Sample Category Title

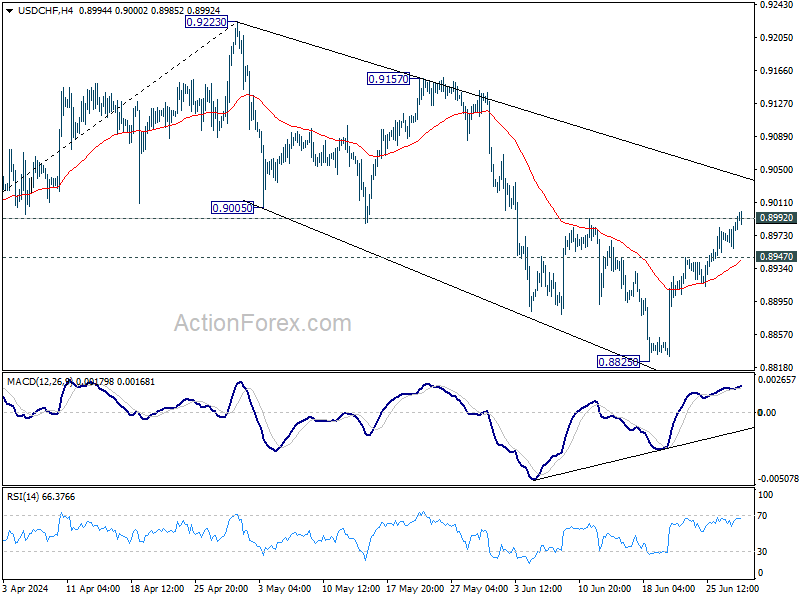

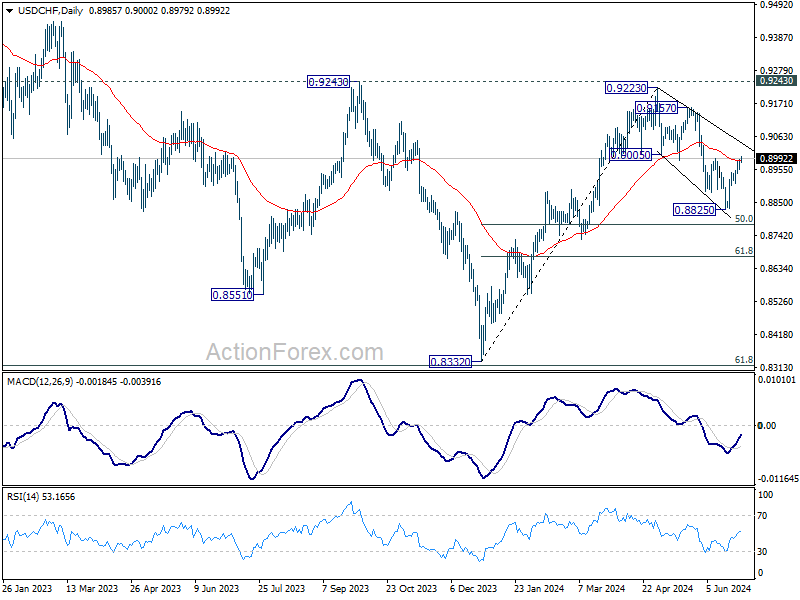

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8968; (P) 0.8979; (R1) 0.9000; More…

The break of 0.8992 resistance now argues that fall from 0.9223 has completed as a three-wave corrective move to 0.8825. Intraday bias is back on the upside for channel resistance (now at 0.9043). Firm break there will target 0.9157 resistance next. On the downside, below 0.8947 minor support will turn intraday bias neutral gain first.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

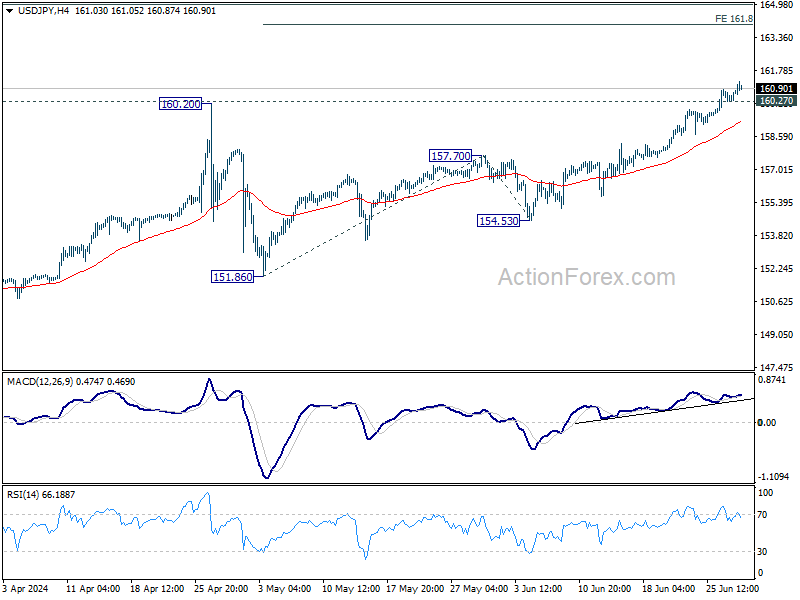

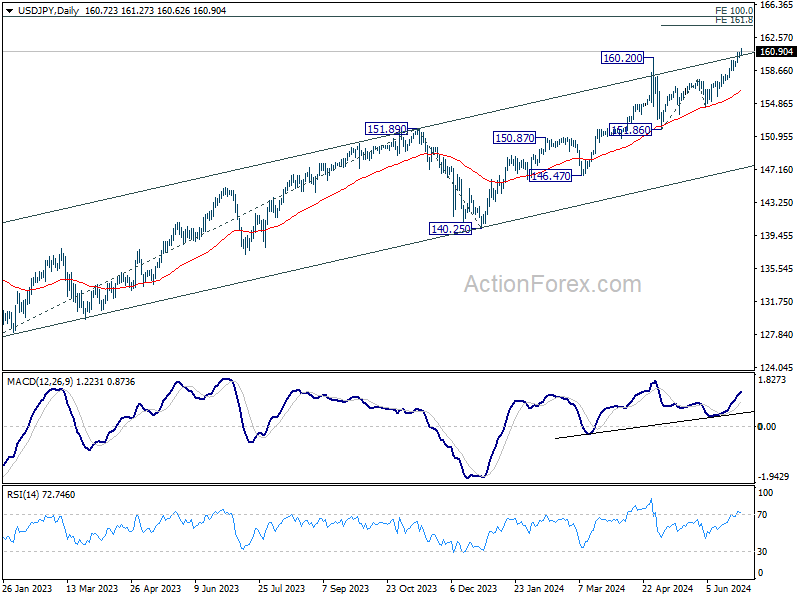

USD/JPY Daily Outlook

Daily Pivots: (S1) 160.43; (P) 160.63; (R1) 160.98; More...

USD/JPY's rally continues today and intraday bias stays on the upside. Next target is 161.8% projection of 151.86 to 157.70 from 154.53 at 163.97. On the downside, below 60.27 minor support will turn intraday bias neutral again first. But outlook will stay bullish as long as 157.70 resistance turned support holds.

In the bigger picture, there is no sign of long term trend reversal yet. Further rally is expected as long as 151.86 support holds. Decisive break of 160.02 will target 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

USD Losses Could be Balanced by Both Euro Caution and Tricky Risk Sentiment

Markets

The US Treasury sell-off from Tuesday and especially Wednesday, ended with the early US eco data yesterday. Disappointing and weak durable goods orders (especially the series used for GDP calculations) and a significant downward revision for personal consumption (1.5% Q/Qa instead of 2%) in the final release of Q1 GDP directed a bid into Treasuries. The final US debt sale of the week ($44bn 7-yr note auction) was strong and offered no way back for US T’s. Overnight, they showed some marginal signs of weakness again during the Biden/Trump debate. The onus wasn’t on atmospheric fiscal trajectories (as warned by the IMF as well; see below), but on Biden’s (physical) performance. It seems that the president was thrown under the bus. A dismal performance in the next election poll could pave the way for eventually putting someone else’s name on the Democratic ticket.

US May PCE deflators today kick-off a string of important US eco numbers. Following earlier released CPI data, we can expect a benign outcome. Headline and core CPI respectively were flat and 0.2% higher on the month, coming in below consensus and significantly slowing the paces recorded in the first four months of the year. Personal income and spending data are also worth watching. Especially spending given recent weakness in retail sales. Data might thus be supportive for US Treasuries and core bonds in general. Some final end-of-quarter repositioning and a preference to err on the safe side going into this weekend’s first round of French parliamentary elections also support that view. The combination of both suggests that USD losses in case of weaker figures could be balanced by both euro caution and a tricky risk sentiment. After today’s PCE deflators, ISM surveys, ADP employment change and US payrolls are lining up next week. Following some labour market warnings by top Fed officials this week (Daly, Cook), risks turn asymmetric for the labour figures with any signs of weakness likely resulting in markets pushing harder for a September rate cut and a faster path downward in 2025. National EMU CPI data (France, Italy, Spain) will set the tone for EMU figures out Tuesday.

News & Views

The Czech National Bank yesterday cut its policy rate by 50 bps, bringing the two-week repo rate at 4.75% with 5 members supporting the decision while two MPC members preferred a 25 bps reduction. Analyst expectations in the run-up to the meeting also split between continuing with a 50 bps or downscaling to a 25 bps cut. The CNB indicated that the fight against inflation isn’t over even as it started lowering rates. Policy must remain tight to keep inflation close to the target in the long term. After yesterday’s decision, real yields remain significantly positive, dampening inflation. Czech inflation returned to 2% in February and since moved back up in the upper halve of the 1% tolerance band around the 2% target. As rates gradually approach neutral levels, the CNB will likely slow the pace of moderation of policy restriction at the meetings ahead or keep rates unchanged for some time if necessary. The MPC will base its decisions on an assessment of newly available data and their implications for the inflation outlook. Markets interpreted the decision as tilting to the dovish side. The Czech 2-y swap yield declined 6 bps. The Czech koruna weakened from near EUR/CZK 24.91 to close the session at 25.06.

In a regular review under an article IV consultation, the IMF assessed that the US economy has proven to be robust, dynamic and adaptable to changing global conditions. Activity and employment continue to exceed expectations and the disinflation process has been considerably less costly than many had feared. At the same time, the Fund concludes that the fiscal deficit is too large, creating a sustained upward trajectory for the public debt-GDP ratio. Specifically, under current policies, the general government debt is expected to rise steadily and exceed 140% of GDP by 2032. To put debt-to-GDP on a clear downward trajectory, a frontloaded fiscal adjustment will be needed that shifts to a general government primary surplus of around 1% of GDP (an adjustment of around 4% of GDP relative to the current baseline). In order to reach this, policies will need to go beyond finding efficiencies in discretionary, non-defense federal spending. Policymakers will need to carefully consider raising indirect taxes, progressively increasing income taxes eliminating a range of tax expenditures, and reforming entitlement programs, the Fund assesses.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative (France) dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield is testing the downside of the 4.2/4.7% trading range.

EUR/USD

EUR/USD is stuck in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

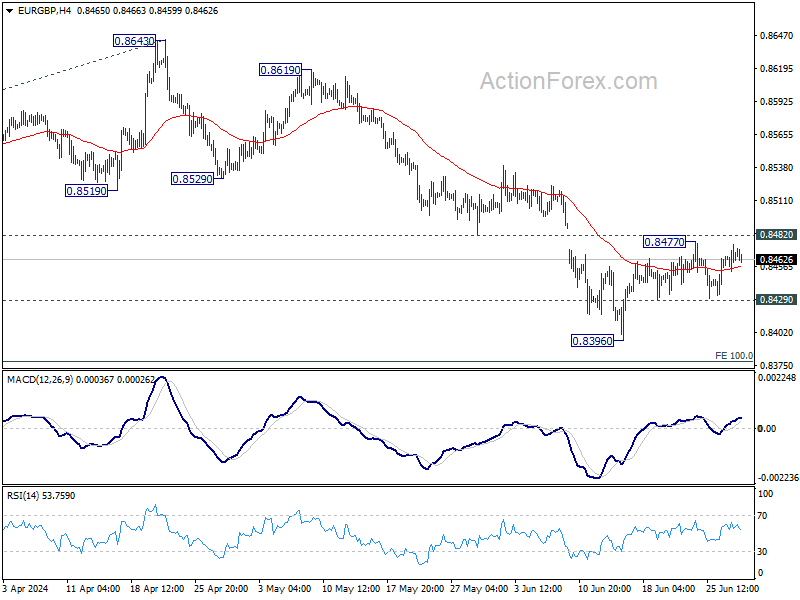

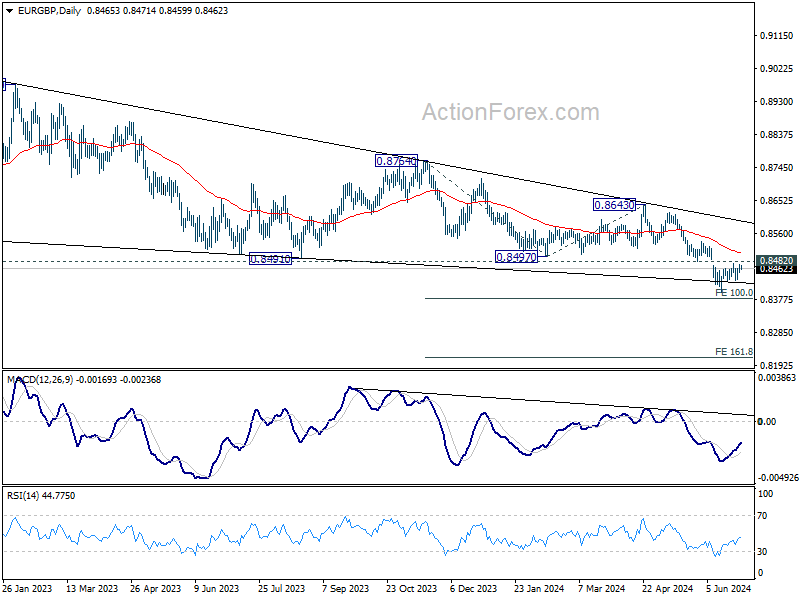

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. This might cap further sterling gains. At the same time, the euro remains vulnerable to political event risk going into the French elections. EUR/GBP 0.84 is becoming solid support.

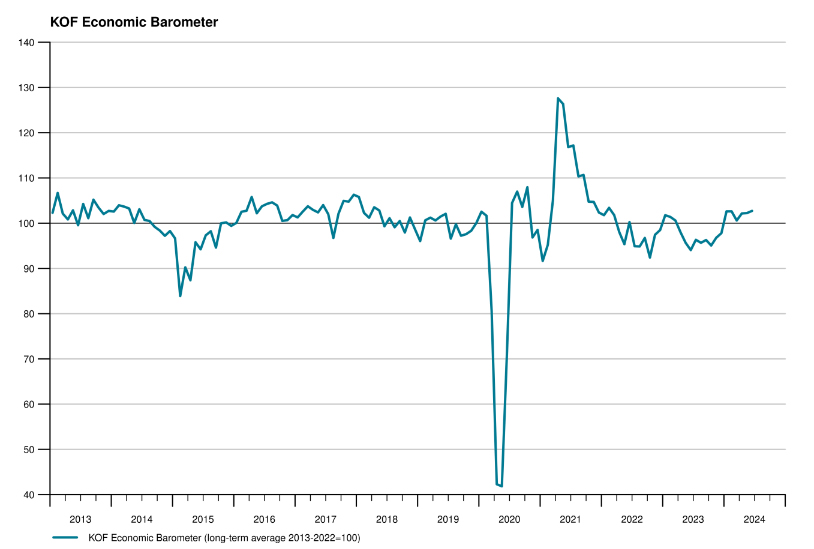

Swiss KOF rises slightly to 102.7, gradual recovery continues

Swiss KOF Economic Barometer rose from 102.2 to 102.7 in June, surpassing expectations of 100.5. According to KOF, the Swiss economy is projected to "continue to recover little by little over the coming months."

This increase is largely driven by a more favorable outlook for foreign demand. Additionally, the hospitality industry is expected to see stronger benefits. The indicators for manufacturing, construction, and private consumption remained virtually unchanged in June. However, the outlook for financial and insurance services, along with other service sectors, has slightly dimmed.

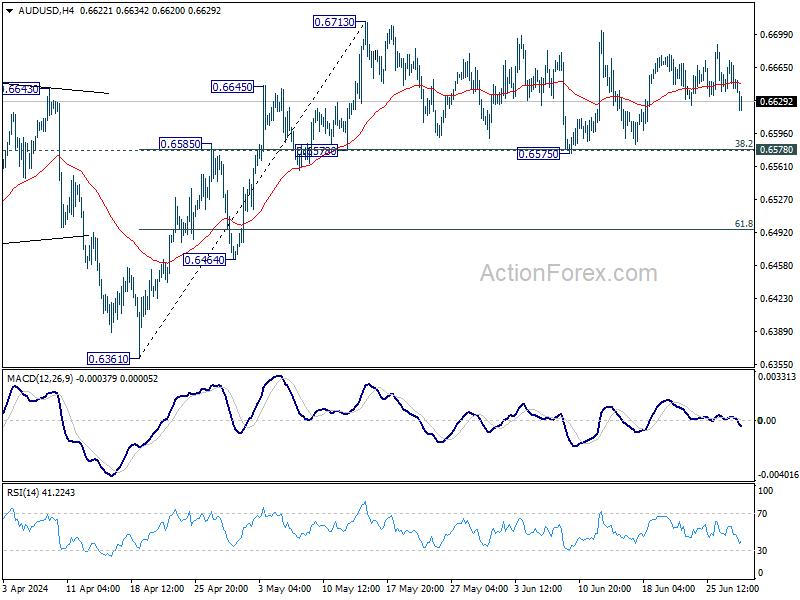

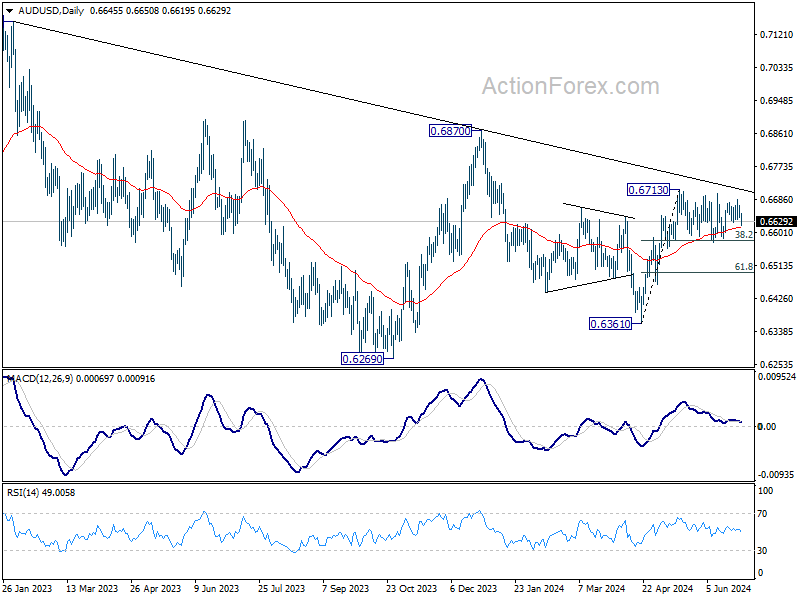

AUD/USD Daily Report

Daily Pivots: (S1) 0.6634; (P) 0.6654; (R1) 0.6667; More...

AUD/USD is still extending sideway consolidation from 0.6713 and intraday bias remains neutral. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

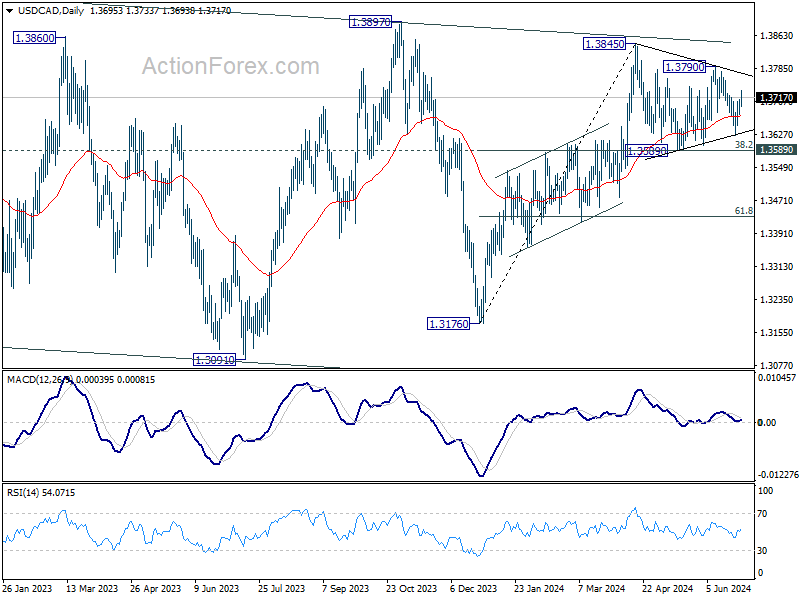

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3681; (P) 1.3696; (R1) 1.3717; More...

Current strong rebound suggests that USD/CAD's fall from 1.3790 has finished at 1.3626. Intraday bias is back on the upside for 1.3790 resistance. Firm break there should indicate that consolidation from 1.3845 has completed with three waves to 1.3626. Retest of 1.3845 high should be seen next. On the downside, below 1.3675 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8456; (P) 0.8466; (R1) 0.8478; More...

No change in EUR/GBP's outlook and intraday bias remains neutral. Further decline is expected with 0.8482 support turned resistance intact. On the downside, below 0.8429 minor support will bring retest of 0.8396 low first. Further break there will resume larger down trend to 0.8376 projection level next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

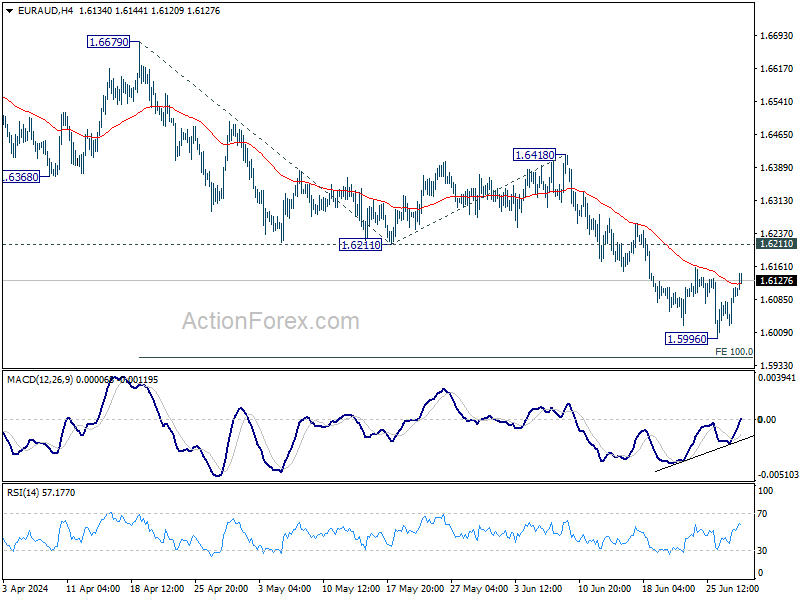

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6046; (P) 1.6081; (R1) 1.6135; More...

Intraday bias in EUR/AUD is turned neutral first with current recovery. Some more consolidations could be seen first, but outlook will stay bearish as long as 1.6211 resistance holds. Below 1.5996 will target 100% projection of 1.6679 to 1.6211 from 1.6418 at 1.5950. Firm break there will target 1.5846 key support next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor at a later stage.

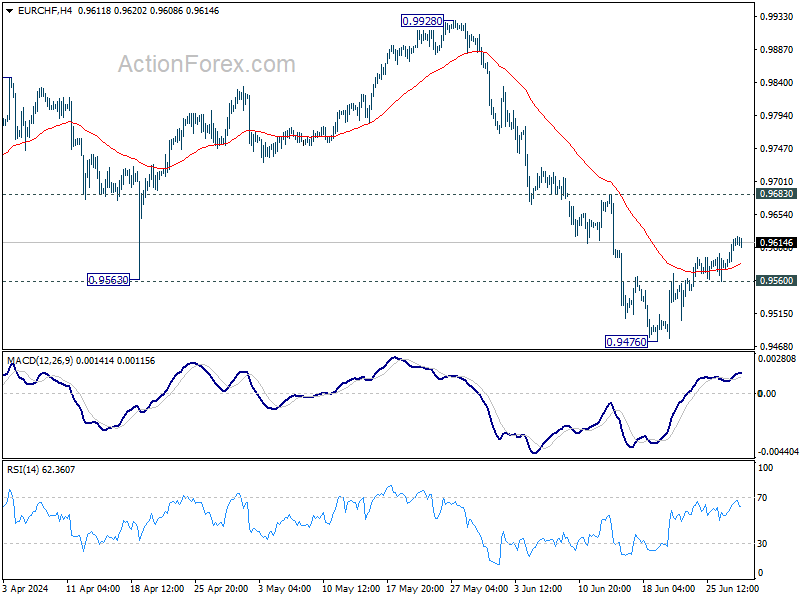

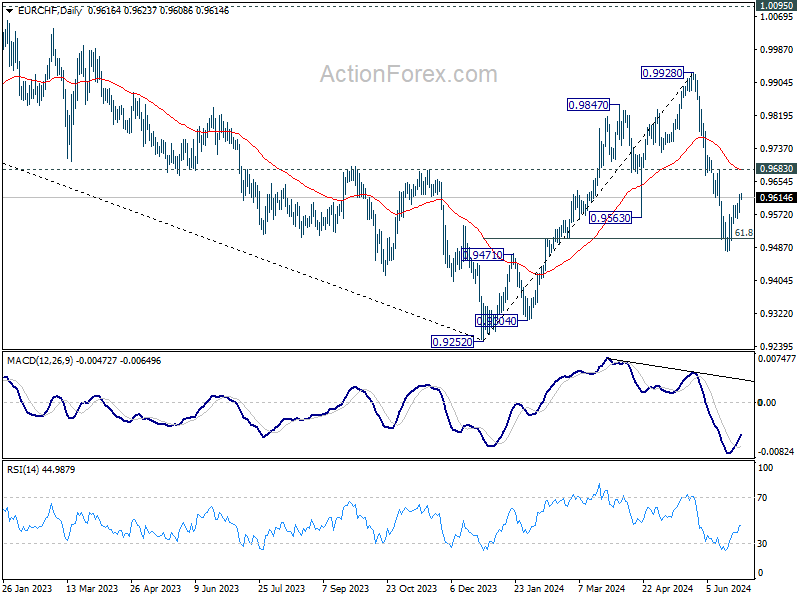

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9592; (P) 0.9607; (R1) 0.9636; More....

Intraday bias in EUR/CHF remains neutral and outlook is unchanged. Further decline is expected as long as 0.9683 resistance holds. On the downside, break of 0.9476, and sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will bring retest of 0.9252 low next.

In the bigger picture, rebound from 0.9252 should have completed at 0.9228. Medium term outlook remains bearish with 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

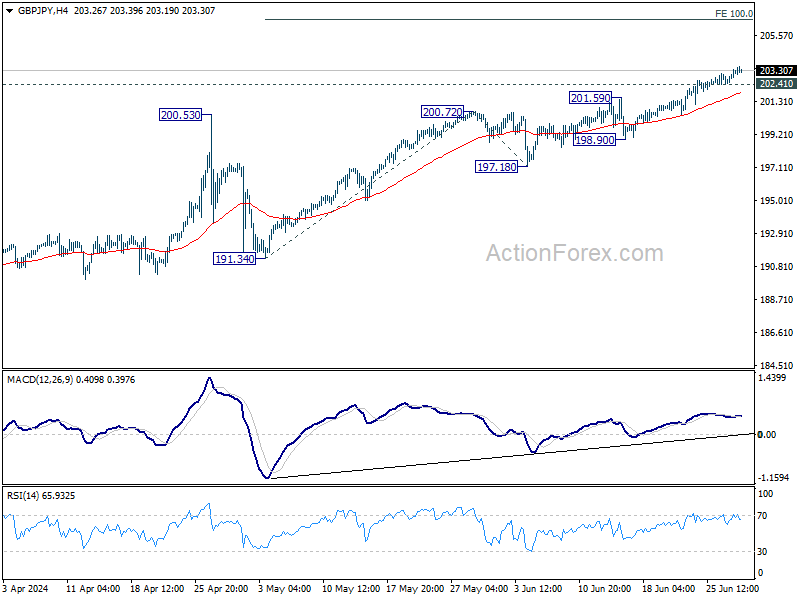

GBP/JPY Daily Outlook

Daily Pivots: (S1) 202.69; (P) 203.04; (R1) 203.58; More...

Intraday bias in GBP/JPY remains on the upside at this point. Current rally should target 100% projection of 191.34 to 200.72 from 197.18 at 206.56 next. On the downside, below 202.41 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 200.72 resistance turned support holds, in case of retreat.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 191.34 support holds, even in case of deep pullback.