Sample Category Title

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2666; (P) 1.2685; (R1) 1.2704; More...

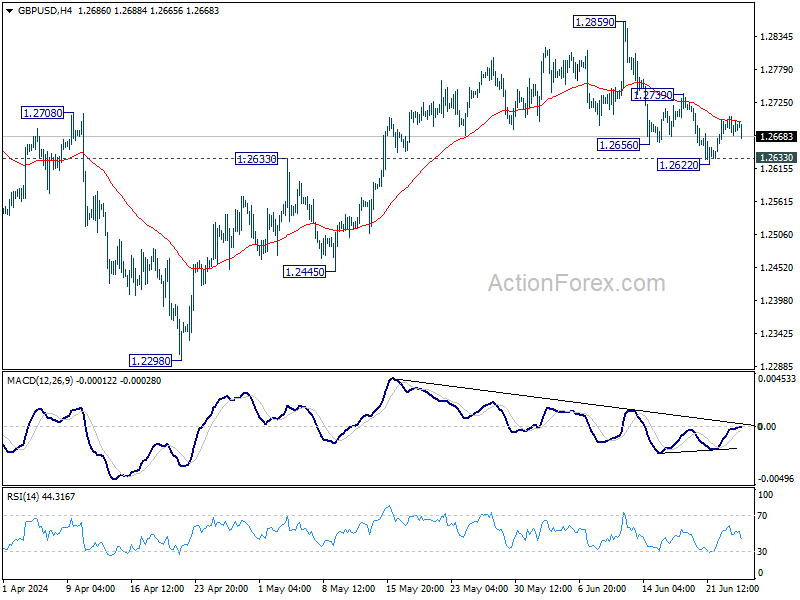

Intraday bias remains neutral for the moment, and further decline is expected in GBP/USD as long as 1.2739 resistance holds. Break of 1.2622, and sustained trading below 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below. However, firm break of 1.2739 will argue that pull back from 1.2859 has completed, and bring retest of this high instead.

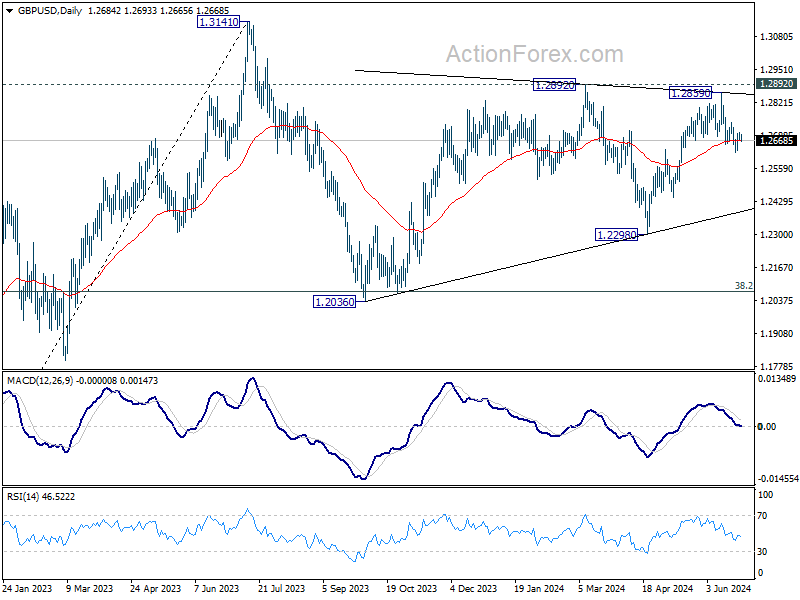

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.

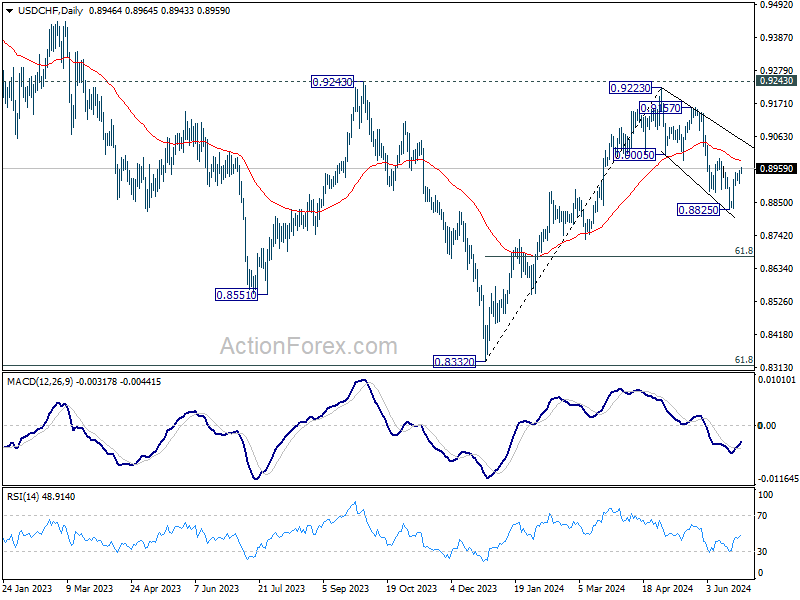

USD/CHF Daily Outlook

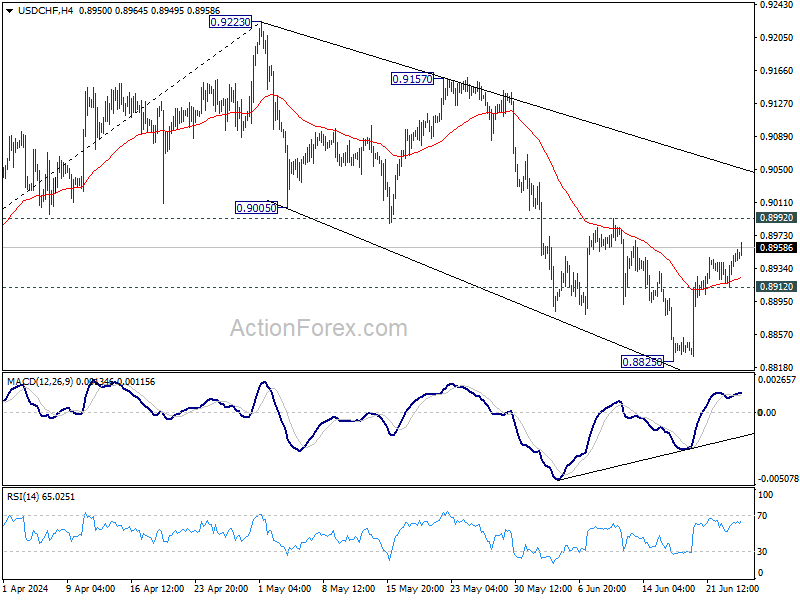

Daily Pivots: (S1) 0.8923; (P) 0.8938; (R1) 0.8964; More….

Intraday bias in USD/CHF remains neutral for the moment. While recovery from 0.8825 might still extend, near term outlook will stay bearish with 0.8992 resistance intact. Below 0.8912 minor support will bring retest of 0.8825 low. Firm break there will resume the fall from 0.9223 to 61.8% retracement of 0.8332 to 0.9223 at 0.8672.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

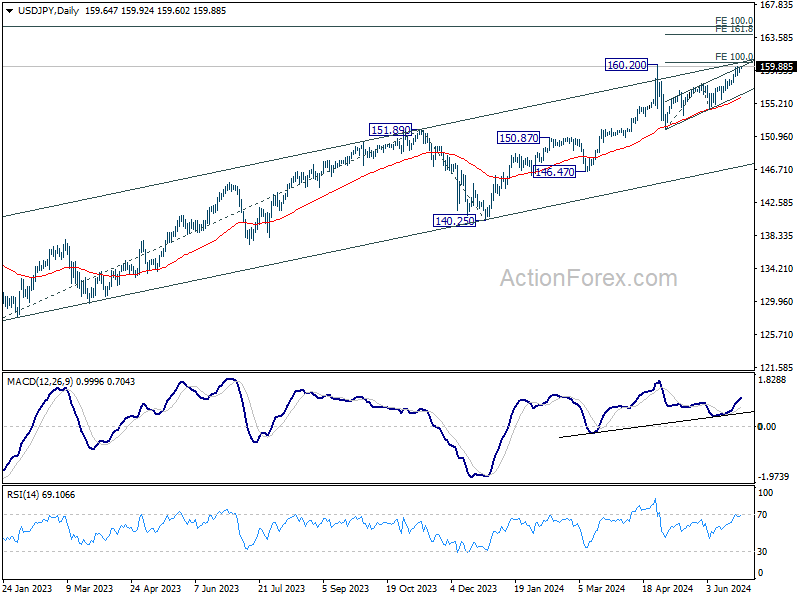

USD/JPY Daily Outlook

Daily Pivots: (S1) 159.33; (P) 159.55; (R1) 159.90; More...

Outlook in USD/JPY remains unchanged and intraday bias stays neutral first. Further rise will remain in favor as long as 157.70 resistance turned support holds. Sustained break of 106.20 and 100% projection of 151.86 to 157.70 from 154.53 at 160.37 will confirm long term up trend resumption, and pave the way to 161.8% projection at 163.97. Nevertheless, firm break of 157.70 will turn bias back to the downside for channel support (now at 156.41) first.

In the bigger picture, there is no sign of long term trend reversal yet. Further rally is expected as long as 150.87 resistance turned support holds. Decisive break of 160.02 will target 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

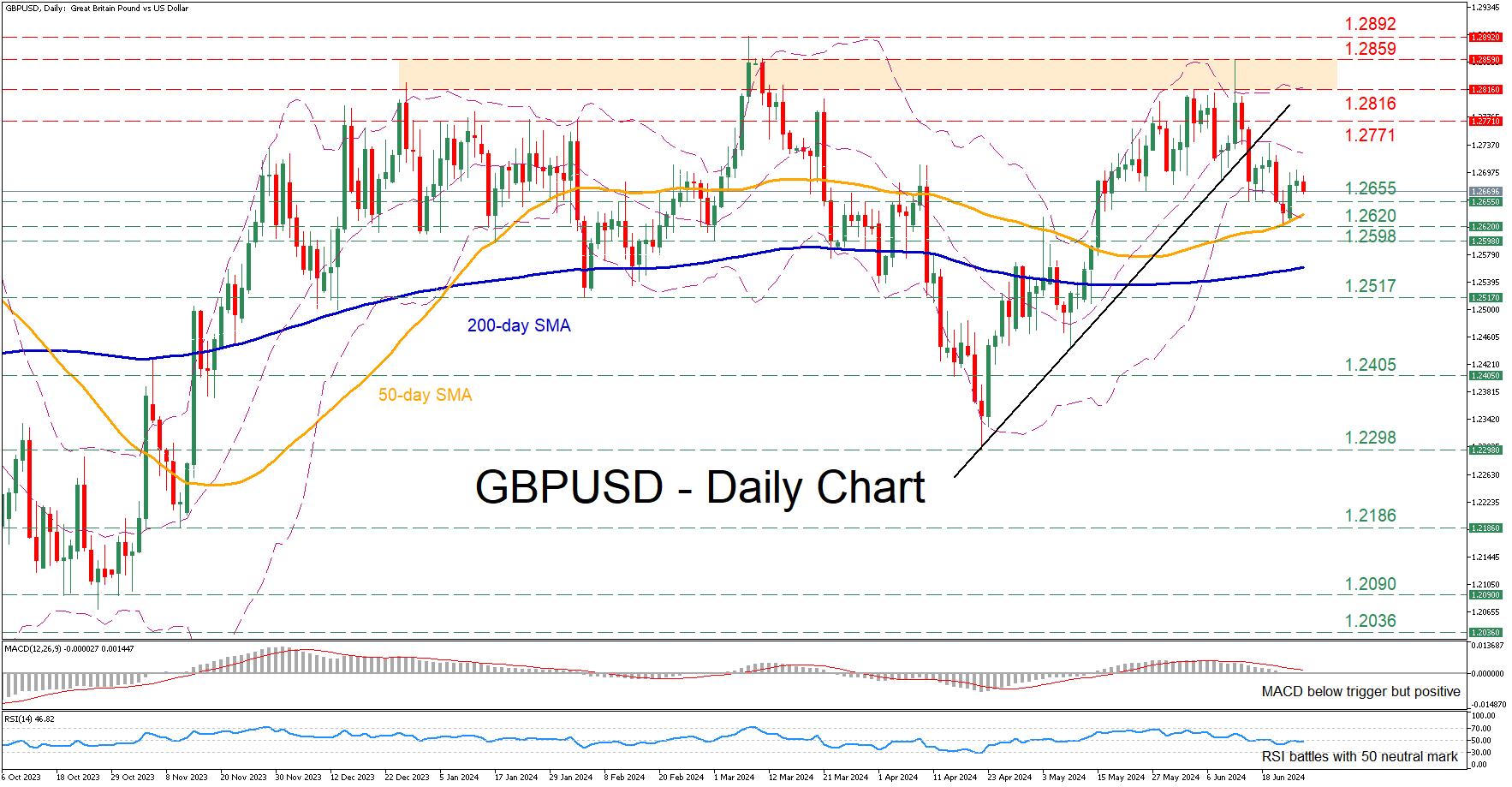

GBPUSD Bounces Off 50-Day SMA

- GBPUSD rebounds from a 1-month low

- But the price trades flat in past couple of sessions

- Momentum indicators improve but remain neutral

GBPUSD came under some selling pressure following its recent three-month peak of 1.2859, breaking below the short-term ascending trendline that connects its higher lows since April. Moreover, the pair fell to a fresh one-month low last week, but the 50-day simple moving average (SMA) prevented further retreats.

Should the short-term pullback extend, the June support of 1.2655 could act as the first line of defence. Sliding beneath that floor, the price could descend towards the recent one-month bottom of 1.2620. Failing to halt there, the pair might challenge 1.2598, a region that held strong both in January and March.

Alternatively, if the bulls regain the upper hand, the January-February resistance region of 1.2771 may come under examination. A violation of that zone could pave the way for the 1.2816-1.2859 range, defined by the recent three-month peak and the December 2023 high. Jumping above that range, the pair could revisit its 2024 high of 1.2892.

Overall, GBPUSD managed to pause its decline at the 50-day SMA, but its rebound does not look very promising. For that bearish sentiment to alter, the pair needs to break its short-term structure of lower lows.

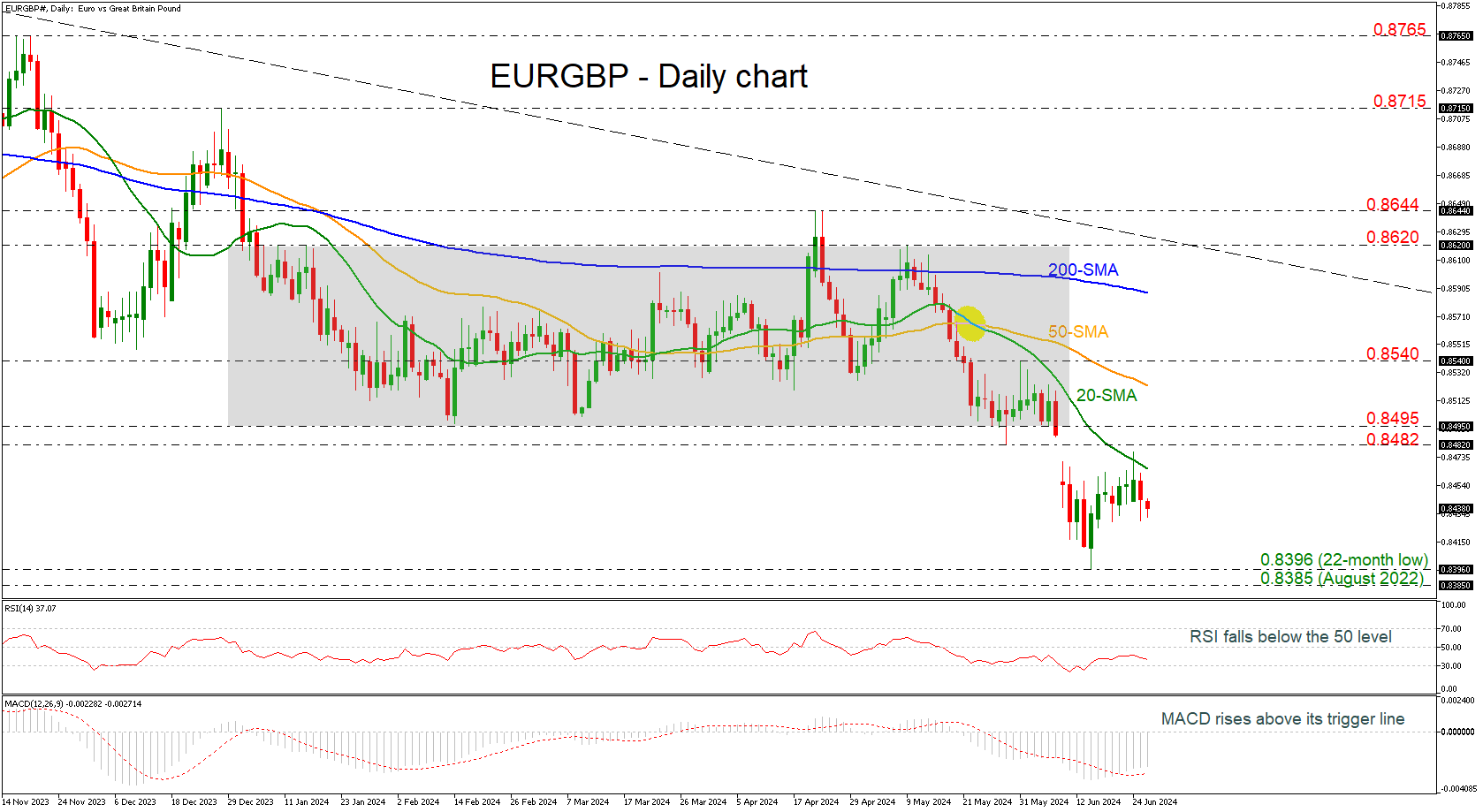

EURGBP Lacks Clear Direction in Short-Term

- EURGBP fails to recoup the negative gap

- RSI ticks down but MACD stands above its trigger line

EURGBP is heading south after the pullback off the 20-day simple moving average (SMA) around 0.8465. The pair is moving sideways after the European elections and the negative gap that was posted back on June 10.

Technically, the momentum oscillators indicate mixed signals. The RSI is sloping down beneath the neutral threshold of 50; however, the MACD oscillator is holding above its trigger line beneath the zero level.

If prices continue to move lower, support should come from the 22-month low of 0.8396 ahead of the August 2022 bottom at 0.8385.

However, should an upside reversal take form, immediate resistance will likely come from the 20-day SMA at 0.8465 ahead of recouping the gap and meeting the 0.8482-0.8495 restrictive region. A break higher could switch the outlook back to neutral one, testing the 50-day SMA at 0.8520.

In the medium-term, the outlook remains negative since prices hold below all the moving average lines and the bearish cross between the 20- and the 50-day SMA stays in place.

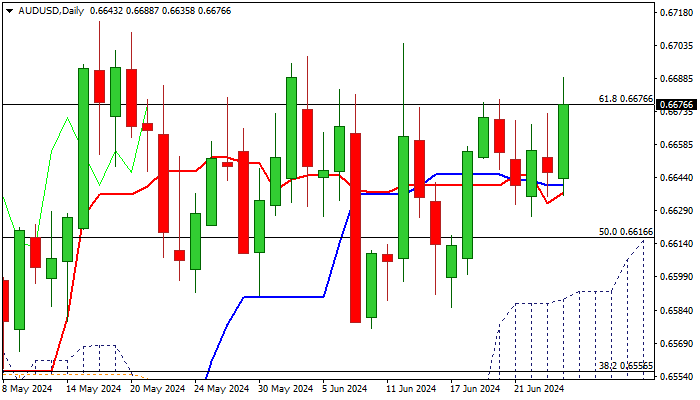

AUD/USD: Jumps on Higher Than Expected Australian Inflation

Australian dollar rose 0.6% in early Wednesday, lifted by higher than expected inflation (May 4.0% vs 3.6% in April and 3.8% f/c), which hit the highest in six months.

Fresh rise in consumer prices adds to RBA’s hawkish stance, with jump in bets for August rate hike making the Aussie dollar more attractive.

Near-term action remains underpinned by rising and thickening daily Ichimoku cloud, Ma’s in bullish setup and 14-d momentum ascending above the centreline.

Fresh bulls probe again through pivotal Fibo barrier at 0.6676 (61.8% of 0.6871/0.6362) where a number of attacks in past three weeks failed and guards key barriers at 0.6691/94 (2024 peaks), break of which to signal continuation of larger uptrend from 0.6362 (2024 low).

Initial supports lay at 0.6646/43 (converging 10/20DMA’s) and 0.6626 (June 26 low) guarding daily cloud top (0.6592).

Res: 0.6694; 0.6714; 0.6728; 0.6750.

Sup: 0.6653; 0.6626; 0.6616; 0.6592.

Aussie Forming Bullish Triangle, Looking for a Break Higher

The Australian dollar is still sideways against the US dollar, trapped in a range for more than a month. However, the price is now moving towards the upper side of thE pattern, suggesting a greater chance that this could be a bullish triangle rather than a deeper corrective move that would take us back to 0.6570. If this analysis is correct, we are currently in a subwave d, meaning there could still be some intraday weakness down to the 0.6620 to 0.6640 potential support levels. This leg down, would be wave "e" then, the final piece of this bullish structure, which should eventually take the price higher.

However, if the price closes above 0.6700 today or tomorrow, the triangle is most likely already finished, and we should expect a straight move higher, possibly even to the 0.6780 area.

I also covered Aussie in our video below.

https://www.youtube.com/watch?v=egoDOIBDzME&t=706s

AUD/USD Daily Report

Daily Pivots: (S1) 0.6630; (P) 0.6652; (R1) 0.6668; More...

AUD/USD jumps notably today but stays in consolidations below 0.6713. Intraday bias remains neutral at this point. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

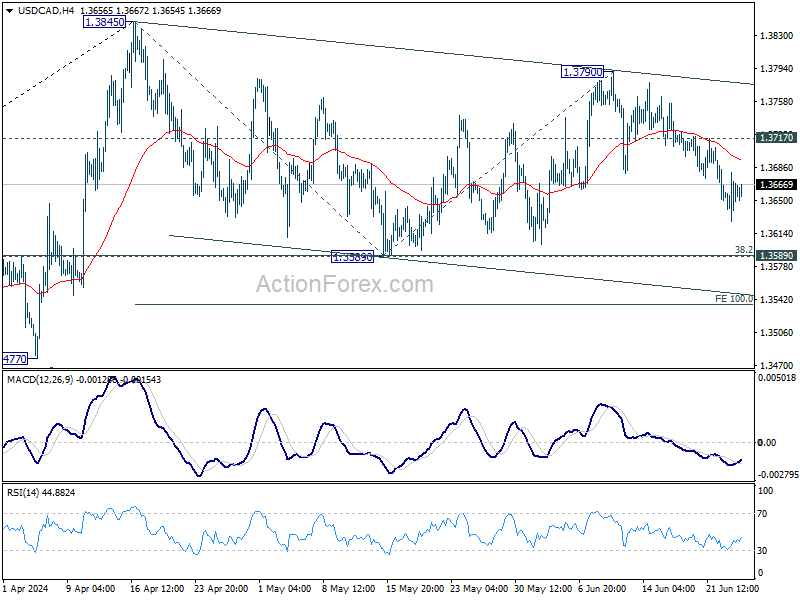

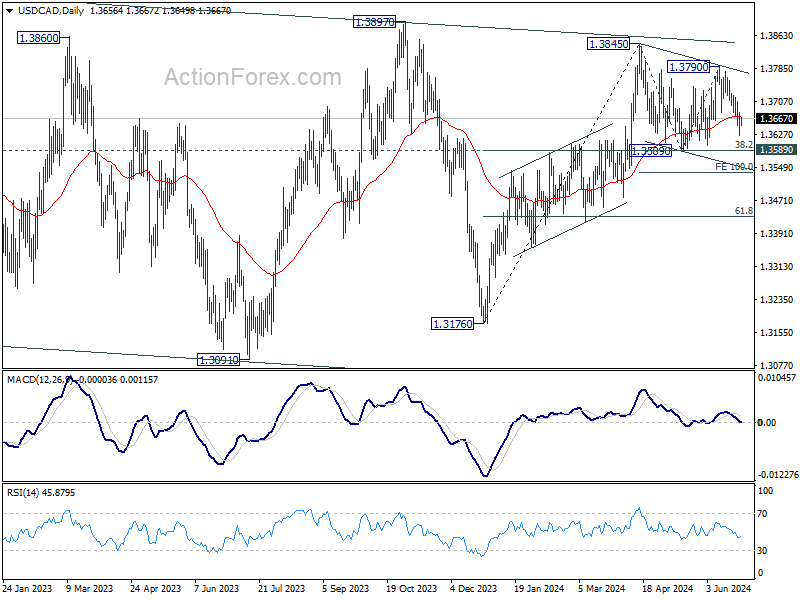

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3633; (P) 1.3657; (R1) 1.3682; More...

Further decline is expected in USD/CAD as long as 1.3717 minor resistance holds. Corrective pattern from 1.3845 is now in the third leg. Deeper decline would be seen to 1.3589 support. Break there will target 100% projection of 1.3845 to 1.3589 from 1.3790 at 1.3534.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

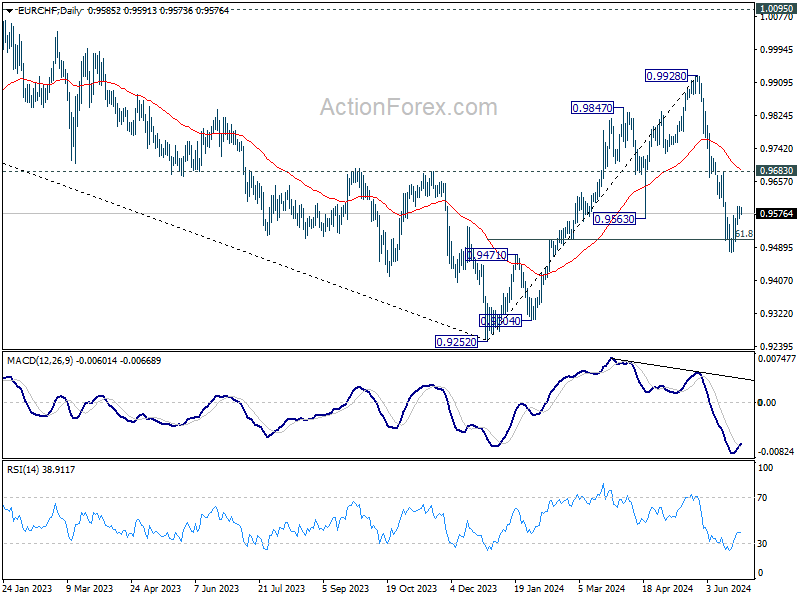

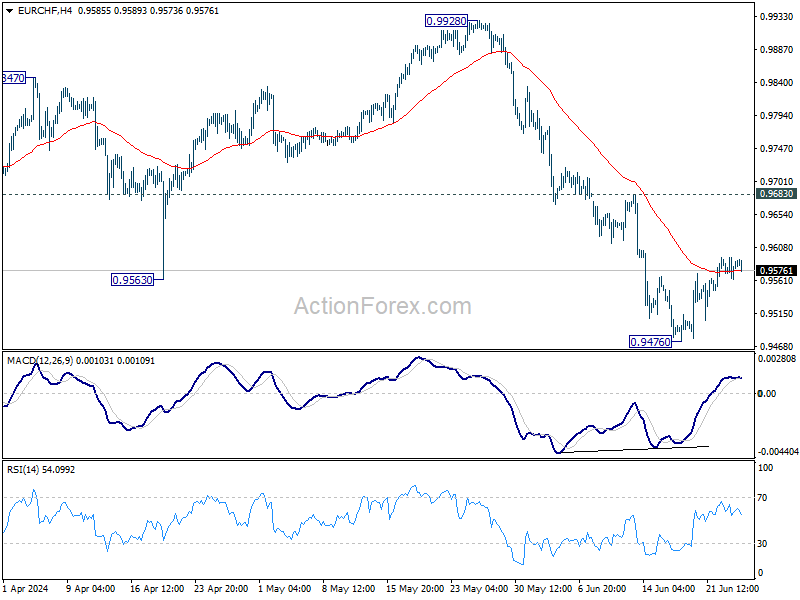

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9569; (P) 0.9582; (R1) 0.9600; More....

EUR/CHF is staying in consolidation from 0.9476 and intraday bias stays neutral. Outlook will remain bearish as long as 0.9683 resistance holds. On the downside, break of 0.9476, and sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will bring retest of 0.9252 low next.

In the bigger picture, rebound from 0.9252 should have completed at 0.9228. Medium term outlook remains bearish with 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).