Sample Category Title

Swiss CPI slows to 0.1% yoy in October, broad decline in prices

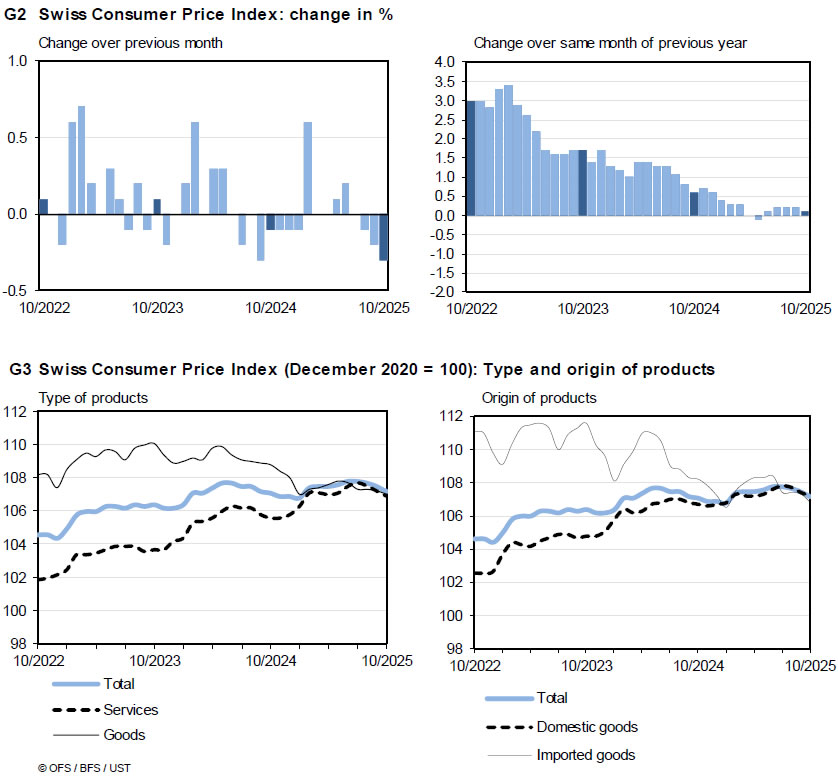

Swiss inflation cooled further in October, with headline CPI slipping -0.3% mom — weaker than expectations of -0.1% mom. Annual inflation eased to just 0.1% yoy from 0.2% yoy, undershooting forecasts of 0.3% yoy. The data confirmed that price pressures remain virtually absent.

Core inflation also weakened notably, falling -0.2% mom and slowing to 0.5% yoy from 0.7% yoy. Both domestic and imported prices fell during the month, by -0.2% mom and -0.5% mom respectively, suggesting broad-based softness. The sharper decline in imported prices reflects the strong franc’s continued dampening effect on imported goods and energy costs, while domestic components also showed only marginal resilience.

OPEC Says Enough

Last week ended with slowing appetite after the Federal Reserve (Fed) cast doubt on another 25bp cut in December and Big Tech earnings failed to impress investors despite beating lofty expectations. But nearly two-thirds of S&P 500 companies have already reported earnings, showing more than 10% year-on-year growth — higher than analysts had expected and marking the fourth consecutive quarter of double-digit earnings growth, according to FactSet. Despite the hectic week, the S&P500 still closed up about 0.71%, while the Nasdaq 100 extended gains by 2% to a fresh high.

The energy sector, in particular, ended the week on a stronger note after Exxon and Chevron reported earnings on Friday. Both companies beat expectations, driven mainly by solid production growth and operational execution despite headwinds from lower oil prices. Exxon leaned heavily into growth (Guyana/Permian) and raised its dividend, while Chevron’s more conservative focus on cash flow, share buybacks, and dividends — combined with the Hess deal — resonated well with investors. SPDR’s energy fund — which tanked after the April tariff announcement, then regained pre-announcement levels before falling again in September — has managed to hold support near a critical Fibonacci retracement level. It tested the 50-DMA to the upside but failed to close above that mark as concerns about the low-price environment kept bulls from extending their bets.

US crude found buyers near the $60 pb level last week, keeping prices above pre-sanction levels, though the 50-DMA continues to cap the topside amid ample supply from OPEC and the Americas and uncertain global demand. The Paris-based IEA projects that global oil supply will rise by around 3 mbpd this quarter and reach a record glut next year. Perhaps in response, OPEC announced over the weekend that it will halt additional supply between January and March, following a 137 K bpd increase in December. That decision helped US crude start the week on a positive note, though bulls still look hesitant to break key technical levels. The $62–$62.15 pb range — which includes the minor 23.6% Fibonacci retracement of the June–October slump and the 50-DMA — will likely remain a tough ceiling for now. That stands in interesting contrast to clean-energy funds, which have performed well since the April dip despite the White House’s pushback against alternative energy sources. VanEck’s Global Clean Energy ETF has jumped more than 60% since April and still trades at a 24% discount to its 2022 peak.

In the medium run, AI-related electricity demand should continue to boost appetite for energy providers — traditional, alternative, and nuclear alike. AI demand is expected to add hundreds of terawatt-hours of consumption over the next decade, on top of growing demand from emerging markets. Energy remains an intriguing play — regardless of which type of energy you prefer or support financing.

Speaking of AI, another week begins with strong appetite for AI-related stocks. Korean tech names are leading gains this Monday morning after Nvidia announced late last week — as promised earlier — that it would supply over 260’000 chips to South Korea’s government and leading firms, including Samsung Electronics and SK Group. The deal is estimated to be worth between $8 billion and $12 billion for GPU supply alone. Samsung is up more than 3% this morning, SK Hynix more than 10%. Even Korean chicken-related companies got a boost after Jensen Huang was spotted eating chicken with Hyundai and Samsung executives. Nasdaq futures, meanwhile, are trading higher and leading gains into the European open. Voila.

This week, in the continued absence of US data due to the ongoing government shutdown — which, by Thursday, will become the longest in history — investors will keep their focus on earnings. In tech, Palantir and AMD (which recently announced deals with Nvidia) and Qualcomm (which just revealed plans to enter the AI-chip market to compete with Nvidia) will head to the earnings confessionals. McDonald’s and Shopify, meanwhile, will help investors gauge US consumer dynamics as concerns rise over consumer health amid perceived weakness in the jobs market and early cracks in housing.

The US Dollar remains relatively strong despite the underlying noise. A more hawkish Fed outlook last week helped the greenback recover part of this year’s losses, but its rebound also reflects heavy sell-offs in two major peers: the Japanese yen and the pound sterling. The yen weakened on expectations that Takaichi will support continued easy monetary policy, while sterling came under pressure on budget concerns ahead of the Autumn Statement and growing odds that the Bank of England (BoE) may need to intervene sooner rather than later to prevent a deeper economic downturn.

The BoE meets this week and is expected to leave rates unchanged, but there’s now a growing chorus suggesting the bank could deliver a surprise cut — or at least sound dovish enough to confirm Cable’s medium-term bearish trend below the critical 1.3140 Fibonacci level.

US Fed Governors Divided Over Rate Path as December Decision Looms

In focus today

From the US, the October ISM Manufacturing index is due for release. The flash PMI released earlier, and the regional Fed indices point to a small uptick. Private-sector data remains in focus in the US amid the shutdown-driven delays in public data releases. US Treasury will publish the first part of its quarterly refunding announcement (QRA) today, containing its latest borrowing estimates and cash balance targets for Q4 and Q1.

In Australia, the Reserve Bank of Australia is expected to keep its policy rate unchanged early Tuesday morning, in line with market and analyst expectations.

In Sweden, the week begins with the release of the October manufacturing PMI today. Recent economic data pointed towards an uptick in activity, and a confirmation of the very strong manufacturing PMI outcome from last month (55.6) would further support this story. On Wednesday, we will get the services PMI numbers and the Riksbank is publishing their monetary policy rate decision. Everything but an unchanged rate of 1.75% would be a huge surprise. Finally, preliminary October inflation figures are scheduled for release on Thursday.

On Thursday, focus will turn to the central bank meetings in Norges Bank and Bank of England.

Economic and market news

What happened since Friday

In the US, the first Fed comments after last week's meeting have shed light into what Powell described as 'strongly differing views' across the committee. On the dovish end, Governor Waller (voter) emphasized that current data does not signal a need to stop cutting and that he still advocates for a rate cut in December. Atlanta Fed's Bostic (non-voter) was more cautious, saying he only 'eventually got behind [last week's] cut' and that he agrees with Powell saying December cut is not a foregone conclusion. On the hawkish end, both Cleveland Fed's Hammack and Dallas Fed's Logan (both 2026 voters) stated they did not see the need for cutting rates last week. Kansas City Fed's Schmid (who voted against the cut) emphasized that 'policy is only modestly restrictive and still needs to lean against demand'. Markets are pricing around 60% probability for a December cut, but we believe the Fed will end up pausing its easing cycle.

In China, manufacturing PMIs for October disappointed with declines in both the official version released on Friday as well as the private RatingDog PMI. Especially the official NBS PMI weakened with a decline from 49.8 to 49.0 (consensus 49.6) while RatingDog PMI manufacturing dropped from 51.2 to 50.6 (consensus 50.7). A reversal in the export order index was behind the decline, which may be related to the threat of 100% tariffs by US President Donald Trump in the first part of October. After some months of improvement in RatingDog PMI, the momentum seems to be fading, albeit not faltering. Other signals still underpin decent manufacturing activity, such as a rise in metal prices in the past two months, a strong reading for Emering Industries PMI in October as well as a rise in the China CKGSB business confidence.

In the euro area, HICP inflation declined to 2.1% y/y in October as expected by consensus. Core inflation surprised on the topside by holding steady at 2.4% y/y (cons: 2.3% y/y). The decline in headline inflation was thus due to lower food and energy inflation while services inflation rose to 3.4% y/y from 3.2% y/y. We expect euro area inflation to average 2.1% in the final quarter of the year before falling below target next year.

In Norway, the unemployment rate (SA) jumped from 2.1% to 2.2% in October, marginally higher than expected. This is also slightly higher than Norges Bank's forecast from the September MPR at 2.1% and should be dovish for the monetary policy outlook. The number of (fully) unemployed increased by c 200 persons in October, signalling a moderate weakness in the labour market. The number of new vacancies dropped sharply, indicating lower demand for labour.

In geopolitics, reports indicate that the Trump administration has finalised plans for targeted strikes on Venezuelan military installations as well as ports and airports linked to drug cartels, following months of military buildup in the Caribbean. With 10,000 troops and advanced military assets already in the region there is speculation that strikes could occur soon. However, Secretary of State Marco Rubio and President Trump have dismissed these reports as false, with Rubio calling it a 'fake story'. While the alleged strikes are expected to focus on narcotics-related sites, we believe risk assets may see volatility, with USD strengthening and Latin American credit spreads widening. However, the broader market impact is expected to remain limited barring major disruptions to global trade or commodity flows.

In the global oil market, OPEC+ agreed to a modest output increase of 137,000 bpd for December while pausing further hikes in early 2026 due to oversupply concerns. New sanctions on Russian producers have added uncertainty to forecasts, and the group aims to stabilise prices, which recently rebounded to USD 65 per barrel from a five-month low of USD 60. The group will reassess its strategy in a meeting on 30 November.

Equities: Equities were mixed on Friday. In fact, equities were mixed throughout last week. Asia has continued to impress, with the Korean Kospi up 7% in a single week! US has climbed, with S&P 500 0.3% higher on Friday (helped by Amazon being up +10% on report) and just below +1% higher for the week. Meanwhile, Europe and Nordics lagged behind, trading somewhat lower on Friday and for the week, with Helsinki the outlier - up an impressive 8% the last month following reports. Bottom line: regional allocation has really mattered in the past months.

Last week centred around tech earnings where the takeaway must be that with +1% on the index, markets handled significantly jacked up capex projections very well. On top of this, the hawkish surprise of Fed delaying the next rate cut, while markets had hoped for December, tested markets. Friday brought further news on this, with a flurry of hawkish FOMC commentary. Admittedly, there has been a lot of good things to balance this; lowered tariffs, an end to QT, strong earnings and AI-linked revenues not least. Nonetheless, some of the risks we flagged when lowering our risk recommendation somewhat in October have now played out, which could warrant a more constructive stance.

FI and FX: JPY and USD rose on Friday vis-à-vis EUR and Scandies on a day when overall risk sentiment was mixed. EUR/USD fell to around 1.1520, EUR/SEK rose to around 10.95 and EUR/NOK towards 11.70. The 10Y US yield held steady just below 4.10 ahead of this week's quarterly refunding announcement. Short-term EUR rates fell as the market digested Thursday's ECB meeting.

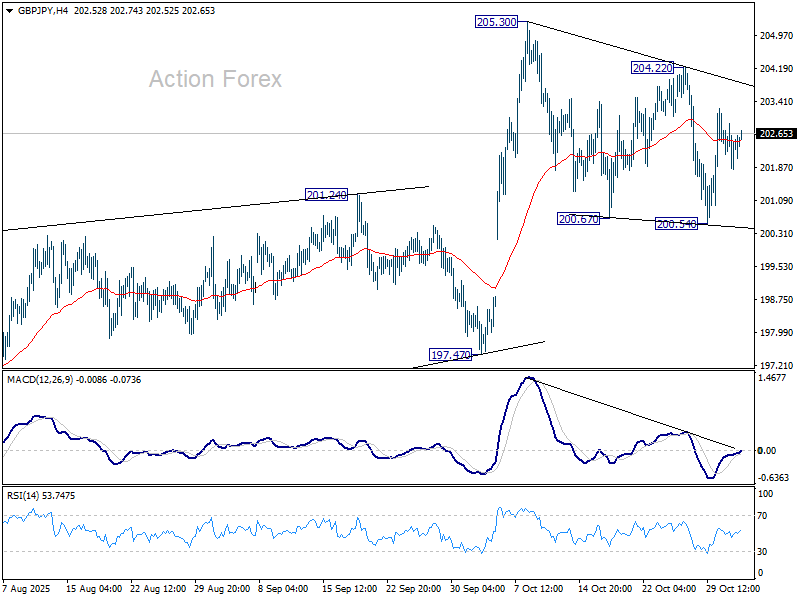

GBP/JPY Daily Outlook

Daily Pivots: (S1) 201.93; (P) 202.42; (R1) 203.00; More...

Intraday bias in GBP/JPY remains neutral for the moment, and further rise is expected. Break of 204.22 will will suggest that rise from 184.35 is resuming through 205.30 towards 208.09 high. However, break of 200.54 will extend the fall from 205.30 to 197.47 key structural support.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.

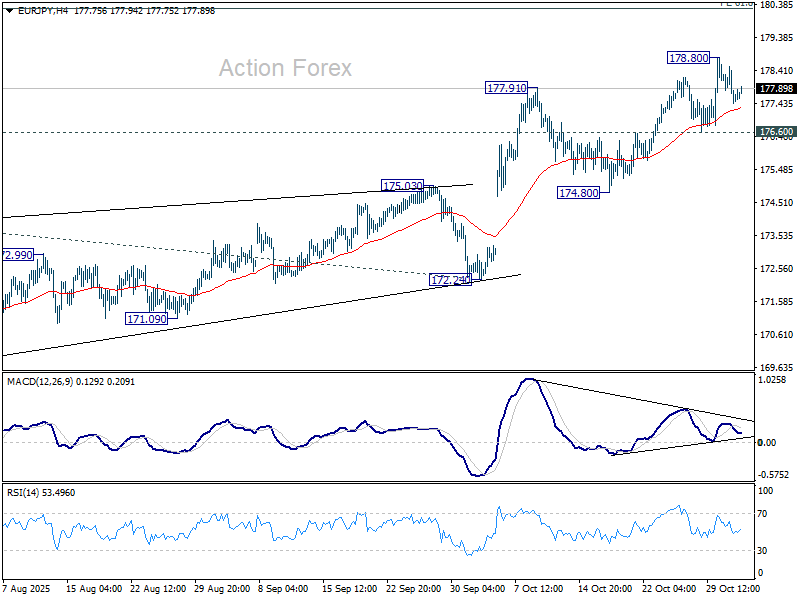

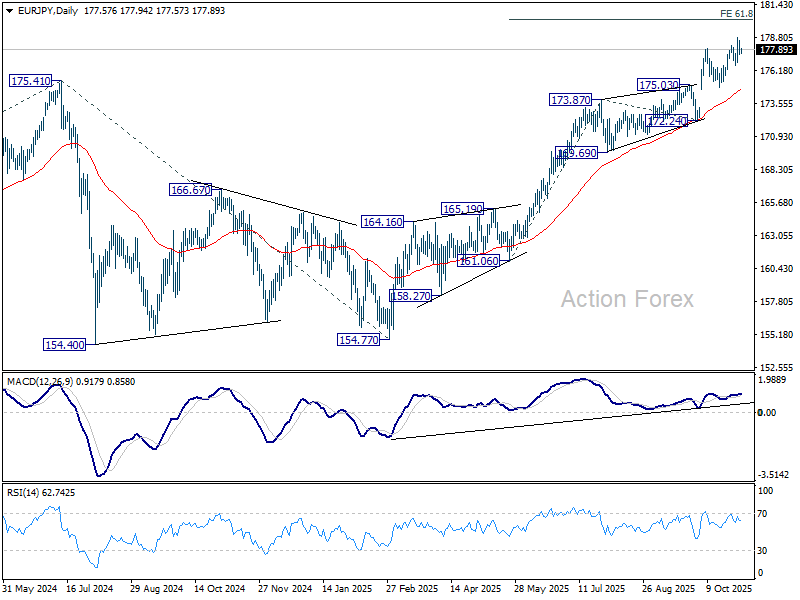

EUR/JPY Daily Outlook

Daily Pivots: (S1) 177.27; (P) 177.92; (R1) 178.38; More...

Intraday bias in EUR/JPY remains neutral and more consolidations could be seen below 178.80. Downside of pullback should be contained above 174.80 support. On the upside, break of 178.80 will extend the up trend to 61.8% projection of 161.06 to 173.87 from 172.24 at 180.15 next. However, considering bearish divergence condition in 4H MACD, firm break of 176.60 will bring deeper correction to 174.80 support instead.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Firm break of 172.24 support will suggests that it has turned into consolidations again. But still, outlook will continue to stay bullish as long as 55 W EMA (now at 167.87) holds, even in case of deep pullback.

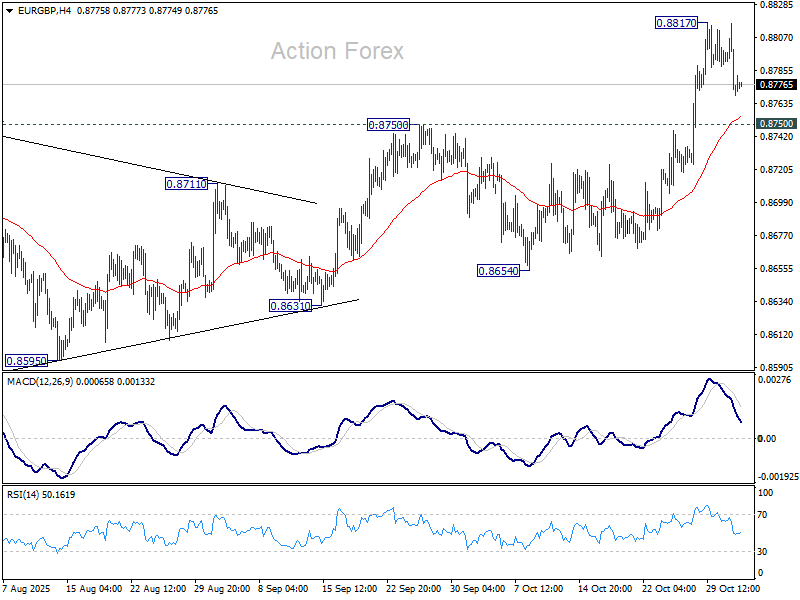

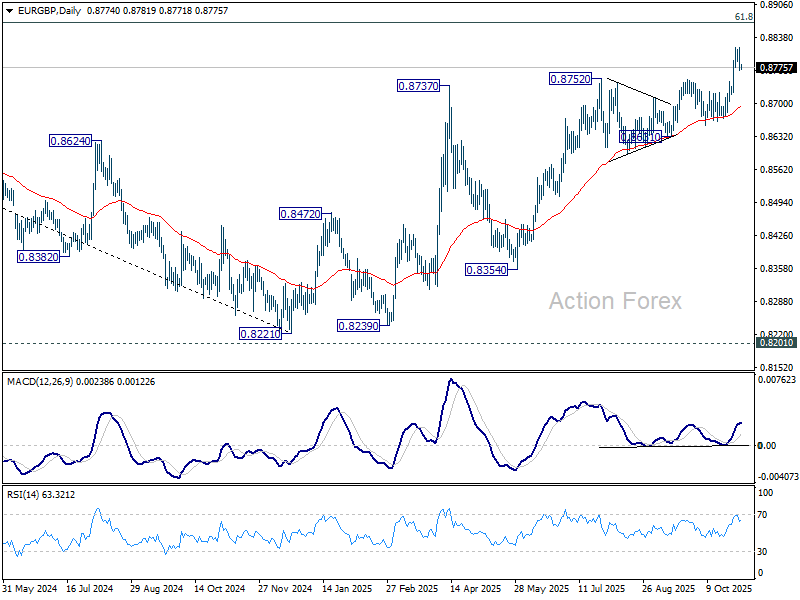

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8785; (P) 0.8799; (R1) 0.8809; More…

Intraday bias in EUR/GBP remains neutral and more consolidations could be seen below 0.8817. Further rally is expected as long as 0.8750 resistance turned above holds. Above 0.8817 will target 0.8867 fibonacci level. Firm break there will carry larger bullish implications. Nevertheless, sustained break of 0.8750 will turn bias back to the downside for 0.8654 support instead.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Firm break of 0.8654 support will be the first sign that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high).

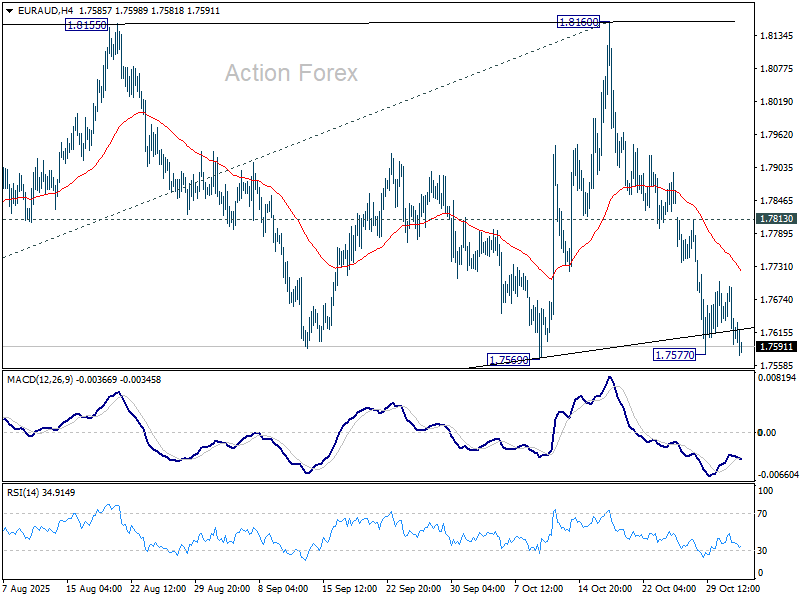

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7584; (P) 1.7641; (R1) 1.7685; More...

Intraday bias in EUR/AUD remains neutral first. On the downside, firm break of 1.7569 support will solidify the case that corrective pattern from 1.8554 is already in the third leg. Deeper fall should then be seen to 1.7254 support next. For now, risk will remain on the downside as long as 1.7813 minor resistance holds.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Sustained break of 55 W EMA (now at 1.7406) will suggest that it's correcting the whole rally from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922. Nevertheless, strong rebound form 55 W EMA will likely bring resumption of the up trend sooner.

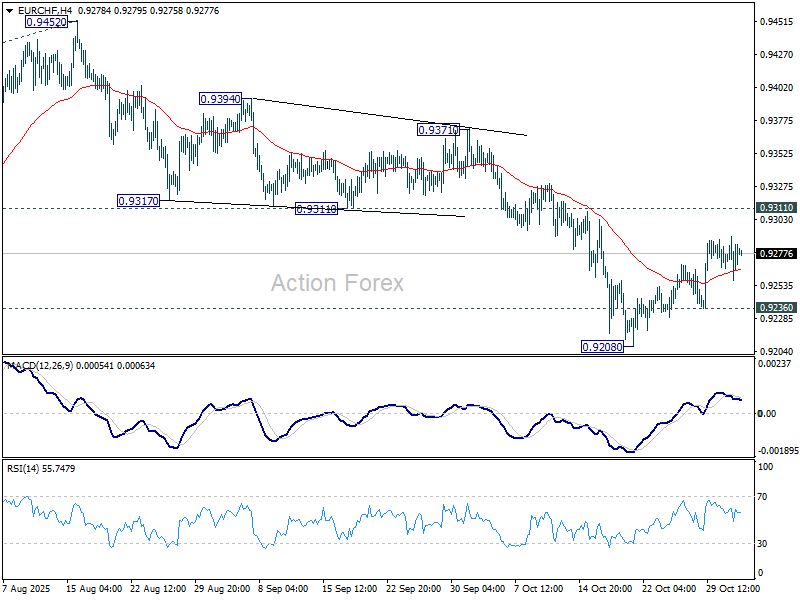

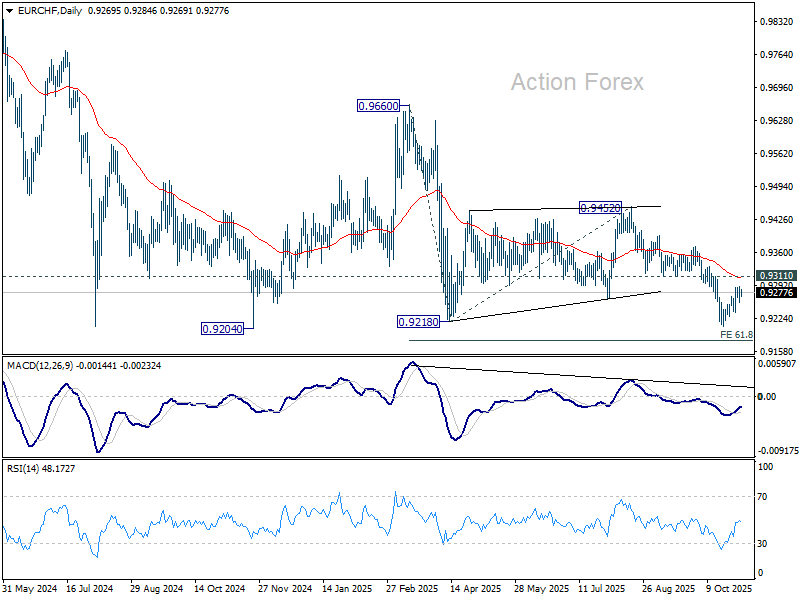

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9264; (P) 0.9278; (R1) 0.9297; More....

Intraday bias in EUR/CHF remains neutral for the moment. Price action from 0.9208 is seen as a corrective pattern, and upside should be limited by 0.9311 support turned resistance. On the downside, below 0.9236 minor support will bring retest of 0.9204/8 support zone. Firm break there will resume larger down trend to 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179. However, sustained break of 0.9311 will bring stronger rebound back to 0.9371 resistance instead.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9386). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming.

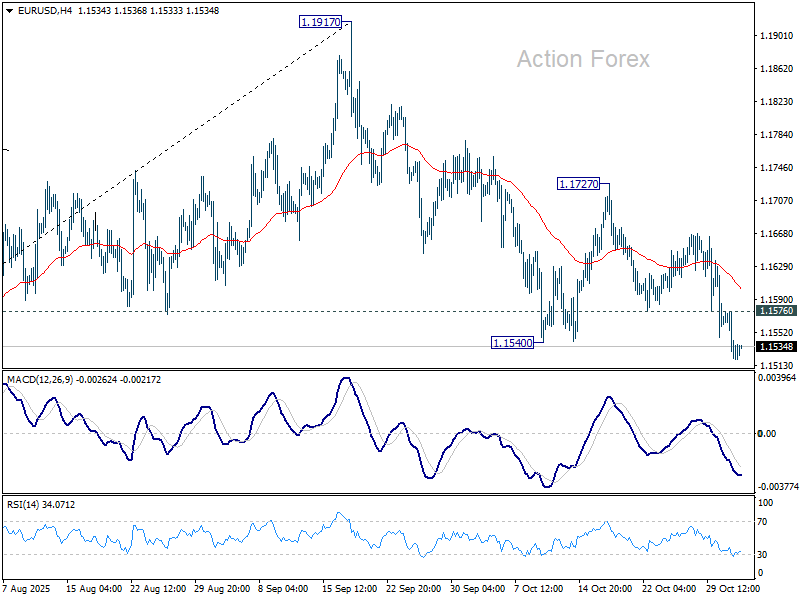

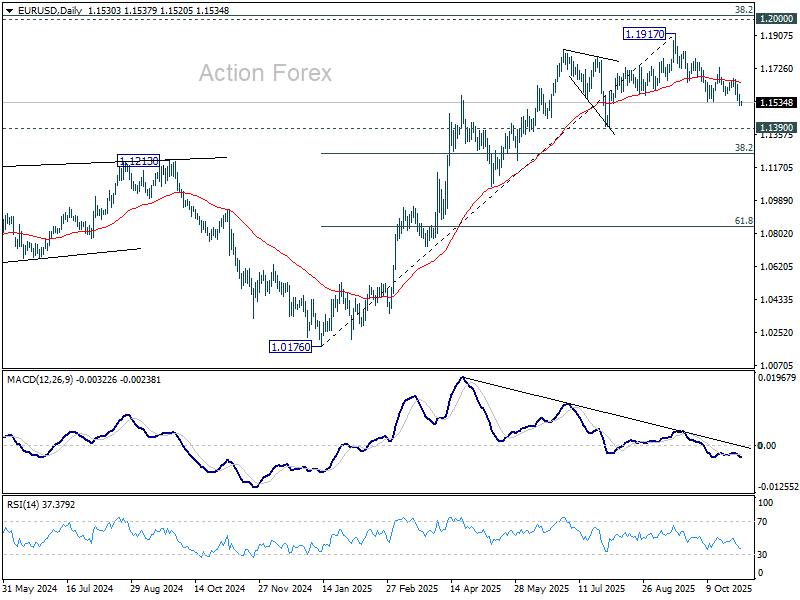

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1513; (P) 1.1545; (R1) 1.1569; More…

Intraday bias in EUR/USD remains on the downside at this point. Current fall from 1.1917 should target 1.1390 support. Break there will extend the decline to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1576 minor resistance will turn bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1306) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

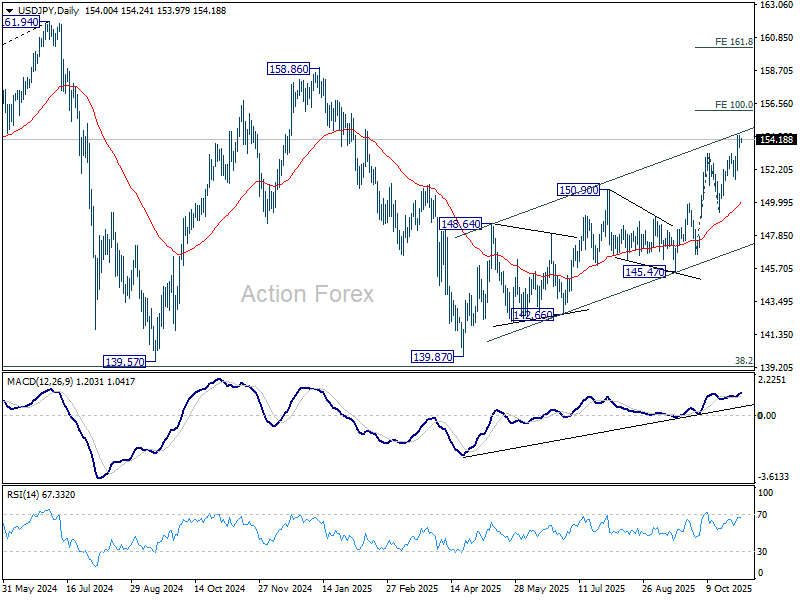

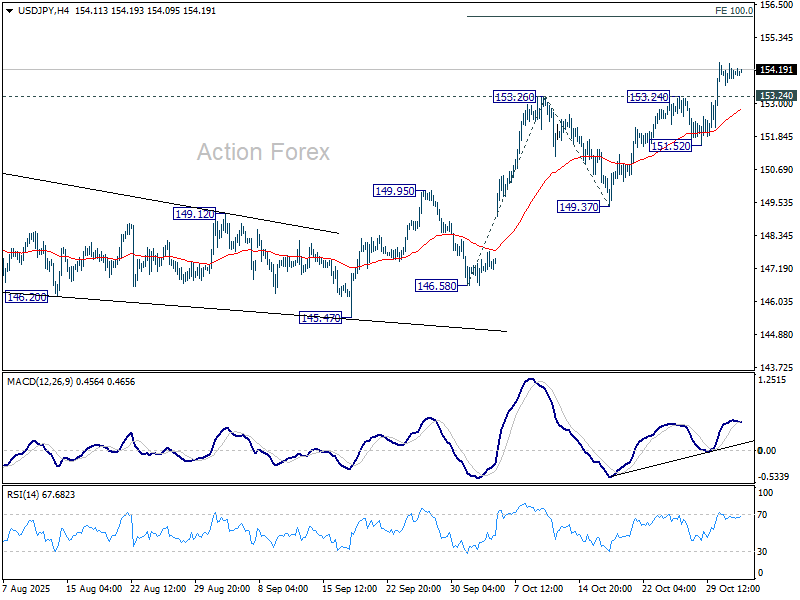

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.64; (P) 154.03; (R1) 154.39; More...

Intraday bias in USD/JPY stays on the upside for 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Firm break there will extend the rally from 139.87 to 158.86 resistance next. On the downside, below 153.24 resistance turned support will turn intraday bias neutral first. But outlook will stay bullish as long as 151.52 support holds, in case of retreat.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.