Sample Category Title

(ECB) Monetary policy accounts

Account of the monetary policy meeting of the Governing Council of the European Central Bank held in Frankfurt am Main on Wednesday and Thursday, 5-6 June 2024

4 July 2024

1. Review of financial, economic and monetary developments and policy options

Financial market developments

Ms Schnabel noted that since the Governing Council's previous monetary policy meeting on 10-11 April 2024, the narrative in financial markets had converged across major advanced economies. It had moved towards a more gradual easing cycle and high-for-longer interest rates, owing to a more protracted "last mile" of disinflation. The key drivers of financial market developments had been a stronger euro area economy, signs of a cooling US economy and strong investor risk appetite.

Euro area macroeconomic data had continued to turn out better than expected over the past four months, strengthening investors' view that the economic recovery was on track. By contrast, macroeconomic data surprises in the United States had become less favourable. Tentative signs of the US labour market cooling and inflation in line with expectations had eased investors' concerns that the Federal Reserve System might have to hike interest rates again.

Looking at how the incoming data had affected expectations for ECB monetary policy, the expected timing of the first rate cut had remained unchanged. Markets and survey participants were almost certain there would be a first cut of 25 basis points in June. Yet the overnight index swap (OIS) forward curve had edged higher beyond June. It was cumulatively pricing in around 20 basis points less in rate cuts by the end of 2024 than it had before the Governing Council's previous monetary policy meeting in April. In the June Survey of Monetary Analysts (SMA) the median participant expected three rate cuts of 25 basis points each by the end of 2024. This was more than the cuts embedded in market pricing, but one cut less than survey participants had expected before the Governing Council's previous monetary policy meeting.

With US inflation having repeatedly surprised on the upside since the Federal Reserve's pivot in December 2023, market pricing in the United States had also gradually shifted towards fewer and later rate cuts in 2024. Most recently, however, more subdued US economic data and an inflation release broadly in line with expectations had caused market participants to again price in a slightly steeper easing cycle.

As a result, the narrative of monetary policy divergence across the Atlantic had not played out strongly so far. By the end of 2024 policy rate cuts were expected to diverge modestly, as the ECB was expected to start its easing cycle ahead of the Federal Reserve, but that divergence was expected to vanish by the end of 2025. Hence, monetary policy was expected to remain relatively synchronised, with markets anticipating a more gradual and cautious easing cycle across both economies. Yet the uncertainty around this gradual easing cycle remained high on both sides of the Atlantic.

Market expectations of a more gradual easing cycle and elevated uncertainty around the rate path rested upon anticipation of a more protracted and bumpier disinflation path. At the start of 2024, investors had expected swift and continuous disinflation. At that time markets had priced in euro area headline inflation (excluding tobacco) returning to the 2% target by June 2024 and subsequently staying around that level. Since then, markets had gradually priced in a bumpier inflation profile. While investors still expected inflation to be close to 2% by June 2025, they expected it to hover in a range of 2.3% to 2.5% until at least the end of 2024. At the same time, the medium and longer-term inflation profile had also edged up, suggesting that investors did not anticipate a scenario in which inflation would return to below-target levels, as seen during the "low-for-long" period.

The reconvergence in policy rate expectations between the euro area and the United States had also been reflected in longer-term risk-free yields. Since the Governing Council's previous monetary policy meeting, the spread between US and euro area nominal yields had narrowed from its peak in April. Movements in yield differentials between the euro area and the United States had been mirrored in the euro-US dollar exchange rate, with the euro recently having recovered some of its losses against the US dollar.

Euro area financial conditions had been mixed in recent weeks. One important driver of these conditions had been risk asset prices. After the downward correction in equity markets in mid-April 2024, when US rate cuts had been pushed out in time, stock markets had recovered across major economies, temporarily even reaching new all-time highs in the euro area and the United States.

The combination of buoyant risk sentiment globally and recovering domestic growth momentum had also continued to contain sovereign bond spreads. At the same time, market absorption in euro area government bond markets had remained smooth, supported by benign liquidity conditions. The smooth market absorption was even more remarkable when considering the further increase in the net issuance of euro area government bonds in 2024. Together with the reduction in the Eurosystem's market footprint, this had resulted in record levels of net supply in 2024.

Strong investor risk appetite had fostered low corporate bond spreads, which had narrowed further for high-yield bonds since the Governing Council's previous monetary policy meeting in April. Therefore, risks of price corrections continued to be elevated, especially in the high-yield segment. Overall, asset price configurations in equity markets and in the sovereign and corporate bond space pointed to stretched valuations in riskier market segments and to risks of price corrections if the historically buoyant risk sentiment turned.

Pricing in risk asset markets continued to be supported by still abundant central bank liquidity. Euro area excess liquidity had continued to decline and stood 33% or €1.6 trillion below its peak of €4.7 trillion in November 2022. The spread between the euro short-term rate (€STR) and the deposit facility rate showed few signs of a lift-off from its floor. At -9.3 basis points, it remained close to the levels seen over the past year.

The global environment and economic and monetary developments in the euro area

Starting with the global economy, Mr Lane stressed that 2023 had still been part of the post-pandemic normalisation process. The supply side had been a big driver of the strong performance of global growth, while euro area competitors' export prices had fallen. The carry-over from that was partly responsible for the low levels of goods inflation now observed in the euro area. Developments in global activity were looking favourable up to April, mainly because of the soft data, but the outlook for global trade in the second quarter was mixed.

Looking ahead, the June 2024 Eurosystem staff macroeconomic projections were built on a stable external environment. In annual terms, world GDP excluding the euro area was projected to grow at 3.3% in 2024 and 2025. Growth in euro area foreign demand was set to recover this year, rising to 2.1% from 0.8% last year. It was subsequently expected to grow at rates of around 3%. The euro had remained broadly stable both against the US dollar and in nominal effective terms since the last monetary policy meeting of the Governing Council. From a longer-term perspective too, the EUR/USD exchange rate had been broadly stable, though the euro had appreciated since the start of the year in trade-weighted terms. Oil prices had shown sizeable fluctuations over the past year and had decreased by 16% to USD 78 per barrel since the April Governing Council meeting. Looking ahead, they were expected to remain volatile, which was also linked to geopolitical risks. Gas prices meanwhile had gone in the other direction: since the last Governing Council meeting, European gas prices had increased by 32% to €36 per megawatt, although demand remained subdued and gas storage levels were high.

Turning to the euro area, headline inflation had been 2.6% in May according to the flash estimate, 0.2 percentage points higher than in April. Energy inflation had increased to 0.3% from -0.6% in April, mainly driven by upward base effects, while food inflation had receded to 2.6% in May from 2.8% in April. Inflation excluding energy and food (core inflation) had risen to 2.9% in May from 2.7% in April. The decline in goods inflation by 0.1 percentage points to 0.8% had been offset by a rebound in services inflation. This had increased to 4.1% in May after having slowed in April – for the first time in five months – to 3.7%.

Most measures of underlying inflation had eased further, reflecting the fading impact of past large supply shocks and weaker demand, and were drifting lower towards 2%. At the same time, some underlying inflation indicators remained relatively high, reflecting the lagged unwinding of past inflationary shocks, strong ongoing labour cost increases and/or the one-off repricing in some services items.

Wage growth was still elevated, driven by the ongoing adjustment to the past inflation surge. Negotiated wage growth had increased to 4.7% in the first quarter of 2024, 0.2 percentage points higher than in the last quarter of 2023. The stronger growth in the first quarter included very large one-off payments in the public sector of the euro area's largest economy. More broadly, the design of some multi-year wage settlements in that economy specified large increases in 2024 – to compensate for the lack of earlier adjustments to the inflation surge – but much smaller increases in 2025.

Forward-looking wage trackers signalled that wage dynamics would remain strong in 2024 but decelerate in 2025. For this year many wage contracts had already been concluded. The Indeed wage tracker had declined to 3.4% in April. Similarly, firms participating in the Corporate Telephone Survey in April expected wages to grow by 4.3% in 2024, compared with 5.4% in 2023. Therefore wage growth would continue to be a key driver of inflation in 2024, even though the net impact of labour cost increases on prices was being buffered by a lower contribution from profits.

The GDP deflator was expected to still come in high for the first quarter of 2024, but to decelerate significantly compared with the fourth quarter of 2023, when it had stood at 5.3%. The deceleration in domestic price pressures was therefore continuing and the projections foresaw a further moderation. This relied on the ongoing compression of profits and a continued decline in unit labour costs, linked to the scale of the procyclical improvement in productivity.

Inflation was projected to fluctuate around current levels in the coming months. The headline inflation profile in 2024 was affected by the rolling back of fiscal measures and upward energy base effects. Headline inflation was then expected to decline towards the target over the second half of the following year, owing to weaker growth in labour costs in 2025 than in 2024, the lagged impact of past monetary policy tightening gradually feeding through to consumer prices, and the fading impact of the energy crisis and the pandemic on price and wage dynamics. The June Eurosystem staff projections saw inflation averaging 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026. Compared with the March ECB staff projections, headline inflation had been revised up by 0.2 percentage points for both 2024 and 2025 and was unchanged for 2026.

For core inflation, staff projected an average of 2.8% in 2024, 2.2% in 2025 and 2.0% in 2026. This implied an upward revision of 0.2 percentage points in 2024 and 0.1 percentage points in 2025, while the projection for 2026 remained unchanged.

A central element in this projection was the gradual easing of nominal wage growth from initially elevated levels. The upward impact of inflation compensation pressures in a tight labour market was seen as fading in the period ahead. A recovery in productivity growth should support the moderation in labour cost pressures. Moreover, profit growth should weaken and partially buffer the pass-through of labour costs to prices.

Measures of shorter-term inflation expectations had declined since the previous year, while longer-term inflation expectations had remained broadly stable, with most standing at around 2%.

With some uncertainty surrounding the staff projections, it was useful to compare projections for the fourth quarter of each year. The fourth quarter was less affected by carry-over effects. Relative to the outlook in September 2023, the projected timely return of inflation to target had been reconfirmed in the December, March and June staff projections. The stability of projected inflation at the end of 2025 over the last four rounds of projections had been remarkable. In addition, the inflation outlook for 2026 had been reconfirmed over the last two rounds.

Turning to economic activity, after five quarters of stagnation, euro area GDP had grown by 0.3% over the first quarter of 2024. Preliminary aggregates for national GDP figures available so far showed that economic growth in the first quarter had mainly been driven by net exports, and domestic demand had only played a fairly limited role. Incoming information suggested continued growth in the short run, driven by a pick-up in consumption growth amid rising real disposable income and improving confidence. Over the medium term the negative impact of the past monetary policy tightening was seen to fade gradually. Growth would also benefit from a resilient labour market, with the unemployment rate declining further from historically low levels.

The services sector had been expanding at a solid pace, with accommodation and food services contributing to the dynamism. Manufacturing activity had also improved significantly in May, according to the Purchasing Managers' Index (PMI) survey, but it remained in contractionary territory.

With regard to consumption, surveys signalled strong developments in contact-intensive services, while for goods – both retail and durable goods such as motor cars – surveys pointed to figures well below normal levels. There had clearly been a recovery in consumer confidence in the course of 2023 as the terms of trade improved, but confidence had been fairly flat for several months now. Consumer uncertainty had come down but was still relatively high. Housing investment had increased in the first quarter – helped by temporary factors in the largest euro area economy, such as the mild weather. Business investment was projected to grow over the year.

For most of 2023 global imports had grown more strongly than euro area exports, leading to a loss in market share for the euro area. Since the start of 2024 euro area exports had been growing more quickly than global imports, but global imports were decelerating. Forward-looking PMIs remained muted for exports, but an expansion of activity in the tourism sector was expected, although not on the same scale as in the previous two years.

The unemployment rate had edged down to 6.4% in April, the lowest level since the start of the euro. Employment had increased in line with economic activity in the first quarter and was expected to grow moderately in the second quarter. Some indicators suggested a marginal softening of labour market conditions. The job vacancy rate had declined by 0.1 percentage points to 2.8% in the first quarter of the year, which was still high but continued the gradual easing from its peak in the second quarter of 2022. The Indeed job postings suggested that this trend would continue in the second quarter.

Developments in fiscal policies pointed to an improvement in the budget balance over the next few years. Active fiscal adjustment in 2024 was seen as easier than in the austerity years because a large part related to the reversal of fiscal subsidies, and this was considerably less painful than cutting pay or reducing employment. The fiscal multipliers were also smaller. In terms of dynamics, there was only a limited revision of fiscal plans compared with the March projections.

The recovery should strengthen in the coming quarters. The latest staff projections saw economic growth at 0.9% in 2024, 1.4% in 2025 and 1.6% in 2026. Compared with the March projections, the outlook for GDP growth had been revised up by 0.3 percentage points for 2024, owing to the positive surprise at the start of the year and improved forward-looking information. For 2025 it had been revised down marginally by 0.1 percentage points, while it was unrevised for 2026.

Risk-free market interest rates had increased for most maturities since the previous monetary policy meeting. The market had priced in higher real rates on the back of higher than anticipated inflation readings and the stronger economy. Financing costs had plateaued at restrictive levels as the past policy rate increases had worked their way through the financial system. The average interest rates on new loans to firms and new mortgages had been unchanged in April, at 5.2% and 3.8% respectively. Credit dynamics remained weak. Bank lending to firms had grown at an annual rate of 0.3% in April, down slightly on the previous month. Growth in loans to households had been unchanged at 0.2% on an annual basis. The annual growth in broad money as measured by M3 had risen to 1.3% in April, from 0.9% in March, as the euro area's growing current account surplus and non-resident demand for euro-denominated securities gave rise to monetary inflows from outside the euro area.

Monetary policy considerations and policy options

Overall, the updated joint assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission (the three elements of the ECB's "reaction function") supported increased confidence that inflation was converging to target in a timely and sustained manner. In particular, inflation was projected by staff to fall from 5.4% in 2023 to 2.5% in 2024, on average, and to decline towards target over the second half of 2025. Reflecting higher energy and non-energy commodity prices and the recent upside surprises in services inflation, this disinflation was somewhat slower in the updated projections. At the same time, the incoming data suggested that the economic recovery was proceeding only at a moderate pace (which, in turn, pointed to contained risks of demand-driven inflation pressures).

A granular analysis of the drivers of domestic inflation, services inflation and wage growth indicated that these should see a marked deceleration in 2025 relative to 2024. The partial data already available for the first quarter of 2024 also showed that the compression of unit profits was helping to absorb wage growth, thus giving grounds for increased confidence about the assumption that profits would be playing an important buffering role. Over time, disinflation would be supported by the restrictive monetary policy stance and the fading impact of past inflation on ongoing price pressures, while the countervailing impact of the reversal of fiscal support measures would fall out of the data.

Relative to the start of the holding period in September 2023, when the ECB had brought the policy rates to their current levels, the projected timely return of inflation to target had been reconfirmed in the December, March and June projection rounds. For instance, the inflation rate projected for the end of 2025 had been remarkably stable over the last four projection rounds. In particular, between the September 2023 and the June 2024 rounds, the projected HICP inflation rate for the fourth quarter of 2025 compared with a year earlier had fluctuated within a very narrow interval of 1.9-2.0%. The inflation outlook for 2026 had been confirmed over the last two projection rounds. Moreover, the overall speed of disinflation had been faster than expected. Over this period, inflation had come down by 2.6 percentage points. Whereas, at the start of the holding period, staff had seen inflation averaging 5.6% in 2023 and 3.2% in 2024, inflation had actually averaged 5.4% in 2023 and the inflation rate for 2024 had been marked down to 2.5% in the latest projection exercise. The set of underlying inflation indicators also showed considerable progress compared with the start of the holding period, with most gauges drifting lower towards 2%. This improvement in the inflation profile had reduced the risk that "too high for too long" inflation posed to the stability of inflation expectations, including through its impact on future wage settlements. Measures of shorter-term inflation expectations had declined over recent months, while measures of longer-term inflation expectations had remained broadly stable, with most standing at around 2%.

Meanwhile, the transmission side of the reaction function remained strong. Mortgage rates were measurably lower than their autumn peak, but indices of the affordability of mortgage loans still pointed to restrictive conditions. Rates on corporate loans had been moving sideways in nominal terms (and therefore upwards in real terms), dampening demand for external finance. Activity was recovering, although less so in the segments of demand most sensitive to interest rates, such as construction activity – abstracting from temporary factors – and non-construction business investment. Overall, the incoming data on financing conditions signalled that the monetary stance remained restrictive, and this would help maintain the disinflationary process. In particular, compared with the start of the holding period, real lending rates for firms and households had risen markedly.

An interest rate decision should be robust across a wide range of scenarios. At a still clearly restrictive level of 3.75% for the deposit facility rate, even large upside shocks to inflation (including more persistent than expected services inflation or weaker than expected monetary transmission) could be addressed by a slower pace of rate cuts than in the baseline rate path embedded in the projections. At the same time, a policy rate level of 3.75% offered greater protection against downside shocks than if it remained at 4.0%.

Based on this assessment, it was now appropriate to moderate the degree of monetary policy restriction after nine months of holding rates steady. Accordingly, Mr Lane proposed that the three key ECB interest rates be lowered by 25 basis points.

At the same time, Mr Lane underlined that the high level of uncertainty and the still elevated price pressures evident in the domestic inflation, services inflation and wage growth indicators meant that a restrictive monetary stance would still need to be maintained, following a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction. Over time, the incoming data would provide information about the balance between one-off elements and the persistent component in inflation, while the evolution of cost dynamics (including the interplay between compensation and productivity) and domestic pricing power would depend on the strength and composition of the cyclical recovery. In charting the future course of policy, the Governing Council should also maintain its three-part evaluation framework based on the inflation outlook, the dynamics of underlying inflation and the state of monetary policy transmission.

The Governing Council should also confirm its previously communicated intention to reduce the PEPP portfolio by €7.5 billion per month, on average, over the second half of the year, and reiterate its intention to discontinue reinvestments under the PEPP at the end of 2024. The operational modalities for partial reinvestments of PEPP redemptions should closely follow the precedent of the APP partial reinvestment phase, which would help ensure that the process remained transparent and as neutral as possible to the pricing in financial markets. Furthermore, Mr Lane proposed that flexibility continue to be allowed in the remaining PEPP reinvestments as an effective first line of defence against fragmentation risks, but to be exercised only if market conditions deteriorated.

Finally, in line with the monetary policy strategy, staff had assessed the links between monetary policy and financial stability. The analysis suggested that euro area banks remained resilient. The improving economic outlook had fostered financial stability, but heightened geopolitical risks clouded the horizon. An unexpected tightening of global financing conditions could prompt a repricing of financial and non-financial assets, with negative effects on the wider economy. Macroprudential policy remained the first line of defence against the build-up of financial vulnerabilities. The measures that were currently in place or would soon take effect were helping to keep the financial system resilient.

2. Governing Council's discussion and monetary policy decisions

Economic, monetary and financial analyses

As regards the external environment, the latest data, both soft and hard, pointed to sustained momentum in global activity and a strengthening of global trade in the first half of 2024. Members pointed to uncertainty related to political and economic developments in the world's two largest economies and their potential spillovers to the euro area. A question was raised regarding growth policies adopted in China and their impact on activity and inflation in the euro area. Strong expansion of manufacturing capacity would boost Chinese exports and likely imply a loss of export market share and lower economic growth for the euro area, associated with stronger disinflationary forces. At the same time, if a large part of European production capacity were to be driven out of the market, it would mean costly write-offs of investment with possibly inflationary consequences.

Concern was expressed that the global trading system could see increased fragmentation into separate economic blocs if authorities engaged in reciprocal tariff-raising. While deglobalisation was, as yet, not clearly visible in the data, it was considered an important risk for the future. However, quantifying this risk was difficult and possible outcomes could lie anywhere between limited sector-specific consequences and a wider breakdown of trade links. The view was put forward that deglobalisation, greater protectionism and the rising costs of climate change were global trends affecting the supply side of the economy and giving rise to longer-term inflation pressures.

With regard to the euro area economy, members widely noted that the June 2024 Eurosystem staff projections entailed upward revisions to both economic growth and inflation. Inflation was likely to stay above target well into next year. Headline and core inflation had both been revised up for 2024 and 2025 compared with the March projections. On economic activity, the latest data lent support to the recovery that had been anticipated in previous projection rounds. After five quarters of stagnation, the euro area economy had grown by 0.3% over the first quarter of 2024.

The upward surprise in first quarter growth was seen as allaying fears of a materialisation of the downside risks that had been identified in previous discussions. Concerns that monetary policy would unduly hold back growth were also diminishing. However, it was argued that the better than expected outcome had relied on a pick-up in construction and net exports, in part reflecting temporary factors. Nonetheless, the surprise had prompted staff to revise up their growth expectations significantly for 2024 as a whole, following a succession of projection rounds with downward revisions.

In this context, some doubts were raised about whether the recovery would take place as expected, since this depended on a pick-up in private consumption for which there was no convincing evidence as yet in the data. It was also noted that the staff projections entailed an upward revision to the saving ratio. In addition, the concern was raised that, in the presence of both domestic political and geopolitical uncertainties, the saving ratio could go even higher than expected. If this were to happen, consumption could be curtailed for longer. However, as the upward revision to household savings came at the same time as a more favourable growth outlook – and the revision kept the ratio well above pre-pandemic levels – a higher propensity to consume could also be envisaged, with the associated upside risk to consumption growth in the baseline.

Like consumption, investment had also remained weak in the first quarter. It was argued that it likely reflected a fair amount of replacement investment, which could not be expected to provide a strong impulse for the recovery. Business investment was being held back by weak final demand and high borrowing costs. At the same time it was suggested that, from a sectoral perspective, the expected recovery in activity was well on track. The weakness in manufacturing appeared to have bottomed out and the latest survey data supported the notion of a services-led recovery. While the impact of restrictive monetary policy was seen to be gradually fading, the services sector had anyway been affected less strongly. This sector was less capital-intensive and thus less interest rate-sensitive, while still responding to the indirect influence of monetary policy through a general dampening of aggregate demand. Tourism was seen as an important component in the growth of services and was driven to a large extent by domestic real incomes in the euro area and, to a lesser extent, by foreign demand.

Turning to the labour market, members considered that, overall, it had remained persistently robust. This was a key element in the soft landing of the economy. It was seen as puzzling that the market indicators of labour hoarding were still relatively unchanged and that there was not more labour shedding and unemployment – at least in industry and construction. Shortages of labour persisted, especially in the services sector. At the same time, the point was made that, coming from historically high employment and low unemployment, the market could realistically only be expected to slacken. Moreover, net employment gains concealed much larger numbers for turnover and new contracts, suggesting that firms were using this churning to foster productivity gains and thus help absorb a rising wage bill.

With respect to fiscal and structural policies, members reiterated that national policies should aim at making the economy more productive and competitive. This would help raise potential growth and reduce price pressures in the medium term. An effective, speedy and full implementation of the Next Generation EU (NGEU) programme, progress towards capital markets union and the completion of banking union, and a strengthening of the Single Market would help foster innovation and increase investment in the green and digital transitions. Implementing the EU's revised economic governance framework fully and without delay would help governments bring down budget deficits and debt ratios on a sustained basis. It was stressed that a speedy and full implementation of NGEU programmes for innovation and green transitioning would also help reduce price pressures in the medium term. Some concern was expressed that, in a period of political uncertainty and multiple elections, fiscal policy might show less consolidation by the end of this year than was factored into the current projections.

Against this background, members assessed that the risks to economic growth were balanced in the near term but remained tilted to the downside over the medium term. A weaker world economy or an escalation in trade tensions between major economies would weigh on euro area growth. Russia's unjustified war against Ukraine and the tragic conflict in the Middle East were major sources of geopolitical risk. Adverse geopolitical developments could result in firms and households becoming less confident about the future and global trade being disrupted. Growth could also be lower if the effects of monetary policy turned out stronger than expected. Growth could be higher if inflation came down more quickly than expected and rising confidence and real incomes meant that spending increased by more than anticipated, or if the world economy grew more strongly than expected. It was suggested that risks to growth could also emerge from wage increases if these decoupled from the pace that firms could realistically absorb in productivity increases, implying a loss of competitiveness and market share, and ultimately a fall in investment and activity. Seen from a different angle, a weaker than expected economic recovery would curtail the expected productivity increases and lead to lower profit margins. This would reduce the economy's capacity to absorb the increases in real wages already embedded in wage contracts and the projection baseline.

With regard to price developments, members concurred with the assessment by Mr Lane that the latest data were a reflection of the bumpy profile of headline inflation expected in 2024. On the one hand, the fact that the latest figures for headline and, in particular, services inflation had been higher than in the March 2024 projections was seen to increase the uncertainty surrounding the further disinflation path. On the other hand, it was argued that the upward surprise in the latest data had been incorporated by staff into the June projections without subsequent offsetting, which was a prudent approach.

It was underlined that the upward revision of inflation in 2024 and 2025 had pushed the return to target to the end of 2025. While the projection for 2026 was unchanged, it was pointed out that this rested on the assumption that energy and food inflation would move below their longer-term averages. In view of the notoriously volatile nature of these two components and their exposure to the effects of geopolitics as well as climate change and transition policies, these benign assumptions were seen to be highly uncertain. In the shorter term, the projected inflation path was bumpy for the remainder of 2024, which was mainly due to base effects and was thus anticipated. When the inflation path was corrected for base effects, both the recent actual outcomes and the projected trend over the short-term horizon were seen to point clearly downwards. It was widely underlined that, despite the upward inflation surprises in April and May, the bigger picture remained one of ongoing disinflation.

Members noted that the May inflation numbers had been released after the cut-off date for the projections. Services inflation, at 4.1% in May, had surprised on the upside, had shown persistence, and was demonstrating strong momentum. However, a lot of persistence was already embedded in the projections and it was therefore argued that recent outcomes should not be viewed unambiguously as an upside risk to the current baseline inflation path. The strength of services inflation in the past few months stemmed, to a large extent, from the resetting of infrequently changed prices in areas such as insurance and healthcare. The wage-sensitive part of services inflation had continued to moderate. It was noted that, for core inflation, the persistence of services inflation had so far been broadly offset by the strong disinflation in the goods sector. This could not be expected to continue, in view of the fading impact of the reversal of past supply side shocks. Moreover, new headwinds could emerge for goods inflation in a world that was more prone to frequent supply chain disruptions, geopolitical fragmentation, protectionism and climate change dynamics. Hence, in the future low goods inflation would not always reliably compensate for an overshooting in services inflation.

Turning to domestic price pressures, wages were still rising strongly, making up for the past inflation surge, and were now the main determinant of inflation persistence. Owing to the staggered nature of the wage-adjustment process and the important role of one-off payments, the process of wages catching up with prices would likely feed into inflation for a considerable time, as seen in the pick-up in the growth of negotiated wages in the first quarter. All labour cost indicators, including Eurostat's new labour cost index, were at very high levels, and the anticipated moderation still had to materialise. At the same time, forward-looking indicators signalled that wage growth would moderate over the course of the year. Profits were absorbing part of the pronounced rise in unit labour costs, which reduced its inflationary effects.

It was reiterated that wages were a key element in the assessment of the inflation outlook. This was related in particular to their prominent role in the setting of services prices, but a range of indicators needed to be considered to form a holistic assessment. Growth in negotiated wages had increased to 4.7% in the first quarter of 2024. Moreover, data already available for a number of euro area countries suggested that growth in compensation per employee for the euro area as a whole was likely to remain in the first quarter at the elevated levels recorded in the fourth quarter of 2023.

The point was made that most of the latest wage information had already been incorporated in the baseline of the June staff projections and thus did not indicate upside risk. The same data, however, had already contributed to upward revisions of wage growth compared with the March projections, which was a warning not to underestimate the strength of wage dynamics and the scope for further surprises in the course of 2024. At the same time, it was emphasised that, taking into account available country-based estimates, the euro area GDP deflator, unit labour costs and unit profits had probably increased more slowly in the first quarter of 2024 than had been embedded in the June projections.

High current wage growth was considered to reflect to a large extent workers seeking compensation for past purchasing power losses. Wage dynamics were therefore likely to slow once this process was complete and inflation was normalising. It was cautioned that the catching up could nonetheless imply a drawn-out process and bumpy wage path, depending on when contracts came up for renewal in the staggered wage-setting process and for which period of inflation they were compensating. Attention was drawn to one-off payments, which played an important role, particularly in light of fiscal incentives that were set to expire. However, there were indications from unions that such one-off payments might not be transitory but in future be factored into regular pay rises.

More generally, a view was expressed that the catching up could lead real wages to exceed their pre-war or pre-pandemic levels or trends in an environment of protracted labour scarcity and possible shifts in bargaining power between capital and labour. In addition, it was remarked that the scope for buffering higher wages via a compression of profit margins was more limited in the services sector, which was also less exposed to international competition and was experiencing robust demand. However, there were also risks going in the opposite direction for the wage growth profile. It was argued that some of the recent high wage settlements had taken place in sectors which had made substantial profits over the past three years. This allowed employers to grant generous wage increases and to absorb them without passing them on to final prices.

Incoming data on the critical relationship between wages, productivity and profits was seen, overall, as supporting prudent inflation projections and an ongoing disinflation process. However, it was also cautioned that uncertainty surrounding the outlook was very high and that, in the transition to lower inflation after a period of large shocks and possible structural changes, such relationships might start evolving differently from historical patterns. Hence, continued prudence was warranted with respect to relying on standard projection models, and more actual data was needed to provide sufficient confidence that disinflation would continue and not stall on the last mile. At the same time, diminishing projection errors were seen to give grounds for renewing confidence in the projections.

As regards longer-term inflation expectations, measures had, overall, remained broadly stable, with most standing at around 2%. Somewhat higher rates for market-based measures essentially reflected higher inflation risk premia, while "genuine" inflation expectations remained anchored at the inflation target. While the anchoring of expectations across indicators could be taken as a sign of the credibility of monetary policy, the literature on "experience effects" warned that extended periods of high inflation could have a lasting impact on the formation of inflation expectations, making them more fragile and anchoring more difficult in the future. In this context, however, comfort was drawn from the gradual lowering of consumer inflation expectations, even if levels in household surveys typically remained above the ECB's inflation target. This was seen as signalling trust in the disinflation process and would have a self-fulfilling element if it contributed to a moderation in wage claims and firms' pricing power.

Members assessed that inflation could turn out higher than anticipated if wages or profits increased by more than expected. Upside risks to inflation also stemmed from the heightened geopolitical tensions, which could push energy prices and freight costs higher in the near term and disrupt global trade. Moreover, extreme weather events, and the unfolding climate crisis more broadly, could drive up food prices. By contrast, inflation could surprise on the downside if monetary policy dampened demand more than expected, or if the economic environment in the rest of the world worsened unexpectedly. It was suggested that there could be further risk factors for inflation, related for instance to the extent of the expected pick-up in productivity growth or the evolution of the fiscal stance underpinning the inflation outlook. However, these elements could develop in either direction and were therefore not decisive elements in the balance of risks.

Against this background, members expressed different views regarding directional changes in the balance of risks. On the one hand, it was argued that, all other things being equal, the staff's upward revisions to the baseline implied a reduction in remaining upside risks and made the risks more balanced. On the other hand, it was maintained that the downside risk related to a stronger transmission of monetary policy was gradually receding, while continued upside risks such as from higher labour costs shifted the balance to the upside.

Turning to the monetary and financial analysis, market interest rates had risen since the Governing Council's previous meeting and real interest rates had also recently increased. Market participants were fully pricing in a 25 basis point cut in the key ECB interest rates at the June meeting, with between one and two further cuts priced in by the end of the year. A shallower easing cycle was now expected on both sides of the Atlantic amid similarities in recent inflation trends globally.

Financial markets were supported by strong risk appetite, which contrasted with the limited risk appetite among euro area consumers and firms. This suggested either that financial market sentiment would weaken at some point or that the real economy would catch up. Market sentiment was also buoyant despite heightened geopolitical risks and uncertainties. The risk of mispricing in financial markets was therefore being monitored, also from a financial stability perspective.

Financing costs had plateaued at restrictive levels as the past policy rate increases had worked their way through the financial system. The average interest rates on new loans to firms and on new mortgages had been unchanged in April. But lending rates had increased in real terms since the time of the last rate hike in September 2023.

Credit dynamics remained weak. Credit flows to firms had been broadly stable at low levels in both March and April, taking bank lending and debt securities together. Firms' demand for loans for investment remained very weak, owing to both low aggregate demand and continuing high borrowing costs. Growth in loans for house purchase remained stagnant, while consumer credit growth was more resilient, yet still weak. The annual growth in broad money – as measured by M3 – continued its gradual recovery while remaining relatively subdued.

Looking ahead, loan growth was likely to gradually pick up. At the same time, it was highlighted that banks had not reduced their liquid asset holdings as targeted longer-term refinancing operations had matured and appeared to have a strong preference for liquidity. The lower supply of central bank liquidity in the system could therefore reduce the appetite of banks to lend. In this respect, the view was also expressed that as long as banks benefited from ample excess reserves remunerated at the deposit facility rate, they had a limited incentive to expand risky lending to the real economy.

In their biannual structured exchange on the links between monetary policy and financial stability, members concurred that euro area banks had remained resilient and continued to have robust capital and liquidity positions. The improving economic outlook had fostered financial stability, as also highlighted in the recently published Financial Stability Review. At the same time, geopolitical factors could increase risks in the period ahead. An unexpected tightening of global financing conditions could prompt a repricing of financial and non-financial assets, with negative effects on the wider economy. Macroprudential policy remained the first line of defence against the build-up of financial vulnerabilities, and the measures currently in place or soon to take effect were helping to keep the financial system resilient.

Monetary policy stance and policy considerations

Turning to the monetary policy stance, members assessed the data that had become available since the last monetary policy meeting in accordance with the three main elements that the Governing Council had communicated in 2023 as shaping its reaction function. These comprised the inflation outlook, the dynamics of underlying inflation, and the strength of monetary policy transmission.

Starting with the inflation outlook, members broadly concurred with the assessment that had been presented by Mr Lane in his introduction. The June staff projections for headline inflation had been revised up for 2024 and 2025 compared with the March projections. Inflation was expected to fluctuate around current levels for the rest of the year, including due to energy-related base effects. But it was still expected to decline towards the ECB's 2% target over the second half of next year, owing to weaker growth in labour costs, the unfolding effects of the ECB's restrictive monetary policy, and the fading impact of the energy crisis and the pandemic. Subsequently, inflation was expected to remain close to the target in a sustainable manner. Measures of longer-term inflation expectations had also remained broadly stable, with most anchored at around the 2% target, even though market-based expectations had moved up in the most recent period. The inflation expectations of consumers and firms had continued to decline gradually as well. Together, these developments in inflation expectations gave an indication of public trust and confidence in the disinflation process and the return of inflation to the 2% target.

Members generally expressed confidence in the inflation outlook confirming an ongoing disinflation process, as also reflected in the staff projections, although recent data suggested inflation could be stickier than had previously been expected and the exact speed at which it would return to target was uncertain. At the same time and from a longer-term perspective, it was highlighted that different vintages of projections made over the past year for inflation in 2025 had fluctuated in a narrow range of between 2% and 2.2%. This renewed stability could give rise to greater confidence in the reliability and robustness of the projections, and showed inflation remaining on track to meet the target in the medium term, notwithstanding the upward revisions in the inflation projections for 2024 and 2025. Smaller projection errors for headline inflation also supported confidence in this inflation outlook.

Members also broadly concurred that further progress had been made in terms of the dynamics of underlying inflation. Most measures of underlying inflation had declined further in April, the last month for which data were available, confirming the picture of gradually diminishing price pressures. At the same time, domestic price pressures remained strong, as wage growth was elevated. The staff projections for core inflation had also been revised up for 2024 and 2025 compared with the March projections, and momentum in both services and core inflation remained fairly strong. It would therefore still take time for more clarity to be obtained on the dynamics of important inflation drivers. Moreover, further evidence was required on both the extent to which unit profits would absorb the inflationary pressures from higher wages and whether productivity growth would rebound as expected.

Finally, members generally agreed that monetary policy transmission remained strong. Real interest rates stood close to their peak in this cycle. Monetary policy clearly remained in restrictive territory and would continue to do so for some time even if interest rates were cut further. This remained true even allowing for an upward shift in the natural rate of interest. The view was expressed that ongoing quantitative tightening also needed to be taken into account in the assessment of the policy stance. The restrictiveness of policy was reflected in weak credit dynamics and subdued aggregate demand. This had helped to lower inflation but also weighed on growth. Transmission would probably continue to unfold for some time, given that monetary policy affected the economy with long and variable lags. While the peak impact of restrictive monetary policy on financing conditions and GDP had probably already occurred, lags between the effect on output and the effect on prices could imply that the peak impact on inflation was still to come. Within that process, the transmission to services inflation could be weaker and slower than the transmission to goods inflation.

Overall, most members expressed continued or increased confidence that inflation was on track to decline sustainably to the 2% inflation target in a timely manner and by the end of 2025 at the latest. Some of the most recent data had been slightly less favourable than anticipated or hoped for in March and April. But it had been expected that the disinflationary path would be bumpy and noisy, with surprises likely in either direction. It was important to recognise that a smooth, linear disinflation process in 2024 was not a prerequisite for confidence in a timely return of inflation to the target. In addition, different indicators were providing contrasting signals on the future disinflation path.

More generally, it was important to step back and focus on the bigger picture. An excessive focus on individual observations and the details of developments between meetings ran the risk of not being able to see the wood for the trees. Being data-dependent meant not only looking at the most recent data but also assessing and being driven by all three reaction function elements, which included considering the wider inflation outlook. Recent developments and noise should not detract from the longer-term perspective indicating consistent disinflation and a timely and sustainable return of inflation to the 2% target. Despite recent volatility, the overall disinflation process had been proceeding well, with substantial progress made since the Governing Council last raised interest rates in September 2023. This was evident in the significant and greater than expected decline in both headline and core inflation since 2022 and since the time of the last rate hike. Headline inflation had halved since the time of the last hike, from 5.2% to 2.6%. The inflation outlook, especially for 2024, had also improved in the latest staff projections compared with the September and December 2023 rounds, even if the pace of disinflation was somewhat slower than had been anticipated in March and inflation projections for 2025 were slightly higher than they had been in September 2023. Market participants had remained confident in the medium-term disinflation process, even if volatility in nearer-term rate expectations reflected uncertainty over the pace of disinflation. It was important, therefore, not to overreact to adverse data or inflation numbers for a single month, since these did not necessarily imply a new trend and could reflect one-off factors, in the same way that it had been important not to overreact to positive numbers in previous months.

On balance, in the discussion of the inflation outlook and of the assessment of risks increased confidence was expressed that inflation would decline towards the 2% target over the second half of 2025 and subsequently remain sustainably at around that level. At the same time, it was underlined that decisions about the future always had to be taken in the face of uncertainty. So a key question was to assess when there was enough confirmation and confidence that inflation would return to target in a timely manner. At some point, it was necessary to make a judgement call based on the information available, even if that information was less conclusive than might be preferred. Such an approach should not be seen as conflicting with data-dependence, as waiting for full confirmation would almost certainly imply cutting interest rates too late, potentially creating a significant risk of undershooting the target.

It was also highlighted that the degree of restrictiveness needed to reduce inflation from 2.6% to 2% was likely to be lower than that in place since September 2023. Moreover, even following a 25 basis point cut, interest rates would remain in restrictive territory in relation to any current estimate of the natural or neutral rate of interest. This meant that stronger demand should not endanger the return of inflation to target and that upside shocks to inflation could be addressed by opting for a slower pace of rate reductions compared with the baseline rate path embedded in the projections. So there appeared to be little risk of needing to reverse policy unless large external shocks occurred, in which case such a policy reversal could be convincingly justified. Moreover, cutting interest rates by 25 basis points offered greater protection against downside shocks than keeping them at their current levels. Cutting interest rates now was thus robust across a wide range of scenarios and still maintained a cautious approach.

Some members felt that the data available since the last meeting had not increased their confidence that inflation would converge to the 2% target by 2025 but instead pointed to greater uncertainty in the outlook. For these members, even if the general disinflation trend remained intact in the bigger picture, the relevant point of comparison was with the data at the time of the last monetary policy meeting, or at most with the previous staff projections. At the time of the April meeting, interest rates had been kept on hold because there had not been sufficient confidence that inflation would return sustainably to the 2% target in a timely manner. Since then, however, wage growth had surprised to the upside and inflation seemed to be stickier, mainly on account of services inflation. Services inflation momentum was very high, and the pace of domestic disinflation had been overestimated in the recent period. Wage growth had also strengthened, and it was suggested that further significant wage pressures were in the pipeline. This pointed to greater stickiness ahead, which could increase price pressures for some time, even if wages themselves were a lagging indicator. In addition, the June staff projections for both headline and core inflation in 2024 and 2025 had been revised up compared with the March projections, with the latest projections for core inflation in 2024 barely changed from last September. Moreover, the projected return of headline inflation to the 2% target had been pushed out to the final quarter of 2025, after an already lengthy period of high inflation. Therefore, any further delay in bringing inflation back to target could make it more difficult to continue to anchor inflation expectations in the future. All of this suggested that the last mile, as the final phase of disinflation, was the most difficult.

These members also viewed risks to the inflation outlook as being tilted to the upside, partly because downside risks to inflation had diminished since the last meeting owing to the ongoing economic recovery but also owing to heightened geopolitical risks. It was argued that a small undershooting of inflation would be much less costly than a continued overshooting, especially as the anchoring of inflation expectations should not be taken as given.

Together, these considerations suggested that cutting interest rates was not fully in line with the principle of data-dependence, and that there was a case for keeping interest rates unchanged at the current meeting. Nevertheless, a willingness to support Mr Lane's proposal was expressed, notwithstanding the reservations put forward.

Monetary policy decisions and communication

Against this background, almost all members agreed with the proposal by Mr Lane to lower the three key ECB interest rates by 25 basis points. Based on the updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission, it was seen as appropriate to moderate the degree of monetary policy restriction after nine months of holding rates steady. Since the meeting in September 2023 inflation had fallen by more than 2.5 percentage points and the inflation outlook had improved markedly. The inflation projection for the fourth quarter of 2025 had fluctuated in a very narrow range of between 1.9% and 2% over that period, increasing confidence in the reliability, solidity and robustness of the projection showing that inflation would return to the 2% target in a timely manner. Underlying inflation had also eased, reinforcing the signs that price pressures had weakened, and over this period inflation expectations had broadly declined at all horizons. Monetary policy had kept financing conditions restrictive. By dampening demand and keeping inflation expectations well anchored, this had made a major contribution to bringing inflation back down.

A dissenting view was upheld, maintaining that the incoming data since the last meeting and upside risks to inflation did not support the case for a rate cut. In particular, current inflationary pressures evident in the recent data showed stickiness in inflation. This stickiness could be exacerbated by several different geopolitical risks. In addition, a decoupling from the path of US interest rates would risk adding to inflationary pressures via exchange rate effects.

With regard to future meetings, members emphasised that they remained determined to ensure that inflation returned sustainably to the 2% medium-term target in a timely manner and affirmed that they would keep policy rates sufficiently restrictive for as long as necessary to achieve this aim. In view of continuing uncertainty surrounding the disinflationary process and the bumpy path ahead, it was seen as important to maintain a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction, and there should be no pre-commitment to a particular rate path, so that full optionality could be retained. Members also reiterated that monetary policy should continue to be based on the established elements of the reaction function.

Turning to communication, members agreed that it was important to convey the increased confidence in the disinflationary process that had justified the policy decision, while highlighting the need for continued caution and patience regarding the future disinflation path and continued determination to bring inflation back to target in a timely manner.

Members agreed with Mr Lane's proposal to confirm the reduction of the Eurosystem's holdings of securities under the PEPP by €7.5 billion per month on average over the second half of the year, with the modalities for reducing the PEPP holdings to be broadly in line with those followed under the APP. They also agreed to continue applying flexibility in reinvesting redemptions falling due in the PEPP portfolio. In this context, it was noted that the earlier announcement of the intended PEPP run-off had been absorbed very smoothly by the markets.

Taking into account the foregoing discussion among the members, upon a proposal by the President, the Governing Council took the monetary policy decisions as set out in the monetary policy press release. The members of the Governing Council subsequently finalised the monetary policy statement, which the President and the Vice-President would, as usual, deliver at the press conference following the Governing Council meeting.

Monetary policy statement

Monetary policy statement for the press conference of 6 June 2024

Press release

Meeting of the ECB's Governing Council, 5-6 June 2024

Members

- Ms Lagarde, President

- Mr de Guindos, Vice-President

- Mr Centeno

- Mr Cipollone

- Mr Elderson

- Mr Hernández de Cos

- Mr Holzmann

- Mr Kazāks*

- Mr Kažimír

- Mr Knot*

- Mr Lane

- Mr Makhlouf

- Mr Müller

- Mr Nagel

- Mr Panetta

- Mr Patsalides*

- Mr Rehn

- Mr Reinesch

- Ms Schnabel

- Mr Scicluna

- Mr Šimkus

- Mr Stournaras*

- Mr Vasle

- Mr Villeroy de Galhau

- Mr Vujčić*

- Mr Wunsch

* Members not holding a voting right in June 2024 under Article 10.2 of the ESCB Statute.

Other attendees

- Ms Senkovic, Secretary, Director General Secretariat

- Mr Rostagno, Secretary for monetary policy, Director General Monetary Policy

- Mr Winkler, Deputy Secretary for monetary policy, Senior Adviser, DG Economics

Accompanying persons

- Ms Bénassy-Quéré

- Mr Dabušinskas

- Mr Demarco

- Mr Gavilán

- Mr Haber

- Mr Horváth

- Mr Kaasik

- Mr Koukoularides

- Mr Kroes

- Mr Lünnemann

- Mr Madouros

- Ms Mauderer

- Mr Nicoletti Altimari

- Mr Novo

- Mr Rutkaste

- Mr Šošić

- Mr Tavlas

- Mr Välimäki

- Mr Vanackere

- Ms Žumer Šujica

Other ECB staff

- Mr Proissl, Director General Communications

- Mr Straub, Counsellor to the President

- Ms Rahmouni-Rousseau, Director General Market Operations

- Mr Arce, Director General Economics

- Mr Sousa, Deputy Director General Economics

Release of the next monetary policy account foreseen on 22 August 2024.

ECB’s Lane Expects wage growth normalization in 2025

ECB Chief Economist Philip Lane, speaking in Italy today, expressed optimism that wage growth will normalize by 2025, based on surveys and forward-looking indicators among companies.

"The reason why we think inflation will come down next year is that this is the last year of high wages," Lane said. He highlighted that wage increases, which were around five or six percent last year, are now projected to be around three to four percent.

Lane also emphasized ECB's focus on domestic inflation, explaining, "What we can mostly influence is domestic inflation because the ability of European firms to raise prices depends on monetary conditions." He acknowledged that while domestic inflation has decreased from its peak a year ago, it remains around 4%, which continues to be a concern.

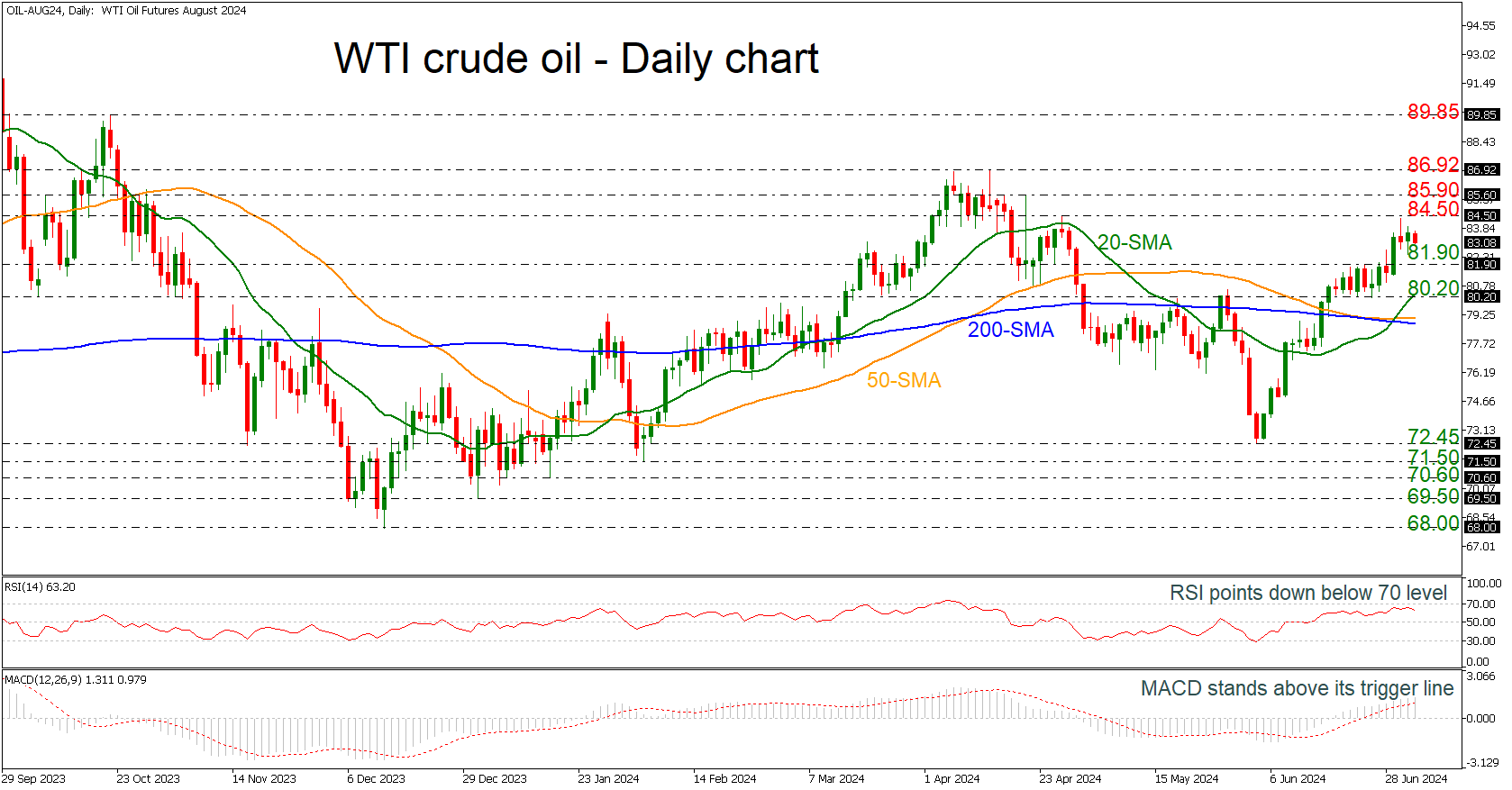

WTI Crude Oil Moves Sideways in the Very Short-term

- WTI crude oil still above SMAs

- RSI and MACD indicate weakening momentum

WTI crude oil futures are continuing to bounce off the 72.45 support level, remaining in an upside mood, but the current very short-term view is neutral. The price stands above the 81.90 support level after the bullish crossover within the 20-, 50- and 200-day simple moving averages (SMAs).

According to technical oscillators, the RSI is still standing above the 50 level but is pointing south, while the MACD is developing above its trigger and zero lines. Both indicate weakening momentum in the near-term.

Rising further, the bulls may find immediate resistance near the 84.50 barricade before traveling towards 85.90 and the previous peak of 86.92.

In the event of a potential downside retracement, the first support for traders to look for is 81.90 before meeting the 20-day SMA near the 80.20 mark. More declines could take the price towards the 200-day SMA at 78.80 before changing the outlook to neutral.

Overall, oil prices have been rising over the past month, but a rise above 86.92 is required to confirm a positive outlook for the overall picture.

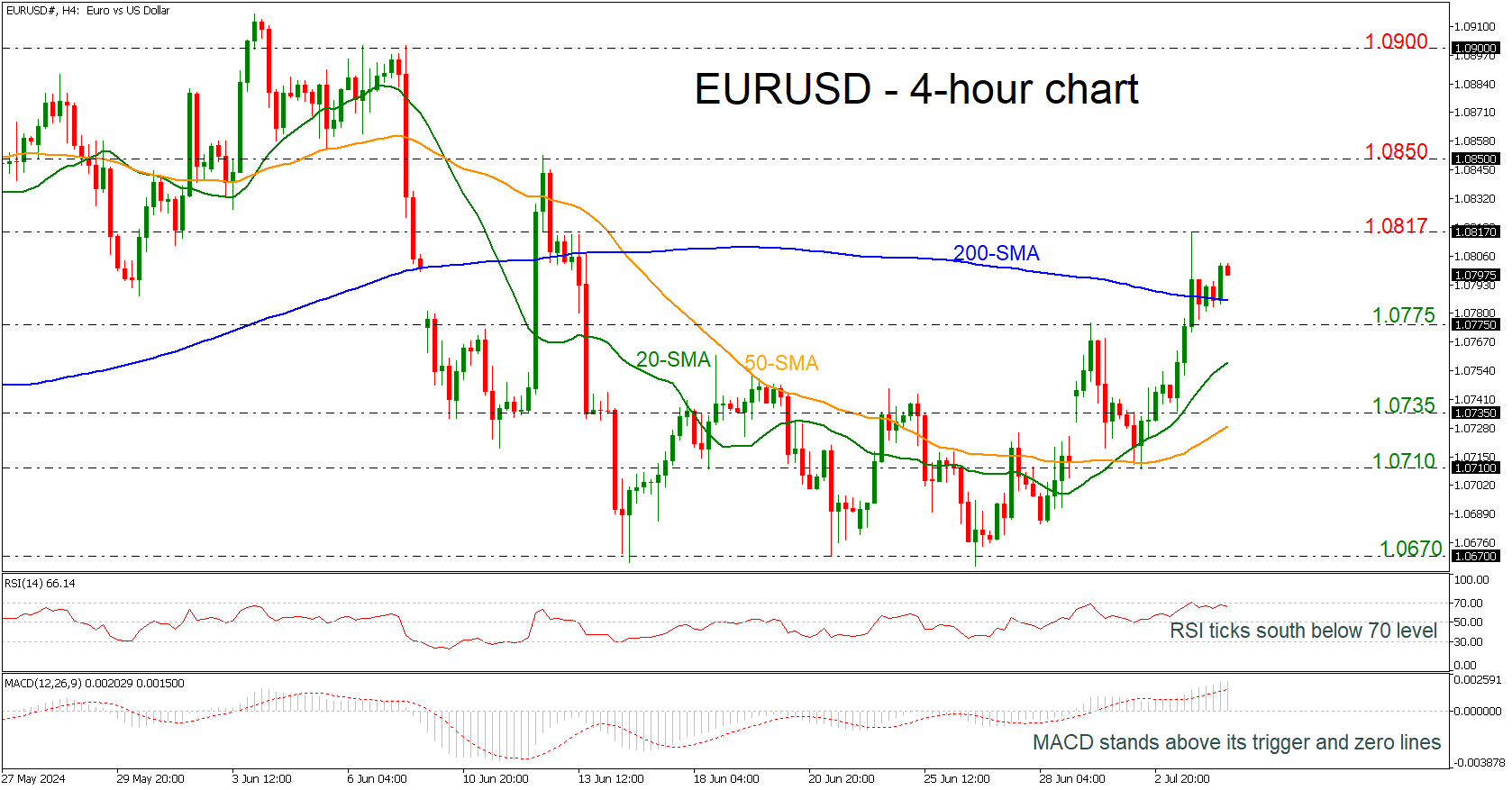

EURUSD Holds Above 200-Period SMA

- EURUSD continues the rebound off 1.0670

- Price is bullish in near term

- Momentum oscillators are mixed

EURUSD is finding strong support at the 200-period simple moving average (SMA) in the 4-hour chart near 1.0785. Also, the pair has been holding in an upside tendency after the bounce off 1.0670, with the MACD oscillator is holding above its trigger and zero lines. However, the RSI is flattening slightly beneath the 70 level.

If the bulls drive the market higher, then the pair could retest the previous spike towards 1.0817 before resting near the 1.0850 level. A challenge to the 1.0900 psychological level could also switch the broader outlook to bullish.

On the flip side, a drop beneath the 200-period SMA could meet immediate support at the 1.0775 level and even lower the 20-period SMA at 1.0757. The 1.0735 bar could act as a reversal point for the market ahead of the 50-period SMA at 1.0730.

To summarize, EURUSD looks bullish in the short term, but bearish in the long term.

Brent Crude – Oil Runs into Resistance as EIA Inventories Fall

- Brent Crude oil prices rose on Wednesday due to a larger-than-expected draw in US crude inventories.

- The market anticipates further inventory reduction, leading to potential support for prices in Q4.

- Technical analysis suggests bullish continuation, with a key resistance level at 87.90 and potential for a move towards 90.00 if this level is breached.

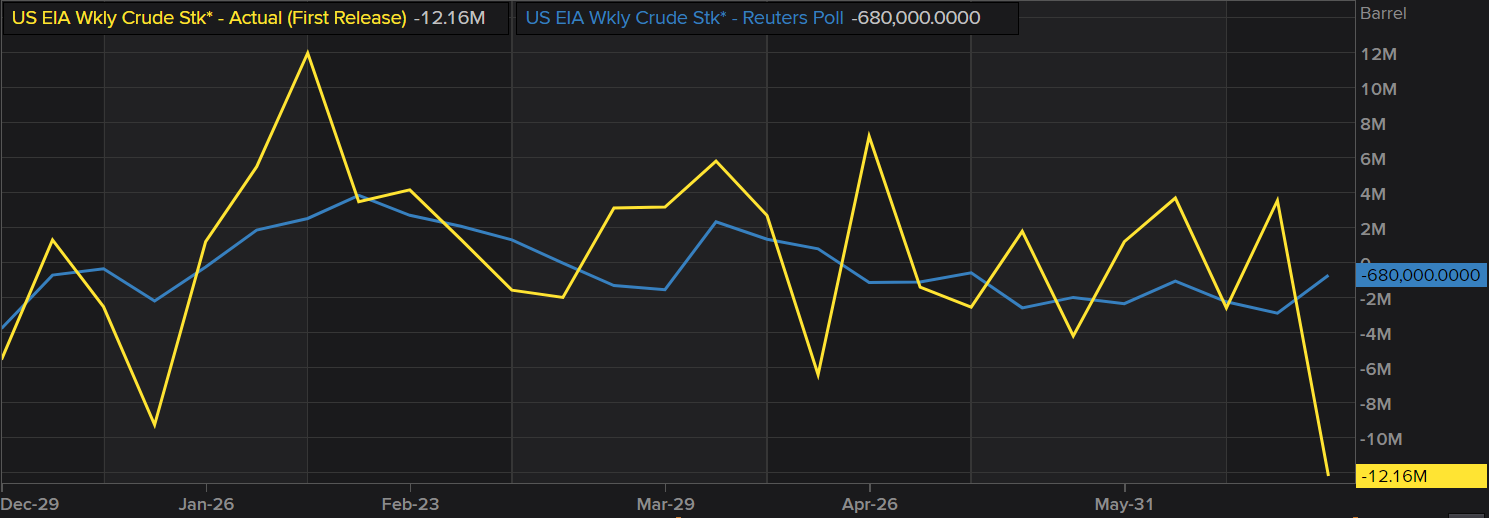

Brent Crude enjoyed a mixed Wednesday as European session losses were wiped out by EIA data. US Crude stocks fell more than expected in a move many had anticipated as the US summer holiday period gets into gear.

Crude inventories decreased by 12.2 million barrels, bringing the total to 448.5 million barrels for the week ending June 28, according to the EIA. This decline significantly exceeded analysts’ expectations in a Reuters poll, which had predicted a draw of 680,000 barrels.

This appears to confirm market participants’ recent optimism, suggesting that a reduction in inventories toward the end of the summer will likely lead to market tightness and support prices as Q4 approaches

The chart below shows US EIA inventory numbers based on the actual first release before revisions (yellow line). The (blue line) shows the expected inventory number based on Reuters polls.

Source: LSEG (click to enlarge)

US and Oil Rig Data Ahead

Today is likely to be a quiet one with the US independence day holiday and UK election. Liquidity might prove to be an issue and thus markets may experience sideways price action.

Friday could be a blockbuster end to the week, with NFP and jobs data from the US and the return of US markets. Baker Hughes oil rig data is also scheduled for release and could also impact oil prices ahead of the weekend.

Technical Analysis on Brent Crude Oil

Oil prices ran into resistance at 87.90 on Tuesday and looked set for retracement. The EIA data yesterday however, helped push oil prices back toward the key resistance level while printing a hammer candlestick on the daily timeframe.

This makes for an interesting day with bullish continuation and a break of 87.90 finally opening the door for an assault at the 90.00 psychological level. The recovery since the beginning of June has been steep with very little retracement, something which continues to concern me.

For now though, price action and EIA data support a move higher. Given the low liquidity environment expected today, there is a chance that oil fails to close above the 87.90 resistance level, in which case NFP data tomorrow could serve as a catalyst for either a push toward 90.00 or a retracement back toward the 85.00 handle.

Brent Crude Daily Chart, July 4, 2024

Source: TradingView.com (click to enlarge)

Key Levels to Keep an Eye on;

Support

- 86.21

- 85.00 (confluence area, MA, Psychological level and previous support)

- 83.70

Resistance

- 87.90 (last week’s highs)

- 90.00 (psychological level)

- 92.50

USD/CAD Breaks Key Support

On 25 June, we noted that the USD/CAD price had approached a crucial support level—the lower boundary of a converging triangle, which indicated a relative balance of supply and demand in the market during May.

Since then, the price has bounced twice from this level (as indicated by the arrow).

Today, as the USD/CAD chart shows, the exchange rate is breaking through this key support, indicating a disruption in balance.

This has been influenced by the weakness of the USD. According to Reuters, the US dollar has declined relative to other currencies due to weaker-than-expected US economic data released on Wednesday. These included a weak ISM Services PMI report and the ADP Non-Farm Employment Change report, which might suggest an economic slowdown.

How might the Canadian dollar's exchange rate change relative to the US dollar?

According to today's technical analysis of the USD/CAD chart:

→ the price is moving within a descending trend channel (shown in red). The median line of the channel may serve as a resistance level;

→ the fact that bulls attempted to push the price upwards, breaking the peak at Point 1, but failed—a bearish signal;

→ the sharp rise to Peak 2 was followed by an even sharper fall—a sign of bearish engulfing.

Therefore, the dominance of supply forces could lead to a continuation of the downward movement. It is not out of the question for the USD/CAD exchange rate to decline to the lower boundary of the red channel, with an attempt to break the May low around 1.359.

However, sharp movements are unlikely today due to the celebration of Independence Day in the USA.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

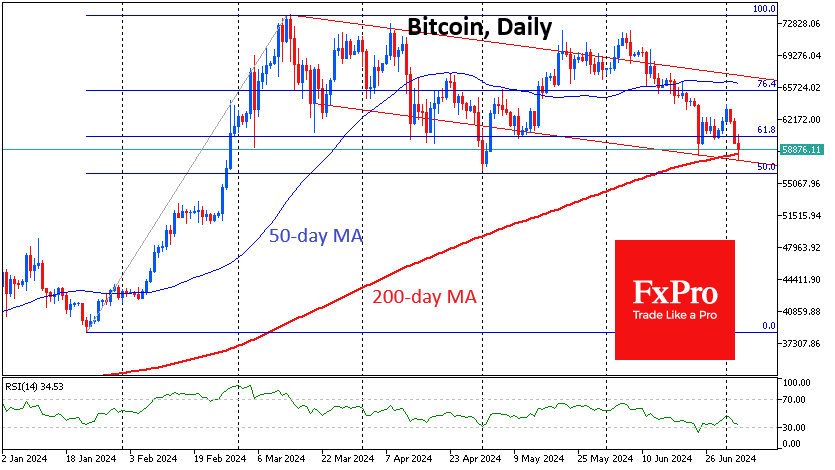

Bitcoin Falls Below $60k to a Two-Month Low

Upon analysing the long-term BTC/USD chart on 16 May, we constructed a "roadmap" for Bitcoin's price, which appeared as an expanding fan and consisted of a median with support levels below it and resistance levels above it.

Analysing the BTC/USD chart last time on 28 June, we pointed out that:

→ the price broke down through Support 1 following a series of weak bullish rebounds;

→ the price found support at the Support 2 line, forming a strong rebound from it on 24 June;

→ according to Marcus Thielen, founder of 10x Research, the BTC/USD rate could decline to $50,000.

How has the market situation changed over the week?

As shown by the BTC/USD chart today:

→ The price of Bitcoin has fallen below the psychological level of $60k;

→ It has also fallen below the 24 June low, marking the lowest point since 1 May.

Currently, the price is in close proximity to the 1 May low, creating a threat of a more significant decline to the price levels seen at the end of February 2024, when Bitcoin's price rapidly increased due to the influx of investors into ETF funds.

How realistic is this threat? Considering that the initiative is on the side of the bears, the scenario of further price decline is quite likely.

As today's technical analysis of the BTC/USD chart with updated data shows:

→ the price continues to decline within the red channel, staying in its lower half (a bearish sign);

→ the price has fallen below the Support 2 line, which may now act as resistance.

According to Coinglass, over the past 12 hours, more than $160 million worth of long positions have been liquidated on major cryptocurrency exchanges. Panic (and liquidation of longs) could intensify if the BTC/USD price falls below the May lows.

Support levels for Bitcoin's price could include:

→ the lower boundary of the red channel;

→ the psychological level of $55k;

→ the Support 3 line, which is part of the previously constructed "roadmap".

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*At FXOpen UK and FXOpen AU, Cryptocurrency CFDs are only available for trading by those clients categorised as Professional clients under FCA Rules and Professional clients under ASIC Rules respectively. They are not available for trading by Retail clients.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

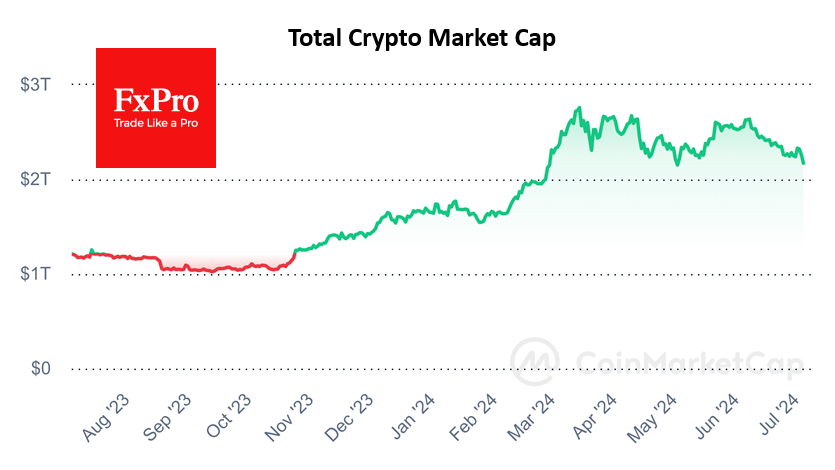

Bitcoin More Likely to Fall to $51.5K Than Rise to $65.8K

Market picture

The crypto market plunged 3.6% in 24 hours to $2.17 trillion, its lowest level since late February. Triggered stop orders in this morning’s thinly liquid market added to the magnitude of the decline, sending Bitcoin briefly below $57.7K and Ethereum to $3150. Top altcoins are losing in a range from -0.7% (Tron) to -9% (Solana).

Bitcoin has lost 9.5% in just over two days of selling. At its low point on Thursday morning, the price touched the lower boundary of the descending channel and dropped below the 200-day moving average but has so far been able to bounce back above it, trying to stay within established patterns. However, this has not been entirely successful, as the price is already below the 61.8% retracement level and has updated the lows from early May. From the current position, a 12% drop to $51.5k (February consolidation area) is more likely than the same amount of growth to $65.8k (50-day MA).

Solana underwent an intensified sell-off after touching the 50-day MA and is now testing support at the 200-day MA. As with Bitcoin, a break below would force the pair to target the late February lows as a potential next stop.

News background

Despite the correction, the options market is still heavily skewed towards BTC growth, as evidenced by the strong interest in long-term options at the $100,000-120,000 strike. According to QCP Capital, this points to the likelihood of a resumption of the rally by the end of the year.

According to River, by the end of the first quarter, 13 of the top 25 US hedge funds had invested in spot bitcoin ETFs. According to the research, 534 organisations—from hedge funds to pension and insurance companies—with more than $1bn in assets have invested in BTC ETFs. Specifically, 11 of the top 25 registered investment advisers and hundreds of smaller firms have placed money in the instrument.

VanEck said the launch of the Solana ETF is largely dependent on the outcome of the upcoming US presidential election and whether Gary Gensler remains at the helm of the SEC. The firm filed to launch such an ETF last week.

Nate Geraci, president of investment firm The ETF Store, suggested that the final Form S-1 filing could be approved by 12 July, opening the way for the Ethereum ETF launch on 15 July.

Despite the ban on cryptocurrency mining in the PRC, Chinese bitcoin mining pools hold 54% of the market share, said CryptoQuant CEO Ki Yun Ju. He suggested that the government could control several cryptocurrency mining pools.

Pump.fun, a Solana-based meme token launch platform, has surpassed Ethereum in terms of daily revenue, reaching $1.99 million. According to Dune Analytics, the platform issued an additional 11,528 tokens on 1 July, bringing its cumulative total to 1,199,685.

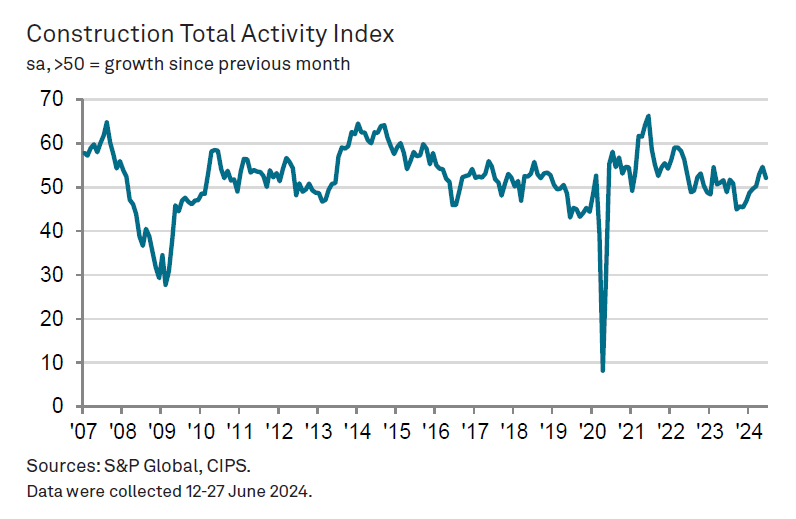

UK PMI construction falls to 52.2, slowing growth amid election uncertainty

UK PMI Construction fell to 52.2 in June, down from 54.7 in May, and below the expected 54.0. S&P Global highlighted the sharpest rise in employment in ten months, while inflationary pressures remained subdued.

Andrew Harker, Economics Director at S&P Global Market Intelligence, noted that the slowdown, particularly in housing activity, was partly due to "election uncertainty". He suggested that trends might improve once the election period ends.

Firms remain optimistic about the year-ahead outlook and increased employment significantly. Inflation pressures stayed low, encouraging firms to expand purchasing activity. Stable supply-chain conditions also supported this positive trend..

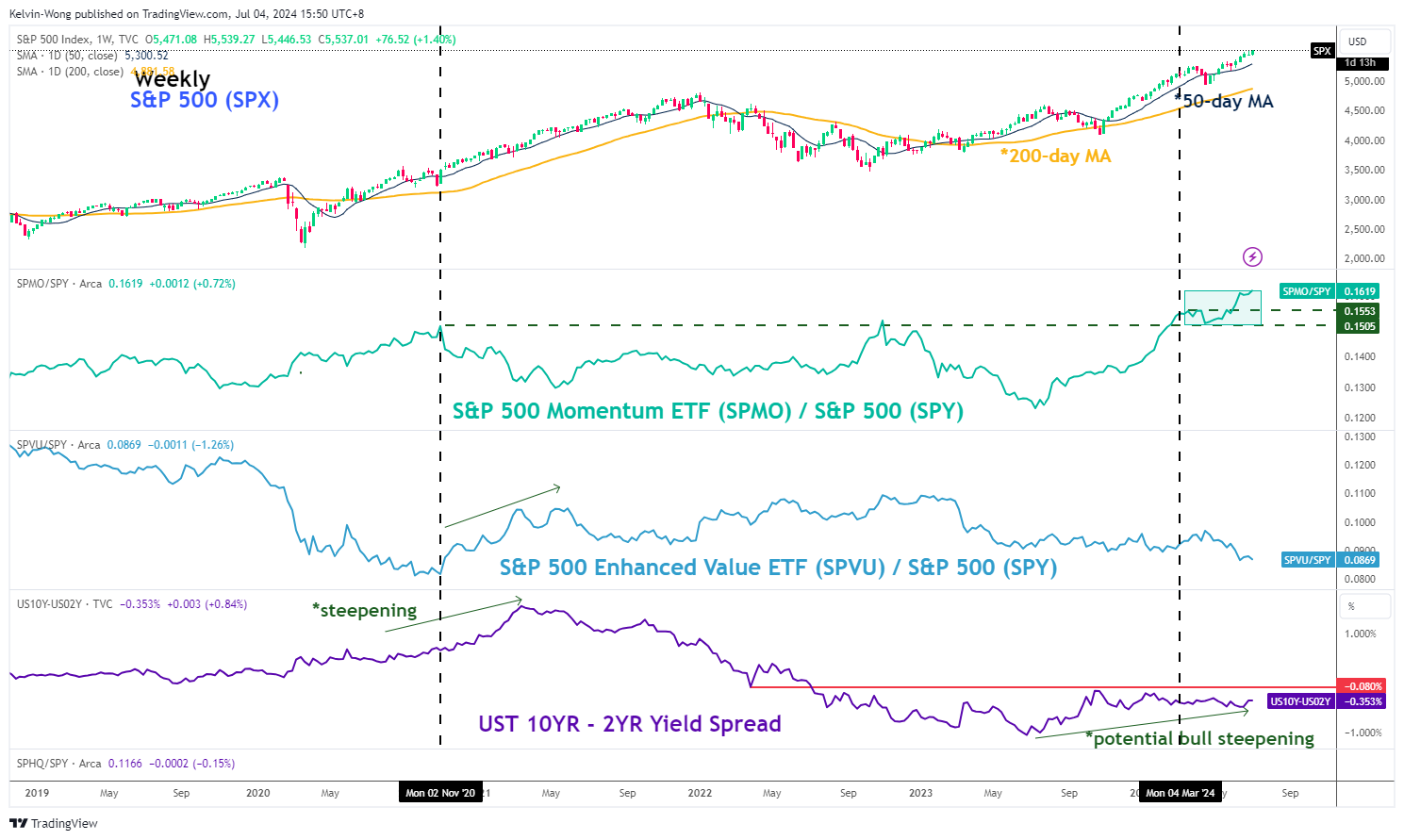

US DJIA: UST Yield Curve Un-inversion May Help the Laggard to Catch Up

- Yesterday’s lacklustre US ISM services PMI and ADP employment data for June increases the odds of a further US Treasury yield curve un-inversion.