Friday, after four straight losing sessions. Currently, USD/CAD is trading at 1.2882, down 0.12% on the day. The Canadian dollar has suffered a rough week, declining 1.3 percent. On the release front, it's a busy day in Canada, with three key releases. GDP, which is released monthly, is expected to post a small gain of 0.1%. Employment Change is forecast to slow to 10.2 thousand, and the unemployment rate is expected to edge lower to 6.2%. Traders should be prepared for some movement from USD/CAD during the North American session.

Canada's economy has slowed down, as GDP numbers have softened in the second half of 2017. In July, GDP came in at a flat 0.0%, and this was followed by a decline of 0.1%, in August, the first contraction since October 2016. Another weak reading for GDP on Friday could make investors frown and hurt the shaky Canadian dollar. On Thursday, USD/CAD climbed to a high of 1.2909, breaking above the 1.29 line for the first time since October 31. Weaker economic activity has given the Bank of Canada some breathing room, and the BoC is not expected to raise interest rates before April 2018. As well, uncertainty over NAFTA, which the US has threatened to torpedo, is weighing against another rate hike.

All eyes are on Washington, as the Senate is set to vote on its version of tax reform. A vote was expected on Thursday night, but this has been delayed until Friday. Republican lawmakers are confident that they have the necessary votes to pass the bill, but with the vote expected along party lines, the results will be close. If the Senate does pass the bill, the stock markets and US dollar will likely respond with gains. The next step in the tax reform saga would be for the House and Senate to bridge the differences between the two bills and come up with a single version, which would have to be voted on by both the House and the Senate.

DAX Slides As US Tax Reform Vote Delayed

The DAX index is down sharply in the Friday session. Currently, the DAX is at 12,859.75, down 1.26% on the day. On the release front, the focus is on manufacturing data. Eurozone Final Manufacturing PMI improved to 60.1, above the estimate of 60.0. German Final Manufacturing PMI climbed to 62.5, matching the forecast. Still, the strong readings failed to stem sharp losses on Friday, as investors remained concerned about a delay in the vote over the US tax reform bill.

The week ended on a positive note for eurozone and German indicators, as manufacturing PMIs improved in October. Eurozone Final Manufacturing PMI climbed to 60.1, and the German indicator improved to 62.5 points. The German reading marked the highest since February 2011, while the eurozone release was the strongest since April 2000. The sparkling numbers underscore stronger global demand for European products, which have boosted the manufacturing and export sectors.

German retail sales continue to struggle, as the key indicator posted a sharp decline of 1.2% in October. This marked the third decline in four months. Germany’s economy is solid and the labor market is strong, so why isn’t the German consumer spending? Strong economic conditions have not translated into higher wages for a large segment of the labor force, and low unemployment numbers have masked the problem of underemployment, ,which of course means lower wages for workers who can’t find full-time work. The lack of inflation in Germany is apparent in the eurozone as well, as inflation levels remain below the ECB’s inflation target of around 2 percent.

All eyes are on Washington, as the Senate is set to vote on its version of tax reform. A vote was expected on Thursday night, but this has been delayed until Friday. Republican lawmakers are confident that they have the necessary votes to pass the bill, but with the vote expected along party lines, the results will be close. Investors are closely following the proceedings, and the delay in the vote has sent global stock markets lower on Friday. If the Senate does pass the bill, the stock markets and US dollar will likely respond with gains. The next step in the tax reform saga would be for the House and Senate to bridge the differences between the two bills and come up with a single version, with the goal to present a new tax bill for President Trump’s signature before Christmas.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

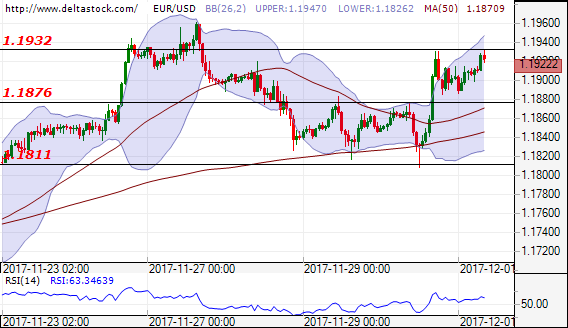

EUR/USD

Current level - 1.1922

The outlook is positive for breakthrough the level at 1.1932 for test at 1.1960 and uptrend up to 1.2050. In negative direction the support levels are at 1.1876 and after that at 1.1811.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1932 | 1.1940 | 1.1880 | 1.1690 |

| 1.1960 | 1.2090 | 1.1811 | 1.1550 |

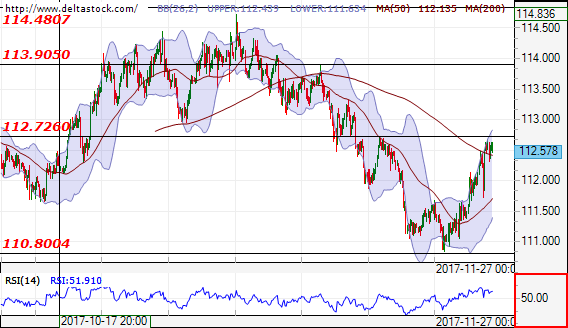

USD/JPY

Current level - 112.57

The movement of the currency pair is right before a test at the level 112.72. Successful breakthrough at this level will lead to movement up to 113.90. In negative direction the support level will be at 110.80.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.72 | 113.90 | 112.00 | 109.50 |

| 113.40 | 114.70 | 109.50 | 107.30 |

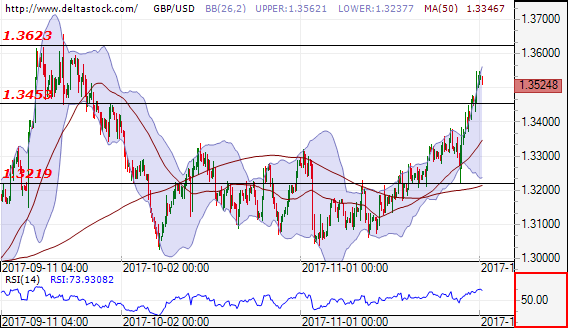

GBP/USD

Current level - 1.3524

After the yesterday breakthrough of the resistance level at 1.3450, the forecast is positive for test at 1.3620. In negative direction for support level we could take the level at 1.3219.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3623 | 1.3460 | 1.3280 | 1.3220 |

| 1.3700 | 1.3660 | 1.3219 | 1.3020 |

Technical Outlook: EURGBP – Bears Are Taking A Breather Before Final Break Below 200SMA

The cross found footstep after steep four-day fall from 0.8981 week's high, with bears being so far contained by 200SMA (0.8795) despite brief probes below. Strength and pace of recent fall suggests corrective action as likely near-term scenario. Recovery attempts were so far capped at 0.8840 (broken Fibo 61.8% of 0.8732/0.9013 rise) with strong barrier at 0.8870 (converged 10/20/55SMA's in attempt to create double bear-cross) expected to cap corrective action. Widening daily cloud maintains downside pressure (cloud base lies at 0.8906) for final break through 200SMA and extension towards key support at 0.8732 (01 Nov multi-month low).

Res: 0.8840, 0.8870, 0.8884, 0.8906

Sup: 0.8795, 0.8776, 0.8745, 0.8732