Sample Category Title

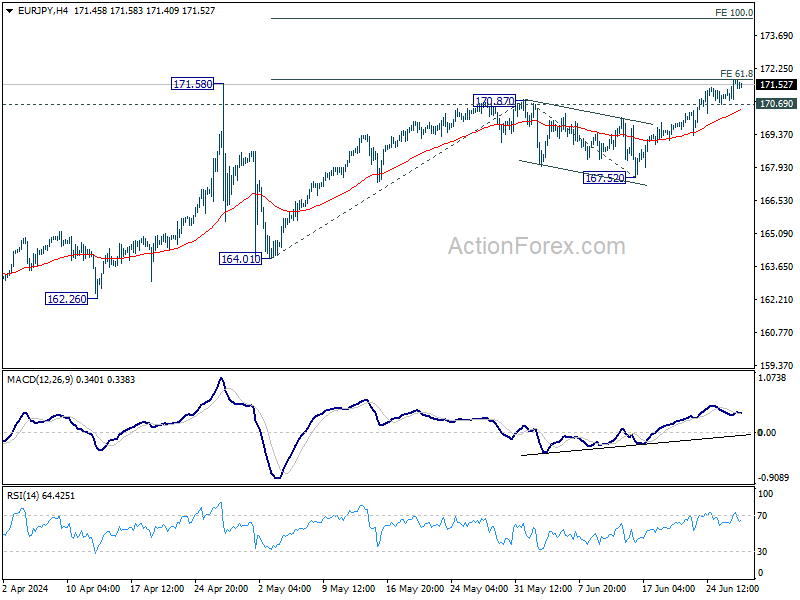

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.11; (P) 171.45; (R1) 172.06; More...

Intraday bias in EUR/JPY is back on the upside as recent rally resumed after brief consolidations. Sustained break of 61.8% projection of 164.01 to 170.87 from 167.52 at 171.75 will target 100% projection at 174.38. On the downside, below 170.69 minor support will turn intraday bias neutral against first.

In the bigger picture, strong support from 55 D EMA indicates that the long term up trend is still in progress. Decisive break of 171.58 will confirm resumption and target 100% projection of 139.05 to 164.29 from 153.15 at 178.38. For now outlook will stay bullish as long as 164.01 support holds, even in case of deep pullback.

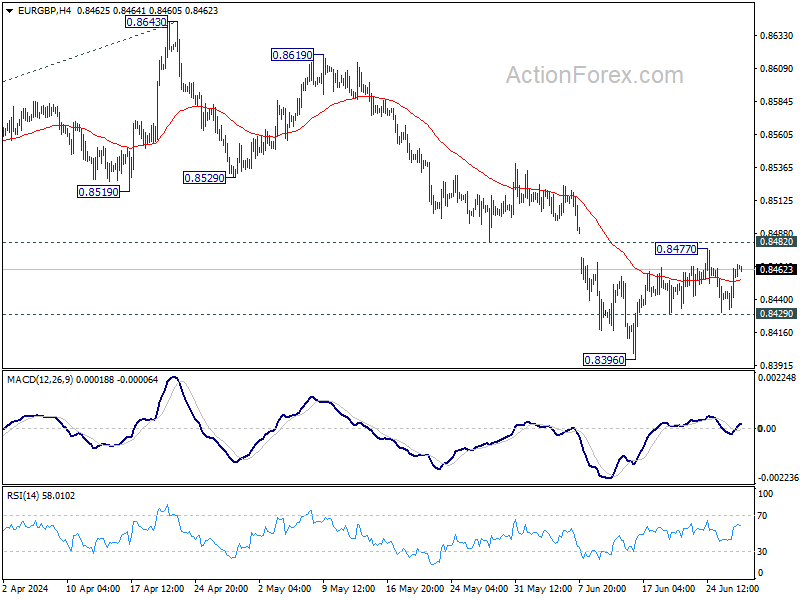

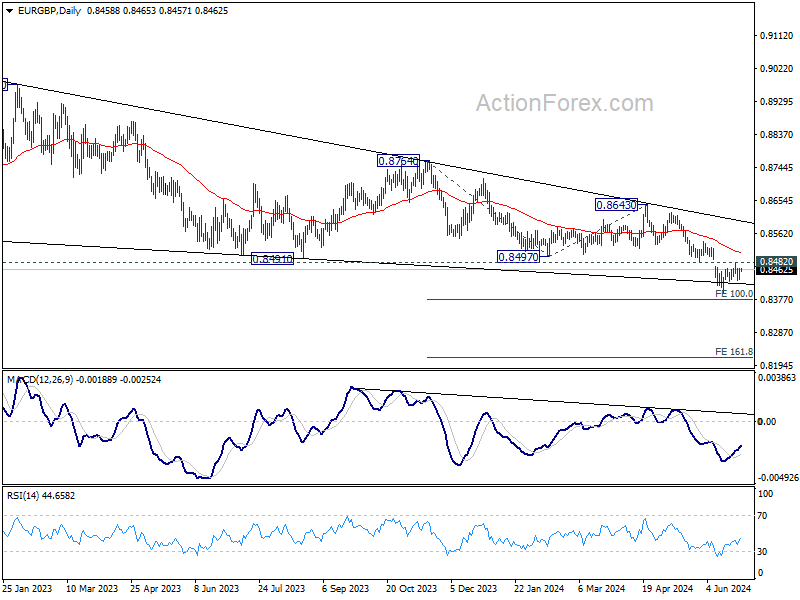

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8442; (P) 0.8453; (R1) 0.8473; More...

Intraday bias in EUR/GBP remains neutral for the moment. Also, outlook stays bearish with 0.8482 support turned resistance intact. On the downside, below 0.8429 minor support will bring retest of 0.8396 low first. Further break there will resume larger down trend to 0.8376 projection level next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

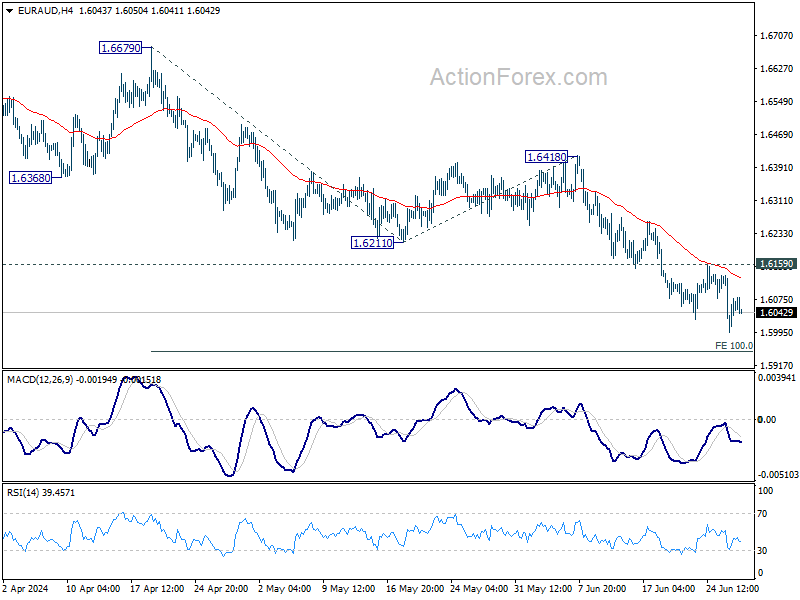

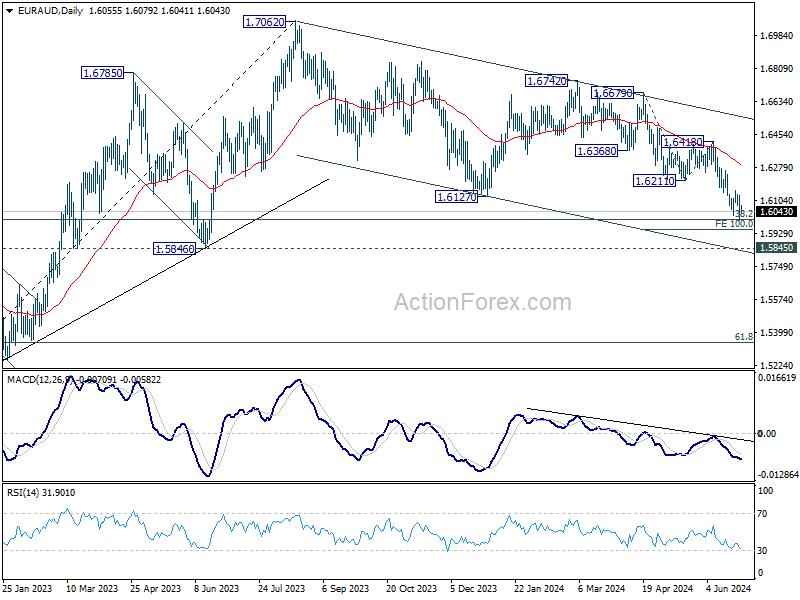

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5995; (P) 1.6068; (R1) 1.6137; More...

Intraday bias in EUR/AUD stays on the downside for the moment. Current decline is expected to continue to 100% projection of 1.6679 to 1.6211 from 1.6418 at 1.5950. Firm break there will target 1.5846 key support next. For now, risk will stay on the downside as long as 1.6159 resistance holds, in case of recovery.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor at a later stage.

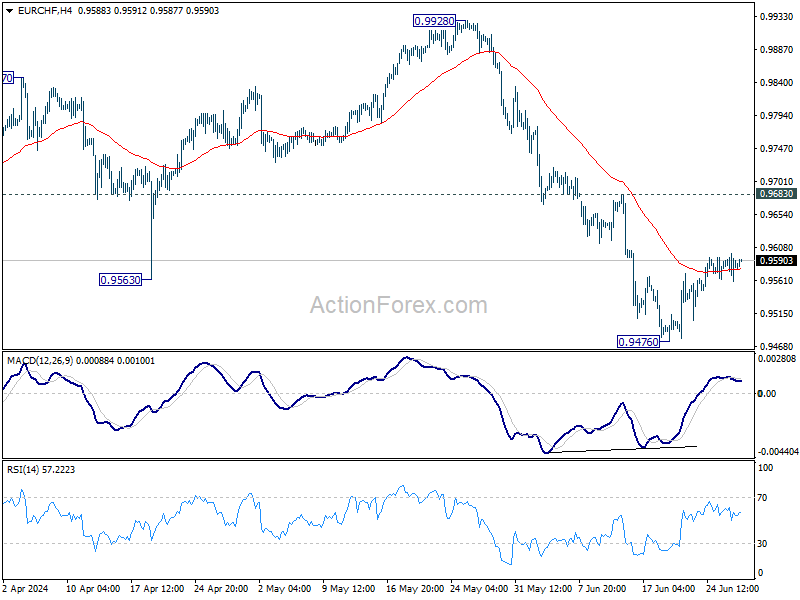

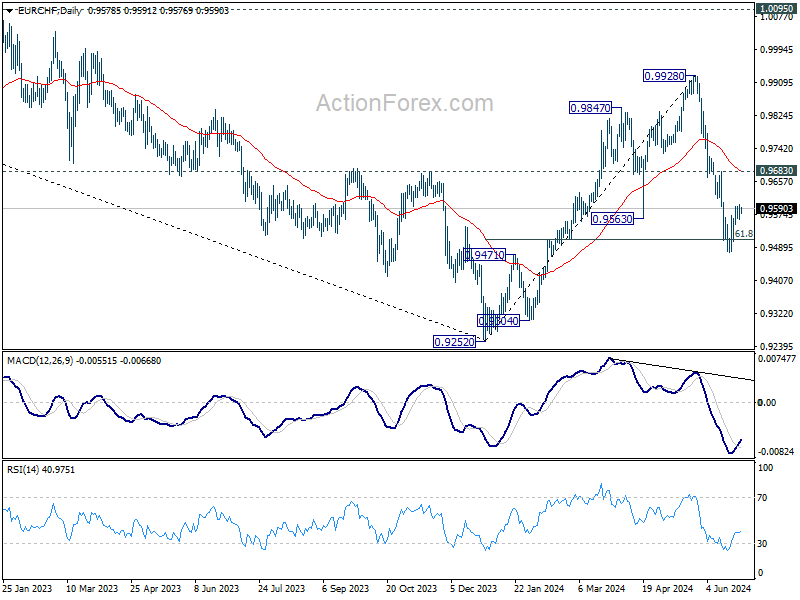

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9564; (P) 0.9582; (R1) 0.9603; More....

No change in EUR/CHF's outlook as consolidation from 0.9476 is extending. Intraday bias remains neutral for the moment. Outlook will remain bearish as long as 0.9683 resistance holds. On the downside, break of 0.9476, and sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will bring retest of 0.9252 low next.

In the bigger picture, rebound from 0.9252 should have completed at 0.9228. Medium term outlook remains bearish with 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

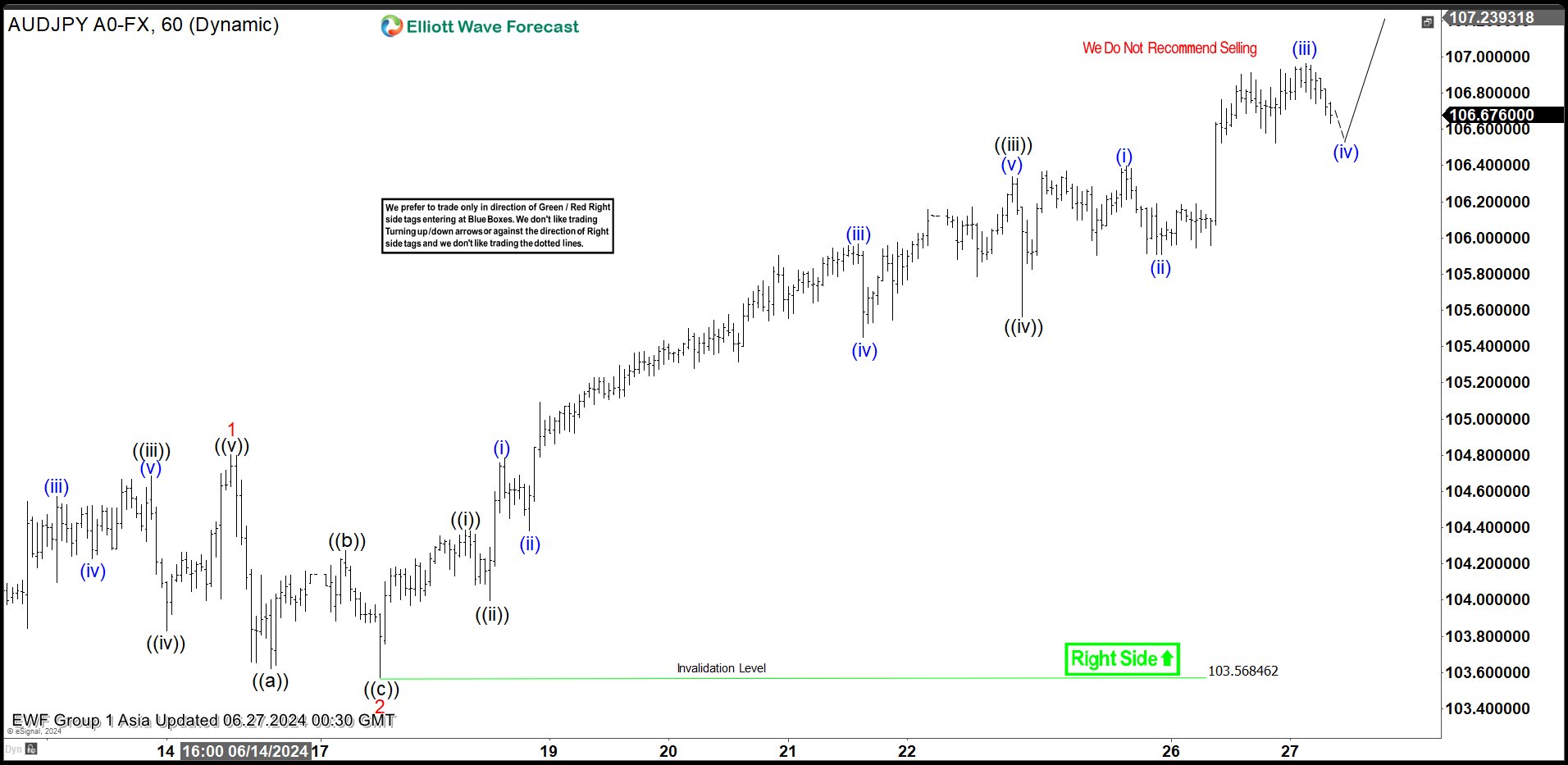

Elliott Wave Intraday Analysis on AUDJPY Looking to End Wave 5

Short Term Elliott Wave in AUDJPY suggests rally from 6.4.2024 low is in progress as a 5 waves impulse structure. Up from 6.4.2024 low, wave 1 ended at 104.8 and pullback in wave 2 ended at 103.57. Internal subdivision of wave 2 unfolded as a zigzag where wave ((a)) ended at 103.6, wave ((b)) ended at 104.27, and wave ((c)) lower ended at 103.56. This completed wave 2 in higher degree and the pair has turned higher in wave 3. Up from wave 2, wave ((i)) ended at 104.38 and pullback in wave ((ii)) ended at 104.

Pair has extended higher in wave ((iii)). Up from wave ((ii)), wave (i) ended at 104.78 and dips in wave (ii) ended at 104.38. Pair extended higher in wave (iii) towards 105.96 and pullback in wave (iv) ended at 105.45. Final leg wave (v) ended at 106.33 which completed wave ((iii)). Pullback in wave ((iv)) ended at 105.56. Pair has extended higher in wave ((v)) with internal as another impulse in lesser degree. Up from wave ((iv)), wave (i) ended at 106.39 and dips in wave (ii) ended at 105.90. Wave (iii) higher ended at 106.96. Expect pullback in wave (iv) before it resumes higher. Near term, as far as pivot at 103.56 low stays intact, expect dips to find support in 3, 7, or 11 swing for further upside.

AUDJPY 60 Minutes Elliott Wave Chart

AUDJPY Elliott Wave Video

https://www.youtube.com/watch?v=vv4Ut_3b2gA

Need Morphine

The selloff in Japanese yen extended yesterday sending the currency to the lowest levels since 1986 against the US dollar and to the lowest levels against the euro. The EURJPY is now flirting with the 172 level, while the USDJPY is consolidating gains above the 160 level. The only thing that prevents the yen from a further fall is the direct intervention risk. But other than that, the yen deserves to lose more blood. One-year risk reversals, which show how traders feel about the yen over a longer time, hint that they're still kind of excited about the yen compared to the dollar. But that excitement is fading fast as the Bank of Japan (BoJ) keeps delaying its intervention plans meanwhile the Federal Reserve delays its rate cutting plans. The BoJ is expected – is obliged – to give a clearer roadmap regarding how it will reduce its bond purchases in July meeting. They might also be obliged to hike rates given that the pressure on the yen won’t ease until concrete steps are taken on the policy front. Everyone knows that a direct FX intervention will be nothing more than just another morphine injection: it won’t give the yen more than a temporary relief.

Elsewhere, the euro remains under the pressure of French political shenanigans. The EURUSD gets comfortable below the 1.07 level and the downside pressure will likely mount from now to the weekly close as many investors will probably chose to exit their long euro exposure before the first round of the legislative election that’s due this weekend in France (and which will likely confirm the French preference for Marine Le Pen’s party). Sentiment data due this morning from the Eurozone could also put numbers on the European political worries.

Across the Channel, the British pound also comes under pressure. Cable cleared important technical supports yesterday as it slid below the 100 and 50-DMAs and below the major 38.2% Fibonacci retracement on April to June rally, meaning that the pair has now stepped into the medium term bearish consolidation zone and is vulnerable to a further fall against the US dollar. The next support zone sits at 1.2560/80, the zone that shelters the 200-DMA and the 50% retracement. We could see the pound bears take aim at this range given that the general election in the UK is approaching. There is not much doubt about a Torie washout. This being said, there is a problem that the FT summarizes very well in just one sentence: Labour and the Conservatives are on course to register their lowest combined vote share in a century, according to pre-election polls. The latter could leave the country with a lot of political uncertainties moving forward.

Far, far away from home, the Australian dollar is among rare major currencies that challenge the dollar’s strength, after the Australian inflation hit 4% in May, leaving the RBA doves with no more energy to fly. But overall, the weakness in euro, pound and yen sent the US dollar index to the highest levels since the beginning of May, and expect more inflows into the greenback before the French election weekend.

One thing that could derail the US dollar’s positive trajectory this week is economic data. Due today, the US will reveal its latest GDP update, and tomorrow we will have a look at the core PCE – the Federal Reserve’s (Fed) favourite gauge of inflation. What the Fed doves want to see is a reasonably softer economic growth combined with softening inflation. The risk is seeing a softening growth with insufficient retreat in inflation. Good news is that the inflation component in the GDP report won’t matter much as inflation has started to ease after an early uptick in Q1, so we won’t have the full picture to speculate on new Fed scenarios before tomorrow’s PCE release. In all cases, rising bets that the Fed could cut rates by 300bp in the next nine months is overdone unless a big, big problem emerges in the US economy.

In equities and bonds, the US 2-year yield was slightly higher yesterday, the 5 and 10-year yields rose to the highest levels in two weeks despite a good 5-year bond auction as the rising Japanese yields rose anxiety among bond investors, but not among stock buyers. The S&P500 and Nasdaq closed slightly higher on Wednesday thanks to a late rally, as Amazon hit a record high following a 3.9% rally and reached the $2 trillion mark in terms of market cap for the very first time after announcing its plans to launch a Temu-like discount section that ships goods directly from China. Temu’s owner PDD plunged below its 50-DMA on the news. Rivian rose 23% after Volkswagen said it will invest $5bn to a joint venture to produce the next generation EVs with the struggling Rivian, while Micron fell 8% in late trading despite better-than-expected earnings and revenue, because the revenue forecast for the current quarter just met analyst expectations of $7.6bn for the current quarter. Yes, anything less than fantastic is not good enough when your share price got multiplied by three in just about 18 months. Finally, FedEx jumped 15% and Novo Nordisk – the biggest European company that sells weight-loss drugs – hit a fresh record after announcing that it could finally got the approval from Chinese authorities to sell its drugs to the Chinese (who wouldn’t need them if they stuck to their own delicious diet… )

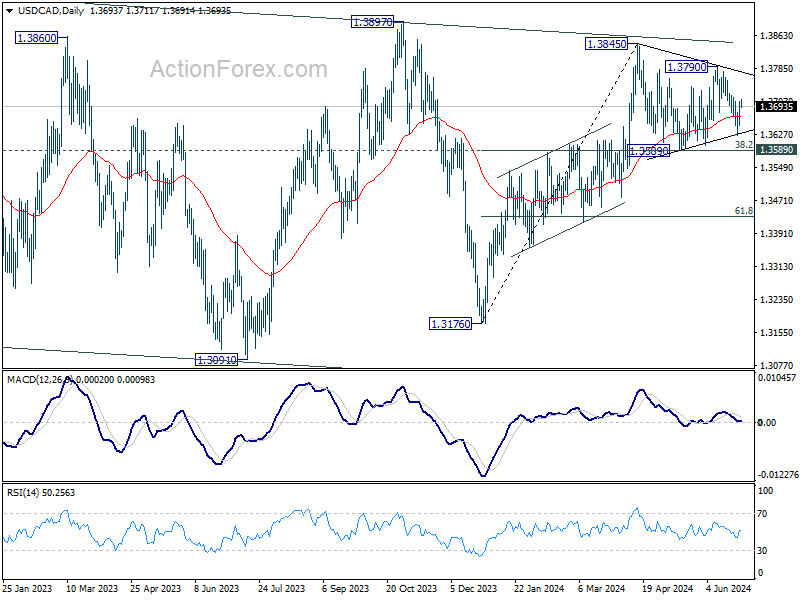

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3663; (P) 1.3685; (R1) 1.3725; More...

Intraday bias in USD/CAD is turned neutral with current rebound. Outlook is unchanged that corrective pattern from 1.3845 is still extending. Below 1.3626 will target 1.3589 cluster support. Nevertheless, break of 1.3717 will turn bias back to the upside for 1.3790 resistance instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6626; (P) 0.6658; (R1) 0.6679; More...

No change in AUD/USD's outlook as consolidation from 0.6713 is still extending. Intraday bias remains neutral at this point. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

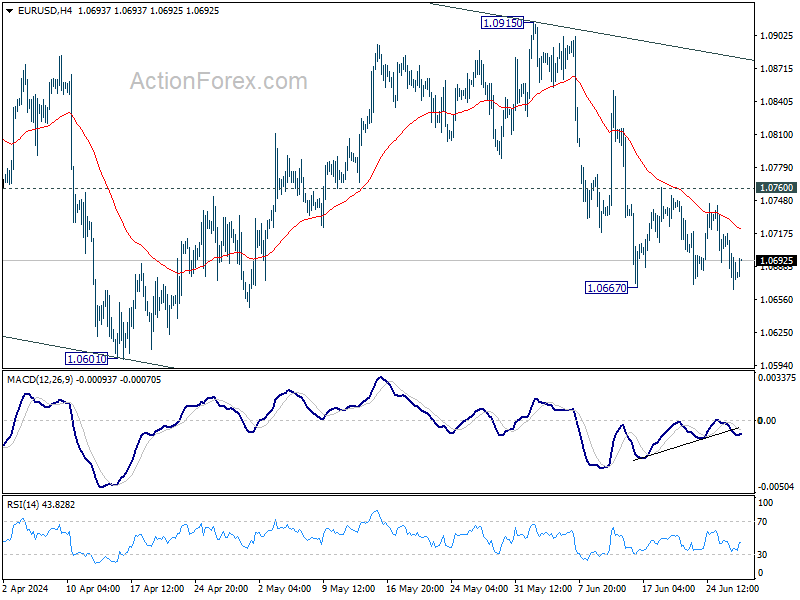

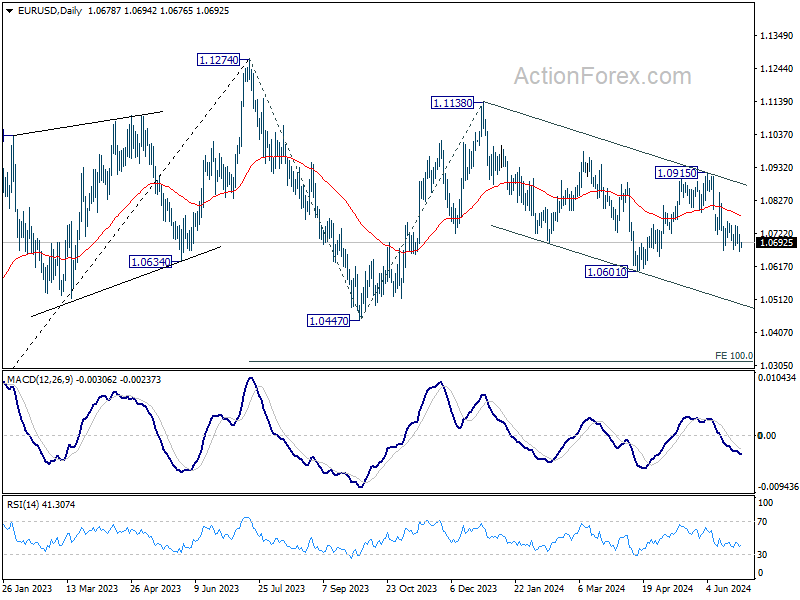

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0658; (P) 1.0688; (R1) 1.0710; More....

Intraday bias in EUR/USD remains neutral and consolidation from 1.0667 could extend. But still, outlook stays bearish with 1.0760 resistance intact. Decline from 1.0915 is seen as another leg in the larger corrective pattern. Break of 1.0667 will target 1.0601 and below. However, firm break of 1.0760 will turn intraday bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

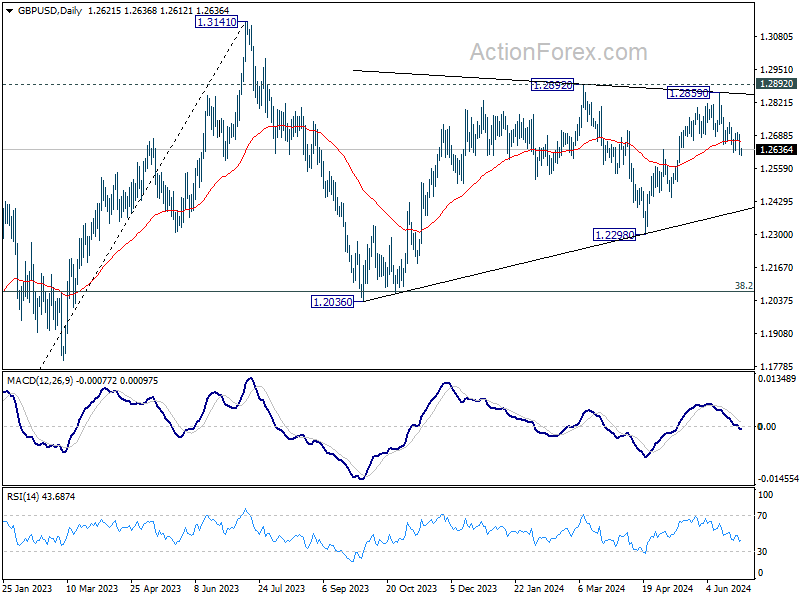

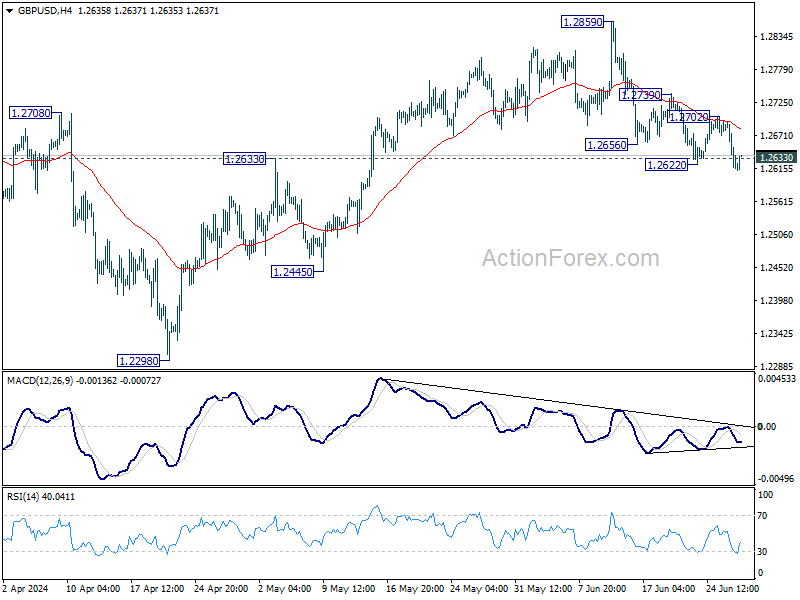

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2594; (P) 1.2644; (R1) 1.2672; More...

GBP/USD's fall from 1.2859 is trying to resume through 1.2622 temporary low and intraday bias is back on the downside. Sustained trading below 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below. On the upside, however, firm break of 1.2702 resistance will argue that pull back from 1.2859 has completed, and bring retest of this high instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.