Sample Category Title

Alarm Bells in USD/JPY (159.80) Keep Ringing

Markets

Washington-based Fed governor Cook in a speech for the Economic Club of NY joined SF Fed Daly (voter) in warning that the US labour market could change very quickly and that official stand ready to respond. She also referred to the fact that payrolls job gains were overstated last year and may continue to be this year. A first big revision by the Bureau of Labour Statistics is due by the end of August and could be a gamechanger in deciding the outcome of the September FOMC meeting. For now, the labour market is “tight, but not overheated” in Cook’s view. Unlike hawkish Fed Bowman earlier on the day, Cook is solely looking in the direction of a rate cut as next move, but the timing remains unclear. She hails progress made on the inflation front and expects three- and six-month inflation rates to continue to move lower on a bumpy path with more favorable monthly inflation readings for the rest of the year (more similar to H2 2023 instead of Jan-Apr this year). She expects a sharper decline next year as the past slowing on new leases starts impacting housing-services inflation. Slightly negative core goods inflation and easing supercore inflation should also help. Cook’s comments didn’t impact yesterday’s intraday market dynamics which were mostly sentiment-driven and technical by nature. US yields eventually added 1-2 bps across the curve but are stuck near recent correction lows. The dollar was again better bid, closing at EUR/USD 1.0714. Alarm bells in USD/JPY (159.80) keep ringing. US consumer confidence held up somewhat better in June (100.4 vs 100 consensus) though coming from a downward revision in May (101.3 from 102). Details showed a bigger deterioration in the expectations component with both future income and business conditions weakening. The US Treasury’s $69bn 2-yr Note auction met with good demand after last month’s little scare. US stock markets (mainly Nasdaq; +1.26%) rebounded, driven by Nvidia.

Today’s eco calendar is extremely thin, paving the way for more rangebound action. ECB Rehn this morning labelled bets for two more ECB rate cuts this year as reasonable and believes that the current market view of a 2.25%-2.50% terminal rate is also fair. He doesn’t see disorderly market move in France or a debt crisis in the making, suggesting that the ECB won’t have to use its “Transmission Protection Instrument”, a back-up tool allowing the ECB to buy bonds from countries experiencing a deterioration in financing conditions mot warranted by fundamentals. EUR/USD is a tad softer near 1.07.

News & Views

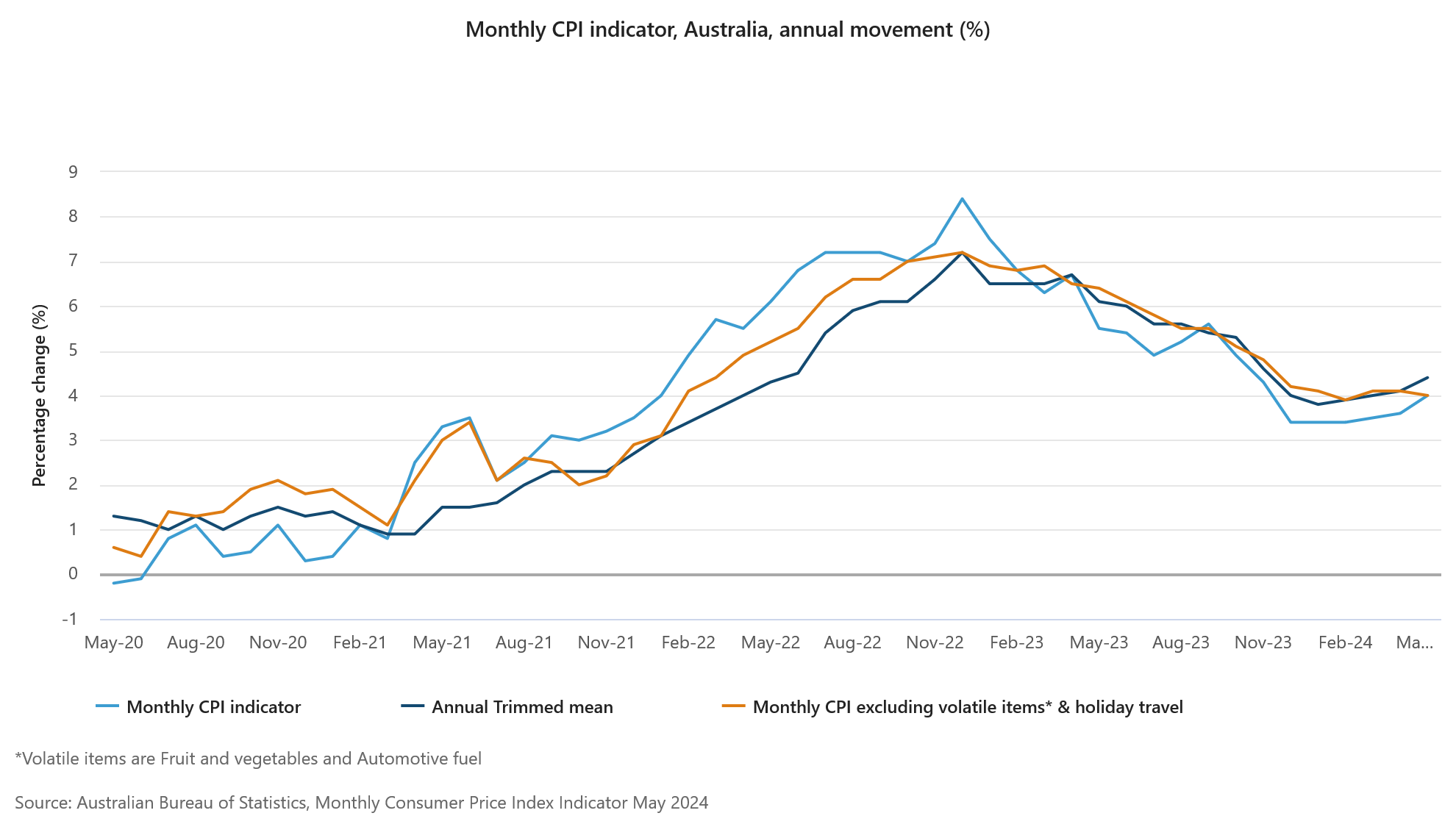

Australian CPI rose to 4% Y/Y from 3.6% in April (vs 3.8% consensus). On a monthly basis inflation eased 0.1%, but this came on the back of a monthly rise of 0.7% in April. The most significant contributors to the annual rise were housing (+5.2%), food and non-alcoholic beverages (+3.3%), transport (+4.9%), and alcohol and tobacco (+6.7%). Inflation excluding volatile items (fruit and vegetables, holiday travel and automotive fuels) eased slightly from 4.1% to 4% but also stays well above the 2-3% RBA inflation target. The trimmed mean measure of core inflation also climbed from 4.1% to 4.4%, the highest level in six months. The next RBA meeting takes place on August 6, a week after the publication of more important quarterly price data (July 31). At its June meeting, the RBA already indicated that felt uncomfortable with inflation easing more slowly than expected, not ruling out further rate hikes. Markets attach a 50% probability to the RBA effectively increasing its policy rate in autumn. The 3-y government bond yields adds 18 bps this morning (to 4.11%). AUD/USD gains from 0.6647 to 0.6685, but holds in the tight range between 0.6575 and 0.6715.

Reserve Bank of India Governor Das said that India needs to keep its focus on bringing inflation back to 4% as this is key to maintain stable growth rates. Indian inflation eased to 4.75% in May, down from 4.83% in April. However, the RBI governor indicated one severe weather-related shock via higher food prices could push headline inflation back to 5%. This risk together with ongoing strong growth should keep the RBI’s focus on inflation. With respect to Indian growth, the RBI governor is confident that the country meets the 7.2% growth projection for current fiscal year. He even sees the country being at the threshold of a structural shift in its growth trajectory that might put it at achieving 8% growth on a sustained basis. The RBI policy rate is unchanged at 6.5% since February of last year.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative (France) dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield is testing the downside of the 4.2/4.7% trading range.

EUR/USD

EUR/USD is stuck in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

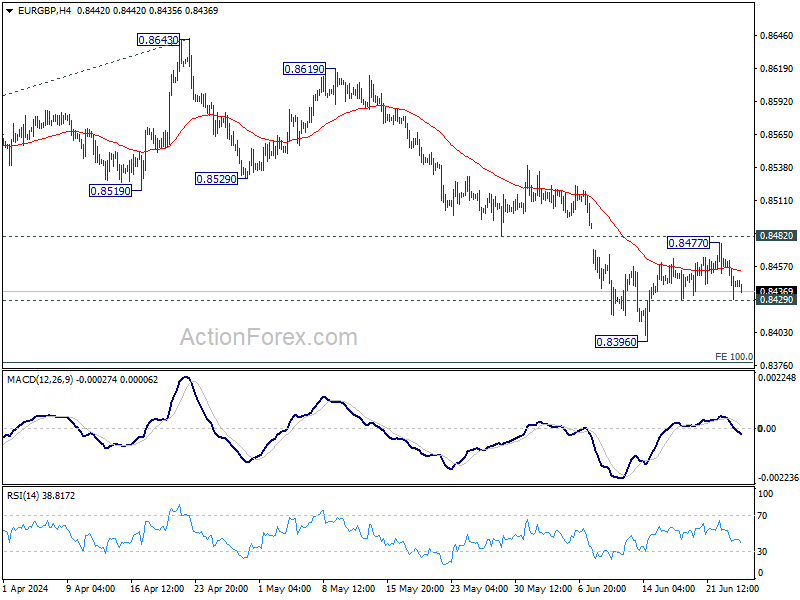

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. This might cap further sterling gains. At the same time, the euro remains vulnerable to political event risk going into the French elections. EUR/GBP 0.84 is becoming solid support.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6083; (P) 1.6113; (R1) 1.6149; More...

EUR/AUD's down trend resumes by breaking through 1.6026 today and intraday bias is back on the downside. Next target is 100% projection of 1.6679 to 1.6211 from 1.6418 at 1.5950. Firm break there will target 1.5846 key support next. For now, risk will stay on the downside as long as 1.6159 resistance holds, in case of recovery.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor at a later stage.

Strong Inflation Boosts Aussie, Euro Struggle Returns

Australian Dollar surged broadly in Asian session following a much stronger-than-expected monthly CPI report, sparking speculation that RBA might return to rate hikes in August. Comments from a top RBA official also indicated that the central bank is vigilant about upside risks to inflation. The upcoming inflation reports for June and the more critical Q2 data will be crucial for RBA's next move. Even if there isn't another rate hike, it's clear that interest rates will need to remain high for longer.

Canadian Dollar is following Aussie as the second strongest currency, continuing to benefit from stronger-than-expected Canadian CPI data released overnight. Dollar is currently the third strongest, supported by renewed weakness in Euro and Yen. Euro is at the bottom of the performance chart along with Swiss Franc, followed by Yen. British Pound and New Zealand Dollar are positioned in the middle.

Technically, EUR/GBP's recovery from 0.8396 might have completed at 0.8447 already, ahead of 0.8482 support turned resistance. Break of 0.8249 minor support will strengthen this bearish case and target 0.8396 low, and below. Downside breakout in EUR/GBP might also align with a break of the 1.0667 support in EUR/USD.

In Asia, Nikkei closed p 1.26%. Hong Kong HSI is up 0.21%. China Shanghai SSE is up 0.47%. Singapore Strait Times is down -0.15%. Japan 10-year JGB yield rose 0.0239 to 1.028. Overnight, DOW fell -0.76%. S&P 500 rose 0.39%. NASDAQ rose 1.26%. 10-year yield fell -0.010 to 4.238.

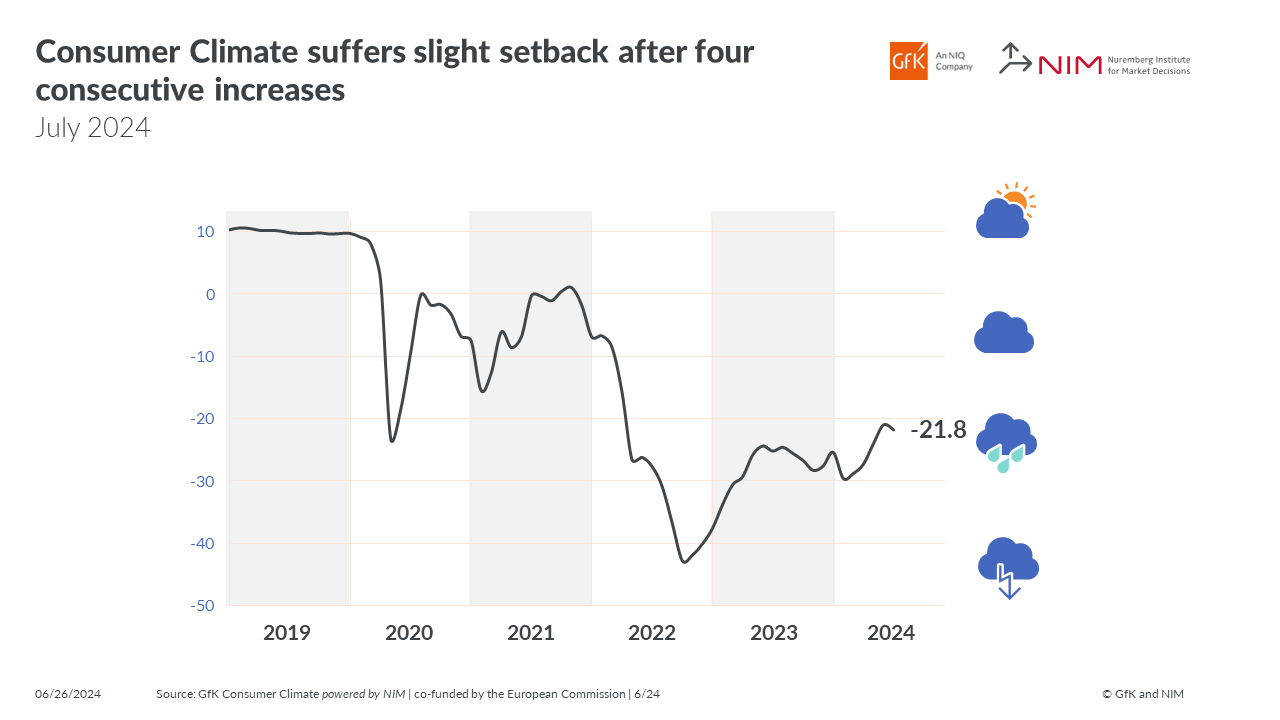

German Gfk consumer sentiment fells to -21.8, interruption of uptrend

Germany's Gfk Consumer Sentiment for July fell from -21.0 to -21.8, below expectation of -20.0. In June, economic expectations fell from 9.8 to 2.5. Income expectations fell from 12.5 to 8.2. Willingness to buy fell from -12.3 to -13.0. Willingness to save jumped again from 5.0 to 8.2.

"The interruption of the recent upward trend in consumer sentiment shows that the road out of the sluggish consumption will be difficult and there can always be setbacks," explains Rolf Buerkl, consumer expert at NIM.

Australia CPI jumps to 4%, trimmed mean rises to 4.4%

Australia's monthly CPI accelerated from 3.6% yoy to 4.0% yoy in May, well above expectation of a fall to 3.5% yoy. The last time it was higher was last November, when it was sitting at 4.3%.

CPI excluding volatile items and holiday travel ticked down from 4.1% yoy to 4.0% yoy. Annual Trimmed Mean CPI, on the other hand, surged from 4.1% yoy to 4.4% yoy.

The most significant contributors to the annual rise to May were Housing (+5.2%), Food and non-alcoholic beverages (+3.3%), Transport (+4.9%), and Alcohol and tobacco (+6.7%).

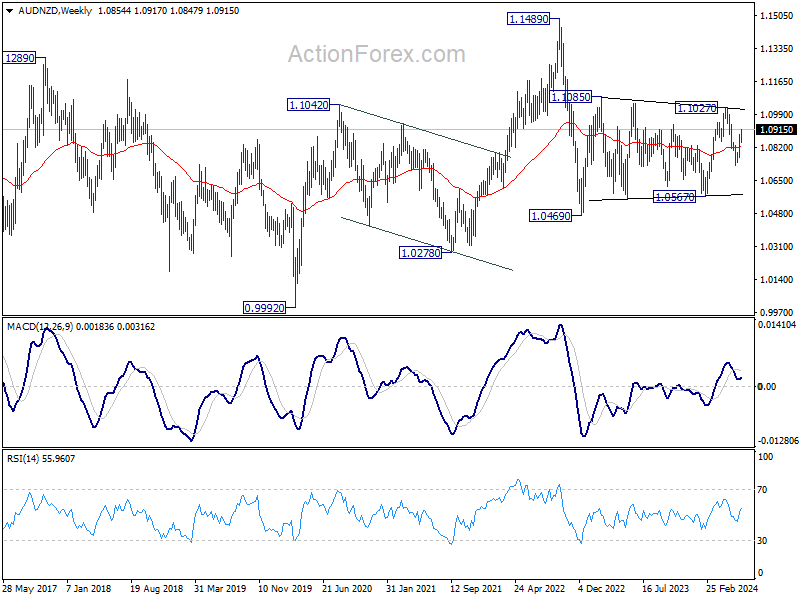

Speculation of RBA August hike drives AUD/NZD higher

Australian Dollar surges broadly today following reacceleration in monthly inflation data, sparking speculation that RBA might need to raise interest rates again. The inflation uptick places significant pressure on RBA to not only refrain from cutting rates anytime soon but potentially consider further rate hikes.

RBA's upcoming meeting in August is now seen as being "live," although a decision is not yet certain. The critical factor remains Q2 CPI report due on July 31, which will provide further clarity on the inflation outlook, will heavily influence RBA's policy decision.

Strength of Aussie is particularly noticeable against Kiwi. AUD/NZD's rally from 1.0730 resumed and hits as high as 1.0917 so far. The development solidifies that case that pull back from 1.1027 has completed at 1.0730, after hitting 61.8% retracement of 1.0567 to 1.1027.

Further rise is expected as long as 1.0846 support holds. Next target is the key resistance zone of 1.1027/1085. Decisive break there will resume whole medium term rebound from 1.0469 (2022 low). However, for this bullish scenario to unfold, RBA would need to actually implement additional tightening, rather then just keeping the option open.

RBA's Kent stresses vigilance amid mixed data and uncertainty over neutral rate

RBA Assistant Governor Christopher Kent, in a speech today, emphasized that recent economic data have been "mixed," reinforcing the need for RBA to "remain vigilant to upside risks to inflation." Kent reiterated that, regarding the path of interest rates, RBA is "not ruling anything in or out."

Kent noted that the recent median estimate among market economists suggested that the cash rate was around 1 percentage point above the nominal neutral rate. This indicates that current monetary policy is restrictive.

However, he acknowledged the significant uncertainty surrounding estimates of the neutral rate, making it unclear how restrictive monetary policy truly is.

Additionally, Kent mentioned that RBA's own models suggest that the neutral rate has increased since the pandemic, aligning with trends observed in other economies.

Fed's Cook: Dual mandate risks better balanced

In a speech last night, Fed Governor Lisa Cook stated that the risks to achieving Fed's dual mandate of employment and inflation have "moved toward better balance this year." However, she emphasized that the economic outlook remains "always uncertain."

Cook stressed the importance of addressing this uncertainty by considering "a range of scenarios," rather than relying solely on the baseline forecast. She believes that Fed's current policy is "well positioned" to respond to any changes in the economic outlook.

"At some point," Cook noted, it will be appropriate to start lowering interest rates. However, the timing of any such adjustment will depend on how economic data evolve and their implications for the outlook and balance of risks.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6083; (P) 1.6113; (R1) 1.6149; More...

EUR/AUD's down trend resumes by breaking through 1.6026 today and intraday bias is back on the downside. Next target is 100% projection of 1.6679 to 1.6211 from 1.6418 at 1.5950. Firm break there will target 1.5846 key support next. For now, risk will stay on the downside as long as 1.6159 resistance holds, in case of recovery.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M May | 0.00% | 0.00% | ||

| 01:30 | AUD | Monthly CPI Y/Y May | 4.00% | 3.50% | 3.60% | |

| 06:00 | EUR | Germany GfK Consumer Confidence Jul | -21.8 | -20 | -20.9 | -21 |

| 08:00 | CHF | UBS Economic Expectations Jun | 18.2 | |||

| 14:00 | USD | New Home Sales M/M May | 650K | 634K | ||

| 14:30 | USD | Crude Oil Inventories | -2.6M | -2.5M |

German Gfk consumer sentiment fells to -21.8, interruption of uptrend

Germany's Gfk Consumer Sentiment for July fell from -21.0 to -21.8, below expectation of -20.0. In June, economic expectations fell from 9.8 to 2.5. Income expectations fell from 12.5 to 8.2. Willingness to buy fell from -12.3 to -13.0. Willingness to save jumped again from 5.0 to 8.2.

"The interruption of the recent upward trend in consumer sentiment shows that the road out of the sluggish consumption will be difficult and there can always be setbacks," explains Rolf Buerkl, consumer expert at NIM.

Sentiment Improves Amid Nvidia Recovery, FedEx Earnings

Nvidia selloff didn’t deepen yesterday, on the contrary, the recent end-of-quarter / end-of-the-first-half pullback attracted dip buyers - if you can call it a dip yet - and Nvidia shares ended up jumping by almost 7% in a single session. Yesterday’s jump will certainly help to cool the downside pressure and ease long squeeze worries for Nvidia, but the decent and rapid price pullback is a sign that we might see an increased volatility and two-sided price moves moving forward. For now though, the fact that the selloff was not due to a fundamental reason certainly helped limiting damages.

When Nvidia smiles, major US indices follow suit. The S&P500 advanced 0.39% yesterday while Nasdaq 100 jumped more than 1%. Bitcoin also recovered after tipping a toe below the $60K per coin earlier in the weak.

In other crispy news, Rivian jumped more than 8.5% yesterday and soared 50% in the afterhours trading after Volkswagen announced that it will invest $5 billion to form a joint venture to develop the ’next generation battery-powered vehicles with leading-edge software’. It won’t bring Rivian’s share price to $180 per share seen right after an incredibly speculative and non-sense IPO, but it could help the company survive and grow at a reasonable pace.

Elsewhere, good news also came from FedEx. The shares jumped 15% after the company announced better-than-expected revenue and earnings amid massive cost cutting efforts tempered capital spending. Fedex expect demand to moderately improve through the next fiscal year and they are believed to be an indicator for the economic health.

All in all, yesterday was a good session, except for the Chinese stocks that were already under pressure and saw the downside pressure increase on news that OpenAI will be further curbing China’s access to its software. European stocks that remained under the pressure of French political shenanigans while Airbus was hit by a 9% selloff after lowering its profit outlook for this year by 20% due to supply chain problems in engines, aerostructures and cabin equipment. The Stoxx 600 was slightly lower on Tuesday, the French CAC 40 fell 0.58% but found support near the 200-DMA and the futures are pointing at a bullish start to the session at the time of writing; positive vibes from the US may help improve European investors’ mood despite political uncertainties and Airbus worries. Elsewhere, stocks in Japan continue to surf on a weak Japanese yen, and the USDJPY is still hovering near the 160 level, with limited appetite for further upside due to the FX intervention threat.

On the bond side, a $69bn US 2-year note sale saw a good demand and kept the 2-year yield near 4.70%. But consumer sentiment data from the US showed that current market conditions improved for the first time since the beginning of this year. Five out of eight Fed surveys released this month indicated increases in employment. Additionally, S&P Global’s preliminary purchasing managers’ index for June revealed that service sector payrolls grew at the fastest pace in five months, while manufacturing payrolls rose at the highest rate in 21 months. So it’s not time to cry victory for bond bulls just yet.

In the FX, the US dollar remains upbeat on mixed economic data and on a foggy outlook regarding what the Federal Reserve (Fed) might and might not do with its rates. The EURUSD remains offered into 1.0750 while the Loonie continues to remain bid on strong appetite for oil, and after a stronger-than-expected CPI update yesterday spoiled the rate cut expectations from the Bank of Canada (BoC).

In commodities, US crude consolidates gains below the $82pb Fibonacci resistance, while cocoa futures extend losses at increased speed on the back of favourable news for cocoa producers, including rain in Ghana that eased the supply concerns The bearish mood is also believed to be amplified by a lack of liquidity and a long squeeze. At this point, it looks like the cocoa bubble may have burst and the downside correction could continue until we reach reasonable levels for cocoa prices. My understanding of reasonable levels goes all the way down $2500/3000 a ton in the long run – which has been the trading range of the last 8 years - while we are still near $7800 a ton right now.

Tech Stocks Rebound

In focus today

Overnight China releases industrial profits for May. Profits grew 4% y/y in April, and we expect it to be roughly the same in May. Stronger export growth and higher commodity prices compared to last year should support profits, but tough competition weighs on profit margins. The next big market mover in China will be PMIs on Sunday 30 June.

In Sweden, markets are eagerly awaiting tomorrow's Riksbank decision. However, markets will have to settle with May PPI numbers released today. The print should be negatively affected by the sharp drop in electricity prices, as also evident in the CPIF. However, we do not expect any significant change to the domestic supply price component of the PPI concerning consumer goods, which is the relevant index for assessing the PPI's impact on CPIF goods prices.

Economic and market news

What happened overnight

In the US, the tech-heavy equity index Nasdaq had a comeback after a Monday marked by widespread losses led by chip maker Nvidia. The Nasdaq rose 1.3%, recovering what had been lost Monday. Asian tech stocks are significantly higher this morning after yesterday's rebound in the US.

What happened yesterday

In the US, Conference Board consumer confidence numbers for June came in at 100.4, thus slightly above consensus expectations of 100.0. This compares to a revised 101.3 in May. Unlike the comparable University of Michigan survey, the Conference Board's measure has consistently exceeded its historical average over the past few years. This is due to the greater emphasis on labour market conditions relative to personal finances (including inflation).

In the EU, sources confirmed to Reuters yesterday that Ursula Von der Leyen would be nominated for another term as Commission President. Former Portuguese Prime Minister Costa would be nominated as European Council President, and Estonian Prime Minister Kallas would be nominated as EU Foreign Policy Chief. All three nominations were widely expected after the four pro-EU factions (S&D, EPP, Renew, and Greens) held on to their majority at the European Parliamentary elections earlier this month. If the trio officially secures the top jobs it will provide some calm to the political uncertainty in the EU that has risen especially on the back of the French election. A second term for VDL means continuity of EU politics while Kallas as high representative means continued support for Ukraine.

The European Union charged Microsoft with breaching anti-trust laws. The EU's executive vice-president in charge of competition policy Margrethe Vestager stated the Commission is concerned 'Microsoft has given Teams an unfair advantage over other video conferencing applications' by bundling Teams together with its Office applications. The charges against Microsoft follow charges brought against fellow tech giant Apple on Monday, which stand accused of stifling competition on its App Store.

ECB will launch interim emission targets for its corporate debt holdings in the APP and PEPP according to a climate disclosure released yesterday. The new targets will be guided by the EU Benchmarks Regulation, including mandatory emission reductions. The targets will be used internally to identify deviations from the desired trajectory, which could lead to 'remedial actions' on a 'case-by-case' basis.

Speculation of RBA August hike drives AUD/NZD higher

Australian Dollar surges broadly today following reacceleration in monthly inflation data, sparking speculation that RBA might need to raise interest rates again. The inflation uptick places significant pressure on RBA to not only refrain from cutting rates anytime soon but potentially consider further rate hikes.

RBA's upcoming meeting in August is now seen as being "live," although a decision is not yet certain. The critical factor remains Q2 CPI report due on July 31, which will provide further clarity on the inflation outlook, will heavily influence RBA's policy decision.

Strength of Aussie is particularly noticeable against Kiwi. AUD/NZD's rally from 1.0730 resumed and hits as high as 1.0917 so far. The development solidifies that case that pull back from 1.1027 has completed at 1.0730, after hitting 61.8% retracement of 1.0567 to 1.1027.

Further rise is expected as long as 1.0846 support holds. Next target is the key resistance zone of 1.1027/1085. Decisive break there will resume whole medium term rebound from 1.0469 (2022 low). However, for this bullish scenario to unfold, RBA would need to actually implement additional tightening, rather then just keeping the option open..

Australia CPI jumps to 4%, trimmed mean rises to 4.4%

Australia's monthly CPI accelerated from 3.6% yoy to 4.0% yoy in May, well above expectation of a fall to 3.5% yoy. The last time it was higher was last November, when it was sitting at 4.3%.

CPI excluding volatile items and holiday travel ticked down from 4.1% yoy to 4.0% yoy. Annual Trimmed Mean CPI, on the other hand, surged from 4.1% yoy to 4.4% yoy.

The most significant contributors to the annual rise to May were Housing (+5.2%), Food and non-alcoholic beverages (+3.3%), Transport (+4.9%), and Alcohol and tobacco (+6.7%).

RBA’s Kent stresses vigilance amid mixed data and uncertainty over neutral rate

RBA Assistant Governor Christopher Kent, in a speech today, emphasized that recent economic data have been "mixed," reinforcing the need for RBA to "remain vigilant to upside risks to inflation." Kent reiterated that, regarding the path of interest rates, RBA is "not ruling anything in or out."

Kent noted that the recent median estimate among market economists suggested that the cash rate was around 1 percentage point above the nominal neutral rate. This indicates that current monetary policy is restrictive.

However, he acknowledged the significant uncertainty surrounding estimates of the neutral rate, making it unclear how restrictive monetary policy truly is.

Additionally, Kent mentioned that RBA's own models suggest that the neutral rate has increased since the pandemic, aligning with trends observed in other economies.

Fed’s Cook: Dual mandate risks better balanced

In a speech last night, Fed Governor Lisa Cook stated that the risks to achieving Fed's dual mandate of employment and inflation have "moved toward better balance this year." However, she emphasized that the economic outlook remains "always uncertain."

Cook stressed the importance of addressing this uncertainty by considering "a range of scenarios," rather than relying solely on the baseline forecast. She believes that Fed's current policy is "well positioned" to respond to any changes in the economic outlook.

"At some point," Cook noted, it will be appropriate to start lowering interest rates. However, the timing of any such adjustment will depend on how economic data evolve and their implications for the outlook and balance of risks.