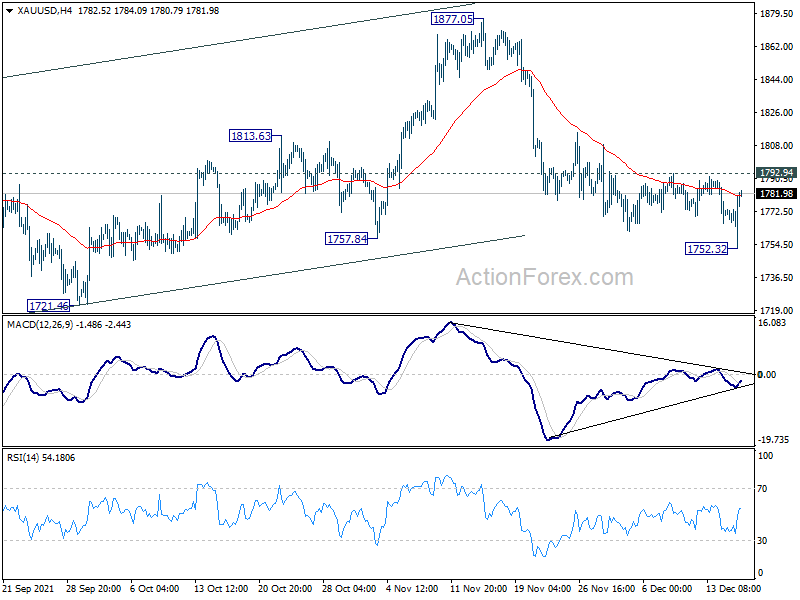

Gold spiked lower to 1752.32 after Fed decided to double tapering pace while the new projections indicated three rate hikes next year. Yet, Gold quickly recovered and there was no follow through buying in Dollar.

For now, further fall will remain in favor in Gold as long as 1792.94 resistance holds. Break of 1752.32 will resume the decline from 1877.05 to 1721.46 first. Break there will target key long term support zone at 1676.55/1682.60.

However, strong break of 1792.94 will now bring sustained trading above 55 day EMA. Considering bullish convergence condition in 4 hour MACD too, that would signal complete of fall from 1877.05 and bring stronger rise back towards this resistance.

SNB stands pat, upgrades 2021 and 2022 inflation forecasts

SNB kept the sight deposits rate unchanged at -0.75% as widely expected. It also remained “remains willing to intervene in the foreign exchange market as necessary, in order to counter upward pressure on the Swiss franc”. The Swiss Franc “remains highly valued”.

The new conditional inflation forecasts for 2021 and 2022 were revised higher “primarily due to higher import prices, all all for oil products and for goods affected by global supply bottlenecks”. New forecast stands at 0.6% for 2021, 1.0% for 2022 and 0.6% for 2023, comparing to September forecasts of 0.5% for 2021, 0.7% for 2022, and 0.6% for 2023. They based on assumption that policy rate remains at -0.75% over the entire forecast horizon.

As for the economy, the baseline scenario is a “continuation of the economic recovery next year”. SNB expects GDP growth of around 3% for 2022 while unemployment is “likely to decline again somewhat”.

Full statement here.