Sample Category Title

Eurozone Sentix falls to -13.8, ECB under pressure to cut further and faster

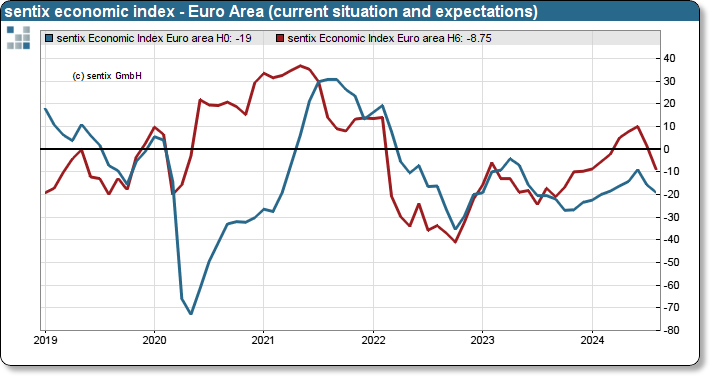

Eurozone Sentix Investor Confidence fell sharply from -7.3 to -13.8 in August, marking its lowest level since January. Current Situation Index dropped from -15.8 to -19.0, the lowest since February, while Expectations Index declined from 1.5 to -8.8, the lowest since last December.

Globally, Sentix Investor Confidence Index also tumbled, falling from 5.9 to -1.5, its lowest level since December. Current Situation Index decreased from 6.0 to -0.6, the lowest since January, and Expectations Index dropped from 5.7 to -2.4, the lowest since November.

Sentix commented on the data, stating that "Following the severe setback of the 'first mover' in the previous month, there is now another, more pronounced economic slump in August. The global recovery comes to a halt."

They added that the economic downturn in Eurozone should put ECB under pressure to "cut interest rates further and faster". Investors are now expecting ECB to address the economic weakness more aggressively, even though the Sentix Inflation Barometer is not indicating any sustained easing in the inflation environment.

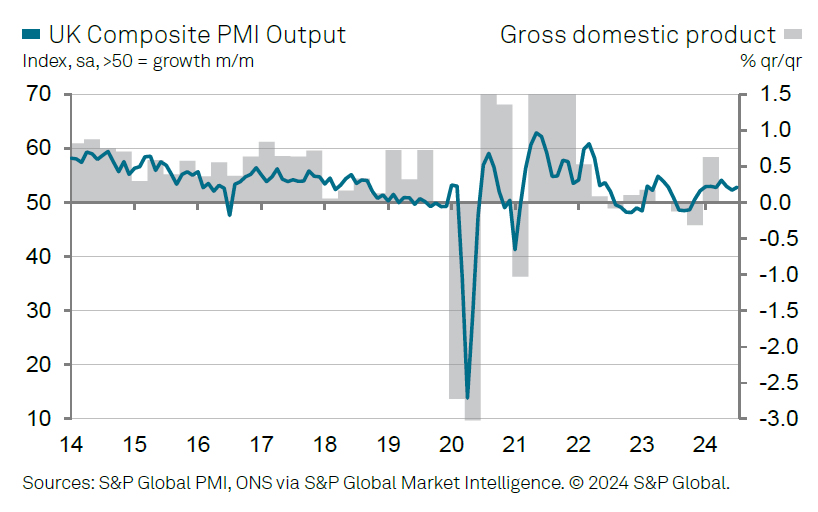

UK PMI services finalized at 52.5, composite at 52.8

UK PMI Services was finalized at 52.5 in July, up from June's 52.1. PMI Composite was finalized at 52.8, up from June's 52.3.

Joe Hayes, Principal Economist at S&P Global Market Intelligence, noted that the UK service sector saw a "modest rebound" following a subdued end to Q2. Business Activity Index saw a slight uptick, but New Business Index jumped by over three points to its highest level in 14 months, reflecting an influx of new clients and contracts. Hayes pointed out that the accelerated expansion in sales activity indicates improved business and consumer confidence, suggesting a positive outlook for GDP growth in Q3.

Hayes highlighted ongoing issues with "sluggish progress on inflation." While price pressures on input costs and output prices are at their lowest since early 2021, the respective PMIs remain above pre-pandemic levels. These benchmarks are critical for BoE to hit before it can declare success in combating inflation.

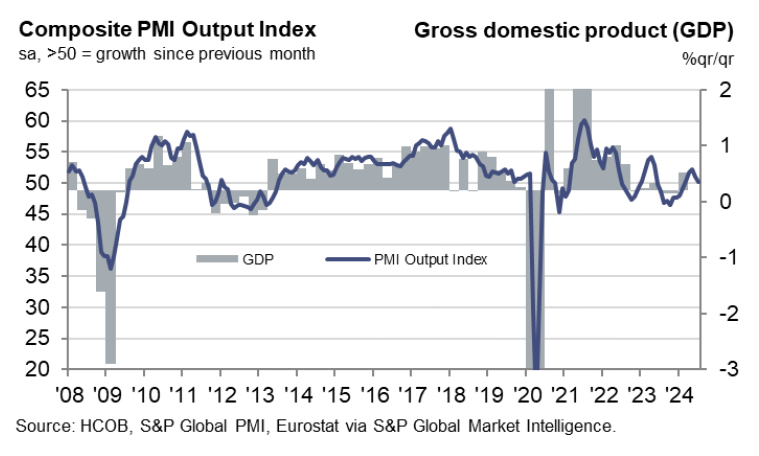

Eurozone PMI composite finalized at 50.2, growing at snail’s pace

Eurozone PMI Services was finalized at 51.9 in July, down from June's 52.8, a 4-month low. PMI Composite was finalized at 50.2, down from June's 50.9, a 5-month low. These figures indicate a slowing economy as the services sector loses momentum and the industrial sector continues its decline.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, stated, "The eurozone's economy is growing at a snail's pace." He noted that while the services sector isn't picking up speed as it did earlier in the year, the industrial slump persists. The HCOB Composite Output PMI barely stays above the expansion line, signaling a weak start to H2 despite surprisingly strong economic growth in the second quarter. De la Rubia added, "Given this situation, our 0.7% growth forecast for the year is still conservative."

Inflation remains a significant concern. Although sales prices are increasing at their slowest rate in 38 months and input costs are generally following suit, inflation is still high relative to the weak economy. Historically, when PMI activity index was at 52.0 or lower, selling prices typically stayed flat, and input prices rose much more slowly than they are now. De la Rubia attributes this to wage pressure caused by demographic shifts, which complicates ECB's efforts to achieve its 2% inflation target.

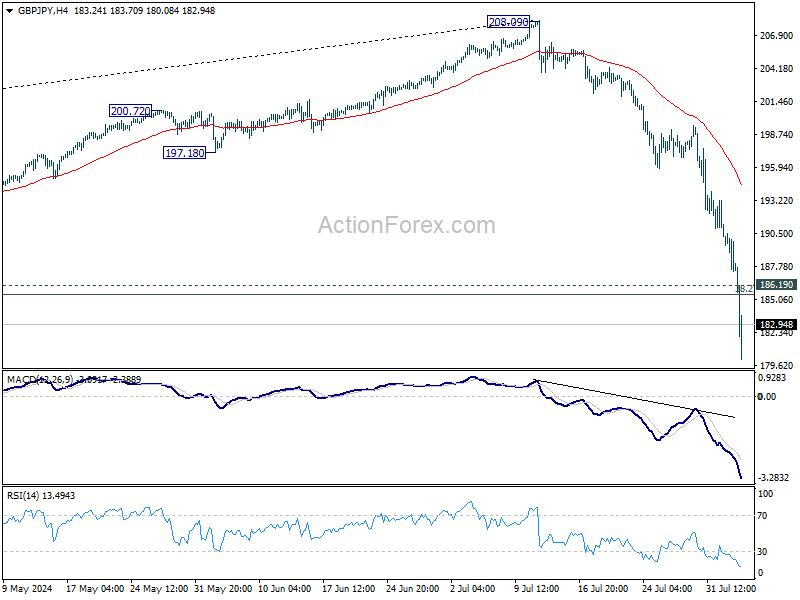

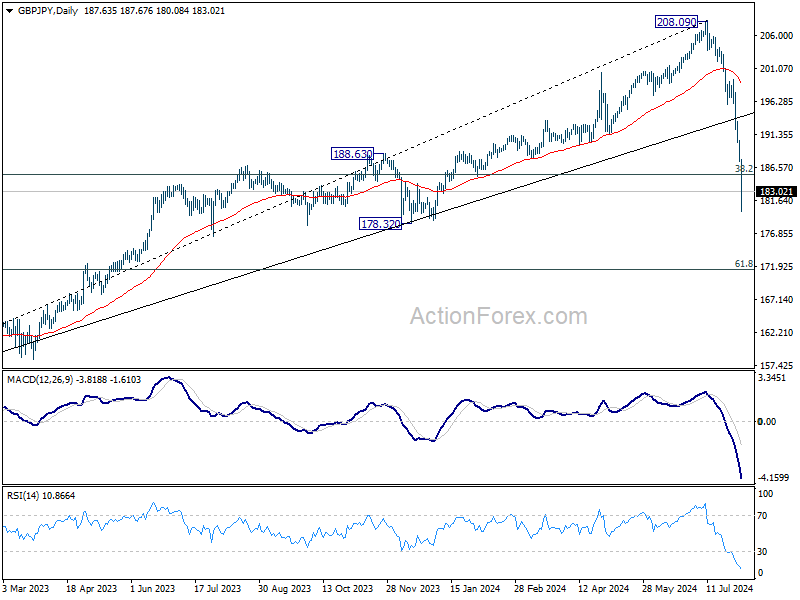

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.37; (P) 188.64; (R1) 189.89; More...

In the bigger picture, fall from 208.09 medium term top is seen as correcting the up trend from 148.93 (2022 low). 38.2% retracement of 148.93 to 208.09 at 185.49 is already met. Decisive break there will argue that even larger scale correction is already underway. For now, risk will stay on the downside as long as 55 W EMA (now at 189.31) holds. in case of rebound.

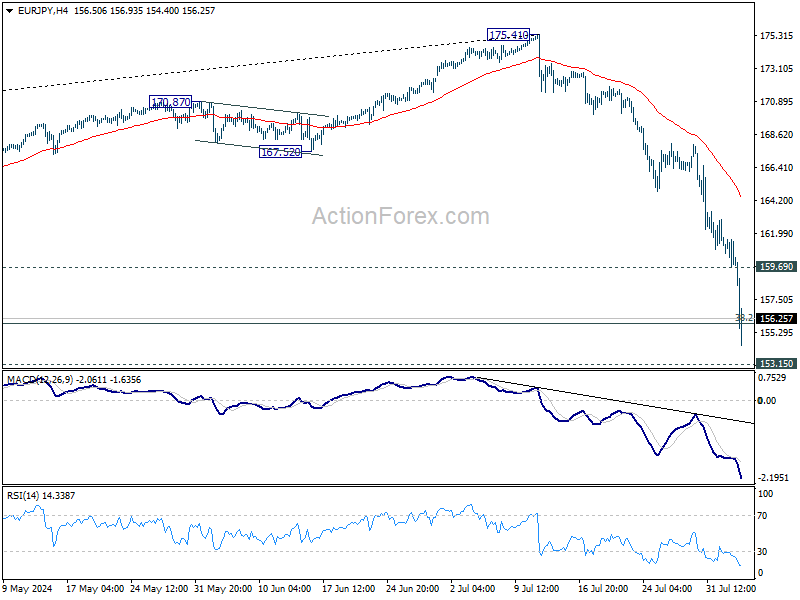

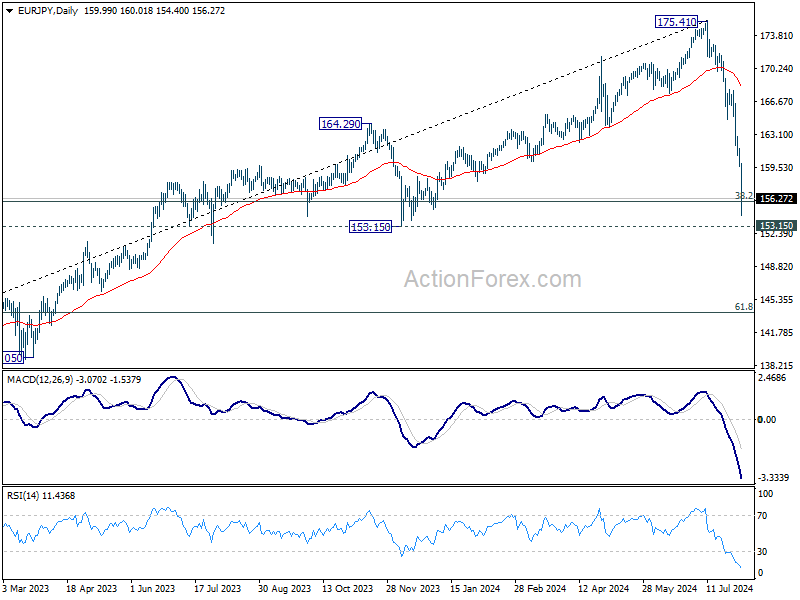

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.20; (P) 160.40; (R1) 161.09; More...

EUR/JPY's decline continues today and breached 155.91 fibonacci level. There is no sign of bottoming yet and intraday bias remains on the downside. Next target is 153.15 support. On the upside, above 159.69 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, fall from 175.41 medium term top is at least correcting the rise from 124.73, with risk of bearish trend reversal. 38.2% retracement of 124.37 to 175.41 at 155.91 is already met. Firm break of 153.15 will target 139.05/148.38 support zone. This will now remain the favored case as long as 55 W EMA (now at 161.79) holds, even in case of strong rebound.

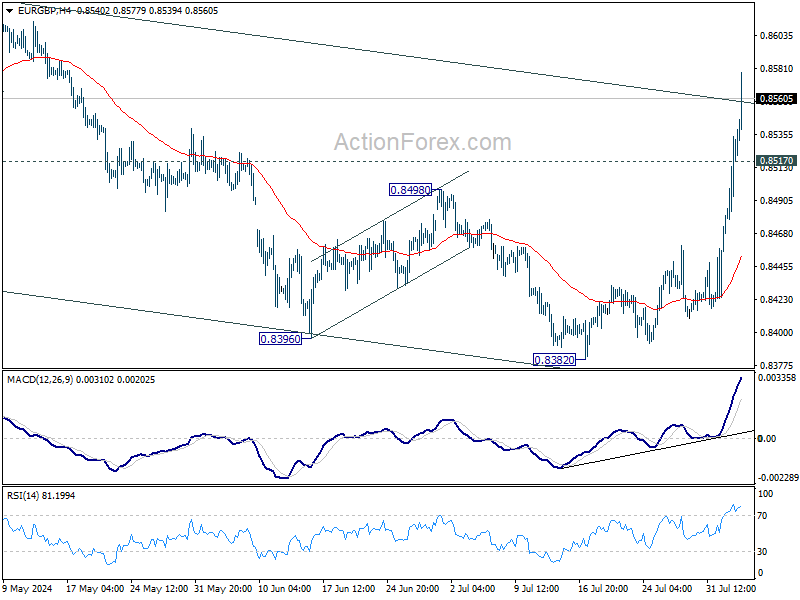

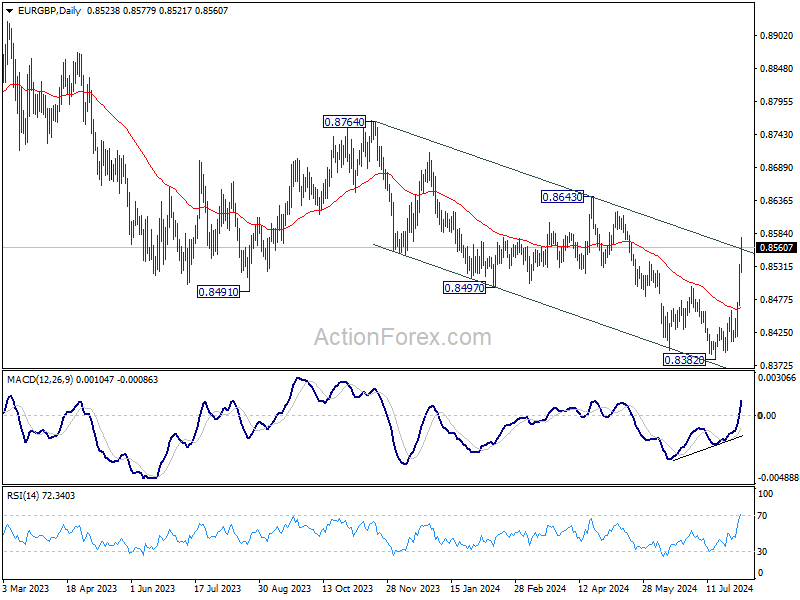

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8476; (P) 0.8505; (R1) 0.8551; More....

EUR/GBP's rally continues today and intraday bias stays on the upside. Sustained break of above falling channel resistance (now at 0.8555) will raise the chance of larger bullish trend reversal and target 0.8643 resistance next. On the downside, below 0.8517 minor support will turn intraday bias neutral first.

In the bigger picture, while the rebound from 0.8382 is strong, there is no confirmation of trend reversal yet. As long as 0.8643 resistance holds, down trend from 0.9267 could still resume through 0.8382 at a later stage. However, firm break of 0.8643 will indicate that such down trend has completed, and turn outlook bullish.

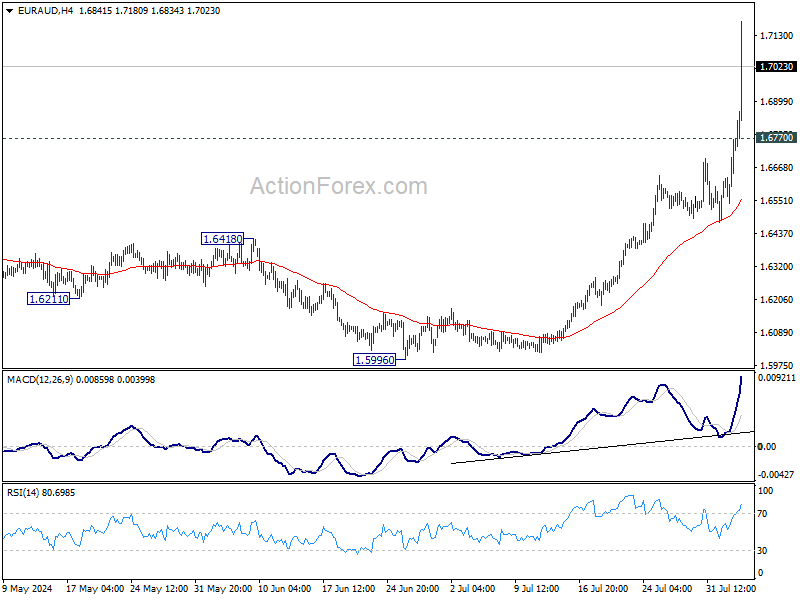

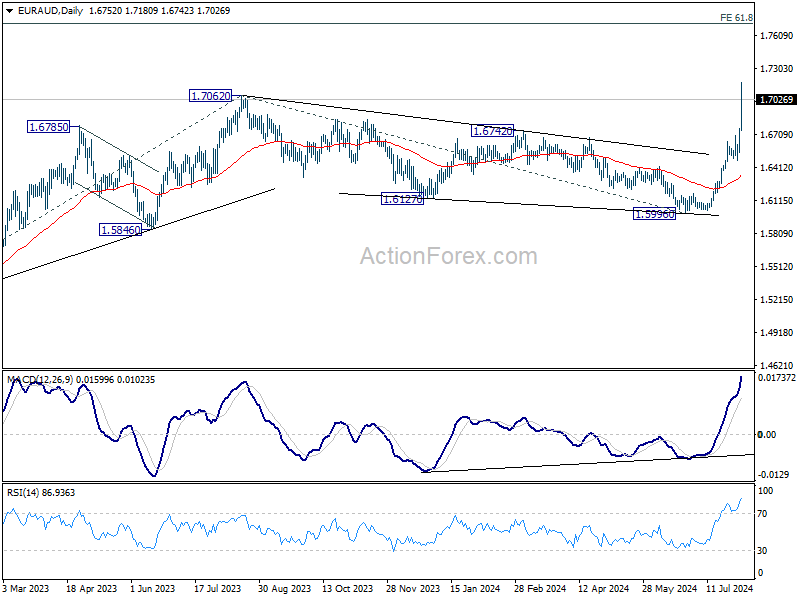

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6611; (P) 1.6690; (R1) 1.6836; More...

EUR/AUD surges to as high as 1.7189 so far today, and the breach of 1.7062 resistance suggests larger rally resumption. Intraday bias remains on the upside for 1.7715 fibonacci projection level next. On the downside, below 1.6770 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, decisive break of 1.7062 resistance will confirm resumption of whole up trend from 1. 1.4281 (2022 low). Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. For now, further rally is expected as long as 55 D EMA (now at 1.6344) support holds, even in case of deep retreat.

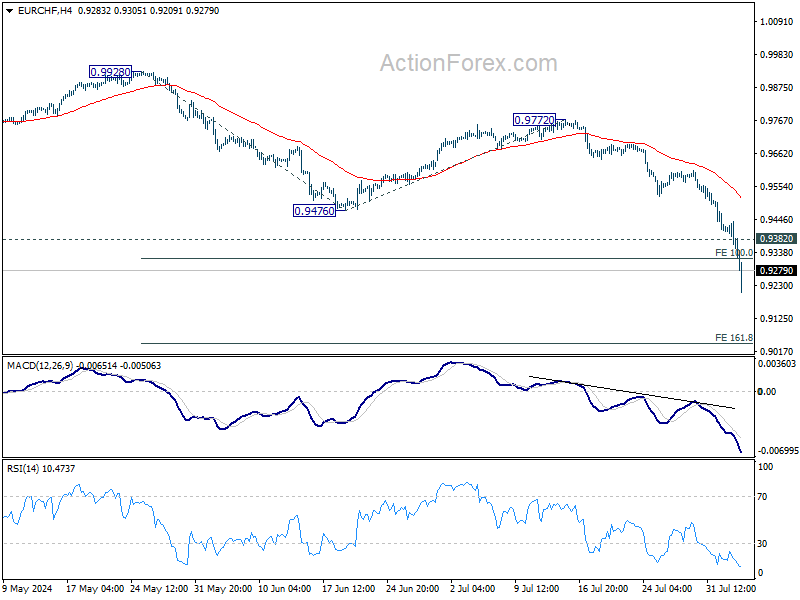

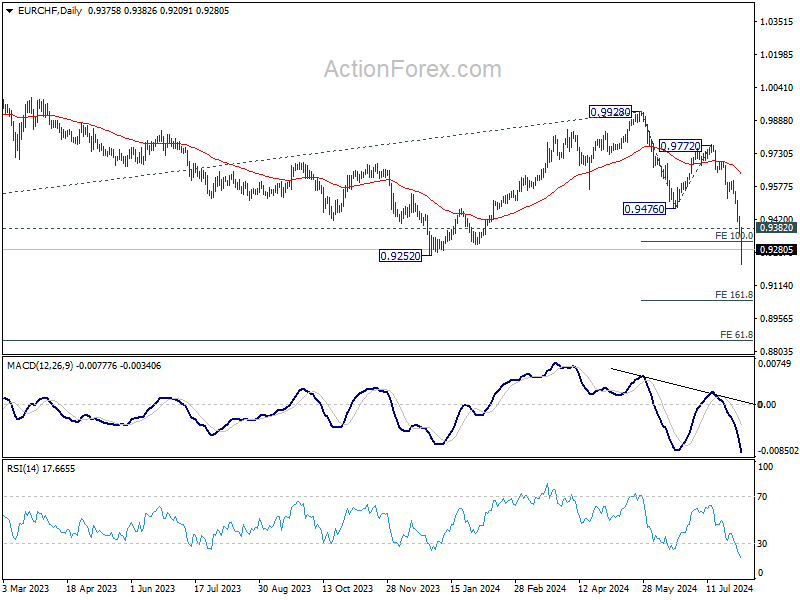

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9330; (P) 0.9385; (R1) 0.9415; More....

EUR/CHF dives through 100% projection of 0.9928 to 0.94767 from 0.9772 at 0.9320 today. Breach of 0.9252 low argues that larger down trend might be resuming. Intraday bias stays on the downside for 161.8% projection at 0.9041 next. On the upside, above 0.9382 minor resistance will turn intraday bias neutral first.

In the bigger picture, current downside acceleration argues that medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

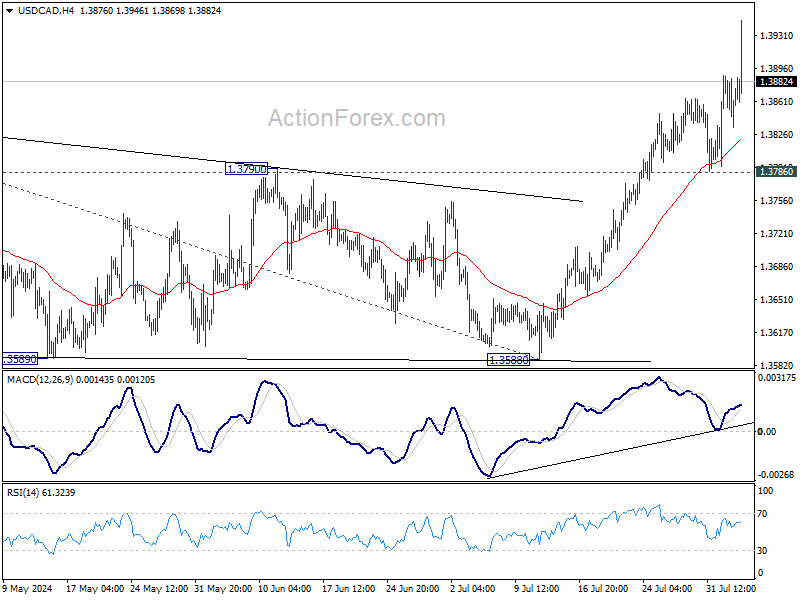

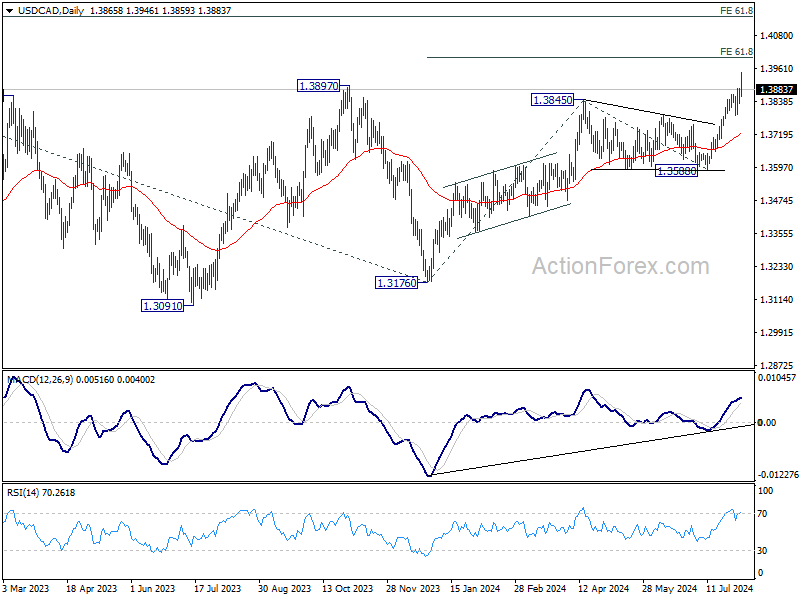

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3841; (P) 1.3866; (R1) 1.3899; More...

USD/CAD's rally continues today and intraday bias stays on the upside. Current rise from 1.3176 should target r 61.8% projection of 1.3176 to 1.3845 from 1.3588 at 1.4025 next. For now break of 1.3786 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

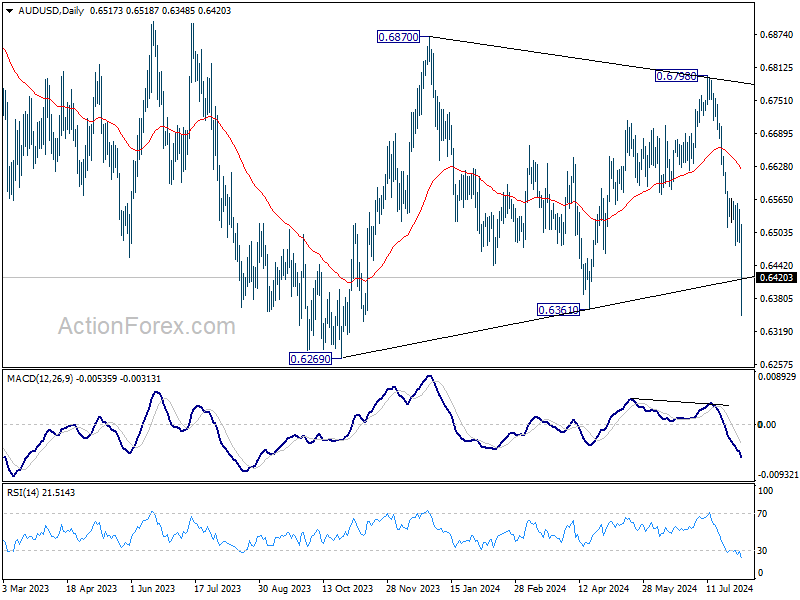

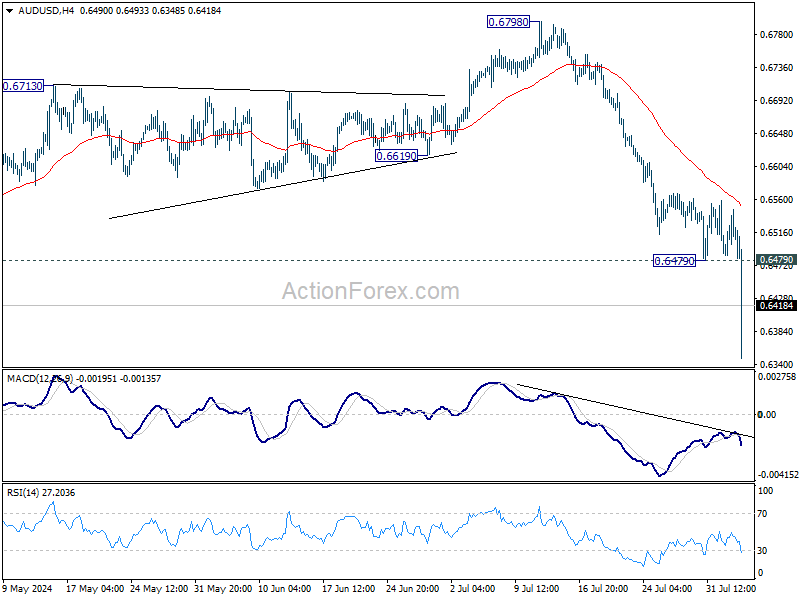

AUD/USD Daily Report

Daily Pivots: (S1) 0.6483; (P) 0.6515; (R1) 0.6543; More...

AUD/USD's fall from 0.6798 resumed by falling through 0.6479 temporary low and intraday bias is back on the downside. 0.6361 support is already breached but there is not sign of bottoming yet. Deeper decline could be seen to 0.6269 support next. On the upside, above 0.6479 support turned resistance will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with fall from 0.6798 as another falling leg. Deeper fall could be seen to the lower side of the range between 0.6169/6361. But strong support should be seen there to contain downside. For now, risk will stay on the downside as long as 55 D EMA (now at 0.6621) holds, in case of rebound.