Sample Category Title

AUD/USD Weekly Report

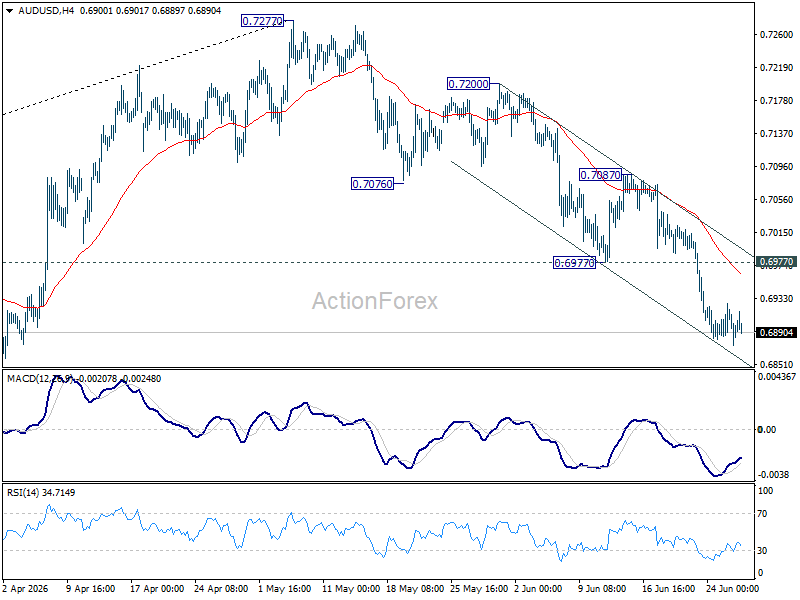

AUD/USD's fall from 0.7277 continued last week. There is no clear sign of bottoming yet despite loss of momentum as seen in 4H MACD. Further decline is expected as long as 0.6977 support turned resistance holds. Retest of 0.6832 support should be seen next. Firm break there will target 0.6756 fibonacci level.

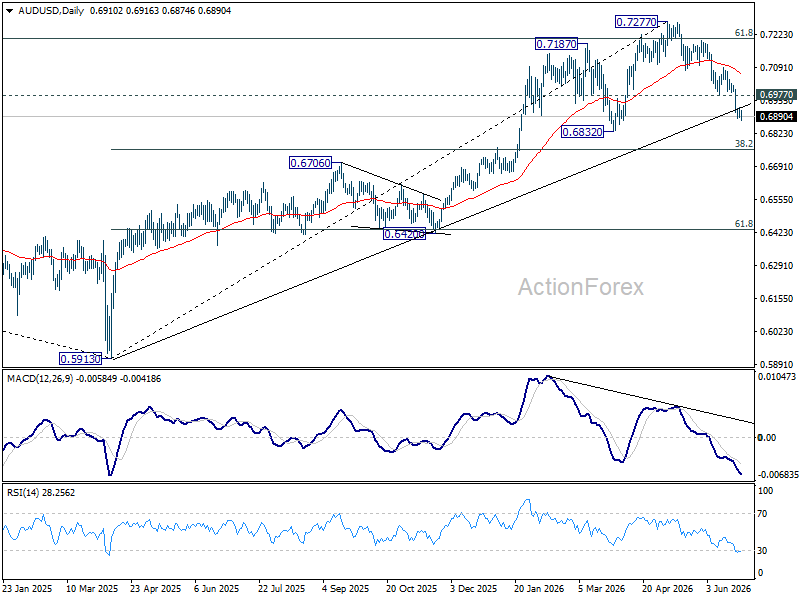

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top could be formed at 0.7277 after failing to sustain above 61.8% retracement of 0.8006 (2021 high) to 0.5913 (2024 low) at 0.7206. Deeper fall could be seen to 38.2% retracement of 0.5913 to 0.7277 at 0.6756 as a correction. But strong support should be seen there to bring rebound. Consolidations would continue below 0.7277 for a while.

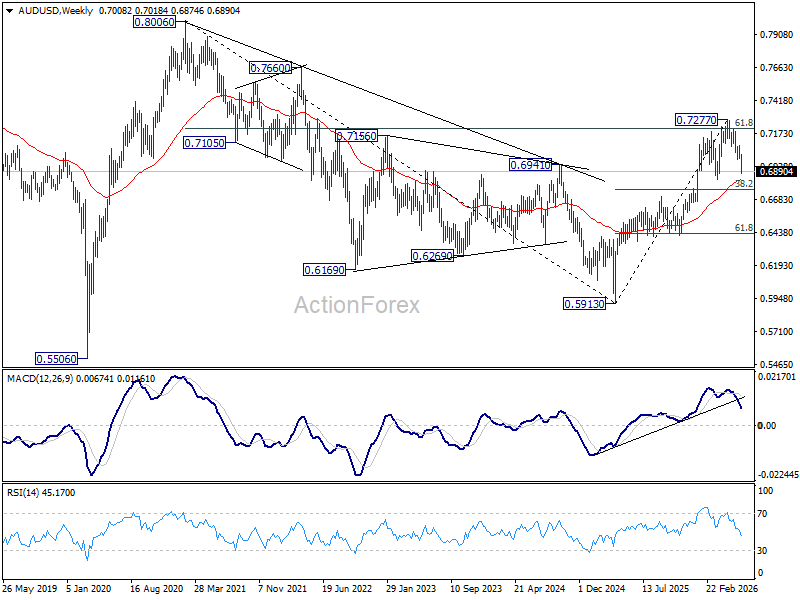

In the long term picture, rise from 0.5913 is seen as the third leg of the whole pattern from 0.5506 (2020 low). It's still early to judge if this is an impulsive or corrective pattern. But in either case, further rise should be seen back to 0.8006 and possibly above. This will remain the favored case as long as 55 W EMA (now at 0.6828) holds.

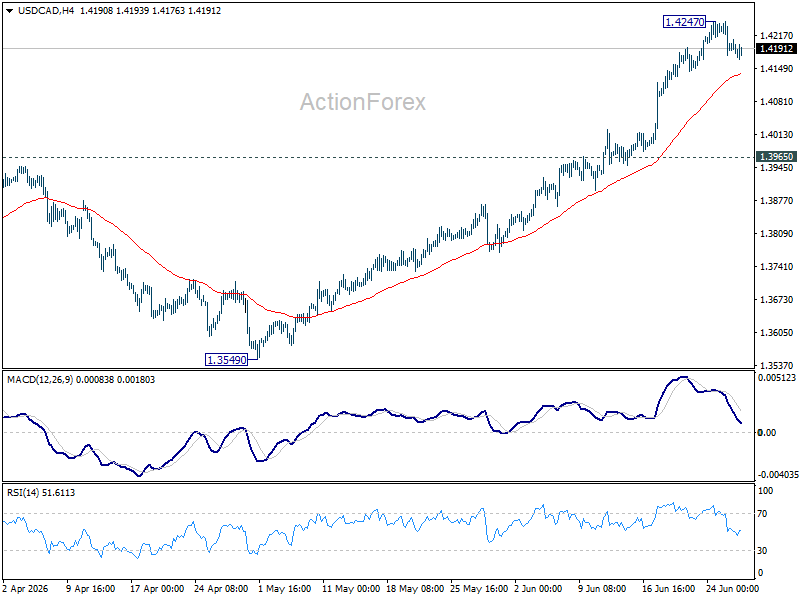

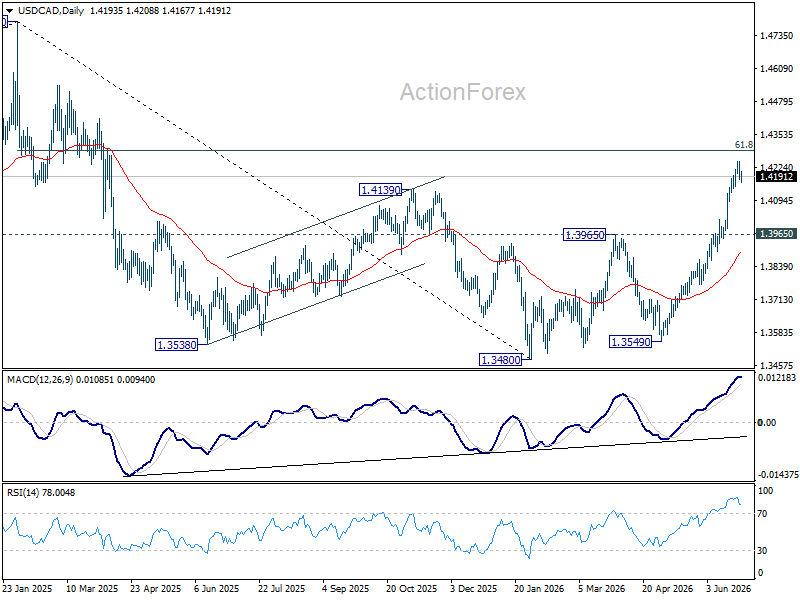

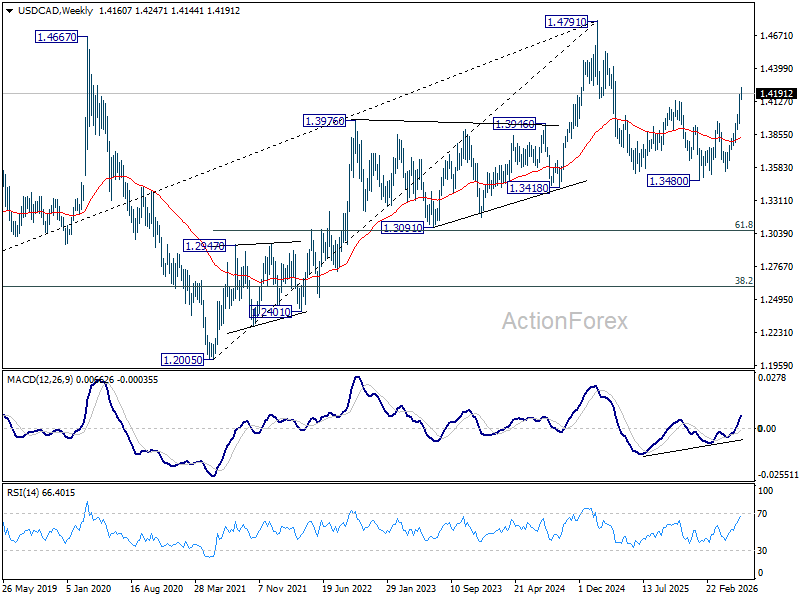

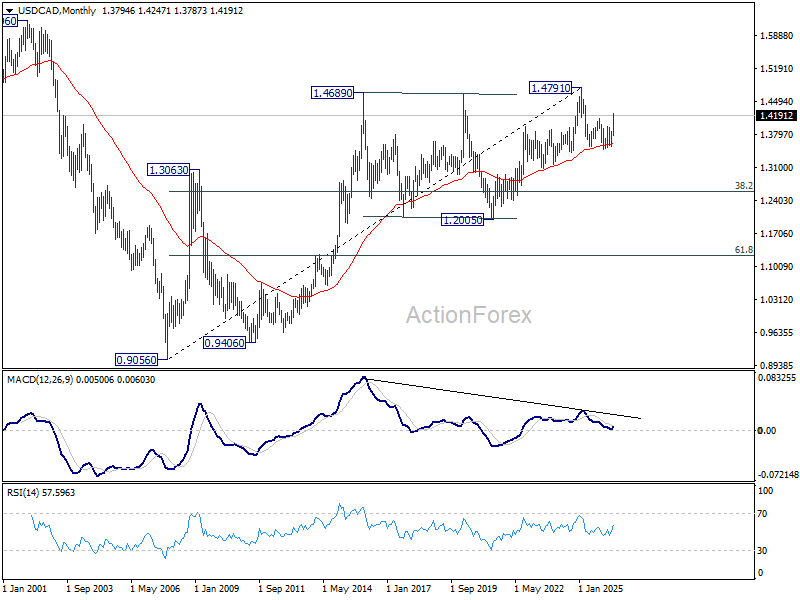

USD/CAD Weekly Outlook

USD/CAD rose further to 1.4247 last week but retreated mildly since then. Initial bias remains neutral this week for consolidations. While deeper pullback cannot be ruled out, downside should be contained above 1.3965 resistance turned support. Above 1.4247 will resume the rally from 1.3480 to 61.8% retracement of 1.4791 to 1.3480 at 1.4290. Firm break there will pave the way back to 1.4791 high.

In the bigger picture, current development suggests that fall from 1.4791 has completed as a three wave correction to 1.3480. It's still early to judge if rise from there a corrective bounce, or resumption of the larger up trend from 1.2005 (2021 low). But in either case, retest of 1.4791 high should be seen next.

In the long term picture, rising 55 M EMA (now at 1.3588) remains intact. Thus, up trend from 0.9056 (2007 low) could still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

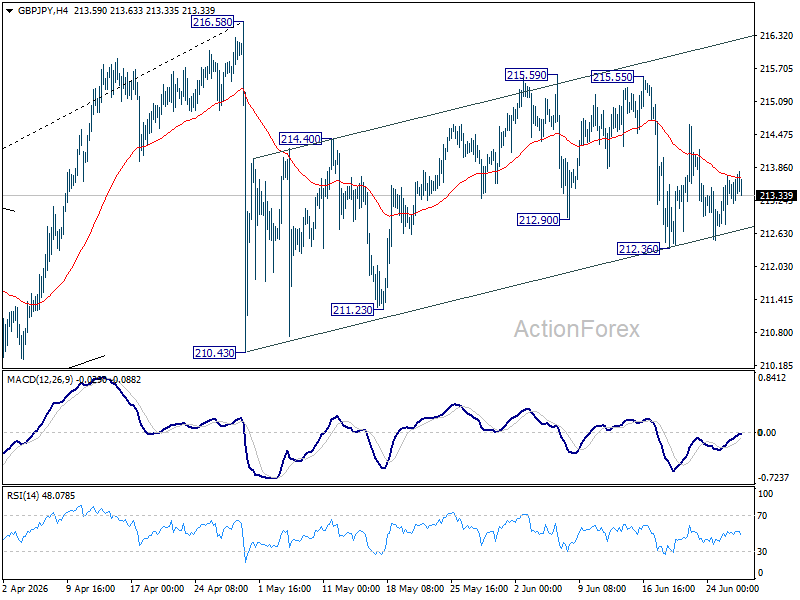

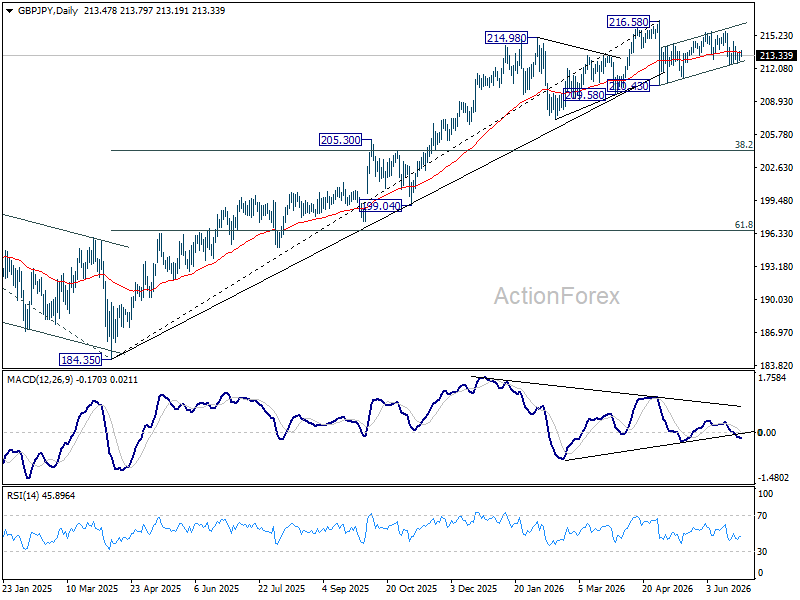

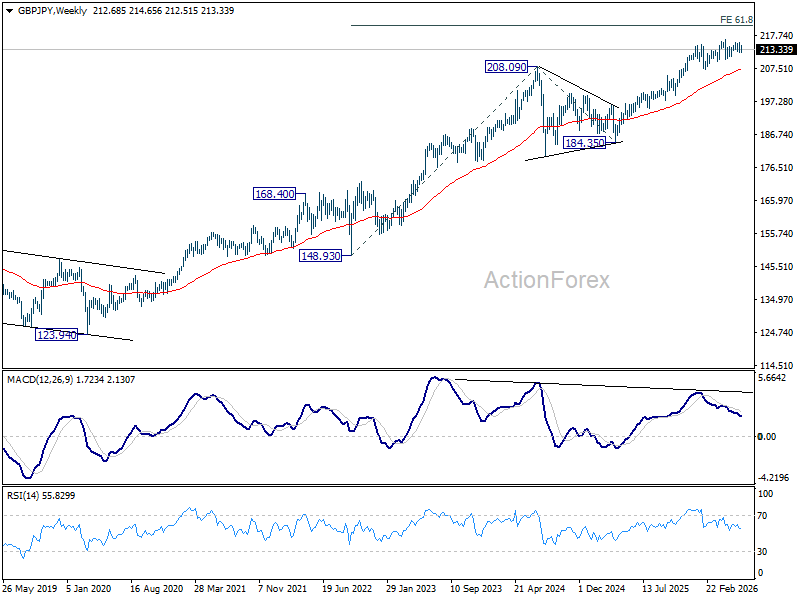

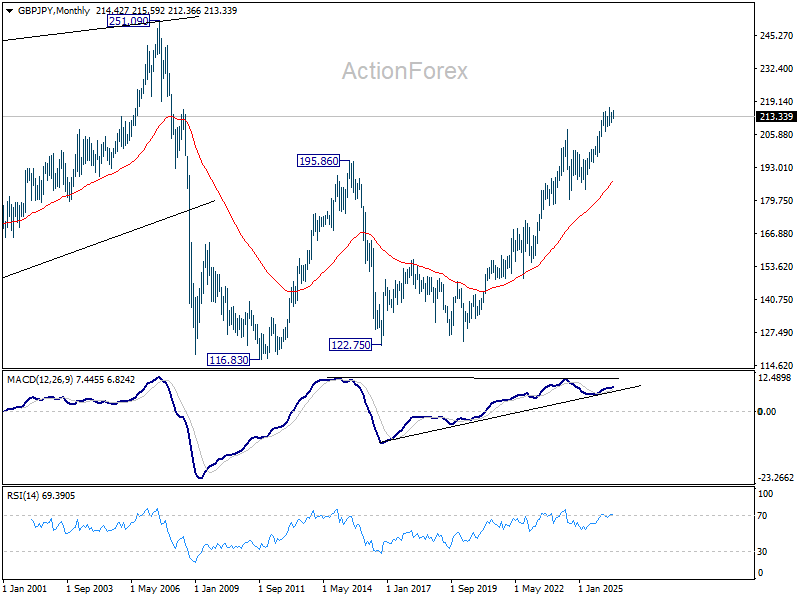

GBP/JPY Weekly Outlook

GBP/JPY turned into sideway trading last week. Initial bias remains neutral this week first. On the downside, below 212.36 will affirm the case that rebound from 210.43 has completed as a correction. Deeper fall would be seen to 211.23 support first. However, break of 215.59 will resume the rebound from 210.43 to retest 216.58.

In the bigger picture, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 207.28) will argue that it's already in medium term down trend for 184.35 support.

In the long term picture, up trend from 116.83 (2011 low) is in progress. Next target is 251.09 (2007 high). This will remain the favored case as long as 55 M EMA (now at 187.79) holds.

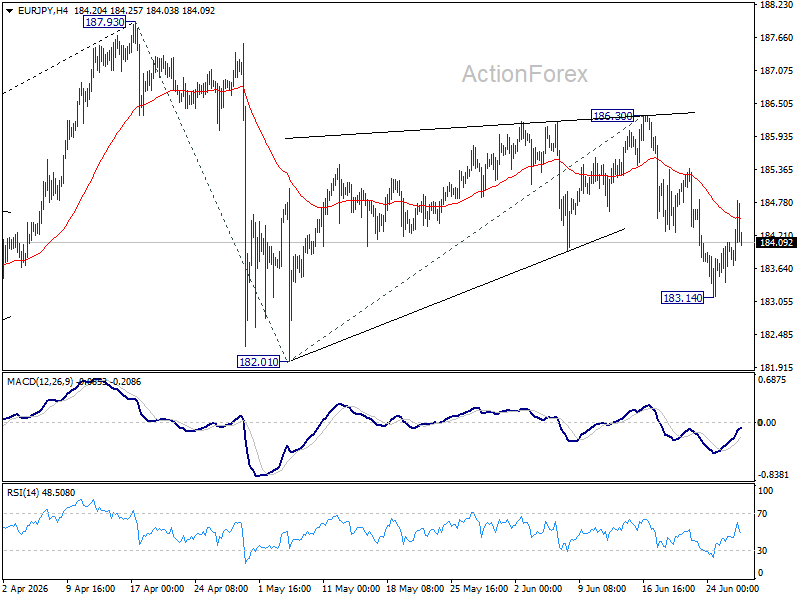

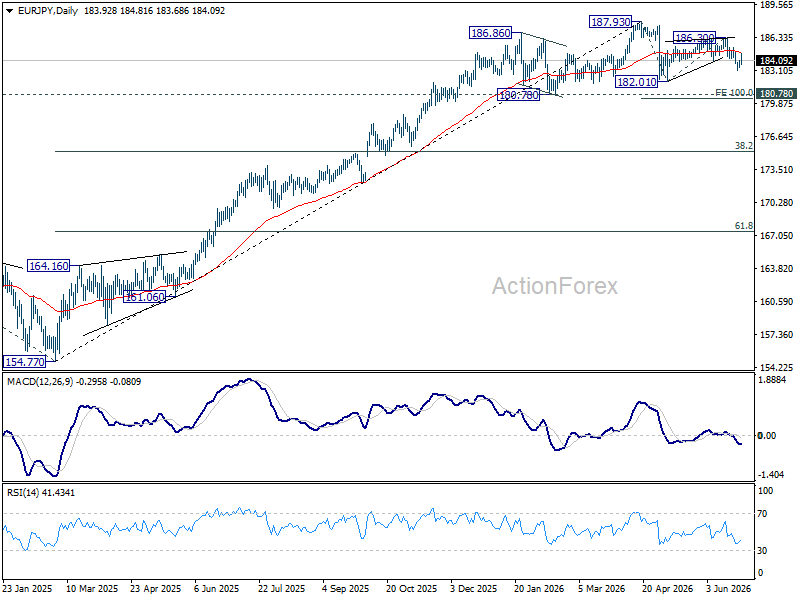

EUR/JPY Weekly Outlook

EUR/JPY fell further to 183.14 last week but recovered since then. Initial bias stays neutral this week first. Fall from 186.30 is seen as the third leg of the pattern from 187.93. Below 183.14 will bring retest of 182.01 support first. Firm break there will resume the fall from 187.93 and target 100% projection of 187.93 to 182.01 from 186.30 at 180.38. This will remain the favored case as long as 186.30 resistance holds.

In the bigger picture, there is no sign of reversal yet. Uptrend from 114.42 (2020 low) is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 179.37) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long 55 W EMA holds.

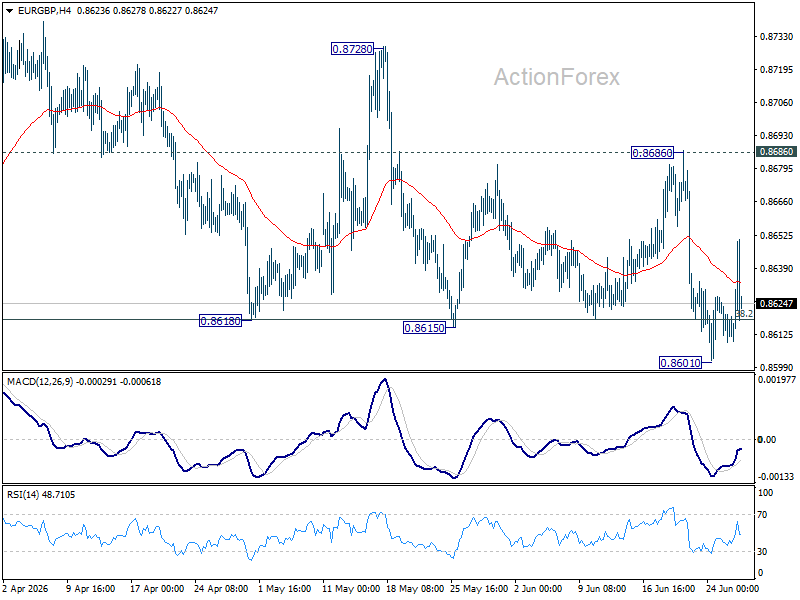

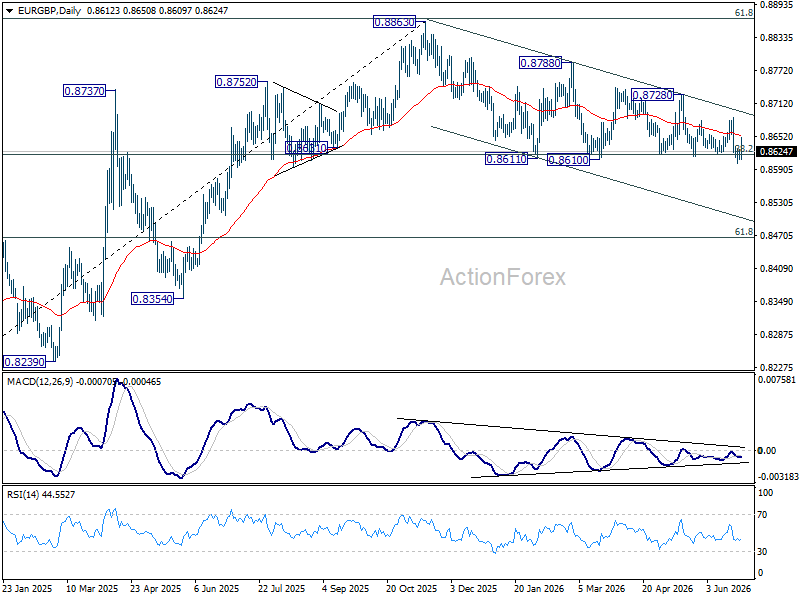

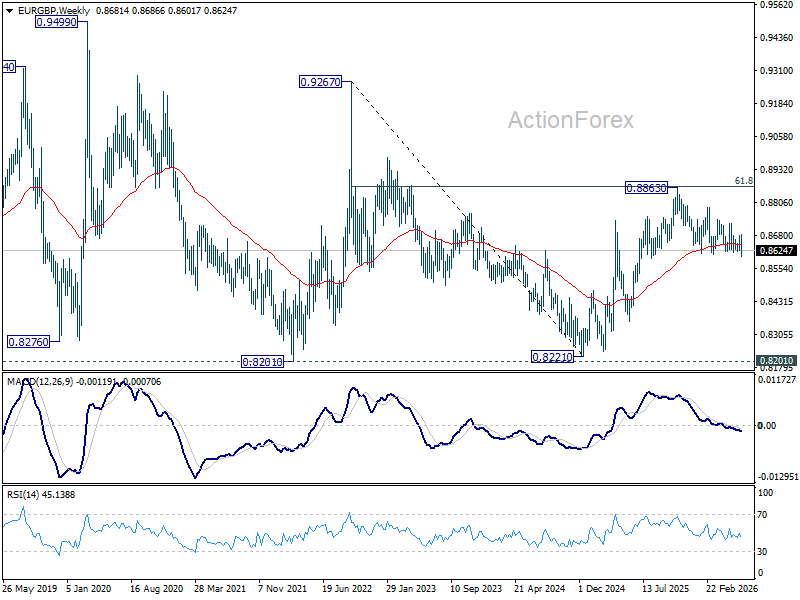

EUR/GBP Weekly Outlook

EUR/GBP edged lower to 0.8601 last week but failed to sustain below 0.8618 fibonacci level and recovered. Initial bias remains neutral this week first. Risk will now be mildly on the downside as long as 0.8686 resistance holds. Firm break of 0.8601 will revive the case of bearish trend reversal. However, break of 0.8686 will turn bias back to the upside for 0.8728 resistance instead.

In the bigger picture, focus is staying on 38.2% retracement of 0.8221 to 0.8863 at 0.8618. Strong rebound from there will retain medium term bullishness. Rise from 0.8221 should resume through 0.8863 at a later stage. Nevertheless, sustained break of 0.8618 will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

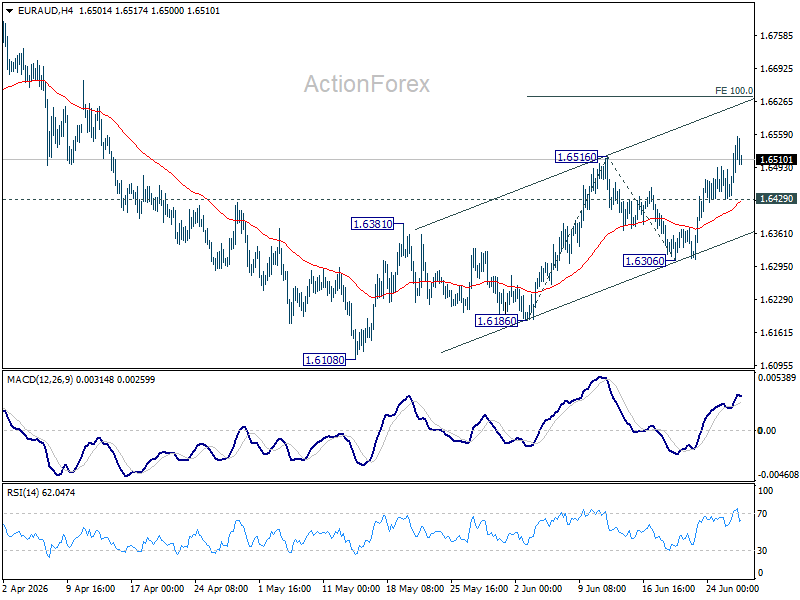

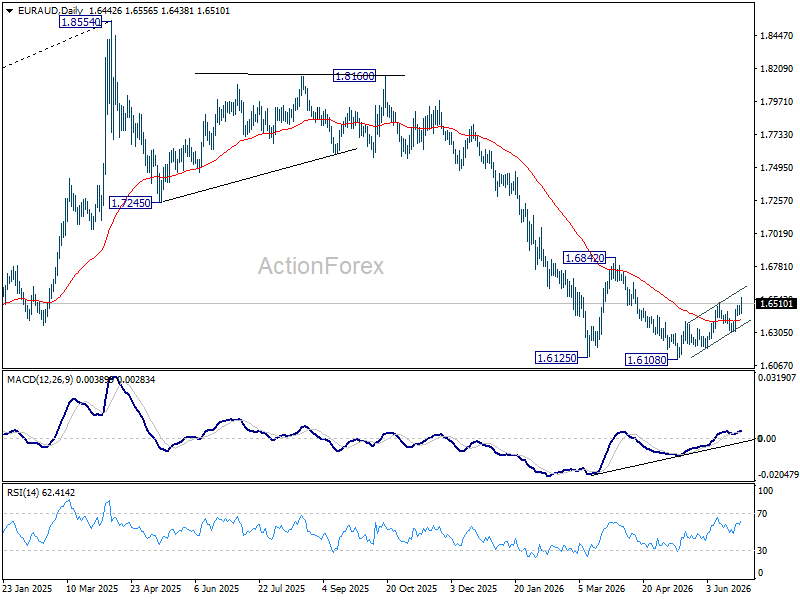

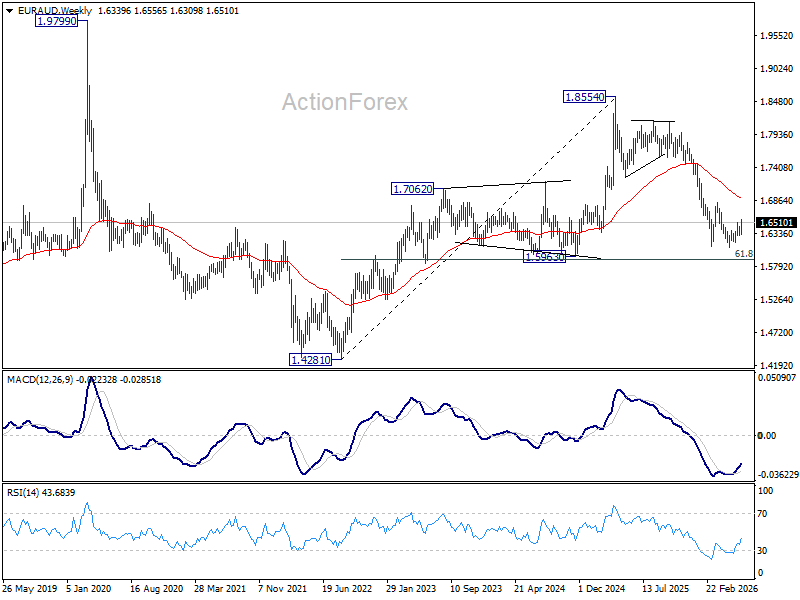

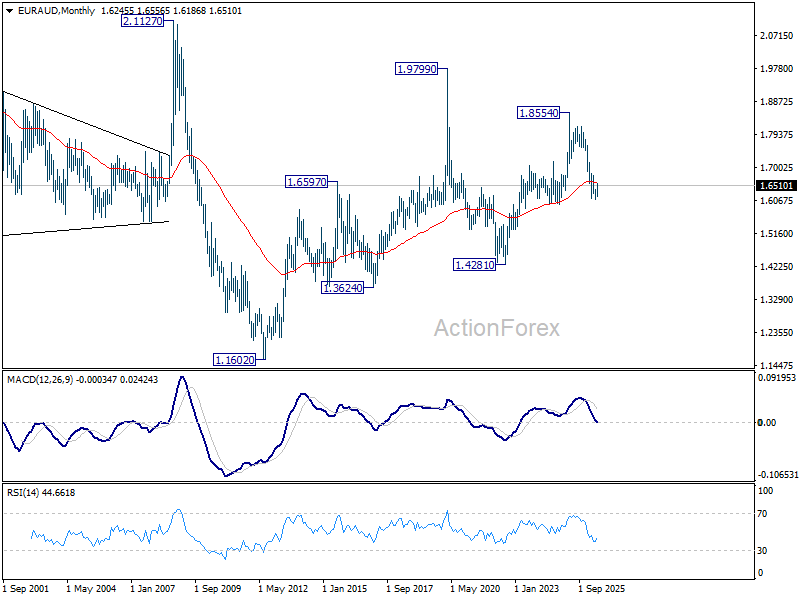

EUR/AUD Weekly Outlook

EUR/AUD's rebound from 1.6108 resumed by breaking through 1.6516 resistance last week. Initial bias remains on the upside this week for 100% projection of 1.6186 to 1.6516 from 1.6306 at 1.6636 next. On the downside, below 1.6429 minor support will turn intraday bias neutral. But further rise will remain mildly in favor as long as 1.6306 support holds, in case of retreat.

In the bigger picture, outlook will stay bearish as long as 1.6842 resistance holds. Fall from 1.8554 (2025 high) is expected to continue to 61.8% retracement of 1.4281 to 1.8554 at 1.5913. Decisive break there will pave the way back to 1.4281 (2022 low). However, firm break of 1.6842 should confirm medium term bottoming, and bring stronger rally.

In the longer term picture, fall from 1.8554 is seen as the third leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). Sustained trading below 55 M EMA (now at 1.6577) will confirm this bearish case, and pave the way back towards 1.4281.

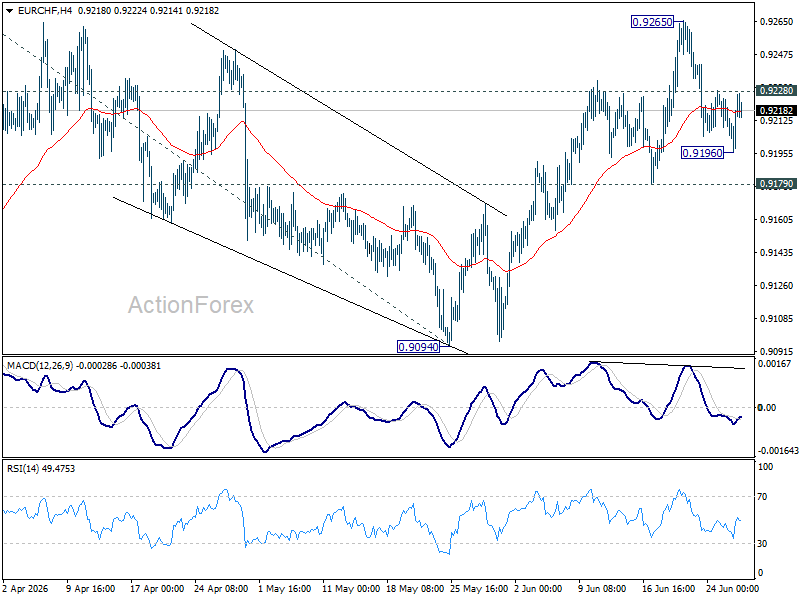

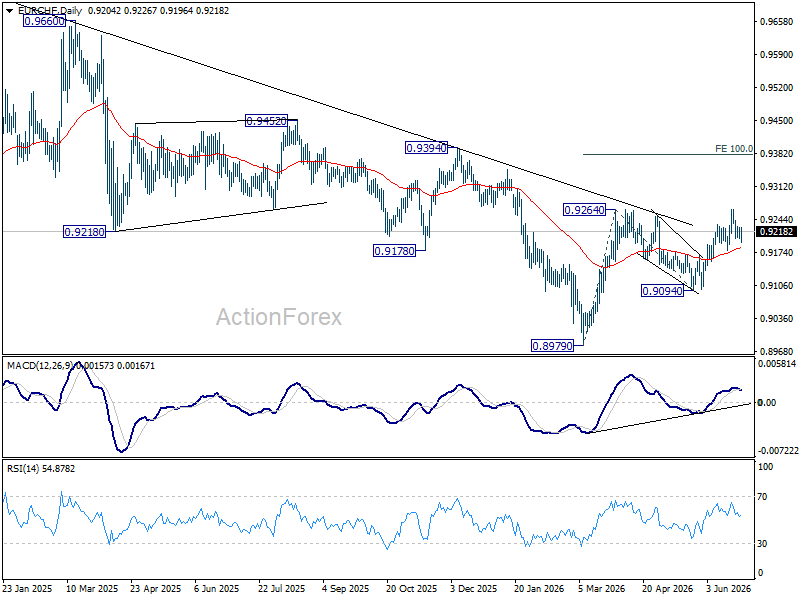

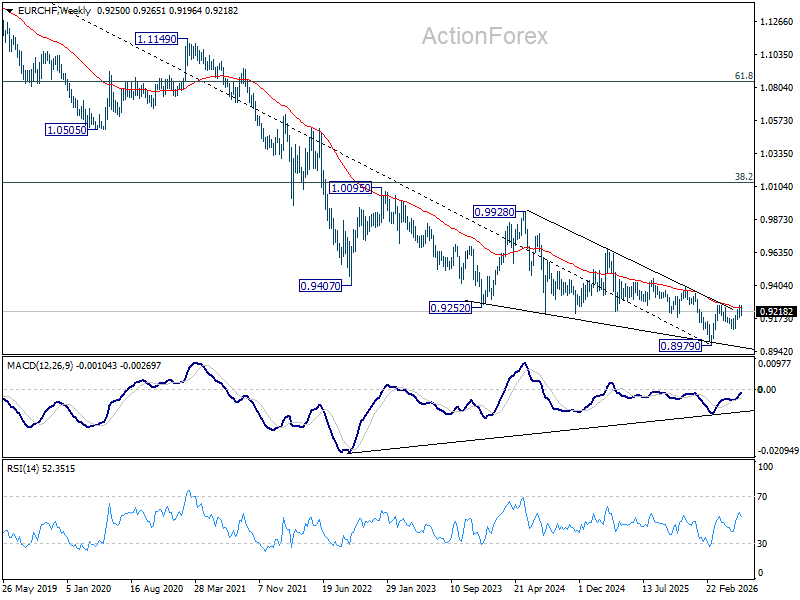

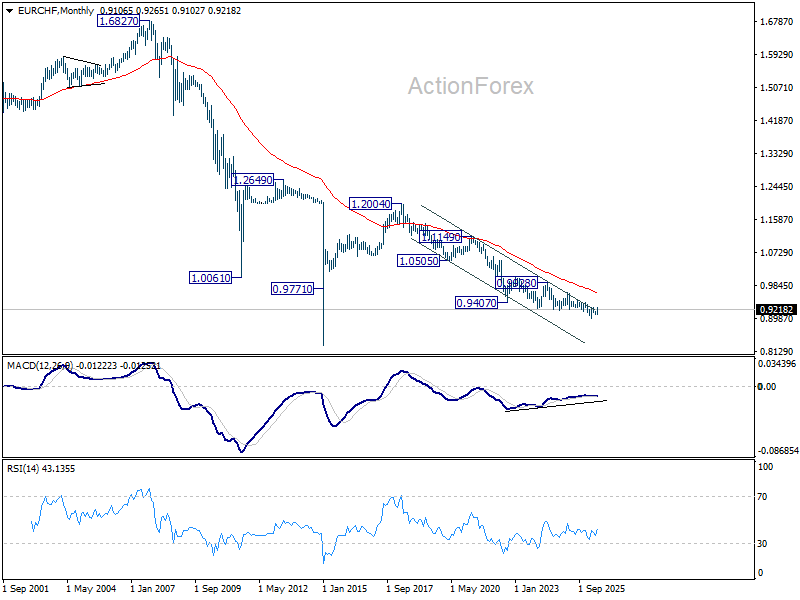

EUR/CHF Weekly Outlook

EUR/CHF edged higher to 0.9265 but was rejected by 0.9264 resistance and retreated. Initial bias stays neutral this week first. Further rally is expected as long as 0.9179 support holds. On the upside, above 0.9228 minor resistance will bring retest of 0.9265 first. Firm break of 0.9264/5 will resume the rally from 0.8979 to 100% projection of 0.8979 to 0.9264 from 0.9094 at 0.9379.

In the bigger picture, the break of medium term falling trend line resistance indicates that 0.8979 is already a medium term bottom. Considering bullish convergence condition in W MACD, rise from there should at least be reversing the fall from 0.9928, with prospect of developing into a medium term up trend. Firm break of 0.9394 resistance will add more credence to this case. For now risk will remain on the upside as long as 0.9094 support holds, in case of retreat.

In the long term picture, outlook will stay bearish as long as 0.9407 support turned resistance (2022 low) holds. However, firm break of 0.9407 will argue that the down trend from 1.2004 (2018 high) has completed with five waves down to 0.8979. Stronger rebound should then be seen to 38.2% retracement of 1.2004 to 0.8979 at 1.0135 in the medium term.

The Weekly Bottom Line: Oil Prices Retreat as AI Volatility Picks Up

Our summary of recent economic events and what to expect in the weeks ahead.

Canadian Highlights

- Canadian inflation accelerated in May, driven primarily by higher gasoline prices, while the Bank's preferred core measures remained close to 2%.

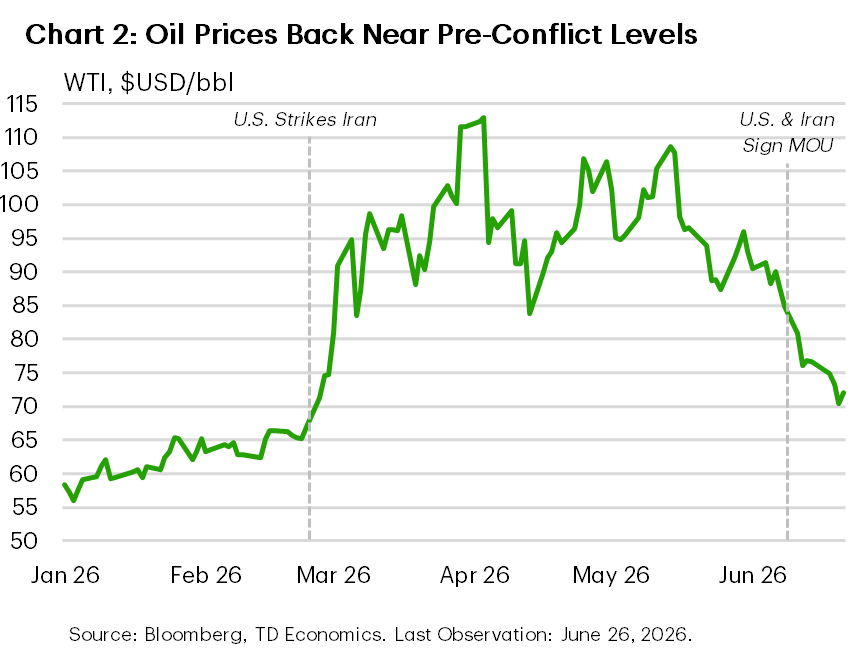

- WTI crude has largely unwound its recent geopolitical premium, retreating to around $70 per barrel. If sustained, this will pull headline inflation lower over the coming months.

- Attention now turns to next week's industry GDP release. We expect a rebound in April, which would be in line with GDP growth to resume at 1.9% annualized pace in the second quarter.

U.S. Highlights

- Oil prices fell below $70/barrel, flirting with pre-conflict levels as the U.S. and Iran continue to negotiate towards a permanent resolution.

- The Federal Reserve's preferred inflation metric, core PCE, rose 3.4% year-over-year in May.

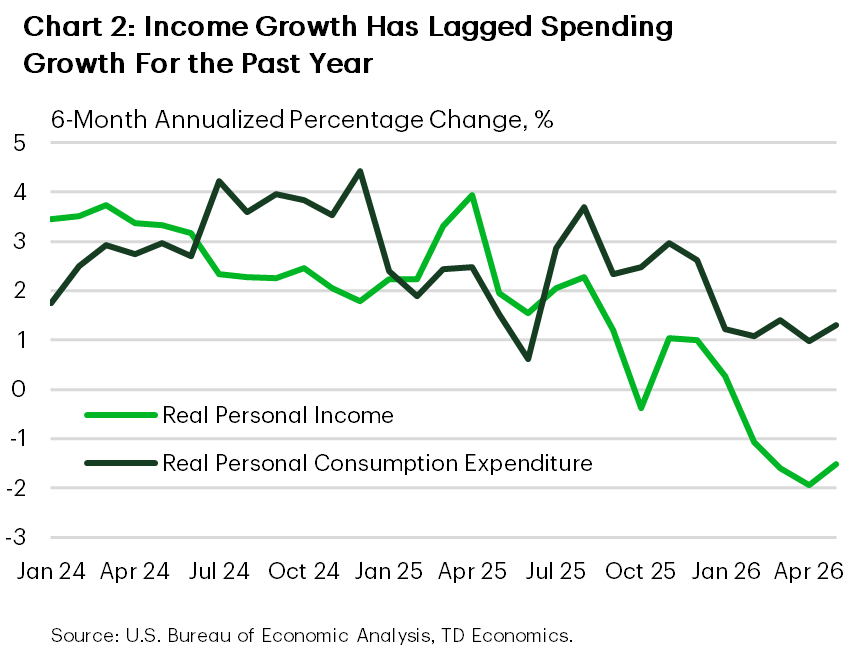

- Personal income and spending both rebounded in price-adjusted terms in May, though households have increasingly relied on savings to support spending.

Canada – Peak Inflation

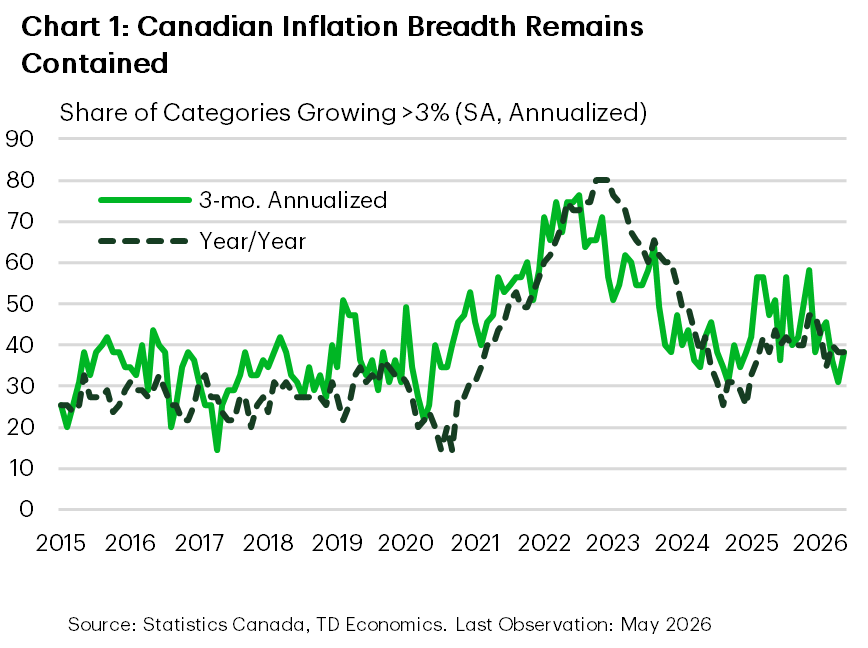

This week's inflation data reinforced a familiar message: the recent inflation gain remains largely energy-driven, while underlying price pressures have remained contained and continue to ease. May's CPI print showed headline inflation re-accelerating to 3.2% year-on-year (y/y) from 2.8% in April, driven primarily by higher gasoline prices. Prices at the pump rose for a third consecutive month, accelerating to 33.2% y/y and reaching their highest levels since June 2022. Air transportation prices also increased as airlines faced higher operating costs, particularly for jet fuel. Another notable outlier was tomato prices, which surged 45.2% y/y, reflecting reduced Mexican supply due to poor weather conditions and a reduction in planted acreage following the implementation of U.S. tariffs.

In contrast, the Bank of Canada's preferred core measures remained close to 2%. While they edged slightly higher on a three-month basis, the increase was modest and not enough to raise alarm bells. The contained pace of core inflation underscores that the recent energy price spike has remained concentrated in a few categories. Inflation breadth – a measure of how broadly price increases are spread across the economy – remained contained. Outside of energy price pressures, prices are broadly consistent with an economy operating below potential.

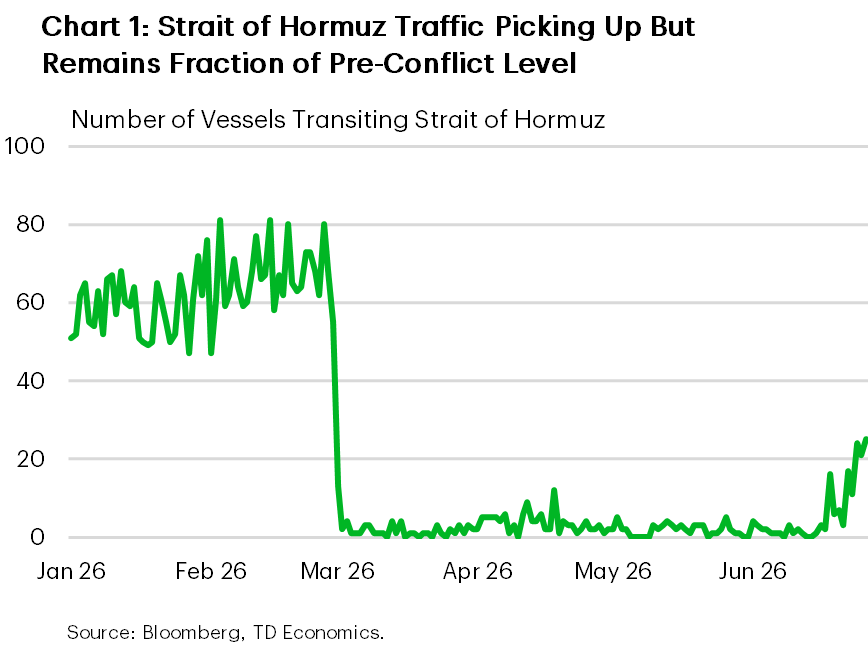

Meanwhile, oil prices have begun to retreat, suggesting that this energy-driven inflation flare-up has peaked. WTI crude has largely unwound its recent geopolitical premium, retreating to around $70 per barrel – close to its pre-conflict level. The decline reflects expectations that oil flows through the Strait of Hormuz will normalize relatively quickly, easing concerns over oil supply disruptions. If those expectations prove correct, lower energy prices will pull headline inflation lower.

Core inflation, however, is likely to remain somewhat elevated for another two to three months, reflecting the typical lag for energy costs to feed through to the broader economy. What's important is that the trend in core inflation is broadly consistent with what the Bank of Canada would like to see. Governor Macklem reiterated this point following his speech in Paris, noting that inflation remains concentrated rather than broad-based, while the Bank's preferred core measures have shown little movement.

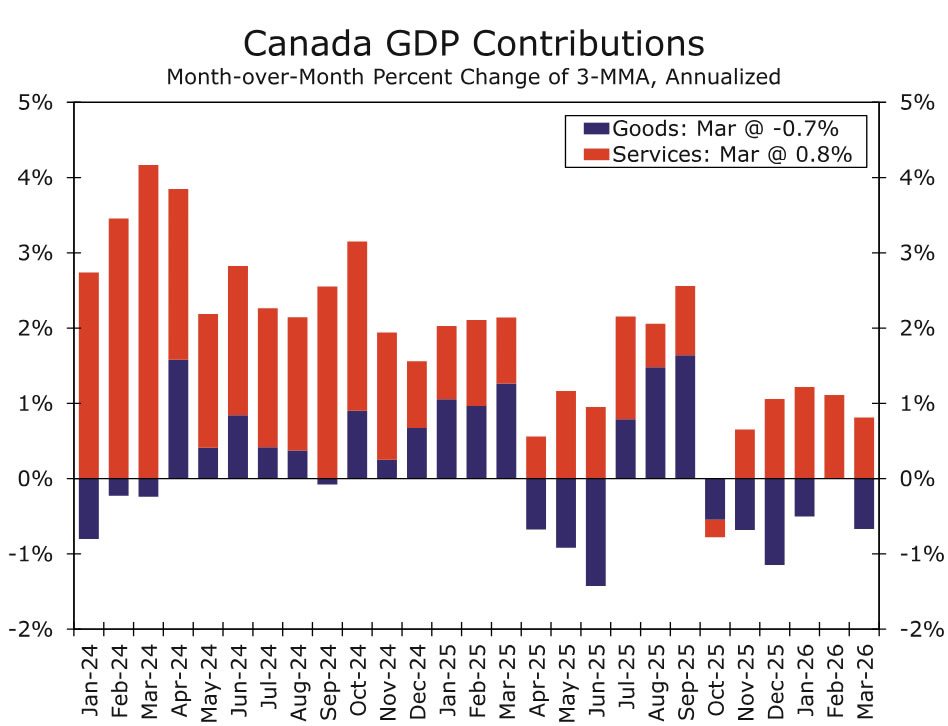

Attention now turns to next week's April industry GDP release. Recall that first-quarter expenditure-based real GDP contracted by 0.1% annualized, weighed down by volatile trade flows and weak domestic demand. The underlying picture, however, was more constructive. Industry-based GDP grew by 0.5% annualized over the quarter, suggesting that the headline contraction might have overstated the degree of underlying weakness. Statistics Canada's flash estimate points to a solid 0.4% month-on-month gain in April, positioning the economy for a stronger start to the second quarter.

This aligns with our broader assessment that the economy is going through a soft patch rather than sliding into recession. We expect growth to resume at 1.9% quarter-on-quarter (annualized) in Q2 2026.

Maria Solovieva, CFA, Economist

U.S. – Oil Prices Retreat as AI Volatility Picks Up

The first week of summer was relatively quiet on the economic data front, with financial markets consumed by developments in the Middle East and evolving trends in AI. The latter proved to be a source of volatility in equity markets this week, as news of personnel changes at Alphabet led to a sell-off that spread to the broader AI ecosystem. This was partially reversed later in the week, but still highlights the inherent sensitivity of markets under the combined influence of elevated valuations and market concentration. The S&P 500 was down 1.8% while U.S. Treasury yields moved modestly lower on the week as of the time of writing.

On the geopolitical front, negotiations between the U.S. and Iran continued after the two sides signed a 60-day memorandum of understanding (MOU) last week. The cessation of hostilities and reopening of the Strait of Hormuz have been enthusiastically welcomed by financial markets, with oil prices now back at their pre-conflict level. However, it bears repeating that the resumption of oil trade through the vital passageway is likely to be a gradual process as evidenced by the current level of maritime traffic through the strait. Combined with the possibility for roadblocks to be encountered during negotiations, risks related to oil prices remain skewed to the upside.

The feedthrough of higher energy prices to the economy was evident in the PCE inflation reading for May. Prices were 4.1% higher year-on-year (y/y) during the month, primarily driven by a 24% increase in energy prices. However, broader inflation pressures were also present, with core PCE inflation, which excludes food and energy products, rising 3.4% y/y. With energy prices having sharply reversed, some downward pressure on overall inflation is already in-tow. However, uncertainty around the magnitude and duration of energy-related second-order effects has given policymakers reason to adopt a more hawkish stance.

Personal income and spending both rebounded in real (price-adjusted) terms in May after softer readings in April, reflecting the sustained resilience of the American consumer. Still, much of the spending in recent months has been driven by a drawdown in savings, with the savings rate remaining at 3% in May – far below its historical average of 5-6%. While robust financial returns over the past few years may be offsetting the extent to which consumers need to save to meet their financial goals, the downward trend in the savings rate also began in mid-2025, coinciding with the introduction of broad tariffs and likely reflective of the multitude of cost pressures that have weighed on consumers over the past year.

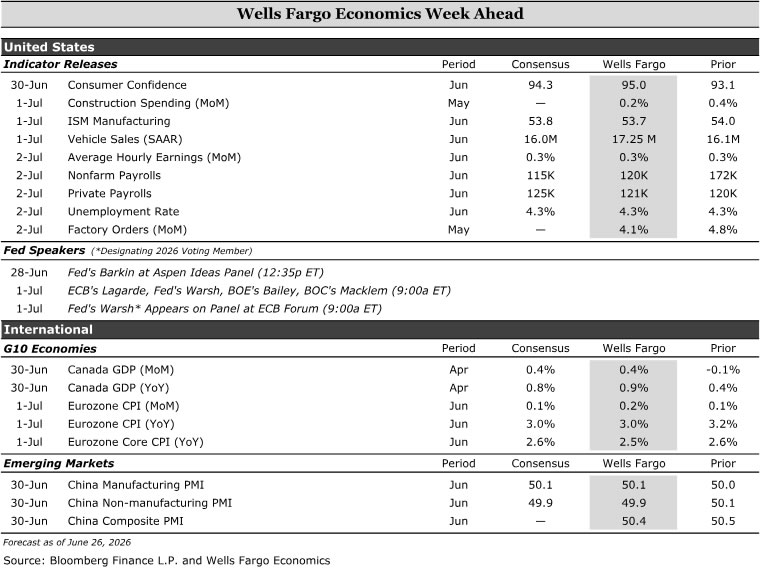

Looking ahead to next week, the June employment data release on Thursday will be the highlight. Markets currently expect 118k new jobs to have been created during the month, marking a moderate deceleration relative to the strong reading in May. Fed Chair Warsh will also participate in a panel discussion next Wednesday, which will be watched closely for any signals on monetary policy decisions over the second half of the year.

Economics Week Ahead

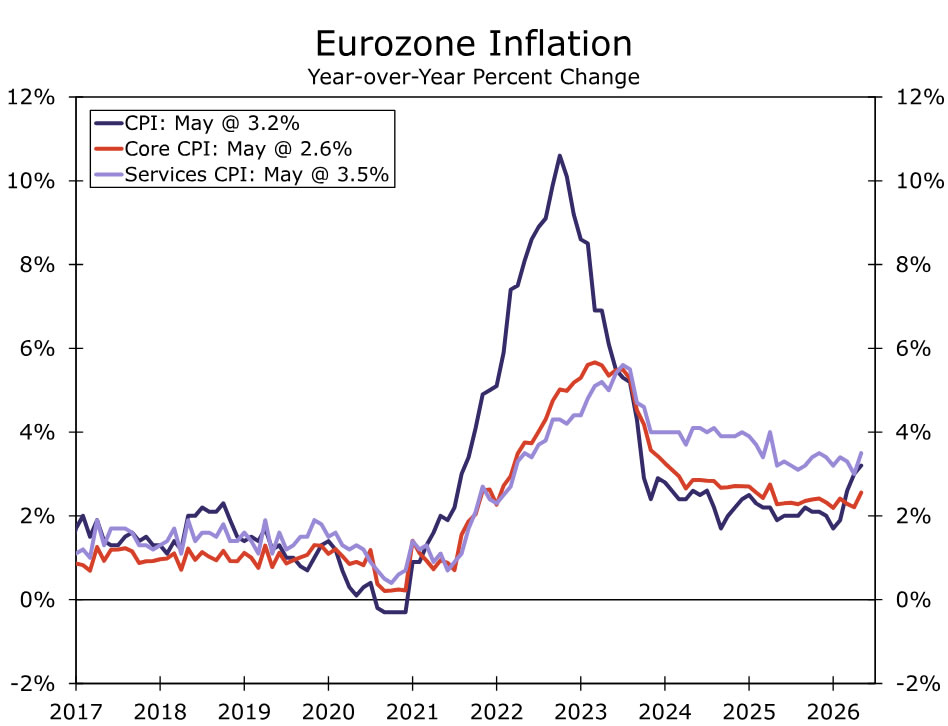

Labor market conditions remain stable, but the recent pace of hiring is unlikely to be sustained. We expect payroll growth to moderate to 120K in June and look for the unemployment rate to hold at 4.3%. Separately, Chair Warsh is expected to outline a more structural framework for central banking and limited forward guidance in his first major public remarks. In Canada, activity is expected to improve modestly following a soft Q1, with energy output providing support but partially offset by weakness elsewhere. In the Eurozone, inflation has heated up alongside temperatures, but we expect headline and core inflation to cool slightly with lower energy prices. In emerging markets, China's June PMI is expected to point to continued softness, with sluggish activity and sentiment suggesting weak medium-term growth momentum.

United States

Warsh Speaking • Wednesday

FOMC Chair Kevin Warsh is set to deliver his first "Fed speak" at the ECB's Sintra Forum alongside central bankers from across the globe. We doubt that Warsh will provide much insight on the near-term policy path and instead emphasize more structural views on the future of U.S. central banking in the years ahead.

We do not expect much forward guidance beyond limited remarks that center on price stability and patience. His comments on structural central banking topics will probably be similar to what he said at the most recent press conference as it relates to communication tools, the Fed's balance sheet, alternative data, AI and productivity, and so forth. Although we don't expect it, we will be listening closely for any guidance on where Warsh's views lie as it relates to the near-term policy outlook as well as the longer-run neutral rate.

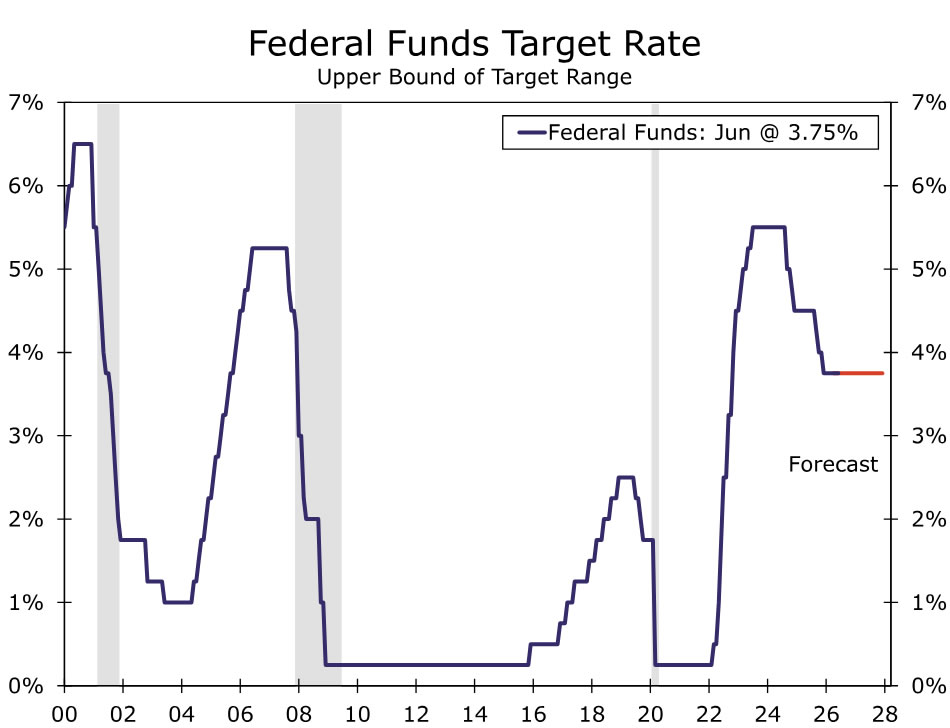

Our base case is for the FOMC to keep the fed funds rate steady at current levels through year-end 2027, with risks tilted towards a few rate hikes if the employment and inflation data come in hotter than expected over the next few months.

Employment • Thursday

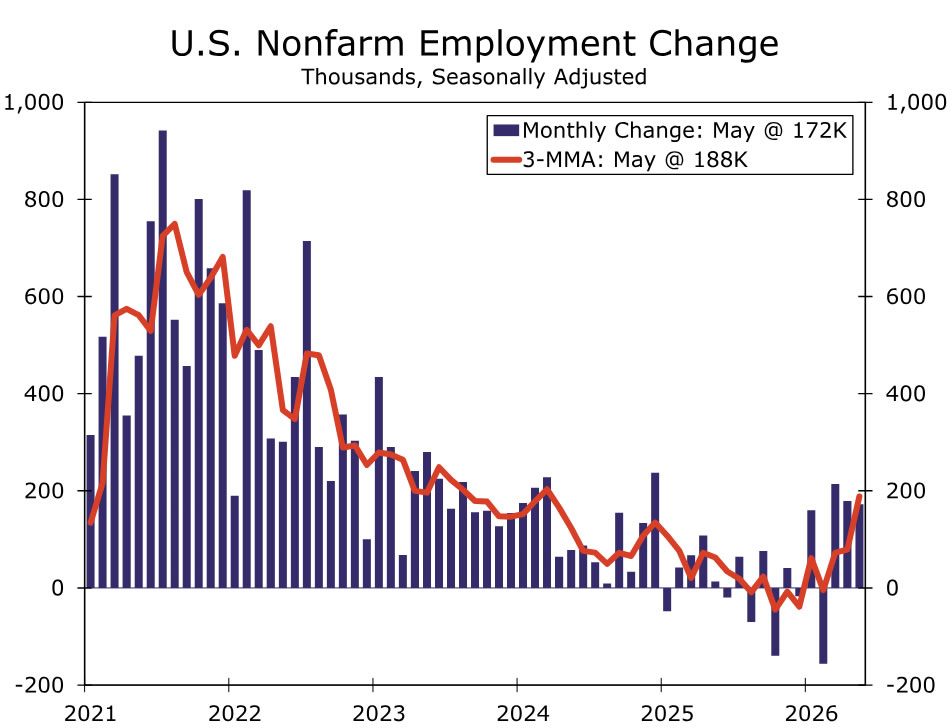

The labor market continues to stabilize after its swoon in 2025. Initial jobless claims are low and regional Fed employment PMIs point to some modest firming in hiring in June. That said, other indicators have softened recently. Indeed job postings and ADP's weekly hiring measure have both turned down since the spring, while small business hiring plans fell to a fresh cycle low in May. Taken together, the data suggest labor demand is holding roughly steady rather than re-accelerating in a meaningful way.

We estimate nonfarm payrolls rose 120K in June, with private payrolls up a similar 121K. While job growth has averaged a 188K pace over the past three months, we suspect that overstates the underlying trend. May's gain was underpinned by outsized gains in leisure & hospitality and local government ex-education, categories where the recent pace of hiring looks unlikely to be sustained and could ultimately be revised away.

We look for the unemployment rate to hold at 4.3%, though risks are tilted to the downside. A rebound in household employment appears likely, but could be accompanied by a pickup in labor force participation which would leave the jobless rate unchanged. Wage growth should remain contained, with average hourly earnings rising 0.3% on the month and 3.5% over the past year. Even with some recent firmness in headline payroll gains, the broader picture remains one of a labor market near balance, with neither labor demand nor wage pressures signaling a return to overheating.

G10 Week Ahead

Canada GDP • Tuesday

Canada's April monthly GDP is likely to rise 0.4% month-over-month, in line with Statistics Canada's advance estimate. Activity should modestly improve after a softer Q1, supported in part by stronger energy sector output, although declines in agriculture, forestry, fishing and hunting may provide a partial offset. While recent PMI surveys also point to some firmness in April, the strength appears tied to stock building amid higher prices and elevated uncertainty around the Middle East conflict rather than a sustained pickup in demand.

For the Bank of Canada (BoC), a stronger April GDP print may not be enough to shift the policy outlook toward tightening. But even as May CPI surprised to the upside, the increase was largely energy-driven, with the BoC's preferred core measures remaining broadly stable, and wage pressures contained.

Against this backdrop, we now see a higher bar for tightening and expect the BoC to remain on hold through year-end. That said, the outlook remains highly contingent on whether the U.S.–Iran interim deal holds and on the trajectory of USMCA negotiations.

Eurozone CPI • Wednesday

We expect next week's Eurozone CPI release for June to show headline inflation easing to 3.0% year-over-year (from 3.2%), with core inflation edging lower to 2.5% (from 2.6%). Lower retail energy prices should help contain headline pressures, with recent pump price data pointing to some relief. PMI data also suggest that lower energy prices are beginning to filter through to businesses, as input cost and selling price inflation eased in June.

Still, we do not expect the data to deter the European Central Bank (ECB) from another hike in Q3. Medium-term inflation expectations remain elevated relative to pre-war levels, even as one-year inflation expectations have moved lower. We expect the ECB to pause in July while policymakers assess developments in the Middle East, including whether the Strait of Hormuz remains open and safe for oil flows, before hiking in September and bringing the Deposit Rate to 2.50%. That said, risks are tilted toward a hold if growth momentum weakens, core inflation surprises to the downside, or price pressures remain narrow.

EM Week Ahead

China PMIs • Tuesday

China's official June PMI figures are due next week and should provide an initial read on whether economic activity stabilized at the end of Q2. We expect the data to remain close to the 50 threshold separating expansion from contraction, with manufacturing PMIs edging up to 50.1 and nonmanufacturing PMI slipping to 49.9.

Momentum has been subdued so far in Q2, with recent data pointing to a soft and uneven backdrop. May PMI readings showed a similar pattern, with manufacturing easing to the neutral threshold while nonmanufacturing was supported by a boost to services around the early-May Labor Day holiday.

Looking ahead, we expect domestic demand to remain soft. External developments, including the potential for lower global oil prices if a U.S.-Iran interim agreement holds, are unlikely to materially alter that outlook, as households remain partly insulated by domestic energy price caps. As such, we continue to see GDP growth slowing to 4.5% in 2026 and 4.3% in 2027, with policy support likely to remain targeted rather than broad-based.

Summary 6/29 – 7/3

Monday, Jun 29, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y May | 3.10% | 2.10% |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y May | 2.70% | 2.70% |

| 08:30 | GBP | M4 Money Supply M/M May | 0.20% | 0.20% |

| 08:30 | GBP | Mortgage Approvals May | 63K | 66K |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jun | 94.3 | 93.5 |

| 09:00 | EUR | Eurozone Industrial Confidence Jun | -7.8 | -8 |

| 09:00 | EUR | Eurozone Services Sentiment Jun | 2.5 | 2.2 |

| 09:00 | EUR | Eurozone Consumer Confidence Jun | -17.7 | -17.7 |

| 23:50 | JPY |

| Retail Trade Y/Y May | |

| Consensus | 3.10% |

| Previous | 2.10% |

| 08:00 | EUR |

| Eurozone M3 Money Supply Y/Y May | |

| Consensus | 2.70% |

| Previous | 2.70% |

| 08:30 | GBP |

| M4 Money Supply M/M May | |

| Consensus | 0.20% |

| Previous | 0.20% |

| 08:30 | GBP |

| Mortgage Approvals May | |

| Consensus | 63K |

| Previous | 66K |

| 09:00 | EUR |

| Eurozone Economic Sentiment Indicator Jun | |

| Consensus | 94.3 |

| Previous | 93.5 |

| 09:00 | EUR |

| Eurozone Industrial Confidence Jun | |

| Consensus | -7.8 |

| Previous | -8 |

| 09:00 | EUR |

| Eurozone Services Sentiment Jun | |

| Consensus | 2.5 |

| Previous | 2.2 |

| 09:00 | EUR |

| Eurozone Consumer Confidence Jun | |

| Consensus | -17.7 |

| Previous | -17.7 |

Tuesday, Jun 30, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | 1.30% | 1.20% |

| 23:30 | JPY | Unemployment Rate May | 2.50% | 2.50% |

| 23:50 | JPY | Industrial Production M/M May P | 0.60% | 0.50% |

| 01:00 | NZD | ANZ Activity Outlook Jun | 25.6 | |

| 01:00 | NZD | ANZ Business Confidence Jun | 10 | |

| 01:30 | AUD | Private Sector Credit M/M May | 0.60% | 0.70% |

| 01:30 | AUD | RBA Meeting Minutes | ||

| 01:30 | CNY | NBS Manufacturing PMI Jun | 50.2 | 50 |

| 01:30 | CNY | NBS Non-Manufacturing PMI Jun | 49.9 | 50.1 |

| 05:00 | JPY | Housing Starts Y/Y May | 32.10% | 11.40% |

| 06:00 | EUR | Germany Import Price Index M/M May | 0.60% | 1.20% |

| 06:00 | EUR | Germany Retail Sales M/M May | 0.00% | -0.30% |

| 06:00 | GBP | Current Account (GBP) Q1 | -21.5B | -18.4B |

| 06:00 | GBP | GDP Q/Q Q1 F | 0.60% | 0.60% |

| 06:00 | GBP | GDP Y/Y Q1 | 1.10% | 1.10% |

| 07:00 | CHF | KOF Leading Indicator May | 99.4 | 98 |

| 07:55 | EUR | Germany Unemployment Rate May | -1K | 6.30% |

| 07:55 | EUR | Germany Unemployment Change May | 8K | -12K |

| 12:00 | EUR | Germany CPI M/M Jun P | 0.10% | -0.20% |

| 12:00 | EUR | Germany CPI Y/Y Jun P | 2.50% | 2.60% |

| 12:30 | CAD | GDP M/M Apr | 0.40% | -0.10% |

| 13:00 | USD | Housing Price Index M/M Apr | 0.20% | 0.10% |

| 13:45 | USD | Chicago PMI Jun | 60 | 62.7 |

| 14:00 | USD | Consumer Confidence Jun | 94.2 | 93.1 |

| 23:01 | GBP |

| BRC Shop Price Index Y/Y Jun | |

| Consensus | 1.30% |

| Previous | 1.20% |

| 23:30 | JPY |

| Unemployment Rate May | |

| Consensus | 2.50% |

| Previous | 2.50% |

| 23:50 | JPY |

| Industrial Production M/M May P | |

| Consensus | 0.60% |

| Previous | 0.50% |

| 01:00 | NZD |

| ANZ Activity Outlook Jun | |

| Consensus | |

| Previous | 25.6 |

| 01:00 | NZD |

| ANZ Business Confidence Jun | |

| Consensus | |

| Previous | 10 |

| 01:30 | AUD |

| Private Sector Credit M/M May | |

| Consensus | 0.60% |

| Previous | 0.70% |

| 01:30 | AUD |

| RBA Meeting Minutes | |

| Consensus | |

| Previous | |

| 01:30 | CNY |

| NBS Manufacturing PMI Jun | |

| Consensus | 50.2 |

| Previous | 50 |

| 01:30 | CNY |

| NBS Non-Manufacturing PMI Jun | |

| Consensus | 49.9 |

| Previous | 50.1 |

| 05:00 | JPY |

| Housing Starts Y/Y May | |

| Consensus | 32.10% |

| Previous | 11.40% |

| 06:00 | EUR |

| Germany Import Price Index M/M May | |

| Consensus | 0.60% |

| Previous | 1.20% |

| 06:00 | EUR |

| Germany Retail Sales M/M May | |

| Consensus | 0.00% |

| Previous | -0.30% |

| 06:00 | GBP |

| Current Account (GBP) Q1 | |

| Consensus | -21.5B |

| Previous | -18.4B |

| 06:00 | GBP |

| GDP Q/Q Q1 F | |

| Consensus | 0.60% |

| Previous | 0.60% |

| 06:00 | GBP |

| GDP Y/Y Q1 | |

| Consensus | 1.10% |

| Previous | 1.10% |

| 07:00 | CHF |

| KOF Leading Indicator May | |

| Consensus | 99.4 |

| Previous | 98 |

| 07:55 | EUR |

| Germany Unemployment Rate May | |

| Consensus | -1K |

| Previous | 6.30% |

| 07:55 | EUR |

| Germany Unemployment Change May | |

| Consensus | 8K |

| Previous | -12K |

| 12:00 | EUR |

| Germany CPI M/M Jun P | |

| Consensus | 0.10% |

| Previous | -0.20% |

| 12:00 | EUR |

| Germany CPI Y/Y Jun P | |

| Consensus | 2.50% |

| Previous | 2.60% |

| 12:30 | CAD |

| GDP M/M Apr | |

| Consensus | 0.40% |

| Previous | -0.10% |

| 13:00 | USD |

| Housing Price Index M/M Apr | |

| Consensus | 0.20% |

| Previous | 0.10% |

| 13:45 | USD |

| Chicago PMI Jun | |

| Consensus | 60 |

| Previous | 62.7 |

| 14:00 | USD |

| Consumer Confidence Jun | |

| Consensus | 94.2 |

| Previous | 93.1 |

Wednesday, Jul 1, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jun F | 51.2 | 51.2 |

| 23:50 | JPY | Tankan Manufacturing Index Q2 | 16 | 17 |

| 23:50 | JPY | Tankan Non - Manufacturing Index Q2 | 35 | 36 |

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | 3.30% | |

| 00:30 | JPY | Manufacturing PMI Jun F | 54.9 | 54.9 |

| 01:30 | AUD | Building Permits M/M May | 0.20% | -3.40% |

| 01:45 | CNY | RatingDog Manufacturing PMI Jun | 52 | 51.8 |

| 05:00 | JPY | Consumer Confidence Index Jun | 34 | 33.6 |

| 06:30 | CHF | Real Retail Sales Y/Y May | 0.80% | 1.60% |

| 07:30 | CHF | Manufacturing PMI Index Jun F | 56.3 | 57.3 |

| 07:50 | EUR | France Manufacturing PMI Jun F | 50.7 | 50.7 |

| 07:55 | EUR | Germany Manufacturing PMI Jun F | 50 | 50 |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | 51.3 | 51.3 |

| 08:30 | GBP | Manufacturing PMI Jun F | 53.3 | 53.1 |

| 09:00 | EUR | Eurozone CPI Y/Y Jun P | 3.00% | 3.20% |

| 09:00 | EUR | Eurozone Core CPI Y/Y Jun P | 2.50% | 2.50% |

| 12:15 | USD | ADP Employment Change Jun | 118K | 122K |

| 13:45 | USD | Manufacturing PMI Jun F | 55.7 | 55.7 |

| 14:00 | USD | ISM Manufacturing PMI Jun | 54.2 | 54 |

| 14:00 | USD | ISM Manufacturing Prices Paid Jun | 79 | 82.1 |

| 14:00 | USD | ISM Manufacturing Employment Index Jun | 48.6 | |

| 14:00 | USD | Construction Spending M/M May | 0.30% | 0.40% |

| 14:30 | USD | Crude Oil Inventories (Jun 26) | -2.9M | -6.1M |

| 23:00 | AUD |

| Manufacturing PMI Jun F | |

| Consensus | 51.2 |

| Previous | 51.2 |

| 23:50 | JPY |

| Tankan Manufacturing Index Q2 | |

| Consensus | 16 |

| Previous | 17 |

| 23:50 | JPY |

| Tankan Non - Manufacturing Index Q2 | |

| Consensus | 35 |

| Previous | 36 |

| 23:50 | JPY |

| Tankan Large All Industry Capex Q2 | |

| Consensus | |

| Previous | 3.30% |

| 00:30 | JPY |

| Manufacturing PMI Jun F | |

| Consensus | 54.9 |

| Previous | 54.9 |

| 01:30 | AUD |

| Building Permits M/M May | |

| Consensus | 0.20% |

| Previous | -3.40% |

| 01:45 | CNY |

| RatingDog Manufacturing PMI Jun | |

| Consensus | 52 |

| Previous | 51.8 |

| 05:00 | JPY |

| Consumer Confidence Index Jun | |

| Consensus | 34 |

| Previous | 33.6 |

| 06:30 | CHF |

| Real Retail Sales Y/Y May | |

| Consensus | 0.80% |

| Previous | 1.60% |

| 07:30 | CHF |

| Manufacturing PMI Index Jun F | |

| Consensus | 56.3 |

| Previous | 57.3 |

| 07:50 | EUR |

| France Manufacturing PMI Jun F | |

| Consensus | 50.7 |

| Previous | 50.7 |

| 07:55 | EUR |

| Germany Manufacturing PMI Jun F | |

| Consensus | 50 |

| Previous | 50 |

| 08:00 | EUR |

| Eurozone Manufacturing PMI Jun F | |

| Consensus | 51.3 |

| Previous | 51.3 |

| 08:30 | GBP |

| Manufacturing PMI Jun F | |

| Consensus | 53.3 |

| Previous | 53.1 |

| 09:00 | EUR |

| Eurozone CPI Y/Y Jun P | |

| Consensus | 3.00% |

| Previous | 3.20% |

| 09:00 | EUR |

| Eurozone Core CPI Y/Y Jun P | |

| Consensus | 2.50% |

| Previous | 2.50% |

| 12:15 | USD |

| ADP Employment Change Jun | |

| Consensus | 118K |

| Previous | 122K |

| 13:45 | USD |

| Manufacturing PMI Jun F | |

| Consensus | 55.7 |

| Previous | 55.7 |

| 14:00 | USD |

| ISM Manufacturing PMI Jun | |

| Consensus | 54.2 |

| Previous | 54 |

| 14:00 | USD |

| ISM Manufacturing Prices Paid Jun | |

| Consensus | 79 |

| Previous | 82.1 |

| 14:00 | USD |

| ISM Manufacturing Employment Index Jun | |

| Consensus | |

| Previous | 48.6 |

| 14:00 | USD |

| Construction Spending M/M May | |

| Consensus | 0.30% |

| Previous | 0.40% |

| 14:30 | USD |

| Crude Oil Inventories (Jun 26) | |

| Consensus | -2.9M |

| Previous | -6.1M |

Thursday, Jul 2, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 22:45 | NZD | Building Permits May | 10.90% | |

| 23:50 | JPY | Monetary Base Y/Y Jun | -10.00% | -12.20% |

| 01:30 | AUD | Trade Balance (AUD) May | 2.18B | 1.79B |

| 06:30 | CHF | CPI M/M Jun | 0.10% | 0.20% |

| 06:30 | CHF | CPI Y/Y Jun | 0.50% | 0.60% |

| 09:00 | EUR | Eurozone Unemployment Rate May | 6.30% | 6.30% |

| 12:30 | USD | Initial Jobless Claims (Jun 26) | 218K | 215K |

| 12:30 | USD | Nonfarm Payrolls Jun | 114K | 172K |

| 12:30 | USD | Unemployment Rate Jun | 4.30% | 4.30% |

| 12:30 | USD | Average Hourly Earnings M/M Jun | 0.30% | 0.30% |

| 13:30 | CAD | Manufacturing PMI Jun F | 52.9 | |

| 14:00 | USD | Factory Orders M/M May | 2.10% | 4.80% |

| 14:30 | USD | Natural Gas Storage (Jun 26) | 81B | 76B |

| 22:45 | NZD |

| Building Permits May | |

| Consensus | |

| Previous | 10.90% |

| 23:50 | JPY |

| Monetary Base Y/Y Jun | |

| Consensus | -10.00% |

| Previous | -12.20% |

| 01:30 | AUD |

| Trade Balance (AUD) May | |

| Consensus | 2.18B |

| Previous | 1.79B |

| 06:30 | CHF |

| CPI M/M Jun | |

| Consensus | 0.10% |

| Previous | 0.20% |

| 06:30 | CHF |

| CPI Y/Y Jun | |

| Consensus | 0.50% |

| Previous | 0.60% |

| 09:00 | EUR |

| Eurozone Unemployment Rate May | |

| Consensus | 6.30% |

| Previous | 6.30% |

| 12:30 | USD |

| Initial Jobless Claims (Jun 26) | |

| Consensus | 218K |

| Previous | 215K |

| 12:30 | USD |

| Nonfarm Payrolls Jun | |

| Consensus | 114K |

| Previous | 172K |

| 12:30 | USD |

| Unemployment Rate Jun | |

| Consensus | 4.30% |

| Previous | 4.30% |

| 12:30 | USD |

| Average Hourly Earnings M/M Jun | |

| Consensus | 0.30% |

| Previous | 0.30% |

| 13:30 | CAD |

| Manufacturing PMI Jun F | |

| Consensus | |

| Previous | 52.9 |

| 14:00 | USD |

| Factory Orders M/M May | |

| Consensus | 2.10% |

| Previous | 4.80% |

| 14:30 | USD |

| Natural Gas Storage (Jun 26) | |

| Consensus | 81B |

| Previous | 76B |

Friday, Jul 3, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:00 | AUD | Services PMI Jun F | 49.9 | 49.9 |

| 00:30 | JPY | Services PMI Jun F | 51.8 | 51.8 |

| 01:45 | CNY | RatingDog Services PMI Jun | 53.6 | 54.4 |

| 06:45 | EUR | France Industrial Output M/M May | -0.30% | 0.10% |

| 07:50 | EUR | France Services PMI Jun F | 47.4 | 47.4 |

| 07:55 | EUR | Germany Services PMI Jun F | 46.8 | 46.8 |

| 08:00 | EUR | Eurozone Services PMI Jun F | 48.9 | 48.9 |

| 08:30 | GBP | Services PMI Jun F | 48.7 | 48.7 |

| 23:00 | AUD |

| Services PMI Jun F | |

| Consensus | 49.9 |

| Previous | 49.9 |

| 00:30 | JPY |

| Services PMI Jun F | |

| Consensus | 51.8 |

| Previous | 51.8 |

| 01:45 | CNY |

| RatingDog Services PMI Jun | |

| Consensus | 53.6 |

| Previous | 54.4 |

| 06:45 | EUR |

| France Industrial Output M/M May | |

| Consensus | -0.30% |

| Previous | 0.10% |

| 07:50 | EUR |

| France Services PMI Jun F | |

| Consensus | 47.4 |

| Previous | 47.4 |

| 07:55 | EUR |

| Germany Services PMI Jun F | |

| Consensus | 46.8 |

| Previous | 46.8 |

| 08:00 | EUR |

| Eurozone Services PMI Jun F | |

| Consensus | 48.9 |

| Previous | 48.9 |

| 08:30 | GBP |

| Services PMI Jun F | |

| Consensus | 48.7 |

| Previous | 48.7 |