Sample Category Title

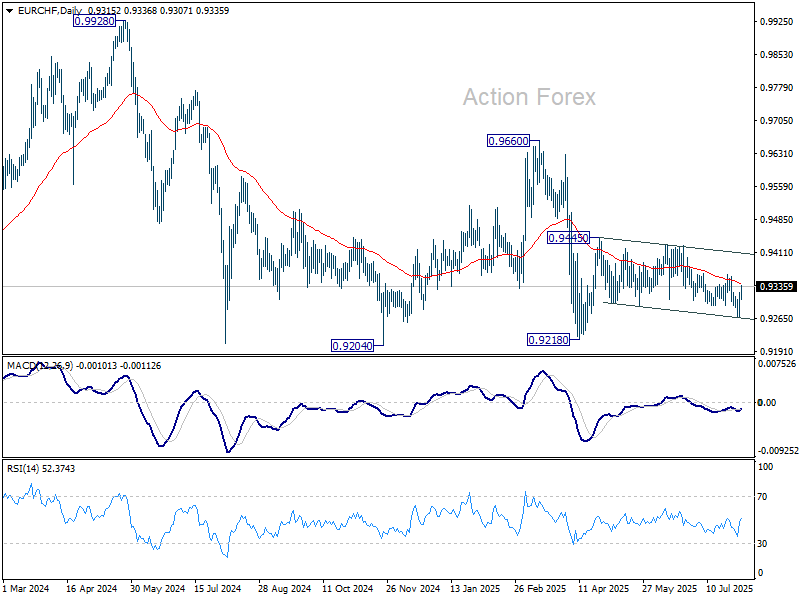

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9285; (P) 0.9305; (R1) 0.9338; More....

Intraday bias in EUR/CHF stays neutral first. Price actions from 0.9445 could still be considered a corrective pattern. On the upside, above 0.9361 resistance will target 0.9428 resistance first. However, below 0.9265 will bring another fall back to retest 0.9218 low.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside position should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

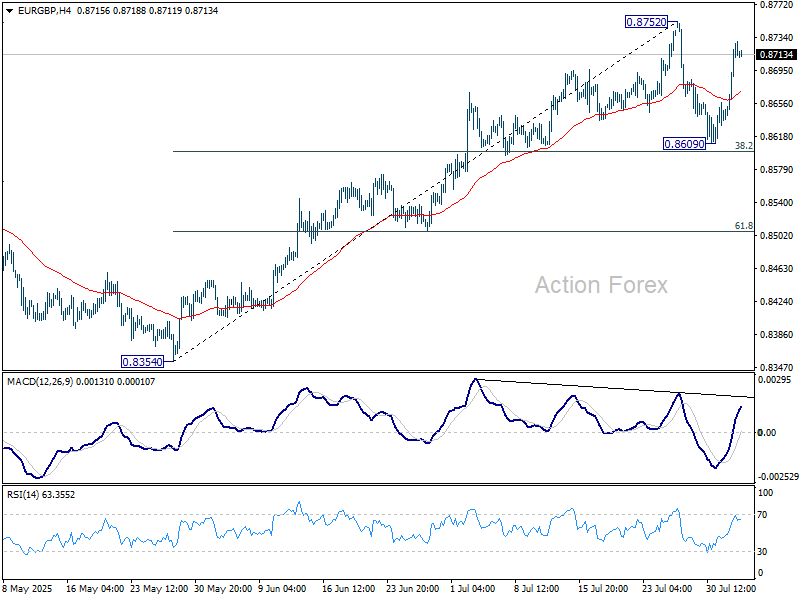

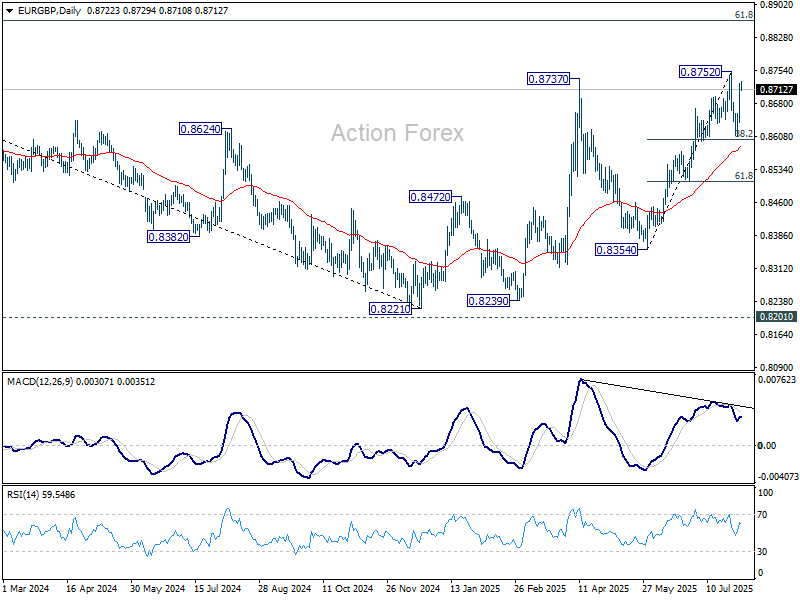

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8666; (P) 0.8698; (R1) 0.8759; More...

Intraday bias in EUR/GBP stays neutral for the moment. Some more consolidations could be seen below 0.8752. But in case of another fall, downside should be contained by 38.2% retracement of 0.8354 to 0.8752 at 0.8600. On the upside, firm break of 0.8752 will resume the rise from 0.8354 towards 0.8867 fibonacci level.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8493) holds.

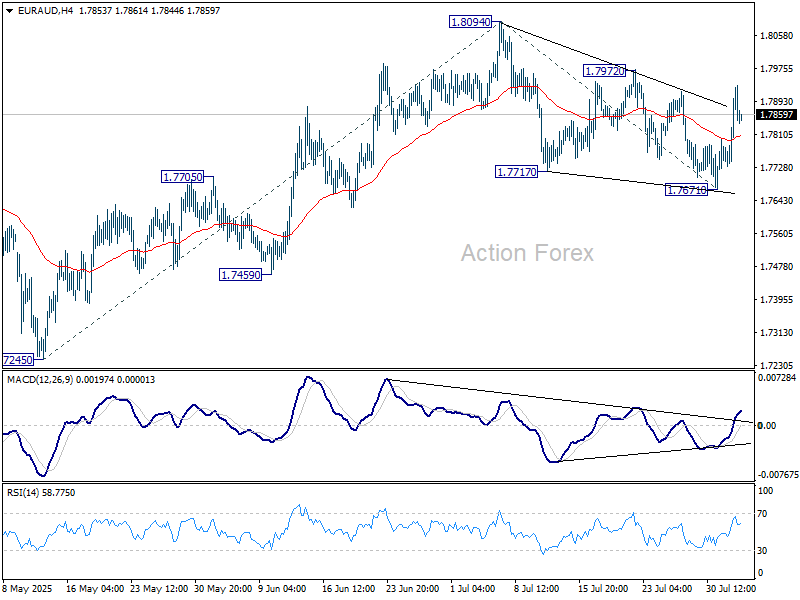

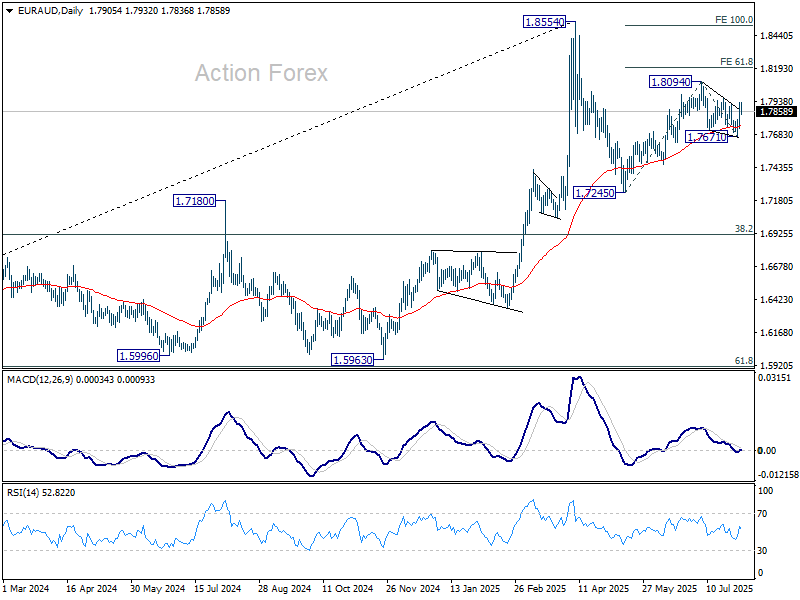

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7785; (P) 1.7859; (R1) 1.7983; More...

Intraday bias in EUR/AUD stays neutral for the moment. On the upside, break of 1.7972 resistance should resume the whole rally from 1.7245 through 1.8094 to 61.8% projection of 1.7245 to 1.8094 from 1.7671 at 1.8196. On the downside, below 1.7671 will bring deeper fall back to 1.7459 support instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is expected to resume at a later stage.

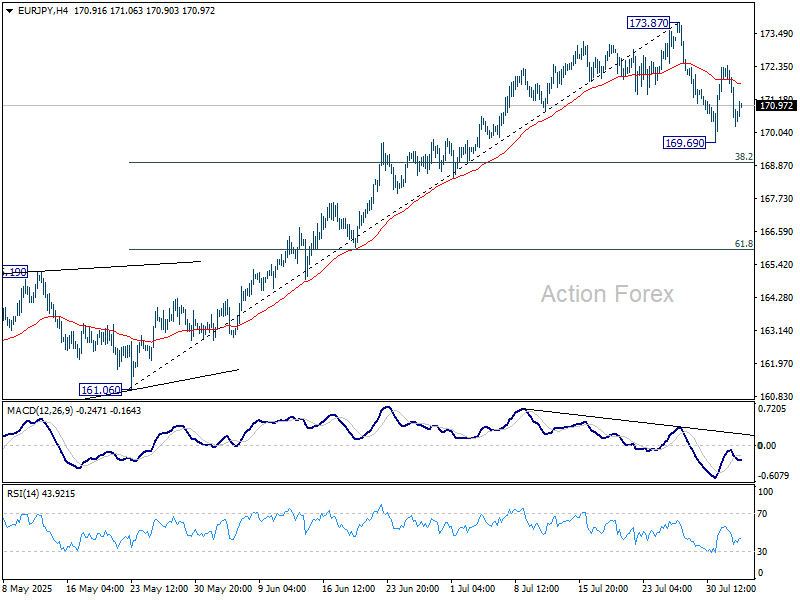

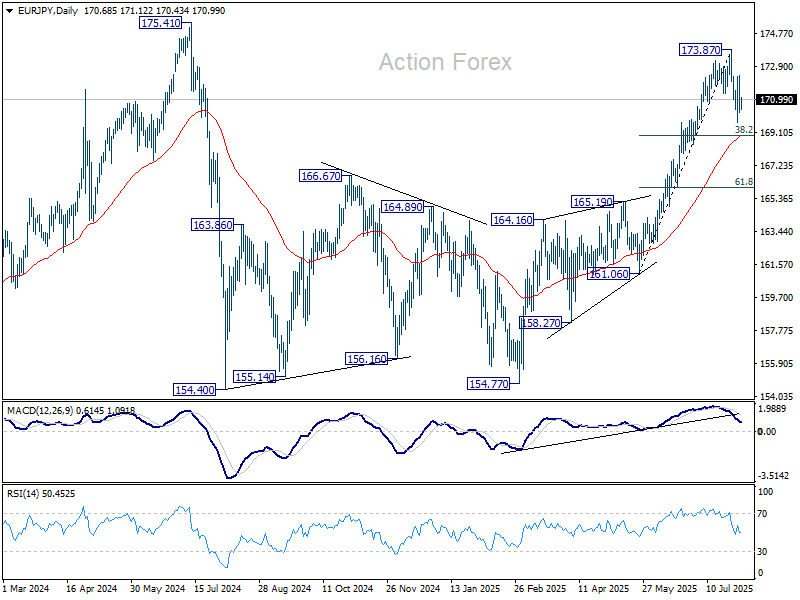

EUR/JPY Daily Outlook

Daily Pivots: (S1) 169.88; (P) 171.14; (R1) 171.99; More...

Intraday bias in EUR/JPY stays neutral and more consolidations would be seen below 173.87. In case of deeper fall, downside should be contained by 38.2% retracement of 161.06 to 173.87 at 168.97 to bring rebound. On the upside, firm break of 173.87 will resume larger rally from 154.77 to retest 175.41 high.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break there will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 168.80) will delay this bullish case.

You’re Fired

Market sentiment is turning sour after last Friday’s weak US jobs data that led to the firing of the Chief of the Bureau of Labor Statistics (BLS)! The BLS reported just 73,000 nonfarm payroll gains for June — far below expectations. But what likely enraged Trump was the revisions: a sharp downward adjustment of 258,000 jobs from the previous two months, which completely reshaped the narrative of a resilient labour market. Taken together, the three-month average job gain fell from 150,000 to just 35,000.

And here’s the rule of thumb: if the US sees NFP figures under 50,000 for six months in a row, that’s considered a recession signal. So, the US may already be halfway there.

The good news — for Donald Trump — is that recession fears have turbocharged rate cut expectations. After Friday’s weak jobs report, the probability of a September Federal Reserve (Fed) rate cut jumped from 38% to above 80%. The US 2-year yield, which tracks rate expectations, dropped sharply from near 4% to below 3.70%.

But the bad news is that a weak economy wasn’t part of Trump’s promise. Cutting rates at the wrong moment won’t magically rescue markets, and scapegoating the BLS for the outcome of his administration’s chaotic policies risks damaging the credibility of US economic data.

One by one, the things that made the US exceptional are being eroded.

But US tech earnings show resilience

The S&P500 earnings season — particularly for tech — is going well. Strong AI demand and a softer dollar have led to better-than-expected results across Big Tech.

Meta once again outperformed expectations, Microsoft’s cloud business grew faster than anticipated, and Google held steady. Even Apple sold more iPhones last quarter and reaffirmed its focus on AI. Tesla and Amazon were rare weak spots: Tesla for reasons well known, and Amazon because investors haven’t yet seen AI investments translate into revenue.

So far, 66% of S&P 500 companies have reported earnings, and Fact Set points that 82% posted positive EPS surprises and 79% reported better-than-expected revenues. The earnings growth rate for the S&P 500 stands at around 10% — well above the 5–7% that investors were expecting.

The issue now is guidance. Outside of AI, it’s not great. Many companies are warning that tariffs could weigh on future results. So maybe — just maybe — those S&P 500 record highs are a bit exaggerated in the current broader context.

Across the Atlantic, earnings have been hit by tariff uncertainty, a stronger euro, and the fact that many companies — particularly automakers — have opted to absorb tariff costs to preserve market share during negotiations. Banks were the exception, benefiting from higher volatility.

The impact of tariffs will persist, though unevenly. Big Tech, financials, utilities, and communications are seen as relative winners in this chaotic reshaping of global trade. Consumer staples, energy, real estate, and healthcare are among the most exposed. Consumer discretionary, industrials, and materials face mixed outcomes, depending on whether they can pass on tariff costs or not.

Eventually, US consumers may end up paying most of the tariffs. To appease Trump’s deficit obsession, they may have to curb their consumption — especially imports. The data released over the next few months will be incredibly interesting to watch — but may also be framed in ways that make the US economy look better than it feels.

US Job Creation Stalls Amid Tariffs

In focus today

This week is light on the data front, with key events including Swedish CPI figures and the Bank of England's bank rate decision on Thursday.

Economic and market news

What happened over the weekend

In the euro area, inflation edged slightly higher than expected in July, reaching 2.0% y/y (cons: 1.9%), in line with earlier country-specific data. The increase was primarily driven by food price inflation, which rose from 3.1% y/y to 3.3% y/y. Core inflation remained steady at 2.3% y/y, as a dip in services inflation to 3.1% y/y was offset by an increase in goods inflation to 0.8% y/y. Following the recent string of events, we have revised our call ECB call, and we now expect the ECB to keep its policy rates unchanged throughout 2025-26. For details see New ECB call: No further cuts in scope, 1 August.

In the US, the non-farm payrolls data revealed a significant slowdown in job creation. July saw only 73k jobs added compared to expectations of +110k, alongside major downward revisions for May (+144k to +19k) and June (+147k to just +14k). This marks a stark contrast to the stronger job growth earlier in the year, with private sector hiring appearing to stall almost entirely after tariffs took effect. Adding to the weak NFP report, unemployment rate increased to 4.2%, these figures boosted expectations of a near-term Fed rate cut and caused the dollar to fall.

In Oil markets, OPEC+ approved a 547,000-bpd production increase for September, continuing its push to reclaim market share amid concerns over potential supply disruptions linked to Russia. The decision was attributed to a strong economy, low inventory levels and that oil prices have remained elevated despite recent output hikes, with Brent crude at USD 69/bbl.

FI and FX: The very weak US labour market report as well as a weak ISM report led to the biggest decline in 2Y US treasury yields since 2023 as well as a steeper US yield curve. Furthermore, there was a substantial shift in the market pricing of US monetary policy as the possibility of a rate cut in September has risen substantially. The broad USD gave up much of last week's gains following the weak jobs report, which included significant negative revisions to previous months. Adding to the pressure, ISM manufacturing declined to a nine-month low. EUR/USD jumped nearly two figures, and a September Fed cut has now been re-established as the base case in markets.

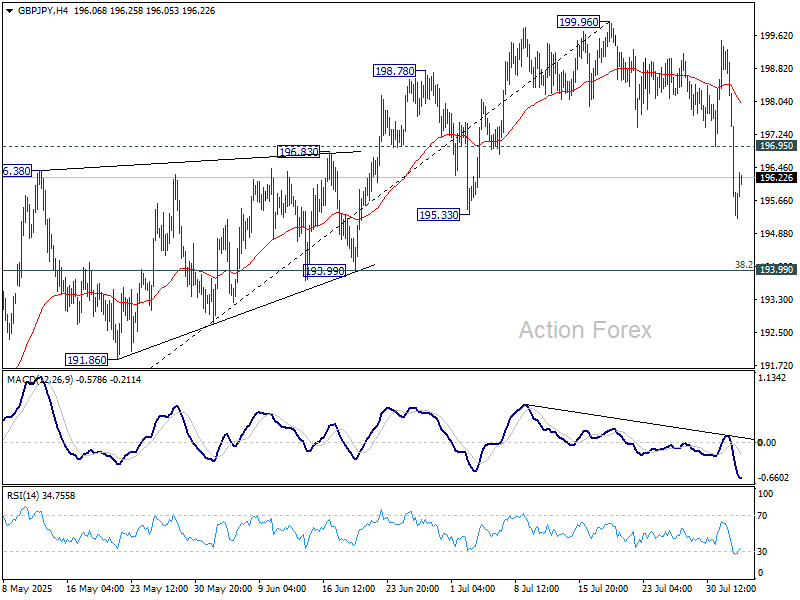

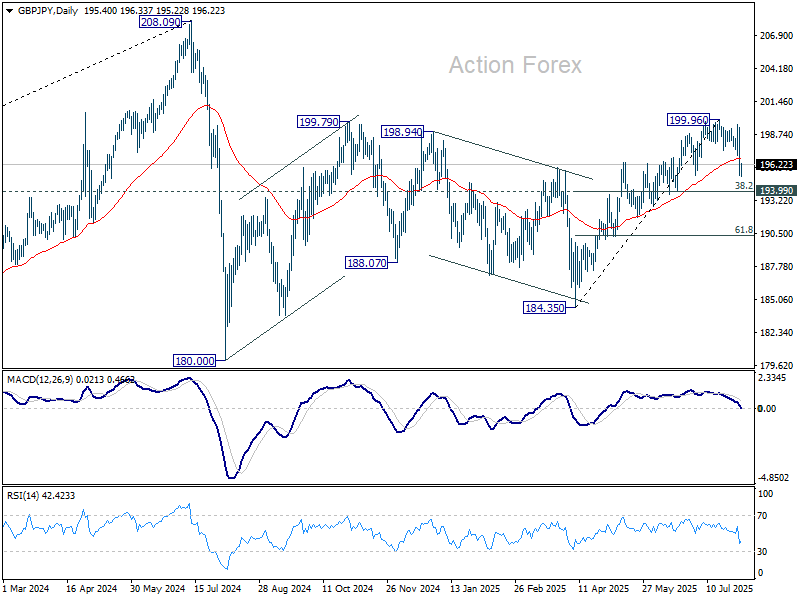

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.28; (P) 196.82; (R1) 198.29; More...

Intraday bias in GBP/JPY stays mildly on the downside for the moment. Fall from 199.96 would extend towards 193.99 cluster support (38.2% retracement of 184.35 to 199.96 at 193.99). Strong support should be seen there to bring rebound, at least on first attempt. On the upside, above 196.95 support turned resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

Asia Unshaken by Wall Street Rout, BoE Set to Steer the Week

Forex markets opened the week on a quiet note, with major pairs and crosses holding tightly within Friday’s ranges during Asian session. Even with last week’s risk-off tone and Wall Street’s steep decline, Asian investors appear to be taking the broader US developments in stride. One outlier is Japan’s Nikkei, which extended its selloff from Friday. Still, the index remains comfortably above the key 40k psychological level, a sign that confidence hasn’t fully eroded. After all, there’s cautious optimism in the region that accelerating Fed rate cuts could eventually support global sentiment.

That said, political tensions in the US are still drawing much attention. US President Donald Trump’s abrupt dismissal of Bureau of Labor Statistics Commissioner Erika McEntarfer, after accusing her of falsifying job numbers, raised fresh concerns over institutional stability. Trump claimed he would name a new BLS head within days, while White House officials attempted to back up his accusation without concrete evidence. Kevin Hassett, head of the National Economic Council, echoed the president’s stance, pointing to “revisions” as proof of wrongdoing.

However, Bill Beach, a former BLS Commissioner and Trump appointee, emphasized that employment figures are compiled by professionals who have served under both parties. He strongly defended the integrity of the agency’s methods. The controversy adds to broader unease after the downward revisions to job growth figures last week further fueled expectations of a Fed policy shift.

On the trade front, Jamieson Greer, the US Trade Representative, said most of last week's new tariff rates are already locked in. That should ease some market fears about ongoing surprises, though not all negotiations are settle, and several key fronts are unresolved. Most notably, talks with China continue ahead of the August 12 tariff truce deadline, and no agreement has been reached on an extension.

India is also under scrutiny, having just been hit with a 25% US tariff. Stephen Miller warned over the weekend that countries financing Russia's war “will face consequences,” with Trump hinting at even higher duties if peace talks fail. Canada is pushing back against a 35% US tariff on goods not covered under the USMCA, though Canadian officials expressed optimism over potential progress in talks. These crosscurrents will keep markets alert for further trade developments.

Looking ahead, attention will shift to monetary policy and data. BoE is expected to cut rates by 25bps this week, though internal divisions remain huge. Traders will also parse the BoJ’s latest meeting notes and monitor upcoming ISM Services data, plus Canadian and New Zealand labor reports.

In Asia, at the time of writing, Nikkei is down -1.49%. Hong Kong HSI is up 0.50%. China Shanghai SSE is up 0.21%. Singapore Strait Times is up 0.83%. Japan 10-year JGB yield is down -0.048 at 1.505.

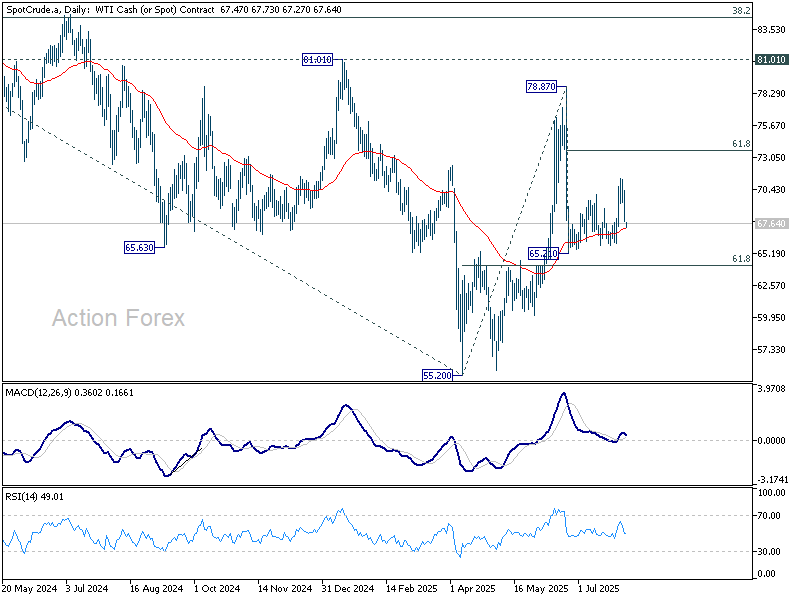

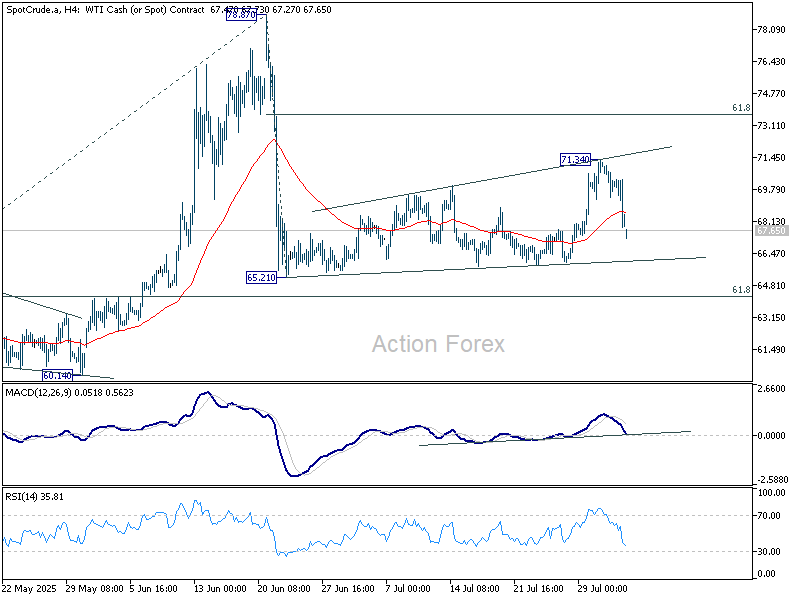

WTI dips on OPEC+ hike, 65 to contain downside in range trade

Crude oil prices slipped on Monday after OPEC+ announced another production boost, this time for September. The group confirmed a planned hike of 547k barrels per day, continuing its aggressive push to regain global market share after years of output cuts meant to prop up prices.

The shift began in April with a small supply increase, but since then OPEC+ has stepped on the gas. May through July each saw 411k bpd added, with larger hikes of 548k in August and now 547k bpd set for September.

Despite briefly surging to nearly 79 in June amid Middle East tensions, WTI crude reversed sharply after the Israel–Iran ceasefire and dropped back to as low as 65.21. The bounce to 71.34 last week failed to sustain, and prices have turned lower again, signaling ongoing sideways consolidation rather than a breakout.

Technically, oil remains trapped in a range. Downside should be anchored near 65, upside appears capped below $73.65. However, even in event of a bounce through 71.34, momentum is expected to fade as oversupply concerns and tepid demand limit further gains below 61.8% retracement of 78.87 to 65.21 at 73.65.

Bitcoin supported by 112k confluence, uptrend still in play

Crypto markets came under pressure last week as risk sentiment soured globally, dragging Bitcoin off recent highs. While the correction was sharp, BTC has found technical footing around a major cluster of support, offering bulls a chance to regroup.

Three key levels are now converging: the prior May high of 112,013, 55 D EMA at 112,331, and trendline support near 111,400. These levels could provide a solid floor for another upside attempt toward the record high at 123,231, assuming broader sentiment doesn’t deteriorate further.

But follow-through may be limited from there as momentum signals suggest caution. Bearish divergence in the daily MACD hints at fading strength, and strong resistance is expected around 100% projection of 49,008 to 109,571 from 74,373 at 134,936 to cap upside.

For now, the uptrend is alive, but ceiling would form below 135k.

BoE eyes another rate cut amid persistent MPC split

BoE is widely expected to deliver another 25bps rate cut this week, continuing its steady pace of one reduction per quarter. That would bring the Bank Rate down to 4.00%. According to a recent Reuters poll, 62 of 75 economists anticipate two more cuts this year — in August and November — keeping the Bank Rate on track to hit 3.75% by year-end.

However, the decision may be far from unanimous. The Monetary Policy Committee remains split, with hawks pointing to persistent inflation risks while doves stress the need to cushion a softening labor market. The middle ground — which has dominated past decisions — still favors a cautious, gradual approach. This internal division is likely to be reflected again in the vote breakdown again, just like the three-way split back in May.

Headline CPI in the UK unexpectedly ticked up to 3.6% in June, reigniting inflation concerns. Survey data also show the public expects stronger price growth ahead. June meeting minutes flagged the risk of rising food prices feeding into broader inflation, and that pressure may force the BoE to revise its 2025 inflation forecast closer to 4%. That’s well above the 2% target and would make it harder for doves to push for a faster pace of easing. Markets will closely watch updated projections for any hawkish tilt that could limit scope for further 2025 easing.

In Japan, the BoJ’s summary of opinions from its July meeting will be scrutinized for signs of how policymakers are responding to the US-Japan trade deal. Optimism about reduced tariff risks could temper some downside concerns. But ongoing trade tensions between the US and other countries, especially China, could have ripple effects across the region.

Another lingering issue is domestic inflation, especially in food. While the BoJ maintains that cost pressures will fade over time, the current pace of increases may challenge that narrative. The tone of the BoJ’s discussions will shape expectations on whether it acts again this year or waits until 2026.

In the US, attention shifts to ISM Services PMI after the sharp downside surprise in last week’s nonfarm payrolls. Markets are growing more confident that the Fed will cut in September, with fed fund futures pricing in nearly 80% probability. A weak ISM read would further validate that view and may raise the likelihood of multiple cuts before year-end. Other data to watch include labor market reports from Canada and New Zealand, and China’s Caixin Services PMI.

Here are some highlights for the week:

- Monday: Swiss CPI, PMI manufacturing; Eurozone Sentix investor confidence; US factory orders.

- Tuesday: BoJ minutes; China Caixin PMI services; Eurozone PMI services final; UK PMI services final; Canada trade balance; US trade balance, ISM services.

- Wednesday: New Zealand employment; Japan average cash earnings; Eurozone retail sales.

- Thursday: Australia trade balance; China trade balance; Swiss foreign currency reserves, unemployment rate; BoE rate decision; US jobless claims; Canada Ivey PMI.

- Friday: Japan house hold spending, BoJ summary of opinions; Swiss SECO consumer climate; Canada employment.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.28; (P) 196.82; (R1) 198.29; More...

Intraday bias in GBP/JPY stays mildly on the downside for the moment. Fall from 199.96 would extend towards 193.99 cluster support (38.2% retracement of 184.35 to 199.96 at 193.99). Strong support should be seen there to bring rebound, at least on first attempt. On the upside, above 196.95 support turned resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

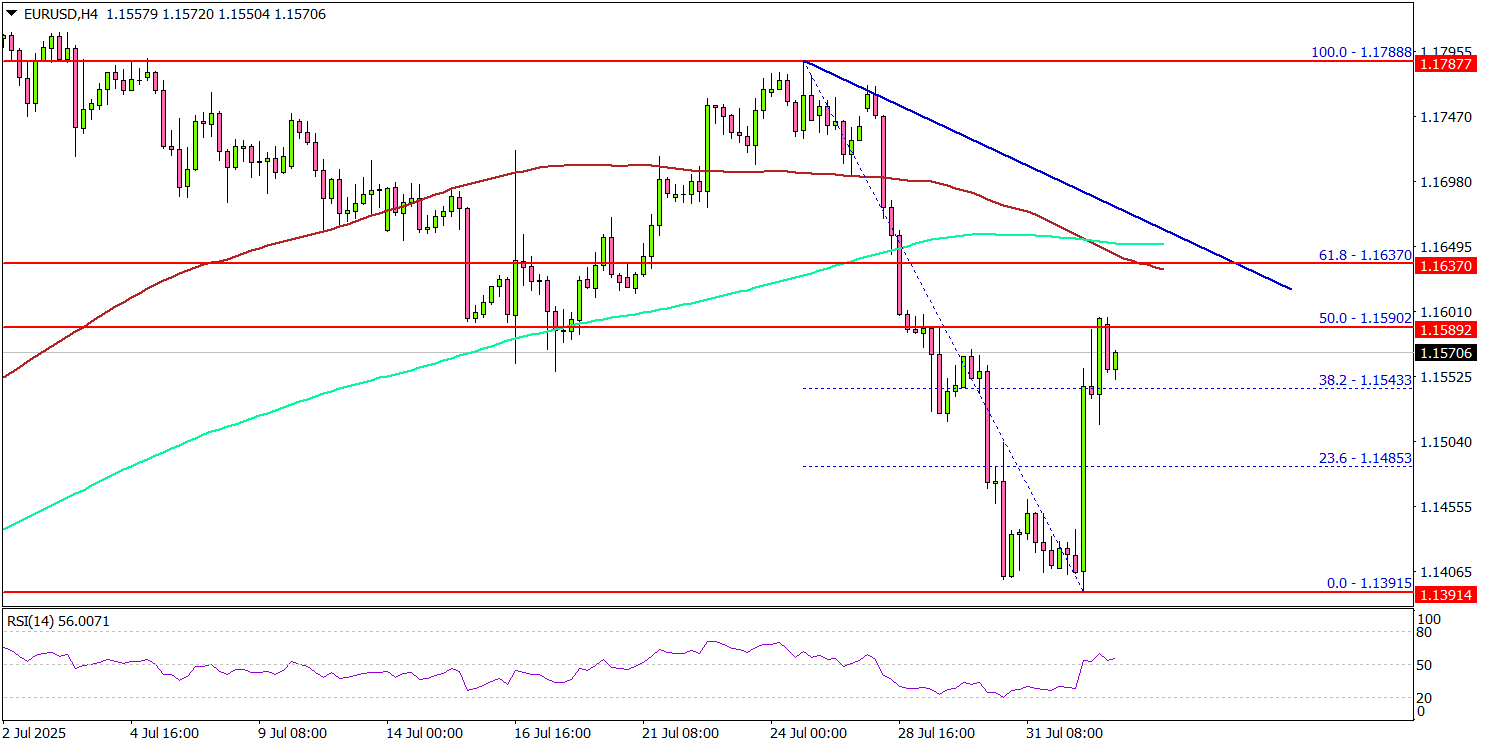

EUR/USD Recovers But Upsides Could Be Capped At 1.1650

Key Highlights

- EUR/USD found support at 1.1400 and started a recovery wave.

- A key bearish trend line is forming with resistance at 1.1640 on the 4-hour chart.

- GBP/USD tumbled below the 1.3500 and 1.3440 support levels.

- Gold prices are moving higher above the $3,350 resistance zone.

EUR/USD Technical Analysis

The Euro started a fresh decline below the 1.1550 level against the US Dollar. EUR/USD declined below 1.1500 before the bulls appeared.

Looking at the 4-hour chart, the pair tested the 1.1400 level. It settled below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

A low was formed at 1.1391 and the pair is now attempting to recover. There was a move above the 1.1480 resistance zone. The pair climbed above 1.1550 and tested the 50% Fib retracement level of the downward move from the 1.1788 swing high to the 1.1391 low.

On the upside, the pair now faces resistance near the 1.1600 level. The next key resistance sits near the 1.1650 level. A close above the 1.1650 level could set the pace for another increase.

In the stated case, the pair could rise toward the 1.1780 resistance. The next major stop for the bulls could be near the 1.1850 resistance.

On the downside, immediate support is near the 1.1520 level. The next key support sits near 1.1450. Any more losses could send the pair toward the 1.1400 support zone.

Looking at GBP/USD, the pair is showing bearish signs and might decline below the 1.3200 support zone.

Upcoming Economic Events:

- Euro Zone Sentix Investor Confidence for August 2025 - Forecast 4.5, versus 4.5 previous.

U.S. Jobs Data Shock Raises Concerns: New Market Trend or Short-Term Volatility?

It was a very volatile week for financial markets. Things started off strong with a trade deal between the U.S. and Europe, but confidence dropped quickly after President Trump announced new global tariffs on August 1. Canada will now face a 35% tariff, up from 25%, and other countries could see tariffs as high as 41% starting August 7 unless new deals are made. This hurt investor sentiment and caused stock markets in Asia and Europe to fall.

The U.S. Federal Reserve decided to keep interest rates unchanged. Fed Chair Jerome Powell said they need more data before making any changes. The U.S. dollar rose earlier in the week thanks to strong GDP data. In Japan, the Bank of Japan also kept rates steady and raised its inflation outlook, but didn’t signal any rate hikes, which caused the yen to weaken. President Trump continued to pressure the Fed to lower interest rates.

On Friday, markets were shaken by much worse-than-expected U.S. jobs data. Fewer jobs were added than expected, and past numbers were revised lower. This increased chances of a Fed rate cut in September. The U.S. dollar dropped sharply, while gold jumped higher. Stocks, oil, and Bitcoin all fell, as investors grew more worried about global trade tensions and a slowing economy.

Markets This Week

U.S. Stocks

The Dow Jones fell every day last week after starting with a key reversal pattern—making a new high but closing lower on Monday. What began as normal profit-taking turned into heavier selling on Friday due to weaker-than-expected U.S. employment data and the announcement of new tariffs on multiple countries as trade talks continued. The drop appears slightly oversold in the short term, but the full impact of the jobs report and trade tensions is still uncertain. Volatility is likely to remain high this week, creating range-trading opportunities. Medium-term traders should be cautious about buying at current levels and may want to wait for further weakness or consider selling into any short-term rebound. Resistance levels are at 44,000, 44,500, and 45,000, while support lies at 43,000, 42,000, and 41,750.

Japanese Stocks

The Nikkei 225 gave up all of its gains from the July 23 U.S.–Japan trade deal last week, falling back to the key 40,000円 level. Although the Bank of Japan maintained a cautious stance on raising interest rates—causing the yen to weaken—the sharp drop in USD/JPY and U.S. equities on Friday pushed the Nikkei lower into the weekend. Despite the decline, the 10-day moving average remains in a bullish trend, and as long as the yen doesn't strengthen further, a rebound this week is likely. Resistance is seen at 41,000円 and 42,000円, while support lies at 40,000円, 39,200円, and 39,000円.

USD/JPY

USD/JPY surged above 150 last week, raising concerns within the Japanese government as strong U.S. economic data and cautious comments from Fed Chair Powell on cutting rates supported the dollar. At the same time, the Bank of Japan signaled it still needs more time before raising rates, adding to the upward pressure. However, all gains were wiped out after much weaker-than-expected U.S. employment data triggered steady selling into the weekend. It’s unclear if this weak trend in U.S. data will continue, but with few major releases scheduled this week, USD/JPY is likely to trade sideways in a broad range. There is a risk of another sharp sell-off if negative headlines emerge around U.S. trade talks. Resistance is seen at 148, 149, and 150, while support lies at 147, 146, and 145.

Gold

Gold spent most of last week under pressure, testing the lower end of its recent range as a stronger U.S. dollar triggered steady selling. However, much weaker-than-expected U.S. employment data reversed the dollar’s strength and sparked heavy gold buying, pushing prices higher by the end of the week. Renewed trade tensions also supported demand for safe-haven assets, bringing buyers back into the market. While gold remains well supported on dips and trade risks are a positive factor, the short-term outlook is slightly overbought, suggesting some consolidation may occur. Resistance is at $3,400 and $3,450, with support at $3,300 and $3,250.

Crude Oil

Crude oil briefly moved above the $70 resistance level midweek after stronger-than-expected U.S. GDP data boosted expectations for oil demand. However, sentiment quickly shifted as President Trump announced increased tariffs on Canada and other countries, and weaker U.S. employment data triggered aggressive selling, pushing prices back toward the middle of the recent range. Ongoing tariff concerns may limit further upside, and with strong support holding around $65, range trading remains the most effective strategy for now. Resistance is seen at $70, $75, and $80, while support continues to hold at $65 and $60.

Bitcoin

Bitcoin dropped every day over the past five days, making it the worst 5-day stretch since June. Ongoing debate in the U.S. government about how to regulate crypto has created uncertainty, causing big investors to pull back. The Federal Reserve delaying interest rate cuts also hurt Bitcoin, since it tends to do better when rates are expected to fall. Selling picked up after President Trump announced new tariffs and weak U.S. jobs data added to market worries. In the short term, prices may fall further, but the market looks oversold, so short-term traders might find chances to buy if prices start to bounce. Medium-term investors may want to wait until there’s more clarity on U.S. trade policy and the economy. Resistance is at $120,000, $125,000, and $150,000, with support at $112,000, $110,000, and $105,000.

This Week’s Focus

- Monday: U.S. Factory Orders

- Tuesday: Japan Monetary Policy Meeting Minutes, Japan au Jibun Bank Services PMI, E.U. HCOB Eurozone Composite PMI, U.K. S&P Global Composite PMI, U.S. Trade Balance, U.S. S&P Global Services PMI, U.S. ISM Non-Manufacturing PMI

- Wednesday: U.K. S&P Global Construction PMI

- Thursday: Australia Building Approvals, Australia Trade Balance, U.K. BoE Interest Rate Decision, U.S. Jobless Claims

- Friday: Japan Household Spending, Japan Current Account

This week could bring more sharp market moves, even though the economic calendar is relatively light. The main scheduled event is the Bank of England meeting on Thursday, where a 0.25% rate cut is widely expected. PMI data from several major economies will also be released, offering clues about global growth. But the bigger focus will be on how markets react to last Friday’s sell-off—whether it signals the beginning of a new trend or was just a short-term move.

U.S. trade policy is likely to dominate sentiment, with President Trump continuing to pressure other countries to negotiate on his terms. Traders will be watching closely for any new headlines or developments on tariffs and trade deals. With uncertainty high and momentum shifting, this could be a volatile week as bulls and bears compete to set the next direction