Sample Category Title

China Caixin PMI manufacturing rises to 50.4, but optimism fades

China’s Caixin PMI Manufacturing rose to 50.4 in June from 48.3, topping expectations of 49.0 and marking a return to expansion territory. However, Wang Zhe of Caixin Insight cautioned that job losses persisted, external demand remained weak, and price pressures were subdued.

While the latest figures point to near-term stabilization, underlying risks remain elevated. Wang stressed that domestic demand has yet to see a fundamental turnaround and that businesses have grown less optimistic. With logistics and purchasing activity still soft, and global uncertainty intensifying, the sustainability of June’s rebound remains in question unless further policy support or demand recovery materializes.

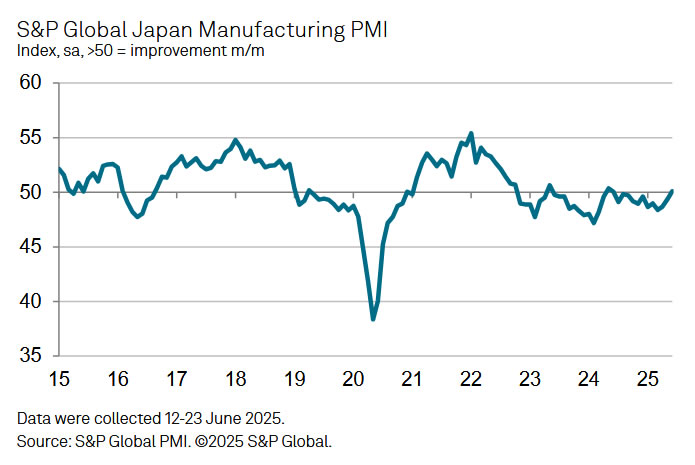

Japan’s PMI manufacturing finalized at 50.1, demand still fragile

Japan’s Manufacturing PMI was finalized at 50.1 in June, rising from 49.4 in May. While production and employment ticked higher, underlying demand remained weak.

According to S&P Global’s Annabel Fiddes, firms reported continued declines in both domestic and overseas sales, reflecting the lingering impact of global uncertainty—particularly around US tariff policy.

Despite soft demand, business sentiment improved, encouraging firms to boost output and hiring. However, Fiddes emphasized that a "renewed and sustained improvement in customer demand" is still needed to drive a broader recovery.

Price pressures also "picked up slightly", with both input costs and selling prices rising above their long-term averages, suggesting inflationary risks remain embedded in supply chains.

BoJ Tankan signals resilience, keeps 2025 hike option alive

Japan’s Q2 Tankan survey showed business sentiment holding firm despite intensifying trade tensions. While today’s Tankan beat won’t trigger immediate action, it keeps the door open for a BoJ hike policy shift before year-end, especially if trade risks stabilize.

Large manufacturers posted a headline index of +13, beating expectations of 10, and reaching the highest level since December 2024. Their forward outlook for September came in at +12, also topping forecasts of 9. The services side was more mixed. Large non-manufacturers remained steady at +34, meeting expectations, but this marked a softening from prior readings, with the September outlook dipping to +27.

Still, capital expenditure plans surprised to the upside: large firms projected FY2025/26 capex to rise 11.5% (vs. 10.0% expected), while small firms were slightly less pessimistic than forecast. The investment data points to continued confidence in the domestic recovery.

Inflation expectations remained broadly stable. Firms anticipate CPI to rise 2.4% over both one-year and three-year horizons—unchanged to slightly lower from the previous survey.

Full BoJ Tankan survey release here.

NZIER survey shows NZ business confidence rising, inflation pressures easing

New Zealand business confidence improved modestly in Q2, with a net 22% of firms expecting better conditions ahead, up from 19% in Q1, according to NZIER’s quarterly survey.

Inflationary pressure appears to be cooling. 1% of firms reported price cuts in Q2, a sharp turnaround from the 8% that raised prices in Q1.

The report pointed to a continued "divergence between firms experiencing weak demand and firms expecting a recovery in demand", underlining an uneven domestic outlook despite improved sentiment.

NZIER said the effect of interest rate cuts since last August has yet to fully feed through to real activity, despite supporting sentiment.

Fed’s Goolsbee dismisses stagflation risk, but warns on dual deterioration

Chicago Fed President Austan Goolsbee downplayed the risk of a 1970s-style stagflation scenario. He noted that with unemployment near 4% and inflation around 2.5% and falling, the current environment bears little resemblance to the high-inflation, high-unemployment era.

Speaking overnight, Goolsbee emphasized that today’s economic fundamentals are far stronger, with inflation far below double digits and labor markets still tight.

However, he cautioned that simultaneous deterioration in both inflation and employment remains possible. “There's definitely the possibility of both things getting worse at the same time,” he said. Goolsbee framed the outlook in terms of evaluating how large and lasting each side’s deviation might be—whether shocks are temporary or structural.

Final Countdown: Trade Peace or Market Panic on July 9?

Global markets are counting down to the July 8 and 9 deadlines set by the Trump administration. By these dates, countries must finalize trade deals with the U.S. — or face a sharp rise in tariffs. What happens could either bring relief to investors or reignite fears of a global trade war.

The trigger came on April 2, when President Trump announced sweeping new tariffs under his "America First" trade plan: a 10% base tariff on most imports, with the threat of much higher country-specific rates of up to 50%. At the same time, the administration paused enforcement for 90 days, giving countries until early July to negotiate individual exemptions.

Markets reacted swiftly:

- Stock prices tumbled as fears of a trade war grew

- Gold surged as investors sought safety

- The U.S. dollar weakened, reflecting doubts about long-term economic strength

- Volatility spiked, and investor confidence took a hit

Now, with the grace period ending on July 8 for most countries and July 9 for the European Union and others, global markets are once again on edge. Will new trade deals be reached? Or will tariffs snap back and disrupt global supply chains?

Let’s break down what’s happening, what to watch, and what the possible outcomes could mean for the markets.

Who Has Made a Deal (and Who’s Nearly There)?

Only a few countries have officially secured agreements so far:

- United Kingdom: Signed a partial trade deal covering cars, metals, beef, and ethanol. It’s not complete yet, but it’s the most advanced.

- China: Reached an agreement to ease tensions. China promised to speed up rare earth exports, and the U.S. scaled back some restrictions. But this is more of a truce than a full peace deal.

- Taiwan & Indonesia: Nearing deals.

- Vietnam & South Korea: Optimism is growing, but nothing signed yet.

Who Is Still at Risk?

Several key players are still negotiating and face the threat of higher tariffs if talks break down:

- European Union: Talks are tense. Some countries want a quick deal, others (like France) are pushing back. Car and steel tariffs are big sticking points.

- India: Progress has been made on energy and some agriculture, but India resists U.S. pressure on genetically modified crops and dairy.

- Japan: Wants a broad agreement but hasn’t agreed to U.S. demands on car tariffs.

- Canada: Talks have collapsed over a digital tax. Tariffs are expected if nothing changes.

- Others: Dozens of smaller nations — including Thailand, Mexico, and Algeria — are still in talks, and many face automatic tariff increases on July 9 if no deal is done.

President Trump has warned that countries without deals will be "sorted into proper buckets," but also said the U.S. "can do whatever we want" — leaving the door open for last-minute changes or extensions.

What the Market Is Expecting

Interestingly, despite all this tension, the stock market has not panicked. In fact, U.S. stocks have fully recovered all their losses from earlier this year and moved sharply higher in the past week. This tells us something important: Markets are expecting that most countries will eventually reach some kind of deal, or at least avoid the worst-case outcome of a full trade war. Here’s why:

- The China deal is done, and that was the biggest risk. With U.S.–China trade tension eased, the worst fears are off the table.

- Trump favors a strong stock market, especially ahead of the election. He’s made progress in improving the U.S. trade position already, and most signs suggest he doesn’t want to trigger a market crash now.

- A large sell-off seems unlikely, even though it’s still possible — Trump remains unpredictable, and markets know it.

- The market focus has started to shift toward U.S. interest rate cuts later this year. With inflation easing and the Fed signaling flexibility, traders are now watching rates more than tariffs.

- Volatility has been quiet for the past week, but that could change quickly as the deadline approaches and Trump begins pressuring countries to finalize deals.

The most likely outcome, based on current price action, is a continued relief rally, even if not every country reaches a full agreement. But traders should still be prepared for surprises.

What Could Happen? (And How Markets May React)

Here are four possible scenarios based on how the deadline plays out:

🟢 Scenario 1: Trade Peace (Deals or Extensions)

Most countries reach partial deals or get more time. The current 10% tariffs stay, but no big new penalties.

Potential Market Reaction:

- Stock markets rally

- Confidence improves

- Gold falls or stabilizes

- Bitcoin and crude oil rise

- USD strengthens

🟡 Scenario 2: Mixed Results (Some Deals, Some Tariffs)

The U.S. signs deals with a few countries but punishes others.

Potential Market Reaction:

- Winners and losers split across countries and industries

- Stocks move more erratically

- Volatility is high as traders try to understand the implications

🔴 Scenario 3: Market Panic (Tariffs on Many Countries)

The U.S. moves forward with high tariffs on multiple nations. No widespread deals.

Potential Market Reaction:

- Global stock sell-off

- Crude oil falls (on fears of weaker demand)

- USD continues to weaken

- Gold and JPY rise as safe havens

- High volatility returns

🔵 Scenario 4: Last-Minute Miracle (Full Breakthrough)

The U.S. unexpectedly reaches broad agreements with major partners.

Potential Market Reaction:

- Strong global rally

- Risk-on sentiment takes over

- Emerging market currencies jump

- Bitcoin rises, gold fall

- USD rises strongly

What to Watch Next

We’re heading into one of the most important trading weeks of 2025, with the July 8–9 tariff deadlines just ahead. Markets are on edge, and the next few days could bring major moves — either a continued rally or a sharp reversal.

Here are the key things to keep an eye on:

- Headlines and tweets from President Trump and U.S. trade officials — last-minute announcements or comments can shift sentiment instantly.

- Which countries finalize deals — and which are left out — will determine sector and regional winners and losers.

- Volatility indicators like the VIX — a spike could signal panic or uncertainty taking hold.

Only the UK and China have firm agreements in place. Most countries are still negotiating. If talks collapse, tariffs will hit and markets may drop. But if deals are made or deadlines are extended, a relief rally could continue. Stay flexible. Stay informed. Stay alert. Whether it’s trade peace or market panic — markets are ready to move.

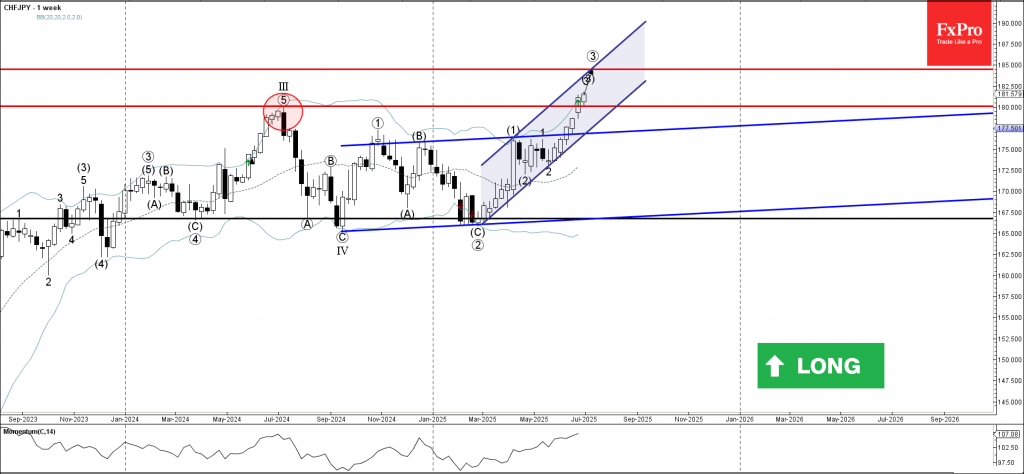

CHFJPY Wave Analysis

CHFJPY: ⬆️ Buy

- CHFJPY broke long-term resistance level 180.00

- Likely to rise to resistance level 185.00

CHFJPY currency pair continues to rise after the pair broke above the long-term resistance level 180.00 (former yearly high from the middle of last year).

The breakout of this resistance level should accelerate the active impulse wave (3) – which is moving inside the well-formed weekly up channel from March.

Given the clear weekly uptrend, CHFJPY currency pair can be expected to rise to the next resistance 185.00 (target price for the completion of the active impulse wave (3)).

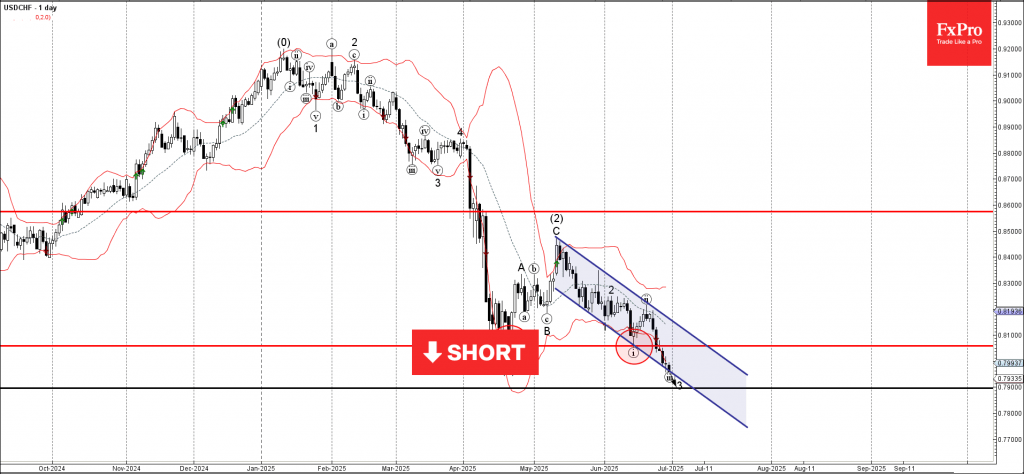

USDCHF Wave Analysis

USDCHF: ⬇️ Sell

- USDCHF falling inside a minor impulse wave

- Likely to fall to support level 0.7900

USDCHF currency pair is falling strongly inside the minor impulse wave 3, which recently broke the daily down channel from the start of May.

The breakout of this down channel follows the earlier breakout of the key support level 0.8055 (which stopped the previous impulse waves (1) and i).

Given the strong daily downtrend and the continuous outflows from US dollar or risk-on mood, USDCHF currency pair can be expected to fall to the next support level 0.7900, the target price for the completion of the active impulse wave 3.

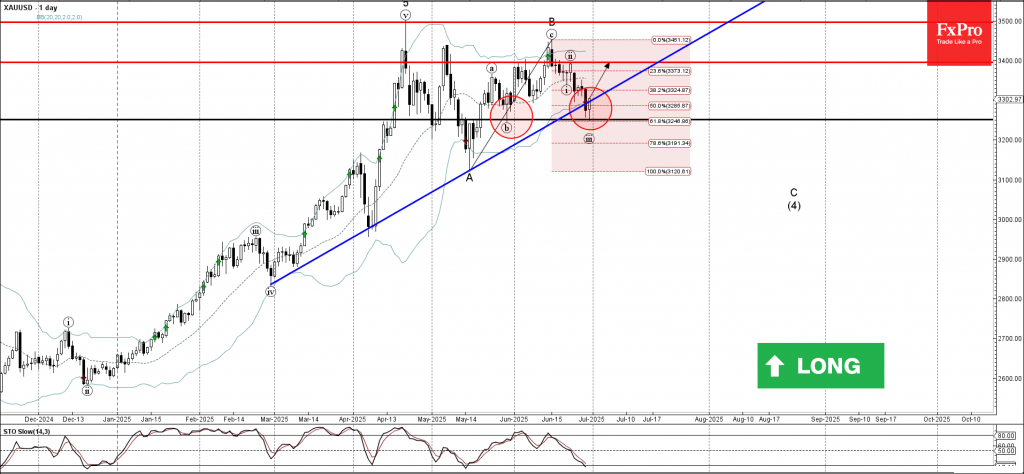

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold reversed from support level 3250.00

- Likely to rise to resistance level 3400.00

Gold recently reversed up from the support level 3250.00 (which stopped wave (b) at the end of May, as can be seen from the daily Gold chart below) intersecting with the lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from May.

The support level 3250.00 was further strengthened by the upward-sloping support trendline from February.

Given the clear daily uptrend, Gold can be expected to rise to the next resistance level 3400.00, which stopped the previous short-term correction ii.

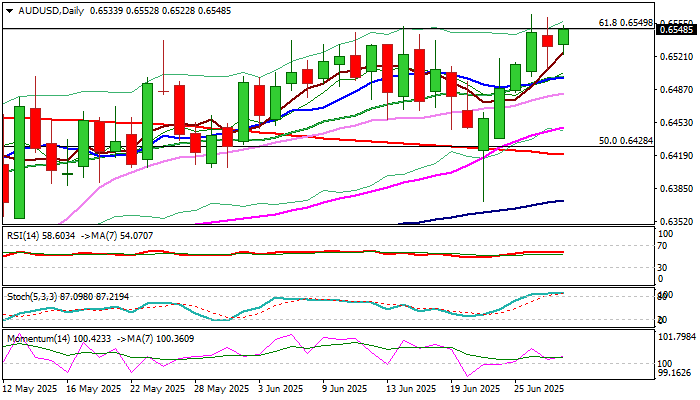

AUDUSD: Larger Bulls Take a Breather Under New 2025 Peak

AUDUSD trades within a narrow consolidation under new 2025 high (0.6563) for the second consecutive day and keeps firm bullish stance for now.

Technical picture remains firmly bullish on daily chart (the action is underpinned by thick ascending daily Ichimoku cloud), with additional positive signal from massive bullish engulfing on weekly chart and the pair being on track for the sixth consecutive monthly gain.

Bulls cracked important Fibo barrier at 0.6549 (61.8% of Sep 2024/Apr 2025, 0.6942/0.5914, downtrend) but were so far unable to register close above this level that would generate fresh bullish signal and expose targets at 0.6700 zone (Fibo 76.4% / 200WMA).

Overbought stochastic on daily chart probably keeps bulls on hold, with more quiet mode seen ahead of release of June report from US labor sector, which is likely to have significant contribution to Fed’s rate decisions in coming months.

Contained by converged 10/20DMA’s (0.6500) offer initial support which should ideally keep the downside protected, though deeper dips cannot be ruled out and should find firm ground above the top of daily cloud (0.6451) to keep bulls intact.

Caution on potential penetration of daily cloud which would expose next trigger at 0.6410 (Fibo 23.6% of 0.5914/0.6563 upleg / daily higher base).

Res: 0.6563; 0.6598; 0.6622; 0.6700

Sup: 0.6500; 0.6451; 0.6410; 0.6372