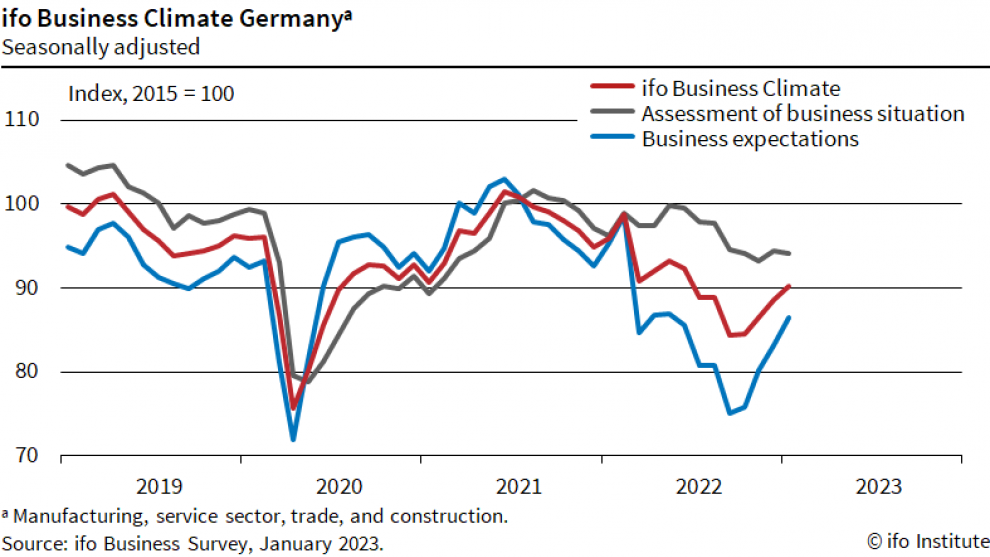

Germany Ifo Business Climate rose slightly from 88.6 to 90.2 in January, below expectation of 90.5. Current Assessment ticked down from 94.4 to 94.1, below expectation of 95.0. Expectations index, on the other hand, improved from 83.2 to 86.4, above expectation of 85.0.

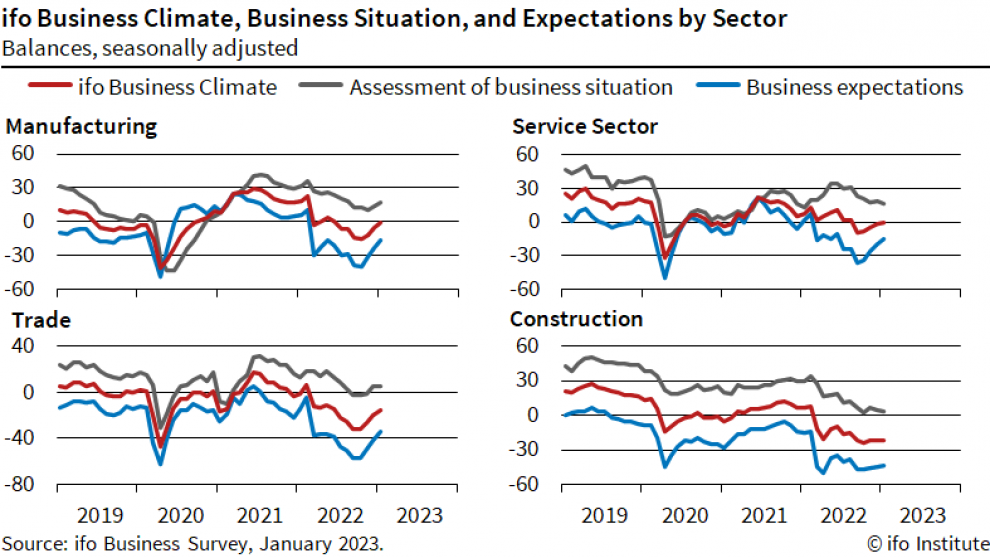

By sector, manufacturing rose from -5.7 to -0.7. Services rose from -1.2 to 0.2. Trade rose from -20.0 to -15.4. Construction also rose slightly from -21.9 to -21.6.

Ifo said: “Sentiment in the German economy has brightened. The ifo Business Climate Index rose to 90.2 points in January, up from 88.6 points in December. This is due to considerably less pessimistic expectations. Companies were, however, somewhat less satisfied with their current situation. The German economy is starting the new year with more confidence.”

ECB Makhlouf: Need to take similar steps to Dec in Feb and Mar

ECB Governing Council member Gabriel Makhlouf said, “We need to continue to increase rates at our meeting next week – by taking a similar step to our December decisions – and also at our March meeting, although our future policy decisions need to continue to be data-dependent given the prevailing uncertainty.”

“Raising the policy rate also signals our commitment to price stability,” Makhlouf added. “It sends a clear message that we will not allow inflation to stay above 2 per cent and helps to contain inflation expectations, guarding against the emergence of self-reinforcing inflation dynamics and tackling the risk of a persistent increase in inflation expectations.”

Separately, Bundesbank President Joachim Nagel said, “For February and March, we have announced that we will raise interest rates sharply again. Then we will look at where the inflation rate is in the spring and what our experts’ forecast looks like. I wouldn’t be surprised if we have to keep raising rates even after the two announced steps.”