Sample Category Title

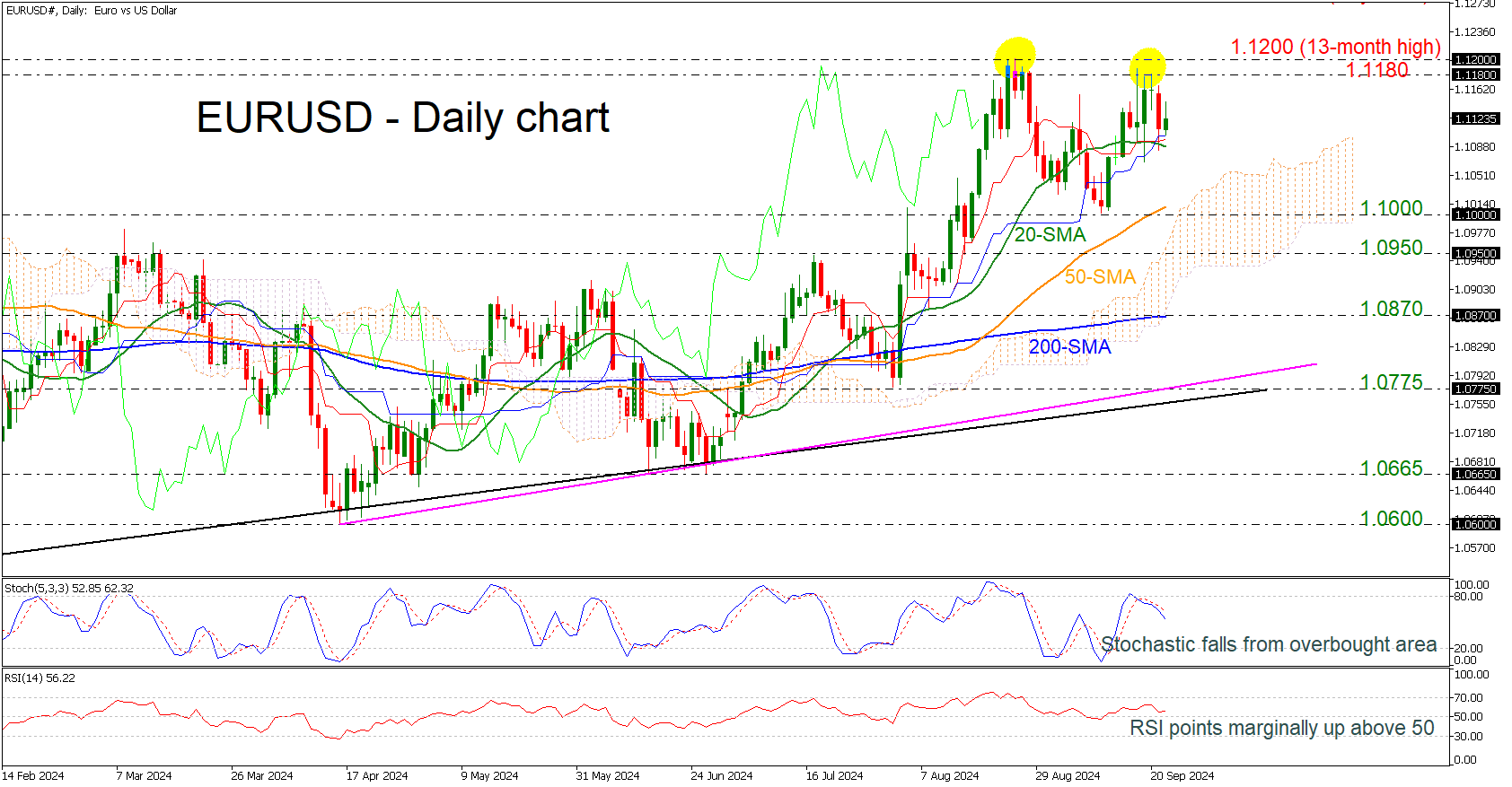

EURUSD Retests 1.1200 Critical Level

- Will EURUSD break the double bottom to the upside?

- Strong support at 1.1100

- Stochastic and RSI look quite positive

EURUSD is continuing the upside rally near the 13-month high of 1.1200, remaining well above the 20-day simple moving average (SMA). A successful break to the upside of the double top pattern could confirm the upside tendency.

Technically, the stochastic oscillator posted a bullish crossover within its %K and %D lines slightly beneath the 80 line, while the RSI is moving horizontally despite that is still standing above the neutral threshold of 50.

If the market manages to pick up speed the July 2023 peak of 1.1275 could offer nearby resistance ahead of the 1.1390 barrier, taken from the high in February 2022.

Should prices decline, immediate support could be found from the 20-day SMA at 1.1100 before tumbling to the 50-day SMA at 1.1017. Slightly lower, the 1.1000 round number, which holds within the Ichimoku cloud may halt bearish actions.

In a nutshell, EURUSD has been in a neutral phase over the last five weeks and needs a boost above 1.1200 to confirm the positive momentum.

China-Sparked Asian Bull Run Continues This Morning

Markets

China’s stimulus announcement impacted all corners of the market. Hopes for a revival of the 2nd largest economy lifted commodity prices. Oil & iron prices both added around 2%. Equities rose with Europe’s EuroStoxx50 adding 1.1%. Wall Street had to digest an unexpected and sharp drop in the Richmond manufacturing index & US consumer confidence first before ending up with new record highs in both the DJI and S&P500. The Conference Board indicator dropped from 105.6 to 98.7, nearing the 2024 lows again. The current assessment deteriorated significantly, tanking 10 points to the weakest level since 2021. The expectations component eased to 81.7, from 86.3. The data releases called off the intraday rise of US yields. Gains of as much as 6 bps (10-yr) made way for net daily losses varying between -0.8 (30-yr) and -4.9 (2-yr) bps with a successful $69bn 2-yr bond auction additionally weighing on front-end yields. European rates fell in a similar curve shift. Both the swap and German 2-yr rate dropped to new YtD lows. Currency markets moves were guided by risk-on as well. JPY and USD lagged G10 peers. The trade-weighted dollar index finished below the previous YtD closing levels (100.46). EUR/USD shrugged off Monday PMI losses and closed at the highest level since end-August (1.118). AUD, NZD, SEK and NOK all printed decent gains. Sterling caught a breather against the euro after a stellar run on Monday but extended gains against the USD (GBP/USD +1.34).

The China-sparked Asian bull run continues this morning with the CSI300 adding another 2%. The PBOC lowered the rate of its 1-yr lending facility by the most since 2016 (-30 bps to 2%), kickstarting the implementation of the measures announced on Tuesday. China’s yuan gapped higher to USD/CNY 7.016. We doubt whether it’ll suffice for European and US markets this time around though. The empty eco calendar won’t interrupt today’s technically inspired trading session. We’re eyeballing the front end of the yield curve in particular. Money markets ramp up easing bets, especially for the ECB. While we don’t agree with growing market conviction of an October cut (+60%), it’ll be difficult to turn the tide for now without influential policymakers such as Lagarde weighing in on the debate. EUR/USD is close to the 1.1202 resistance. A break higher probably requires additional USD weakness and would pave the way for a return to the 2023 high of 1.1276.

News & Views

In its updated 2024 World Oil Outlook through 2050, OPEC sees an ongoing need for more energy as economies grow, populations expand and urbanization levels increase. OPEC states that ‘Global energy demand in this year’s WOO is set to expand by 24% in the period to 2050, driven by significant expansion in the non-OECD region. The Outlook sees the need for an expansion in all energy sources, with the exception of coal. For oil alone, we see demand reaching over 120 million barrels a day by 2050, with the potential for it to be higher. There is no peak oil demand on the horizon’. OPEC holds a different view compared to many other forecasters like the IEA which see oil demand peaking much earlier. OPEC expects oil and gas to still make up for over 50% of the energy mix in 2025. To meet demand OPEC raised the number of needed investments to $17.4 bn by 2050.

The National bank of Hungary after a pause last month cut its policy rate again by 25 bps to 6.5%. Inflation in August (3.4%) declined back in the MNB tolerance band of 3% +/- 1%, even as this was mainly due to lower fuel prices and base effects. Disinflation in market services was rather slow. MNB expects inflation to fall further in September, but to rise again to 4.0% by the end of the year. Core inflation might return to 5% end 2024. Disinflation should nonetheless continue in Q1 2025. MNB sees inflation averaging between 3.5% and 3.9% this year, 2.7%-3.5% in 2025 and 2.5%-3.5% in 2026. Growth for this and next year was downwardly revised (1.0%-1.8% & 2.7%-3.7%). 2026 was upwardly revised to 3.5%-4.5%. Vice governor Virag said the MNB will consider small cuts as well as the option to hold at each of the remaining monthly meetings this year, which can be seen as a slightly more dovish stance compared to last month (one or two rate cuts this year). The Hungarian 2-y swap yield declined 4.5 bps to 5.52%. The forint whipsawed at the time of the press conference, but in the end closed marginally stronger near EUR/HFU 394.3.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) make follow-up moves less evident. We expect the central bank to stick with the quarterly reduction pace. Disappointing US and unconvincing-to-outright-weak EMU activity data dragged the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed kicked off its easing cycle with a 50 bps move. It is headed towards a neutral stance now that inflation and employment risks are in balance. Conservative SEP unemployment forecasts risk being caught up by reality and with it the dot plot (50 bps more cuts in 2024). We hold our call for two more 50 bps cuts this year. Pressure on the front of the curve and weakening eco data keeps the long end in the defensive for now as well.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large rate cuts trumped traditional safe haven flows into USD. An ailing euro(pean economy) only briefly offset some of the general USD weakness. EUR/USD’s dollar-driven ascent is nearing resistance around 1.12 again.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. But the economic picture is increasingly diverging to the benefit of sterling. EUR/GBP succumbed to horrible European September PMI’s. Support at 0.84 broke and brings the 2022 low (0.8203) on the radar.

Riksbank to Deliver 25bp Cut Today

In focus today

The most important event today will be the Riksbank's rate decision at 9.30 CET. On the back of a slightly weaker economy and lower inflation than expected, we expect Riksbank to cut the repo rate by 25bp and reduce the repo rate path by some 40bp compared to the June forecast. Such a downward correction, however, is not sufficient to match market pricing of 99bp for the coming three meetings including today's decision. Market pricing for today is 32bp or a 28% chance of a 50bp cut.

Economic and market news

In China, the PBOC followed Tuesday's stimulus package with a 30bp cut to the medium-term lending facility rate, as expected. The move supported the momentum in Asian equities with the Hang Seng index up 1.9% this morning following yesterday's 4.1% gain.

In the US, rates slid after a weak conference board sentiment print where labour market metrics suggested a continued softening. In response, markets slightly raised the implied probability of a 50bp cut in November, which as of this morning sits at 60%.

Oil found support from both supply- and demand-side factors, as continued tensions in the Middle East sowed fears of supply disruptions, while a monetary stimulus package by the PBOC raised prospects for demand. Brent almost reached 76 USD/bbl. but ended at about 74.96 which was still in the positive.

The RBA left rates unchanged as expected by markets and us. The forward guidance remains hawkish compared to the Fed and most other G10 central banks as it still sees underlying inflation stabilizing close to target only in late 2025. AUDUSD shifted higher after the announcement and was also supported by the Chinese stimulus package announced, the cross ended the day up some 0.5%.

Equities: Global equities were higher yesterday, led by China following a broad spree of monetary and fiscal stimulus. That said, all regions posted gains yesterday, with the S&P 500 marking its 41st all-time high this year. Looking at sector performance, we also see the effects of the Chinese stimulus, as materials was the best performing sector (though the worst performing YTD). It can be challenging to separate hot and cold water, but macro data was not the driver yesterday. In our opinion, the macro data suggested a very different outcome from what we observed in the equity markets yesterday. In the US yesterday, the indices showed modest gains: Dow +0.2%, S&P 500 +0.3%, Nasdaq +0.6%, and Russell 2000 +0.2%. China is continuing its stimulus efforts this morning, which has led to a sharp rise in Chinese stocks again today. The rest of Asia is more mixed, while European and US futures are lower this morning.

FI: 10Y Treasuries seem to be stabilising after having risen some 13bp since Monday last week. We have a string of US data this week, where the US inflation data (US PCE price index) published on Friday is the main event. If the data is weaker than expected the market will focus on the possibility of a 50bp rate cut at the next FOMC meeting.

FX: While EUR/SEK has kept within a tight range through September, yesterday saw a tentative break below the lower end of the 11.30-11.40 interval and starts Wednesday at 11.2950. Focus on the Riksbank decision at 09:30 CET where we and consensus expect 25bp. EUR/NOK downside rejected at 11.60, trades at 11.6450. EUR/DKK fell to 7.4570, its lowest point since March. EUR/USD erased losses that followed weak European PMIs earlier this week and gained further after soft US consumer confidence. This morning the cross tests August highs at 1.12. Weak dollar pulled USD/JPY lower to trade around 143.30. Yesterday we booked profit on our long GBP/CHF.

Equities Extend Rally on China Stimulus, Fed Cut Bets

Let’s continue to count. 41. The S&P500 celebrated its 41st record high yesterday. Even though yesterday’s session began on a softish note – after the data showed the biggest drop in the US consumer sentiment since August 2021, another one revealing that Jensen Huang is done selling his Nvidia shares outshined the doom and gloom of the consumer sentiment and sent Nvidia 4% higher and the S&P500 to 5735. Nasdaq 100 added on to its gains, the Dow Jones traded at an ATH even though Visa tumbled 5.5% after being sued by the DoJ for illegally monopolizing the debit card market. Small caps eked out small gains. In summary, investors sentiment is far better than your average consumer’s, and the fact that consumer sentiment is weak contributes to inflating the dovish Federal Reserve (Fed) expectations. Swap markets now price in more than 75bp cut from the Fed for the remainder of this year and activity on Fed funds futures assesses more probability to another 50bp cut in November (58%) than a 25bp cut.

More China boost

The People’s Bank of China (PBoC) cut its repo, RRR and existing mortgage rates earlier this week, and announced a 30bp cut to their MLF rate today. The latter further fueled the Chinese equity rally. The CSI 300 which rallied more than 4% yesterday, added another 2% this morning. The Hang Seng index recorded about the same rally and is now testing the May highs. And wait, Nasdaq’s Golden Dragon China index jumped 9% yesterday in the US. Alibaba advanced nearly 8% while PDD jumped 11% on hope that the latest stimulus measures will bring investors back to China. The problem is, the stimulus measures will take time to show in the economic data. And more worryingly, they won’t do much to fix the country’s deepest issues – they won’t reverse local governments’ heavy debt burden, China’s aging population, and will hardly boost the demand-led growth. As such long-term investors appreciate the efforts but prefer to watch from a distance for now.

This being said, the Chinese stimulus measures help improve mood among global mining companies. BHP for example jumped 3% yesterday and another 3% today in Australia, Rio Tinto and Glencore jumped 4% yesterday and will probably continue their journey to the north today. The commodity friendly Aussie remains bid – somehow retained by the fact that inflation in Australia hit a 3-year low. But the Aussie bulls now set their eyes on the 70 cents level against the US dollar as the next natural target, and the prospects for the FTSE 100 are improving.

Doom and gloom

The EURUSD is testing the 1.12 offers again this morning. But the US dollar’s weakness has more to do with the EURUSD’s gains than the European fundamentals themselves. Germany’s business outlook deteriorated further in September and reinforced fears of possible recession. That, combined to soft PMI figures released earlier this week boost the probability of another European Central Bank (ECB) cut in October. If there is no surprise in the upcoming inflation updates, there will be a strong case for a 25bp cut from the ECB next month. And the latter should limit the euro’s upside potential.

Elsewhere, the USD remains broadly under pressure, the dollar index continues to push toward this year’s lows as investors increase Fed cut bets. The price of an ounce runs from record to record, in the overbought territory, with the rising tensions between Israel and Lebanon giving an additional hand from those who fly to safety.

In this context, crude oil is also better bid. The rising geopolitical tensions and the Chinese stimulus measures strengthen the oil bulls hands, but the $72.85pb level is yet to be cleared to send the price of a barrel into the medium term bullish consolidation zone. Soft global demand prospects and amply supply keep the topside limited.

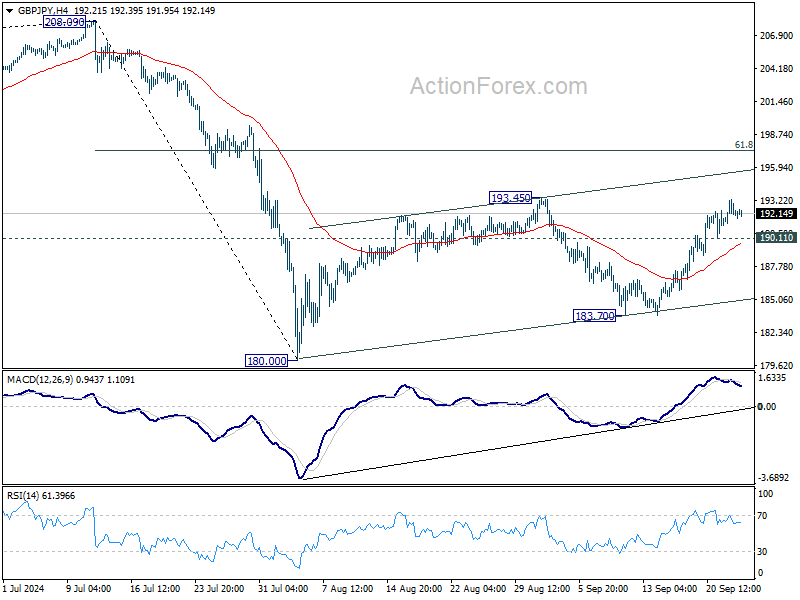

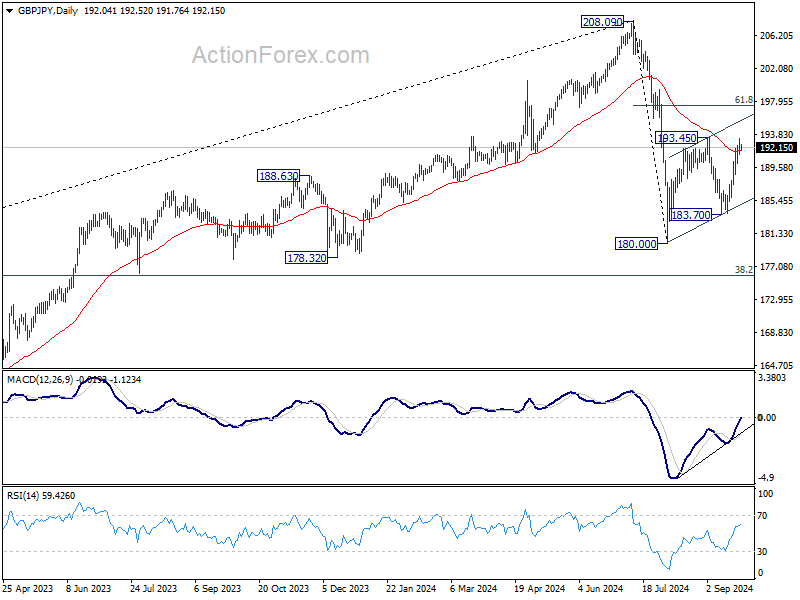

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.19; (P) 192.26; (R1) 193.17; More...

Intraday bias stays not the upside with 190.11 minor support intact. GBP/JPY's rise e from 183.70, as the third leg of the corrective pattern from 180.00, is in progress for 193.45 resistance. Firm break there will target 61.8% retracement of 208.09 to 180.00 at 197.35. On the downside, though, below 190.11 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

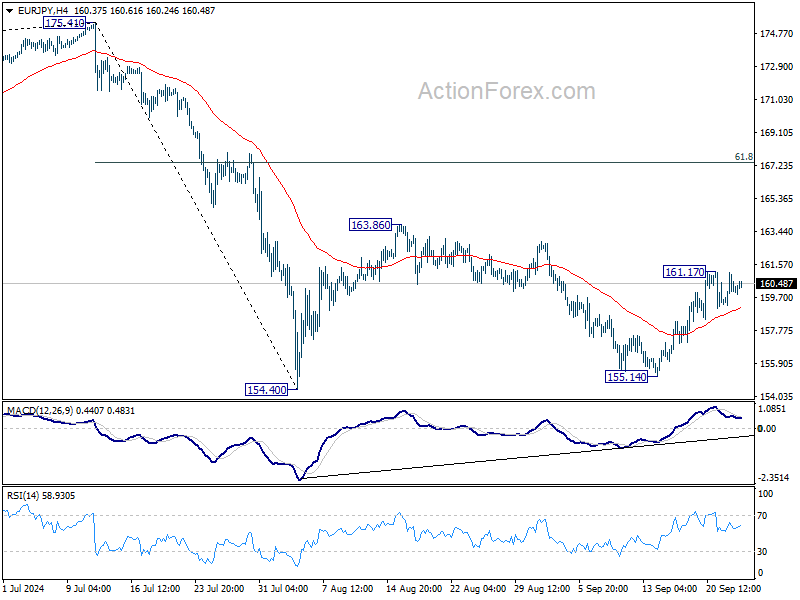

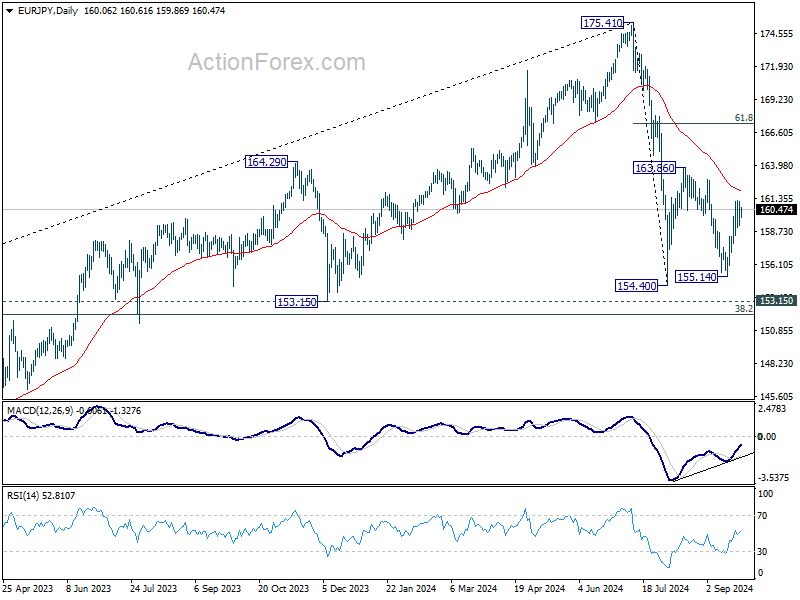

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.20; (P) 160.15; (R1) 161.07; More....

Intraday bias in EUR/JPY remains neutral and some consolidations could be seen below 161.17 temporary top. But further rally is expected as long as 155.14 support holds. Above 161.17 will resume the rise from 155.14, as the third leg of the corrective pattern from 154.40, to 163.86 resistance. Break there will target 61.8% retracement of 175.41 to 154.40 at 167.38.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

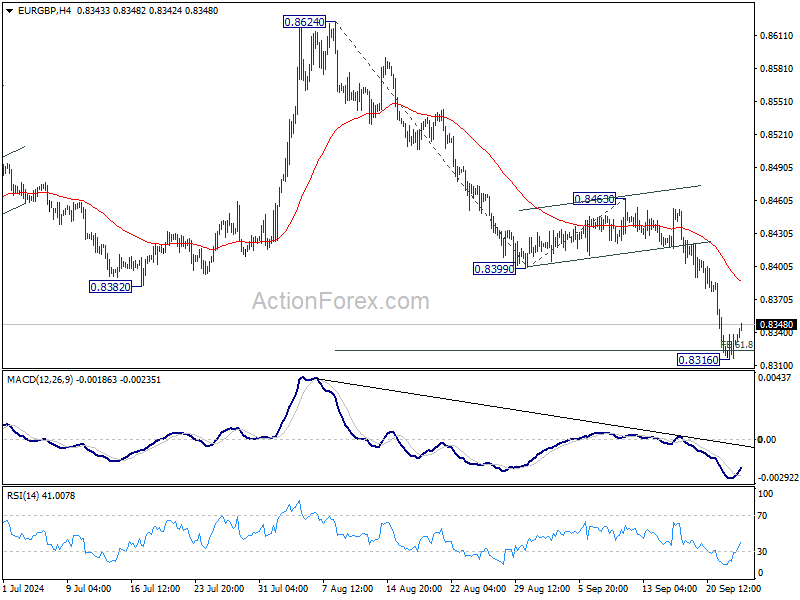

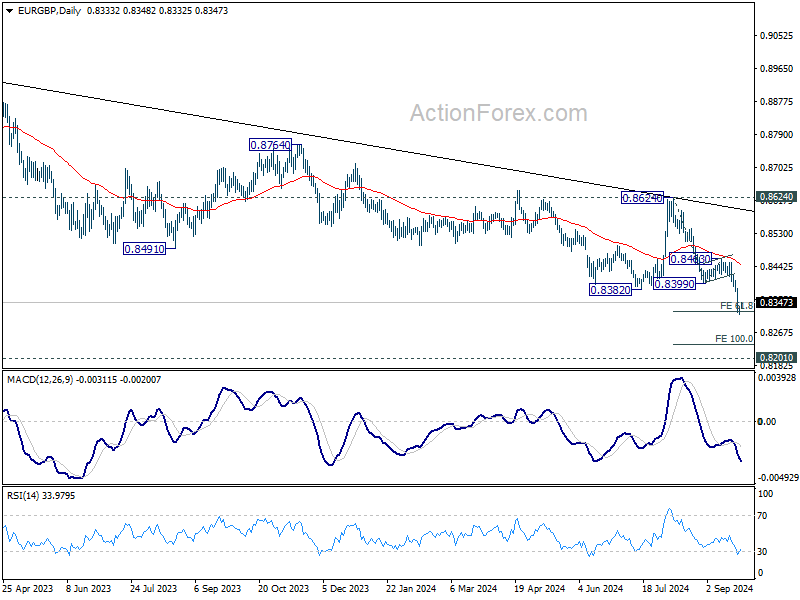

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8302; (P) 0.8345; (R1) 0.8366; More...

Intraday bias in EUR/GBP is turned neutral as it recovered after hitting 61.8% projection of 0.8624 to 0.8399 from 0.8463 at 0.8324. Some consolidations would be seen first, but outlook will remain bearish as long as 0.8399 support turned resistance holds. On the downside, below 0.8316 and sustained trading below 0.8324 will pave the way to 100% projection at 0.8237 next.

In the bigger picture, down trend from 0.9267 (2022 high) is resuming. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. Outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound.

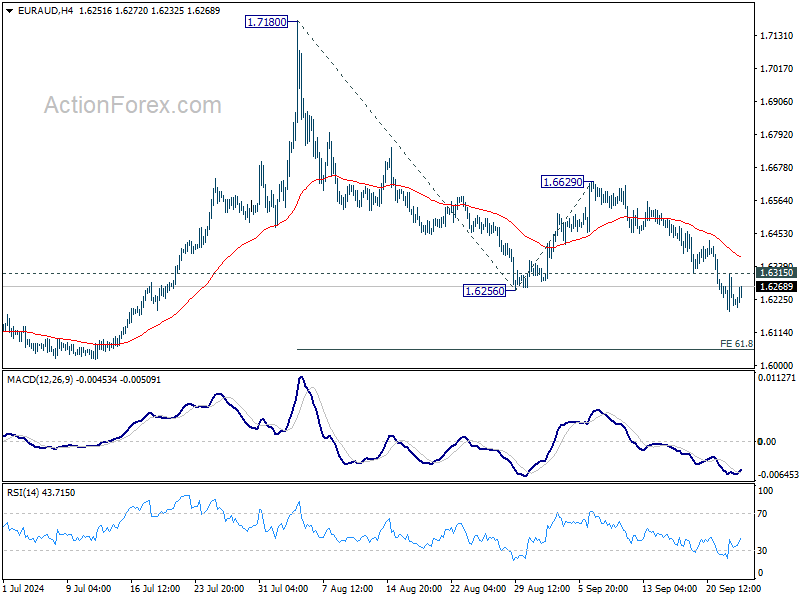

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6167; (P) 1.6241; (R1) 1.6295; More...

Intraday bias in EUR/AUD stays mildly on the downside with 1.6315 minor resistance intact. Current fall is part of the whole decline from 1.7180 and should target 61.8% projection of 1.7180 to 1.6256 from 1.6629 at 1.6058, which is close to 1.5996 key support level. On the upside, above 1.6315 minor resistance will turn intraday bias neutral first. But outlook will remains bearish as long as 1.6629 resistance holds.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still in favor to resume at a later stage. Firm break of 1.7180 will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715.

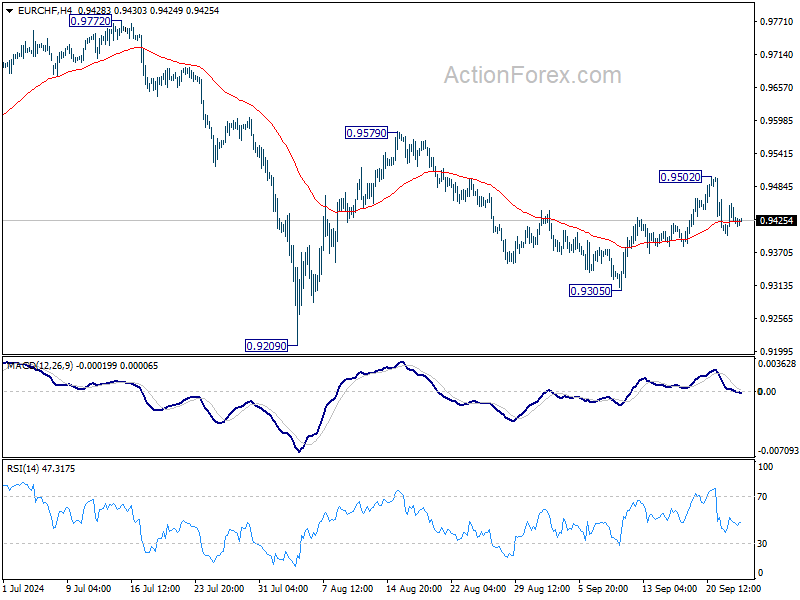

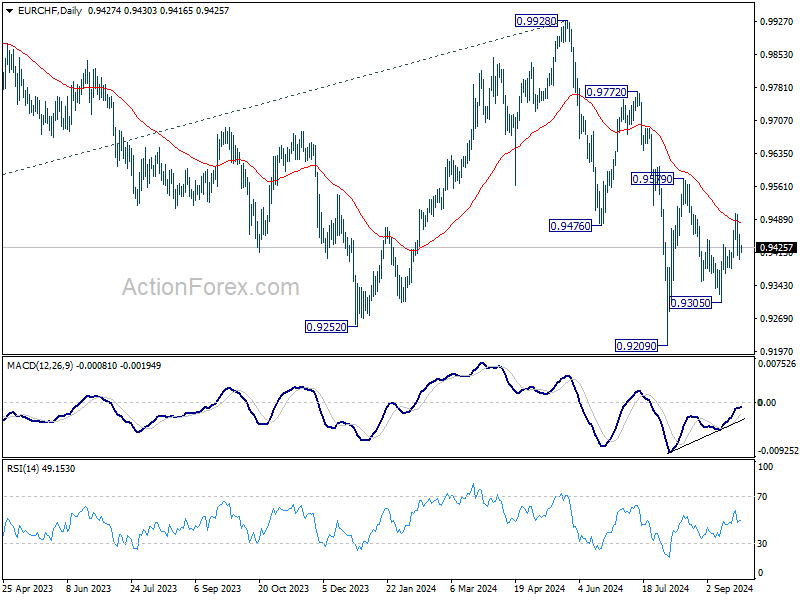

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9401; (P) 0.9429; (R1) 0.9456; More....

Intraday bias in EUR/CHF remains neutral for the moment, and another rally is still in favor as long as 0.9305 support holds. On the upside, above 0.9502 will resume the rally from 0.9305, as the third leg of the pattern from 0.9209, to 0.9579 resistance. However, break of 0.9305 will resume the decline from 0.9579 towards 0.9209 low.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

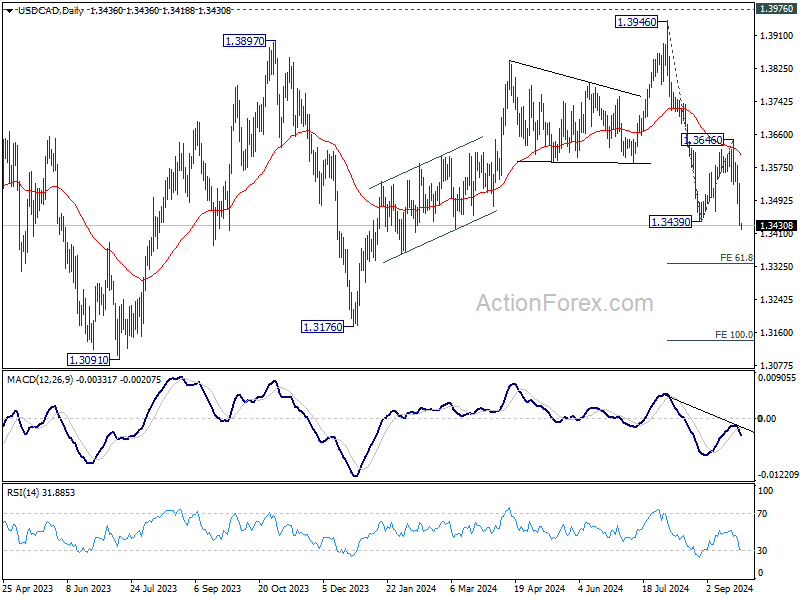

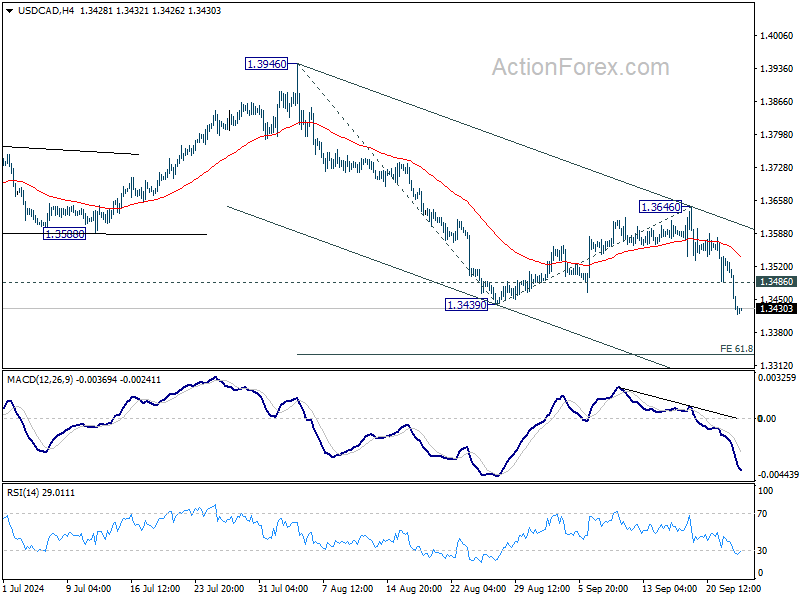

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3389; (P) 1.3473; (R1) 1.3515; More...

USD/CAD's break of 1.3439 support confirms resumption of whole fall from 1.3946. Intraday bias remains on the downside for 61.8% projection of 1.3946 to 1.3439 from 1.3646 at 1.3333. On the upside, above 1.3486 minor resistance will turn intraday bias neutral for consolidations. But outlook will remain bearish as long as 1.3646 resistance holds, in case of recovery.

In the bigger picture, corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.