Sample Category Title

GBP/USD Price Forecast: Cable Plummets to Fresh Seven-Month Lows Ahead of BoE Decision

Trading at 1.30244, a level last seen in early April, GBP/USD has fallen 0.87% in today’s session alone.

Continuing a period of bearish momentum, cable is now on pace for its worst two-weekly performance since November 2024, with four days to spare until the candle closes.

Recently breaking through previously held support and the 200-day SMA, one has to ask:

What’s next for GBP/USD?

GBP/USD: Key takeaways 30/10/2025

- With today’s session signifying the worst GBP/USD performance in over 140 calendar days, price action has convincingly broken previously held support at 1.31403, and the 200-day SMA at 1.31011

- Writing ahead of the Bank of England’s Thursday decision, Governor Andrew Bailey is in a difficult position, faced with rising inflation, which would support higher rates, alongside rising unemployment and weak economic growth, which would support lower rates

- Otherwise, and with the dust beginning to settle on last week’s Federal Reserve rate decision, a hawkish tone from Powell to suggest a shallower easing cycle has added a significant tailwind to falling cable pricing

GBP/USD: All eyes on sterling

It would only make sense that, considering monetary policy matters scheduled for later this week, much of the market has the pound sterling in its focus.

It is fair to say, however, that this newfound focus comes at an inopportune time for GBP/USD, between warnings of “hard choices” in the upcoming Autumn budget by Chancellor Rachel Reeves, and a central bank stuck between a rock and a hard place in their upcoming decision.

As a a result, GBP currently underperforms its currency peers by some margin.

"It is my job to deal with the world as we find it, not the world that I might wish it to be"

Rachel Reeves, Chancellor of the Exchequer, speaking at Number 10 Downing Street, 04/11/2025

GBP/USD: Fundamental Analysis 04/11/2025

Fiscal health of UK remains in question: At risk of repeating myself from previous coverage, questions around sovereign debt and government borrowing costs continue to reign supreme in GBP/USD markets.

Speaking today at Number 10 in a rare pre-budget speech, Rachel Reeves addressed speculation about her upcoming Autumn budget, tasked with plugging an estimated £22bn hole in public finances, compounded by falling UK productivity.

Rachel Reeves fails to rule out breaking manifesto pledges on tax in major speech

Blaming previous governments, Reeves crucially did not rule out rises to income tax, national insurance, or VAT, despite campaign pledges not to raise taxes on working people

Tying this back to GBP/USD, the current narrative surrounding sovereign debt in the UK is weighing harshly on sterling, and despite somewhat questionable government spending in the US, markets are voting with their feet and selling the British pound in favour of other, seemingly more stable stores of wealth.

Increased rate cut bets ahead of BoE meeting: To be clear, the majority of markets still predict that the Bank of England will vote to maintain rates at 4.00% in its decision later this week.

Although when considering October’s CPI numbers reported inflation unchanged MoM at 3.8%, and that unemployment and GDP data still leaves much to be desired, it would be wrong not to acknowledge a school of thought to cut rates by 25 basis points.

In the unlikely event that the Bank of England does choose to cut, however, we can expect this to weigh heavily on sterling pricing in two ways:

- In a vacuum, lower interest rates are currency negative

- Within the context that a cut would surprise markets, and considering current sovereign debt, jobs market, and GDP data, the cut would likely be seen as an emergency response by the BoE, hurting investor confidence

Although it is a firmly minority view, it would be fair to say that rate cut bets are increasing somewhat ahead of Thursday, which is adding to the cable downside.

Bringing this discussion back to earth, inflation remains almost twice the target in the UK, at 3.8%, which would make rate cuts hard to justify unless Governor Bailey can reasonably suggest that current inflation is in some way temporary and will resolve itself.

GBP/USD: Technical Analysis 04/11/2025

GBP/USD: Daily (D1) chart analysis:

GBP/USD, D1, OANDA, TradingView, 04/11/2025

I’m pleased to say both price targets set in my previous commentary have been met, with GBP/USD sliding lower as predicted.

Failing to find support at the 200-day SMA or the triple bottom-lows as highlighted, bearish momentum continued, and for now, looks set to continue.

Price targets and support/resistance levels:

- Price target/Resistance #1 - $1.30000 - Key psychological level

- Price target/Resistance #2 - $1.28847 - Lower boundary of previous range

While it seems remiss to suggest any evidence of GBP bulls after today, price action may stage some kind of recovery at each price target/area of resistance, especially considering the 14-day RSI rates current price action as ‘oversold’ for the first time since January.

Gold (XAU/USD) Price Slips 1.5% as $4000/oz Handle Remains Elusive. What Comes Next?

Gold prices saw a sharp decline in the US session today with the precious metal down around 1.5%. Gold tested the $4000/oz in the European session but failed to break higher as the rally ran out of steam.

The current resurgence in the US dollar which accelerated following a hawkish recalibration of market expectations regarding the Federal Reserve’s (Fed) monetary policy has played a big part in the precious metals struggles.

Fundamental Catalysts: The Fed Repricing Shock and USD Strength

After last week's Fed meeting, officials made it clear they are less likely to cut rates soon. The market's confidence in a rate cut this December quickly fell from 94% to about 70%.

This expectation of higher-for-longer interest rates makes it more expensive to hold gold, which doesn't pay interest, compared to holding the interest-earning US dollar, pushing the gold price (XAU/USD) down. Key Fed leaders have also confirmed this view; some said inflation is still too high and they're ready to raise rates if needed, while another expressed concern about cutting too soon.

These signals strengthen the US dollar, which is hurting gold. If the US Dollar Index (DXY) keeps rising strongly above the 100 mark, it would be a major sign that dollar strength is here to stay, likely causing precious metals prices to drop significantly.

Adding a small, secondary pressure, a new tax policy in China that removes some exemptions on gold purchases is expected to temporarily reduce how much gold Chinese consumers buy.

US Government Shutdown Continues

The recent Fed rhetoric suggests a greater dependency on data moving forward. This is of course inconvenient given the ongoing US government shutdown which is disrupting the normal release of economic reports, which means we have less information than usual.

Because of this limited data, the few reports that do come out, especially tomorrow's job report from ADP, will likely have a much bigger impact on the markets than they normally would. The overall lack of data may also lead to periods where currency trading lacks a clear direction.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Technical Analysis - Gold (XAU/USD)

From a technical standpoint, Gold needs a four-hour candle close below the 3924 handle for a new lower low to be printed.

The current highest-probability trend is a continued decline toward the 3782 to 3797 target range, contingent upon Gold remaining beneath the 4000 psychological level.

For the bullish bias to be revived in the near term, XAU/USD must achieve a four-hour candle close above the 4000 psychological level and the 50-day MA at around the 4012 handle.

Until such a reversal is confirmed, pressure will persist. It is important to note that while the intermediate trend is negative, the long-term uptrend remains underpinned by the 50-day and 100-day MA on the daily timeframe, which rests at 3844 and 3595 respectively.

Gold (XAU/USD) Four-Hour Chart, November 4, 2025

Source: TradingView (click to enlarge)

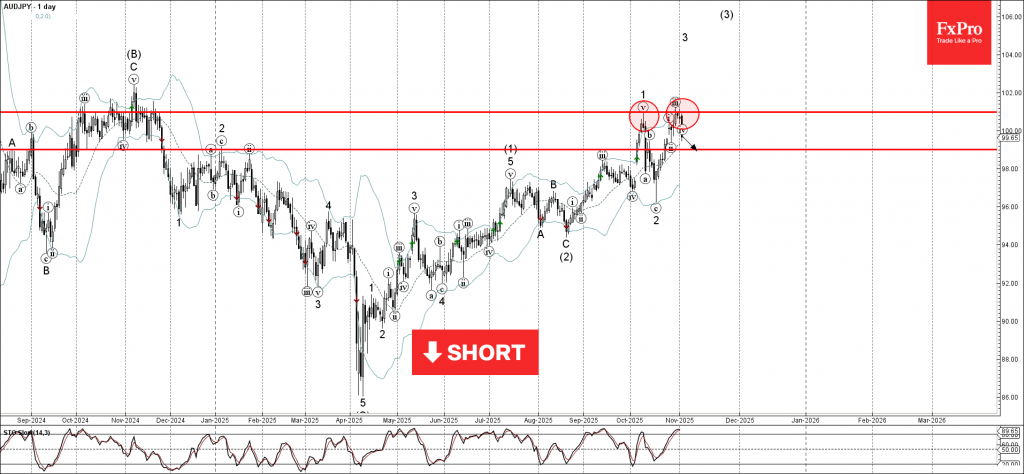

AUDJPY Wave Analysis

AUDJPY: ⬇️ Sell

- AUDJPY reversed from key resistance level 101.00

- Likely to fall to support level 99.00

AUDJPY currency pair recently reversed from the resistance zone between the key resistance level 101.00 (which stopped the previous minor impulse wave 1 at the start of October) and the upper daily Bollinger Band.

The downward reversal from this resistance area created the daily Japanese candlesticks reversal pattern Evening Star Doji – which stopped the previous impulse waves 3 and (3).

Given the strength of the resistance level 101.00 and the overbought daily Stochastic indicator, AUDJPY currency pair can be expected to fall to the next support level 99.00.

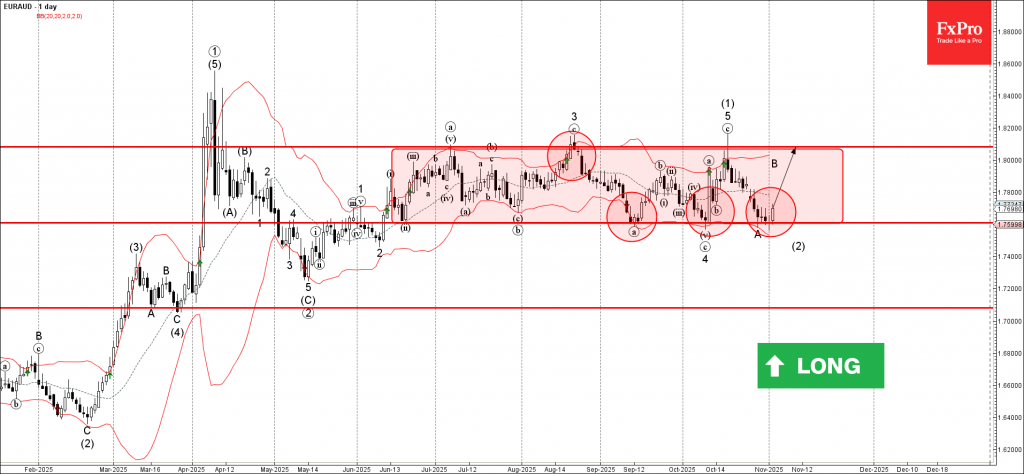

EURAUD Wave Analysis

EURAUD: ⬆️ Buy

- EURAUD reversed from support level 1.7600

- Likely to rise to resistance level 1.8085

EURAUD currency pair recently reversed from the support zone between the support level 1.7600 (lower border of the narrow sideways price range inside which the pair has been trading from June) and the lower daily Bollinger Band.

The upward reversal from this support area stopped the previous short-term impulse wave A.

Given the strength of the support level 1.7600 and the bullish euro sentiment seen today across the FX markets, EURAUD currency pair can be expected to rise to the next resistance level 1.8085 (upper border of the active sideways price range).

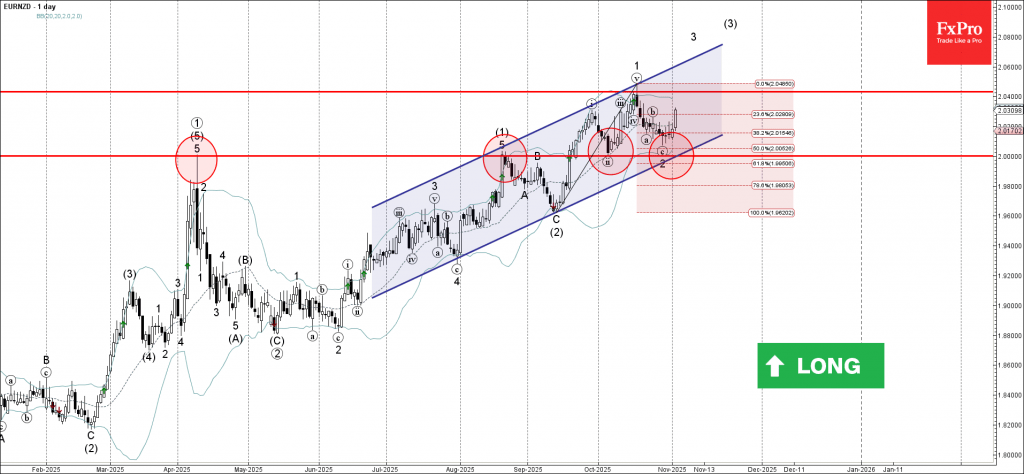

EURNZD Wave Analysis

EURNZD: ⬆️ Buy

- EURNZD reversed from support area

- Likely to rise to resistance level 2.0430

EURNZD currency pair recently reversed from the support area between the key support level 2.0000, support trendline of the daily up channel from June and the lower daily Bollinger Band.

The upward reversal from this support area stopped the previous short-term ABC correction 2.

Given the predominant daily uptrend, EURNZD currency pair can be expected to rise to the next resistance level 2.0430, which stopped the previous minor impulse wave 1 in the middle of October.

Sunset Market Commentary

Markets

Risk sentiment turned sour today, both in Europe and in the US. Signs of fatigue were showing up in recent days. Many stock indices hovered sideways near the record highs with higher openings often used as a moment to take some chips off the table. It were Palantir’s earnings released after-market yesterday that ignited today’s broader profit-taking. Q3 results topped analyst estimates and the company even raised its annual revenue outlook. But it received a thumbs down by the market nevertheless, instantly prompting more general valuation concerns. The tech/AI sector proves particularly vulnerable with the likes of Nvidia, Tesla, Amazon, Meta Platforms and AMD all losing ground. Tech index Nasdaq slides 1.6% at the opening bell, the S&P500 is down 1.2%. Europe’s EuroStoxx50 loses around 1% but is off the intraday lows. Risk aversion filters through into bond markets as well, supporting US Treasuries and German bunds. US rates ease 1.4-3 bps in a bull steepening move. Bund yields limit losses to less then 2 bps, the belly outperforming the wings. Gilt yields decline around 2.1-2.7 bps across the curve. UK chancellor Reeves held a pre-budget speech that got picked up by the national broadcasters. It’s very unusual for a chancellor to lift the veil somewhat and doing so suggests she wanted to massage the public into swallowing the bitter pill the November 26 budget is going to be. Reeves reaffirmed her commitment to the fiscal rules so to have the balances check out, the only options remain spending cuts and/or tax hikes. The latter have long been categorically ruled out in politically sensitive areas such as income taxes which create the bulk of the government receipts. PM Starmer was the first not to do so any longer last week and Reeves followed suit today, refusing to reiterate the party’s manifesto commitment against broad-based tax hikes. She noted instead that the world had changed since Labour came to Power in July last year, citing bigger obligations to adhere to (eg. NATO). Sterling braces for economic impact: EUR/GBP is doing another attempt to take out 0.88, GBP/USD slides to 1.304, the weakest level since mid-April. Safe haven flows push the greenback higher against most other peers as well. EUR/USD (1.1479) snapped below the 1.15 barrier and looks at 1.1392 for support. DXY finally punched through 100 and is less than in inch away from the August high (100.25). A test is all but certain. The only currency besting the USD is JPY. The Japanese yen strengthens from north of USD/JPY 154 to 153.47 currently. EUR/JPY tanks to a two-week low of 176.17.

News & Views

ECB’s Lagarde today in Sofia delivered a speech titled ‘Bulgaria on the euro’s doorstep: towards a shared future’. In this speech, the ECB Chair painted the context as the country will officially adopt the euro on January 2026. Lagarde advocated that joining the euro will offer additional prosperity and security to for the country. Aside from lower conversion costs, adopting the euro will also open the door wider to European capital markets. It will lower funding costs and provide a more stable basis for long-term investment. Regarding financial security, Lagarde acknowledged that the currency board has long insulated Bulgaria by eliminating euro-lev fluctuations. Even so, joining the broader currency area still provides a higher credibility. Lagarde also addressed sceptics in the country as surveys suggest about half of the population might oppose joining the euro. With respect to the fear of losing sovereignty, Lagarde indicates contrary to what is the case in the currency board regime where the country is only ‘importing’ monetary policy, the Governor of the Bulgarian national bank now will have the same vote and responsibility as every other member. Lagarde also acknowledged the concern that the change of currency might lead to higher prices but indicated a series of mechanisms to address this issue. However, she indicated that ‘the greatest risk countries faced was not losing sovereignty or seeing an increase in prices. It was losing reform momentum once inside the euro area and thus missing out on the full benefits of the single currency’.

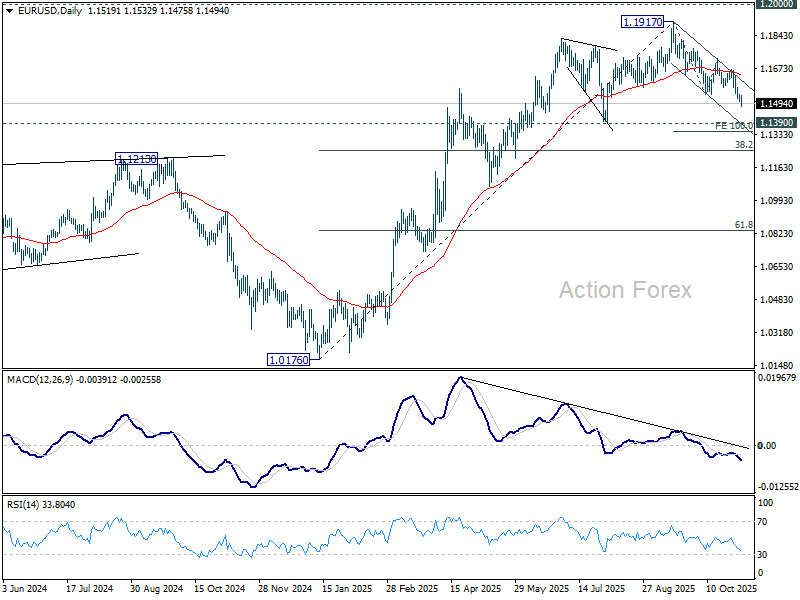

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1503; (P) 1.1522; (R1) 1.1539; More…

EUR/USD's fall from 1.1917 is in progress. Intraday bias stays on the downside for 100% projection of 1.1917 to 1.1540 from 1.1727 at 1.1350. Decisive break there would prompt downside acceleration to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1540 minor resistance will turn bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1306) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

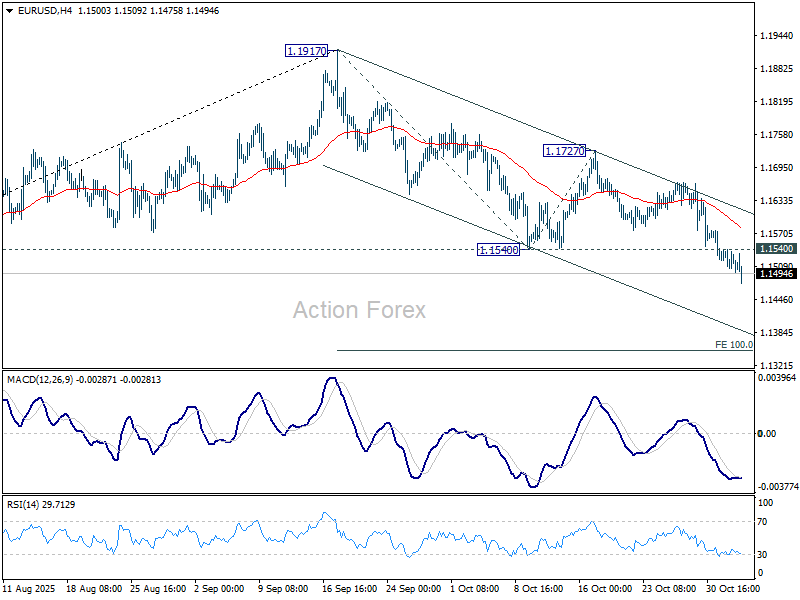

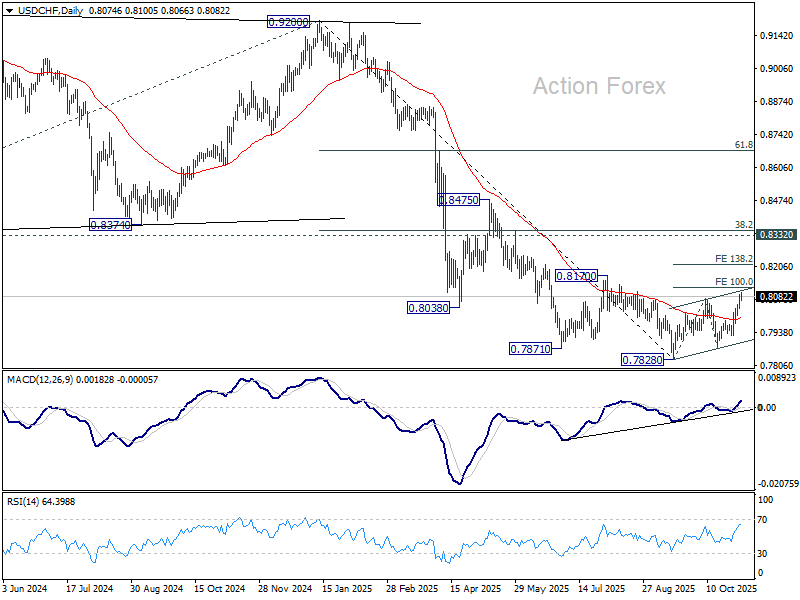

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8045; (P) 0.8069; (R1) 0.8104; More…

USD/CHF's rally is still in progress and intraday bias stays on the upside for 100% projection of 0.7828 to 0.8075 from 0.7872 at 0.8119. Break there will extend the corrective rally from 0.7828 to 138.2% projections at 0.8213. On the downside, below 0.8037 minor support will turn intraday bias neutral.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

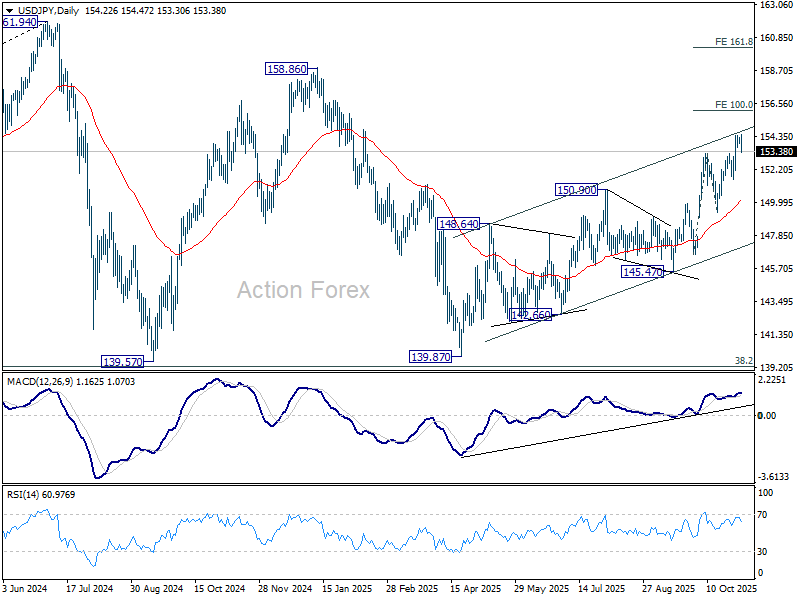

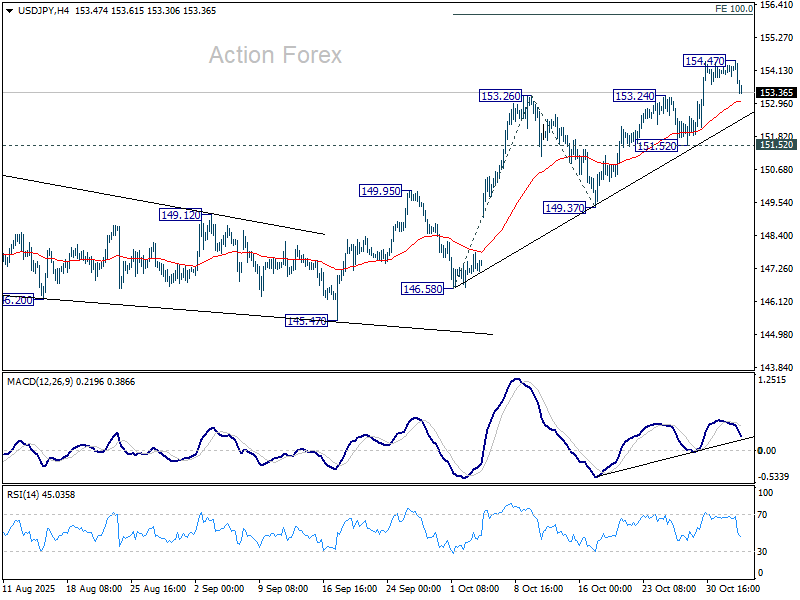

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.99; (P) 154.14; (R1) 154.38; More...

Intraday bias in USD/JPY remains neutral for consolidations below 154.47 temporary top. Further rally is expected as long as 151.52 support holds. Above 154.47 will resume larger rise from 139.87 to 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.