Sample Category Title

Canadian Dollar Edges Higher Ahead of Retail Sales

- Canada to release retail sales today, GDP on Friday

- US GDP expected to confirm estimate 5.2% gain

The Canadian dollar is slightly higher on Thursday. In the European session, USD/CAD is trading at 1.3324, down 0.19%.

Canadian retail sales, GDP expected to improve

It’s a busy end of the week for Canadian releases, with retail sales today and the GDP on Friday. Both indicators are expected to accelerate, which could give a boost to the Canadian dollar. The US releases third-estimate GDP for the third quarter, which is expected to confirm the previous estimate of 5.2%.

Canada’s retail sales are showing some strength, raising hopes that the Christmas season will be marked by strong consumer spending. In September, retail sales grew by 0.6%, which was the fastest growth rate in five months. The consensus estimate for October stands at 0.8% m/m.

The economy has not looked all that strong, although fears of a shallow recession failed to materialize as the economy posted weak growth in the third quarter. September GDP came in at just 0.1% m/m and October is expected to tick up to 0.2%.

The manufacturing sector is in a slump, as domestic activity has been weak and global demand for Canadian products has decreased. Manufacturing Sales slipped 2.8% m/m in October and the November data will be released on Friday.

Inflation has fallen to around 3% but is proving to be stubborn as the Bank of Canada tries to bring it back down to the 2% target. The BoC has signalled that it expects inflation to remain sticky and has projected an inflation rate of 3.5% through the middle of 2024. The central bank has paused rates three straight times and with a sputtering economy, there isn’t much reason to hike rates, which makes the BoC’s rate hike warnings appear rather hollow.

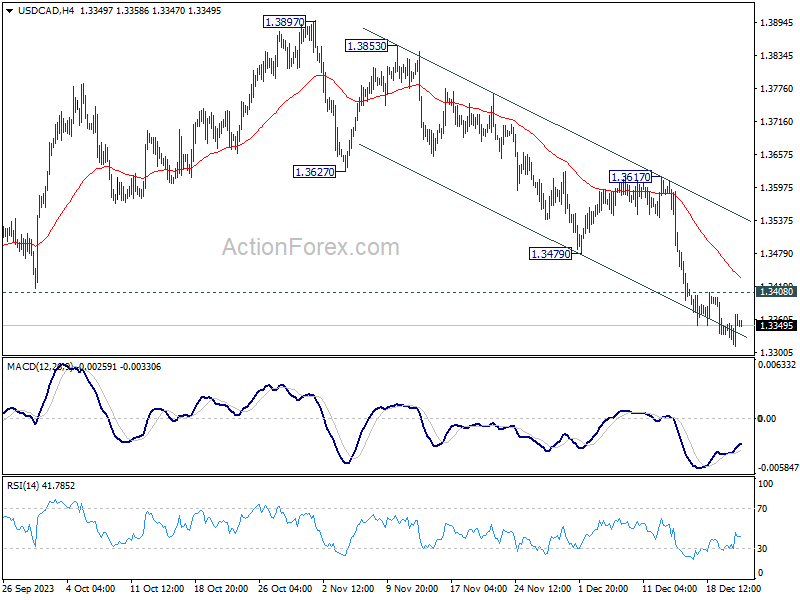

USD/CAD Technical

- USD/CAD is testing support at 1.3350. Below, there is support at 1.3281

- There is resistance at 1.3450 and 1.3550

ECB’s de Guindos: Premature for rate cut discussions, emphasizes Europe’s growth challenge

In an interview with 20 Minutos, ECB Vice President Luis de Guindos emphasized that it is "too early" to discuss rate cuts, despite recent favorable data. He stressed that the data available are still insufficient for ECB to alter its current monetary policy stance for now.

De Guindos highlighted ECB's data-dependent approach: "We are data-dependent. The data have been favorable but still not enough for us to change our monetary policy."

He also expressed confidence in the current interest rate levels, stating, "If sustained for a sufficiently long period of time, current interest rates will help bring inflation down to 2%."

Addressing the prospect of a recession, de Guindos noted that ECB does not anticipate a technical recession, defined as two consecutive quarters of negative growth. However, he acknowledged a broader structural growth issue within Europe's economy. ECB's projections, along with those of European Commission, foresee only modest growth of around 1% until 2026.

De Guindos identified low productivity and the energy crisis as key challenges hindering Europe's economic competitiveness, particularly given Europe's reliance on energy imports. He argued for the necessity of structural reforms to address these issues.

While ECB's focus remains on reducing inflation, de Guindos emphasized that achieving growth requires a broader set of solutions: "Structural reforms are therefore necessary. The aim of monetary policy is to reduce inflation, but to achieve growth, other factors must be brought into play."

After BoJ Decision, Yen Traders Turn to CPIs and Summary of Opinions

- BoJ keeps policy ultra-loose, does not hint at change

- Friday’s data may reveal slowdown in inflation

- Wage negotiations key for exiting negative rates

- Next week’s Summary of Opinions also in focus

Yen traders turn attention to national CPI numbers

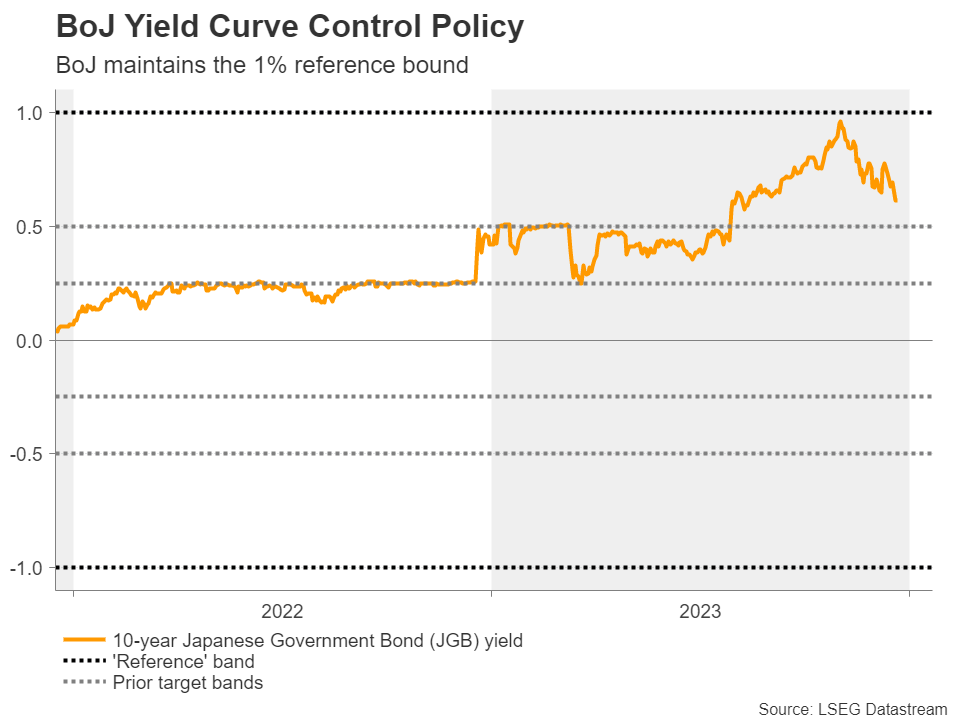

On Tuesday, the Bank of Japan decided unanimously to keep interest rates untouched at -0.1% and stick to its yield curve control policy framework that places an upper bound of 1% for the 10-year Japanese government bond yield as reference. With the Bank giving no signals that the era of ultra-loose policy conditions is nearing its end, yen traders were largely disappointed, with the currency turning south again.

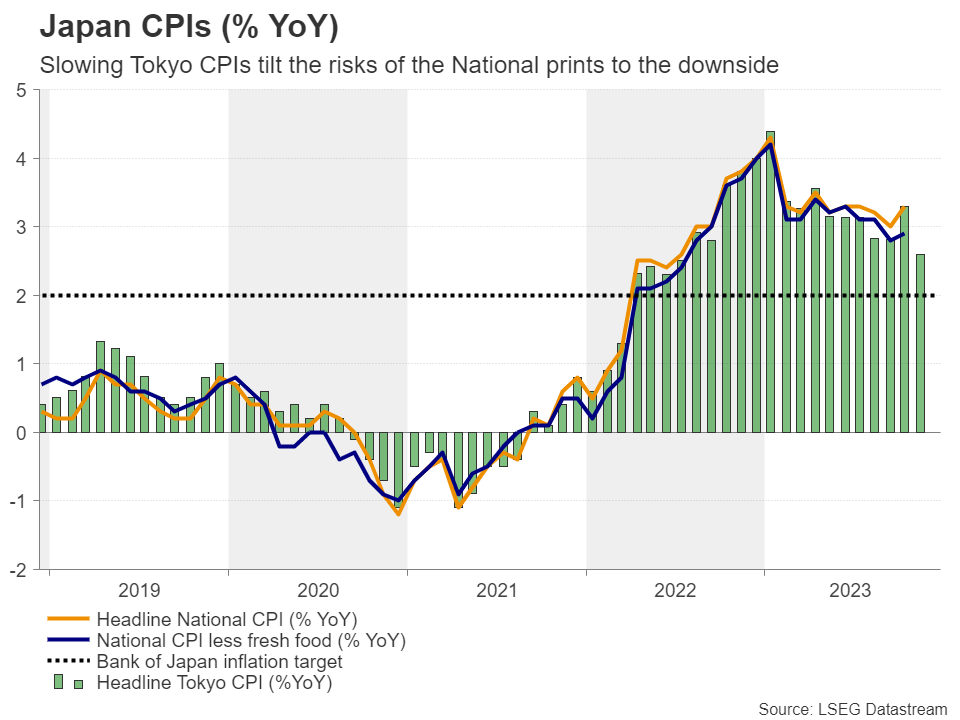

Whether the slide will continue for a while longer or not may depend on the national inflation numbers for November, due out during the Asian session Friday, and the core one is anticipated to have declined to 2.5% y/y from 2.8%. The Tokyo CPI data for the month revealed notable slowdowns in both headline and core consumer prices, corroborating the forecast for the National core CPI and suggesting that the headline rate may have also declined.

Will a slowdown impact BoJ’s pivot decision?

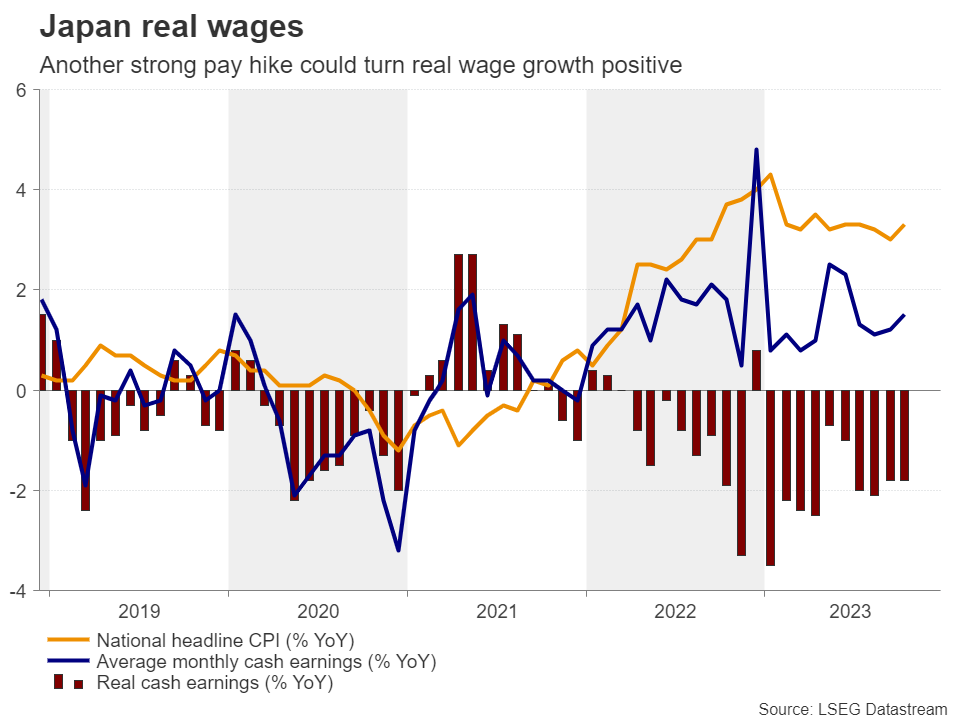

That said, a slowdown in inflation may not necessarily mean that the BoJ will dismiss the idea of raising interest rates at some point in the months to come as both metrics are still lying above the Bank’s 2% objective. What’s more, the Bank is paying very close attention to wage growth and a meaningful acceleration may be the signal for policymakers to take interest rates out of negative territory.

With that in mind, a very likely month for doing so may be April, just after next year’s spring wage negotiations. In October, Japan’s umbrella labor union, Rengo, said that they will demand hikes of at least 5%, which could take real wage growth into positive territory. Considering that the market expects the Fed to cut interest rates by around 150bps next year, this may allow the yen to stay in uptrend mode against its US counterpart, even if the latest slide continues for a while longer.

Summary of Opinions could reveal more

Governor Ueda gave no clear signals on when the Bank could exit negative rates on Tuesday, saying that they will not rush into raising rates just because the Fed could start cutting in a few months, adding that if they were to act, interest rates would only rise slightly. Yet, the market assigns a nearly 40% chance for a minor rate increase at the January meeting, with that percentage rising to 80% in April.

Perhaps investors are hoping to get more clarity from the meeting’s Summary of Opinions next week, on Wednesday. Back in October, some members discussed the conditions and possible timing of a future exit from negative interest rates, but the November summary highlighted that the Bank needs to patiently continue with monetary easing. If the December one reveals that there is a fresh discussion on the matter, then the yen could stage a decent comeback.

Dollar/yen rebounds, but stays in downtrend

From a technical standpoint, despite the latest recovery, dollar/yen remains below the downtrend line drawn from the high of November 13. What’s more, Tuesday’s advance was halted near the 144.00/80 zone, with the price returning below the 200-day exponential moving average thereafter. This means that the bears could take charge again at some point soon and perhaps aim for another test near the 141.50 territory. A break lower could confirm a lower low and perhaps see scope for extensions towards the next key support area at around 138.00.

On the upside, a break above 146.50 could turn the outlook neutral, while the move signaling that the bulls are in full control may be a break above 148.75, as it may confirm the pair’s return above the prior uptrend line drawn from the low of March 24.

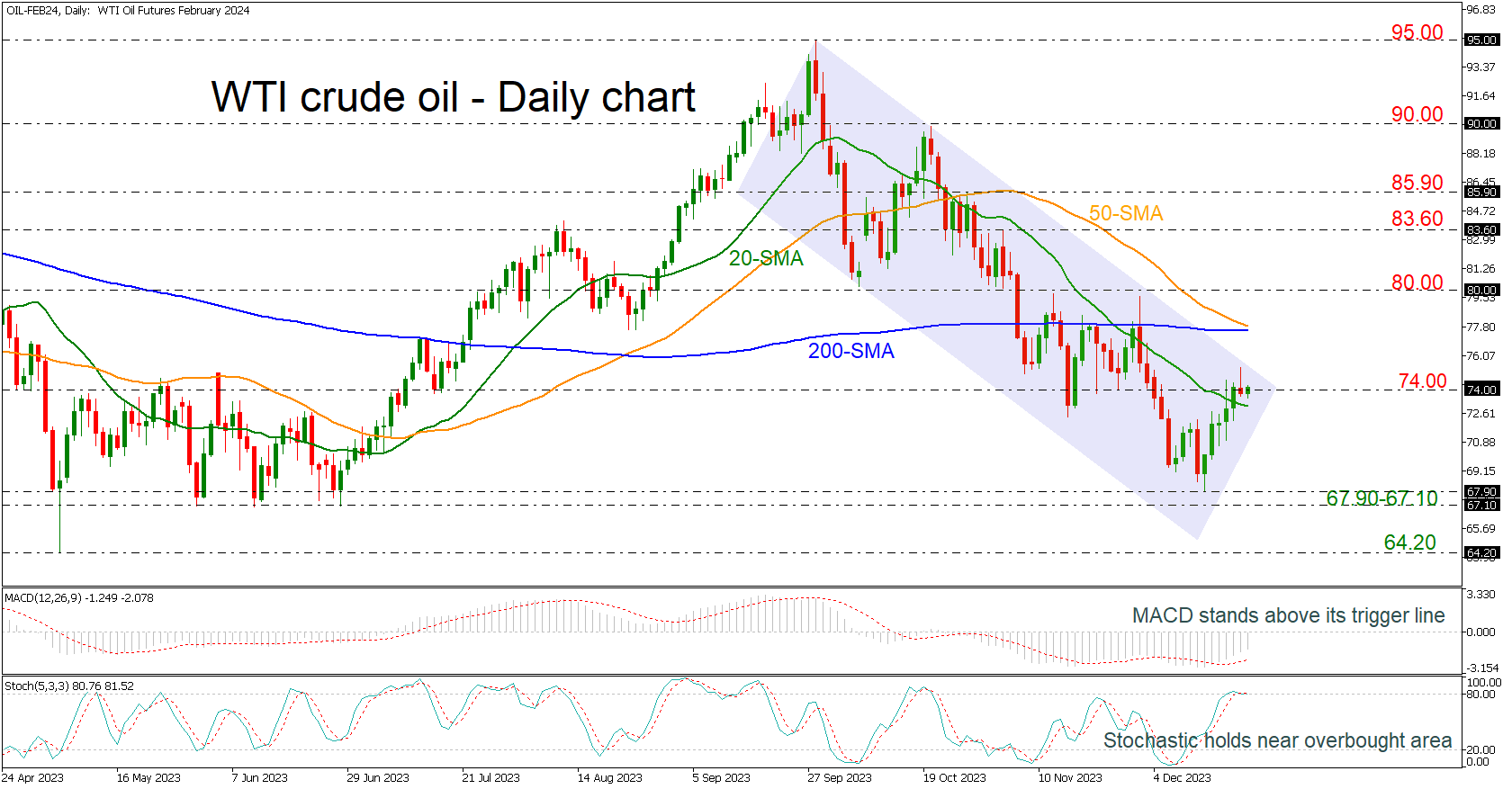

WTI Crude Oil Hovers Near the Upper Boundary of the Channel

- WTI crude attempts to surpass 74.00

- Immediate resistance near 200-day SMA

- Stochastic looks overbought

WTI crude oil futures are battling with the 74.00 round number, within a downward sloping channel that has been drawn since September 28.

Technically, the MACD is advancing above its trigger line in the negative territory, while the stochastic oscillator is still standing near the 80 level, indicating that the market may be in an overbought territory.

Steeper increases could penetrate the descending channel to the upside, heading towards the flat 200-day simple moving average (SMA) at 77.56, which also lies near the 50-day SMA. Even higher, the bulls may test the 80.00 handle, adding some optimism for more bullish actions.

On the flip side, a failure to surpass the 74.00 barrier could take the market beneath the 20-day SMA, resting near the 67.90-67.10 support. A dive below this restrictive region could confirm the bearish structure taking the price towards the 64.20 support, taken from the low on May 4.

To sum up, oil prices are showing some signs of a bullish correction but they need to climb above the channel and the 200-day SMA.

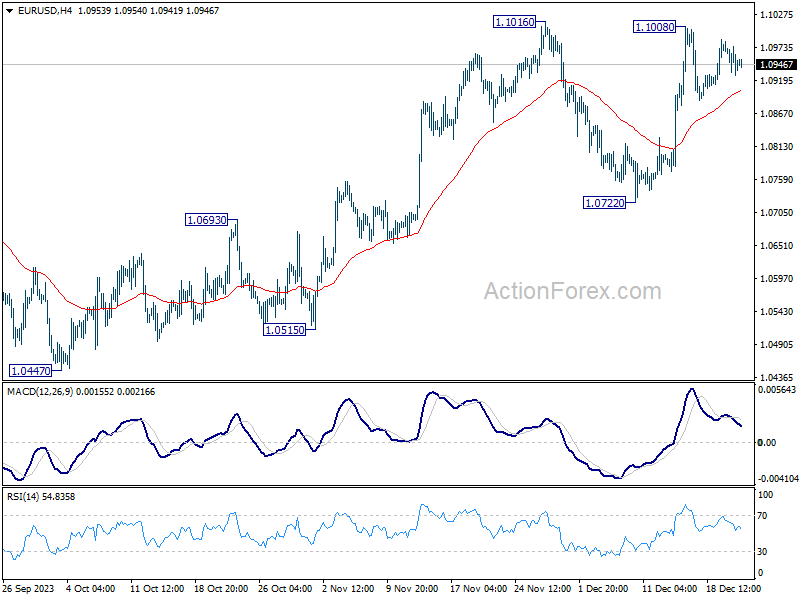

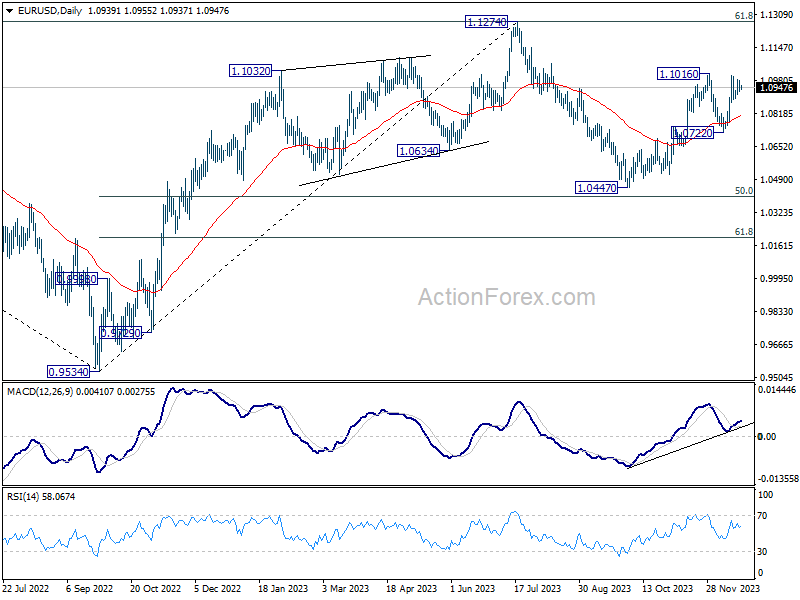

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0920; (P) 1.0953; (R1) 1.0975; More...

Intraday bias in EUR/USD remains neutral as consolidation from 1.1008 is still extending. Further rally is expected as long as 1.0722 support holds. On the upside, break of 1.1016 will resume the whole rise from 1.0447 to retest 1.1274 high.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

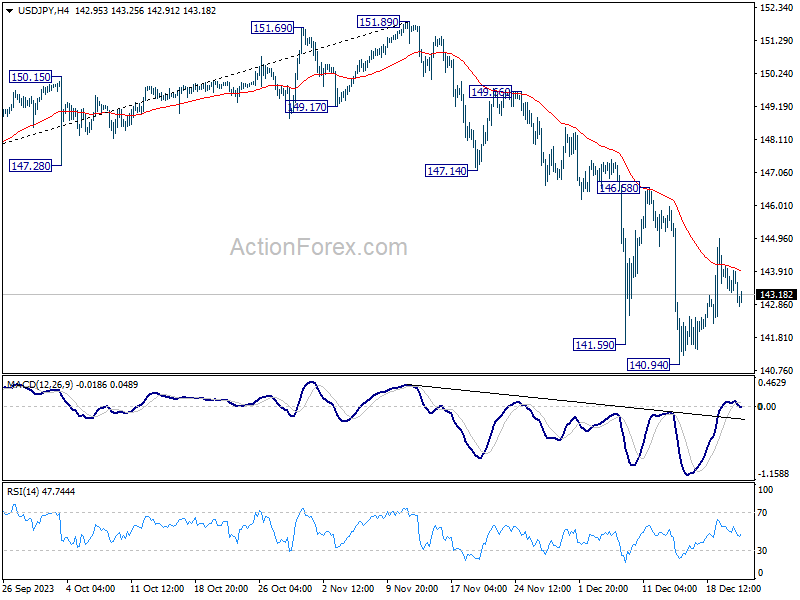

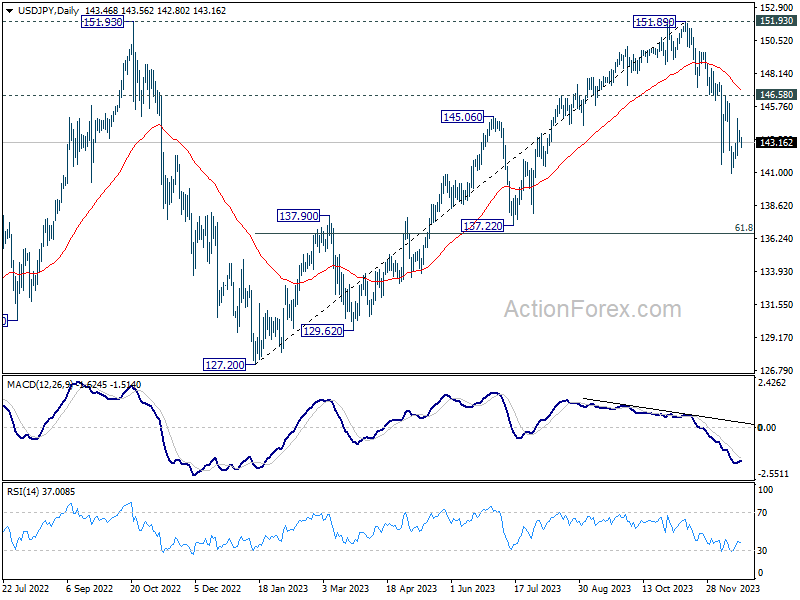

USD/JPY Daily Outlook

Daily Pivots: (S1) 143.18; (P) 143.64; (R1) 144.02; More...

Intraday bias in USD/JPY stays neutral for the moment, as consolidation from 140.94 is extending. Upside of current recovery should be limited below 146.58 resistance to bring another decline. Firm break of 140.94 will resume the whole fall from 151.89. Next target will be next fibonacci level at 136.63.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

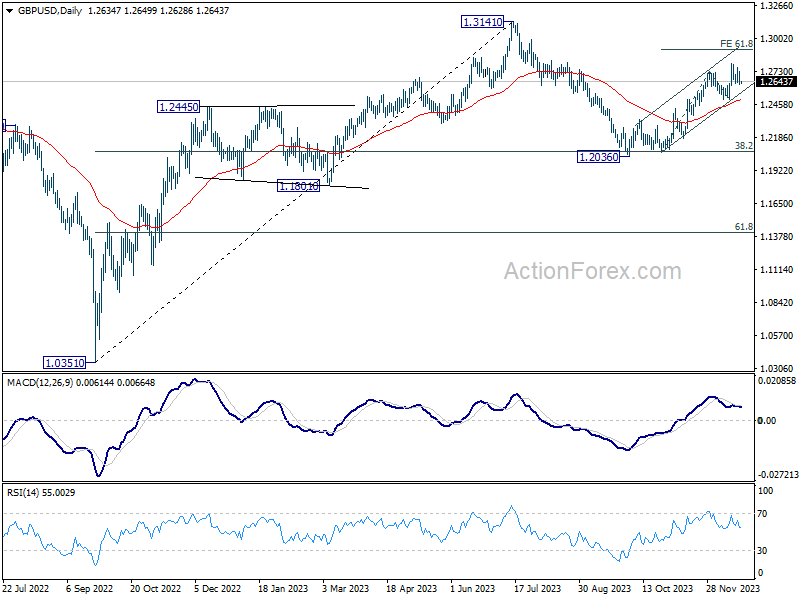

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2596; (P) 1.2667; (R1) 1.2710; More...

Intraday bias in GBP/USD remains neutral for the moment as consolidation from 1.2793 is extending. While sideway trading could extend, further rally is still expected as long as 1.2499 support holds. . On the upside, firm break of 1.2793 will resume the rally from 1.2036. Next target is 61.8% projection of 1.2068 to 1.2731 from 1.2499 at 1.2909.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

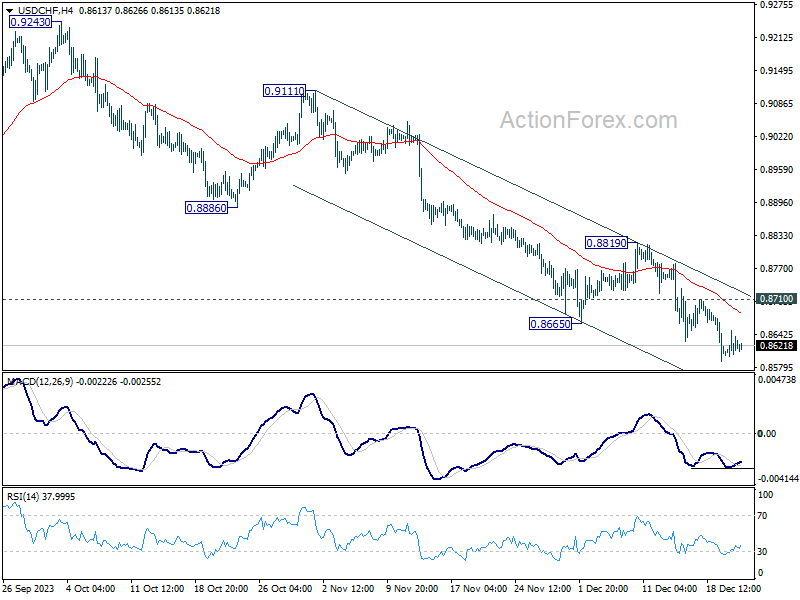

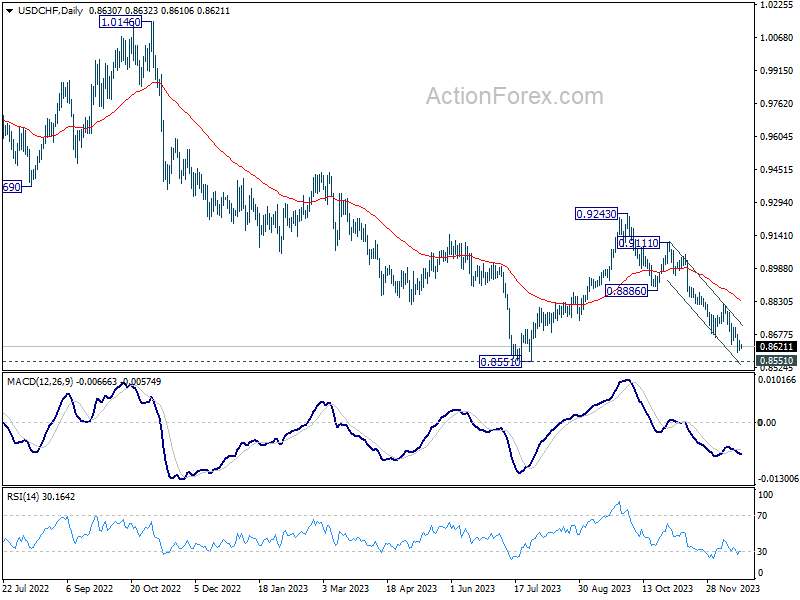

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8599; (P) 0.8625; (R1) 0.8654; More....

Further decline is expected in USD/CHF as long as 0.8710 resistance holds. Current fall from 0.9243 is in progress for retesting 0.8551 key support next. On the upside, however, break of 0.8710 will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 0.8551 are currently seen as a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Strong support should be seen 0.8551 to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243.

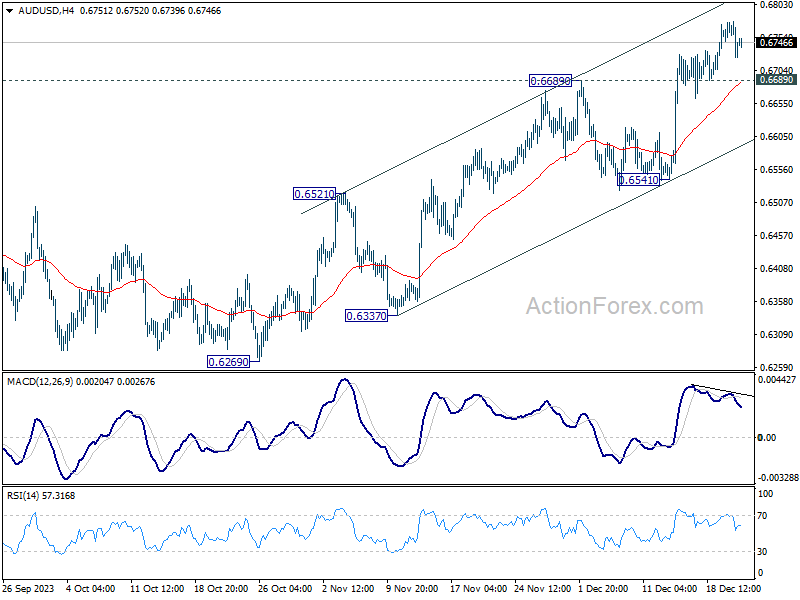

AUD/USD Daily Report

Daily Pivots: (S1) 0.6710; (P) 0.6744; (R1) 0.6765; More...

Further rally is in favor in AUD/USD as long as 0.6689 support holds. Rise from 0.6269 would target 0.6894 resistance first. Sustained break there will target 0.7156 next. Nevertheless, break of 0.6689 will indicate short term topping, and turn bias back to the downside for deeper pull back

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. Price actions from 0.6169 (2022 low) could be just a medium term corrective pattern. Rise from 0.6269 is seen as the third leg of the pattern. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

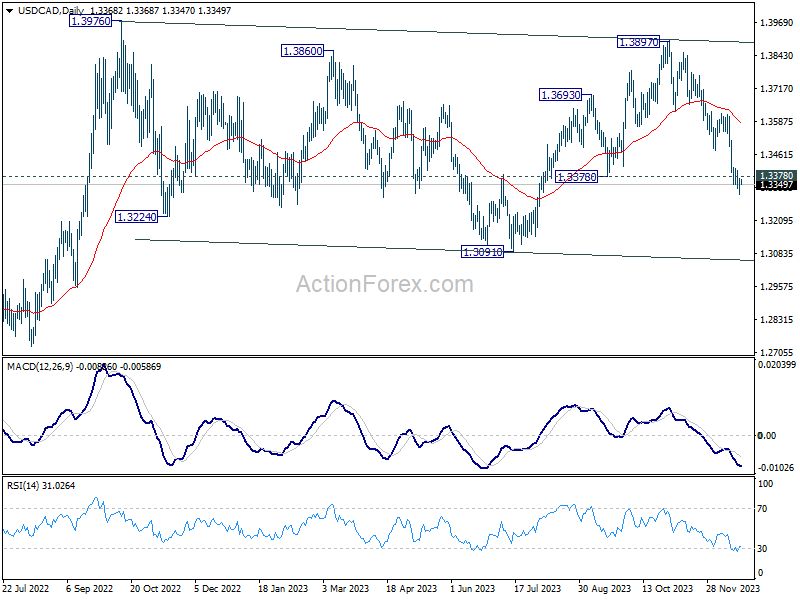

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3330; (P) 1.3350; (R1) 1.3388; More...

Further decline is expected in USD/CAD as long as 1.3408 minor resistance holds. Fall from 1.3897 would target a retest on 1.3091 support. Nevertheless, break of 1.3408 will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, outlook is mixed up by deeper then expected fall from 1.3897. But after all, price actions from 1.3976 (2022 high) are viewed as a corrective pattern that's in progress. Larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage as long as 1.2947 resistance turned support holds.