Sample Category Title

Sunset Market Commentary

Markets

Some last-minute economic data including stronger-than-expected Q3 GDP and national inflation numbers (see below) ahead of the ECB policy meeting highlighted the logic of the outcome. The deposit rate was kept unchanged at 2% today. That unanimously decided status quo was based on the fact that inflation, including underlying gauges, remains close to the 2% medium-term target and developed in line with the September outlook. There was no risk balance offered. But based on the opposing arguments, including a return of supply chain bottlenecks (hello, 2020), spelled out, we assume the risks are considered being balanced. A robust labour market and earlier monetary easing amongst others keeps the economy growing against the backdrop of a challenging global environment. The ECB chair, citing today’s GDP release, added she wouldn’t worry too much about growth at this point in time. Some of the downside risks mitigated, she said, following the trade deal sealed with the US, the ceasefire in the middle east and the progress in China-US relations announced this morning. That assessment comes after Lagarde in September said risks to the economy “become more balanced”. ECB Lagarde singled out (digital) services a key engine for growth. Manufacturing was instead held back by higher tariffs and a stronger euro, denting external demand. The ECB expects this divergence with solid internal demand to persist. As usual, Lagarde kept the cards close to her chest in terms of what to expect from policy going forward. The ECB remains in a good place but it’s not a fixed good place. Decisions will be made on meeting-by-meeting basis and take into account incoming economic and financial data. Given that neither the risks to nor the outlook of inflation had changed and with the ECB becoming less negative on growth risks, a 2% deposit rate for the months ahead remains our base scenario. If anything, the bar for rate cuts after today shifted higher. The money market implied probability barely changed and remains well below 50%. European swap yields retain most of the earlier rise with net daily changes varying between +1 bp and +2 bps. Treasury yields stabilize after the Fed-driven 10 bps jump yesterday. The euro loses some ground against the dollar in a move more inspired by the risk-off mood than anything else. EUR/USD eases to below 1.16 but in technically irrelevant trading. A disappointing JPY in the wake of the Bank of Japan’s unchanged rates decision this morning underperforms global peers. USD/JPY surges to a 9-month high north of 154. Stock markets slip to around 1% in the US (Nasdaq) with investors taking some chips off the table after the 5-day 5% rally.

News & Views

Belgian inflation rose by 0.36% M/M in October after two monthly declines in August and September. The most significant price increases in October were registered for holiday villages, clothing, private rents, participation in recreational sporting services, plane tickets, restaurants and cafés and personal care. Hotel rooms, natural gas, electricity and package holidays had a downward effect. Annual inflation slowed from 2.1% Y/Y to 2% and is actually hovering sideways between 1.9% and 2.1% since May. Core inflation was unchanged at 2.6% Y/Y. Services inflation increased from 3.5% to 3.6% while rent inflation was unchanged at 4%. Food inflation slowed from 3.3% to 2.7% and energy dropped by 1.9% Y/Y from -1.5% Y/Y in September. Other European countries reporting inflation data today were Spain and Germany. Spanish inflation showed an unexpected acceleration in harmonized CPI from 0.2% M/M to 0.5% M/M (3.2% Y/Y from 3%; core 2.5% from 2.4%). German inflation also rose more than expected (0.3% M/M & 2.3% Y/Y) suggesting upside risks to tomorrow’s EMU print. Consensus expects 0.2% M/M and 2.1% Y/Y.

Czech GDP grew by 0.7% Q/Q in Q3 according to the preliminary estimate with year-on-year growth of 2.7% being mainly driven by final consumption expenditure of households and gross capital formation. External demand also helped quarterly growth. Both significantly beat consensus (0.3% Q/Q & 2.3% Y/Y). Full details will only be released by the end of the month (Nov 28). The Hungarian statistical office also published a first indication for Q3 growth. It disappointed with no-growth on a quarterly basis and GDP rising by 0.6% Y/Y.

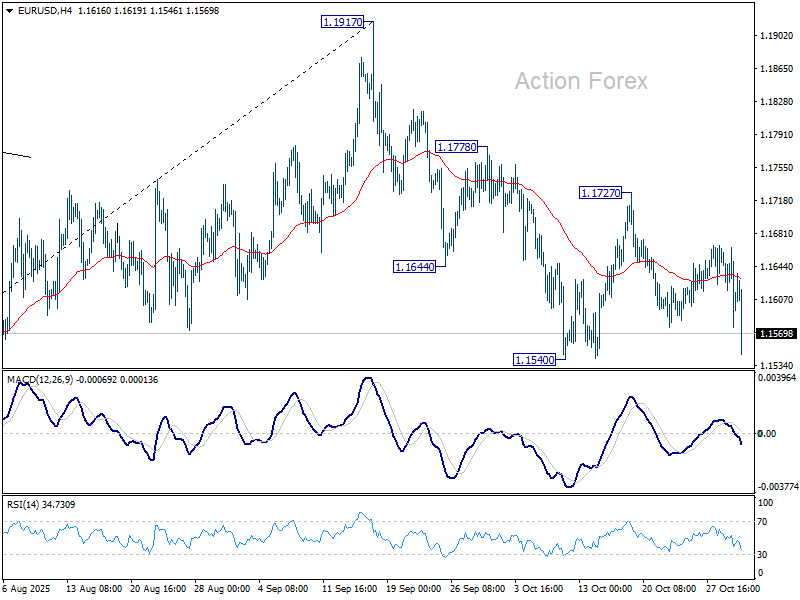

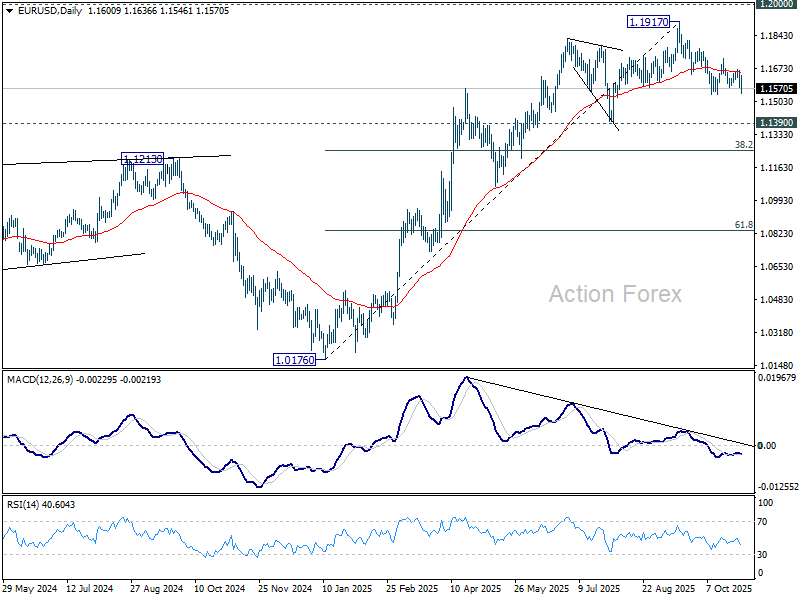

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1564; (P) 1.1615; (R1) 1.1652; More…

Focus is now on 1.1540 support as EUR/USD's decline continues today. Firm break there will resume the fall from 1.1917 and target 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1301) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

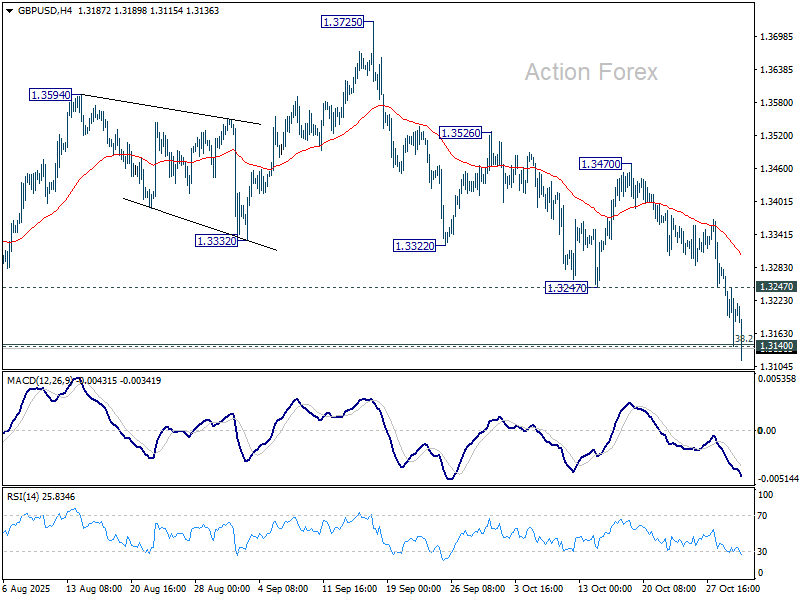

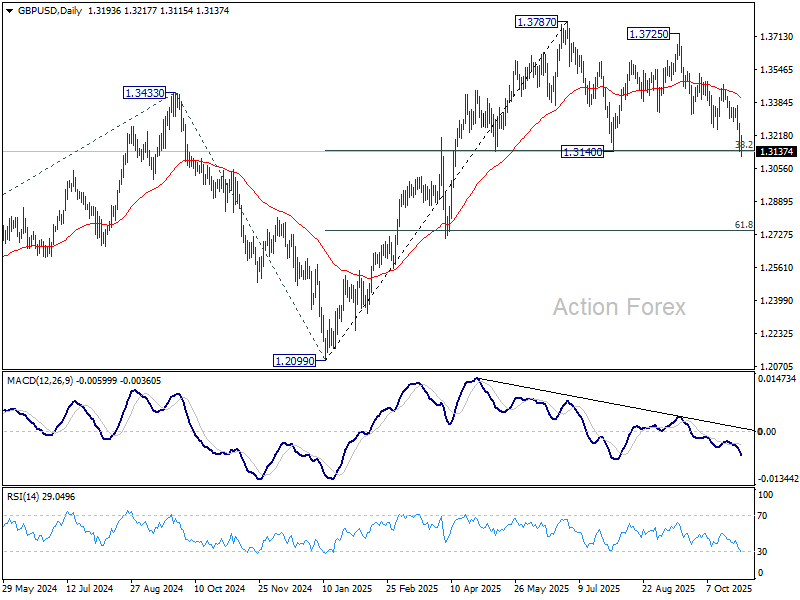

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3130; (P) 1.3206; (R1) 1.3270; More...

Focus stays on 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Decisive break there will complete a double top pattern (1.3787/3725) and turn near term outlook bearish. Deeper decline should then be seen to 61.8% retracement at 1.2744 next. On the upside, above 1.3247 support turned resistance will turn intraday bias neutral first.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

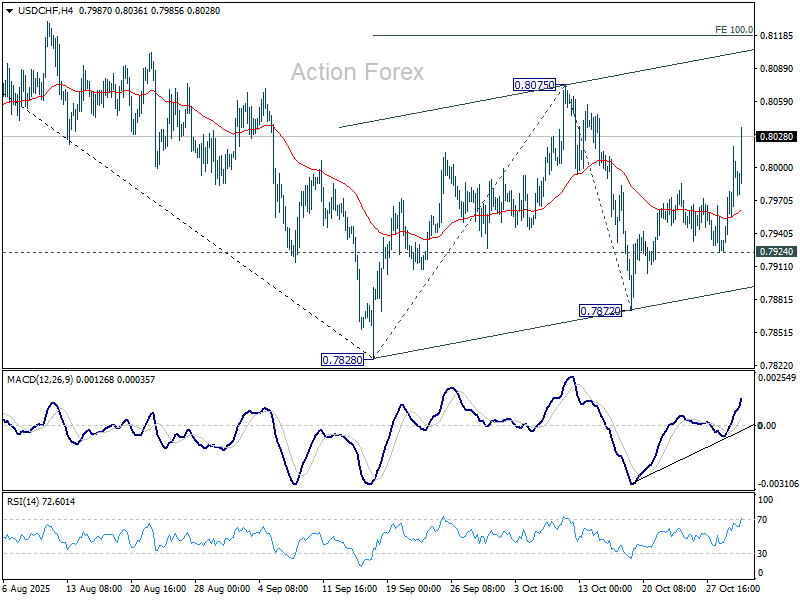

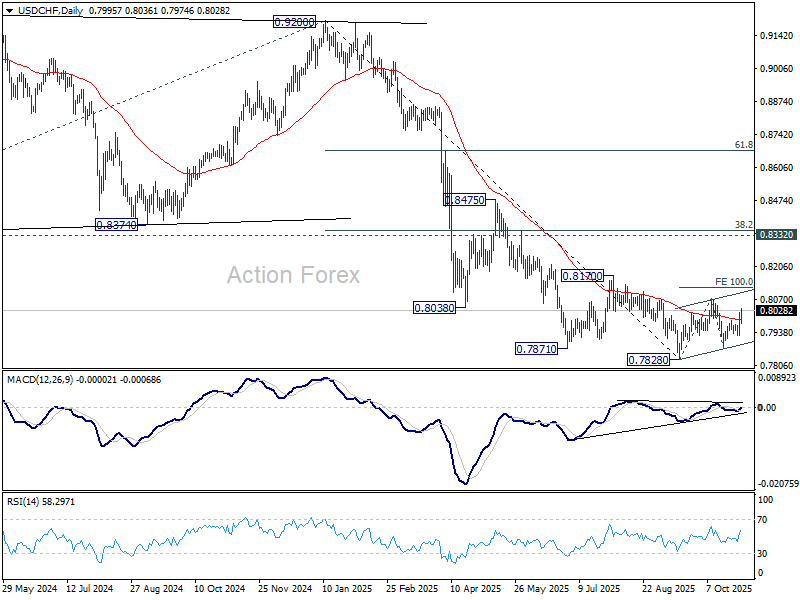

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7943; (P) 0.7981; (R1) 0.8037; More…

Intraday bias in USD/CHF remains on the upside at this point. Current development suggest that corrective pattern from 0.7878 is extending with another rising leg. Further rise should be seen to 0.8075 resistance. Firm break there will target 100% projection of 0.7828 to 0.8075 from 0.7872 at 0.8119. For now, risk will be mildly on the upside as long as 0.7924 support holds, in case of retreat.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

ECB holds at 2.00%, not pre-committing to any rate path

The ECB kept its deposit rate unchanged at 2.00%, in line with expectations, and signaled no change in its cautious, data-dependent approach. Policymakers reaffirmed that inflation remains close to the 2% medium-term target, with the Governing Council’s assessment of the outlook “broadly unchanged.”

In its statement, the ECB noted that the Eurozone economy continues to grow despite a difficult global backdrop. It cited the robust labor market, solid private sector balance sheets, and the supportive effects of past rate cuts as key "sources of resilience". However, the Bank acknowledged that the outlook remains uncertain, highlighting persistent global trade disputes and geopolitical risks as ongoing headwinds.

The Governing Council reiterated that future policy decisions will be made on a meeting-by-meeting basis and guided strictly by incoming data. ECB emphasized that it is "not pre-committing to a particular rate path."

(ECB) Monetary policy decisions

30 October 2025

The Governing Council today decided to keep the three key ECB interest rates unchanged. Inflation remains close to the 2% medium-term target and the Governing Council’s assessment of the inflation outlook is broadly unchanged. The economy has continued to grow despite the challenging global environment. The robust labour market, solid private sector balance sheets and the Governing Council’s past interest rate cuts remain important sources of resilience. However, the outlook is still uncertain, owing particularly to ongoing global trade disputes and geopolitical tensions.

The Governing Council is determined to ensure that inflation stabilises at its 2% target in the medium term. It will follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance. In particular, the Governing Council’s interest rate decisions will be based on its assessment of the inflation outlook and the risks surrounding it, in light of the incoming economic and financial data, as well as the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

Key ECB interest rates

The interest rates on the deposit facility, the main refinancing operations and the marginal lending facility will remain unchanged at 2.00%, 2.15% and 2.40% respectively.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP and PEPP portfolios are declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation stabilises at its 2% target in the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.

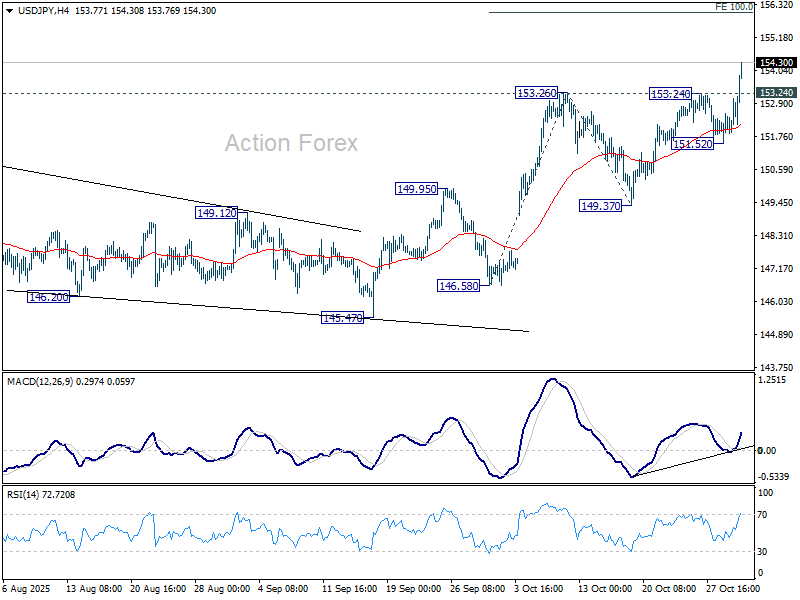

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.83; (P) 152.45; (R1) 153.35; More...

Dollar's strong break of 153.26 confirms resumption of whole rise from 139.87. Intraday bias is back on the upside for 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Firm break there will target 158.86 resistance next. On the downside, below 153.24 resistance turned support will turn intraday bias neutral first. But outlook will stay bullish as long as 151.52 support holds, in case of retreat.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Dollar Rises Along with Yields as Fed Expectations Adjustment Continues

Dollar extended its rebound as North American trading got underway, gaining further momentum following Wednesday’s hawkish Fed rate cut. The greenback’s strength came as markets continued to digest the Fed’s divided decision and Chair Jerome Powell’s pushback against expectations for another cut in December.

U.S. Treasury yields also climbed, with the 10-year yield breaking above 4.1% and appearing poised to extend its near-term rebound. The move reflects a market reassessment of the Fed’s trajectory after Powell emphasized that future easing is “not a foregone conclusion.” As a result, the probability of a December rate cut has slipped to 68.8%, down sharply from around 90% at the start of the week.

Still, the broader policy debate remains nuanced. The Fed’s latest Summary of Economic Projections places the neutral rate—the level neither stimulating nor restricting the economy—within a 2.8% to 3.5% range. With the current policy rate at 3.75–4.00%, the stance is still modestly restrictive, but not overly tight. Some policymakers may still see room to bring rates slightly closer to neutral as a form of insurance, particularly given the data blackout caused by the ongoing government shutdown.

For now, Dollar is the day’s top performer, followed by Swiss Franc and Euro, which is trading cautiously ahead of the ECB decision. The euro remains steady, with investors expecting the central bank to hold its deposit rate at 2.00% and maintain a neutral tone, signaling comfort with current policy settings.

At the other end of the spectrum, Yen is under heavy pressure, with selling resuming after the BoJ’s uneventful policy hold. Aussie and Kiwi also softened, reflecting a cooling of risk-on sentiment following earlier optimism over the Trump–Xi trade deal. Elsewhere, Sterling and Loonie are trading mid-pack.

On the trade front, China’s Commerce Ministry said it will cooperate with the U.S. to “properly resolve” issues surrounding TikTok’s U.S. operations. But there is not timeline nor details provided. TikTok will likely remain a sticky issue despite the progress in de-escalation trade tension with the Trump–Xi summit in South Korea.

In Europe, at the time of writing, FTSE is down -0.61%. DAX is down -0.15%. CAC is down -0.91%. UK 10-year yield is up 0.005 at 4.445. Germany 10-year yield is up 0.032 at 2.657. Earlier in Asia, Nikkei rose 0.04%. Hong Kong HSI fell -0.24%. China Shanghai SSE fell -0.73%. Singapore Strait Times fell -0.06%. Japan 10-year JGB yield fell -0.007 to 1.647.

Eurozone GDP beats expectations with 0.2% growth in Q3

The Eurozone economy expanded by 0.2% qoq in Q3, outpacing expectations of a 0.1% increase. EU GDP rose 0.3% qoq, marking a modest but welcome pickup in growth momentum. Compared with the same period last year, seasonally adjusted GDP grew 1.3% yoy in the Eurozone and 1.5% across the EU.

Among member states, performance was uneven but generally positive. Sweden led the bloc with a robust 1.1% quarterly increase, followed by Portugal (+0.8%) and Czechia (+0.7%). In contrast, Lithuania (-0.2%), Ireland, and Finland (both -0.1%) saw mild contractions. The data show that 14 countries posted positive year-on-year growth, with only one economy contracting.

Swiss KOF climbs to 101.3, outlook brightens

Switzerland’s KOF Economic Barometer rose more than expected in October, advancing from 98.0 to 101.3 against forecasts of 99.0. The index’s move above the 100-threshold suggests that short-term prospects are now slightly above the long-term average, hinting at a firmer growth backdrop heading into year-end.

The KOF Institute noted that most indicator groups contributed positively to the uptick. In particular, manufacturing, financial and insurance services, and other service industries all displayed a more favorable outlook. However, the report pointed out a setback in private consumption, underscoring that household spending remains a relative weak spot even as business sentiment strengthens.

BoJ holds at 0.50%, keeps gradual tightening bias intact

The BoJ left its overnight call rate unchanged at 0.50% as widely expected. The decision came by a 7–2 vote, with Hajime Takata and Naoki Tamura again dissenting in favor of a 25bps rate hike to move policy a little closer to neutral. The repeat split highlights the growing divergence within the board as policymakers debate how quickly to normalize monetary conditions.

In its quarterly Outlook Report, the BoJ made only marginal revisions to its forecasts, signaling that the economic and inflation outlook remains broadly stable. The bank raised its fiscal 2025 GDP forecast slightly from 0.6% to 0.7%, while projections for 2026 and 2027 were left unchanged at 0.7% and 1.0%, respectively.

On prices, the BoJ kept its core CPI forecast at 2.7% for 2025, 1.8% for 2026, and 2.0% for 2027. Core-core CPI (excluding both fresh food and energy) was nudged higher to 2.0% in 2026 from 1.9%, with other years unchanged (2026 at 2.8% and 2027 at 2.0%). The bank reiterated that underlying inflation is expected to reach 2% in the latter half of the projection period through March 2027, retaining language from July that risks to the inflation outlook remain “roughly balanced.”

The BoJ also reiterated that it would continue to raise its policy rate and adjust the degree of monetary support “in accordance with improvements in the economy and prices.”

New Zealand ANZ business confidence surges to seven-month high, green shoots emerging

New Zealand’s ANZ Business Confidence Index surged sharply in September, rising from 49.6 to 58.1, the highest level since February. Own Activity Outlook also improved modestly, up from 43.4 to 44.6, marking its strongest reading since April.

Inflation expectations, meanwhile, remained broadly steady. The share of firms expecting to raise prices over the next three months eased slightly from 46% to 44%. Those anticipating cost increases ticked up from 75% to 76%. One-year-ahead inflation expectations edged higher from 2.71% to 2.75%.

ANZ noted that “green shoots are emerging, particularly for interest-rate-sensitive sectors.” The bank highlighted stronger retail sentiment as evidence that the economy is beginning to warm alongside the spring season, with monetary easing and high rural incomes supporting regional confidence and broader recovery momentum.

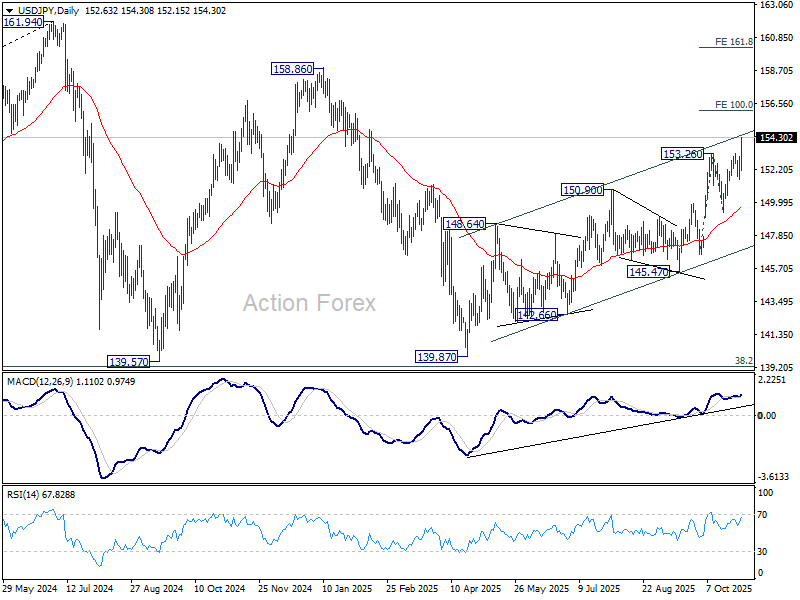

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.83; (P) 152.45; (R1) 153.35; More...

Dollar's strong break of 153.26 confirms resumption of whole rise from 139.87. Intraday bias is back on the upside for 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Firm break there will target 158.86 resistance next. On the downside, below 153.24 resistance turned support will turn intraday bias neutral first. But outlook will stay bullish as long as 151.52 support holds, in case of retreat.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

GBP/USD Price Forecast: Cable to Test 5-Month Lows of 1.31400 as Fiscal Worries Worsen

Falling under 1.32000 yesterday, GBP/USD currently trades 1.3176, down -0.13%.

Succumbing to selling pressure, yesterday’s session goes on record as cable’s worst daily performance in thirty-four days.

GBP/USD now looks for support both at monthly lows and the 200-day SMA, or will risk a further move to the downside.

What’s next for GBP/USD?

Let’s discuss.

GBP/USD: Key takeaways 30/10/2025

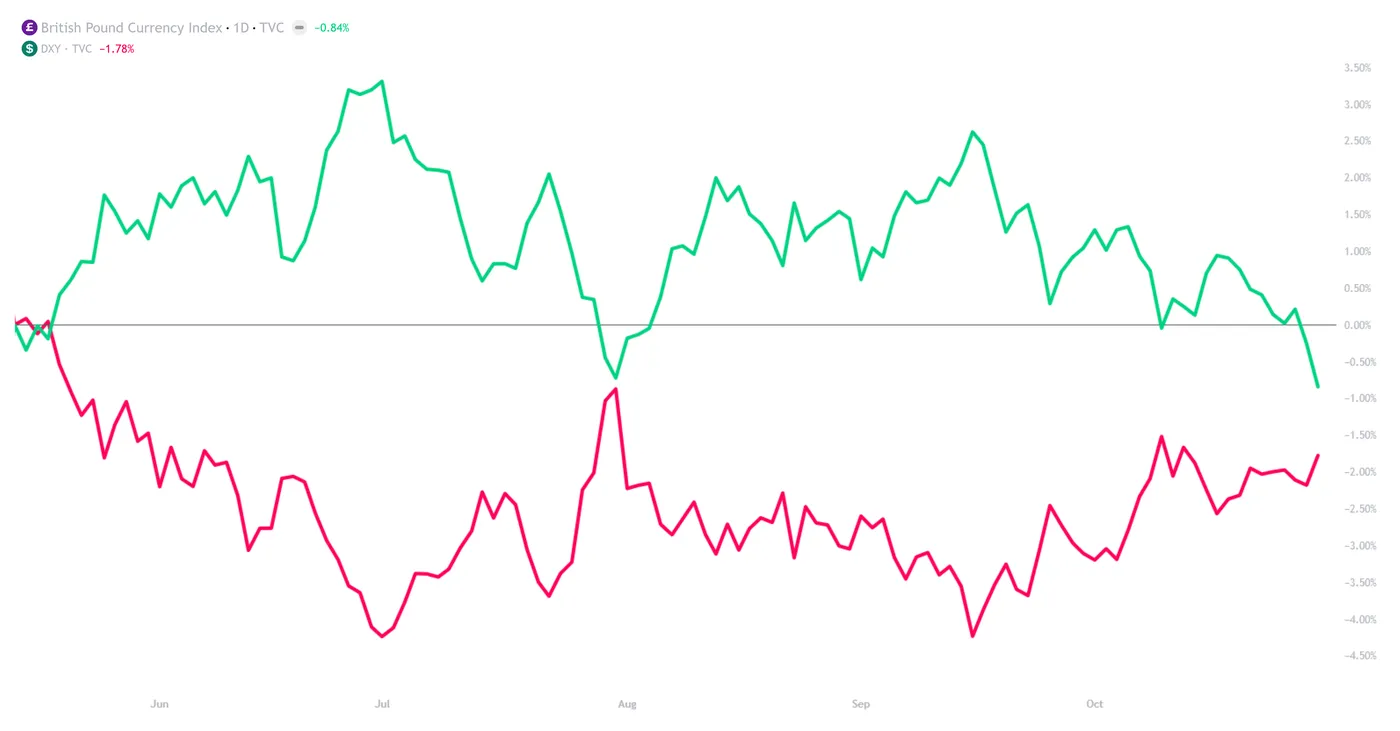

- While still up around 5.40% year-to-date, owing mainly to dollar downside as opposed to pound strength, GBP/USD has recently fallen to 5-month lows of 1.31400

- Later this week, an Office for Budget Responsibility (OBR) assessment is expected to rein in productivity estimates for the UK economy, boding poorly for investor sentiment on the UK economy, weighing harshly on sterling pricing

- Bank of England Governor Andrew Bailey has recently acknowledged softening labour conditions and poor economic growth, but will be hard-pressed to cut rates in the upcoming decision, while inflation is nigh on twice the target of 2%

GBP/USD: Cable under tension

As an Englishman, I can say that the collective feeling amongst the British public regarding the UK economy currently leaves much to be desired.

The highest inflation of any G7 nation, rising unemployment, and, at best, a middling economy.

Safe to say, things are not looking too peachy going into Chancellor of the Exchequer Rachel Reeves' budget next month, which is almost sure to raise taxes in some capacity.

Put simply, the current outlook for the UK economy, particularly in terms of public finances, is less than stellar, which is encouraging those to sell sterling in favour of other currencies.

Let’s take a look at two headline macroeconomic themes within GBP/USD markets.

British Pound Currency Index (BXY) & US Dollar Currency Index (DXY), D1, TVC, TradingView, 30/10/2025

GBP/USD: Fundamental Analysis 30/10/2025

Markets are nervous of UK fiscal woes: While the public finances of many developed nations are currently somewhat dubious at best, this is particularly true for the United Kingdom, with a multibillion-pound hole that needs to be addressed by the upcoming budget in November.

While developments concerning the budget continue to do the media rounds, which will inevitably only increase as November 26th approaches, Rachel Reeves is stuck between a rock and a hard place, between honoring campaign pledges not to raise taxes on working people and VAT while simultaneously needing to find an estimated £30bn to balance spending with tax income.

To make matters worse, and coming at an inopportune time for the Chancellor of the Exchequer, an assessment to be released on Friday by the Office for Budget Responsibility (OBR) is expected to substantially downgrade UK productivity forecasts, resulting in a further estimate of £20 billion in shortfall.

Not to mention: government borrowing also exceeded estimates in the first half of 2025 by £7.2bn as per last week’s OBR commentary.

Tying this back to GBP/USD, however, is remarkably simple: the fiscal health of the UK economy appears to be worsening, and investors are collectively demanding a higher level of risk premium to hold sterling-denominated assets.

This fundamental downgrade in sterling’s rating when compared to other stores of wealth is what has led, in no small part, to recent GBP/USD downside.

The UK economy is at serious risk of stagflation. Granted, the term is often used loosely, but stagflation is a genuine concern for the UK economy. Currently, the Bank of England is faced with a serious ‘catch-22’:

- Rising unemployment, now at 4.8%, its highest level since July 2021

- Poor GDP growth, with recent estimates for Q2 at a measly 0.3%

- Stubborn inflation, at 3.8% YoY in September and, crucially, almost double the 2.0% target

Naturally, the top two bullets would support the notion of cutting rates, while stubborn inflation would support hiking, putting Governor Andrew Bailey and his team of decision makers in an inevitable position.

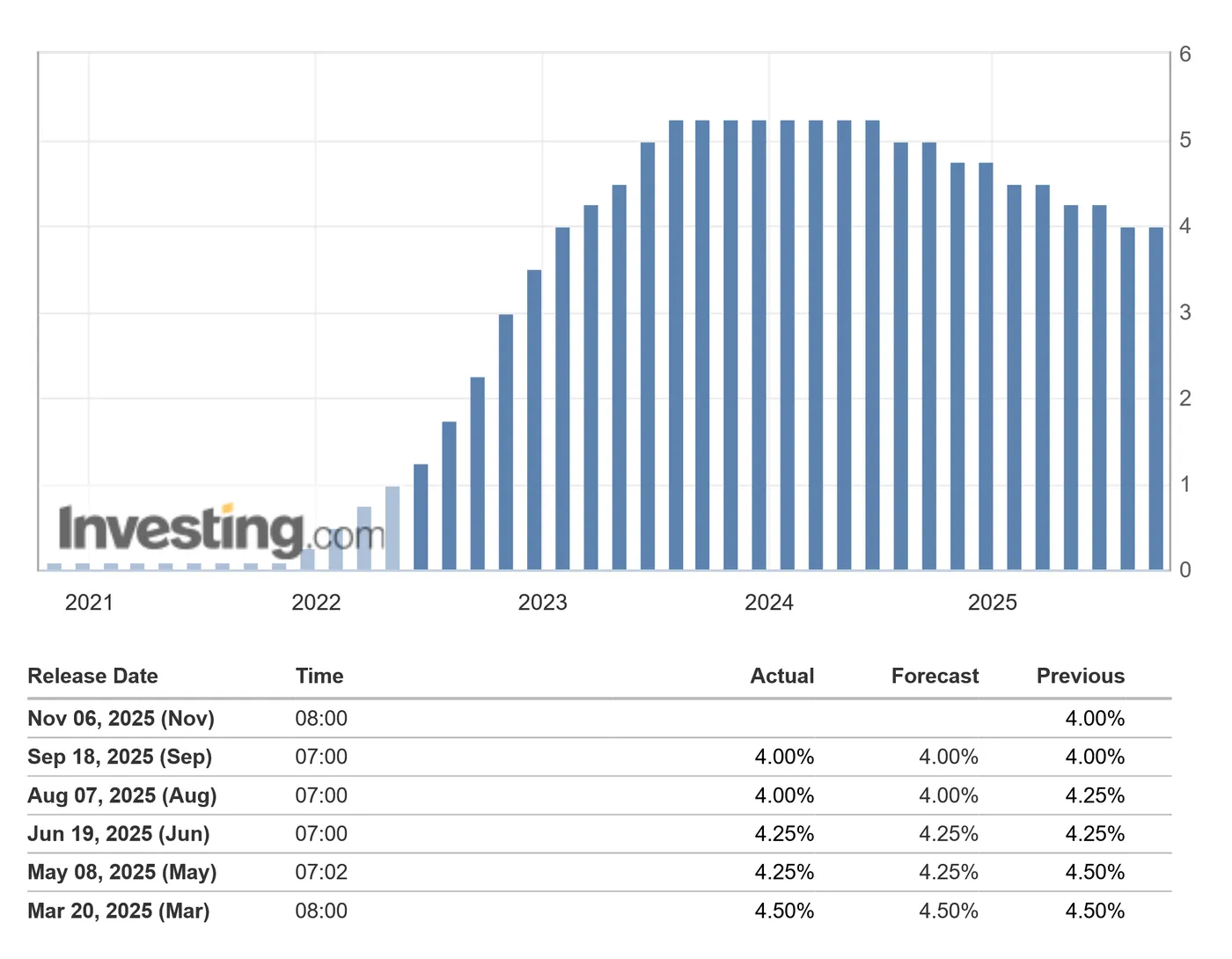

While the Bank of England is due to vote on monetary policy on November 6th, most predict their hand will be forced in maintaining rates at 4.00%, owing to recent inflation trends.

UK Interest Rates, investing.com 30/10/2025

By extension, a decision to hold would put further pressure on an already weak UK labour market and economy, which seems to be a conclusion the markets have already come to, with the first possibility of a rate cut expected to be in February 2026 at the time of writing.

At least one outcome of the above is the apparent decline in sterling value, with the current situation for the Bank of England enough to spook investors into rethinking their exposure to GBP.

GBP/USD: Technical Analysis 30/10/2025

Gold (XAU/USD): Daily (D1) chart analysis:

GBP/USD, D1, OANDA, TradingView, 30/10/2025

Having traded in range for some time, recent downside could be enough to break consolidation to the downside.

Fair to say, recent performance is decisively bearish, with a pin bar forming in yesterday’s session that bears will look to fill today.

Now with 5-month lows of 1.31400 and the 200-day SMA, GBP/USD will need to find support or risk a further move down:

Price targets and support/resistance levels:

- Price target/Resistance #1 - $1.31403 - Triple bottom lows

- Price target/Resistance #2 - $1.31011 - April highs/structure

- Support #1 - $1.32904 - Previous consolidation