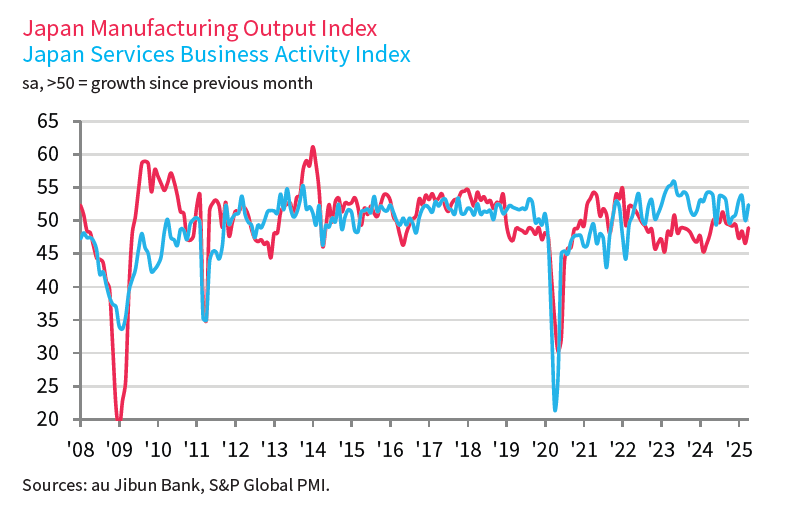

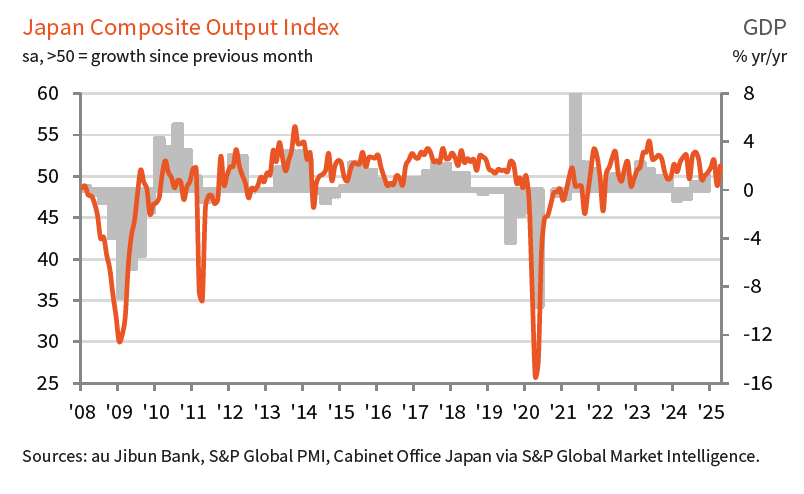

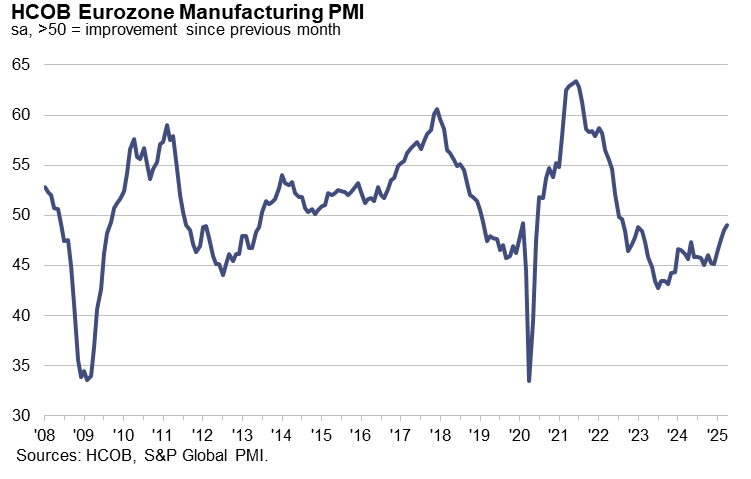

Japan’s private sector returned to expansion in April, as the final PMI Composite rose to 51.2 from March’s 48.9. The improvement was driven entirely by the services sector, with its PMI climbing to 52.4, while manufacturing remained in contraction.

According to S&P Global’s Annabel Fiddes, stronger services activity helped offset the drag from factories, where new orders fell sharply in response to the global tariff environment.

While services firms reported stronger demand, confidence among both services and manufacturing sectors deteriorated. Businesses expressed concern about the broader global outlook and the negative implications of recent US tariff moves on growth potential.

Adding to the pressure, input price inflation accelerated to a two-year high, prompting firms to raise selling prices to protect margins.

NZ employment grow 0.1% in Q1, wages growth cool

New Zealand’s employment grew just 0.1% qoq as expected, while the unemployment rate held steady at 5.1%, better than forecast of 5.3%.

However, the quality of employment deteriorated, with a notable shift from full-time to part-time roles. Over the year, full-time employment dropped by -45k while part-time roles increased by 25k.

Participation rate edged down to 70.8% and the employment rate slipped to 67.2%, both suggesting a gradual loss in labor market momentum.

Wage growth also moderated, with the labour cost index rising 2.9% annually, down from 3.3% in the previous quarter.

Full NZ employment release here.