Sample Category Title

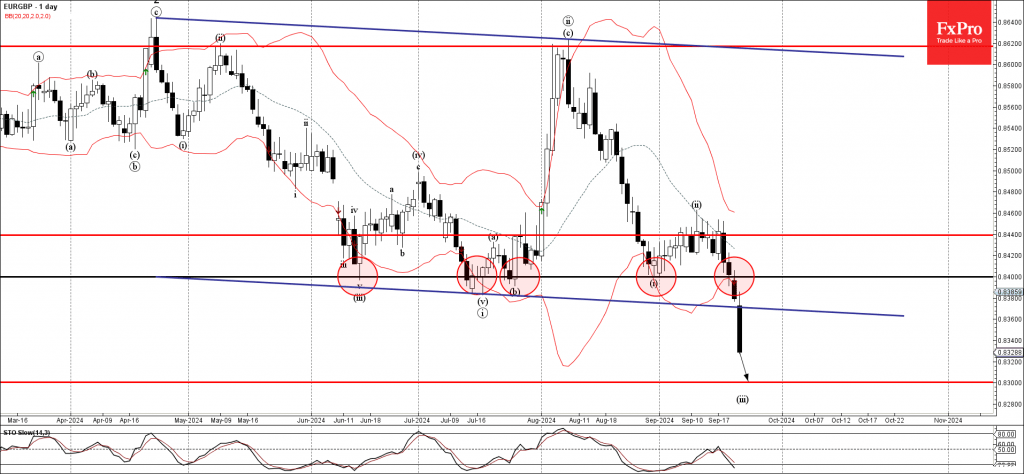

EURGBP Wave Analysis

- EURGBP broke the support area

- Likely to fall to support level 0.8300

EURGBP currency pair recently broke the support area located between the key support level 0.8400 (which has been reversing the price from June) and the support trendline of the wide daily down channel from April.

The breakout of this support area accelerated the active impulse waves iii and 3.

Given the clear daily downtrend and the strongly bearish euro sentiment seen today, EURGBP currency pair can be expected to fall further to the next support level 0.8300 – target price for the completion of the active impulse wave iii.

Gold Reaches New Record as Investors Eye Further Rate Cuts

Gold prices soared to a new all-time high, with the troy ounce surpassing 2614 USD. This surge is primarily driven by expectations of additional interest rate cuts and ongoing geopolitical tensions, which enhance gold's appeal as a safe-haven asset.

Following the US Federal Reserve's decision last week to reduce its interest rate by 50 basis points – the first such cut in four years – the market expects an equivalent reduction by the year's end. This week, attention is focused on upcoming US macroeconomic releases, including the Core PCE report and personal income and expenditures data. These indicators will provide insights into the potential direction of future Fed rate adjustments.

Gold becomes increasingly attractive as an investment during periods of lower lending costs, which typically lead to reduced yields on government bonds and a lower Dollar Index (DXY). Unlike other assets, gold does not generate coupon income, making it more appealing when other yields decline.

Additionally, the escalation of hostilities between Israel and Gaza has further boosted demand for gold. In times of heightened global uncertainty and conflict, gold traditionally performs well as a defensive investment.

Despite some strengthening of the US dollar, this has not significantly impacted the upward trajectory of gold prices.

Technical analysis of gold (XAU/USD)

Gold has broken through the resistance at 2611.00 USD and is now targeting 2672.00 USD. Upon reaching this level, a corrective movement back to 2611.00 USD may occur, followed by another growth phase targeting 2750.00 USD. The MACD indicator supports this bullish outlook, with the signal line well above zero and ascending sharply.

The H1 chart shows that gold has reached 2611.00 USD and is now consolidating around this level. The consolidation range is defined between 2603.00 USD and 2625.25 USD. A breakout above 2625.25 USD would likely lead to a continuation of the upward momentum towards 2672.00 USD, confirming the ongoing bullish trend. This scenario is corroborated by the Stochastic oscillator, with its signal line progressing towards 80, indicating sustained upward momentum.

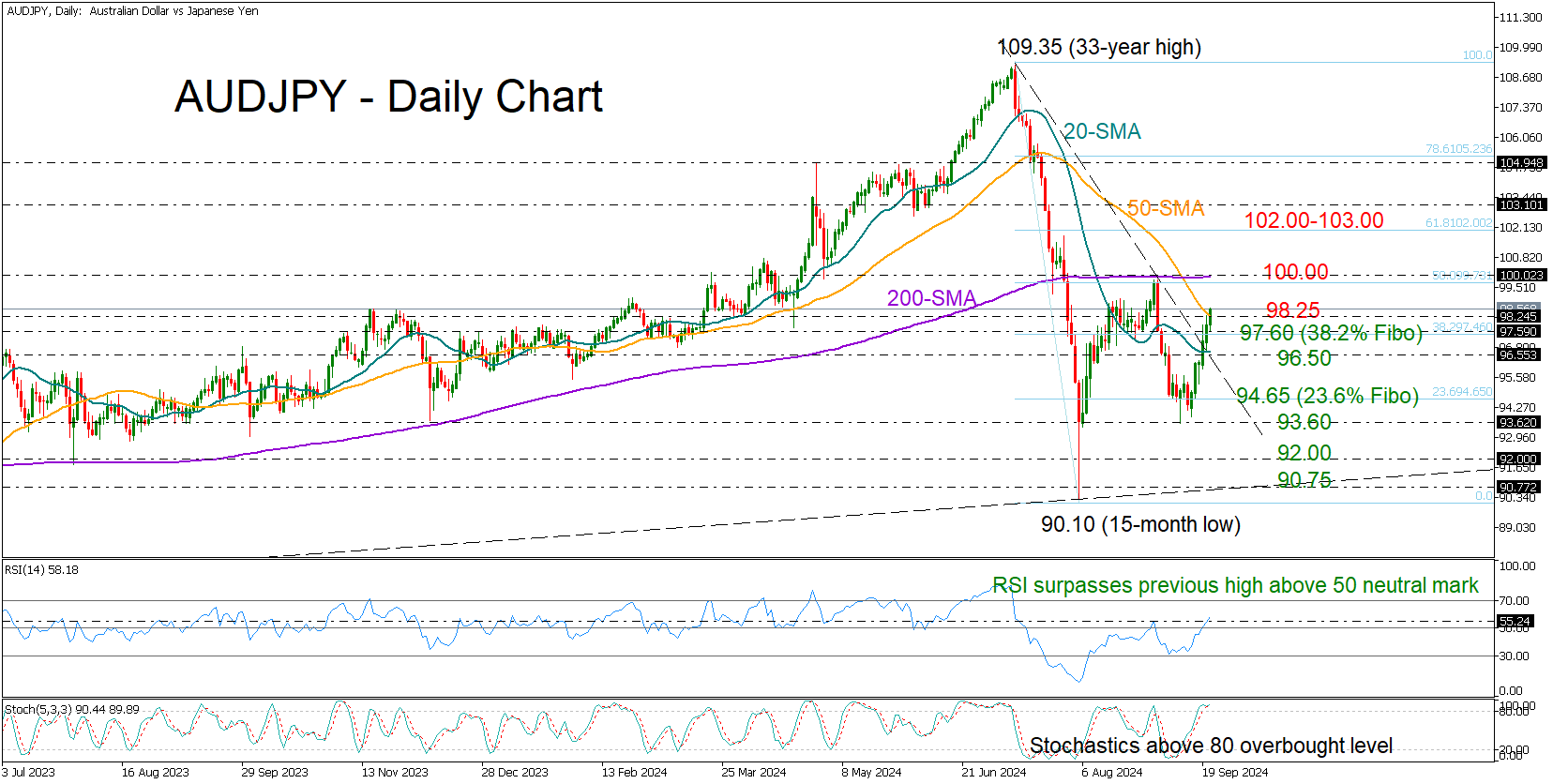

AUDJPY Stalls Near 50-SMA Ahead of RBA Rate Decision

- AUDJPY pauses recovery phase around 50-day SMA

- Risk skewed to the upside; major resistance near 100

- RBA policy announcement due on Tuesday at 04:30 GMT

AUDJPY has been pushing for a close above its 50-day simple moving average (SMA) at 98.25 since Friday. The pair is encountering a sense of déjà vu from July when the same line led to a bearish continuation, but this time the bulls may have luck on their side.

With the RSI surpassing its previous high above its 50 neutral mark, there might be sufficient buying appetite for an extension towards the critical flattening 200-day SMA at 100, which ceased the bounce off the 15-month low of 90.10 at the start of the month. The area overlaps with the 50% Fibonacci retracement of July’s freefall, a break of which could confirm an extension towards the 102.00-103.00 region.

If the bears return, the 38.2% Fibonacci mark at 97.60 and the 20-day SMA might prevent a decline towards the 23.6% Fibonacci of 94.65. Should the floor at 93.60 crack too, the sell-off might expand towards the tentative ascending line, which connects the 2023 and 2024 lows, seen near 90.75, unless the former barrier around 92.00 comes to the rescue this time.

Summing up, AUDJPY bulls could stay active as the technical signals remain positive. For an outlook upgrade, the pair must find new buyers above 100.00.

AUD/USD Rises to Eight-Month High, RBA Next

The Australian dollar has started the week with gains. AUD/USD touched a high of 0.6850, its highest level this year. In the North American session, the Australian dollar is trading at 0.6842, up 0.51% on the day.

Reserve Bank expected to hold rates

The Reserve Bank of Australia is expected to maintain the cash rate at 4.35% at Tuesday’s meeting. The RBA has held rates since November, making it an outlier among the major central banks, most of which have lowered interest rates. Underlying inflation is at 3.9%, much higher than the target of between 2% and 3%. Australia releases August CPI on Wednesday, with headline CPI expected to fall to 2.8%, compared to 3.5% in July.

The RBA was more cautious than other central banks during the rate-tightening cycle and its cash rate peaked one percent below the Federal Reserve. The flip side is that the RBA has been less aggressive as far as cutting rates and Governor Bullock has said that there are no plans to cut before February 2025.

The RBA’s rate hikes have chilled economic growth as consumption has fallen sharply and GDP grew by only 1% in the second quarter. Still, the labor market has remained robust and unemployment is at 4.2%, as large-scale immigration has boosted the economy and helped avoid a recession.

In the US, today’s PMIs had no impact on AUD/USD. The manufacturing PMI slipped to 47.0 in September, down from 47.9 in August and well off the market estimate of 48.5. This was the lowest level in thirteen months as new orders fell sharply. The services sector is in better shape as the PMI ticked lower to 54.4, compared to 54.6 in August and slightly above the market estimate of 54.3.

AUD/USD Technical

- 0.6865 has held in resistance since December 2023. Above, there is resistance at 0.6923

- 0.6781 and 0.6723 are the next support levels

Sunset Market Commentary

Markets

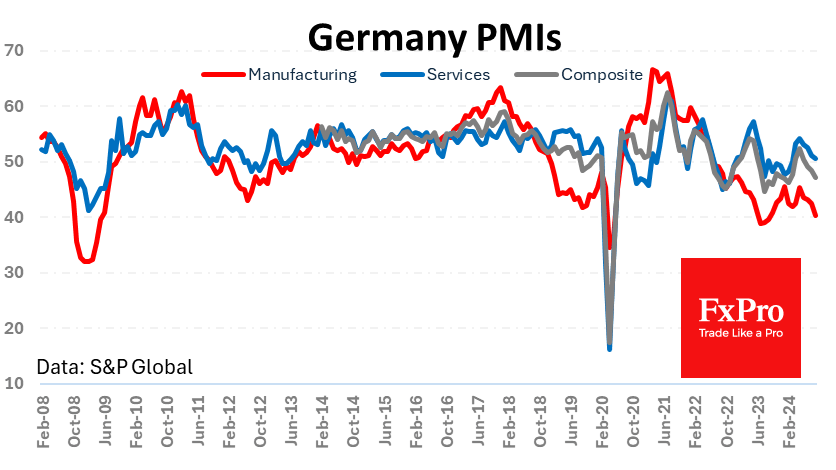

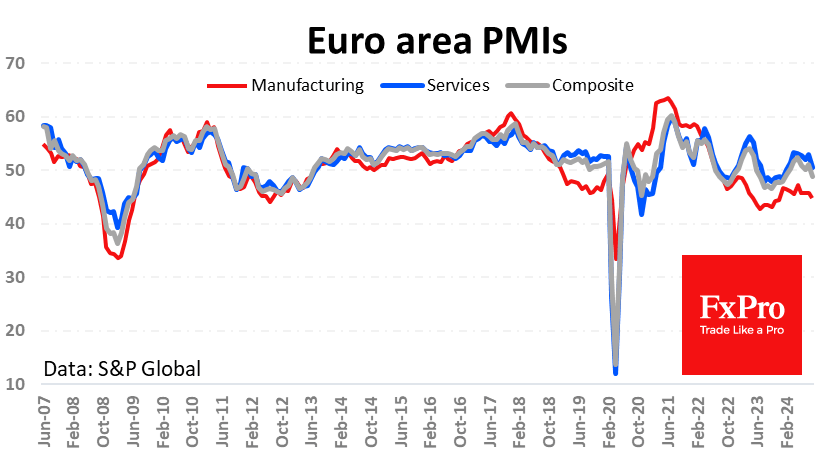

Its going from bad to worse with the EMU economy. According to the Flash PMI, activity contracted in September for the first time since February. The headline composite index slipped from 51 to 48.9 , substantially below the 50.5 expected. Germany fell further in contraction territory (47.2 from 48.4). Activity in France is deflating from a temporary summer uptick due to the Olympic games (47.4 from 53.1). Before September, a sharp contraction in EMU manufacturing was compensated for by ongoing growth in services. Contraction in manufacturing is becoming ever deeper (44.8 from 45.8). Services growth remains positive) except for France (48.3 from 55.0), but also nears a standstill (50.5 from 52.9). According to S&P global, the decline in overall activity comes amid a sustained reduction new orders. New business decreased at the sharpest pace since January. With new orders and volumes of outstanding business falling at sharper rates and business confidence at a ten-month low, companies scaled back workforce numbers for the second month running. Demand weakness resulted in slower inflation of both input costs and output prices

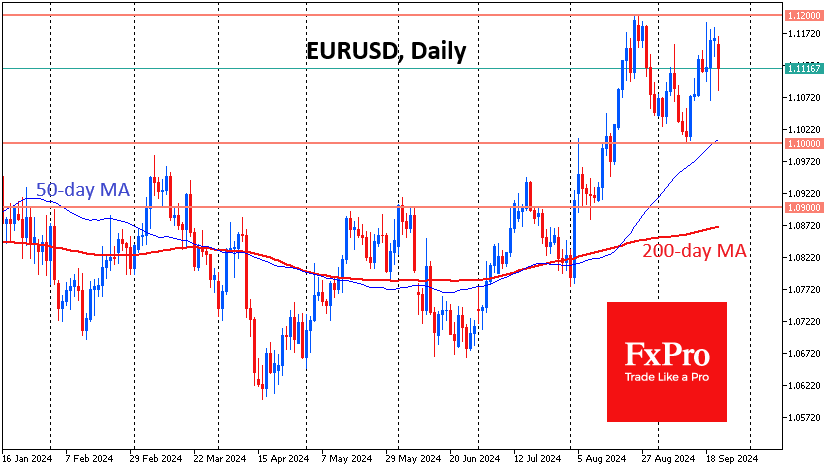

From a market point of view, the key question is what this awful PMI means for a data-dependent ECB. A brief inter-meeting period with few data releases between the September and October decisions and slightly upward revisions to its (core) inflation forecasts (2024 & 25), suggested a high bar to accelerate the pace of rate cuts. After the PMI’s, markets are raising the odds that the ECB will (have to) make a Fed-like move and give more priority to supporting growth. German/EMU yields declined sharply after the release but currently are trading off the intra-day lows. German yields cede between 5.5 bps (2-y) and 1 bp (30-y). EMU money markets see about a 40% chance of an October ECB rate cut. Maybe a bit surprising, EMU equities quite easily reversed a post-PMI dip (Eurostoxx 50 +0.4%). Similar story for the euro. EUR/USD swiftly tumbled from the 1.116 area to test the 1.1085 area, but currently again trades near 1.113. The damage could have been much bigger. Underlying USD weakness clearly still is at work. Sterling in the meantime continues its outperformance on a better PMI (cf infra) , especially against the euro. At 0.8345, EUR/GBP now trades now well below the 0.8383 previous low

US PMI’s mostly are not as influential for US markets as they are for EMU. At the time of finishing this report, the US PMI’s are reported to have held up very well (composite 54.4 from 54.6). In a first reaction, US yields gained modest ground with yields rising between 1.5 bps (2-y) and 3.2 bps (30-y). The dollar still hardly profits.

News & Views

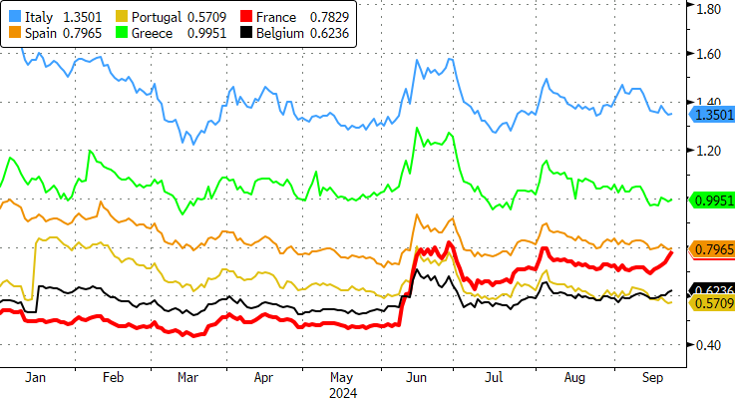

The French spread vs Germany’s 10-yr yield touched the highest level since the June snap election announcement (80 bps). OAT underperformance followed very weak French PMIs compounded with the announcement of a new French cabinet over the weekend. It’s a mixture of conservatives and centrists who haven’t always been on the best terms with each other. In addition, opposition blocs to both the left and the right have threatened to topple the fresh government through a vote of no confidence. This would plunge the country in renewed political uncertainty. The government coalition falls far short of the votes needed to prevent that from happening. The lift-wing NFP party said it’ll call for one at the earliest occasion. That would be October 1, when PM Barnier is due to address the parliament. It still needs the backing of the right-wing to do so, though. The right-wing Front National’s VP said its decision to support a no-confidence bill depends on the budget and Barnier’s approach.

UK PMI’s eased more than expected in September. The composite gauge fell from 53.8 to 52.9 on weaker readings in both manufacturing (51.5 vs 52.2 expected) and services (52.8 vs 53.5). Still, Output in both sectors rose thanks to rising customer demand and improving domestic economic conditions. Employment grew at the weakest pace since June. A marginal increase in services was counterbalanced by renewed job cuts in manufacturing. Cost burdens picked up from a 45-month low on higher container shipping costs and rising salary payments. Prices charged went the other way and rose at the slowest pace since February 2021. Business activity expectations remained upbeat and even picked up from last month, though firms cited lingering autumn budget-related uncertainty.

Graphs

Intra-EMU spreads: France (red) underperforms the region as political uncertainty still prevents budget consolidation.

2-y German yield testing recent low as markets reconsider chances for ECB October rate cut post very weak PMI’s.

EUR/USD holding up rather well despite EMU economy heading to contraction territory.

Cable: Sterling outperforms both euro- and USD weakness.

Nosedive in Eurozone Economic Activity

Preliminary Eurozone PMI estimates sent the EURUSD down 0.67% over the hour, as they were much weaker than expected and increased pressure on the ECB to continue easing monetary policy.

This is not the first time that a significant divergence of preliminary PMIs from expectations has become a driver of the European currency market. In terms of impact on the EURUSD, they rival the US employment data.

France’s economic boom did not last long, as the composite PMI estimate for September fell to 47.4 from 53.1 the previous month and well below the expected 52.7. The manufacturing PMI has been hovering around 44 for the past three months and has only been above 50 once in the past two years. The services sector fell below the 50 mark to 48.3, its lowest level since March.

Estimates of business activity for September suggest that German manufacturing activity slowed at the fastest pace in 12 months, continuing its decline since May and falling to 40.3. The services sector also reversed the decline of four months ago, although it remains formally in expansion territory above 50.

Manufacturing activity is contracting at the fastest pace since last December. At 50.5, the services sector is expanding at its slowest pace since February this year, but it’s still growing.

The negative surprise in the data triggered a new downward momentum in the EURUSD and a temporary dip below 1.11. The pair has failed to consolidate above 1.12 for the past month, and the current decline, if sustained, would look like a double top formation with a potential near-term downside target of 1.10 and a more distant one of 1.09. The obstacle to a longer-term weakening of the euro against the dollar is Fed policy. The FOMC cut rates by 0.5% last week, and current forecasts point to more active easing than the ECB.

US PMI indicates 2.2% annualized GDP growth, inflation remains a concern

US PMI Manufacturing fell from 47.9 to 47.0, marking a 15-month low. PMI Services slipped slightly from 55.7 to 55.4, while Composite PMI edged down from 54.6 to 54.4, indicating continued economic growth but at a slower pace.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, noted, "The data points to an economy growing at an annualized rate of 2.2% in the third quarter, driven by the robust service sector."

However, rising inflationary pressures are cause for concern, with prices charged for goods and services increasing at the fastest rate in six months. Input costs in services, particularly wages, have surged to their highest in a year.

"FOMC may need to move cautiously in implementing further rate cuts," Williamson added.

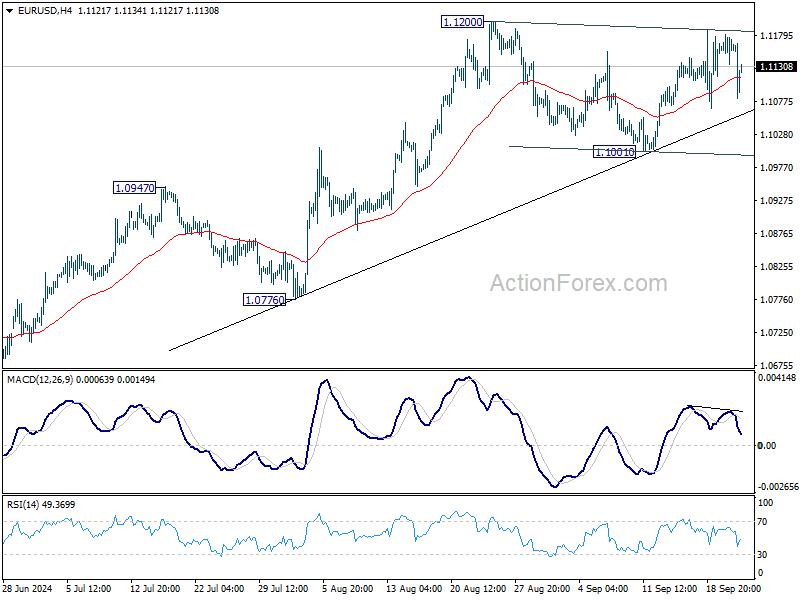

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1139; (P) 1.1161; (R1) 1.1185; More....

EUR/USD falls notably today but stays in range above 1.1001 support. Intraday bias remains neutral and further rally is expected. On the upside, above 1.1200 will target 1.1274 high. Firm break there will resume larger up trend. However, firm break of 1.1001 will indicate near term bearish reversal.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

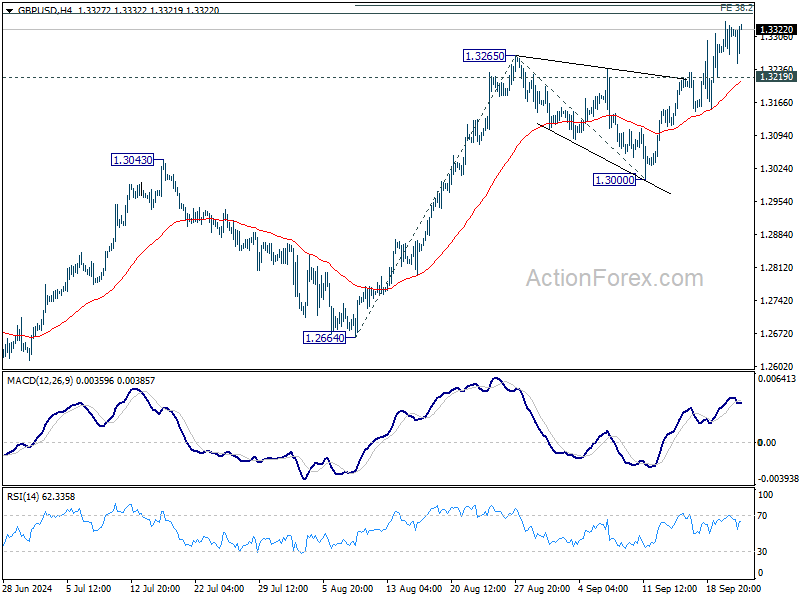

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3278; (P) 1.3309; (R1) 1.3354; More...

Intraday bias in GBP/USD stays on the upside for 61.8% projection of 1.2664 to 1.3265 from 1.3000 at 1.3371. Firm break there will pave the way to 100% projection at 1.3601 next. On the downside, below 1.3219 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 1.3000 support holds.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. Decisive break there will target 61.8% projection at 1.4022. For now, outlook will stay bullish as long as 1.2892 resistance turned support holds, even in case of deep pullback.