Sample Category Title

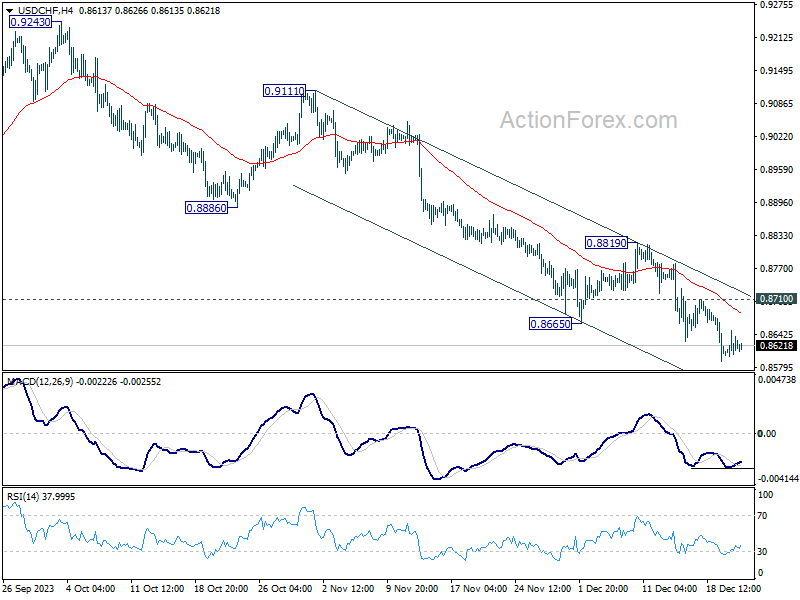

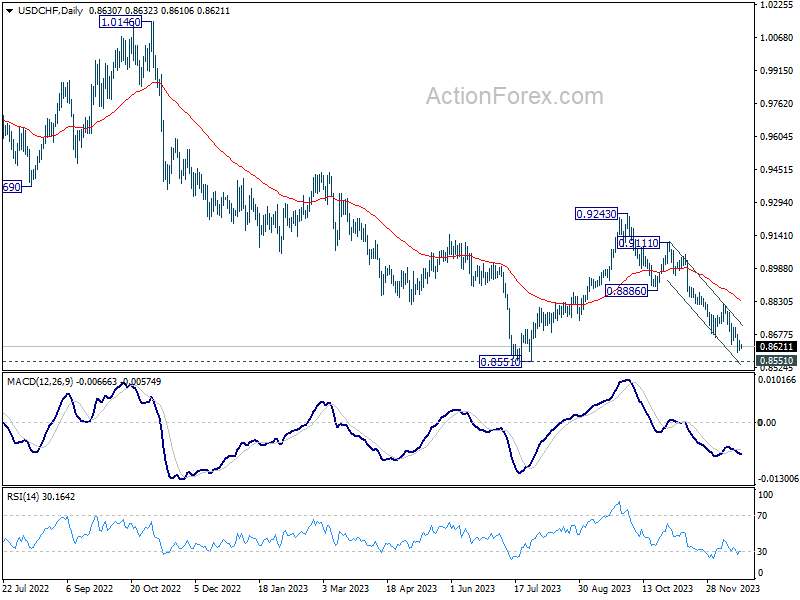

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8599; (P) 0.8625; (R1) 0.8654; More....

Further decline is expected in USD/CHF as long as 0.8710 resistance holds. Current fall from 0.9243 is in progress for retesting 0.8551 key support next. On the upside, however, break of 0.8710 will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 0.8551 are currently seen as a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Strong support should be seen 0.8551 to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243.

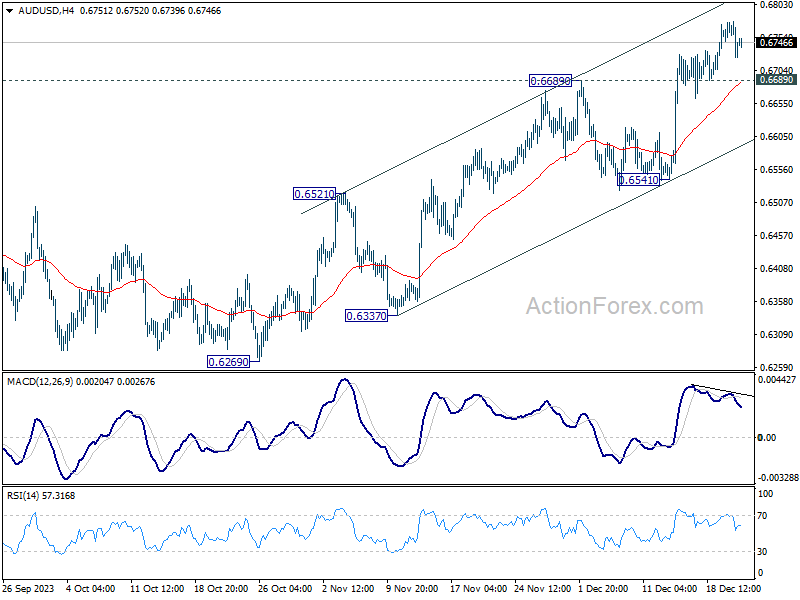

AUD/USD Daily Report

Daily Pivots: (S1) 0.6710; (P) 0.6744; (R1) 0.6765; More...

Further rally is in favor in AUD/USD as long as 0.6689 support holds. Rise from 0.6269 would target 0.6894 resistance first. Sustained break there will target 0.7156 next. Nevertheless, break of 0.6689 will indicate short term topping, and turn bias back to the downside for deeper pull back

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. Price actions from 0.6169 (2022 low) could be just a medium term corrective pattern. Rise from 0.6269 is seen as the third leg of the pattern. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

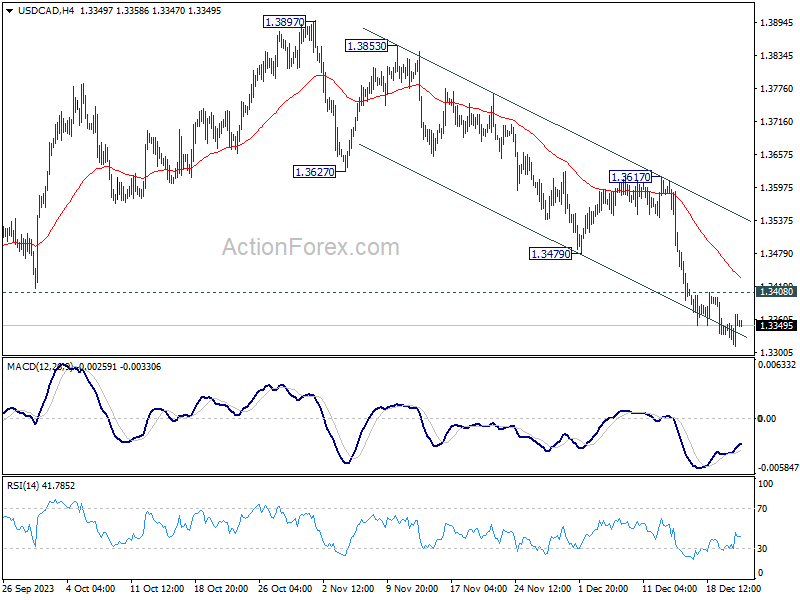

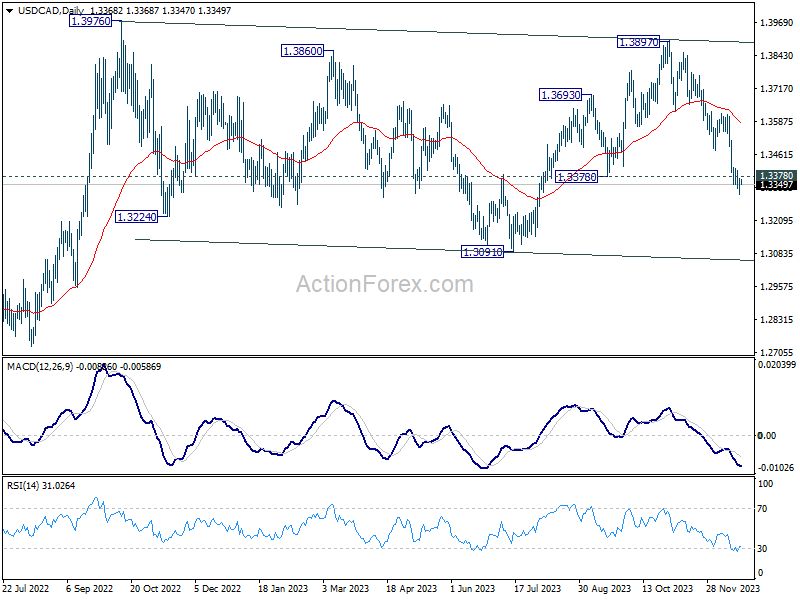

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3330; (P) 1.3350; (R1) 1.3388; More...

Further decline is expected in USD/CAD as long as 1.3408 minor resistance holds. Fall from 1.3897 would target a retest on 1.3091 support. Nevertheless, break of 1.3408 will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, outlook is mixed up by deeper then expected fall from 1.3897. But after all, price actions from 1.3976 (2022 high) are viewed as a corrective pattern that's in progress. Larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage as long as 1.2947 resistance turned support holds.

Cracks

We start feeling the cracks in market optimism: the bonds extended their rally yesterday after the inflation data in Britain surprised to the downside, but major US indices saw a sharp retreat. A 12% plunge in FedEx – which acts like a gauge of economic activity, the overbought market conditions in major global stock indices and the awareness that a further fall in bond yields weaken the idea of soft landing triggered a much-needed retreat in equity valuations.

The British FTSE 100 is fueled by a dovish shift in Bank of England (BoE) expectations, cheap sterling and returning appetite for energy stocks. Appetite for the Stoxx 600 is limited near last week’s peak, while the S&P500 recorded a sharp fall from near ATH, and Nasdaq 100 also saw a sharp retreat after hitting a fresh ATH earlier in the session. European futures are in the red, while US futures are in the green.

We know that a further correction in equity valuations is on the cards. We just don’t know what the trigger will be.

A positive breakout?

The barrel of US crude is still working on clearing the $74/75 resistance. Yesterday’s rising US inventories somehow broke the positive momentum. But strengthening trend and momentum indicators hint that a positive breakout is possible, and a potential rally could send the barrel of crude to 200-DMA, which stands a touch below the $78pb. Yet the upside is seen limited as any significant rally in oil prices will boost global inflation expectations, crush the dream of seeing the central banks call the end of policy tightening and increase recession odds. And rising recession odds are negative for oil.

Enjoy while it lasts

Investors could still enjoy a soft US inflation read for November, and the latter could keep the bond rally intact into Xmas. If that’s the case, the US dollar will remain under pressure. The latter will allow the euro to extend its gains against the US dollar. The pair could make another attempt on the 1.10 mark. For those who love pure tech plays, the current cup and handle formation in the EURUSD is a bullish technical formation and could be interesting for entering fresh long positions. But note that fundamentally, the euro’s strength against the US dollar is not perfectly deserved. The strong US economy calls for a hawkish Federal Reserve (Fed) reaction, the soft European growth and falling inflation call for a dovish European Central Bank (ECB) stance. But what we see today is the exact opposite. So, if the central bankers and the market come back to their senses, the EURUSD should not rally above 1.10. But it may take time before the rectification happens. Today’s US growth number could remind us that the US economy grew more than 5% in Q3.

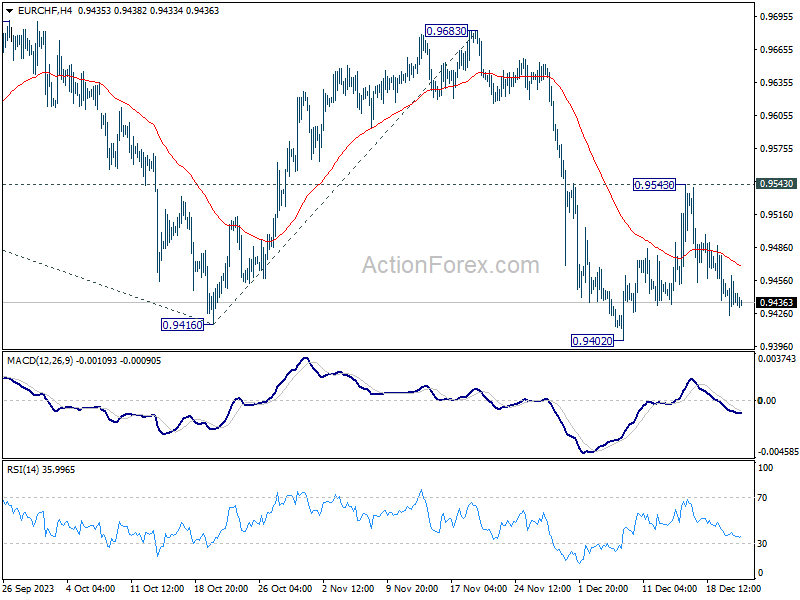

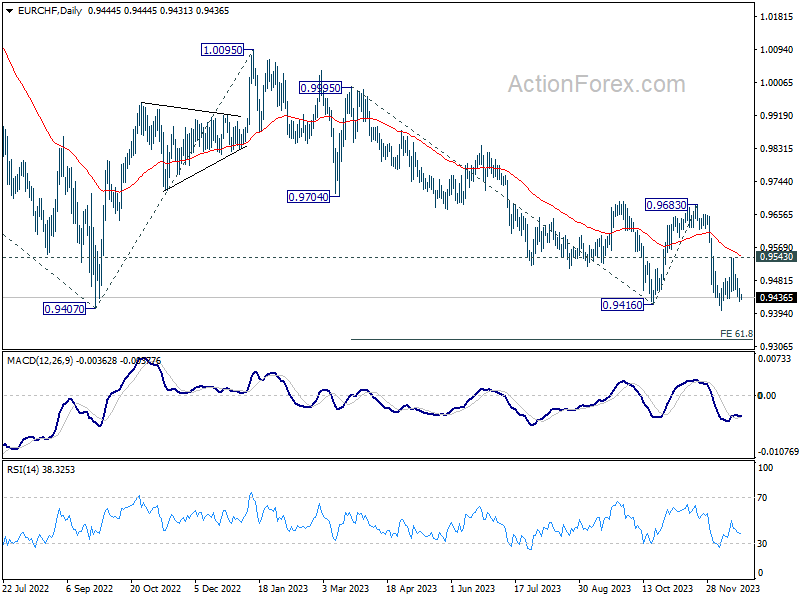

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9424; (P) 0.9443; (R1) 0.9460; More...

Intraday bias in EUR/CHF remains neutral at this point. Consolidation from 0.9402 could extend further. But deeper decline is expected with 0.9543 resistance intact. On the downside, firm break of 0.9407 will confirm larger down trend resumption. Next target is 61.8% projection of 0.9995 to 0.9416 from 0.9683 at 0.9325. However, sustained break of 0.9543 will bring further rally back to 0.9683 resistance instead.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Firm break of 0.9407 (2022 low) will resume long term down trend. Next target will be 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

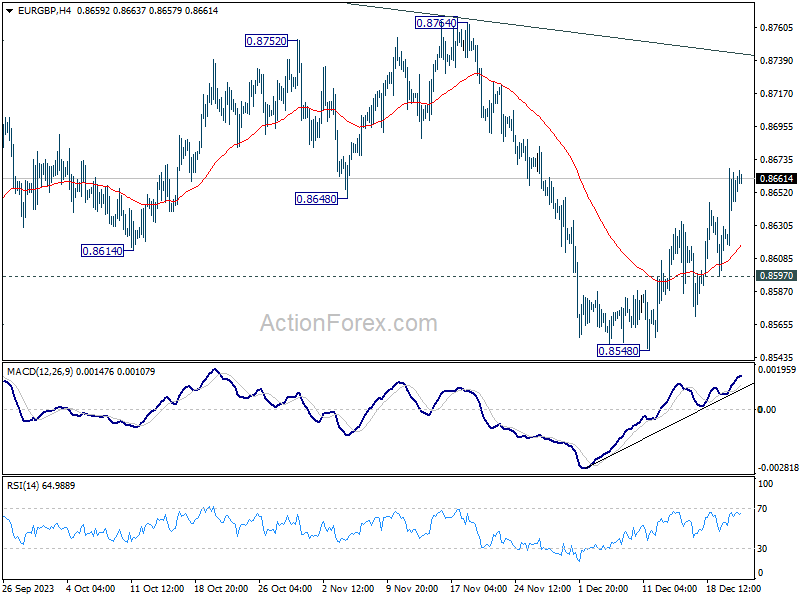

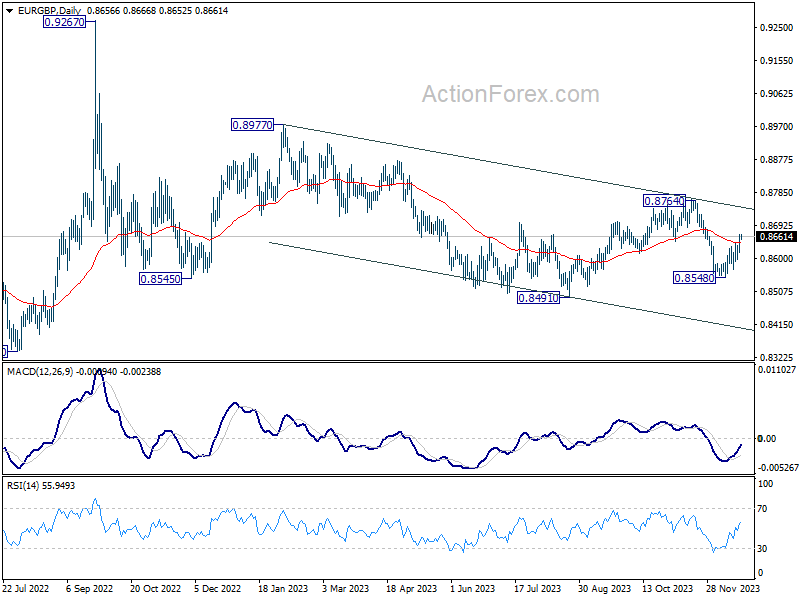

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8628; (P) 0.8648; (R1) 0.8679; More....

Intraday bias in EUR/GBP remains on the upside at this point. Rebound from 0.8548 would target 0.8764 key resistance next. On the downside, however, break of 0.8597 will turn bias back to the downside for 0.8548 support instead.

In the bigger picture, current development suggests that down trend from 0.9267 (2022 high) is still in progress. This decline is seen as the third leg of the pattern from 0.9499 (2020 high). Break of 0.8201 will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969. In any case, outlook will stay bearish as long as 0.8764 resistance holds.

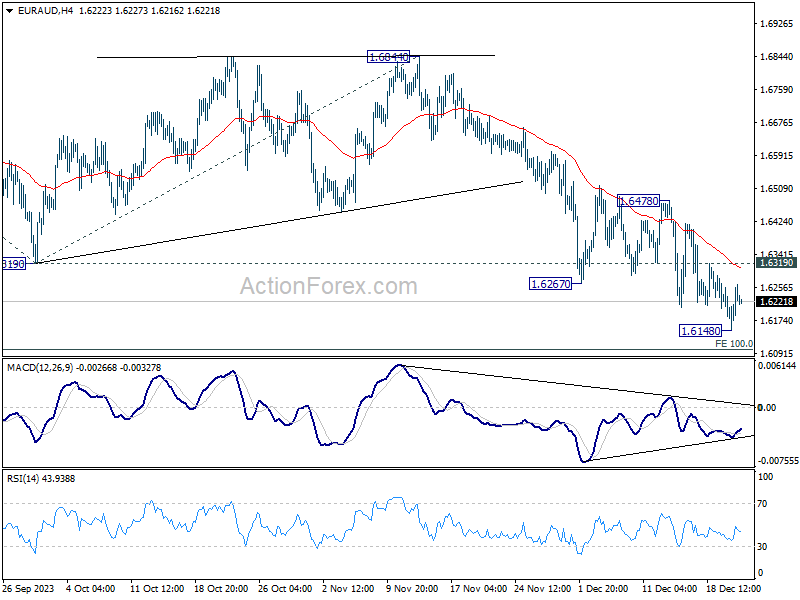

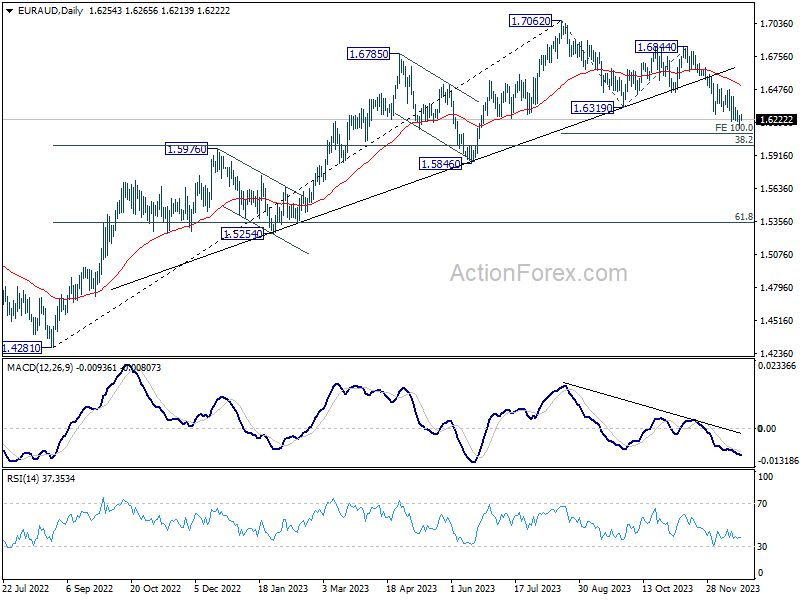

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6186; (P) 1.6223; (R1) 1.6297; More...

Intraday bias in EUR/AUD is turned neutral first with current recovery. On the upside, break of 1.6319 resistance will now indicate short term bottoming, on bullish convergence condition in 4H MACD. Intraday bias will be back on the upside for 1.6478 resistance. Nevertheless, on the downside, below 1.6148 will resume recent decline for 100% projection of 1.7062 to 1.6319 from 1.6844 at 1.6106.

In the bigger picture, fall from 1.7062 medium term top is seen as correcting the whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound on first attempt. But risk will stay on the downside as long as 1.6844 resistance holds. Sustained break of 1.6000 would bring further fall to 61.8% retracement at 1.5343.

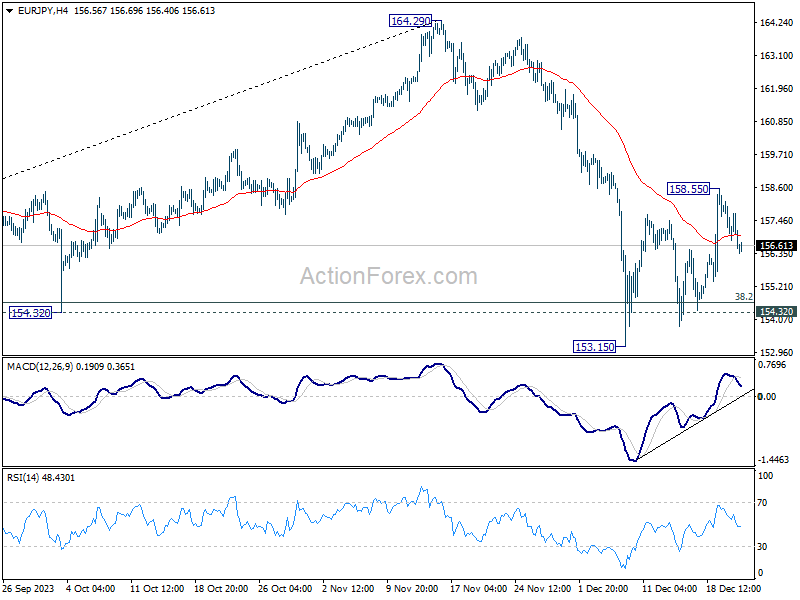

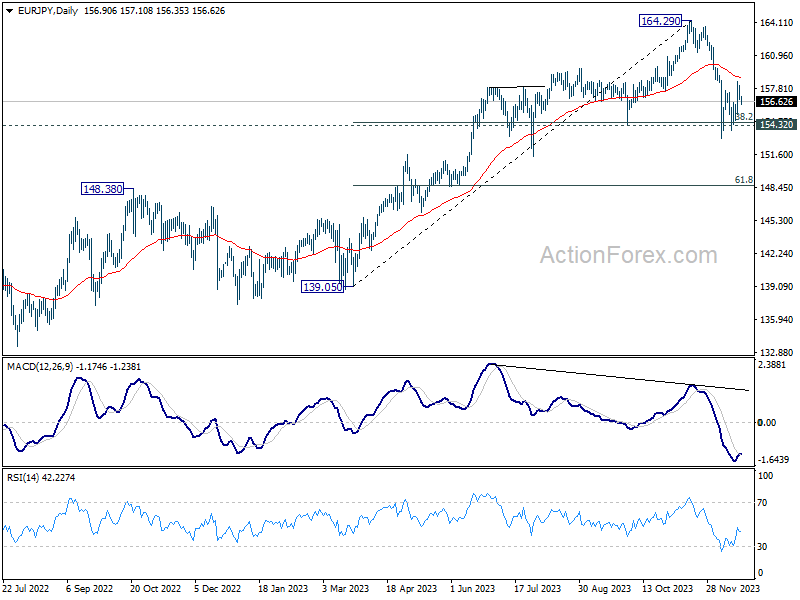

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.55; (P) 157.33; (R1) 157.88; More..

EUR/JPY retreated after hitting 158.55 and intraday bias is turned neutral first. On the upside, above 158.55 will resume the rebound from 153.15 to 55 D EMA (now at 158.82). On the downside, break of 153.15 will resume whole fall from 164.39 to 61.8% retracement of 139.05 to 164.29 at 148.69.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

EU Agrees on New Fiscal Rules

In focus today

Not much on the data calendar before Christmas. In Sweden, markets will take a close look at NIER's December survey. In particular retail trade and private services price plans will be scrutinized for further signs of moderation. Any widening cracks in confidence or hiring plans are also in focus.

In Norway, unemployment rate for December will be released.

Overnight, we will get November inflation print from Japan. Consensus expects headline inflation to fall to 2.8% y/y from 3.3% in October.

The 60 second overview

Risk sentiment: Market's risk sentiment weakened unexpectedly last night with equities turning lower, yields still falling and USD regaining some strength. This marked a shift from the rally sparked by last week's FOMC meeting, where equities, bond markets and cyclical FX all appreciated on the expectation of looming rate cuts. Yesterday's macro data was not particularly downbeat however, with UK inflation surprising to the downside and consumer sentiment recovering both in the euro area and the US. Even so, the Fed's Harker cautioned that he has heard signals of 'things starting to soften faster than data suggests' and that 'a lot of things could thwart a soft landing'. ECB's Knot noted that a rate cut in H1 2024 remains unlikely based on today's information and Lane reminded that markets should not extrapolate the November's positive inflation surprise for what's to come.

EU fiscal rules: Yesterday evening, the EU economy and finance ministers struck a deal on a new set of fiscal rules for the EU. The new rules include stricter overall limits on spending while it provides leeway for countries to invest in key EU priorities like defence and the green transition and allow structural reforms. The old thresholds of a maximum public deficit of 3% of GDP and the 60% debt to GDP remain. Countries with debt over 90% of GDP must trim it by 1 percentage point per year, while countries with debt between 60% and 90% need to make half that effort. Countries that both breach the 60% and 3% thresholds must aim at cutting deficits to 1.5% of GDP by improving the structural balance with 0.4% of GDP each year. Enforcement of the new rules will be tougher and countries that deviates from their spending plans will have to reduce spending by 0.5% of GDP per year. However, a last-minute concession won by France secured that for such countries interest payments will be excluded from the calculation in 2025-27. 16 out of 27 EU countries will not comply with either the deficit target or debt to GDP threshold next year according to the EU Commission estimates. Thus, we should expect an overall tighter fiscal stance in the EU next year. Among the larger countries this will especially affect spending plans in France, Italy and Belgium.

Equities: Global equities lower yesterday as the US cash session went from positive to sharply negative in the afternoon. No obvious trigger and all sectors were lower with no relation to cyclicality or rates etc. The only go to explanation being, the very strong rally leading up to this. Hence it looks like investors said too far too fast and therefor took some chips of the table. We have seen these dynamics before and typically don't recommend chasing sudden shifts unless the fundamental drivers have shift. That was not the case yesterday where we got very solid macro data and yet another set of benign inflation prints.

In US yesterday -1.3%), S&P 500 -1.5%, Nasdaq -1.5% and Russell 2000 -1.9%.

Most Asian markets are lower this morning while China moving against the trend. European futures are lower while US once are higher.

FI: European yields ended lower across the board with a parallel of about 4-5bp supported by the weak UK inflation print in the morning. This took 10y Bund yields below the 2% mark. Intra euro area spreads remaining broadly stable into the holiday period. With only a couple trading days left and no tier 1 data releases scheduled, we may be in for similar sessions with low liquidity period similar to yesterday. Also today, there is no key data releases on the agenda. Yesterday's comments from ECB's Knot on rate cuts in the first half is rather unlikely was disregarded by markets.

FX: In majors, EUR/USD moved slightly lower yesterday, yet still in the mid-1.09s. EUR/GBP hold on to gains after the UK inflation surprise, trades at 0.8660. USD/JPY has continued lower after recent test of 145 and is now below 143. In Scandies, NOK/SEK gave up some of recent days gains as EUR/NOK recovered to above 11.30 whereas and EUR/SEK remains under pressure at around 11.12. NOK/SEK still holds above 0.98.

Credit: The December holiday slowdown has hit the credit market with limited new issue activity and only small changes to spreads. iTraxx Main was unchanged at 60bp while iTraxx Xover was 2bp wider at 323bp.

Nasdaq 100 Technical: Potential Start of Minor Corrective Decline

- Bearish reversal candlestick formed yesterday, its steepest daily loss since 27 October 2023.

- Odds now have skewed towards a potential minor corrective decline sequence within a medium-term uptrend phase.

- Watch the 16,800 key short-term resistance.

The price actions of the US Nas 100 Index (a proxy for the Nasdaq 100 futures) have continued to rally and surpassed the 16,590 short-term resistance as highlighted in our previous analysis and the former 16,772 all-time high printed on 22 November 2021.

It continued to inch higher yesterday, 20 December during the first half of the US session where it rallied by +0.3% intraday and printed a fresh all-time high of 16,898. But it could not maintain its initial bullish momentum and reversed down to end the US session with a daily loss of -1.37%

Steepest daily loss since 27 October 2023

Fig 1: US Nas 100 medium-term trend as of 21 Dec 2023 (Source: TradingView, click to enlarge chart)

The US Nas 100 Index has formed a daily “bearish Marubozu” candlestick with a daily loss of -1.37% which is the steepest daily decline since the medium-term uptrend kickstarted on 27 October 2023.

These observations suggest the prior seven consecutive weeks of higher positive closes are likely to give way to a potential mean reversion decline sequence; at least a short-term multi-day corrective decline to retrace a portion of the enormous swift rally of +20% from the low of 23 October 2023 to yesterday’s fresh intraday all-time high of 16,898.

Short-term bullish trend exhaustion

Fig 2: US Nas 100 minor short-term trend as of 21 Dec 2023 (Source: TradingView, click to enlarge chart)

Its price actions have broken below a minor ascending channel support from the 7 December 2023 low as depicted on the hourly chart.

The retest seen yesterday, 20 December on the former ascending channel support turned pull-back resistance has been accompanied by a bearish divergence condition flashed out on the hourly RSI momentum indicator at its overbought zone.

These short-term bearish elements have reinforced the potential start of a minor corrective decline sequence within its medium-term uptrend phase that is still intact.

If 16,800 key short-term pivotal resistance is not surpassed, the Index may see the next immediate support coming in at 16,430 and a break below it exposes the next support at 16,160/125 (also the upward sloping 20-day moving average).

On the flip side, a clearance above 16,800 invalidates the minor corrective decline scenario for a potential continuation of the bullish impulsive upmove towards the next immediate resistances of 16,950/990 and 17,150/200.