Sample Category Title

ECB’s Lane Says Inflation Outlook Worsened as June Hike Expectations Build

European Central Bank Chief Economist Philip Lane gave markets little reason to doubt that a rate hike is approaching next month. As investors increasingly price tighter policy following the Middle East energy shock, Lane signaled that policymakers are comfortable with those expectations, saying, “I don't think the market needs some kind of extra guidance from us.”

His remarks add to a growing chorus inside the ECB arguing that the inflation consequences of the Iran conflict are becoming more persistent. Lane warned that “there are several factors related to the Iran war that show that the macroeconomic outlook has gotten worse,” while also acknowledging that oil prices are likely to remain elevated for longer than the ECB had projected in March.

Although stronger U.S. natural gas exports could help stabilize energy markets, he stressed that “on net” the impact has still been “upward pressure on inflation.”

Perhaps most importantly for markets, Lane confirmed that the ECB is preparing to raise its inflation forecasts again in June. “We are likely to make a further upward adjustment to the inflation forecast in June,” he said.

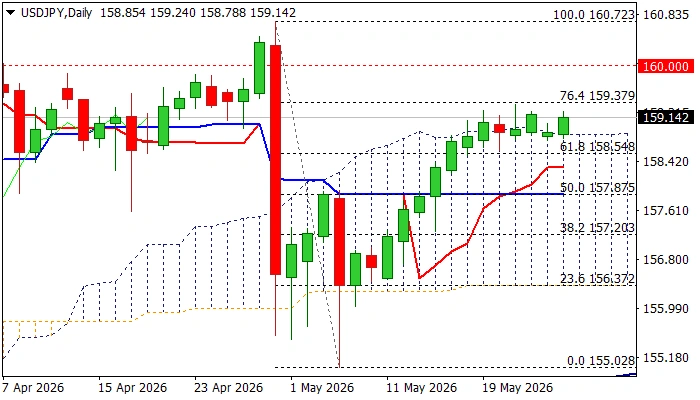

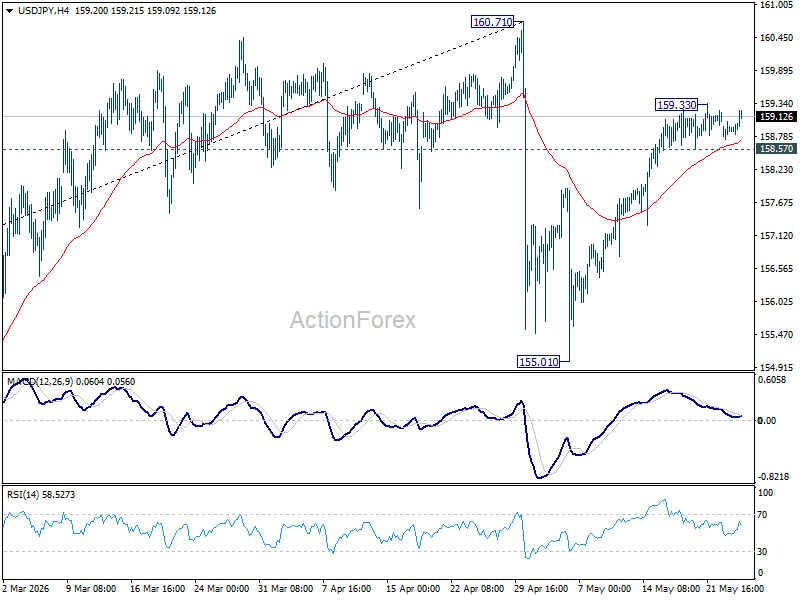

USD/JPY: Thick Daily Cloud Underpins Strongly But Traders Cautious on Looming Intervention

USD/JPY jumped on Tuesday as short-lived risk appetite was hit by renewed tensions in the Middle East that pushed the price to the upper side of a narrow near term range (158.80/159.35).

The action remains well supported by thick daily Ichimoku cloud (top of the cloud lays at 158.85), as well as bullish daily studies (strengthening positive momentum / multiple DMA bull-crosses) that keeps near term focus at the upside for now.

On the other hand, traders remain very cautious, keeping the price within narrow range for a couple of days, as the pair approaches 160 level, where Japan’s authorities intervened on Apr 30, with another action to boost weakening currency, not ruled out.

In such environment near-term direction remains unclear, with quick changes in risk mode from the situation in the Middle East, adding to current picture.

However, anticipated impact from intervention and bearish divergence on daily stochastic, suggests that the downside is still vulnerable, with cautious shorts (accompanied with tight stops) would be preferred near term scenario (violation of cloud top to generate bearish signal).

Res: 159.30; 159.85; 160.00; 160.45.

Sup: 158.80; 158.55; 158.30; 157.87.

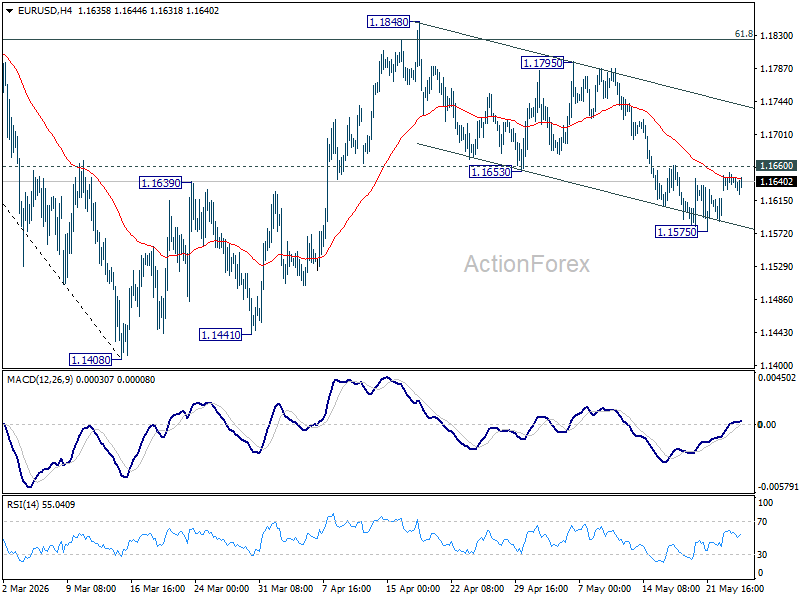

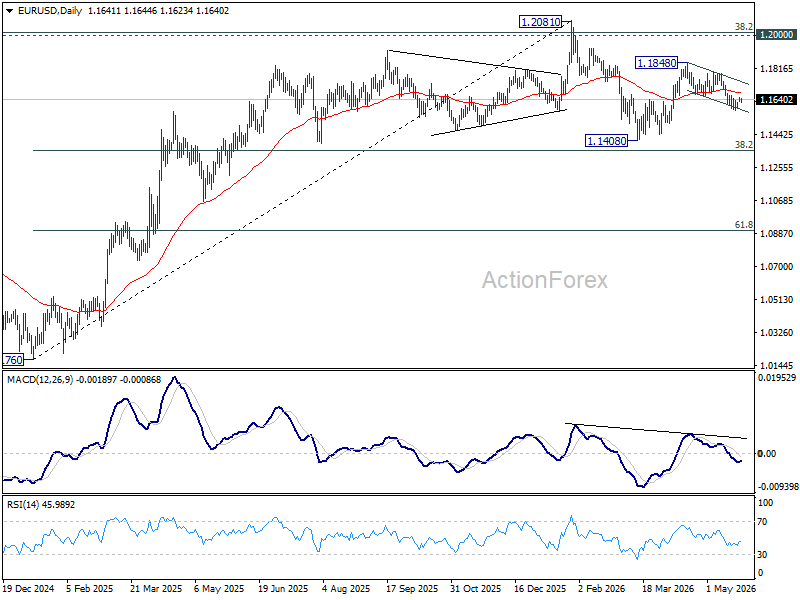

EUR/USD Daily Outlook

Range trading continues in EUR/USD and intraday bias stays neutral at this point. On the upside, firm break of 1.1660 resistance will argue that fall from 1.1848 has completed as a correction at 1.1575. Intraday bias will be back on the upside for 1.1795 resistance first. On the downside, break of 1.1575 will solidify the case that rebound from 1.1408 has completed at 1.1848, and bring deeper fall back to retest 1.1408 low.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1544). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

USD/JPY Daily Outlook

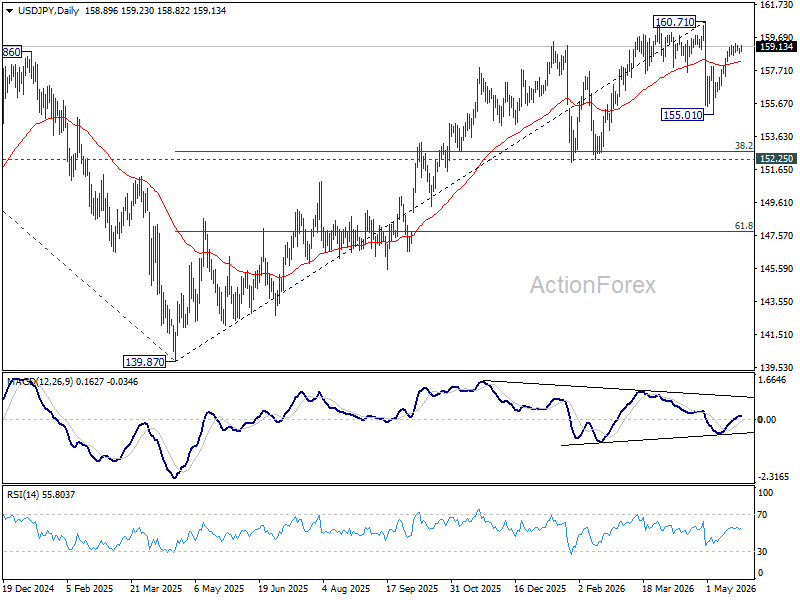

USD/JPY is staying below 159.33 temporary top and intraday bias remains neutral for consolidations. On the upside, firm break of 159.33 will extend the rise from 155.01 to retest 160.71 high. Strong resistance is expected from there to start the third leg of the near term corrective pattern. On the downside, break of 158.57 will turn bias to the downside for 55 D EMA (now at 158.21) and below.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.53) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

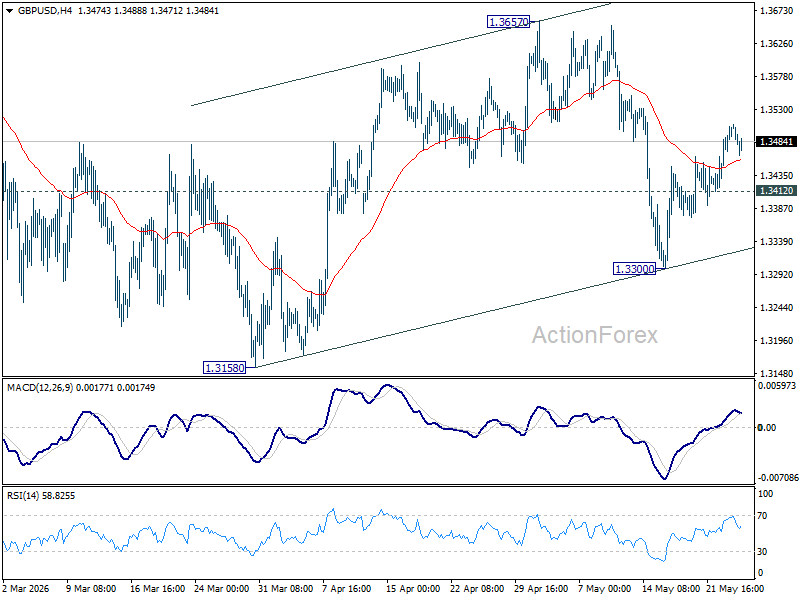

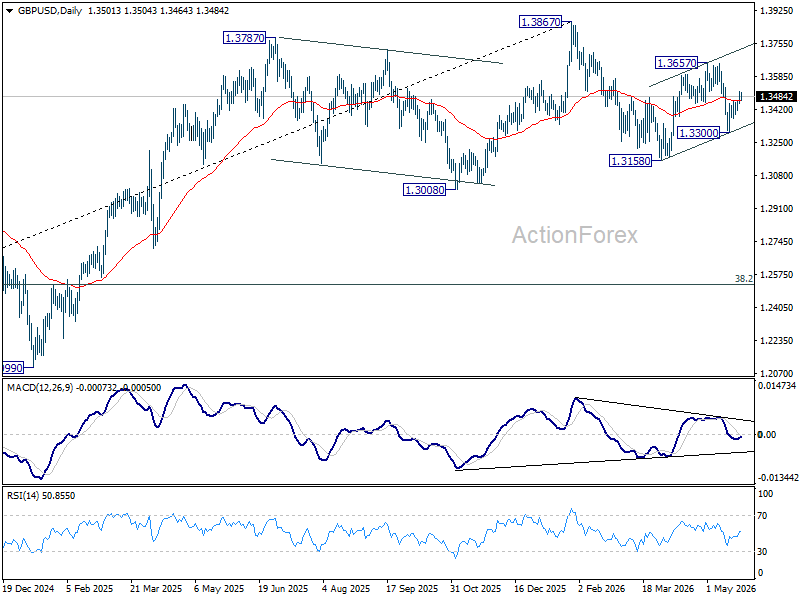

GBP/USD Daily Outlook

Intraday bias in GBP/USD stays mildly on the upside at this point. Rebound from 1.3300 should extend to retest 1.3657 resistance first. Firm break there will resume the rally from 1.3158. On the downside, below 1.3412 minor support will turn intraday bias neutral again.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

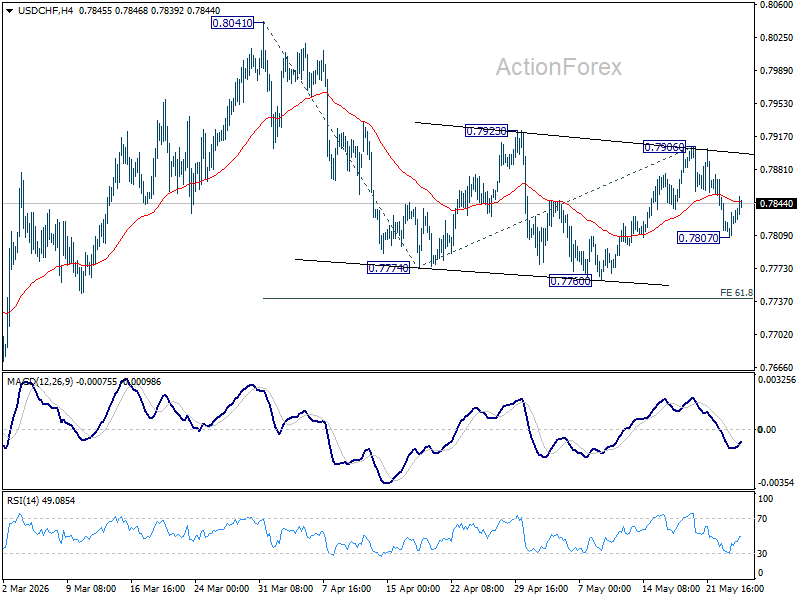

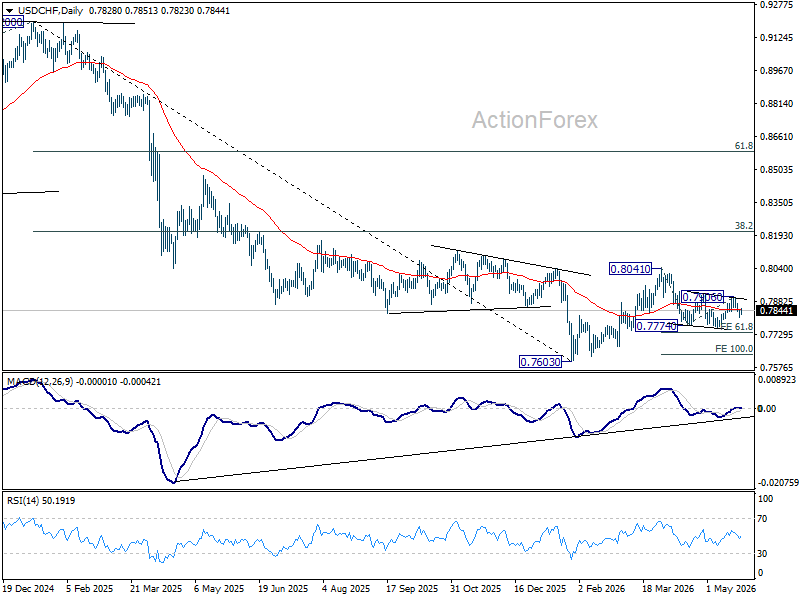

USD/CHF Daily Outlook

Intraday bias in USD/CHF is turned neutral with current recovery. But risk remains on the downside with 0.7906 resistance intact. Below 0.7807 will target 0.7760 first. Firm break there will resume the fall from 0.8041, and target 61.8% projection of 0.8041 to 0.7774 from 0.7906 at 0.7741.

In the bigger picture, as long as 55 W EMA (now at 0.8035) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

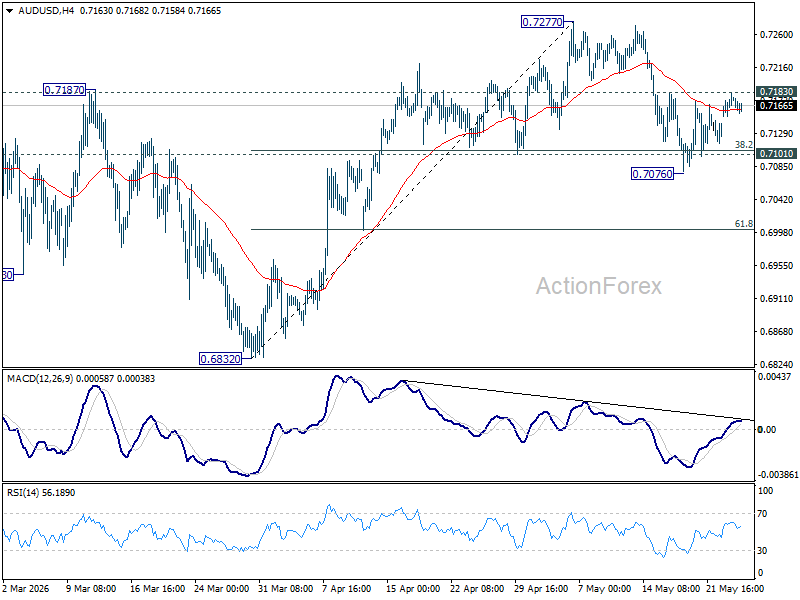

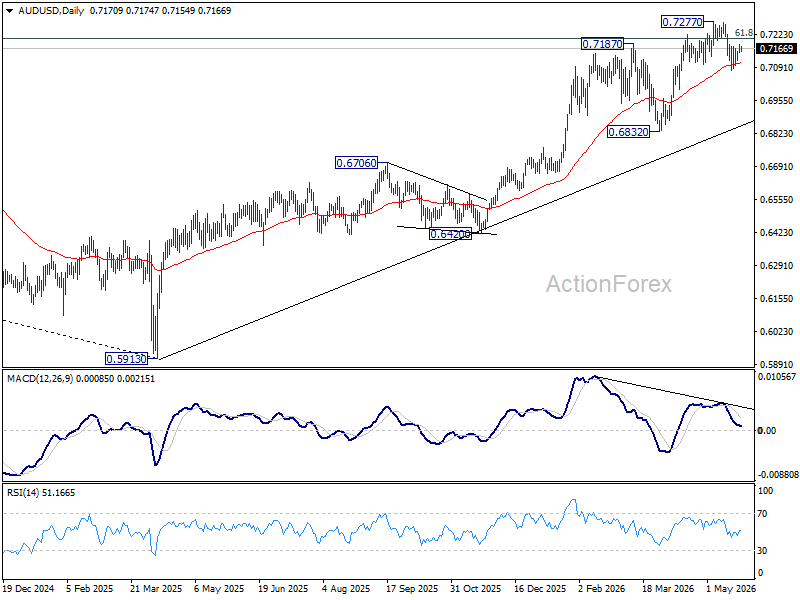

AUD/USD Daily Report

AUD/USD is still bounded in range below 0.7183 and intraday bias remains neutral. On the upside, firm break of 0.7183 resistance will suggest that pullback from 0.7277 has completed. Stronger rally should then be seen to retest 0.7277 high. However, decisive break of 0.7076 will indicate that larger scale correction is underway and target 0.6832 support instead.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

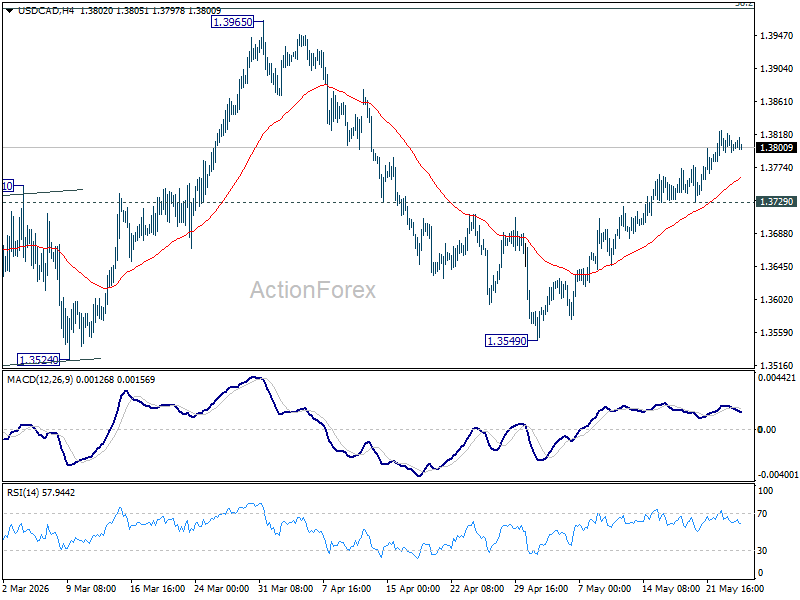

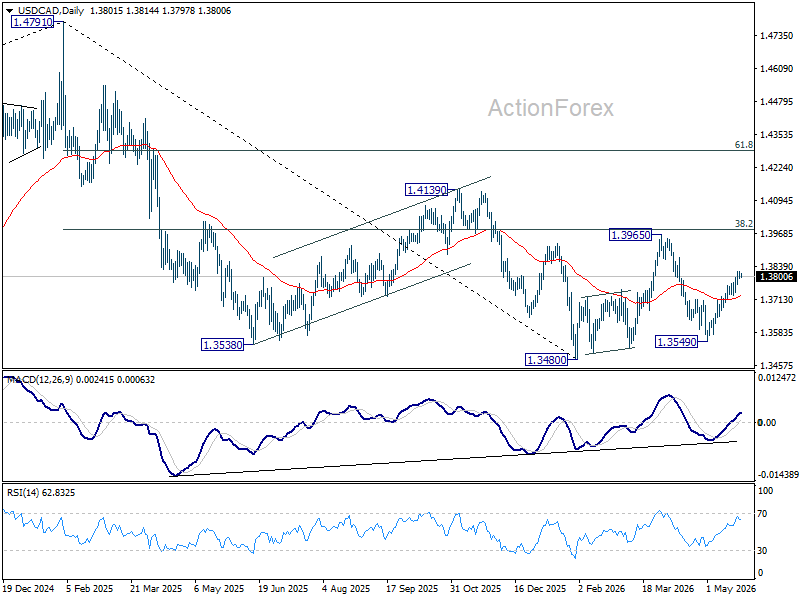

USD/CAD Daily Outlook

Intraday bias in USD/CAD stays mildly on the upside fro the moment. Rise from 1.3549 is in progress and it's seen as the third leg of the pattern from 1.3480. Further rally should be seen to 1.3965 resistance. On the downside, below 1.3729 support will turn intraday bias neutral again.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

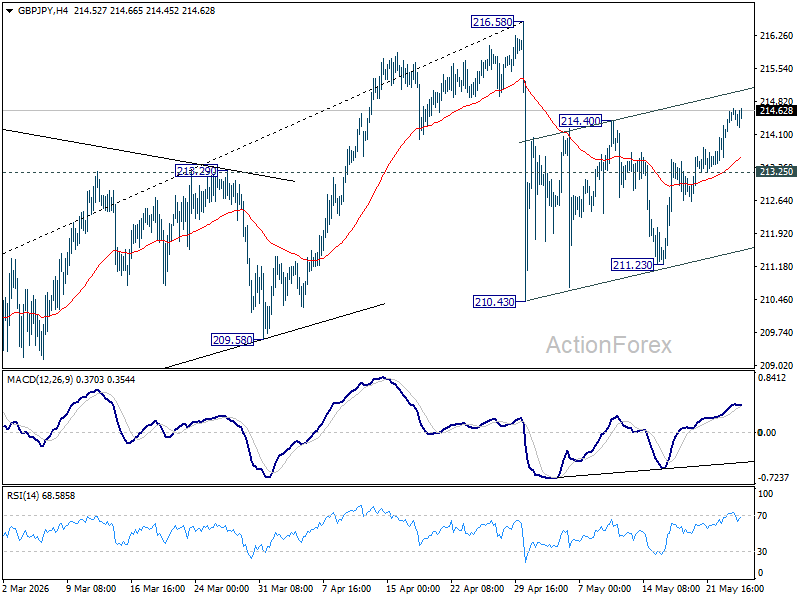

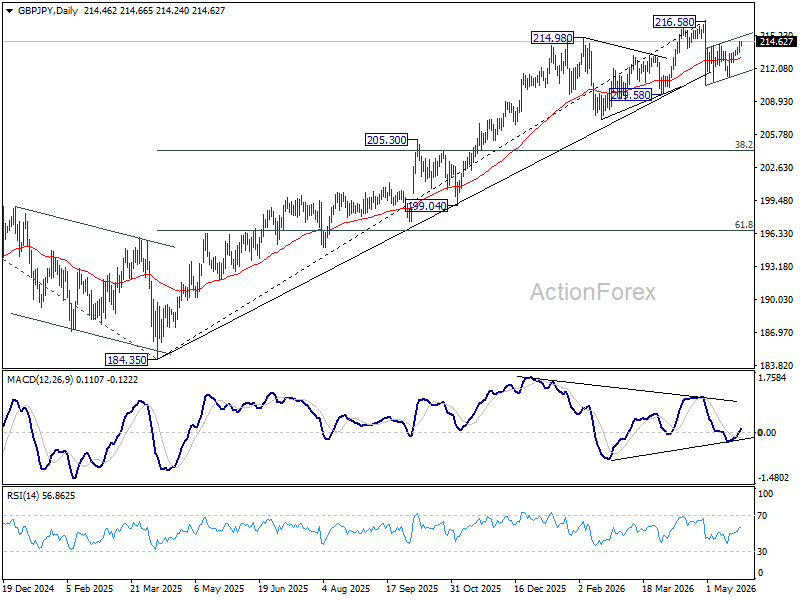

GBP/JPY Daily Outlook

Intraday bias in GBP/JPY remains on the upside at this point. Rebound from 210.43 is in progress and should target a retest on 216.58 high. Strong resistance should be seen there to cap upside, at least on first attempt. On the downside, below 213.25 minor support will turn intraday bias neutral again first.

In the bigger picture, while the fall from 216.58 is steep, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 206.27) will argue that it's already in medium term down trend for 184.35 support.

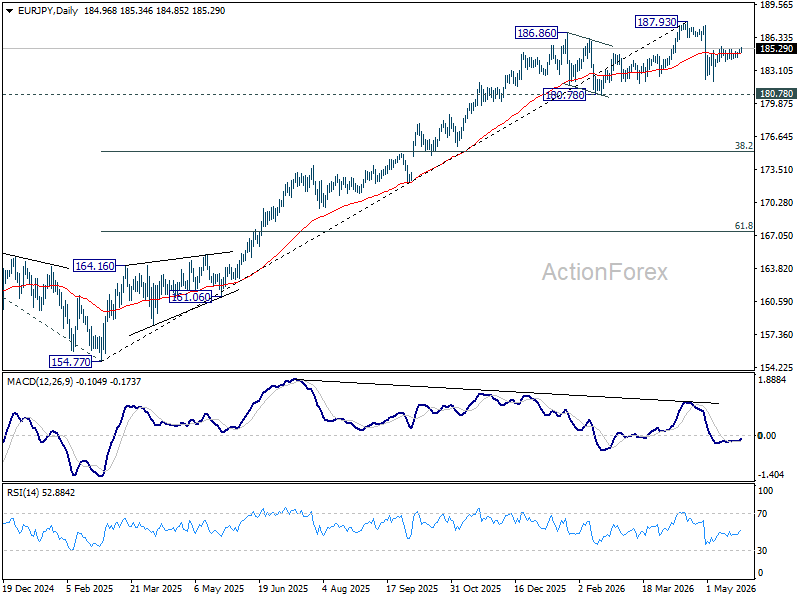

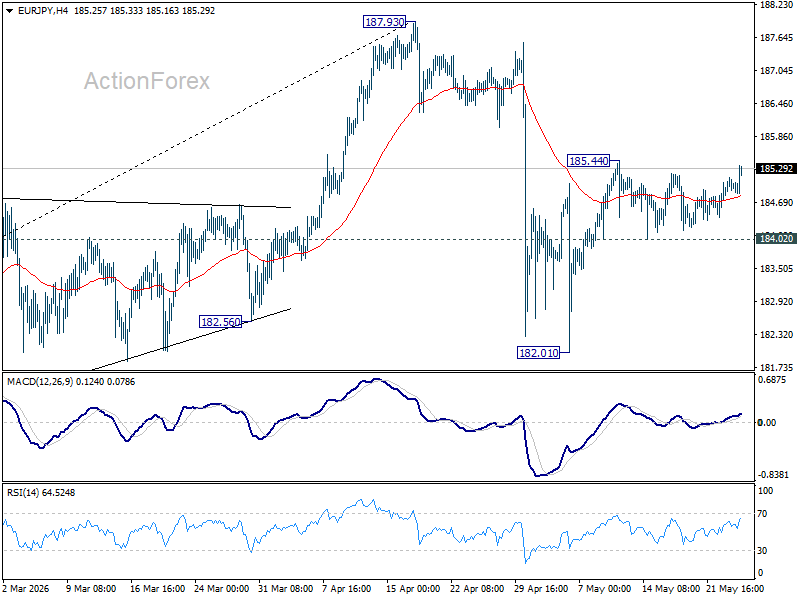

EUR/JPY Daily Outlook

Range trading continues in EUR/JPY and intraday bias stays neutral. Further rise is in favor with 184.03 support intact. Rise from 182.01 is seen as the second leg of the corrective pattern from 187.93. Above 185.44 will target a retest on 187.93 high. However, firm break of 184.02 support will bring deeper decline back to 182.01 instead.

In the bigger picture, the pullback from 187.93 is steep, there is no sign of reversal yet. Uptrend from 114.42 (2020 low) is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 178.51) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.