Sample Category Title

Bitcoin Hits Record, Gold Rises Before Powell Testimony

Bitcoin hit a record. The price of a coin advanced past the $69K, then shortly dipped below $60K, and is now settling at around the $65K. Volatility is high as the coin flirts with new record levels. The latter attracts new interest and speculation, of course. Fundamentally, though, the demand is surging thanks to the introduction of new spot ETFs which made cryptocurrencies easier to invest for institutional players. Halving due in April means that the Bitcoin supply will be divided by two. Higher demand and lower supply points at a higher price. We should still figure out where we can use Bitcoin, but the ‘to-the-mooners’ have all the reasons to believe that Bitcoin could hit $100K per coin.

In the more traditional space

Gold rose on safe haven demand walking into the Federal Reserve (Fed) Chair Jerome Powell’s testimony before the Congress. Powell is expected to ask policymakers for patience before cutting interest rates. The US economic growth remains resilient, the jobs market remains hot – remember the last two NFP prints in the US were above the 300K mark, and disinflation has given signs of slowing at the beginning of the year. Due today, the ADP report is expected to print around 150K new private job additions and we might see lower job openings. A sufficiently soft data would make Powell’s job easier into the first rate cut, while a stronger-than-expected set of data will keep the Fed watchers wondering whether the Fed should cut rates anytime at all this year.

Gold is higher on expectation that the lofty equity valuations could finally lead to a sizeable downside correction and gold could serve as a hedge. Even though higher yields – that would result from a hawkish shift in Fed expectations – are not favourable for the valuation of gold, the size and the amplitude of a potential market selloff could help investors look past the higher opportunity cost of holding the non-interest-bearing gold and push the price of an ounce further up.

But keep in mind that the major US equity indices do not necessarily react to yield changes since AI disrupted the negative relationship between equity valuations and the US yields.

Sour Apple

Apple is not having a good time. The stock price fell another 2.84% yesterday on news that its iPhone sales in China fell 24% over the first six weeks of the year. iPhone’s market share in China fell below 16% from 19% a year earlier. Huawei amassed some good demand and increased its own marker share from below 10% to above 16% over the same period. And it’s not only China. The company is coming too late to the AI race, which makes it vulnerable to any broad market selloff unless it comes up with a project that would excite investors. It was removed from Goldman’s high conviction list and it’s no longer in Evercore ISI’s tactical outperform list. The stock price is in a free-fall mode. Earlier this week, the $180 support was broken, and yesterday the stock fell and closed below a key technical level: the major 38.2% retracement on the bullish trend forming since the beginning of 2023. Technically, the stock has now stepped into the medium-term bearish consolidation zone and could extend losses to $162 per share, the 50% Fibonacci level.

Elsewhere

The Bank of Canada (BoC) is expected to keep its policy rate steady today and the UK Chancellor of the Exchequer will reveal the budget. He is expected to aim for tax cuts to please British voters, but he has a limited margin and some tax cuts could lead to inflationary pressures prompting the Bank of England (BoE) to maintain a tighter monetary policy for an extended period, which may further burden mortgage payers. Hunt should find a fine balance.

The 10-year gilt yield fell to 4% and Cable is testing the top of this year’s downtrending range. It’s up to Jeremy Hunt to keep the market at this sweet spot.

Trump Big Winner on Super Tuesday

In focus today

In the U.K. Chancellor of the Exchequer Jeremy Hunt will deliver his spring budget. With the general election looming the chancellor is expected to present a range of expansionary measures, namely tax cuts.

In the US we get both JOLTs for January as well as ADP employment numbers for February. FOMC chairman Powell will also be giving testimony in the House of Representatives.

In Poland and Canada, the respective central banks both announce rate decisions today. We expect both central banks to keep rates unchanged at 5.75% in Poland, and 5.00% in Canada respectively.

In the euro area we await retail sales for January due at 11.00 CET.

Economic and market news

What happened overnight

Former president Donald Trump expectedly came out a major winner of the so-called Super Tuesday. Trump had by 6.45 CET secured 662 delegates out of the 1215 republican that were up for grabs between the 15 different states that voted in the republican primaries yesterday. His opponent Nikki Haley had Tuesday secured 36 at that point in time.

What happened yesterday

In the US, the ISM non-manufacturing PMI disappointed slightly at 52.6 whereas a consensus of economists polled by Reuters had expected 53.0.

In Europe, the European Commission presented a draft for a European Defence Industry Strategy. Besides focusing on building the EU defence sector and ensuring that the EU buys defence equipment from European producers, the draft proposed mobilising EUR 1.5bn from 2025-2027 funded by the EU budget.

Released country data indicates euro area wage growth as measured by compensation per employee is likely to have slowed to 4.65% in Q4 2023 down from 5.3% in Q3. As the ECB likely knows the euro area aggregate figure when meeting Thursday, they may sound less hawkish on the upside risk to inflation from wage growth. However, as wage growth is high despite the decline, the ECB may prefer seeing Q1 2024 data before cutting rates as the wage-sensitive services inflation is hot. Q1 data is available for the ECB's June meeting.

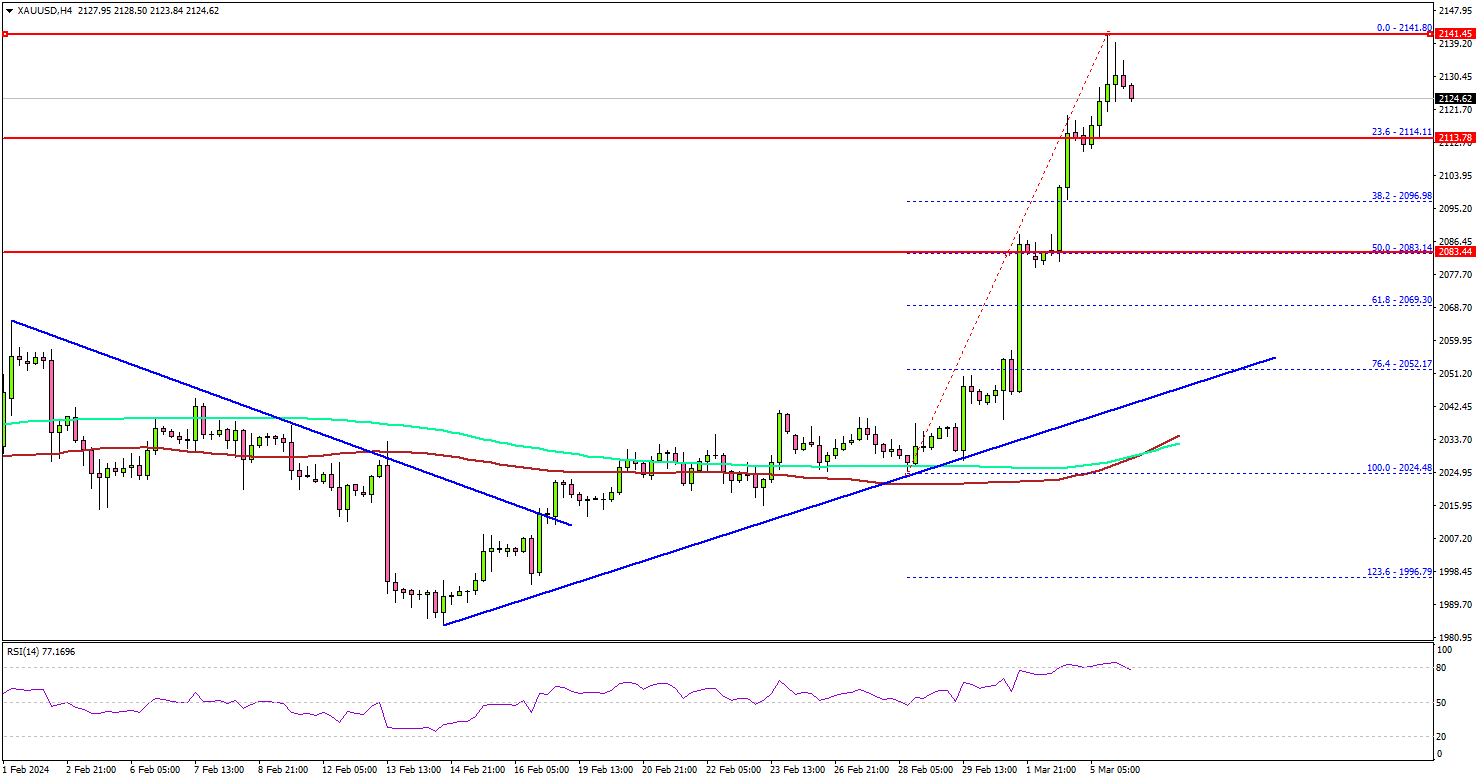

Amongst precious metals, spot gold surged to an intraday record as it rose to as high as USD 2141.59 per troy ounce beating its previous record from 4 December of USD 2135.40 per troy ounce.

Equities: Global equities were lower yesterday with most sectors and regions lower. However, US tech was in focus, ending down more than 2% despite a late hour rally. Also, consumer discretionary was lower as Tesla was taking a 2-day beating of more than 10%. Add to this that Bitcoin was down almost 10%, and we have a picture of stocks that have been rallying sharply since October now getting beat down. Hence, this was not a macro story but much a reflection of the heavy positioning tilt towards the AI, tech and growth space. In US yesterday, Dow -1.0%, S&P 500 -1.0%, Nasdaq -1.7% and Russell 2000 -1.0%. Asian markets are mostly lower this morning while China going against the trend. Futures in Europe and US are higher this morning.

FI: Risk-off sentiment in US equity markets and weak ISM details supported global bonds yesterday, with the 10Y tenor seeing substantial declines across markets. The German government yield curve was down by 5-6bp throughout yesterday's session, while peripherals continued to outperform with 10Y BTP yields declining 10bp. The Bund ASW-spread was close to unchanged at 34bp, still standing at the lowest level since mid-2021, while the 5Y5Y EUR Inflation swap rate dropped a bit following ISM. The weakening of US data seen over the past week has led to a convergence between the expected amount cuts in 2024 from the ECB (now 90bp) and the FOMC (85bp). We pencil in 75bp for both.

FX: After a short-lived spike toward 1.0875, EUR/USD is back at around 1.0850. JPY is a bit stronger with USD/JPY dipping below the 150 mark and with EUR/JPY back below 163. EUR/GBP is lower, yet in the tight range around 0.8550. USD/CAD is challenging, still without taking out the 1.36 level. The Antipodeans are flirting with the lower end of their recent trading ranges vs the USD. EUR/DKK spot continues to trade around the 7.4540-50 level, while both SEK and NOK has had a weak start to the week.

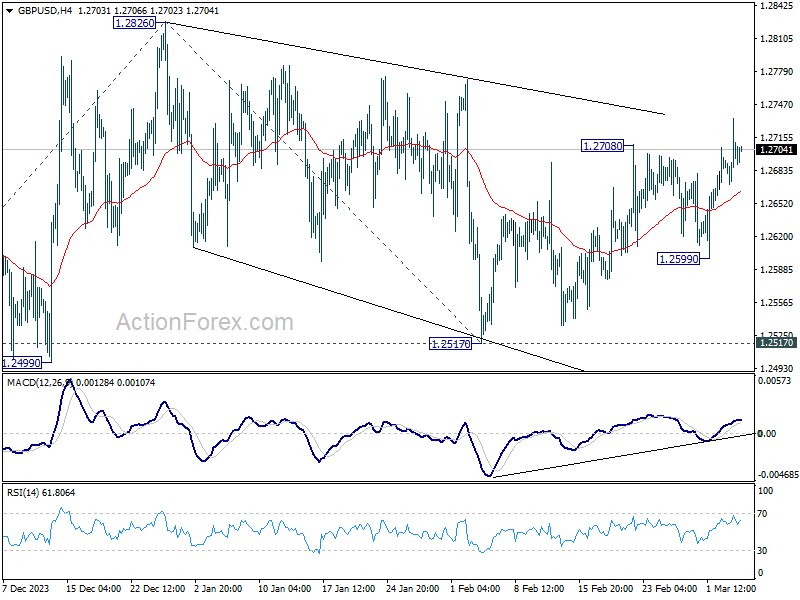

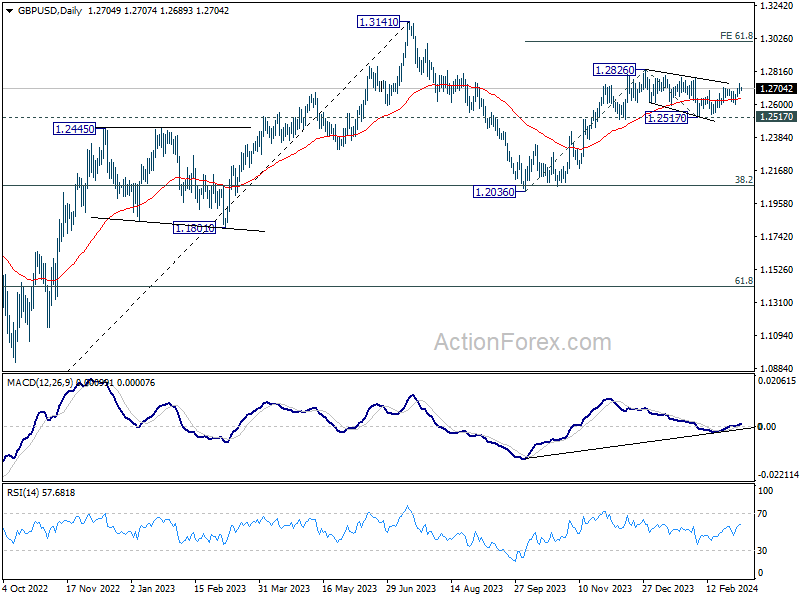

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2672; (P) 1.2704; (R1) 1.2736; More...

Gold's rise from 1.2517 resumed by breaking through 1.2708 and intraday bias is back on the upside. Further rally would be seen to 1.2826 resistance first. Firm break there will target 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005 next. For now, further rise will remain in favor as long as 1.2599 support holds, in case of retreat.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Record-Breaking Gold Amid Falling US Yields, Eyes Set on Fed Powell and BoC

Dollar faced some selling pressure overnight, as dragged down by the sharp decline in the 10-year treasury yield. Despite this, the impact on the greenback was relatively contained, thanks to significant pullbacks in major stock indices, which provided a cushion against more substantial losses. Today's spotlight turns to Fed Chair Jerome Powell's semiannual testimony, an event that, despite low expectations for groundbreaking revelations, is highly anticipated for its impact on financial market, particularly in stocks and bonds.

Simultaneously, Canadian Dollar finds itself among the week's laggards, in tandem with other commodity currencies. The spotlight is now on BoC as it gears up for its latest rate decision. While analysts broadly anticipate the central bank will maintain rates, the focal point will be the tone of BoC's statement and Governor Tiff Macklem's press conference, specifically whether a dovish stance will be adopted. Or, BoC would adopt a cautious "wait and see" approach, contingent on forthcoming data, will prevail to set the stage for future rate cuts.

Sterling leads as the week's top performer, with Euro and Yen trailing behind. Swiss Franc and Dollar are mixed, while New Zealand Dollar, Australian Dollar, and Canadian Dollar lag at the bottom of the performance chart.

Technically, Gold surged to new record high at 2141.53 overnight and stays firm. Current interpretation is that rise from 1984.50 is resuming the rise rise from 18102.6 (which is a five-wave impulsive rise with a failure fifth ended at 2088.24). Further rally is expected as long as 2088.24 resistance turned support holds. Next target is 61.8% projection of 1810.26 to 2088.24 from 1984.05 at 2155.84.

But the ultimate target for this round would be cluster level at around 2260, 100% projection of 1810.26 to 2088.24 from 1984.05 at 2262.03 and 100% projection of 1614.60 to 2062.95 from 1810.26 at 2259.15

In Asia, Nikkei fell -0.02%. Hong Kong HSI is up 1.80%. China Shanghai SSE is down -0.05%. Singapore Strait Times is up 1.17%. Japan 10-year JGB yield rose 0.0080 to 0.716. Overnight, DOW fell -1.04%. S&P 500 fell -1.02% NASDAQ fell -1.65%. 10-year yield fell -0.082 to 4.137.

RBNZ's Conway: OCR to stay restrictive for some time into the future

RBNZ Chief Economist Paul Conway, speaking at a webinar today, noted that emphasizing the contractionary nature of current interest rates is effectively "tapping the brakes" on the economy to moderate its pace of growth and address inflationary pressures.

Conway expressed optimism about the recent declines in core inflation and business inflation expectations. However, he also highlighted ongoing concerns regarding elevated household inflation expectations, which pose a potential risk to the inflation outlook.

Looking forward, Conway underscored the necessity for OCR to maintain a restrictive level "for some time into the future" to get headline inflation, currently at 4.7%, back into the 1-3% target band.

An interesting consideration Conway raised was the impact of Fed's policy moves on New Zealand's monetary policy trajectory. He suggested that if Fed were to initiate rate cuts towards the end of the year, and RBNZ did not follow suit, the resulting appreciation in NZD could alleviate inflationary pressures in New Zealand. This scenario might prompt RBNZ to reassess its rate cut timeline, leading to earlier-than-anticipated adjustments depending on the broader economic implications.

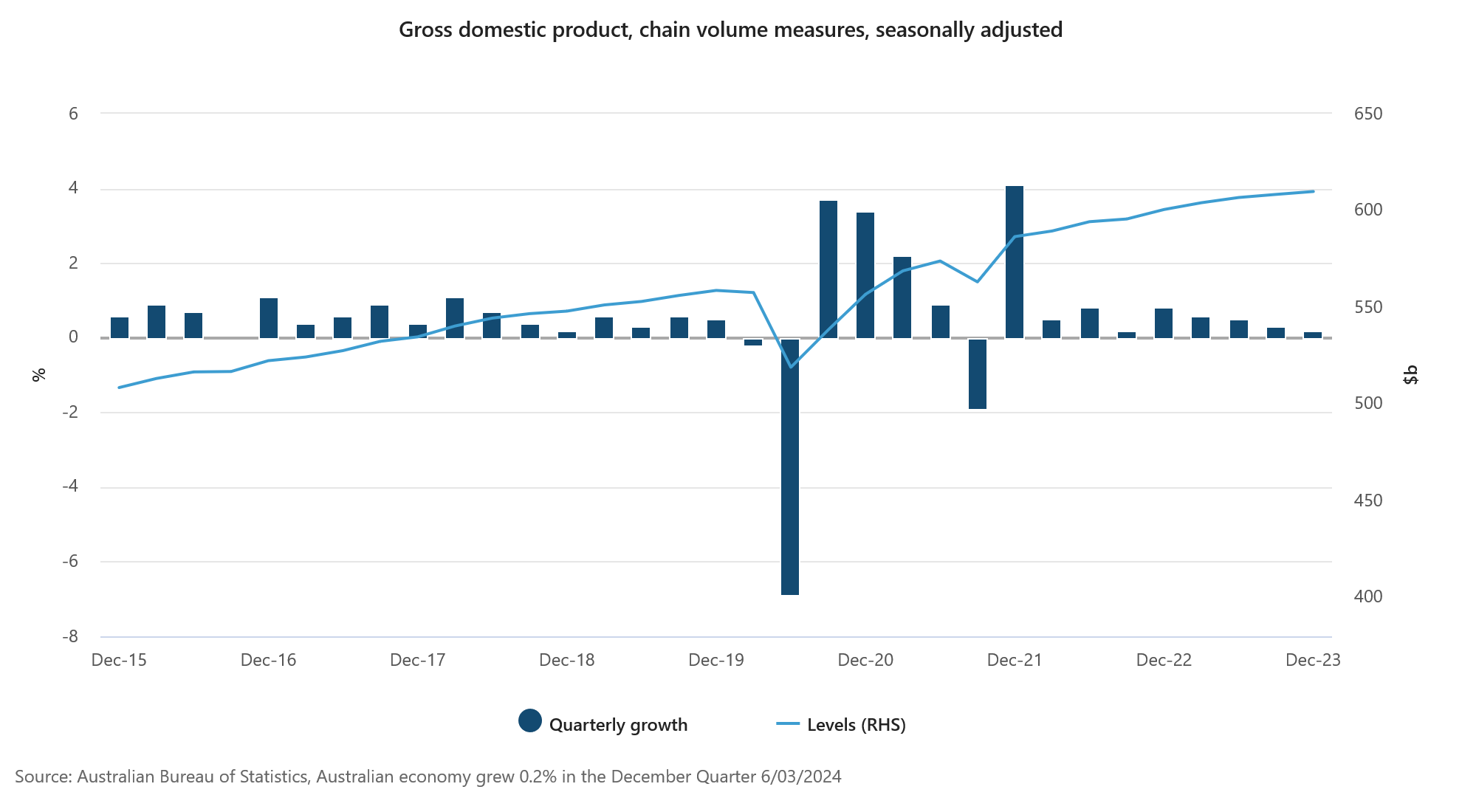

Australia's GDP up 0.2% qoq in Q4, continuing consistent slowdown

Australia GDP grew 0.2% qoq in Q4, slightly below expectation of 0.3% qoq. On an annual basis, the economy expanded by 1.5% yoy.

The data indicates deceleration in economic momentum as the year progressed, with Katherine Keenan, the head of national accounts at ABS, noting a consistent slowdown across each quarter of 2023.

The main pillars supporting GDP growth were identified as government spending and private business investment. Government final consumption expenditure saw 0.6% qoq increase , while private business investment grew 0.7% qoq.

The significant contribution of net trade, which added 0.6 percentage points to the overall GDP growth, was largely attributed to a -3.4% qoq decrease in import.

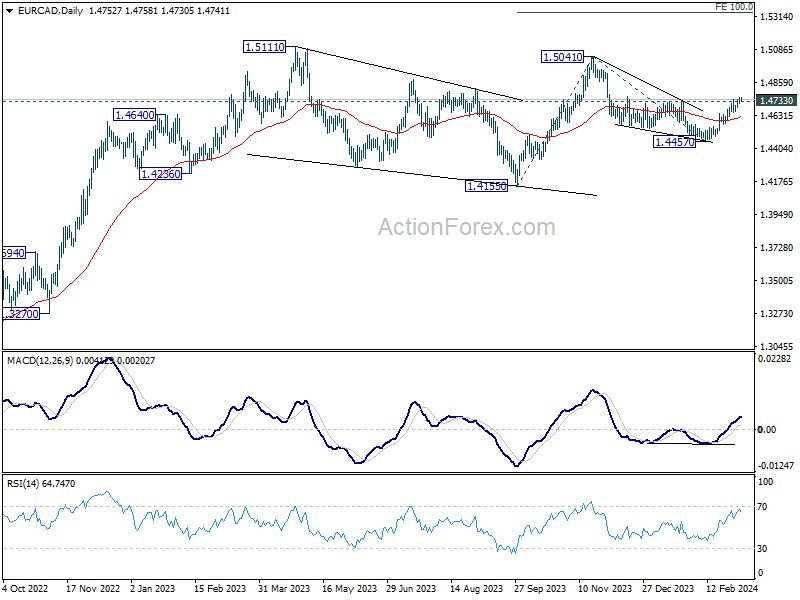

BoC to hold rates steady, EUR/CAD and GBP/CAD extending gains

BoC is widely anticipated to maintain benchmark overnight rate at 5.00% today, marking the fifth consecutive meeting without change. While dropping its tightening bias in January, it is deemed premature for BoC to adopt a loosening stance at this point. The central bank might reiterate the ongoing process to bring inflation back to target, indicating that the desired state has not been fully achieved yet. The critical aspect to observe will be how Governor Tiff Macklem articulates the current inflation outlook.

A recent Bloomberg survey highlighted consensus among economists predicting the first rate cut to occur in June. Overnight swaps markets attributing a mere 30% chance for a cut in April and anticipating the initial full 25 basis points reduction in July. Nonetheless, these projections remain flexible, hinging on forthcoming data and economic developments.

Canadian Dollar is trading as the month's weakest performer so far, particularly struggling against Euro and Sterling. More downside is in favor for the Loonie in the near term as traders continue to reverse their bets on earlier ECB and BoE cut. The persistence of this selling momentum, however, ultimately depends on which central bank initiates rate cuts first and the subsequent rate of policy easing.

Technically, EUR/CAD's breach of 1.4733 resistance suggests that correction from 1.5041 has already completed with three waves down to 1.4457. Further rally is now in favor as long as 55 D EMA (now at 1.4625) holds. Further rally would be seen to retest 1.5041 resistance first. Firm break there will resume the larger up trend to 61.8% projection of 1.4155 to 1.5041 from 1.4457 at 1.5343 next.

GBP/CAD's breach of 1.7270 resistance this week suggests that consolidation from there has completed at 1.6919 already. Further rise is in favor as long as 55 D EMA (now at 1.7060) holds. Decisive break of 1.7332 high will resume the larger up trend from 1.4069 and target 100% projection of 1.6355 to 1.7270 from 1.6919 at 1.7834.

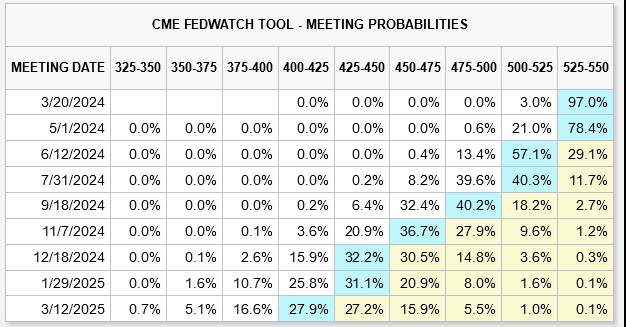

Fed Powell's testimony eyed, 10-year yield takes a preemptive drop

Fed Chairman Jerome Powell is set to begin his two-day semiannual Congressional testimony today, drawing significant attention from the markets as participants seek clarity on the Fed's monetary policy direction for the year. Key questions include the timing of the first rate cut and the total number expected throughout the year.

Powell is anticipated to reiterate the cautious stance echoed by his colleagues, indicating that Fed is not in a hurry to lower interest rates. The central bank seeks further assurance that inflation is on a consistent downward path to target before considering rate reductions. Regarding the number of rate cuts, Powell may reference the median projection of three cuts this year, emphasizing that any adjustments will be contingent on incoming economic data.

Currently fed fund futures suggest a slightly less than 70% probability of the initial rate cut occurring in June. By year-end, the likelihood exceeds 80% that federal funds rate will adjust to a range of 4.50-4.75%, marking three 25bps reductions from the present 5.25-5.50% level.

A key to watch is the reactions in 10-year yields the break of 55 D EMA (now at 4.188) affirms the case that corrective recovery from 3.785 has completed at 4.354 already. Risk will now stay on the downside as long as this EMA holds. Deeper fall is in favor towards 3.785 low. This development would keep Dollar under some pressure, or at least cap its rally momentum. A daily close above 55 EMA would delay the bearish case. But upside potential for rebound should be limited below 4.354.

On the data front

Germany trade balance, UK PMI construction and Eurozone retail sales will be released in European session. Canada will release labor productivity and Ivey PMI later in the day. Fed will also publish Beige Book economic report.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2672; (P) 1.2704; (R1) 1.2736; More...

Gold's rise from 1.2517 resumed by breaking through 1.2708 and intraday bias is back on the upside. Further rally would be seen to 1.2826 resistance first. Firm break there will target 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005 next. For now, further rise will remain in favor as long as 1.2599 support holds, in case of retreat.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q4 | 0.20% | 0.30% | 0.20% | 0.30% |

| 07:00 | EUR | Germany Trade Balance (EUR) Jan | 21.0B | 22.2B | ||

| 09:30 | GBP | Construction PMI Feb | 49.2 | 48.8 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Jan | 0.10% | -1.10% | ||

| 13:15 | USD | ADP Employment Change Feb | 150K | 107K | ||

| 13:30 | CAD | Labor Productivity Q/Q Q4 | -0.10% | -0.80% | ||

| 14:45 | CAD | BoC Interest Rate Decision | 5.00% | 5.00% | ||

| 15:00 | USD | Fed's Chair Powell testifies | ||||

| 15:00 | USD | Wholesale Inventories Jan F | -0.10% | -0.10% | ||

| 15:00 | CAD | Ivey PMI Feb | 54.4 | |||

| 15:30 | USD | Crude Oil Inventories | 2.4M | 4.2M | ||

| 19:00 | USD | Fed's Beige Book |

Fed Powell’s testimony eyed, 10-year yield takes a preemptive drop

Fed Chairman Jerome Powell is set to begin his two-day semiannual Congressional testimony today, drawing significant attention from the markets as participants seek clarity on the Fed's monetary policy direction for the year. Key questions include the timing of the first rate cut and the total number expected throughout the year.

Powell is anticipated to reiterate the cautious stance echoed by his colleagues, indicating that Fed is not in a hurry to lower interest rates. The central bank seeks further assurance that inflation is on a consistent downward path to target before considering rate reductions. Regarding the number of rate cuts, Powell may reference the median projection of three cuts this year, emphasizing that any adjustments will be contingent on incoming economic data.

Currently fed fund futures suggest a slightly less than 70% probability of the initial rate cut occurring in June. By year-end, the likelihood exceeds 80% that federal funds rate will adjust to a range of 4.50-4.75%, marking three 25bps reductions from the present 5.25-5.50% level.

A key to watch is the reactions in 10-year yields the break of 55 D EMA (now at 4.188) affirms the case that corrective recovery from 3.785 has completed at 4.354 already. Risk will now stay on the downside as long as this EMA holds. Deeper fall is in favor towards 3.785 low. This development would keep Dollar under some pressure, or at least cap its rally momentum. A daily close above 55 EMA would delay the bearish case. But upside potential for rebound should be limited below 4.354.

DAX Bullish Impulse Looks Incomplete

Short Term Elliott Wave View in DAX suggests that rally from 1.17.2024 low is in progress as a 5 waves impulse. Up from 1.17.2024 low, wave ((i)) ended at 17049.52 and dips in wave ((ii)) ended at 16834.94. Up from there, wave ((iii)) is in progress as a 5 waves impulse. Wave (i) ended at 17198.45 and pullback in wave (ii) ended at 17019.15. The Index extends higher again in wave (iii). Up from wave (ii), wave i ended at 17084.87 and wave ii dips ended at 17029.59. Wave iii higher ended at 17429.66 and wave iv ended at 17354.76. Final leg wave v ended at 17816.52 which completed wave (iii).

Pullback in wave (iv) ended at 17643.11 with internal subdivision as a double three. Down from wave (iii), wave w ended at 17690.89 and wave x ended at 17759.02. Final leg wave y ended at 17643.11 which completed wave (iv) in higher degree. The Index then resumes higher in wave (v). Up from wave (iv), wave i ended at 17746.57 and wave ii ended at 17677.03. Near term, as far as pivot at 16834.94 stays intact, expect Index to extend higher.

DAX 60 Minutes Elliott Wave Chart

DAX Elliott Wave Video

https://www.youtube.com/watch?v=2HPF2xx3Qto

BoC to hold rates steady, EUR/CAD and GBP/CAD extending gains

BoC is widely anticipated to maintain benchmark overnight rate at 5.00% today, marking the fifth consecutive meeting without change. While dropping its tightening bias in January, it is deemed premature for BoC to adopt a loosening stance at this point. The central bank might reiterate the ongoing process to bring inflation back to target, indicating that the desired state has not been fully achieved yet. The critical aspect to observe will be how Governor Tiff Macklem articulates the current inflation outlook.

A recent Bloomberg survey highlighted consensus among economists predicting the first rate cut to occur in June. Overnight swaps markets attributing a mere 30% chance for a cut in April and anticipating the initial full 25 basis points reduction in July. Nonetheless, these projections remain flexible, hinging on forthcoming data and economic developments.

Canadian Dollar is trading as the month's weakest performer so far, particularly struggling against Euro and Sterling. More downside is in favor for the Loonie in the near term as traders continue to reverse their bets on earlier ECB and BoE cut. The persistence of this selling momentum, however, ultimately depends on which central bank initiates rate cuts first and the subsequent rate of policy easing.

Technically, EUR/CAD's breach of 1.4733 resistance suggests that correction from 1.5041 has already completed with three waves down to 1.4457. Further rally is now in favor as long as 55 D EMA (now at 1.4625) holds. Further rally would be seen to retest 1.5041 resistance first. Firm break there will resume the larger up trend to 61.8% projection of 1.4155 to 1.5041 from 1.4457 at 1.5343 next.

GBP/CAD's breach of 1.7270 resistance this week suggests that consolidation from there has completed at 1.6919 already. Further rise is in favor as long as 55 D EMA (now at 1.7060) holds. Decisive break of 1.7332 high will resume the larger up trend from 1.4069 and target 100% projection of 1.6355 to 1.7270 from 1.6919 at 1.7834.

Australia’s GDP up 0.2% qoq in Q4, continuing consistent slowdown

Australia GDP grew 0.2% qoq in Q4, slightly below expectation of 0.3% qoq. On an annual basis, the economy expanded by 1.5% yoy.

The data indicates deceleration in economic momentum as the year progressed, with Katherine Keenan, the head of national accounts at ABS, noting a consistent slowdown across each quarter of 2023.

The main pillars supporting GDP growth were identified as government spending and private business investment. Government final consumption expenditure saw 0.6% qoq increase , while private business investment grew 0.7% qoq.

The significant contribution of net trade, which added 0.6 percentage points to the overall GDP growth, was largely attributed to a -3.4% qoq decrease in import.

Gold Price Surges Above $2,100, Bitcoin Sets New ATH

Key Highlights

- Gold rallied above the $2,080 and $2,100 resistance levels.

- A connecting bullish trend line is forming with support at $2,045 on the 4-hour chart.

- Bitcoin extended gains above the $68,800 resistance.

- Ethereum bulls seem to be aiming for a move toward $4,000.

Gold Price Technical Analysis

Gold prices started a fresh increase from the $2,020 support against the US Dollar. The bulls cleared the $2,065 resistance to start a strong rally.

The 4-hour chart of XAU/USD indicates that the price settled above the $2,080 level, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours).

The bulls were able to pump the price above the $2,100 and $2,120 levels. If they remain in action, there could be a move toward the $2,150 level. Any more gains might open the doors for a test of $2,180.

Initial support is near the $2,110 level. The first major support sits at $2,080. Any more losses might call for a move toward the $2,050 level in the coming days.

There is also a connecting bullish trend line forming with support at $2,045 on the same chart, below which Gold might decline and test the 100 Simple Moving Average (red, 4 hours) at $2,030.

Looking at Bitcoin, there was a strong upward move above the $66,000 and $68,000 levels. The next key resistance sits at $70,000.

Economic Releases to Watch Today

- Euro Zone Retail Sales for Jan 2024 (YoY) - Forecast -1.3%, versus -0.8% previous.

- BoC Interest Rate Decision – Forecast 5.0%, versus 5.0% previous.

RBNZ’s Conway: OCR to stay restrictive for some time into the future

RBNZ Chief Economist Paul Conway, speaking at a webinar today, noted that emphasizing the contractionary nature of current interest rates is effectively "tapping the brakes" on the economy to moderate its pace of growth and address inflationary pressures.

Conway expressed optimism about the recent declines in core inflation and business inflation expectations. However, he also highlighted ongoing concerns regarding elevated household inflation expectations, which pose a potential risk to the inflation outlook.

Looking forward, Conway underscored the necessity for OCR to maintain a restrictive level "for some time into the future" to get headline inflation, currently at 4.7%, back into the 1-3% target band.

An interesting consideration Conway raised was the impact of Fed's policy moves on New Zealand's monetary policy trajectory. He suggested that if Fed were to initiate rate cuts towards the end of the year, and RBNZ did not follow suit, the resulting appreciation in NZD could alleviate inflationary pressures in New Zealand. This scenario might prompt RBNZ to reassess its rate cut timeline, leading to earlier-than-anticipated adjustments depending on the broader economic implications.