Sample Category Title

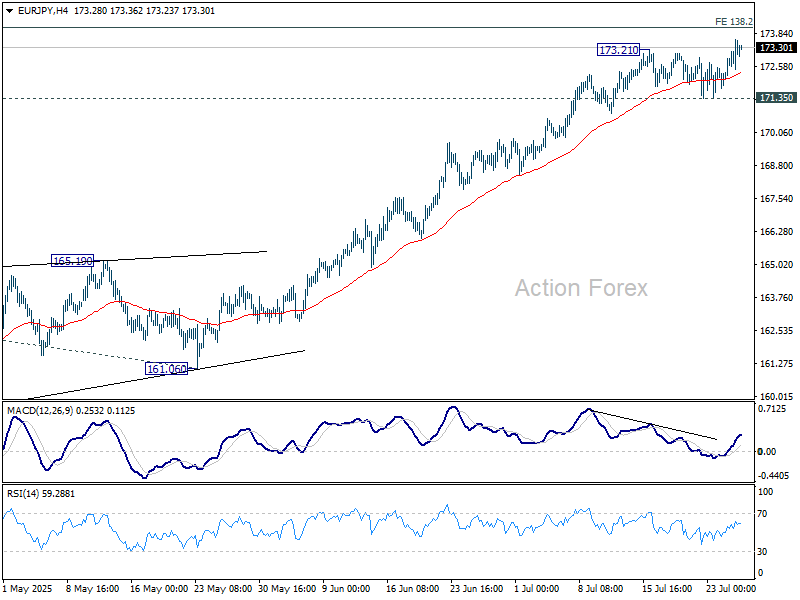

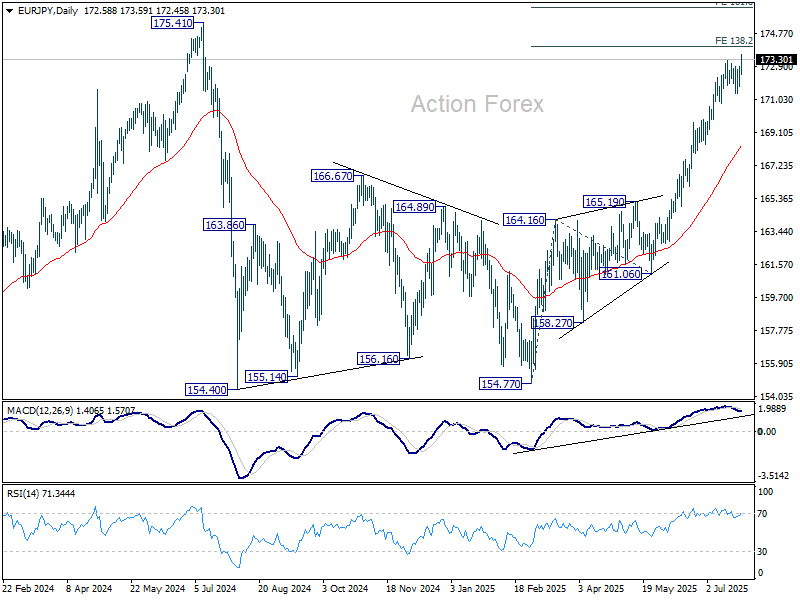

EUR/JPY Weekly Outlook

EUR/JPY's consolidations from 173.21 completed late last week with upside breakout. Initial bias is back on the upside this week for 138.2% projection of 154.77 to 164.16 from 161.06 at 174.03. Break there will bring retest of 175.41 high. For now, near term outlook will remain bullish as long as 171.35 support holds, in case of retreat.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break there will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 168.37) will delay this bullish case.

In the long term picture, up trend fro 94.11 (2021 low) is still in progress. On resumption, next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32.

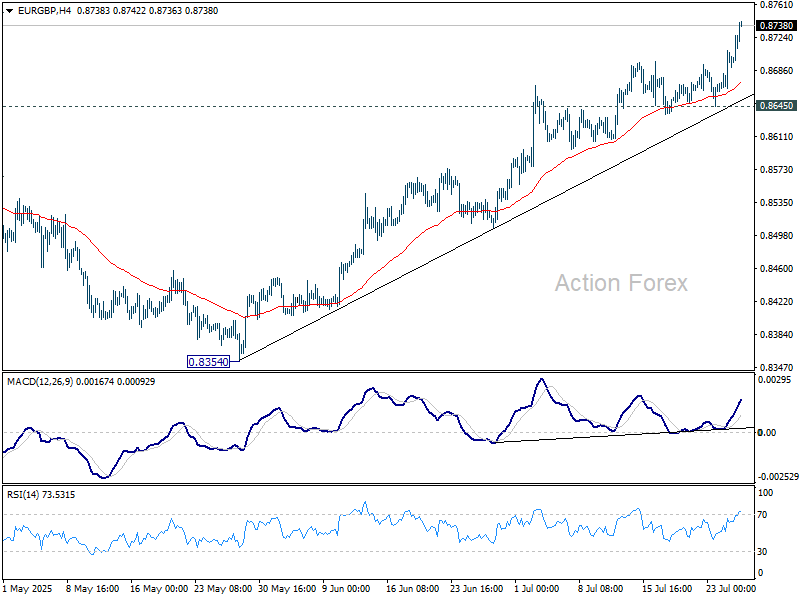

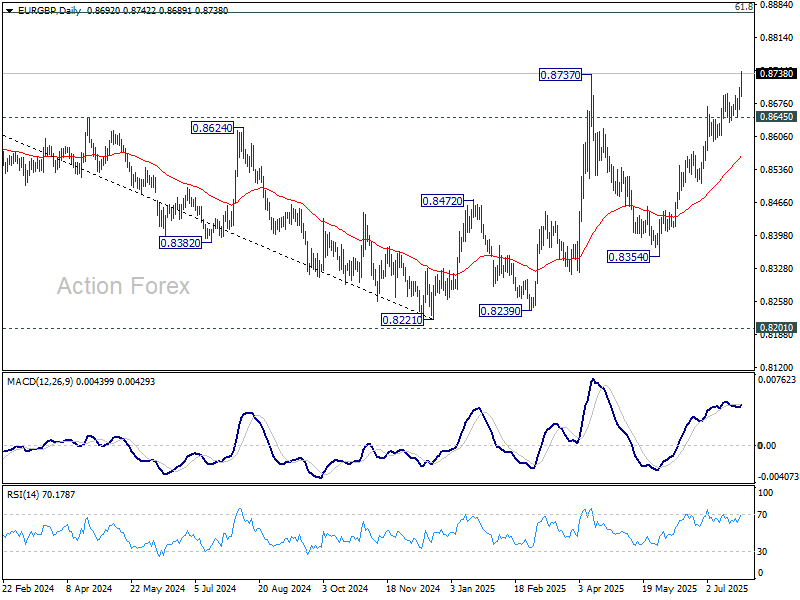

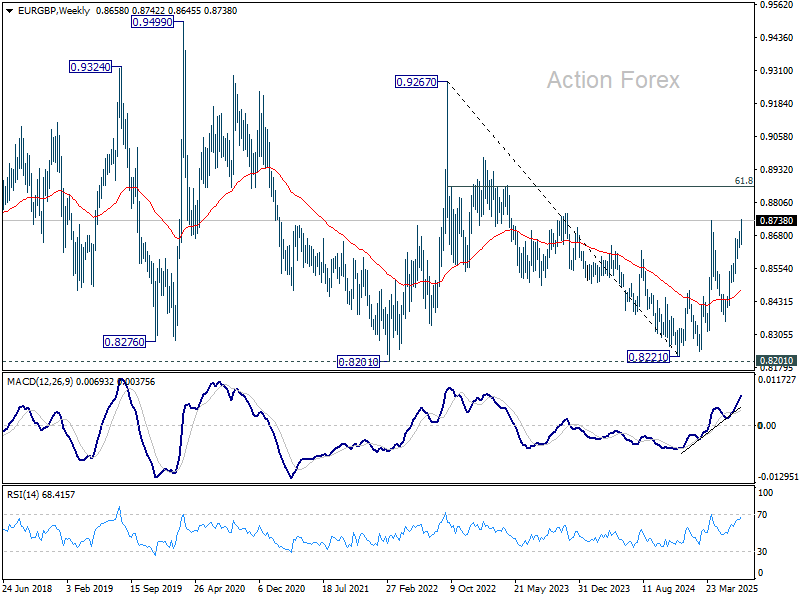

EUR/GBP Weekly Outlook

EUR/GBP's rally from 0.8354 continued last week and breached 0.8737 resistance before closing strongly. Initial bias stays on the upside this week. Sustained trading above 0.8737 will resume the whole rise from 0.8221. Next target is 0.8867 fibonacci level. For now, outlook will stay bullish as long as 0.8645 support holds, in case of retreat.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8476) holds.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

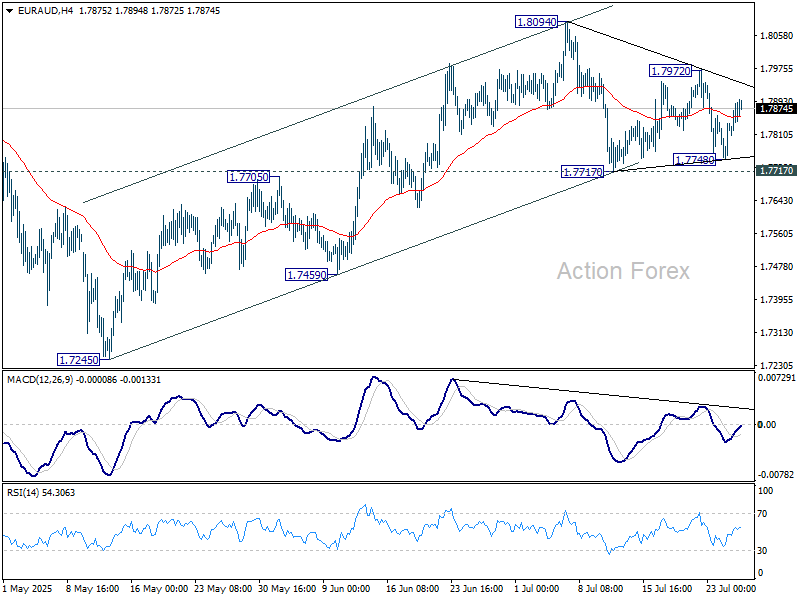

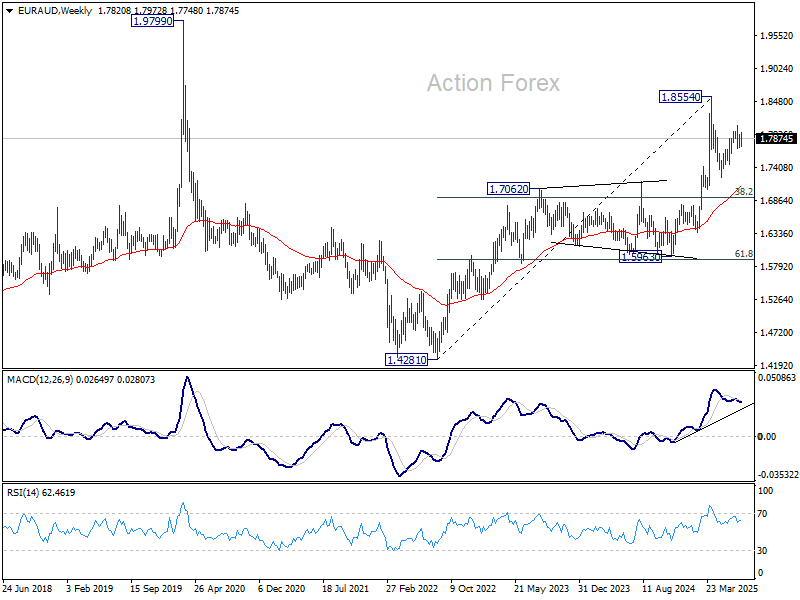

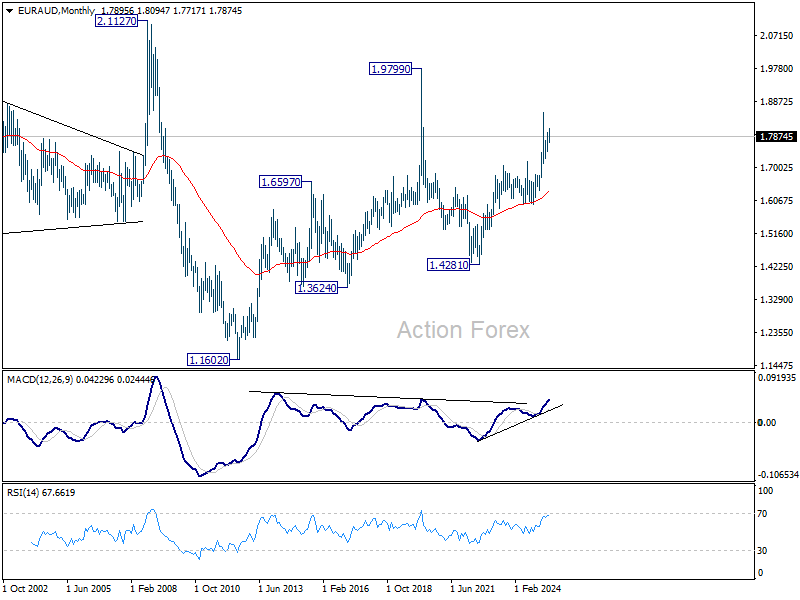

EUR/AUD Weekly Outlook

EUR/AUD's rebound was limited well below 1.8094 resistance as sideway trading extended. Initial bias remains neutral this week first, and further rally is expected as long as 1.7717 support holds. On the upside, above 1.7972 will bring retest of 1.8094. Firm break there will resume the rise from 1.7245 to towards 1.8554 high. However, break of 1.7717 support will revive the case that rise from 1.7245 has completed. Corrective pattern from 1.8554 should have then started the third leg.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. While deeper pullback might be seen, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is expected to resume at a later stage.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6365) holds, this second leg could still extend higher.

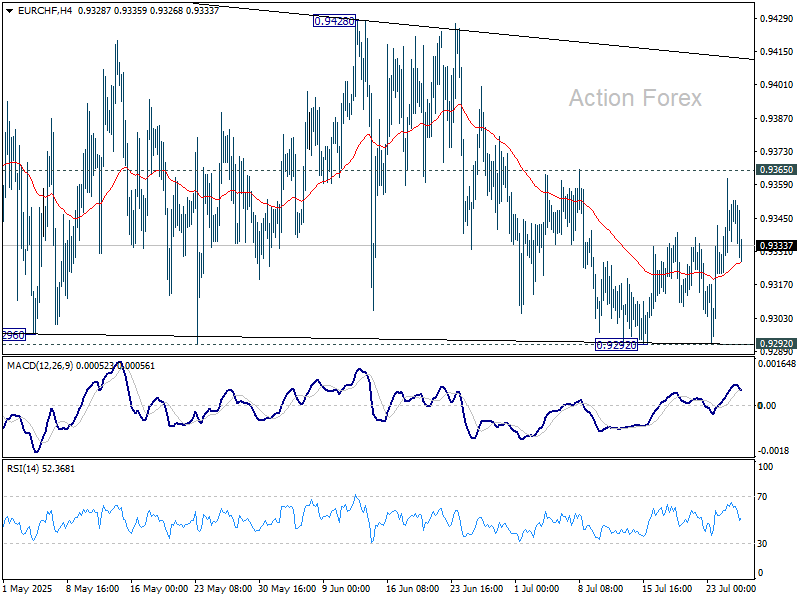

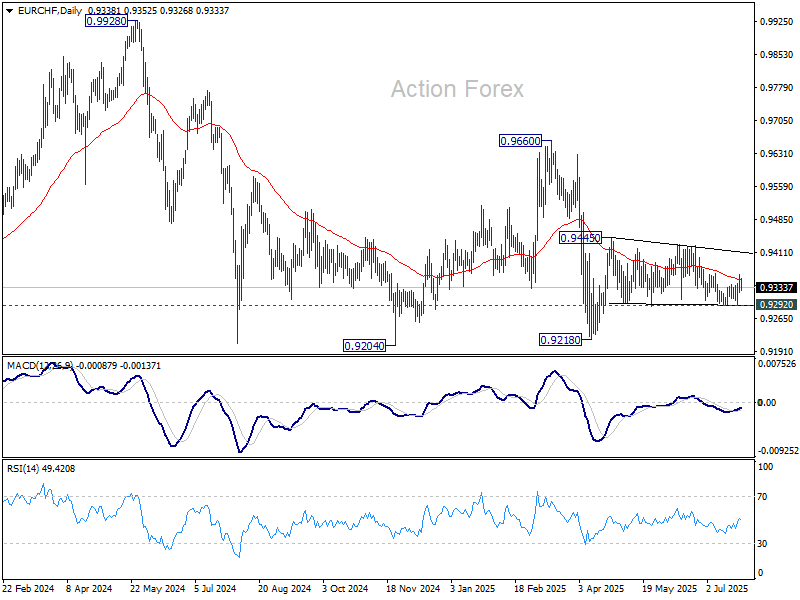

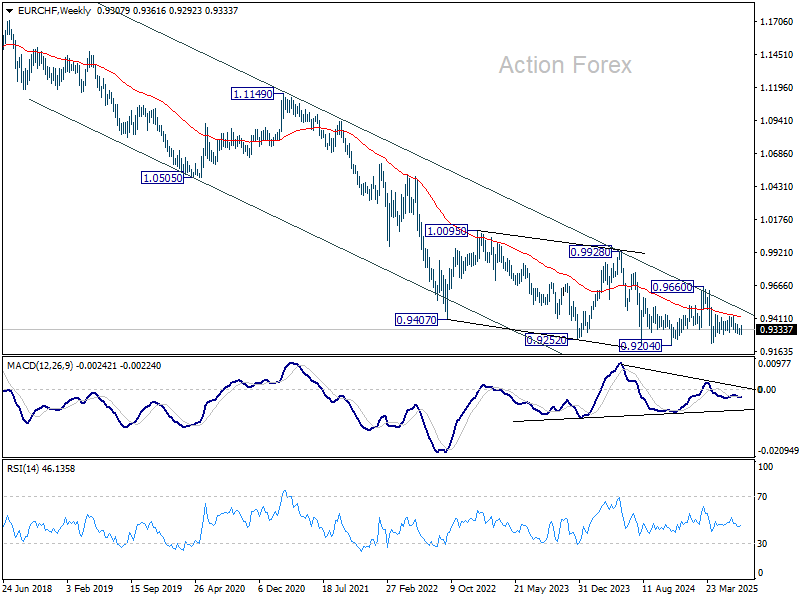

EUR/CHF Weekly Outlook

EUR/CHF bounced after dipping to 0.9292 last week but lost momentum ahead of 0.9365 resistance. Initial bias stays neutral this week first. On the upside, firm break of 0.9365 will be he first sign that corrective pattern from 0.9445 has already completed. Further rise should then be seen to 0.9428/45 resistance zone. Firm break there will resume the rebound from 0.9218 low. However, firm break of 0.9292 will bring retest of 0.9218 instead.

In the bigger picture, while downside momentum has been diminishing as seen in W MACD, there is no sign of bottoming yet. EUR/CHF is still staying below 55 W EMA (now at 0.9424) and well inside long term falling channel. Outlook will stay bearish as long as 0.9660 resistance holds. Break of 0.9204 (2024 low) will confirm resumption of down trend from 1.2004 (2018 high).

In the long term picture, overall long term down trend is still in progress in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9877) holds.

Summary 7/28 – 8/1

Monday, Jul 28, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 10:00 | GBP | CBI Realized Sales Jul | -28 | -46 |

| 23:01 | GBP | BRC Shop Price Index Y/Y Jul | 0.20% | 0.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 10:00 | GBP | CBI Realized Sales Jul | |

| Forecast: -28 | Previous: -46 | ||

| 23:01 | GBP | BRC Shop Price Index Y/Y Jul | |

| Forecast: 0.20% | Previous: 0.40% | ||

Tuesday, Jul 29, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 08:30 | GBP | M4 Money Supply M/M Jun | 0.30% | 0.20% |

| 08:30 | GBP | Mortgage Approvals Jun | 63K | 63K |

| 12:30 | USD | Goods Trade Balance (USD) Jun P | -98.3B | -96.4B |

| 12:30 | USD | Wholesale Inventories Jun P | -0.10% | -0.30% |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y May | 2.90% | 3.40% |

| 13:00 | USD | Housing Price Index M/M May | -0.20% | -0.40% |

| 14:00 | USD | Consumer Confidence Jul | 95.9 | 93 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 08:30 | GBP | M4 Money Supply M/M Jun | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 08:30 | GBP | Mortgage Approvals Jun | |

| Forecast: 63K | Previous: 63K | ||

| 12:30 | USD | Goods Trade Balance (USD) Jun P | |

| Forecast: -98.3B | Previous: -96.4B | ||

| 12:30 | USD | Wholesale Inventories Jun P | |

| Forecast: -0.10% | Previous: -0.30% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y May | |

| Forecast: 2.90% | Previous: 3.40% | ||

| 13:00 | USD | Housing Price Index M/M May | |

| Forecast: -0.20% | Previous: -0.40% | ||

| 14:00 | USD | Consumer Confidence Jul | |

| Forecast: 95.9 | Previous: 93 | ||

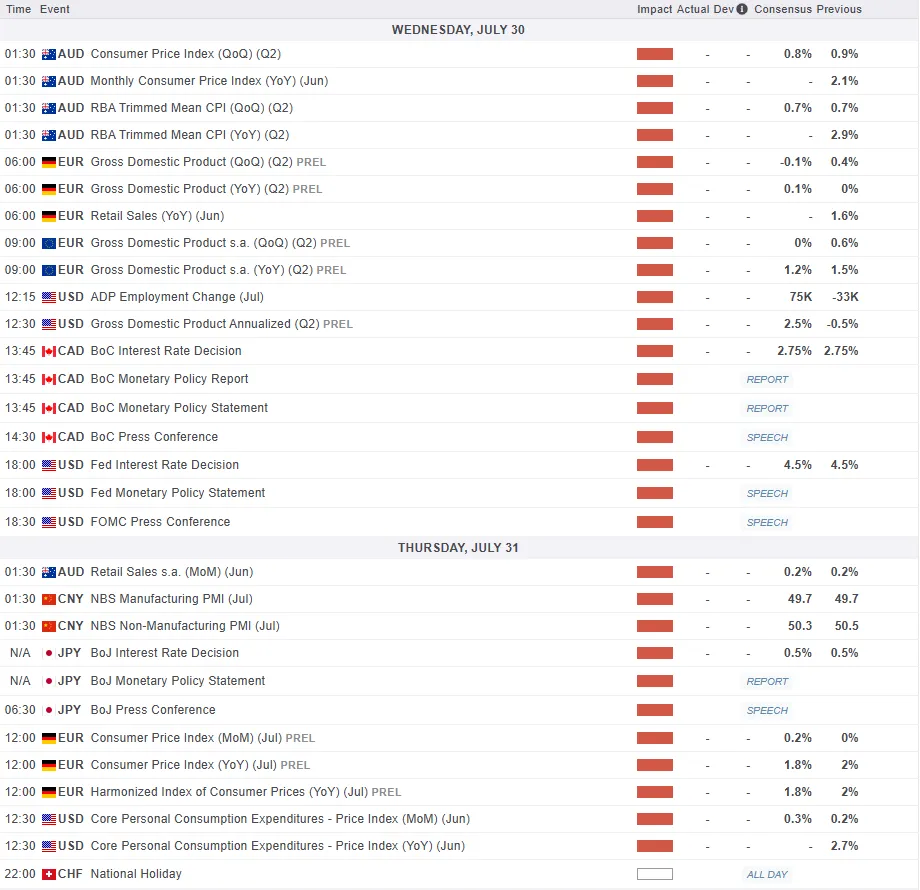

Wednesday, Jul 30, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Jul | 46.3 | |

| 01:00 | NZD | ANZ Activity Outlook Jul | 40.9 | |

| 01:30 | AUD | Monthly CPI Y/Y Jun | 2.10% | 2.10% |

| 01:30 | AUD | CPI Q/Q Q2 | 0.80% | 0.90% |

| 01:30 | AUD | CPI Y/Y Q2 | 2.20% | 2.40% |

| 01:30 | AUD | Trimmed Mean CPI Q/Q Q2 | 0.70% | 0.70% |

| 01:30 | AUD | Trimmed Mean CPI Y/Y Q2 | 2.90% | |

| 05:30 | EUR | France Consumer Spending M/M Jun | -0.30% | 0.20% |

| 05:30 | EUR | France GDP Q/Q Q2 P | 0.10% | 0.10% |

| 06:00 | EUR | Germany Retail Sales M/M Jun | 0.50% | -1.60% |

| 06:00 | EUR | Germany GDP Q/Q Q2 P | -0.10% | 0.40% |

| 08:00 | CHF | UBS Economic Expectations Jul | -2.1 | |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 0.00% | 0.60% |

| 09:00 | EUR | Eurozone Economic Sentiment Jul | 94.8 | 94 |

| 09:00 | EUR | Eurozone Industrial Confidence Jul | -11 | -12 |

| 09:00 | EUR | Eurozone Consumer Confidence Jul | -14.7 | -14.7 |

| 09:00 | EUR | Eurozone Services Sentiment Jul | 3.4 | 2.9 |

| 12:15 | USD | ADP Employment Change Jul | 75K | -33K |

| 12:30 | USD | GDP Annualized Q2 P | 2.40% | -0.50% |

| 12:30 | USD | GDP Price Index Q2 P | 2.30% | 3.80% |

| 13:45 | CAD | BoC Interest Rate Decision | 2.75% | 2.75% |

| 14:00 | USD | Pending Home Sales M/M Jun | 0.30% | 1.80% |

| 14:30 | CAD | BoC Press Conference | ||

| 14:30 | USD | Crude Oil Inventories | -3.2M | |

| 18:00 | USD | Fed Interest Rate Decision | 4.50% | 4.50% |

| 18:30 | USD | FOMC Press Conference | ||

| 23:50 | JPY | Industrial Production M/M Jun P | -0.70% | -0.10% |

| 23:50 | JPY | Retail Trade Y/Y Jun | 1.80% | 1.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Jul | |

| Forecast: | Previous: 46.3 | ||

| 01:00 | NZD | ANZ Activity Outlook Jul | |

| Forecast: | Previous: 40.9 | ||

| 01:30 | AUD | Monthly CPI Y/Y Jun | |

| Forecast: 2.10% | Previous: 2.10% | ||

| 01:30 | AUD | CPI Q/Q Q2 | |

| Forecast: 0.80% | Previous: 0.90% | ||

| 01:30 | AUD | CPI Y/Y Q2 | |

| Forecast: 2.20% | Previous: 2.40% | ||

| 01:30 | AUD | Trimmed Mean CPI Q/Q Q2 | |

| Forecast: 0.70% | Previous: 0.70% | ||

| 01:30 | AUD | Trimmed Mean CPI Y/Y Q2 | |

| Forecast: | Previous: 2.90% | ||

| 05:30 | EUR | France Consumer Spending M/M Jun | |

| Forecast: -0.30% | Previous: 0.20% | ||

| 05:30 | EUR | France GDP Q/Q Q2 P | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 06:00 | EUR | Germany Retail Sales M/M Jun | |

| Forecast: 0.50% | Previous: -1.60% | ||

| 06:00 | EUR | Germany GDP Q/Q Q2 P | |

| Forecast: -0.10% | Previous: 0.40% | ||

| 08:00 | CHF | UBS Economic Expectations Jul | |

| Forecast: | Previous: -2.1 | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | |

| Forecast: 0.00% | Previous: 0.60% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Jul | |

| Forecast: 94.8 | Previous: 94 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Jul | |

| Forecast: -11 | Previous: -12 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Jul | |

| Forecast: -14.7 | Previous: -14.7 | ||

| 09:00 | EUR | Eurozone Services Sentiment Jul | |

| Forecast: 3.4 | Previous: 2.9 | ||

| 12:15 | USD | ADP Employment Change Jul | |

| Forecast: 75K | Previous: -33K | ||

| 12:30 | USD | GDP Annualized Q2 P | |

| Forecast: 2.40% | Previous: -0.50% | ||

| 12:30 | USD | GDP Price Index Q2 P | |

| Forecast: 2.30% | Previous: 3.80% | ||

| 13:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 2.75% | Previous: 2.75% | ||

| 14:00 | USD | Pending Home Sales M/M Jun | |

| Forecast: 0.30% | Previous: 1.80% | ||

| 14:30 | CAD | BoC Press Conference | |

| Forecast: | Previous: | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -3.2M | ||

| 18:00 | USD | Fed Interest Rate Decision | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 18:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Industrial Production M/M Jun P | |

| Forecast: -0.70% | Previous: -0.10% | ||

| 23:50 | JPY | Retail Trade Y/Y Jun | |

| Forecast: 1.80% | Previous: 1.90% | ||

Thursday, Jul 31, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | 0.50% | 0.50% | |

| 01:30 | AUD | Retail Sales M/M Jun | 0.40% | 0.20% |

| 01:30 | AUD | Private Sector Credit M/M Jun | 0.50% | 0.50% |

| 01:30 | AUD | Import Price Index Q/Q Q2 | -0.30% | 3.30% |

| 01:30 | AUD | Building Permits M/M Jun | 1.90% | 3.20% |

| 01:30 | CNY | NBS Manufacturing PMI Jul | 49.7 | 49.7 |

| 01:30 | CNY | NBS Non-Manufacturing PMI Jul | 50.3 | 50.5 |

| 01:30 | AUD | Building Permits Y/Y Jun | 6.50% | |

| 05:00 | JPY | Housing Starts Y/Y Jun | -34.40% | |

| 05:00 | JPY | Construction Orders Y/Y Jun | -16.30% | 14% |

| 05:00 | JPY | Consumer Confidence Index Jul | 35.2 | 34.5 |

| 06:00 | EUR | Germany Import Price Index M/M Jun | -0.20% | -0.70% |

| 06:30 | CHF | Real Retail Sales Y/Y Jun | 0.20% | 0.00% |

| 07:00 | CHF | KOF Leading Indicator Jul | 96.1 | |

| 07:55 | EUR | Germany Unemployment Change Jun | 15K | 11K |

| 07:55 | EUR | Germany Unemployment Rate Jun | 6.40% | 6.30% |

| 09:00 | EUR | Eurozone Unemployment Rate Jun | 6.30% | 6.30% |

| 12:00 | EUR | Germany CPI M/M Jul P | 0.20% | 0.00% |

| 12:00 | EUR | Germany CPI Y/Y Jul P | 1.80% | 2.00% |

| 12:30 | CAD | GDP M/M May | -0.10% | -0.10% |

| 12:30 | USD | Initial Jobless Claims (Jul 25) | 220K | 217K |

| 12:30 | USD | Personal Income M/M Jun | 0.20% | -0.40% |

| 12:30 | USD | Personal Spending Jun | 0.40% | -0.10% |

| 12:30 | USD | PCE Price Index M/M Jun | 0.30% | 0.10% |

| 12:30 | USD | PCE Price Index Y/Y Jun | 2.30% | |

| 12:30 | USD | Core PCE Price Index M/M Jun | 0.30% | 0.20% |

| 12:30 | USD | Core PCE Price Index Y/Y Jun | 2.70% | |

| 12:30 | USD | Employment Cost Index Q2 | 0.80% | 0.90% |

| 13:45 | USD | Chicago PMI Jul | 41.2 | 40.4 |

| 14:30 | USD | Natural Gas Storage | 23B | |

| 22:45 | NZD | Building Permits M/M Jun | 10.40% | |

| 23:30 | JPY | Unemployment Rate Jun | 2.50% | 2.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: 0.50% | Previous: 0.50% | ||

| 01:30 | AUD | Retail Sales M/M Jun | |

| Forecast: 0.40% | Previous: 0.20% | ||

| 01:30 | AUD | Private Sector Credit M/M Jun | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 01:30 | AUD | Import Price Index Q/Q Q2 | |

| Forecast: -0.30% | Previous: 3.30% | ||

| 01:30 | AUD | Building Permits M/M Jun | |

| Forecast: 1.90% | Previous: 3.20% | ||

| 01:30 | CNY | NBS Manufacturing PMI Jul | |

| Forecast: 49.7 | Previous: 49.7 | ||

| 01:30 | CNY | NBS Non-Manufacturing PMI Jul | |

| Forecast: 50.3 | Previous: 50.5 | ||

| 01:30 | AUD | Building Permits Y/Y Jun | |

| Forecast: | Previous: 6.50% | ||

| 05:00 | JPY | Housing Starts Y/Y Jun | |

| Forecast: | Previous: -34.40% | ||

| 05:00 | JPY | Construction Orders Y/Y Jun | |

| Forecast: -16.30% | Previous: 14% | ||

| 05:00 | JPY | Consumer Confidence Index Jul | |

| Forecast: 35.2 | Previous: 34.5 | ||

| 06:00 | EUR | Germany Import Price Index M/M Jun | |

| Forecast: -0.20% | Previous: -0.70% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Jun | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 07:00 | CHF | KOF Leading Indicator Jul | |

| Forecast: | Previous: 96.1 | ||

| 07:55 | EUR | Germany Unemployment Change Jun | |

| Forecast: 15K | Previous: 11K | ||

| 07:55 | EUR | Germany Unemployment Rate Jun | |

| Forecast: 6.40% | Previous: 6.30% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Jun | |

| Forecast: 6.30% | Previous: 6.30% | ||

| 12:00 | EUR | Germany CPI M/M Jul P | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 12:00 | EUR | Germany CPI Y/Y Jul P | |

| Forecast: 1.80% | Previous: 2.00% | ||

| 12:30 | CAD | GDP M/M May | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 25) | |

| Forecast: 220K | Previous: 217K | ||

| 12:30 | USD | Personal Income M/M Jun | |

| Forecast: 0.20% | Previous: -0.40% | ||

| 12:30 | USD | Personal Spending Jun | |

| Forecast: 0.40% | Previous: -0.10% | ||

| 12:30 | USD | PCE Price Index M/M Jun | |

| Forecast: 0.30% | Previous: 0.10% | ||

| 12:30 | USD | PCE Price Index Y/Y Jun | |

| Forecast: | Previous: 2.30% | ||

| 12:30 | USD | Core PCE Price Index M/M Jun | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Jun | |

| Forecast: | Previous: 2.70% | ||

| 12:30 | USD | Employment Cost Index Q2 | |

| Forecast: 0.80% | Previous: 0.90% | ||

| 13:45 | USD | Chicago PMI Jul | |

| Forecast: 41.2 | Previous: 40.4 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 23B | ||

| 22:45 | NZD | Building Permits M/M Jun | |

| Forecast: | Previous: 10.40% | ||

| 23:30 | JPY | Unemployment Rate Jun | |

| Forecast: 2.50% | Previous: 2.50% | ||

Friday, Aug 1, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | PPI Q/Q Q2 | 0.90% | |

| 01:30 | AUD | PPI Y/Y Q2 | 3.70% | |

| 01:45 | CNY | Caixin Manufacturing PMI Jul | 50.2 | 50.4 |

| 07:50 | EUR | France Manufacturing PMI Jul F | 48.4 | 48.4 |

| 07:55 | EUR | Germany Manufacturing PMI Jul F | 49.2 | 49.2 |

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | 49.8 | 49.8 |

| 08:30 | GBP | Manufacturing PMI Jul | 48.2 | 48.2 |

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | 1.90% | 2.00% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | 2.30% | 2.30% |

| 12:30 | USD | Nonfarm Payrolls Jul | 102K | 147K |

| 12:30 | USD | Unemployment Rate Jul | 4.20% | 4.10% |

| 12:30 | USD | Average Hourly Earnings M/M Jul | 0.30% | 0.20% |

| 13:30 | CAD | Manufacturing PMI Jul | 45.6 | |

| 13:45 | USD | Manufacturing PMI Jul F | 49.5 | 49.5 |

| 14:00 | USD | ISM Manufacturing PMI Jul | 49.6 | 49 |

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | 66.5 | 69.7 |

| 14:00 | USD | ISM Manufacturing Employment Index Jul | 45 | |

| 14:00 | USD | UoM Consumer Sentiment Jul F | 61.8 | 61.8 |

| 14:00 | USD | UoM 1-year Inflation Expectations Jul F | 4.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | PPI Q/Q Q2 | |

| Forecast: | Previous: 0.90% | ||

| 01:30 | AUD | PPI Y/Y Q2 | |

| Forecast: | Previous: 3.70% | ||

| 01:45 | CNY | Caixin Manufacturing PMI Jul | |

| Forecast: 50.2 | Previous: 50.4 | ||

| 07:50 | EUR | France Manufacturing PMI Jul F | |

| Forecast: 48.4 | Previous: 48.4 | ||

| 07:55 | EUR | Germany Manufacturing PMI Jul F | |

| Forecast: 49.2 | Previous: 49.2 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | |

| Forecast: 49.8 | Previous: 49.8 | ||

| 08:30 | GBP | Manufacturing PMI Jul | |

| Forecast: 48.2 | Previous: 48.2 | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | |

| Forecast: 1.90% | Previous: 2.00% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | |

| Forecast: 2.30% | Previous: 2.30% | ||

| 12:30 | USD | Nonfarm Payrolls Jul | |

| Forecast: 102K | Previous: 147K | ||

| 12:30 | USD | Unemployment Rate Jul | |

| Forecast: 4.20% | Previous: 4.10% | ||

| 12:30 | USD | Average Hourly Earnings M/M Jul | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 13:30 | CAD | Manufacturing PMI Jul | |

| Forecast: | Previous: 45.6 | ||

| 13:45 | USD | Manufacturing PMI Jul F | |

| Forecast: 49.5 | Previous: 49.5 | ||

| 14:00 | USD | ISM Manufacturing PMI Jul | |

| Forecast: 49.6 | Previous: 49 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | |

| Forecast: 66.5 | Previous: 69.7 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jul | |

| Forecast: | Previous: 45 | ||

| 14:00 | USD | UoM Consumer Sentiment Jul F | |

| Forecast: 61.8 | Previous: 61.8 | ||

| 14:00 | USD | UoM 1-year Inflation Expectations Jul F | |

| Forecast: | Previous: 4.40% | ||

Markets Weekly Outlook – US Data Dump, Earnings Season and Trade Deals

Week in review: Trade Deals Materialize

The August 1 tariff deadline approaches and with it we have had a few trade deal announcements which came out this week. Market sentiment seemed to get a boost, with Gold in particular feeling the heat of a stronger US Dollar.

Market participants remain at least partially on the edge of their seats as we have not seen any details of agreements as yet. This led to early signs of cracks in potential trade deals with the US announcing a Japan trade deal which included significant investments in the US.

However, Japanese officials and US officials seem to have differing views of the deal with Japanese officials stating that the US will secure only 90 per cent of profits from joint investments with Japan if it takes on a proportional amount of risk and financing. This seems to suggest that cracks may be present in the two allies’ interpretation of their hastily agreed trade deal.

Japanese officials further stressed there was no written agreement with Washington & no legally binding one would be drawn up after Trump administration officials claimed Tokyo would back investments in the US from which American taxpayers would reap nine-tenths of the profits.

Wall Street and the dollar strengthened on Friday as investors prepared for the upcoming week. All three major indexes were slightly up in early trading and set to end the week with gains.

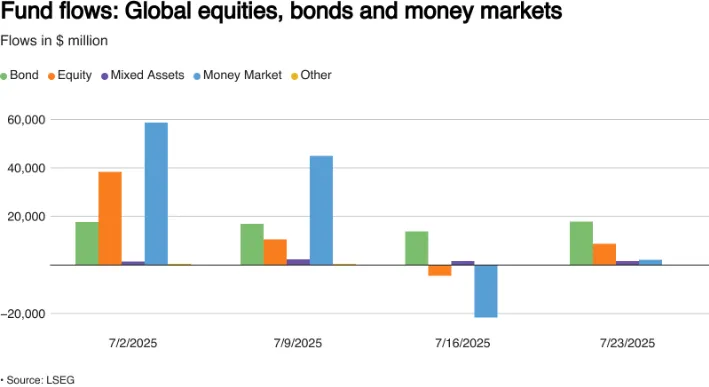

The week also saw global investors snap up a net $8.71 billion worth of equity funds during the week, reversing a $4.4 billion net withdrawal in the prior week, data from LSEG Lipper showed.

Source: LSEG

With just a week left before Trump's trade deadline, the US and its partners are rushing to finalize deals. European negotiators are optimistic after the trade agreement with Japan earlier this week.

The dollar strengthened but is still set for its biggest monthly drop as investors focus on upcoming trade talks and central bank meetings.

The dollar index rose 0.28% to 97.72, while the euro fell 0.2% to $1.173. Against the yen, the dollar gained 0.4%, reaching 147.57.

In cryptocurrencies, bitcoin dropped 3.08% to $115,133.22, and Ethereum fell 2.63% to $3,641.43.

Oil prices dipped as investors considered global demand and a possible supply increase from Venezuela. US crude fell 0.56% to $65.63 per barrel, and Brent dropped 0.39% to $68.91.

Gold prices also declined as the stronger dollar and optimism over US-EU trade talks reduced demand for the safe-haven metal. Spot gold fell 0.93% to $3,336.52 an ounce.

Earnings Season

Over a third of S&P 500 companies have reported earnings, with 80% beating expectations, according to LSEG data.

Analysts now predict second-quarter earnings will grow 7.7% compared to the 5.8% estimate from July 1.

Next week, four big tech companies Amazon, Apple, Meta, and Microsoft will release their earnings. Investors will closely watch their updates to see if spending on AI is delivering results and if trade tariffs are still affecting their future plans.

The Week Ahead: US Very Much in Focus, Fed Decision, Trade Deals and Earnings

The week ahead has several important data releases lined up. The US and UK will release inflation data with key GDP data from China and manufacturing data from Japan.

Asia Pacific Markets - US/China Trade Talks

The key focus this week is the US-China trade talks in Sweden. A 90-day tariff ceasefire, which started in May, is set to end on August 12. Markets are watching closely to see if the ceasefire will be extended or if there will be changes to current tariffs. An agreement is expected, but uncertainty remains despite President Trump's claims that a framework is in place.

On the data front, China's official July PMI (out Thursday) is expected to stay in contraction at 49.6. The S&P PMI (focused on private and export-driven firms) will follow on Friday. Over the weekend, June industrial profits data will be released. After a sharp drop in May, markets are eager to see if profits recover due to eased trade tensions or if the decline continues.

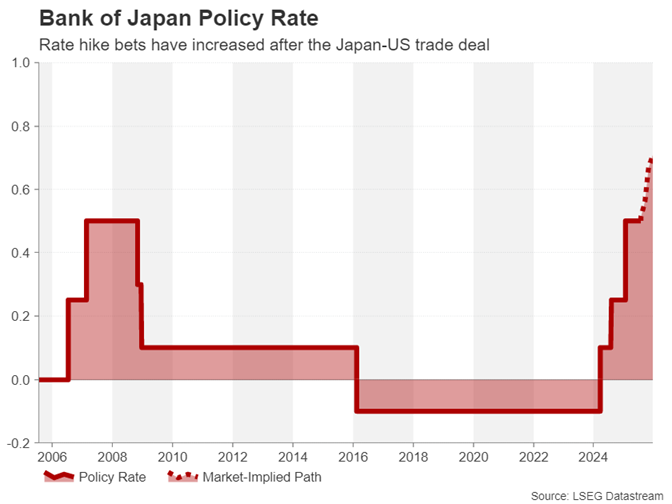

The Bank of Japan (BoJ) is not expected to make any changes at its meeting on July 30-31. However, markets will pay attention to the BoJ's updated economic outlook. The recent US-Japan trade deal has reduced uncertainty, which may ease pressure on the BoJ. If inflation forecasts are raised, it could give clues about future interest rates. On the downside, weak industrial production data for June may hurt growth, but this could be balanced by a rebound in retail sales.

Economic Data from Europe, UK and the US

The US will be a key focus next week thanks to a data dump and of course trade deal announcements.

On Wednesday, we will get 2nd quarter GDP data which I expect to grow 3.3% (above the 2.5% forecast), driven by strong trade and investment. However, consumer spending, a key growth driver, has slowed since late 2024 due to tariff concerns and economic uncertainty.

This will be followed by the Fed rate decision later in the day. We obviously have the ongoing attacks at Fed Chair Jerome Powell by US President Trump and his administration. However, this is unlikely to sway the Fed at this stage as they are likely to adopt a wait and see approach. The economy is slowing but stable. The Fed is unlikely to cut rates now though I could see a 50bp cut in December if inflation eases.

The US data week will end with focus on Jobs data and PCE.

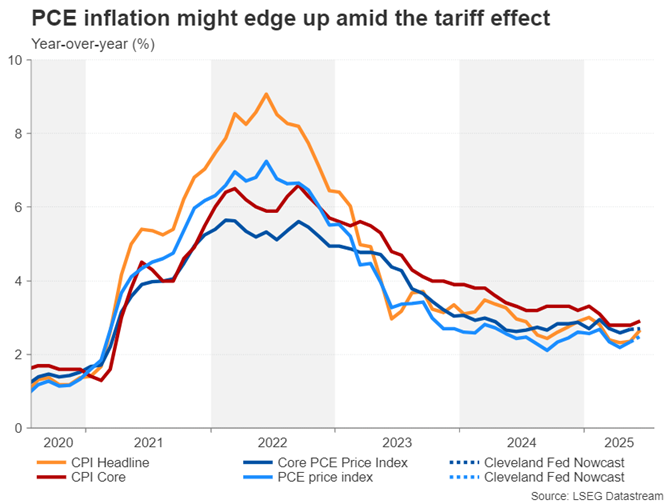

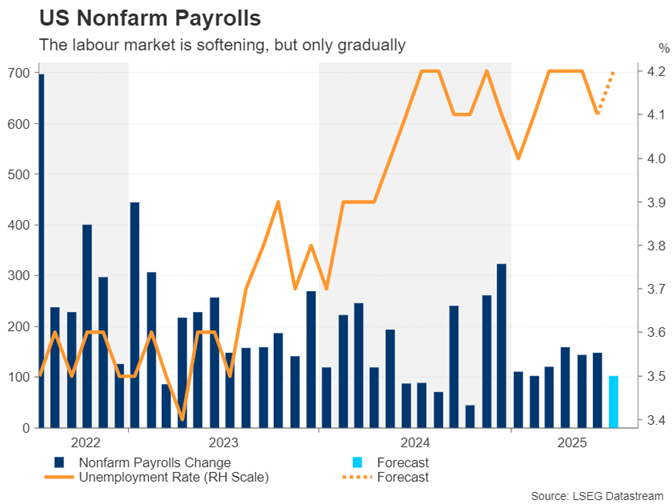

The Fed's preferred inflation measure, the core PCE deflator, is expected to rise 0.3% in June, slightly higher than CPI's 0.2%. NFP data on Friday is expected at 100-120k, with unemployment ticking up to 4.2%.

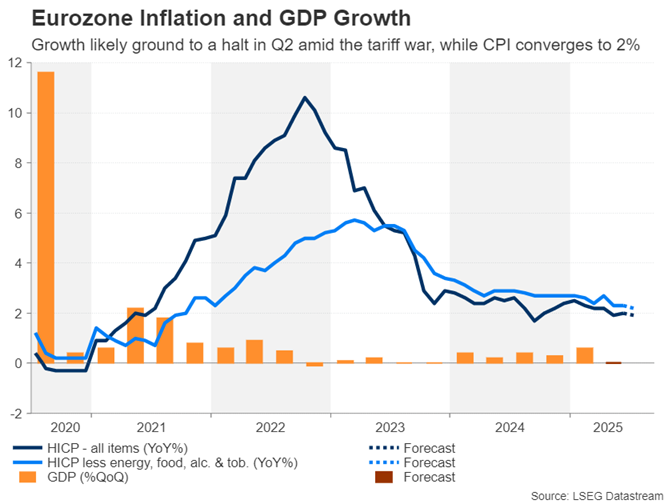

As Europe heads into summer, key eurozone data is due. GDP is expected to slow after a strong 1Q boosted by U.S. trade activity. April saw drops in production and exports, though May had a rebound, especially in pharmaceuticals. Overall, U.S. developments likely hurt eurozone GDP, and weak service sector performance may add to the slowdown.

On Friday we will get Euro Area inflation data. ECB President Lagarde has highlighted stable inflation and steady growth as positives. July's inflation data is expected to stay calm, but the focus will be on the U.S.-EU trade relationship as the August 1 deadline nears.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week - Gold (XAU/USD)

This week's Chart of the week is Gold (XAU/USD).

Gold has shrugged off its early week gains and dropped over a $100 from the weekly highs around the $3440/oz mark.

Looking at the chart below and we have the triangle pattern which appeared to experience a upside breakout earlier in the week before reversing now to test the lower band of the triangle pattern.

Gold has been mixed since making fresh all-time highs in April of $3500/oz with higher highs followed by lower lows. However, the failure this week to take out the most recent swing high at $3451/oz on June 16 may warrant caution for bulls.

A break below the lower end of the triangle pattern would usually be a sign of further downside, however following the false breakout this week, market participants may rightly be slight confused.

If the trendline holds, bulls may return, however if it does give way then the door may be opening for a larger retracement and the $3300 level is the next key spot of support i will pay attention to.

Gold (XAU/USD) Daily Chart - July 25, 2025

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 3300

- 3278

- 3251 (100-day MA)

Resistance

- 3350

- 3400

- 3425

The Weekly Bottom Line: Trade Deals Trickle in Ahead of August 1st

Canadian Highlights

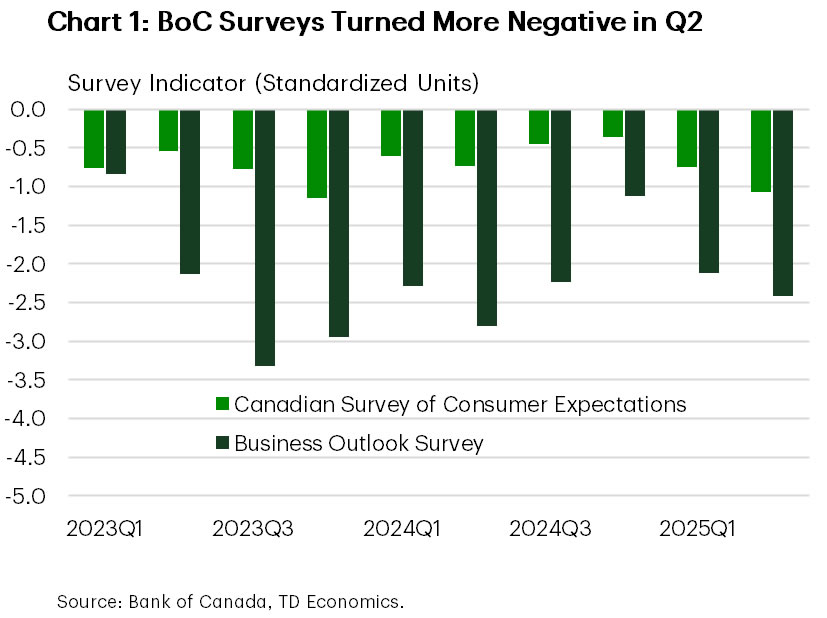

- This week offered a clearer picture of business and consumer sentiment. Both surveys turned more negative in Q2, with domestic demand expected to remain soft and investment outlook flashing a weak signal for Q3.

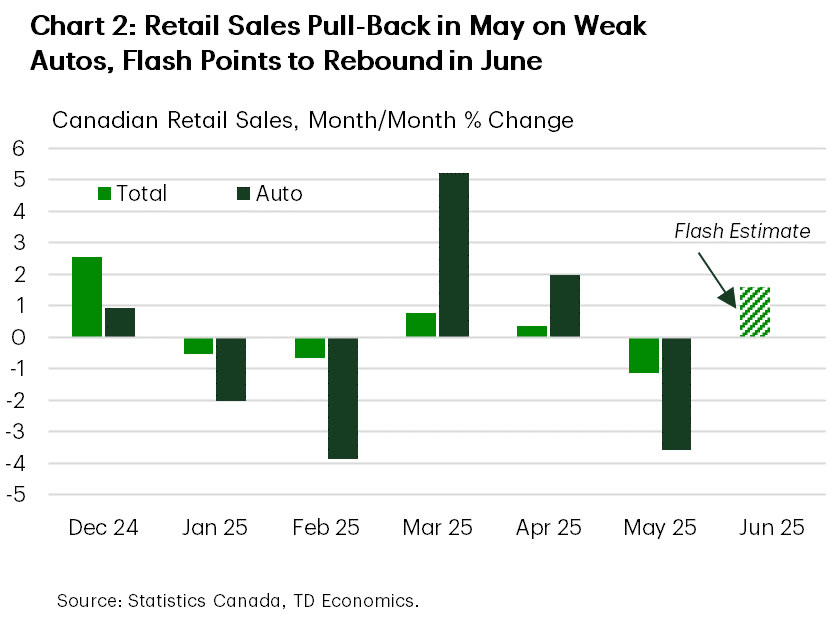

- The retail sales report showed a sharp pull-back in May spending, led by autos. The advance estimate for June suggests a rebound, likely keeping quarterly goods spending steady overall.

- Longer-term consumer inflation expectations ticked slightly higher, though are unlikely to cause much concern for the BoC. July’s rate decision is essentially locked in as a hold – the real question is whether the Bank stays on hold in September and beyond.

U.S. Highlights

- President Trump announced a few trade deals this week, most importantly with Japan. Under this “deal” Japanese imports will still face a 15% “reciprocal” tariff, which is lower than the 25% threatened in the past. The deal included a $550 billion Japanese investment package, but the details remain scarce.

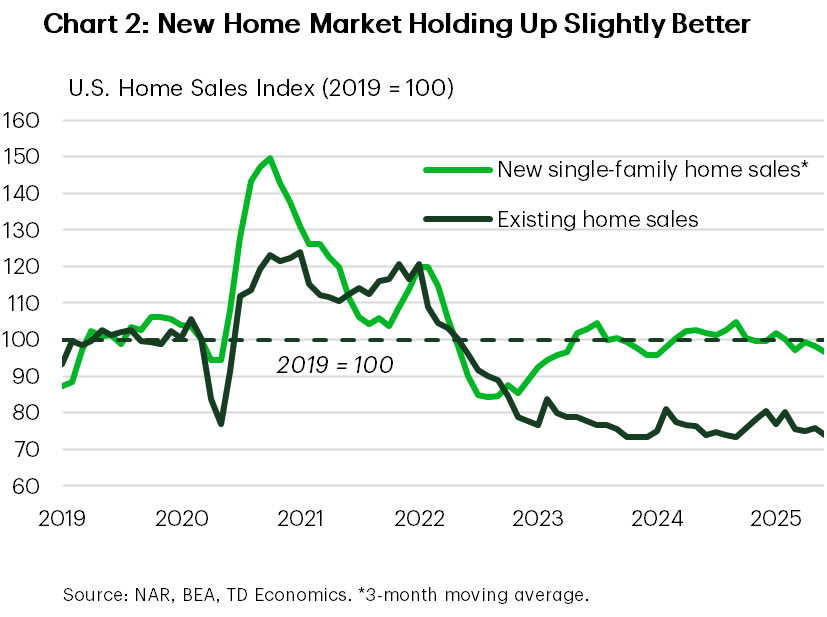

- Existing home sales weakened more than expected in June, with the level of sales holding near GFC lows. However, median home prices rose 2.0% y/y, a slight improvement from the month prior.

Canada – Not Strong Enough to Cheer, Not Weak Enough to Cut

This week’s economic calendar wasn’t expected to move markets. Equity markets drifted higher on optimism around U.S. trade deals, while bond yields edged up modestly after falling for most of the week.

Instead, the data offered a clearer picture of business and consumer sentiment, along with a detailed look at May’s retail spending. Both the business and consumer surveys turned more negative in Q2, reversing the cautious optimism that had emerged late last year (Chart 1). However, the interviews, conducted from late April through May, came after the temporary relief was granted to CUSMA-compliant trade, which helped ease some pressure. Recession fears among firms and households ticked lower, and businesses reported modest improvement in some areas affected by trade.

Despite easing recession fears, the tone from businesses was far from upbeat. Domestic demand is expected to stay soft. Firms’ future sales expectations turned negative for the first time in a year. The outlook for exports sales improved for all but the manufacturing and auto-related sectors. The investment outlook, while slightly better than last quarter, remains well below average and just a quarter of where it stood in late 2024. Even then, most firms are sticking to routine maintenance rather than expanding capacity or improving productivity – a weak signal for the third quarter investment outlook.

On the consumer side, the Bank’s new sentiment index showed a second straight quarterly decline, reflecting slowing spending growth. That was confirmed by May’s retail sales report, which showed nominal spending down 1.1% and inflation-adjusted spending down 1.4% month-on-month. The sharp pull-back was led by auto sales, as the tariff-driven front-loading in March and April reversed course (Chart 2). Core sales, which excludes auto sales and receipts at gas stations, were flat in nominal and real terms. The flash estimate for June sales points to a rebound, which could keep quarterly goods spending steady overall. But services will determine the broader trajectory of personal consumption – and if consumers act on what they are saying in the survey, it will likely remain subdued.

Meanwhile, longer-term consumer inflation expectations ticked slightly higher, though are unlikely to cause much concern for the Bank of Canada. Firms also expect somewhat stronger input costs due to tariffs, though most say that they’ll absorb them through profit margins given weak demand. Services inflation remains the sticking point. According to CMHC, new rents are falling thanks to increased supply. However, existing rent inflation remains elevated, even as it has slowed relative to last year.

In short, the data doesn’t signal a collapse, but it doesn’t suggest strength either. This week’s releases don’t shift the dial for the Bank with July’s rate decision now essentially locked in – the employment report sealed a hold. The real question now is whether it stays on hold in September and beyond. For now, markets are only pricing in half a cut by year-end.

U.S. – Trade Deals Trickle in Ahead of August 1st

This fourth week of July was light on the data front, with only housing data on the docket. Trade developments continued to dominate the limelight, with trade “deals” announced with Japan, the Philippines and Indonesia. Progress on the trade front appeared to prop up financial markets, with the S&P 500 up 1.3% on the week.

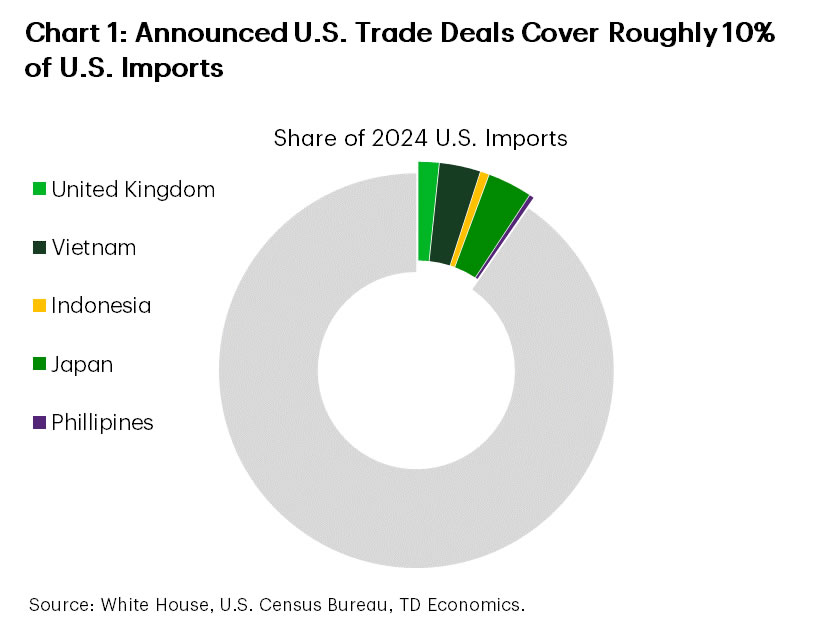

U.S.-Japan goods trade is worth about $227 billion, so a trade deal is certainly a welcome development. Imports from Japan ($148.4 billion last year) will now face a 15% so-called reciprocal tariff, which is lower than the 25% that had been threatened in the past. The deal also reportedly included a $550 billion Japanese investment package, but the fine details on it remain scarce. Shares of Japanese carmakers rose on the news, but the largest American carmakers expressed concern that the deal could put them at a disadvantage. The trade deal with the Philippines received less attention. Imports from the Philippines will face a slightly higher tariff of 19%, slightly higher than the 17% announced on Liberation Day. This adds to a string of recent agreements, including those with the U.K., Vietnam and Indonesia (Chart 1). But the more important ones, such as those with China, Canada, Mexico and the EU, have yet to be reached.

On the data front, the housing market continues to struggle under the weight of high mortgage rates. Existing home sales fell 2.7% m/m in June, coming in well-below expectations for a lighter pullback. Sales were down 8% from the end of last year and at a level of 3.93 million (seasonally adjusted annual rate) continued to hover near GFC lows. The months’ supply of inventory improved slightly, coming in at a seasonally adjusted 4.4 months from 4.3 in May. Amidst this backdrop, home price growth remained in the slow lane, but did see a modest improvement, rising to 2.0% year-on-year (y/y) from 1.6% in the month prior. With mortgage rates holding stubbornly near 7%, we’re unlikely to see a sustained turnaround in resale activity over the near-term. An improved interest rate backdrop expected later this year should help at the margin. High mortgage rates also continue to take a toll on the new home market, even as activity in this small corner of housing is holding up slightly better, with builder incentives likely providing some modest support (Chart 2).

Next week is sure to be more action packed. Aside from the potential for more trade deals to emerge ahead of Trump’s August 1st deadline, a host of important data reports are slated to be released next week. This includes second-quarter GDP, June’s PCE inflation, the July jobs report, and an FOMC rate-setting meeting. Market odds suggest the Fed is all but certain to keep the policy rate unchanged next week. That said, it appears that there will be at least one dissenter among the voters with Fed Gov. Waller recently urging for a July cut, while Fed Gov. Bowman has also expressed her openness to this. Signs of a growing divide within the Fed could lead to more volatility. In this vein, next week’s FOMC decision will be parsed over thoroughly for any of these signs and any potential clues as to how soon the committee could begin cutting rates, with September our current base case.

Weekly Economic & Financial Commentary: How to Finance President Trump’s Agenda?

Summary

United States: Housing Market Enters an Early Winter

- This week’s data highlighted the mounting challenges facing home buyers, sellers and builders. Both existing and new home sales came in below market expectations in June. High rates and economic uncertainty also continued to exert pressure on durable goods orders, which set the stage for a weaker equipment spending print in Q2.

- Next week: GDP (Wed.), Employment (Fri.), ISM Manufacturing (Fri.)

International: European Central Bank Pauses, and So Do Europe's Economies

- The European Central Bank (ECB) held its Deposit Rate steady at 2.00% this week. In the U.K., July PMI data showed modest improvement in the Eurozone. Meanwhile, data reinforced expectations for a 25 bps Bank of England rate cut in August. Finally, Turkey surprised markets with a larger-than-expected 300 bps cut to 43.00%.

- Next week: Australia CPI (Wed.), Bank of Canada Policy Rate (Wed.), Bank of Japan Policy Rate (Thu.)

Interest Rate Watch: How to Finance President Trump's Agenda?

- We do not expect any major policy shifts at the upcoming quarterly refunding announcement from the U.S. Treasury. In our view, Treasury's current coupon auction schedule is well-suited to meet its financing needs for the next few quarters, and any unexpected swings in the government's financing needs can be met by an expansion or contraction in the supply of Treasury bills.

Credit Market Insights: Lending Hesitation Remains but Financial Conditions Ease

- The July Beige Book revealed that credit markets remain subdued, with most Federal Reserve districts reporting flat or modest loan growth. Lending has been affected, as borrowers delay activity in response to elevated risk. Despite these headwinds, financial conditions have eased from their post-tariff lows, suggesting some resilience in the broader economy.

Topic of the Week: If Your Friends Slashed Rates, Wouldn't You?

- Slowing economic growth and softer inflation reports have led many major G10 central banks to ease monetary policy. The Federal Reserve isn't following the same pace, partly due to relatively firmer upside pressures amid more resilient growth and uncertainty over the inflationary impulse of higher tariffs.

Fed Preview: September Cut on the Horizon

- We expect the Fed to maintain its monetary policy unchanged in the July meeting, in line with consensus and market pricing.

- With no new economic projections, all eyes will be on Powell’s remarks. Unclear data will not allow the Fed to pre-commit, but Powell could verbally open up the door for a cut in the September meeting.

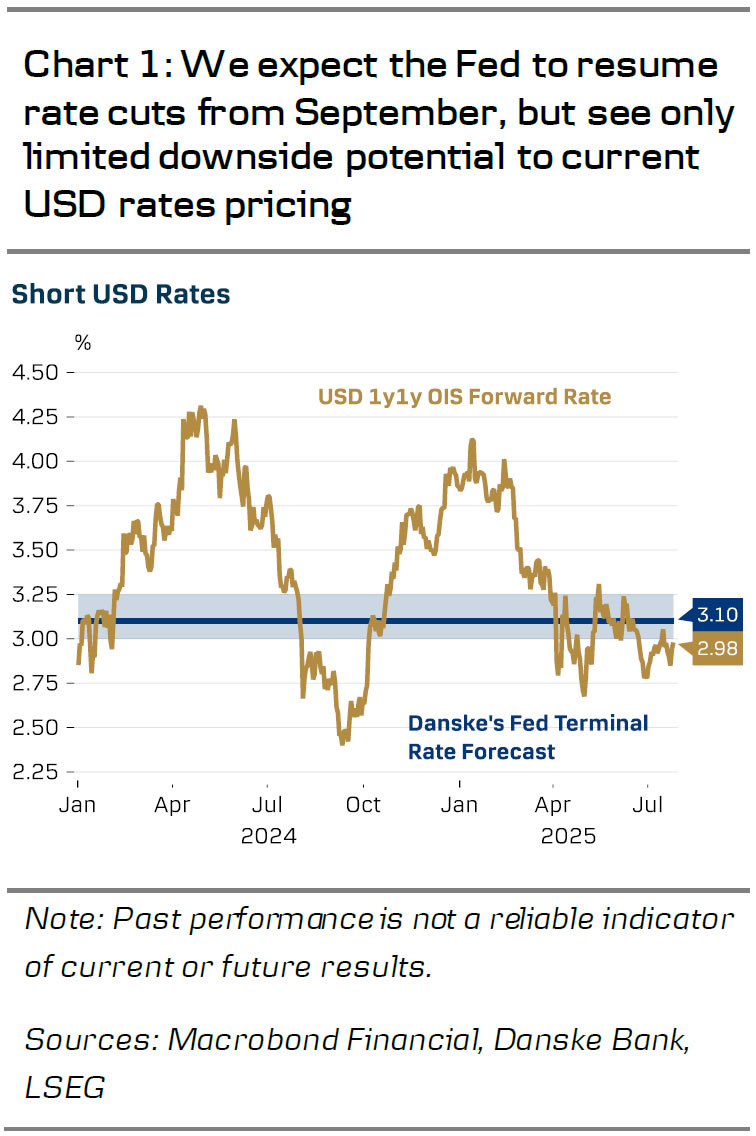

- Market is pricing around 16bp worth of cuts by September, and cumulative 43bp by year-end. Risks are skewed towards a modestly dovish reaction on Wednesday evening, but further out we think downside potential to USD rates is limited.

The Fed is inching towards resuming its cutting cycle but now is not yet the time. The June meeting was characterized by divided views across the FOMC – few participants did not see cutting rates this year as appropriate at all, while others favoured cutting already in July. Governor Waller has continued to signal that he could dissent in favour of a cut.

Since then, macro indicators have shifted in favour of further cuts, but data remains distorted. Higher realized and expected inflation were flagged as hawkish risks in the June minutes, but both have surprised to the downside since then. The July flash manufacturing PMI was weaker than expected, but the decline at least partly reflected slowdown in front-loading and firms awaiting clarity on tariffs.

The uncertain outlook for tariffs beyond 1st of August make pre-committing difficult at this stage, but we still think a cut in September looks likely. Needless to say, Powell will dodge any questions regarding political motivations for monetary policy changes.

As tariff payments continue to rise, firms will eventually have to either start passing through the costs to higher prices or look for ways to cut costs elsewhere. While we do pencil in accelerating goods and food inflation towards the fall, we are more concerned with the risk of tariffs causing weaker labour markets, than persistent inflation.

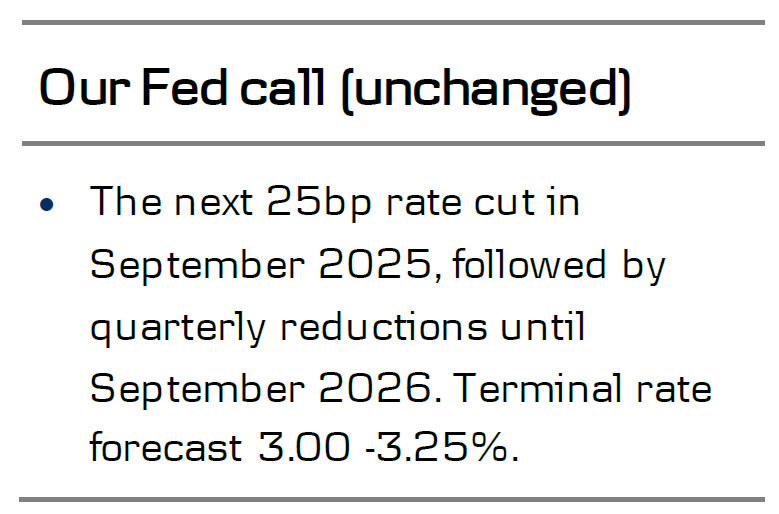

Beyond September, we pencil in quarterly 25bp reductions until the Fed Funds Rate target reaches 3.00-3.25% in September of 2026. Risks around the outlook are balanced in our view. We can easily sketch a scenario, where the Fed ends up cutting in every meeting after September, if macro data begins to undershoot expectations. But on the other hand, the renewed fiscal support from the start of 2026 could also ease the need for further cuts.

Altogether, we think the downside potential to USD rates is limited from current level. In the short-end of the curve, market is pricing cumulative 43bp worth of cuts by the end of 2025 – slightly less than we forecast. But from 2026 onwards, the pricing is well aligned with our call. In the long-end, we think the recent decline in term premium is unlikely to last given the fiscal outlook. We forecast the 10y UST yield at 4.50% in 12M horizon.

We still forecast further weakening for the broad USD, and maintain our 12M EUR/USD target at 1.23. We think the persistent policy uncertainty and structurally slowing economic growth are likely to weigh on the attractiveness of USD denominated assets even if our relative rates view is more neutral for the cross.

Week Ahead – Fed Decides Ahead of NFP and Tariff Deadline – BoC and BoJ Meet Too

- Fed to hold rates, unlikely to bow to Trump’s pressure.

- US GDP, PCE and jobs reports eyed too as August 1 deadline looms.

- BoC and BoJ decisions, Eurozone and Australian CPI also in focus.

Fed to likely stay on pause, risk Trump’s wrath

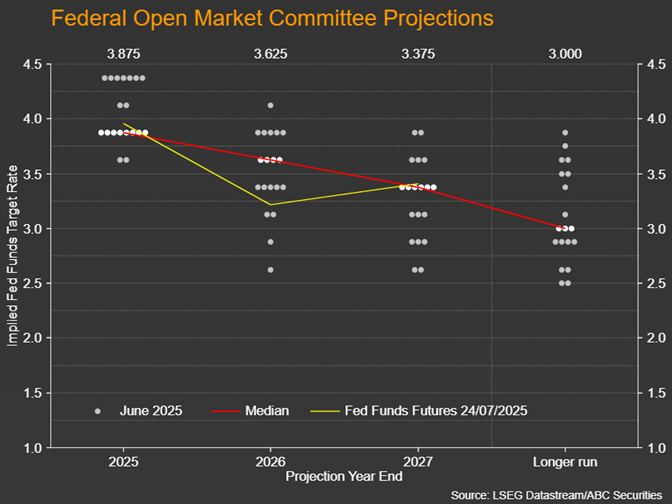

The Federal Reserve meets on Tuesday amid a cooling trade war and is widely expected to leave interest rates unchanged on Wednesday for the fifth time this year, even as President Trump relentlessly pressures the central bank to slash borrowing costs. But aside from the drama with the White House, the July meeting will be significant nevertheless, as a dovish tilt is possible, amid the doves within the Fed becoming more vocal. Not only that, but September is one meeting away and some kind of messaging will be necessary if a rate cut then is on the cards.

The latest dot plot and minutes of the June meeting revealed an almost 50-50 split among FOMC participants between those that prefer to lower rates sooner rather than later and those that are inclined to remain on pause for the foreseeable future. Not so long ago, there was growing talk that the Fed might surprise with a cut in July, but the subsequent data quashed the speculation.

CPI inflation measures edged up in June and there was a solid increase in nonfarm payrolls. Unfortunately for the Fed, the next NFP report isn’t due until two days after it meets, while the next inflation data – the PCE price indices – will be released the following day. This makes the July gathering a tricky one for Chair Jerome Powell, who faces a daily barrage of insults by Trump.

But Powell himself had left the door open to a July cut, amid lack of clarity about the strength of the economy and the inflationary effects of Trump’s tariffs, and his instincts may be right. Underneath the hood, the June jobs report wasn’t so strong as there was a notable slowdown in private sector employment. And with the number of trade deals being agreed finally gathering pace, the risk of a sharp jump in average import duties on August 1 has come down substantially.

Thus, the Fed is on track to resume its easing cycle in September as the majority of policymakers have been predicting. Flagging the likelihood of a rate cut in September while holding them steady for now is probably the best compromise Powell can achieve at this moment in time. This would unlikely be enough to satisfy his critics, but all the indications are that Trump is not currently planning on firing Powell – whether by upping the pressure on him to resign or finding legal grounds to do so such as using the costly renovations of the Fed headquarters building to allege misconduct.

All eyes on NFP, PCE and GDP reports

On the data front, it’s going to be a jam-packed agenda, as apart from the NFP and PCE inflation figures, there’s also the advance GDP report, as well as a slew of other releases.

First up on Tuesday are the S&P CoreLogic Case-Shiller 20-City Composite Home Price Index, the consumer confidence index for July and the JOLTS job openings for June. Pending home sales and the ADP employment change will follow on Wednesday, while on Thursday, Challenger Layoffs and the Chicago PMI for July will be the other second-tier releases.

All those indicators will be watched closely for wider clues on the health of the economy but are unlikely to attract as much attention as the week’s data highlights, the first of which is Wednesday’s advance GDP reading for the second quarter.

The jump in imports in the first quarter before higher tariffs kicked in was a big drag on GDP, which contracted by 0.5%. It’s expected to have rebounded by 2.5% in the June quarter as most tariffs were put on pause. Still, this data will be seen as somewhat outdated as investors and policymakers are more eager to see where the economy is headed.

The Fed is worried about how much inflation will rise over the coming months while keeping one eye firmly on the labour market. The June CPI numbers already pointed to some price hikes due to higher tariffs. If Thursday’s PCE inflation readings do the same, particularly core PCE, then the Fed might even forego September, and this is why a 25-bps rate cut at that meeting is only two-thirds priced in.

The Cleveland Fed’s own Nowcast model isn’t predicting any fireworks, however. The core PCE price index is estimated to have stayed unchanged at 2.7% year-on-year in June, but headline PCE is forecast to have picked up to 2.5% from 2.3%.

Potentially even more crucial will be the July payrolls numbers out on Friday. The headline print is expected at 102k, down from 147k in the prior month. The unemployment rate is projected to tick up to 4.2%, and growth in average hourly earnings to accelerate slightly to 0.3% month-on-month.

Also important on Friday will be the ISM manufacturing PMI, which is expected to improve from 49.0 in June to 49.6 in July.

Any weakness in the upcoming data would likely boost rate cut bets for September but investors are increasingly sceptical about the possibility of a third reduction in 2025 so the downside risks to the US dollar are somewhat limited.

Will the BoJ talk up rate hike expectations?

If the greenback does come under greater selling pressure, it’s more likely to be down to the strength of other currencies, such as the yen, which received a leg up from the US-Japan trade agreement.

Whilst there’s a sizable risk that Japan’s economy will take a hit from this new deal, as it still leaves Japanese exporters worse off from where they were before the trade war, the end of the uncertainty does potentially pave the way for the Bank of Japan to restart its tightening campaign. The BoJ last hiked rates in January and following the deal, investors have ratcheted up their bets of another 25-bps increase in the policy rate by year end, helping the yen to recover from near the 150 level against the dollar.

For the July meeting, which takes place on Wednesday and Thursday, the odds of a policy change are near zero, although the Bank will publish its latest quarterly outlook report. Should policymakers revise up their forecasts for inflation and see reduced risks to growth, rate hike expectations could further intensify, boosting the yen.

In terms of data, preliminary industrial output for June is out on Thursday, along with retail sales for the same month.

BoC to stay on hold as Canada hopes to avert 35% tariffs

Before the Fed and Bank of Japan decisions, it will be the Bank of Canada’s turn on Wednesday to set rates. But the meeting could turn out to be a non-event as the BoC is not anticipated to announce any changes, keeping its overnight rate at 2.75%.

It’s been a tough few months for Canadians, least of all for BoC policymakers who’ve had to worry about both a resurgence in inflation and a recession as the country’s biggest trading partner is threatening tariffs of up to 35%. Although the steeper levy rate won’t apply to goods covered under the USMCA agreement, it could nevertheless cause significant disruption to trade between the two neighbouring countries, potentially pushing the economy into a recession.

According to the BoC’s latest outlook survey, businesses are a little less pessimistic than in the prior quarter, as the recent trade deals have boosted hopes that Trump and Prime Minister Mark Carney will be able to reach some kind of an agreement before August 1.

But with more than 70% of Canada’s exports destined for the United States, it’s probably too soon to rule out a recession. (Thursday’s monthly GDP reading will provide an update for May). At the same time, Canada’s retaliatory tariffs of 25% on certain US goods is pushing up prices domestically. Even before the onset of the trade war, underlying inflation in Canada began to head higher and this limits the scope for rate cuts should the economic picture deteriorate further.

For now, and in the absence of a trade deal announcement over the next few days, the BoC will likely maintain the same tone as in the June meeting, with the risks to the Canadian dollar being tilted sightly to the downside.

Eurozone data may fail to excite

It’s not just Canada that’s in a rush to reach a trade agreement with the US as the European Union has also not struck a deal yet, although reports suggest that negotiators are closing in on one. The European Central Bank has already done its bit to safeguard the Eurozone economy from the trade war risks and decided to keep rates on hold in July for the first time in eight meetings, having halved the deposit rate to 2.0%.

Policymakers likely want to retain some firepower in case trade tensions with America escalate again as time is running out before the August 1 deadline. But assuming that a deal is agreed, it could be several months before the ECB cuts again, if at all. Hence, next week’s data may not spur much reaction in the euro.

The preliminary GDP estimates for the second quarter are due on Wednesday, followed by flash CPI numbers for July on Friday.

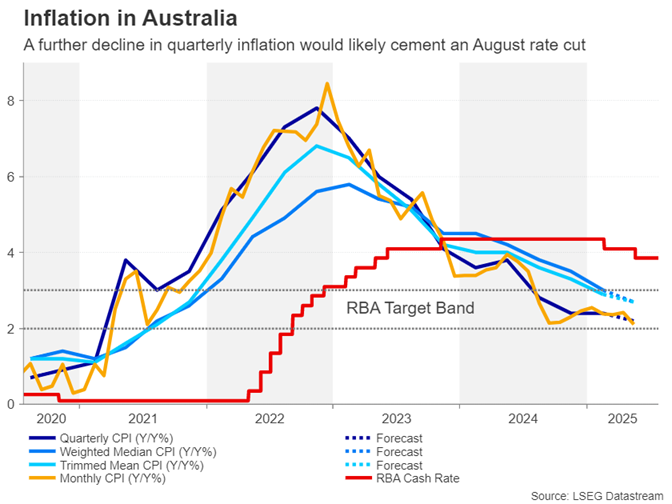

Will Australian CPI give RBA the green nod?

In Australia, quarterly CPI data could be crucial for the Reserve Bank of Australia’s next policy decision, something that Governor Michelle Bullock had referenced when justifying the surprise hold in July.

Australia’s statistics office won’t begin publishing a complete monthly CPI dataset until November. Until then, the RBA is putting more weight on the quarterly release than the experimental monthly reads.

The second quarter figures are due on Wednesday when the RBA will be hoping to see a further moderation in the core CPI measures. As for headline CPI, it dipped to 2.1% in May, but the RBA wants to see a similar decline in the quarterly print before trimming rates again.

A rate cut at the RBA’s next meeting in August is not fully priced in so the Australian dollar could extend its recent gains if the CPI figures are stronger than expected, further denting easing bets. Meanwhile, traders will also be watching Chinese manufacturing PMI due on Thursday.