Sample Category Title

EUR/USD and GBP/USD Advance on Reports of a US–Iran Agreement

European currencies are staging a solid recovery after a period of heightened demand for the US dollar, which had previously been supported by geopolitical tensions in the Middle East. Reports that the United States and Iran have reached preliminary agreements regarding a potential ceasefire and the normalisation of shipping through the Strait of Hormuz have significantly improved market sentiment and reduced investors’ appetite for safe-haven assets.

According to incoming reports, the two sides have moved closer to agreeing on the key terms of a potential deal that would include a cessation of hostilities and a gradual stabilisation of the regional situation. Although the final memorandum is not expected to be signed until 19 June in Geneva, the progress in negotiations itself has been viewed as a positive signal by market participants. Against this backdrop, demand for the US dollar as a safe-haven asset has eased somewhat, allowing both the euro and the pound to recover from their recent declines.

Additional support for European currencies may come from today’s macroeconomic releases. Investors will be closely monitoring the publication of the ZEW Economic Sentiment Indices for Germany and the euro area. Any improvement in business confidence and economic sentiment could strengthen the euro’s position, particularly after a period of elevated uncertainty.

EUR/USD

From a technical perspective, EUR/USD continues to recover after testing a key support zone. The pair has managed to hold above important levels and is now attempting to develop a bullish correction. Further price action will depend on whether buyers can establish a foothold above nearby resistance levels and confirm the formation of a more sustainable recovery.

A move and close above 1.1620 could open the way towards 1.1660–1.1690. Failure to secure gains above 1.1620 may result in a retest of the recent low near 1.1600.

Key events for EUR/USD:

- Today at 12:00 (GMT+3): Germany ZEW Current Conditions Index;

- Today at 12:30 (GMT+3): German 5-year Bobl bond auction;

- Tomorrow at 15:30 (GMT+3): US Housing Starts.

GBP/USD

GBP/USD is also showing positive momentum. Sterling is benefiting not only from improving global risk appetite but also from expectations that the UK economy will remain relatively resilient. At the same time, market participants continue to monitor signals from the Bank of England and the outlook for the central bank’s monetary policy.

Technical analysis of GBP/USD points to the possibility of a move towards 1.3460–1.3500 if the 1.3400 level turns into support. A decisive break below the 1.3400–1.3380 area could trigger another test of the 1.3300 level.

Key events for GBP/USD:

- Today at 17:00 (GMT+3): Atlanta Fed GDPNow indicator;

- Tomorrow at 09:00 (GMT+3): UK Consumer Price Index (CPI);

- Tomorrow at 11:30 (GMT+3): UK House Price Index.

The easing of geopolitical tensions between the United States and Iran has allowed European currencies to recover after recent pressure from the US dollar. However, the continuation of the upward moves in EUR/USD and GBP/USD will depend both on incoming economic data from Europe and the United States and on further progress in negotiations between Washington and Tehran. For now, market sentiment remains moderately positive, although fresh fundamental developments are likely to determine the next directional move.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Hang Seng Underperforms on Weak China’s Retail Sales, USD/JPY Firmed Above 159.75 After BoJ

Key takeaways

- Markets embraced a strong risk-on rally after the US and Iran agreed on a framework to extend the ceasefire for 60 days and fully reopen the Strait of Hormuz, sharply reducing geopolitical and energy-related inflation risks.

- Technology stocks reclaimed market leadership, with the Nasdaq 100 surging 3% as investors rotated back into mega-cap growth names, supported by lower oil prices, Nvidia’s planned US$20 billion bond offering, and continued enthusiasm around AI infrastructure spending.

- Attention now shifts to central bank policy, particularly the inaugural FOMC meeting under Fed Chair Kevin Warsh, as markets assess whether lower energy prices are sufficient to temper expectations for a potential Fed rate hike later this year.

- Chart of the day: USD/JPY minor uptrend remains intact above 159.75 key support as it probes the 160.65 intervention risk level.

Chart of the day - USD/JPY’s minor uptrend remains intact

Fig. 1: USD/JPY minor trend as of 16 Jun 2026 (Source: TradingView). The information presented is historical information, and past performance is not indicative of future performance.

The price action of USD/JPY is holding at its 20-day moving average after its prior two retests on it on 12 June and 15 June, indicating a “cautious” minor bullish impulsive up move sequence as USD/JPY continues to probe its recent intervention level of 160.65 (see Fig. 1).

Watch the 159.75 key short-term pivotal support to maintain the near-term bullish tone on USD/JPY towards the key intermediate resistance at 160.65, and above it, the 161.14/120 resistance is next to watch.

However, a break and an hourly close below 159.75 invalidates the bullish tone, opening the door to a minor drop towards the next intermediate supports at 159.45 and 159.10/158.80 (also the 50-day moving average).

Top macro headlines

- The US and Iran agreed to a framework to extend the ceasefire for 60 days and fully reopen the Strait of Hormuz: Global supply chains and financial markets captured an extraordinary sigh of relief on Monday. Both sides had confirmed the establishment of a 60-day structural framework to completely halt conflict operations, fully reopen the Strait of Hormuz, and negotiate over Iran’s nuclear enrichment programme during the 60-day window. Formal signing of the agreement is expected on Friday, 19 June in Switzerland.

- Wall Street rallies and the Nasdaq 100 jumps 3% as the geopolitical premium dissipates: Risk appetite returned to the global equity landscape with extreme force. Driven by the breakthrough in the Persian Gulf, the S&P 500 surged nearly 2% to approach its best single-session performance since April, while the tech-heavy Nasdaq 100 jumped a massive 3.0% and the Dow Jones Industrial Average rocketed to a brand-new historic all-time high.

- Crude oil collapses below $85 as energy inflation fears evaporate: Global energy benchmarks capitulated as the threat of an extended military blockade dissolved. West Texas Intermediate (WTI) and Brent crude plunged steeply, with US crude settling at $81.17/bbl. The swift deflation of input energy costs has immediately recalculated near-term upstream inflation targets for global manufacturing sectors.

- NVIDIA set to raise $20 Billion in landmark corporate bond debut: Highlighting the massive, ongoing capital demands of global artificial intelligence infrastructure projects, Reuters reported that chip giant Nvidia is coming to the U.S. debt market to raise $20 billion. The offering, consisting of seven tranches maturing in 2056, represents the firm’s first major corporate bond sale in five years, arranged by Goldman Sachs, J.P. Morgan, and Morgan Stanley.

Key macro themes

- Structural deflation of the Persian Gulf shock: The core structural mechanism steering multi-asset allocations on Monday was the aggressive extraction of the geopolitical stagflation premium. The formal signature of the US-Iran memorandum immediately altered intermediate inflation expectations by removing the immediate threat of a prolonged blockage of global trade choke points. As energy prices retreated beneath critical psychological supports, macro traders dramatically unwound bets on defensive commodities and scaled back expectations for emergency tightening metrics from developed-market central banks.

- The transition to the Warsh Fed era and Wednesday’s Dot Plot: Despite the massive relief rally catalysed by plunging oil prices, market participants are keeping focus pinned on Wednesday’s monumental FOMC meeting, marking newly appointed Federal Reserve Chair Kevin Warsh’s inaugural interest rate decision. Fed funds futures traders are still expecting around a 70% chance of a 25 bps rate hike to come in December, despite the cooling energy complex, while market participants widely expect the committee to keep the benchmark rate unchanged at 3.50% to 3.75% on Wednesday, 17 June. The market will look to see whether Chair Warsh removes the historical easing bias from the median dot plot, particularly given that headline metrics like May CPI reached a three-year high of 4.2%.

- Intraday breadth and the Tech leadership resurgence: Monday’s price action represented a tactical interruption to the “Great Rotation” of 2026. While recent weeks had seen institutional funds steadily exit overextended large-cap growth names to deploy into small-cap value and industrial cyclicals, the sheer velocity of the geopolitical relief bounce immediately drew capital right back into high-beta technology blocks. Powered by stabilised energy inputs and massive primary issuances such as NVIDIA’s $20 billion bond placement and SpaceX’s robust post-IPO secondary performance, mega-cap growth recaptured near-term liquidity dominance.

Global markets impact (last 24 hours)

Equities: The S&P 500 climbed nearly 2.0% in its best single-session performance since April. The tech-heavy Nasdaq 100 led global benchmarks with a vertical 3.0% surge, while the blue-chip Dow Jones Industrial Average scaled new historic highs. In contrast, energy producers lagged significantly (-3.6% for the S&P Energy sector).

Fixed Income: Sovereign bonds caught a wave of structural re-buying as hawkish rate-hike fears subsided alongside energy metrics. The policy-sensitive US two-year Treasury yield dropped by 2 bps to settle at 4.07% on Monday, 15 June. In Europe, Germany’s 10-year Bund yield and the UK 10-year Gilt yield edged lower by 3 bps and 1 bps, reflecting broader macro decompression.

FX: The U.S. Dollar Index (DXY) traded on a softer tone but held its 20-day moving average, acting as a key intermediate support at 99.50. The British pound underperformed, trading almost unchanged at 1.3412 against the US dollar; earlier intraday gains were wiped out amid political risk in the UK (uncertainty surrounding PM Starmer’s fate).

The Japanese yen remained weak at 160.20 per US dollar as the BoJ hiked its policy rate by 25 bps, as expected, to 1%, a 31-year high, and offered a dovish element, saying it will pause its JGB taper from April 2027.

Commodities: WTI and Brent crude oil tumbled and broke below key medium-term supports of $85.50/bbl and $86.25/bbl. Lower energy prices reduced the stagflation risk narrative, allowing precious metals to extend their corrective rebound into a third consecutive session. Gold rallied 2.1% to close at $4,308/oz on Monday, 15 June, below its 20-day moving average ($4,405/oz).

Asia Pacific impact

- APAC tech and export hubs join global resurgence: Regional stock benchmarks across Japan, South Korea, and Taiwan experienced pronounced institutional capital inflows on Tuesday morning. Local export-oriented entities captured intense upside momentum, responding directly to the 3.0% vertical surge across the New York mega-cap technology space. Nikkei 225 (+0.6%), KOSPI (+2.1%), and TAIEX (+0.7%).

- China and Hong Kong underperform due to weak domestic consumption: China’s retail sales for May plummeted into negative territory (-0.6% y/y), the first time since December 2022, indicating very weak consumer sentiment and spending, as the Labour Day holiday in early May failed to offset the weakness. China A50 (-0.5%), and the Hang Seng Index (-1.3%).

- Regional Currencies Bounce from Low Floors: The South Korean Won and the Indonesian Rupiah showed clear signs of stabilisation. The rapid retreat in the global dollar index and the sharp deflation of crude oil import prices have materially alleviated structural balance-of-payments pressures across non-OPEC emerging economies.

- BOJ JGB Program under scrutiny: Japanese fixed-income markets traded calmly after the BoJ’s latest monetary policy decision to pause its JGB tapering programme from April 2027. The 10-year JGB yield continues to stabilise at 2.64% after spiking to a 30–year high of 2.75% in May 2026.

Top 3 events to watch today

- RBA Interest Rate Decision & Press Conference - 12.30 pm & 1.30 pm SGT Impact: AUD/USD, AUD crosses, ASX 200

- Germany Zew Economic Sentiment (Jun) - 5:00 pm SGT (consensus: -6, May; -10.2) Impact: EUR/USD, EUR crosses, DAX

- US Housing Starts (May) - 8:30 pm SGT (consensus: 1.43M, Apr: 1.465M) Impact: USD, US stock indices

US-Iran Deal Paves Way to Reopen Hormuz – BoJ Hikes to 1.0%

In Focus Today

The US-Iran deal is in the spotlight after a series of overnight updates. The agreement has effectively been signed, ending the US naval blockade of Iranian ports, reopening the Strait of Hormuz and launching 60 days of nuclear talks. Trump said ships are already moving and Hormuz will be fully open by Friday, though mine clearance will take time. Passage is expected to be toll-free for at least 60 days, with Iran and Oman managing the strait thereafter. Details remain unclear, and Israel's leadership and Hezbollah's ongoing attacks underscore persistent regional tensions.

In Sweden, the NIER releases its economic forecast, providing an update on consumer and business sentiment and, crucially, new information on price plans, which are highly important for the Riksbank.

In Germany, the ZEW survey is released and will provide a first assessment of sentiment in June. Though it remains at low historical levels, the May survey was slightly better than expected as expectations improved.

Economic and Market News

What Happened Overnight

In Japan, the Bank of Japan (BoJ) raised its policy rate by 25bps to 1.0%, the highest level since 1995. The vote split was 7-1, with Governor Ueda absent due to hospitalization. The BoJ signaled further rate hikes and outlined a gradual reduction in JGB purchases, effectively pausing quantitative tightening from 2027. Market reaction was modest, leaving USD/JPY just above 160 and keeping intervention risk alive ahead of tomorrow's FOMC meeting, with Deputy Governor Uchida now in focus.

China's latest monthly releases underscored a deepening two-speed economy. Retail sales fell from 0.2% y/y in April to -0.6% y/y in May, while property investment slumped further and new home prices continued to decline, although sales appear to be stabilizing. In contrast, industrial production accelerated to 4.5% y/y from 4.1% y/y. The figures argue for more consumer stimulus, but Beijing may refrain as external demand and technology continue to underpin growth and deflationary pressures have eased.

In Australia, the RBA left its policy rate unchanged at 4.35%, in line with market expectations. This follows a 25bp hike in May, the third increase in 2026, as the RBA responds to persistent inflationary pressures. Higher energy prices linked to the Middle East conflict and broader capacity pressures are key drivers. The unemployment rate rose in April, although other labour market indicators remain relatively resilient, while growth in consumer spending is slowing.

What Happened Yesterday

ECB speeches: Lagarde described the US-Iran ceasefire as "good news" if confirmed, potentially easing energy tensions, but warned that key issues remained unresolved. Nagel saw no near-term relief for euro area inflation, noting that oil supply normalization would take months and keeping all rate options open. Kazimir stressed that oil-related damage could not be reversed quickly and signaled that further monetary tightening was likely.

In Sweden, unemployment measured by the Labour Force Survey rose to 8.8% in May from 8.5% in April. The survey has become increasingly volatile, and Statistics Sweden has noted that non-response composition may have led to overestimated unemployment in March and underestimated employment in March and April. By contrast, the Public Employment Service's less volatile statistics have shown unchanged unemployment for five consecutive months.

Equities: Who would have imagined European equities underperforming on the day of the Iran peace headlines? However, that is exactly what happened. European equities started strongly only to grind lower throughout the session. By the closing bell, the Stoxx 600 was only 0.2% higher. Rate-sensitive sectors and styles underperformed; banks outperformed real estate, large caps outperformed small caps, and so on. This was not the textbook reversal where companies most negatively affected by higher energy prices or rates staged the strongest rebound. Instead, the sector rotation was more consistent with cyclical outperformance funded by defensives, reflecting the surprisingly limited reaction in bond markets.

The limited reaction in European equities stands out even more in contrast to the much stronger move in US markets. There, equities ended sharply higher with the S&P 500 gaining 1.7%, helped by a rebound in technology shares, while consumer discretionary, materials and industrial stocks also advanced around 1%. Memory and semiconductor names rallied strongly, with Micron, AMD and Lam Research gaining around 10% in a single session.

FI and FX: The BoJ hiked rates by 25bps to 1.00% as expected, the highest policy rate since 1995, and signaled further hikes ahead. USD/JPY showed very little reaction and continues to trade above the 160 threshold, as the move was widely anticipated. Brent crude is trading broadly unchanged around USD 83/bbl. European rates stabilized yesterday after the initial rally, while US Treasury yields have started to move higher again this morning, with the 10-year yield back near Friday's closing levels. China published a batch of data showing a concerning picture of weakening consumer demand. Trump and JD Vance have signed an electronic copy of the memorandum of understanding, although very few details of the agreement have been released.

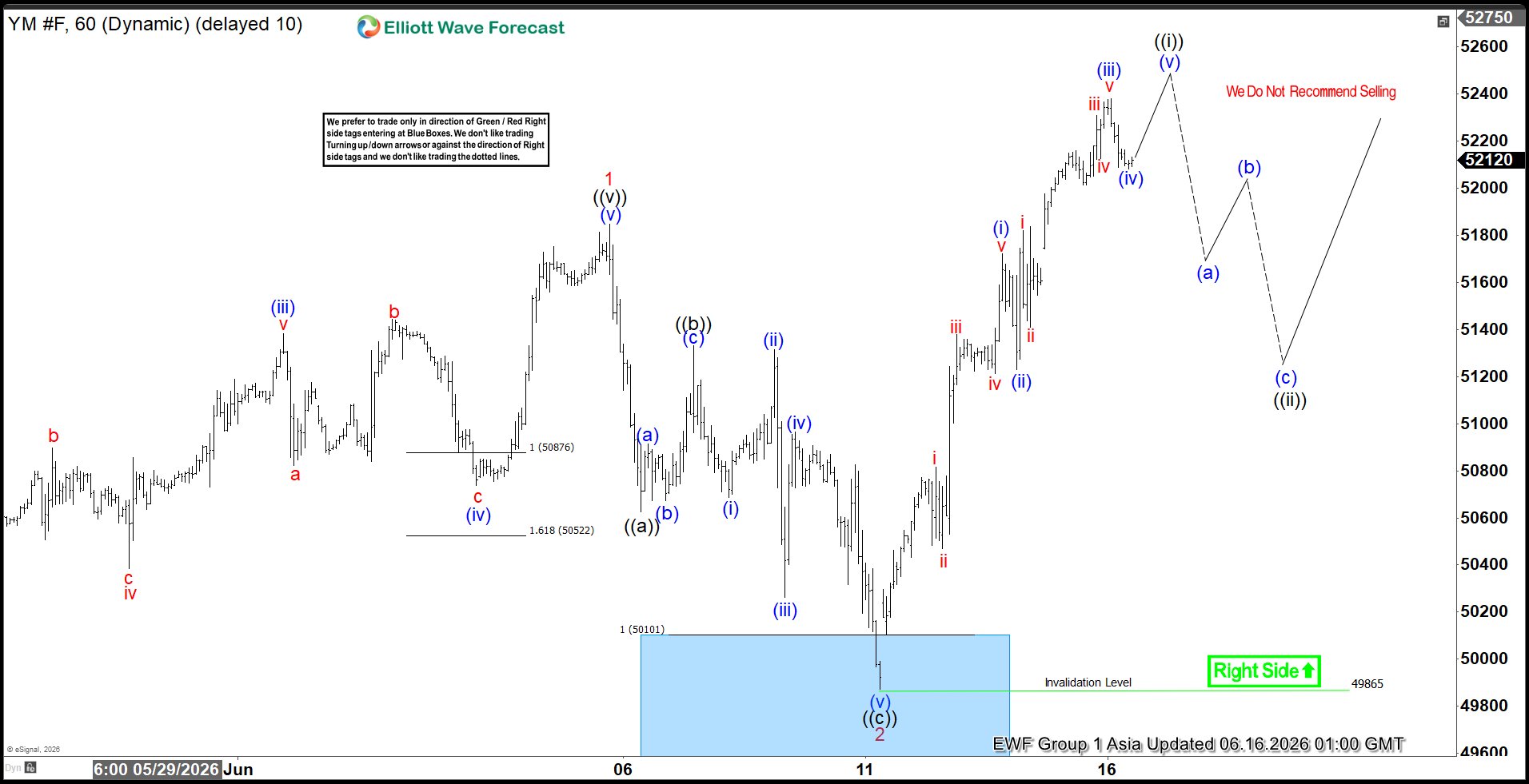

Elliott Wave View: Dow Futures (YM) Breakout Signals Start of New Bullish Phase

Dow Futures (YM_F) ended their correction against the cycle from the March 30, 2026 low and extended higher. The rally from that low completed wave 1. The pullback in wave 2 unfolded as a zigzag Elliott Wave structure. Within this correction, wave ((a)) ended at 50624, wave ((b)) concluded at 51331, and wave ((c)) finished at 49865. This sequence confirmed the completion of wave 2 at a higher degree.

The Index has since resumed higher in wave 3. From the end of wave 2, wave (i) reached 51723, while the pullback in wave (ii) ended at 51230. The advance continued with wave (iii) finishing at 52380. The subsequent pullback in wave (iv) is proposed complete at 52080. Near term, expectations favor another leg higher in wave (v). That move should complete wave ((i)) of the larger degree. Afterward, a corrective phase in wave ((ii)) is anticipated. This correction will address the cycle from the June 11, 2026 low before the broader rally resumes.

As long as price remains above 49865, pullbacks should attract buyers. Corrective phases are expected to resolve within 3, 7, or 11 swings. This reinforces the bullish outlook and supports further upside potential.

Dow Futures (YM_F) 60-Minute Elliott Wave Chart

YM_F Elliott Wave Video:

https://www.youtube.com/watch?v=K1xiAKuAZlk

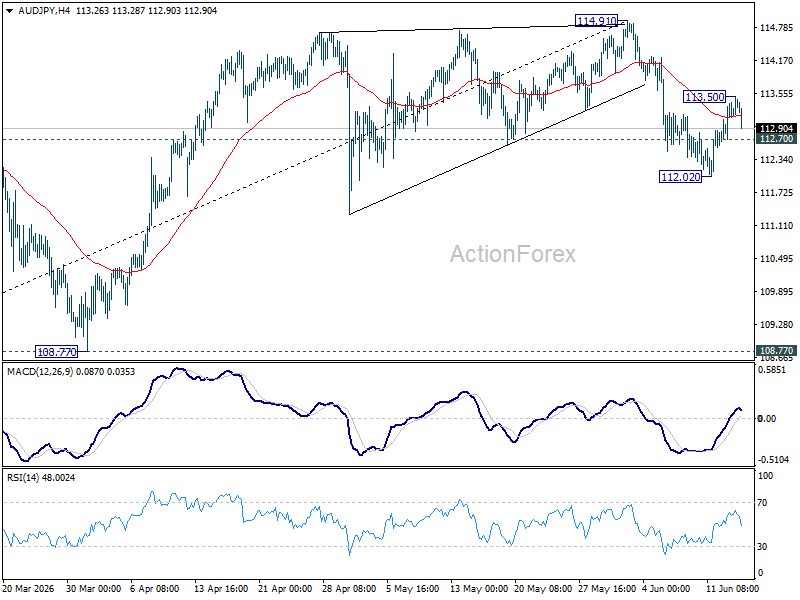

AUD/JPY Weakens After BoJ Hike and RBA Hold, Risks Build Towards 112 and Below

The Bank of Japan hiked. The Reserve Bank of Australia paused. Neither decision surprised markets. Yet the reaction in AUD/JPY may be telling a more important story.

The cross drifted lower after the BoJ raised rates by 25 basis points to 1.00%, the highest level since 1995, while the RBA kept rates unchanged at 4.35%. On paper, neither outcome represented a major policy surprise. But traders appear to have come away more convinced that Japan's normalization cycle still has room to run than that Australia is preparing another near-term rate increase. That subtle shift in expectations is beginning to work against AUD/JPY.

The BoJ's message was straightforward. Inflation risks are still tilted to the upside, helped by higher energy costs and a weak Yen. However, the 7-1 vote also highlighted ongoing caution within the Board, with one member arguing that risks to growth and employment outweighed inflation concerns. There was no strong signal that policymakers are preparing to accelerate tightening. Instead, the market's base case remains another rate increase by the end of the year. Even so, that is enough to keep the Yen supported.

The RBA, meanwhile, delivered what can best be described as a hawkish hold. Officials warned that inflation remains too high and acknowledged that higher fuel costs are feeding into broader prices. But they also pointed to slowing consumer spending, softer housing activity and signs that tighter policy is gaining traction. The statement kept the door open to another hike if needed, yet stopped well short of signaling that August is the likely timing. For traders hoping for a stronger tightening signal, that was a disappointment.

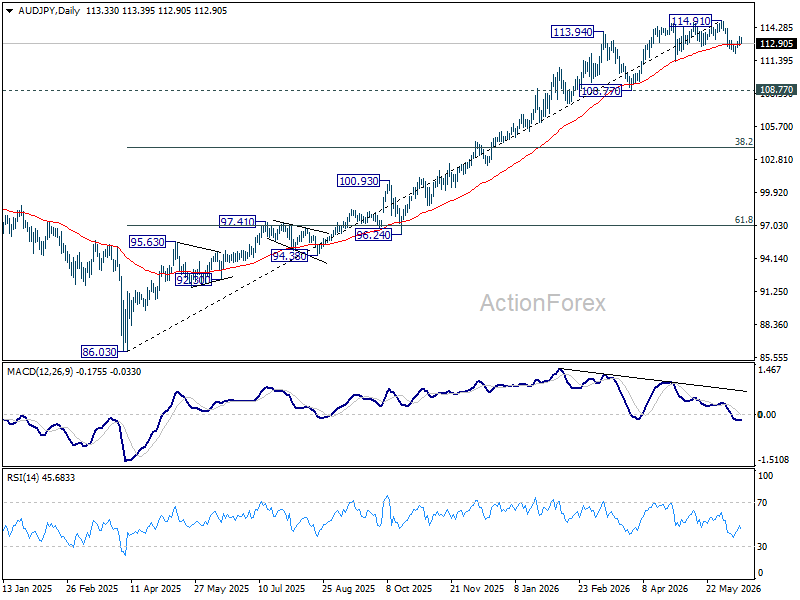

Technically, the picture is becoming more interesting. AUD/JPY has slipped below its 55 4H EMA, raising the possibility that the recovery from 112.02 to 113.50 has already run its course. A break of 112.70 would expose the 112.02 low, while a decisive move below that support would confirm that the decline from 114.91 is resuming.

The bigger risk lies beyond the short-term charts. Bearish divergence on D MACD is visible. If AUD/JPY breaks 112.02 and establishes itself below 55 D EMA (now at 112.83) sustainably, the case for a medium-term correction would strengthen considerably. In that scenario, a move back toward 108.77 becomes increasingly plausible.

The policy gap between Australia and Japan remains wide, but it is no longer moving decisively in Australia's favor. That may be the first warning sign that AUD/JPY's powerful rally is finally running out of steam.

RBA Holds at 4.35% but Keeps Tightening Bias Alive

The Reserve Bank of Australia left the cash rate unchanged at 4.35% as widely expected, with the accompanying statement carried a distinctly hawkish tone. While policymakers acknowledged that financial conditions have tightened following three rate hikes this year and that the economy is slowing as expected, they repeatedly stressed that inflation remains a problem. The Board noted that "headline and underlying inflation are still too high" and warned that "inflation is likely to remain high for some time."

A key focus of the statement was the impact of the Middle East energy shock. The RBA said that "higher fuel prices have added directly to inflation" and that there are signs these costs are now "passing through to the prices of other goods and services." It also cautioned that the resolution of the conflict remains "at an early stage" and that global oil supply issues "will take some time to resolve," suggesting policymakers are not yet ready to assume a rapid easing in inflation pressures.

Still, the statement stopped short of signaling that another rate hike is imminent. The Board highlighted slowing consumer spending, softer housing market conditions and a higher-than-expected unemployment rate as evidence that tighter policy is gaining traction. The overall message is more hawkish than a simple hold, but not hawkish enough to make an August hike the base case.

Instead, the RBA appears content to wait for additional data while retaining an explicit tightening bias, reiterating that "it will do what it considers necessary to achieve that outcome, including increasing the cash rate target further if required".

(RBA) Statement by the Reserve Bank Board: Monetary Policy Decisions

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.35 per cent.

Inflation picked up materially in the second half of 2025, and information since the beginning of this year confirms that some of the increase reflected greater capacity pressures. The latest data show that headline and underlying inflation are still too high. Oil prices have eased in recent weeks, although energy and most related commodity prices remain higher than they were prior to the conflict in the Middle East. There are signs that some firms experiencing cost pressures are increasing the prices of their goods and services and others are looking to do so. Short-term measures of inflation expectations have eased but remain higher than earlier in the year.

Financial conditions have tightened this year in response to three increases in the cash rate target. Money market interest rates and government bond yields have risen, and the exchange rate has appreciated. There are signs that growth in consumer spending is slowing as expected and momentum in the housing market has shifted, with housing prices falling in some capital cities. The unemployment rate was higher than expected in April, but other measures of labour market conditions have been more resilient. Growth in business investment is strong and credit is readily available to both households and businesses.

There continue to be heightened uncertainties about the outlook for domestic economic activity and inflation. Resolution of the conflict in the Middle East is at an early stage, and there are plausible scenarios where inflation is higher and activity lower than envisaged under the May baseline forecasts. Global oil supply issues will take some time to resolve, maintaining upward pressure on global energy prices and inflation. At the same time, a period of prolonged uncertainty may also cause growth to be lower in Australia’s major trading partners and in Australia.

Decision

As expected, the disruption to global oil supply is having an impact on inflation. Higher fuel prices have added directly to inflation and there are indications that this is passing through to the prices of other goods and services, so inflation is likely to remain high for some time. This inflation impulse is in addition to the high inflation recorded around the start of 2026, reflecting capacity pressures in the economy.

The Board remains focused on ensuring that inflation does not become embedded once the impulse from higher oil prices has passed through. To achieve this, growth in demand needs to slow to reduce capacity pressures and help bring inflation back to target. Following the three increases in the cash rate target since the beginning of the year, financial conditions are now tighter than they were, and there are signs that the economy is slowing as expected. But inflation is still too high and the Board judged that it was appropriate to leave the cash rate target unchanged while it assesses the response to previous interest rate rises and the impact of the oil supply disruption.

The Board will be attentive to the data and the evolving assessment of the outlook and risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand and the outlook for inflation and the labour market. Monetary policy is well placed to respond to developments and the Board is focused on its mandate to deliver price stability and full employment. It will do what it considers necessary to achieve that outcome, including increasing the cash rate target further if required.

Today’s policy decision was unanimous.

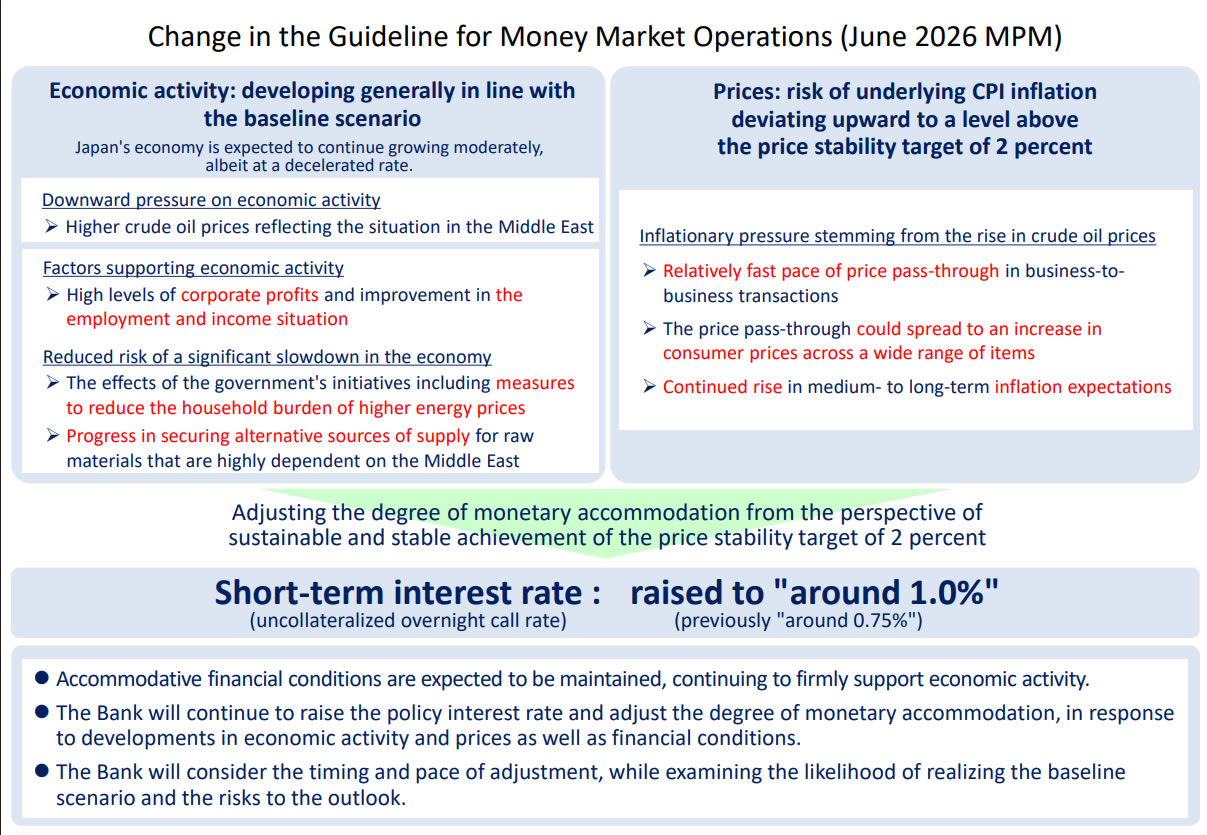

BoJ Reaches Key Milestone With First 1% Interest Rate Since 1995

The Bank of Japan raised its policy rate by 25 basis points to 1.00%, as widely expected, marking the highest interest rate level in 31 years and the first time since 1995 that rates have reached 1%. The move follows December's increase from 0.50% to 0.75% and represents another step in the central bank's gradual normalization process after decades of ultra-loose monetary policy.

The decision was approved by a 7-1 majority vote. Board member Toichiro Asada dissented, arguing that downside risks to production and employment stemming from the Middle East situation outweighed upside risks to inflation. He therefore favored leaving policy unchanged. The meeting was also notable for the absence of Governor Kazuo Ueda, who is currently hospitalized for treatment of a hepatic cyst infection, leaving other policymakers to guide communications around the decision.

Alongside the rate increase, the BoJ announced adjustments to its government bond purchase program. The central bank will continue reducing Japanese government bond purchases by around JPY 200bn per quarter through March 2027, maintaining its current pace of quantitative tightening. However, from April 2027 onward, it plans to slow the pace of reductions, a move that comes as long-term Japanese bond yields have risen sharply in recent months.

Under the revised plan, monthly bond purchases will decline to around JPY 2.1tn by the January-March quarter of 2027. The combination of a rate hike and a more cautious approach to future balance-sheet reduction suggests the BoJ remains committed to policy normalization, while also seeking to avoid excessive volatility in the government bond market. Markets will now look to July's updated projections and the eventual return of Ueda for clearer guidance on how far rates could rise from here.

China’s Retail Sales Fall for First Time Since 2022 as Domestic Demand Slumps

China's latest activity data painted a mixed picture of the economy in May, with stronger factory output masking a sharp deterioration in domestic demand. Industrial production accelerated from 4.1% yoy to 4.5% yoy, beating market expectations of 4.2%y yoy and suggesting manufacturers continued to expand output despite slowing conditions elsewhere in the economy.

The more concerning developments came from consumption and investment. Retail sales dropped from 0.2% yoy to -0.6% yoy, marking the first year-on-year decline in more than three years.

Fixed-asset investment also weakened significantly, falling from -1.6% ytd yoy to -4.1% ytd yoy. The property sector remained a major drag, with real estate investment inflows down -16.2% in the first five months of the year. Manufacturing investment slipped into contraction for the first time since late 2020, while infrastructure spending also declined.

The divergence reinforces concerns that China's growth model remains heavily reliant on production while domestic demand struggles to gain traction. In an unusually direct assessment, the statistics bureau described the imbalance between strong supply and weak demand as "acute." The comments suggest policymakers may face increasing pressure to introduce measures aimed at supporting employment and household spending, particularly as investment activity continues to lose momentum.

| Indicator | Apr | May | Expected |

|---|---|---|---|

| Industrial Production Y/Y | 4.1% | 4.5% | 4.2% |

| Retail Sales Y/Y | 0.2% | -0.6% | 0.0% |

| Fixed Asset Investment YTD Y/Y | -1.6% | -4.1% | -2.0% |

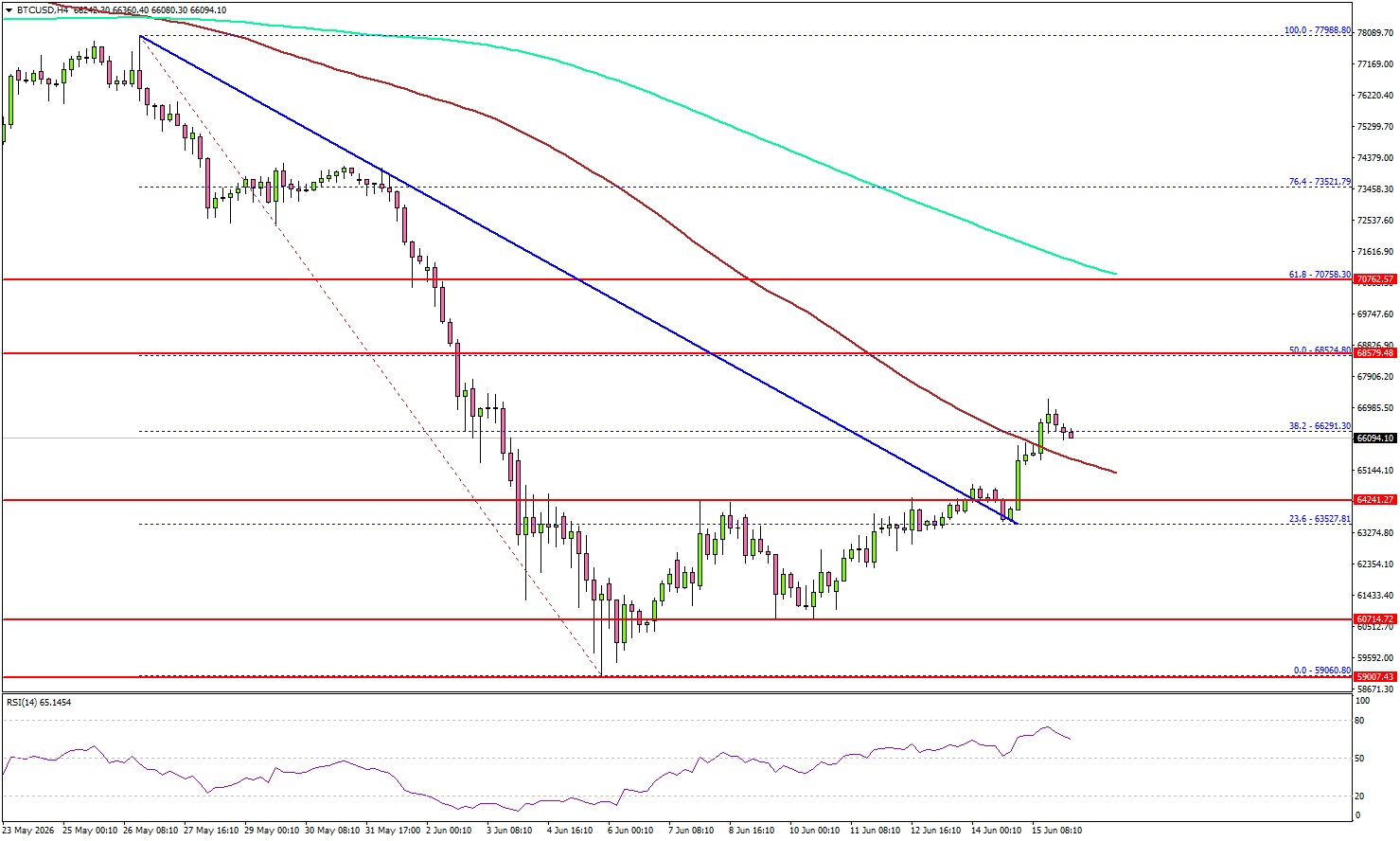

Bitcoin Climbs Off the Lows, Facing a Wall of Resistance Ahead

Key Highlights

- Bitcoin tested $60,000 before it started a recovery wave.

- BTC/USD traded above a bearish trend line with resistance at $62,500 on the 4-hour chart.

- Ethereum recovered by over 10% and climbed above $1,750.

- WTI Crude Oil prices extended losses and traded below $82.00.

Bitcoin Price Technical Analysis

Bitcoin price extended losses and tested $60,000 against the US Dollar. BTC formed a base above $60,000 and recently recovered some losses.

Looking at the 4-hour chart, the price climbed above the $62,500 and $63,500 resistance levels. The price traded above a bearish trend line with resistance at $62,500. It opened the doors for a move above the 38.2% Fib retracement level of the downward move from the $77,988 swing high to the $59,060 low.

Moreover, the price surpassed the $65,000 level and the 100 simple moving average (red, 4-hour). If the price extends gain, there could be a test of the 50% Fib retracement level at $68,500.

The main resistance sits near $70,000 and the 200 simple moving average (green, 4-hour). A close above $70,000 could send the price toward $73,200. Any more gain might call for a test of $75,000.

If there is a fresh decline, immediate support might be $65,000 and the 100 simple moving average (red, 4-hour). The first key support could be $64,200. The main breakdown support could be $63,500. A downside break below $63,500 might start another decline. The next major support might be $60,000, below which BTC could decline toward $58,000.

Looking at Ethereum, the price also started a recovery wave and was able to surpass the $1,750 resistance zone.

Today’s Key Economic Releases

- US Import Price Index for May 2026 (MoM) – Forecast +1.0%, versus +1.9% previous.

- US Export Price Index for May 2026 (MoM) – Forecast +1.2%, versus +3.3% previous.

- US Housing Starts for May 2026 (MoM) – Forecast 1.430M, versus 1.465M previous.

- US Building Permits for May 2026 (MoM) – Forecast 1.420M, versus 1.423M previous.