Sample Category Title

Canada’s Job Market Hits a Double in October, Unemployment Rate Falls to 6.9%

Canada gained 67k new jobs in October (0.3% m/m), defying forecasters, and building on September's gain. Gains through September and October have now offset losses in July and August. However, the details were mixed, with the private sector driving the increase (+73k), but positions were mainly part-time (+85K).

Job gains pushed the unemployment rate down two tenths to 6.9%, back to its level in July. Labour force growth has slowed sharply in 2025, but it continues to outpace job creation, with the unemployment rate still up three tenths from 6.6% in January.

Job gains were seen in wholesale and retail trade (+41k), transportation and warehousing (+30k) and information, culture and recreation (+25k). However, job losses were seen in construction (-15k).

Wage growth actually picked up in October with average hourly wages for employees up 3.5% versus a year ago, versus a 3.3% pace in September.

Key Implications

Canada's job market has hit a double, with solid back-to-back job growth in September and October. The labour market is proving a bit more resilient to trade tensions than we had expected, but October's data is not a home run. Zooming out, we see that the labour market has still softened through 2025 along a number of dimensions. Even with tighter immigration policy reducing labour force gains, the unemployment rate has risen, and wage pressures have cooled relative to a year ago.

This report will make the Bank of Canada more comfortable to sit on the sidelines and let the 275 basis points of rate cuts in this cycle work their way through the economy. While this report shows some resilience in Canada's labour market, it is not strength. Overall job market conditions remain soft. The Bank expects reduced inflation pressures from a weak domestic economy to weigh against inflation pressures from to U.S. tariffs and restructuring global supply chains.

Canada employment surges 66.6k in October, driven by part-time work

Canada’s labor market surprised to the upside once again in October, as employment jumped by 66.6k, far exceeding expectations of -4k decline. The robust increase followed an already strong 60.4k rise in September, signaling that continuous hiring momentum. Unemployment rate slipped from 7.1% to 6.9%, beating forecasts for 7.2%, while employment rate edged up from 60.6% to 60.8%.

However, the composition of the October gains was less encouraging. The headline strength was largely driven by part-time positions, which rose by 85k, while full-time employment contracted. On a more positive note, private-sector jobs increased by 73k, marking the first rise since June,.

Wage data also showed mild upward pressure, with average hourly pay up 3.5% yoy, accelerating from 3.3% yoy in September.

Fed’s Jefferson: Economy holding up, to proceed cautiously near neutral

Fed Vice Chair Philip Jefferson said in speech today that despite the lack of official data amid the ongoing U.S. government shutdown, private-sector indicators show the overall economy "has not changed much" in recent months. Growth continues at a moderate pace, while the labor market appears to be gradually cooling.

On inflation, Jefferson acknowledged that price growth remains elevated, but he attributed the "lack of progress in headline inflation" largely to tariff effects. He noted that underlying inflation measures continue to “make progress” toward target.

Jefferson reiterated his support for last week’s 25bps rate cut given the shift in risks toward weaker employment. He added that the policy stance remains somewhat restrictive but is now closer to neutral, making it sensible for the Fed to “proceed slowly” from here.

Looking ahead, Jefferson emphasized that future policy decisions will be made on a meeting-by-meeting basis. With the government shutdown likely to continue suppressing key releases before December, "this approach is especially prudent".

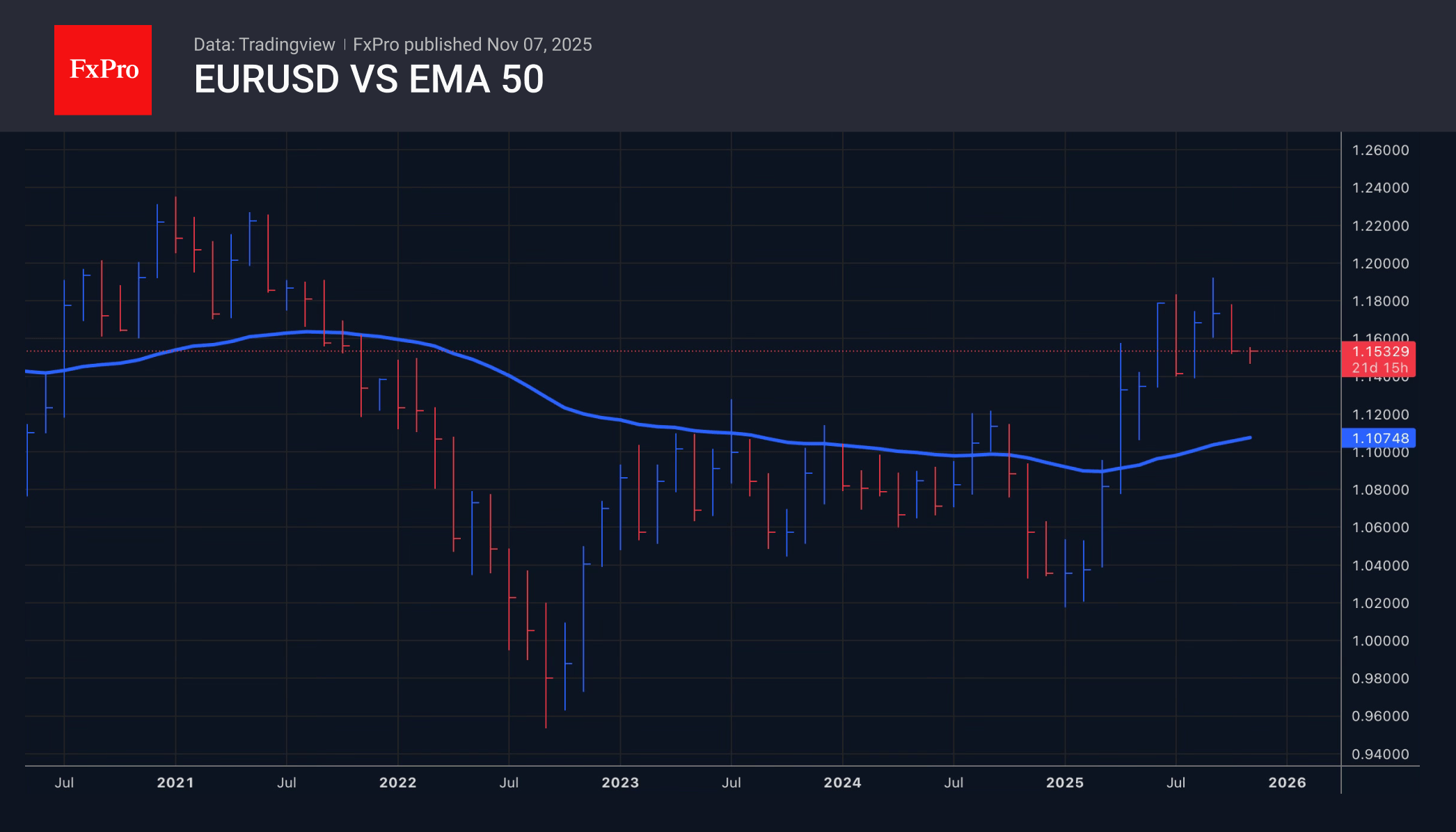

Dollar Risks Losing Support from Tariff Revenues

- The US risks losing tariff revenues.

- The American labour market is cooling down.

- EURUSD may rise to 1.21.

- The pound rose but remains under pressure.

The US dollar retreated against major world currencies after further evidence of labour market weakness and a decline in Donald Trump’s chances of winning in the Supreme Court to 20%, according to Polymarket. There is a lot at stake. The Treasury estimated budget revenues from tariffs at $750 billion by mid-2026. The president spoke of trillions of dollars in investment from other countries. The cancellation of tariffs does indeed risk being devastating for the US economy.

Donald Trump claims that his defeat in the Supreme Court will plunge the whole world into depression, and he is preparing plan B. After all, the tariffs were introduced to counter China’s restrictions on the export of rare earth elements.

Indeed, the removal of tariffs will accelerate both international trade and global GDP. The primary beneficiaries will be the currencies of exporting countries, including the euro. Unsurprisingly, Reuters experts predict that the EURUSD will strengthen to 1.18 and 1.20 in one and three months, respectively, and to 1.21 in six months.

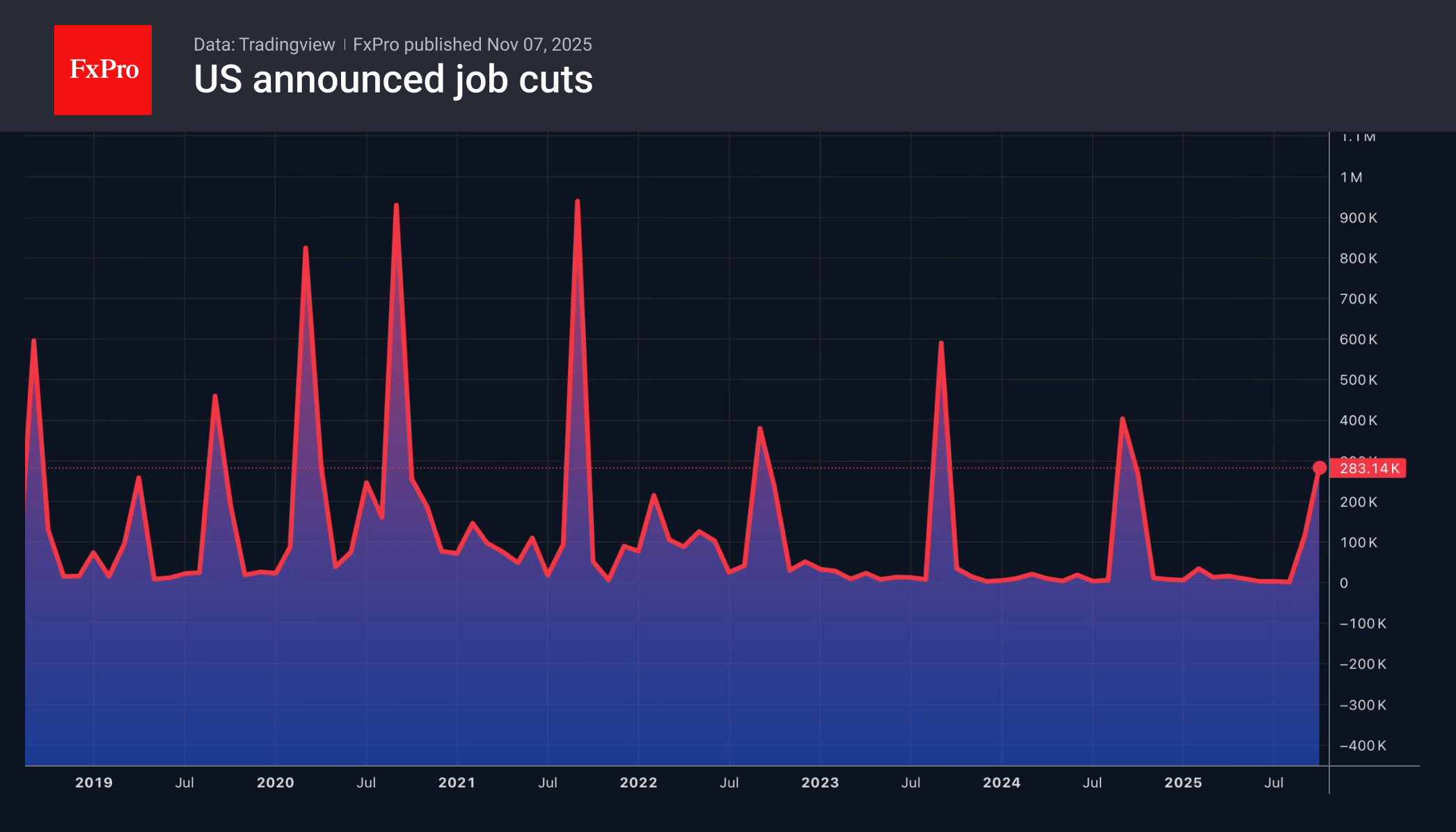

The US economy is cooling even without the cancellation of tariffs. In the absence of official data from the BLS, investors have to pay attention to alternative sources of information. They signal structural weakness in the labour market. This will most likely force the Fed to continue cutting rates. According to Challenger, US companies planned to cut more than 150,000 jobs in October, the highest number for that month in 22 years. This is bad news for the dollar.

Even the pound, frightened by the BoE’s resumption of its monetary expansion cycle, as well as imminent tax increases and government spending cuts, managed to counterattack against the greenback. The Bank of England kept its repo rate at 4% by a vote of five to four. However, the word ‘caution’ was removed from the accompanying statement. In addition, the MPC stated that the recent 3.8% consumer inflation rate would be the peak. Andrew Bailey argues that inflation risks have declined and become more balanced.

The dovish rhetoric suggests a high probability of a cut in the repo rate in December. Coupled with concerns about the Labour Party’s draft budget presentation at the end of November, this will put pressure on the pound.

From Bounce to Barrier: Oil Path to the Next Sell Zone

The short term price action in OIL suggests that the decline from 23rd June 2025 peak ended in 3 waves structure. Up from there, it has made a 5 waves bounce from the lows therefore we suspect that it can be correcting that cycle in simple zigzag correction into the path to the next sell zone. Now lets take a look at this hourly chart below:

OIL 1-Hour Elliott Wave Chart From 11.07.2025

Above is the latest hourly view on OIL from 11.07.2025 Asia update. In which, the decline from $56.29 low has completed wave (W) of the decline from 6.23.2025 peak. Up from there, the bounce unfolded in 5 waves impulse sequence where wave ((i)) ended at $58.27 high. Wave ((ii)) pullback ended at 56.99 low, wave ((iii)) rallied towards $62.20 and wave ((iv)) ended at $61.21 low. Then a new high towards $62.59 high ended wave ((v)) thus completed wave A of a zigzag correction.

Down from there, OIL is correcting the cycle from 10.20.2025 low in wave B pullback. The internals of this ongoing pullback is taking place as double three correction where wave ((w)) ended in lesser degree 3 waves at $59.70 low. Then another 3 wave bounce ended wave ((x)) at $61.50 high. Since than, wave ((y)) is unfolding in another 3 waves. But it can reach $58.61- $56.82 area lower first before starting the C leg higher.

OIL Elliott Wave Video:

https://www.youtube.com/watch?v=z8PN2rerR_w

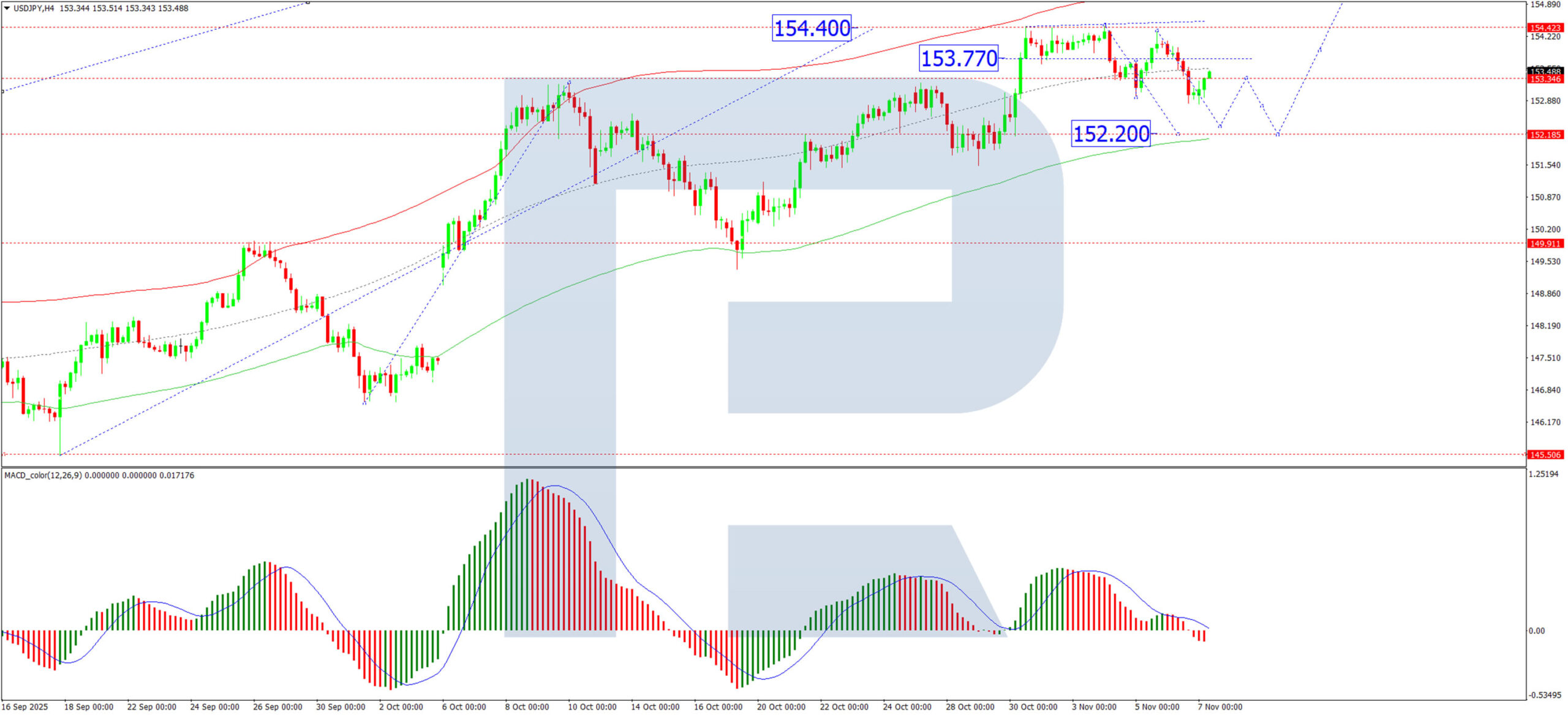

USD/JPY Declines as Safe-Haven Demand Bolsters the Yen

The USD/JPY pair retreated to 153.10 on Friday, with the yen retaining a portion of its recent gains amid a flight to safety. A sharp uptick in stock market volatility, driven by concerns over a potential overvaluation of artificial intelligence stocks, prompted investors to seek refuge in traditional safe-haven assets, thereby supporting the Japanese currency.

The pair faced additional pressure from a broadly weaker US dollar. Signs of a cooling US labour market have reinforced market expectations of an imminent interest rate cut from the Federal Reserve.

Domestic data from Japan presented a mixed picture. Consumer spending in September rose by a modest 1.8%, following a 2.3% increase in August and falling short of the 2.5% forecast. While nominal wage growth accelerated to 1.9%, real household incomes continued their decline, falling 1.4% year-on-year. This marks the ninth consecutive month of decline in real incomes, highlighting the persistent squeeze on purchasing power.

In light of this, Bank of Japan Governor Kazuo Ueda stated that the central bank's wage growth forecast for 2026 will be a critical determinant for resuming rate hikes. For now, the BoJ maintains its accommodative stance, leaving monetary policy unchanged.

Technical Analysis: USD/JPY

H4 Chart:

On the H4 chart, USD/JPY is forming a consolidation range around 153.33. We anticipate a near-term expansion of this range to the downside, targeting 152.20. Following this, the primary scenario involves an upward breakout, initiating a new bullish wave towards 155.70. An alternative downward breakout would signal a deeper correction towards 149.90 before any sustained recovery can begin. The MACD indicator supports this view, with its signal line below zero and pointing downward, confirming the current corrective momentum.

H1 Chart:

On the H1 chart, the pair is completing a corrective rise to test 153.50 from below. A tight consolidation range is forming around this level. We expect this range to break downwards initially, with a first target at 152.52. A rebound to 153.50 may follow. The broader trajectory hinges on the subsequent breakout. An upward breakout opens the path to 155.70, while a downward breakout would likely extend the correction towards 149.90. The Stochastic oscillator on the H1 offers a conflicting short-term signal. Its signal line is above 50 and rising towards 80, suggesting the potential for limited near-term upside before the next directional move.

Conclusion

USD/JPY is caught between a weaker US dollar and mixed domestic signals from Japan. The immediate driver is risk sentiment, which has provided the yen with temporary support. Technically, the pair is in a consolidation phase, with a near-term bias for a dip towards 152.20. The medium-term outlook, however, remains tentatively bullish, targeting 155.70, contingent on a successful upside breakout from the current range.

Gold Stays Flat as WTI Crude Faces Hurdles

Gold price corrected gains, traded below $4,000, and started a consolidation. Crude oil is showing bearish signs and might decline below $58.80.

Important Takeaways for Gold and WTI Crude Oil Prices Analysis Today

- Gold price started a downside correction below $4,100 and $4,000 against the US Dollar.

- A key bullish trend line is forming with support at $3,985 on the hourly chart of gold at FXOpen.

- Crude oil prices failed to clear the $61.20 region and started a fresh decline.

- There is a bearish trend line forming with resistance at $60.00 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price formed a base above $3,915. The price remained in a bullish zone and started an upward move within a range above $3,930.

There was a decent move above the 50-hour simple moving average and $3,975. The bulls pushed the price above the $4,000 and $4,010 resistance levels. A high was formed at $4,019 before the price saw a pullback.

The price dipped below the 23.6% Fib retracement level of the upward move from the $3,928 swing low to the $4,019 high, and the RSI declined below 50. Initial support on the downside is near $3,985, a bullish trend line, and the 50-hour simple moving average.

The first major area of interest for the bulls is near the 50% Fib retracement at $3,975. If there is a downside break below $3,975, the price might decline further. In the stated case, the price might drop toward $3,950. Any more losses might push the price toward $3,930.

Immediate resistance is near $4,020. The next major hurdle for the bulls is $4,030. An upside break above $4,030 could send Gold price toward $4,045. Any more gains may perhaps set the pace for an increase toward $4,090.

WTI Crude Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price struggled to clear $61.20 against the US Dollar. The price started a fresh decline below $60.00.

The bears gained strength and pushed the price below $59.50 and the 50-hour simple moving average. Finally, the price tested $58.80 and recently started a recovery wave. There was a move above $59.40, and the 23.6% Fib retracement level of the downward move from the $61.21 swing high to the $58.80 low.

The bears are now active below $59.80. If there is a fresh increase, the price could face a barrier near $60.00. There is also a bearish trend line forming with resistance at $60.00.

The first major resistance is near the 76.4% Fib retracement at $60.65. The next stop for the bulls could be near $61.20. Any more gains might send the price toward $62.00. Conversely, the price might start another decline and test $59.40.

The next major area of interest for the bulls on the WTI crude oil chart is $58.80. If there is a downside break, the price might decline toward $57.50. Any more losses may perhaps open the doors for a move toward $55.00.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Risk Sentiment Vulnerable to More Pronounced Correction Lower

Markets

Core bonds gained ground in yesterday’s risk-off trading session with US Treasuries significantly outperforming German Bunds. The former erased outsized losses suffered on Wednesday. US yields fell by 5.8 bps to 8.3 bps on a daily basis with the belly of the curve outperforming the wings. Changes on the German yield curve range between 1.7 bps and 2.3 bps. On both occasions, limited available US eco data were at least partly responsible for the move. First following better ADP employment data and a firm services ISM, next after a significant surge in… October Challenger job cuts. A data point which normally doesn’t make the shortlist of market-movers. US companies announced 153k job cuts in October, driven by technology and warehousing sectors. Year-to-date job cuts have exceeded 1 million, the most since the pandemic. In the same period, US-based employers have announced the fewest hiring plans since 2011. Markets are starving for more official numbers as the US government this week passed the previous record for longest shutdown. The US Senate is expected to vote again today on a new package to end the deadlock but it’s far from certain that it already satisfies Democratic demands. According to the WSJ, the package combines a short-term spending measures with three full-year funding bills (legislative branch, agriculture and military construction & veteran affaires). It would reopen the government through mid-December or January. Today’s eco calendar would have centred around October payrolls if it weren’t for the shutdown. Now we’ll have to do with November University of Michigan consumer confidence. It sets the stage for more sentiment-driven trading. Risk sentiment is vulnerable to a more pronounced correction lower. We look out whether the (trade-weighted) dollar makes a new attempt to break key resistance at 100.26 (August high & 200d moving average) in such circumstances.

The Bank of England left its policy rate unchanged yesterday at 4% in a 5-4 split vote. BoE governor Bailey who casted the tie-breaking vote, opened up for a rate cut as soon as December. Asked about his motives, he said that the (lower) September CPI was just one datapoint of the disinflation process being back on track. He also thinks that inflation peaked in September, implying that he’ll get the disinflation evidence he is looking for by December. Contrary to August when the onus was still on inflation, Bailey now thinks that risks (upside inflation vs downside growth/labour market) are now more in balance. It sets the stage for a Fed-like risk management exercise. The BoE-governor felt comfortable with the market implied rate path, landing the policy rate around 3.5%. On several occasions, he stressed that there was broad agreement – doves and hawks - that as the policy rate approached neutral, the contribution of monetary policy to underlying disinflation would become harder to discern, making the case for further policy easing more finely balanced. Sterling and broader UK markets weren’t really impacted by the BoE’s dovish hold with EUR/GBP still hovering near 0.88.

News & Views

Chinese October foreign trade data were substantially weaker than expected, both regarding exports and imports. Exports (in dollar terms) declined 1.1% Y/Y compared to still a 8.3% Y/Y gain in September. At the same time, import growth also slowed markedly from 7.4% Y/Y to 1 Y/Y. The trade surplus eased slightly to $90.07bn (from $90.45bn) while a modest further rise was expected. Both technical factors (high base effect from last year) and underlying momentum impacted the numbers. Exports to the US declined 25.2 % Y/Y. Exports to the EU grew a modest 0.9% down from +14.2% in September. Exports to ASEAN economies still rose 11.1% Y/Y, but that pace also slowed compared to September (15.8%). The data suggest that exports (mainly to economies outside the US) is receding as a driver to keep up economic growth. At the same time, the slow rise in imports hints at mediocre domestic demand. In its new five-year plan following the Central Committee’s Communist Party meeting, the government reinforced the case for private consumption to have a bigger role to support overall economic growth goring forward.

What a Time to Be Alive

Just a day after a weak but better-than-expected ADP report weakened the Federal Reserve (Fed) doves’ hand, a disquieting report from Challenger came to the rescue of bond holders — showing that US companies announced the biggest job cuts in October since 2003, thanks to the AI revolution. The news isn’t great, fundamentally speaking — human jobs are being replaced by machines, just as they were back in 2003 when the internet wave hit. But the strong job-cuts figure revived hopes of a December Fed rate cut.

The 2-year Treasury yield, which best captures Fed expectations, tanked, and the dollar headed for its biggest drop in three weeks. The probability of a December rate cut recovered to 67%. Yet falling yields and a stronger case for the next Fed cut did little to revive risk appetite. Sellers returned after Wednesday’s brief pause, pushing the S&P 500 down more than 1% and the Nasdaq 100 almost 2% lower.

And beyond yields and macro narratives, Big Tech deserved to fall yesterday on two incredible pieces of news.

First, Elon Musk had his trillion-dollar compensation package approved by 75% of Tesla shareholders. The vote comes after Musk’s strong support for Trump and several global far-right figures, a stance that quickly cost him the White House’s goodwill following the US election — and tarnished Tesla’s reputation, especially among its customer base. Tesla’s car deliveries have plunged this year, and last quarter’s brief sales jump was mostly due to a rush of demand before EV tax credits expired — credits Trump refused to extend amid their falling-out.

The good news? Musk’s record-breaking pay package only materializes if Tesla’s valuation hits $8.5 trillion — a fantastical figure for a company already trading at a P/E above 300, mostly on dreams rather than fundamentals, and facing mounting competitive and leadership pressure. In other words, Tesla would need either divine intervention — or the US dollar to turn into confetti — to make that valuation and that pay package come true.

Then came the second bizarre headline: OpenAI. The company reportedly asked the US government for guarantees on its massive infrastructure spending — an investment of more than $1 trillion. OpenAI is an incredible company, no doubt, but asking for government backing at a time when markets already fear the circularity of AI money flows, the formation of an AI bubble and uncertainty around returns — well, that didn’t sit well with investors.

So yes, this week can’t end soon enough. Nasdaq futures are somehow in the green this morning, but Asian tech indices are closing the week deep in the red. The Kospi is set for its worst week since November, the Nikkei is testing the 50,000 support as SoftBank, closely tied to AI names, dropped another 7% today. And the Hang Seng is also down over 1% — though at least it offers some diversification for tech investors: it’s not caught in the OpenAI loop.

And that’s without mentioning that the US government just broke another record — the longest shutdown in American history, as politicians fail to agree on critical issues like extending medical care programs. Imagine if they actually ended up backing OpenAI’s trillion-dollar ambitions!!

So, between the government shutdown, bizarre corporate news, stretched valuations and an underlying economy showing cracks beneath the glossy growth data, investors are understandably hesitant to take on risk. Gold wavered this week but seems to be building a floor near $4’000 per ounce. But even gold is acting oddly amid the growing absurdity of the news flow.

Oil, meanwhile, slid below $60 per barrel as US crude inventories rose by more than 5 million barrels last week — a clear signal of slowing activity. Let’s see whether the dollar’s recent weakness will help revive appetite for black gold.

Speaking of the dollar — it’s losing steam, also helped by news - or lack thereof - from abroad. Japan’s finance minister pushed back against yen shorts this week, and France, for once, didn’t announce a new shutdown. The EURUSD bounced to 1.1552, and Cable climbed past 1.31 after the Bank of England (BoE) refrained from cutting rates yesterday — though just barely. The vote was split 5-4, tilting more dovish than expected, and markets now price a 55% chance of a December cut.

Still, as tax rises loom, BoE expectations will likely soften further, assuming inflation allows. Sterling’s post-BoE rebound is surprising — but probably more about the Fed’s dovish turn than confidence in the UK outlook. Yet, sterling rallies remain interesting sell opportunities into the Autumn Budget, both against the greenback and the euro. Cable remains stuck in its June-to-remember bearish trend below 1.33, while EURGBP seems destined to test the 0.90 mark.

Cooling US Labour Market Sees October Job Cuts Reach 20-Year High

In focus today

From the US, University of Michigan's November flash consumer sentiment survey is due for release. We will keep a close eye on the inflation expectations, which have remained clearly elevated this year. Note that the US October Jobs Report, which would normally be due for release today, is delayed by the ongoing government shutdown.

In Norway, today brings the wage figures for Q3, which will be interesting after they surprised on the upside in Q2 with an increase in annual growth to 5.3% and a full 6.3% including variable payments. The wage figures released so far in Q3 indicate that wage growth slowed to around 4.8% in Q3, which would mean that the risk of sustained high wage growth becomes a little less acute.

Have a great weekend!

Economic and market news

What happened overnight

In the US, President Trump met leaders from Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan, and Uzbekistan to strengthen ties on critical minerals, energy, and trade. Agreements included mineral cooperation, Boeing sales, and Uzbekistan's USD 100bn US investment pledge, aiming to reduce reliance on Russia and China while boosting US influence in the region.

In Sweden, this morning, we already received figures from Svensk Mäklarstatistik that showed an unchanged number of transactions in October (seasonally adjusted). However, house prices rose for both villas and condominiums, well in line with expectations.

In China, exports surprised to the downside in October as it dropped into negative growth of -1.1% y/y (consensus 2.9% y/y) from 8.3% y/y in September. However, the decline may be due to the uncertainty around Trump's 100% tariff threat and extra holiday in October compared to last year. We expect exports to rebound in November as the US-China trade deal in late October led to a tariff decline of 10% to the US rather than the increase of 100%. It is also important for China, though, that the export engine keeps running as domestic demand is still struggling. So, it will be important to monitor.

What happened yesterday

In the US, the Challenger report showed further signs of a cooling labour market, with 153,074 job cuts in October - the highest for the month in over 20 years. Layoffs were largely driven by cost-cutting, AI restructuring, and overcapacity, particularly in the tech and warehousing sectors. Year-to-date hiring plans are also at their lowest since 2011. This contrasts with the stronger-than-expected ADP report earlier this week and, all else equal, supports a dovish stance for the Fed.

Also in the US, the White House announced a deal with Novo Nordisk and Eli Lilly to lower the prices of weight-loss drugs like Ozempic, Wegovy, and Zepbound. Prices will drop to USD 149-350 per month through the upcoming TrumpRx site, with Medicare co-pays capped at USD 50 starting mid-2026. In exchange, the companies gained tariff exemptions and accelerated FDA reviews for upcoming oral weight-loss pills.

In Sweden, October flash inflation figures surprised to the upside. Core inflation came in at 2.8% y/y (Danske: 2.65%, Cons.: 2.6%, RB: 2.56%) and CPIF at 3.1% (Danske: 2.95%, Cons.: 2.9%, RB: 2.66%), both exceeding the Riksbank's forecasts. Inflation details will be released on 13 November.

In Norway, Norges Bank held rates unchanged at yesterday's interim meeting, with no new policy signals and repeating the September monetary policy guidance. Markets interpreted the communication as slightly hawkish; however, we think history has shown that Norges Bank just wants to refrain from giving any news to markets at the interim meetings unless the pricing for the subsequent big meeting is off. We still expect the third 25bp cut in March 2026, followed by quarterly cuts through 2026 (June, September, December), bringing the key policy rate to 3.00% by end-26.

In the UK, the Bank of England kept the Bank Rate at 4.00% with a 5-4 vote split, showing a more dovish stance than expected. Further easing hinges on the continuance of the recent promising disinflation. We now forecast Bank rate cuts in December and April, ending the cycle at 3.50%. Read more in Bank of England Review - Dovish hold, 6 November.

In the euro area, retail sales declined 0.1% m/m in September, falling short of an expected rise of 0.2% m/m. Retail sales have thus declined in two consecutive months after a rise in the first half of the year, leaving it up 1.0% y/y. Continued low consumer confidence likely explains the weakness in spending despite solid household financials and rising real incomes. We expect consumption to gradually rise next year due to a strong labour market and real income gains, but low confidence should keep consumers quite cautious.

In Germany, industrial production rose 1.3% m/m in September (cons: 3.0%), with gains in automotive and electronics offset by weakness in mechanical engineering. This marks a rebound from August's sharp -4.3% decline led by the automotive sector, but production remains one percent lower than September last year.

Equities: US equities were sharply lower again, with S&P 500 selling off -1.1% and Nasdaq -1.9%, not far off intraday lows. Once again, this was a sell-off related to AI scepticism and not by pure macro worries - despite a surprising amount of layoff taking investors by surprise. However, looking at the sector composition, we can pinpoint weakness to AI, as AI heavy sectors like tech, consumer discretionary and communication were down 2-3%. Pure cyclicals like banks and industrials were down only -0.4% which would not have been the case if labour market fears triggered the selloff. US futures are little changed this morning.

Like earlier this week, the sell-off is spreading to the tech-heavy Asian markets, with Kospi and Nikkei down 2-3% and on track for a 5% correction so far this week. This setback is of course a challenge to our Asia overweight call (well, after months of tremendous outperformance). Our thesis was that Asian tech are the indirect winners on AI capex - so far so good - but to a much lower multiple and hence lower downside risk if and when the tide is turning. Yet so far, the Asian selloff has been more pronounced than we had expected. While Kospi is down 6% the last five trading days, S&P 500 is only down by half.

FI and FX: GBP rose vis-à-vis rest of G10, but less so vis-à-vis EUR after BoE kept rates unchanged yesterday after some speculation it would cut rates. Norges Bank also kept rates unchanged, which was widely expected. EUR/NOK rose, but that was likely on the back of the sour risk sentiment. EUR/USD also rose yesterday. A rebound seemed on the cards following the recent sell-off as the US government shutdown drags on. Bond yields dropped - most in the US - as equities fell.