Sample Category Title

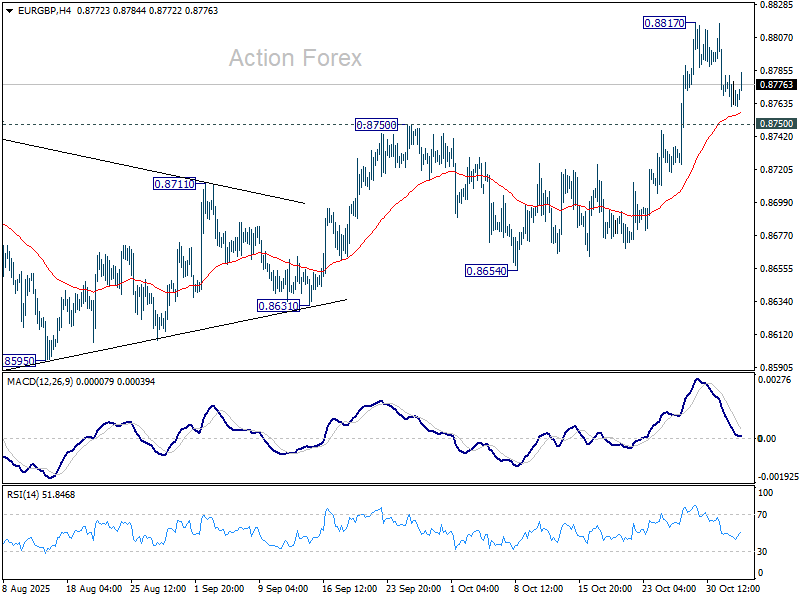

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8759; (P) 0.8771; (R1) 0.8780; More…

EUR/GBP is staying in consolidations below 0.8817 and intraday bias remains neutral. Further rally is expected as long as 0.8750 resistance turned above holds. Above 0.8817 will target 0.8867 fibonacci level. Firm break there will carry larger bullish implications. Nevertheless, sustained break of 0.8750 will turn bias back to the downside for 0.8654 support instead.

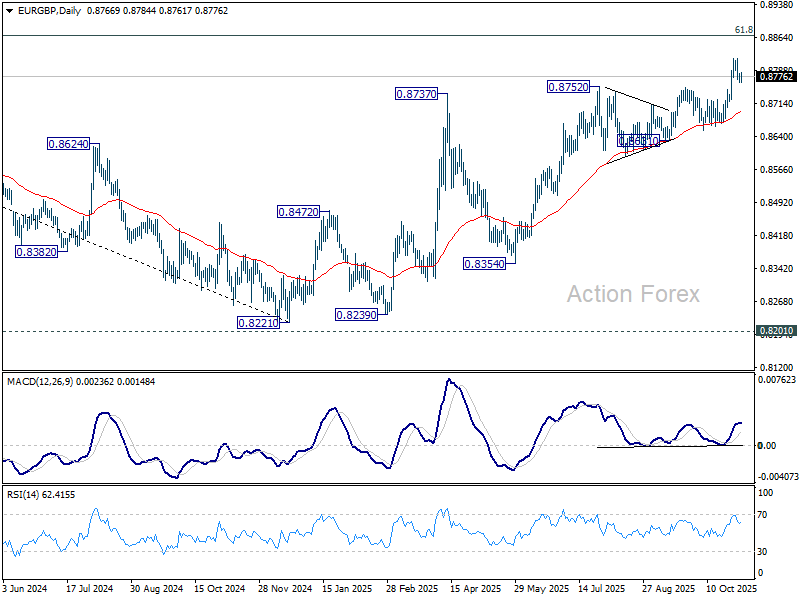

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Firm break of 0.8654 support will be the first sign that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high).

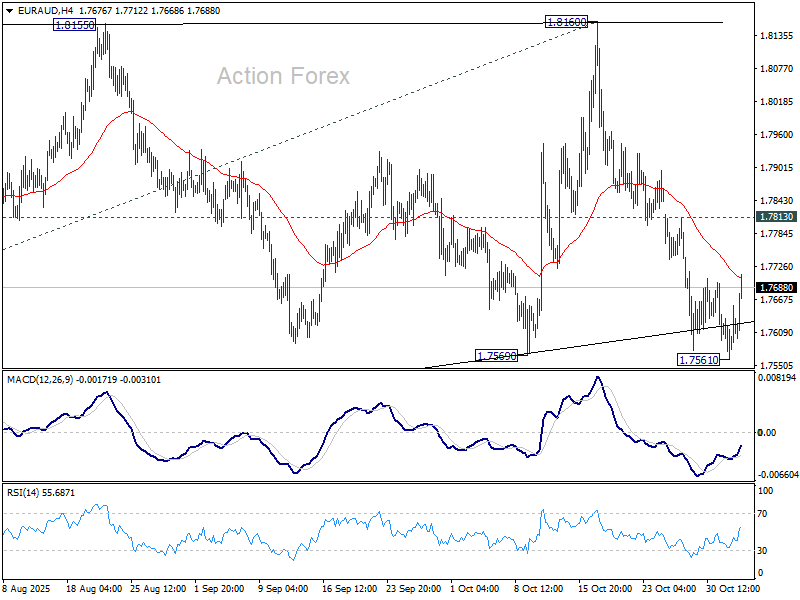

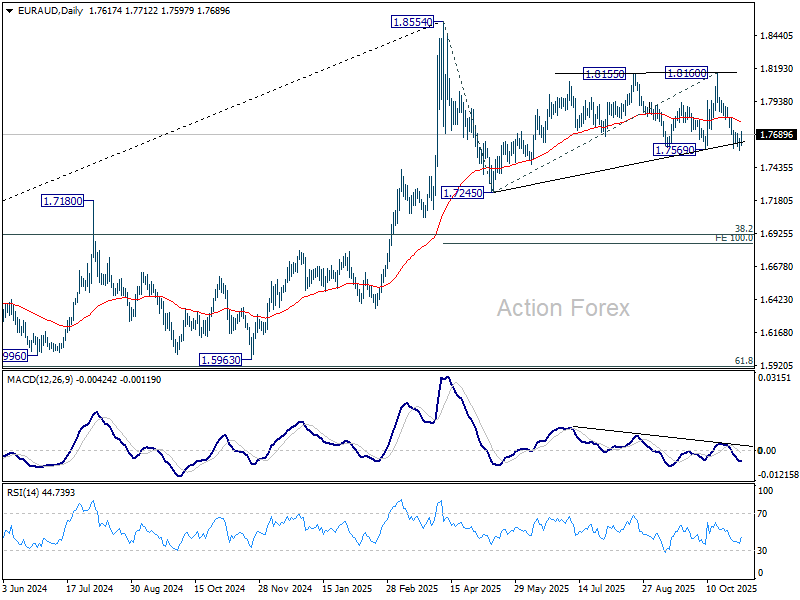

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7570; (P) 1.7614; (R1) 1.7664; More...

EUR/AUD recovered after edging lower to 1.7561 and intraday bias remains neutral. Further fall is in favor as long as 1.7813 resistance holds. Decisive break of 1.7569 support solidify the case that corrective pattern from 1.8554 is already in the third leg. Deeper fall should then be seen to 1.7254 support next.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Sustained break of 55 W EMA (now at 1.7406) will suggest that it's correcting the whole rally from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922. Nevertheless, strong rebound form 55 W EMA will likely bring resumption of the up trend sooner.

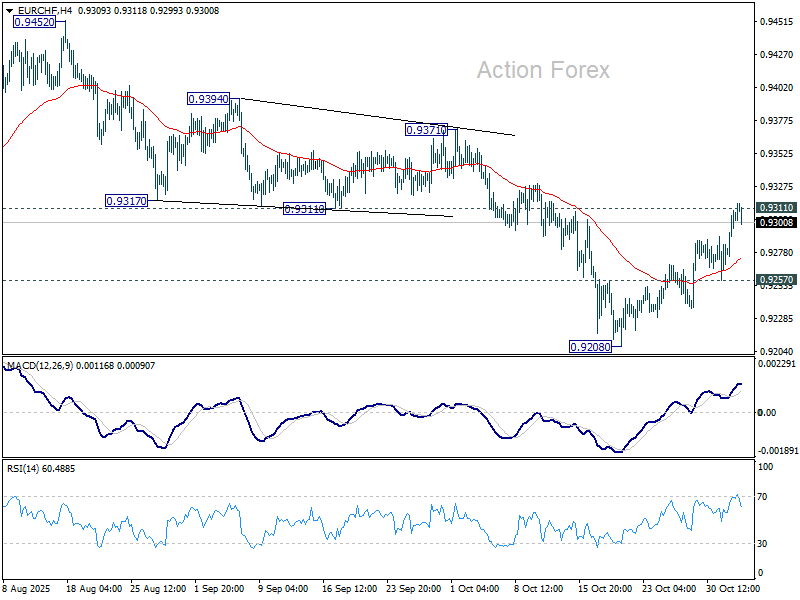

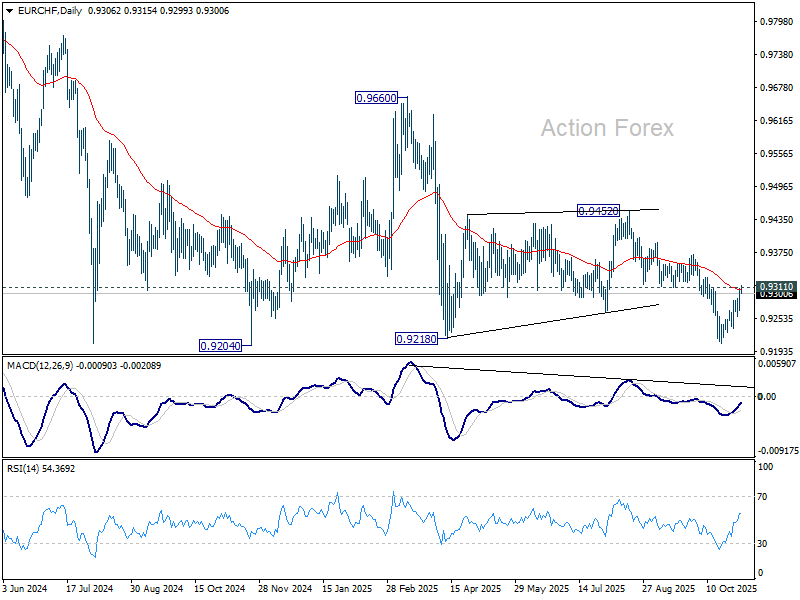

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9279; (P) 0.9295; (R1) 0.9325; More....

Intraday bias in EUR/CHF stays neutral at this point. On the upside, decisive break of 0.9311 support turned resistance and 55 D EMA (now at 0.9307) will suggest that whole fall from 0.9660 has completed as a corrective move. Further rise should then be seen to 0.9452 resistance for confirmation. On the downside, though, below 0.9257 minor support will retain near term bearishness and bring deeper fall to retest 0.9204/8 support zone. Firm break there will resume larger down trend.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9386). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming.

RBA Holds Cash Rate at 3.6%, Stuck Near Neutral

RBA holds cash rate steady at 3.6% in November, expects some of the recent rise in inflation to be temporary but partly also a signal of capacity pressures. No near-term moves likely, with a cautious Board assessing the extent of spare capacity.

- The RBA Monetary Policy Board (MPB) kept the cash rate on hold at 3.6% as expected in a unanimous vote. The September quarter inflation shock lifted the near-term inflation outlook. Some of this increase is seen as temporary, such that the RBA’s trimmed mean inflation forecast is back near the midpoint of the 2–3% target range by mid-2027. But the MPB remains cautious given recent evidence of “more persistent inflation”.

- The RBA’s post-meeting communication recognised “a recent easing” in the labour market but still regards it to be “a little tight”. The unemployment forecast was edged up but remains flat through the whole forecast period, with a risk it might rise. Other key risks related to the ongoing pick-up in private demand, and how it balances against the slowdown in growth in public demand.

- While the RBA, appropriately, expects inflation to be lower once the September quarter spike has washed through, it is cautious about the outlook and likely to remain on hold until inflation falls below the target midpoint, or the labour market eases more than it currently expects.

As was universally expected, the RBA kept the cash rate on hold following the November meeting of the Monetary Policy Board (MPB). The September quarter CPI result was well above expectations. Some of this surprise was seen as evidence of inflation being a little more persistent than expected. Underlying (trimmed mean) inflation is expected to remain elevated in the near term before returning close to the midpoint of the 2–3% target range by mid-2027. In the media conference following the meeting, the Governor characterised the MPB as having no bias and that it will be taking things meeting by meeting from here. The stance of policy was seen as “pretty close to neutral”, though the closer you are to that point, the harder it is to gauge what side of a very fuzzy line you are on.

Overall, the language was not as hawkish as it could have been. The RBA acknowledged that some of the latest inflation spike was temporary, and an increase in the cash rate was not considered. Still, with a technical assumption of one rate cut mid next year resulting in an inflation forecast that is not quite at the target midpoint, the MPB must be assumed to be on hold until something happens to change that forecast.

The RBA has concluded from the latest upside inflation surprise that there is a bit less capacity in the economy than it previously thought. As well as the inflation data, it rested this assessment on survey measures of capacity utilisation and related indicators, even as the labour market softened. We think this may assume a very fast pass-through from shifts in capacity to pricing decisions. In its annual forecast review included in the Statement on Monetary Policy (SMP), it also acknowledged an alternative explanation: that firms used the recent pick-up in domestic demand to recover earlier margin compression. This could mean that inflation remains a little elevated in the near term. Without household income growth also picking up, though, further widening in margins would result in a renewed squeeze on household spending power. That would see the recovery in private demand growth falter later on.

The RBA also provided guidance on the transition the full Monthly CPI, which begins next month. The ABS will continue to publish the quarterly Trimmed Mean for the next 18 months, using quarterly data as it currently does. To maintain historical consistency, the Bank will continue to focus on this measure of core inflation while the ABS collects the additional data required to effectively seasonally adjust all relevant monthly CPI components.

In the interim, the monthly Trimmed Mean will include components with incomplete seasonal adjustment. Some series will be smoothed to mitigate seasonal effects. As a result, the monthly Trimmed Mean will behave differently from the quarterly measure, and the three-month average of the monthly Trimmed Mean is unlikely to match the quarterly Trimmed Mean. Along with the RBA’s assessments of spare capacity, this leaves plenty of room for judgement.

The post-meeting communication characterised the labour market as still “a little tight”, despite “a recent easing”. The unemployment rate has recently picked up by more than the RBA expected , but it assesses the outlook from here as “stable” and the labour market more broadly as “healthy”. It acknowledges a risk that the labour market eases more in the near term than it currently expects. We note, however, that much of the RBA’s assessment of current labour market conditions rests on labour market indicators derived from non-public longitudinal labour market data, particularly the quit rate (a point noted in the post-meeting media conference Q&A). Indeed, most of the indicators of full employment in the RBA’s preferred suite pointed to further easing since the March quarter. The only exceptions were a small tick up in the NAB survey measure of difficulty finding suitable labour, and the two separation rates based on non-public data.

At this stage, the RBA’s capacity and growth assessments seem to leave little scope for further easing. Under the assumed path for the cash rate (about 25bps in easing) “capacity pressures are expected to remain and be slightly more pronounced over the forecast period than assessed at the time of the August forecasts. The below-trend growth and gradual easing in the labour market over the past three years has brought demand and supply in the economy closer to balance, but capacity pressures are not expected to ease much further”. There is plenty of uncertainty around this view though: “Demand is expected to be slightly above potential supply over the forecast period, given the market path for the cash rate, although that assessment is uncertain.” If things played out in line with Westpac’s somewhat lower inflation and higher unemployment forecasts, it is clear from the RBA’s communication that the MPB would not resile from adjusting monetary policy.

Observations about the forecast changes

The RBA’s forecasts on the real economy were little changed. GDP growth was marked up slightly in the near term but expected to track at or slightly below 2%yr from here (in line with the RBA’s recently revised estimate of potential output growth). An upgrade to private demand is offset by a downgrade to public demand. (Interestingly, the SMP acknowledges that this shift will boost measured productivity a bit, something we have been saying for a long while). Westpac is considerably more positive on the private demand outlook across consumption, dwelling investment and business investment.

Underlying inflation is expected to be slightly higher, staying above the 2–3% target range until the second half of 2026. The unemployment rate is forecast to increase slightly in quarterly terms, stabilising at 4.4%. Nonetheless, the Bank assesses “there will be slightly more capacity pressure in the economy than previously thought, so the outlook for inflation and wages growth have been revised a little higher”.

Relative to the RBA, Westpac expects inflation to subside more quickly with slightly more slack in the labour market and a marginally softer profile for public demand growth. That in turn gives scope for additional policy easing driving a firmer medium term growth path for demand.

One way to think about the flat inflation forecasts in recent RBA SMPs is that the labour market was seen as a little tight, imparting a tendency for inflation to drift up, which was offset by monetary policy also being a little tight. While the starting point for inflation is now higher, shifts in the labour market and the assumed policy path both imply that a downward slope is appropriate this time around. That is what the revised forecasts deliver, with trimmed mean inflation returning to be close to the midpoint of the target range during 2027.

The RBA’s August forecasts were based on an assumed path for the cash rate that involved one further cut (to 3.3%) in 2025 and two more in 2026, for a trough cash rate of 2.9%. The pricing last week that underpinned this quarter’s forecasts was significantly higher. Only one cut (to 3.3%) was priced, and not until mid 2026. The RBA assesses the current policy stance as being mildly restrictive, which implies some downward pressure on inflation. Even if that were not the case, the November forecasts should still be showing some downward pressure on inflation relative to the flat profile in the August forecasts. The RBA’s workhorse MARTIN model would suggest something of the order of at least 0.1%pt; some of the other models the RBA uses are more sensitive than this, but not by much.

Similarly, the starting point for the labour market is softer than the August forecasts assumed. While the RBA was still characterising the labour market as ‘a little tight’ based on a broader range of indicators, again, relative to the August forecasts the labour market must be creating relatively less upward inflation pressure. The size of this impetus is harder to gauge, but the flat profile in prior rounds implies that the upward pressure from the tight labour market was of a similar order of magnitude to the downward pressure from the policy stance. So count in at least another 0.1%pt off inflation late in the forecast period for this shift.

A welcome feature of the RBA’s current forecasts is that it now acknowledges that its flat participation rate forecast reflects the combination of the dampening effect of cyclical drivers offsetting a structural upward trend. Recall that some of the recent strength in the participation rate reflected the strong jobs market attracting people into (or to stay in) the labour market. On top of this, cost-of-living pressures induced people to supply more labour than normal. These two features are now unwinding, as we predicted over a year ago. At the same time, the structural upward trend from rising female (and we note, older) participation continues. This justifies a flat trend in participation for the next little while – but, we caution, not forever.

Several Fed Policymakers Showcase Broad Array of Views

Markets

Several Fed policymakers hit the wires yesterday and showcased the broad array of views that led chair Powell to push back strongly against expectations for a December rate cut. To grab a few, Goolsbee (Chicago) said the threshold for cutting then is indeed higher than last month, citing concerns over inflation in the services sector in particular. SF Fed Daly supported the October cut urged officials to keep an open mind for next month. She sees more vulnerability in consumer spending data. Governor Cook saw more risks to the labour market than inflation and said there’s reason to be concerned about an unemployment uptick. The job market can turn quickly, she added. Their comments had little direct market impact, nor did a too-close-to-expectations manufacturing ISM (48.7) for October. The latter is also the lesser important one with the services reading still coming up Wednesday. US Treasury yields added a few bps across the curve, varying between 3.1 and 4 bps in a steepening move. European rates rose similarly while Gilts marginally outperformed. The US dollar had a slight edge in FX, supported by a less ecstatic risk rally. Not all indices on Wall Street for example closed in the green and those that did finished below the opening levels. Equity futures suggest a more difficult day lies ahead. EUR/USD lost support from the October low and remains under pressure this morning. The couple tested the 1.15 big figure for the first time since August. Assuming dollar strength persists (eg. in a more fragile risk environment), there’s room for a revisit of the August low at 1.1392. DXY flirted with the 100 barrier yesterday and again this morning but a push higher is not yet materializing. JPY is holding the trade-weighted dollar back, by appreciating to USD/JPY 153.57 after a short-lived (?) adventure north of 154. Japanese PM Takaichi pledged parliament she’ll put together a new growth strategy by next summer. “We aim to strengthen Japan’s supply structure, increase incomes, improve consumer sentiment, boost corporate profits and increase tax revenues without raising taxation rates.” Long-term Japanese bonds underperform. The empty economic calendar today (no JOLTS because of the shutdown) sets the stage for technical and sentiment (currently clearly negative) driven trade. Both favour the US dollar, which is on the verge of breaking through several resistance areas in a range of currencies. Core bonds strengthen with US yields giving up some of yesterday’s gains. Bund futures suggest a yield drop at the open as well.

News & Views

The Reserve Bank of Australia (RBA) left its policy rate unchanged at 3.60%. The decision was widely expected after the recent higher than expected inflation data. RBA takes notice of Q3 trimmed mean inflation accelerating to 1% Q/Q and 3% Y/Y in the September quarter (was 2.7% in Q2), an outcome materially higher than expected. Headline inflation also increased above the 2-3% inflation target range (3.2% in Q3). Even as the RBA assesses that part of the rise in in underlying inflation is due to temporary factors, a new forecast now sees inflation rising above 3% in the coming quarters before settling at 2.6% in 2027, a scenario based on one more rate cut in 2026. On activity, the RBA indicates that the pick-up in demand continues and that the housing market strengthened further. Labour market conditions are assessed as being tight even as the unemployment rate rose from 4.3% to 4.5%. On the monetary policy stance, the RBA says that there are uncertainties regarding the assessment that monetary policy remains a little restrictive. Given recent evidence of more persistent inflation, the Board judged that it was appropriate to remain cautious, updating its view of the outlook as the data evolve. The reaction to the decision was modest. The 3-y government yield rises 3.4 bps (3.67%). Money markets still see chance of about 75% of one additional rate cut by mid-next year. The Aussie dollar is ceding modest ground this morning (AUD/USD 0.651).

Inflation in South Korea unexpectedly accelerated in October by 0.3% M/M and 2.4% Y/Y up from 2.1% and vs 2.2% expected. Underlying inflation also picked up from 2% to 2.2%. Base effects only explain a part. The acceleration was also driven by monthly price rises for clothing, transport and recreation and culture. Frood price inflation also remains rather elevated at 3.5% Y/Y. Combined with the BoK keeping a close eye at property price rises, today’s data suggest that there is little room for the BoK to ease policy further anytime soon. The BoK left its policy rate unchanged at the three previous meetings (2.5%). The next meeting is scheduled for November 27. The won continued trading in the defensive this morning (USD/KRW 1438.2).

AI Euphoria Masks a Softer Market Pulse

The new week, and the new month, kicked off on a sweet note — again on the back of a renewed AI boost. South Korean chipmakers rallied in the early hours of the new week following Nvidia’s announcement last Friday that it will sell 260,000 chips to several South Korean companies and to the South Korean government. Nvidia also gained 2% yesterday.

Then, Amazon jumped 5% to a fresh all-time high on an at least $38 billion deal with OpenAI, giving the latter access to hundreds of Nvidia chips as part of a seven-year partnership. As such, Amazon became the latest company to seal a deal with OpenAI — which has been announcing fresh partnerships with sector giants in recent weeks to secure as much computing power as it can, from wherever it can. Each announcement has offered these companies — and their investors — a moment of glory. So far, OpenAI has announced deals with, on top of Microsoft, Oracle, Google, AMD, CoreWeave, Broadcom, and now Amazon.

Meanwhile, Microsoft announced a deal with the Australian firm IREN — formerly a crypto mining company — which upgraded its data center to rent out capacity to insatiable Big Tech companies. IREN jumped more than 11% on the Nasdaq. Another one of these mining companies, Cypher Mining, also jumped 16% after announcing a $5 billion deal with Amazon.

In summary, tech stocks had a strong Monday session following these announcements, even though some skeptics continued to raise their eyebrows, concerned by the circularity of these deals.

European carmakers were another bright pocket of the market yesterday as China signaled it would ease the export ban on Nexperia chips, following tensions sparked last month by the Dutch government’s takeover of Nexperia from its Chinese owner over governance and security concerns — a move that triggered fresh diplomatic tensions between the two blocs. China’s decision to block exports of finished chips to European carmakers had disrupted key supply chains. The easing of these restrictions triggered a relief rally across European carmakers, pushing Volkswagen up around 2.3%. Renault, Mercedes, and Stellantis also gained.

Gains in Europe were also on the menu for Rheinmetall, ASML, and the big banks — making the move quite broad-based. That was not the case in the US, where a set of weak ISM data prevented the S&P 500 from extending gains beyond tech. In fact, 300 companies in the S&P 500 fell yesterday, and the S&P 500 equal-weight index closed 0.24% lower on worries that US economic activity may be weakening — without a clear guarantee that the Federal Reserve (Fed) will cut rates again in December.

Indeed, the probability of another 25 bp Fed cut in December has now eased to 65% from above 90% last week, and Chicago Fed’s Austan Goolsbee rubbed salt in the wound by saying he’s more concerned about inflation than jobs right now. Even though other Fed members sounded more dovish, the US 2-year yield — which reflects Fed rate expectations — rose yesterday, hinting that the doves lost further ground despite soft data and the US shutdown, which should further weigh on US growth expectations.

Higher yields helped the US dollar extend gains against major peers — exactly the opposite of what was expected during a government shutdown. And this shutdown is not a short one; on the contrary, it’s on track to become the longest in US history.

But here we are. Major US indices are holding their ground, even though tech continues to do the heavy lifting — and bubble and circularity concerns keep bubbling. Yields are higher than last week but still near their lowest levels since the April dip, and the US dollar is recovering. Market volatility remains contained, and earnings are coming in better than expected.

Meanwhile, Big Tech bond issuance is drawing exceptionally strong demand on both sides of the Atlantic — we’re talking five to ten times oversubscription for names like Oracle, Google, and Meta — as investors look for AI exposure through a different, and arguably less risky, instrument.

So what could go wrong? Many analysts bet that the rally in major global indices will continue on the back of insatiable AI appetite, robust earnings and easing trade tensions. Plus, November and December tend to be good months for stock investors. If all goes well, the year could end without another April-like sharp selloff across global financial markets.

But it’s worth remembering that the buzzy AI headlines continue to mask a deteriorating reality: if you take tech out, the rest is not necessarily sweet. Even within tech, valuations are extremely high, and the urge to see ROI is growing.

Bank of America, for example, predicts that AI capex will reach 94% of operating cash flow in 2026, up from 76% in 2024 — a reason why these companies are now issuing debt. High valuations combined with falling cash flow mean that investors will grow pickier about returns — and the latest market reactions offer a warning: Palantir became the third major tech company — after Microsoft and Meta — to fall despite announcing record, better-than-expected results.

And if tech sneezes, global financial markets — starting with the US — will catch a cold.

On the macro front, despite the lack of fresh official data, private indicators suggest a slowing economy and a weakening labour market. US layoffs have already reached their highest level since 2020. Inflationary risks persist due to tariffs, the geopolitical and trade setup remains unstable, and developed-market politics — and budget discussions — aren’t looking good either.

Today, major US and European indices are in the red. But there are no particularly worrying signs of stress. We continue to watch earnings: AMD, Shopify and Uber are among companies that could impact sentiment.

FX Reserves Unlikely to Show Intervention in EUR/DKK

In focus today

Today is expected to be a quiet day in terms of tier 1 data.

In Denmark, Nationalbanken will publish its press release on October's FX reserve, revealing whether it intervened in the FX market last month. While EUR/DKK has reached its highest level in three years, it remains below the threshold that triggered intervention in 2020. Hence, we do not expect Nationalbanken intervened in October. Nevertheless, we will monitor the release today for confirmation.

Economic and market news

What happened overnight

In Australia, the Reserve Bank of Australia kept its policy rate unchanged at 3.60%. The decision was widely expected following higher-than-expected Q3 inflation figures on 29 October. Annual inflation growth rose back above the RBA's target range, prompting the central bank to emphasise the need for caution and a data-driven approach to its economic outlook.

What happened yesterday

In the US, the ISM Manufacturing Activity Index for October came in at 48.7, below the consensus of 49.6 (prior: 49.1). While the headline figure was weaker, the details were more positive. The new orders index recovered, while inventories declined, leading to the order-inventory balance turning increasingly positive. This tends to be a positive sign for production growth over coming months. At the same time, the prices index fell, suggesting tariff-driven inflation pressures remain subdued. Imports stayed low, continuing the trend from previous months.

Several Fed officials were on the wire on Monday, highlighting divisions ahead of December's meeting. Cook called the meeting 'live' but not a lock for a rate cut, Goolsbee flagged inflation concerns, Miran reiterated his view that policy remains too restrictive, and Daly expressed an open mind about a December rate cut. Markets currently price a 60% chance of a cut next month.

In the euro area, the final manufacturing PMI for October confirmed the flash release of 50.0, indicating the sector has exited contractionary territory. France was revised up to 48.8, while Germany's release confirmed the flash estimate of 49.6. Combined with services PMIs reaching a one-year high, the euro area saw a positive start to Q4. This supports our view that the ECB will not deliver more rate cuts this year or in 2026.

In Sweden, the October Manufacturing PMI decreased slightly to 55.1, largely driven by declines in employment, new orders and inventories, while production improved. This follows last month's strong reading of 55.6 and indicates continued growth in manufacturing activity, albeit at a slightly slower pace.

In the US-China tech landscape, President Trump announced that Nvidia's most advanced Blackwell AI chips will be exclusive to American companies, barring exports to China and others. Meanwhile, the Financial Times reported this morning that China has ramped up subsidies to reduce energy costs for major data centres by up to 50%, supporting domestic tech giants as they face higher electricity costs from the Nvidia chip ban.

Equities: Equity markets saw a rather uneventful session, with both Europe and the US ending little changed. Key macro data offered limited direction, leaving equities broadly flat. Instead, AI-related headlines dominated, with Amazon rising 4% after announcing a major partnership with OpenAI. This marks one of several recent deals OpenAI has struck to support its ambitious data centre capex plans. Another trend in equity markets has been a pick-up in M&A over the past months. Yesterday, it was Kimberly-Clark's turn to announce a sizable acquisition. Increased M&A activity should support our preference for small caps, as they are more likely to be the 'buying candidates'.

FI and FX: It was a relatively quiet day in the global markets on Monday. On the FX market Scandies and the USD saw marginal gains vis-à-vis the EUR and JPY. EUR/USD traded close to the 1.1500 mark yesterday, while EUR/SEK fell below 10.95 and EUR/NOK dropped close to 11.65 again. Bond yields rose 2-3bp across the curve both in Europe and the US.

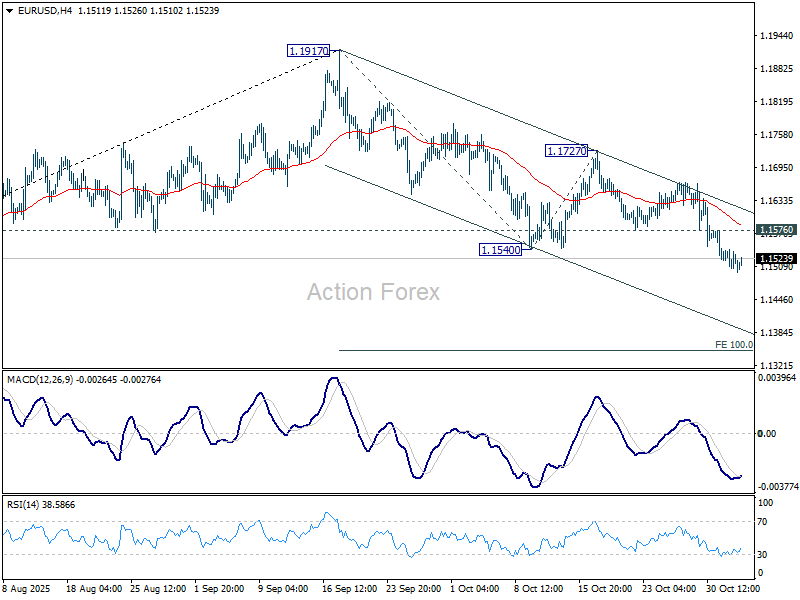

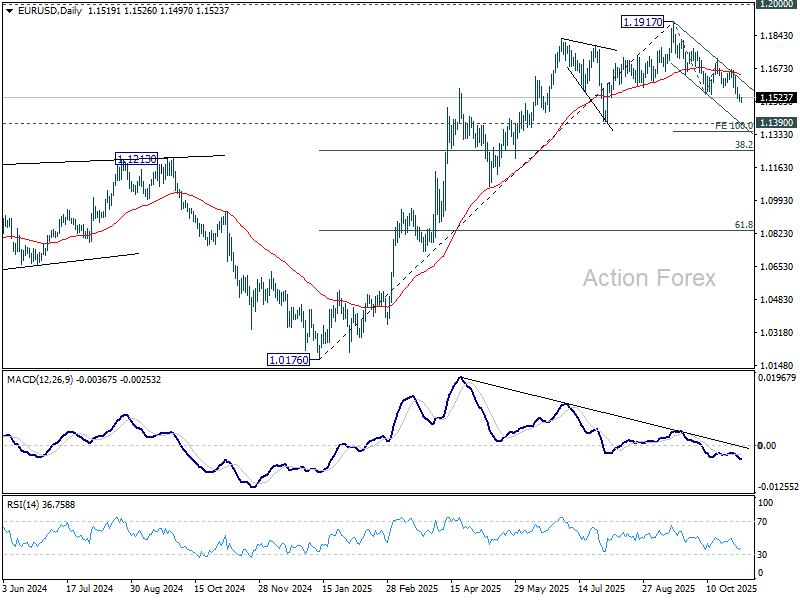

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1503; (P) 1.1522; (R1) 1.1539; More…

Intraday bias in EUR/USD stays mildly on the downside for the moment. Fall from 1.1917 should target 100% projection of 1.1917 to 1.1540 from 1.1727 at 1.1350. Decisive break there would prompt downside acceleration to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1576 minor resistance will turn bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1306) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

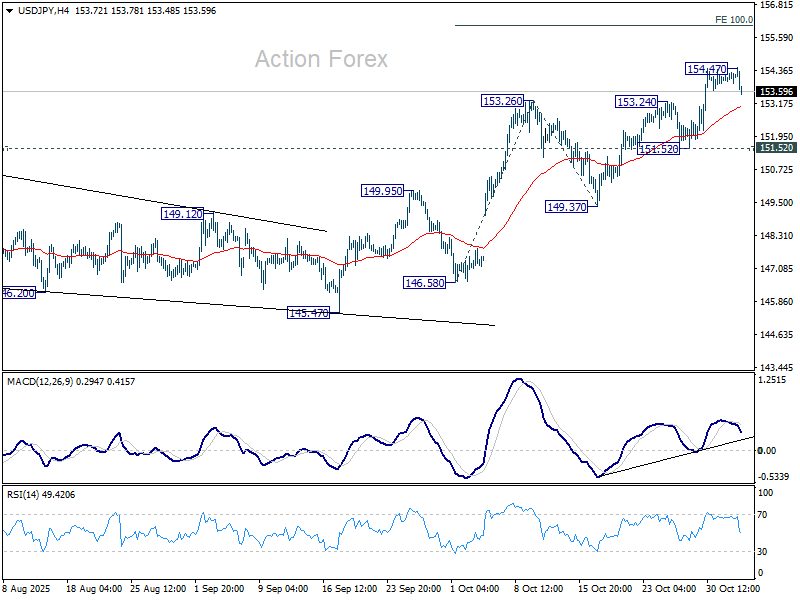

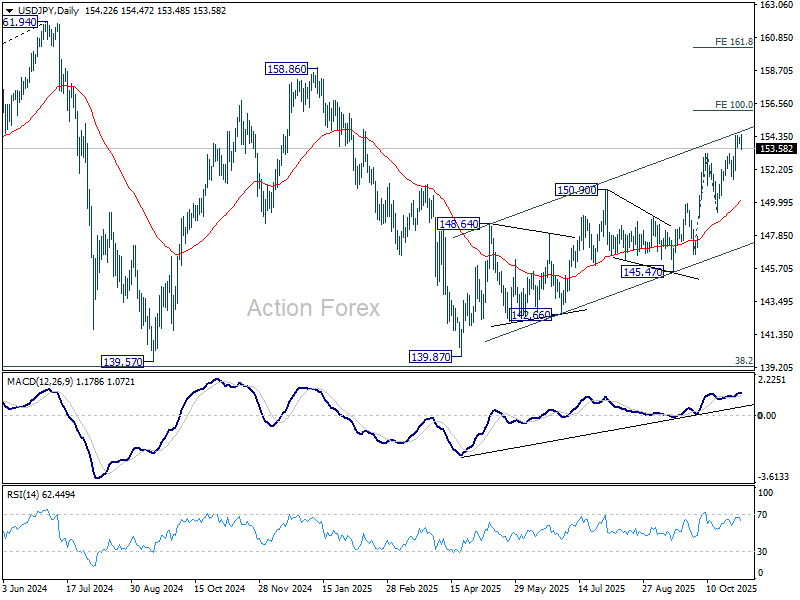

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.99; (P) 154.14; (R1) 154.38; More...

Intraday bias in USD/JPY is turned neutral with current retreat, and some consolidations would be seen below 154.47 temporary top. Further rally is expected as long as 151.52 support holds. Above 154.47 will resume larger rise from 139.87 to 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

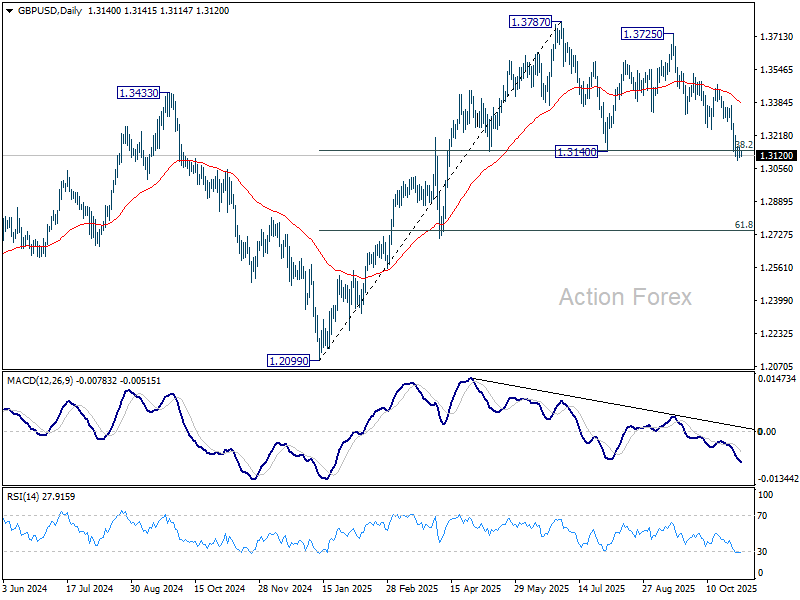

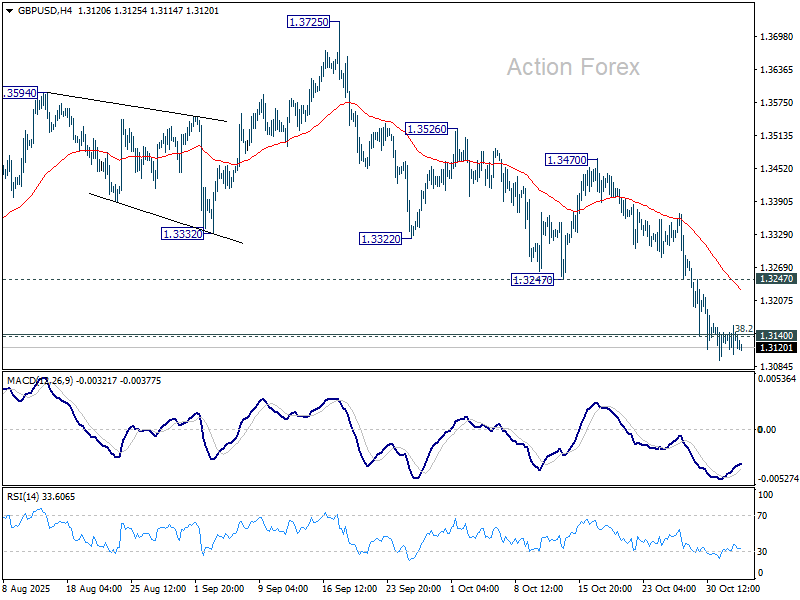

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3111; (P) 1.3137; (R1) 1.3164; More...

Further decline is expected in GBP/USD as long as 1.3247 support turned resistance holds. Sustained trading below 1.3140 support should confirm completion of double top pattern (1.3787, 1.3725). Further decline should then be seen to 61.8% retracement of 1.2099 to 1.3787 at 1.2744 next.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Sustained trading below 55 W EMA (now at 1.3185) will argue that a medium term top has already formed and bring deeper fall back to 1.2099. Firm break there will confirm bearish reversal. In case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside.