Sample Category Title

Price of Gold Continues to Hit Record Highs

As shown by today's XAU/USD chart, the price of an ounce of gold is around $2,628, marking a new all-time high for three consecutive trading days: 20th, 23rd, and 24th September.

The bullish sentiment in the gold market is driven by:

→ the reaction to Wednesday’s decision by the Federal Reserve to cut interest rates by 50 basis points;

→ another surge in tensions in the Middle East.

Technical analysis of the XAU/USD chart shows gold’s price is moving within an upward channel (marked in blue), with the bullish momentum becoming more pronounced in September. Since the beginning of the month, bulls have managed to:

→ break through the resistance level of $2,530;

→ lift the price into the upper half of the blue channel;

→ establish a steeper upward trajectory (shown by yellow lines).

However, it’s worth noting that:

→ each new record high is only slightly above the previous one;

→ the RSI indicator is forming a divergence.

This suggests that the bullish momentum may be weakening. It’s possible that market participants may look to take profits from long positions, leaving the price vulnerable to a pullback, potentially towards the lower boundary of the yellow channel, which is reinforced by the blue median line.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

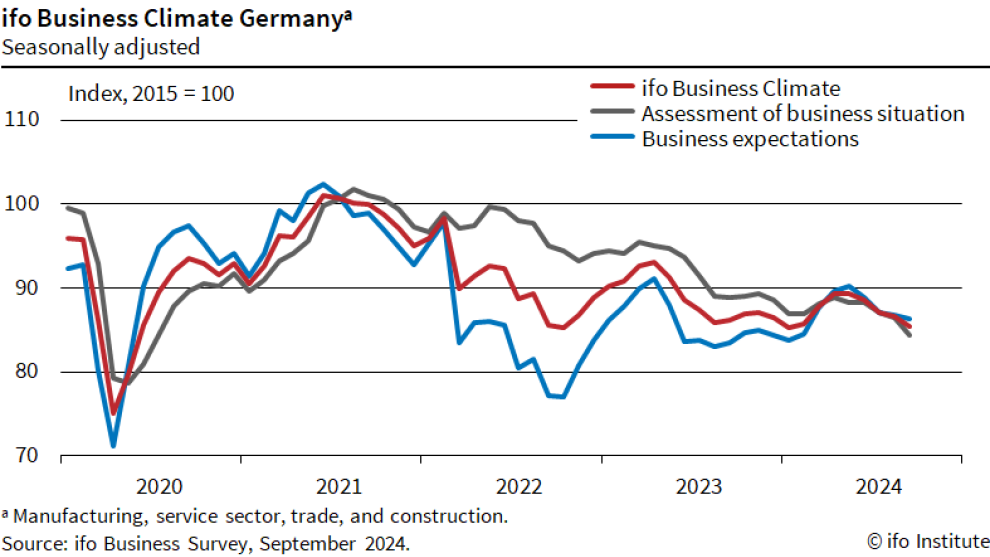

Germany’s Ifo falls to 85.4 as economic pressure mounts

Germany's Ifo Business Climate Index dropped from 86.6 to 85.4 in September, falling below market expectations of 86.1. This decline signals rising concerns for the German economy as key sectors show signs of strain. Current Assessment Index also fell, from 86.5 to 84.4, missing forecasts of 86.0. However, Expectations Index, which reflects sentiment about future economic conditions, remained relatively stable, easing only slightly from 86.8 to 86.3, in line with expectations.

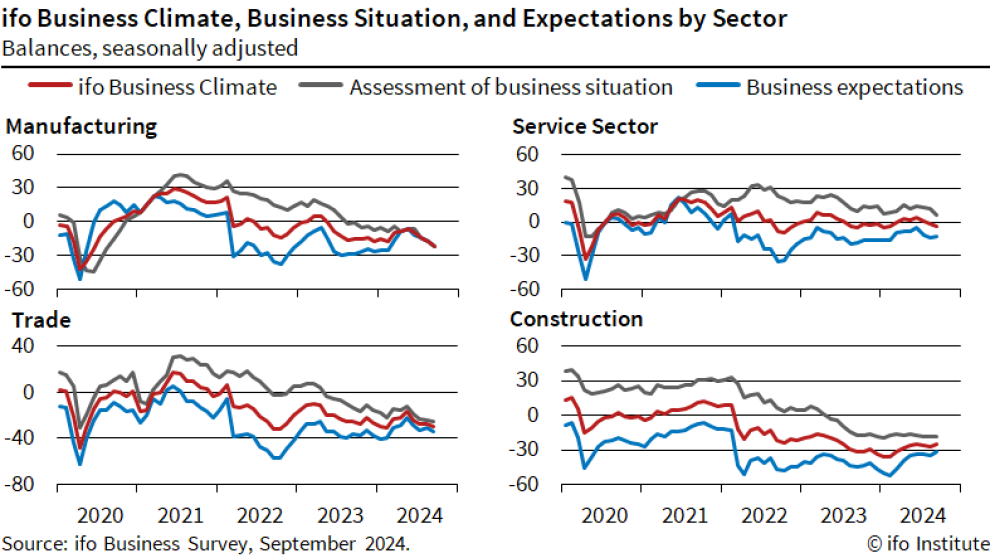

Sectoral data shows widespread weakness. The manufacturing sector posted a significant drop from -17.8 to -21.6, while the services sector also deteriorated, falling from -1.3 to -3.5. The trade sector saw a deeper contraction, with the index dropping from -27.4 to -29.8. On the other hand, construction provided a rare positive, showing a slight improvement from -26.8 to -25.2.

According to the Ifo Institute, "The German economy is coming under ever-increasing pressure." With multiple sectors showing increasing strain, the data suggests the German economy could remain in a precarious position, adding to recession concerns as the Eurozone's overall economic prospects look uncertain.

BoJ’s Ueda signals no rush to hike rates amid global uncertainties

In a speech today, BoJ Governor emphasized that the central bank will need to thoroughly assess factors such as financial and capital market developments both domestically and internationally, as well as the broader global economic environment. Importantly, Ueda indicated that there is "enough time" to make these evaluations, suggesting that BoJ is not in a hurry to raise interest rates again.

Ueda reaffirmed BoJ's commitment to adjusting its policy based on its economic and inflation outlook, stating that if the projections in the Outlook Report are met, the BoJ would indeed raise the policy interest rate. However, he also stressed the unpredictability of the current environment.

"Given the high uncertainties surrounding economic activity and prices, unexpected situations may occur," Ueda noted, adding that policy actions will need to be timely and flexible rather than adhering to any "fixed schedule."

Ueda further commented on Yen, noting that the recent one-sided depreciation has been partially retraced since August. This, along with a slowdown in the rise of import prices, has reduced the upside risk to inflation driven by higher import costs.

RBA on Hold, Seeking Sustainable Disinflation

RBA remains on hold at 4.35% as expected. The Board remains vigilant to upside risks to inflation and wants to return it to target sustainably, not just briefly.

As expected, the RBA remained on hold at its September meeting, with the cash rate target kept at 4.35%. The media statement was broadly unchanged in tone; the shifts in language were mostly incremental. The statement repeated the language that the Board remains vigilant to upside risks and is not ruling anything in or out. A noteworthy revelation from the media conference, though, was that there was not an explicit consideration of a rate hike versus remaining on hold, as there was at the August meeting. Rather, the Board considered what would need to change to shift them from being on hold. We see this as indicating that the Board is a bit more firmly on hold than before. Given the uncertainties, though, it is still not willing to rule out rate hikes entirely.

The media statement acknowledged the decline in headline inflation and that there was more to come. In the media conference, Governor Bullock also acknowledged that headline inflation could print below 3% tomorrow. But the Board wants to see inflation sustainably in the 2–3% target range, not just temporarily. The language of the media release showed a clear pivot to emphasise trimmed mean as the key indicator of the trend in inflation. The media statement and subsequent media conference both highlighted that the RBA does not expect trimmed mean inflation to be sustainably in the target range until 2026.

The Board would have been reluctant to be too hawkish given the August monthly CPI indicator will be released tomorrow. This is expected to show headline inflation below 3%; our own nowcast and the market consensus is at 2.7%. But because much of this decline reflects temporary measures such as the electricity rebates and other cost-of-living measures, this is not enough to keep inflation in target. That said, it will have a welcome effect on people’s inflation expectations, as will the recent decline in petrol and other prices that have been shown to be salient in forming those expectations.

Another key (and promising) change in the language is that the statement no longer includes mention of wages growth exceeding the rate that can be sustained given current rates of growth in productivity. This has been replaced with the sentence, ‘Wage pressures have eased somewhat but labour productivity is still only at 2016 levels, despite the pickup over the past year.’ In the media conference, Governor Bullock described herself as a productivity optimist and attributed much of the softness in productivity here and abroad (except for the United States) as being partly a lingering effect of the pandemic. We would note that productivity in the market sector is already well above 2016 levels, and that this is more important for price setting than the economy-wide figure.

There was also a more prominent mention of the tightness in the labour market in the announcement. This lined up with the recent speech by Chief Economist Sarah Hunter, which stated that the labour market was still tighter than the RBA’s view of full employment. Robust employment growth and a consolidation in average hours, associated with record high labour force participation, has been met with only a gradual uptick in the unemployment rate. These are welcome outcomes for a Board that has committed to a policy strategy that puts more weight toward maintaining the employment gains made following the pandemic.

In the media conference, the Governor again pointed to the strategy that the Board has been following for the entire rate-hiking cycle: raising rates by a bit less than its peers did, in an effort to hold onto the gains in the labour market. The Governor also noted that some of the peer economies that are already cutting rates have had much more marked increases in unemployment.

The media statement acknowledged that growth in demand has been slow and that there are risks around consumer spending. This is part of the strategy to get demand and supply back into balance. There was, however, an interesting pivot to emphasise the spending measure including temporary residents rather than consumption of long-term residents as defined in the national accounts. The broader measure has grown more quickly, but this is largely because the corresponding population measure has as well.

Based on today’s statement and media conference, we do not see any reason to change our current view, that the RBA will remain on hold this year and start lowering the cash rate from February. There are uncertainties around this if events should turn out very differently than expected. Overall, though, we see the RBA Board as a bit more firmly on hold than last month.

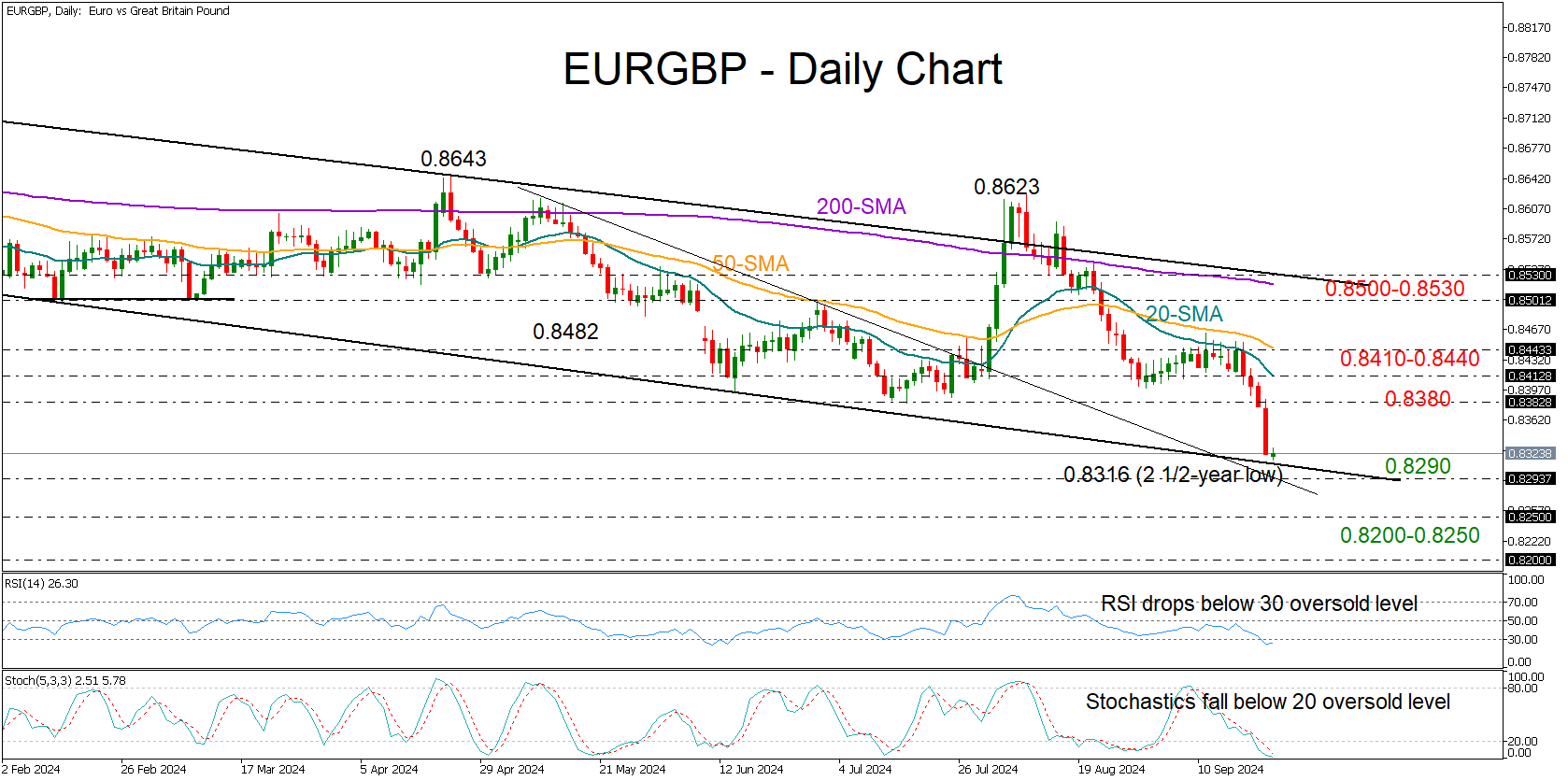

EURGBP Sinks to the Lowest Since 2022

- EURGBP resumes downtrend, falls rapidly to 2½-year low

- Oversold signals detected, price trades at the bottom of a channel

EURGBP plummeted to a 2½-year low of 0.8316 but held above the support line of the almost one-year-old bearish channel, fueling hopes that the bulls could still find a footing.

It is important to exercise caution as the RSI and stochastic oscillator have not yet found a bottom in the oversold zone, suggesting that downside pressures could persist for a bit longer before a potential upturn.

If sellers press the price below 0.8290-0.8300, they may face a critical test between the 0.8250 handle and the 2022 six-year low of 0.8200. Below the latter, there is no key obstacle till the 2016 resistance of 0.8115.

On the other hand, strong momentum is necessary for the bulls to overturn the current freefall and rise above July’s low of 0.8381. Closing above the 20-day simple moving average (SMA) at 0.8410 and the 50-day SMA at 0.8440 might be necessary as well to accelerate towards the 0.8500-0.8530 barrier.

Still, the short-term outlook can only turn bullish if there is a sustainable rally above the 200-day SMA and the long-term bearish channel.

Overall, although downside risks have not fully evaporated, EURGBP is trading near a significant support area, which suggests the possibility of bullish activity.

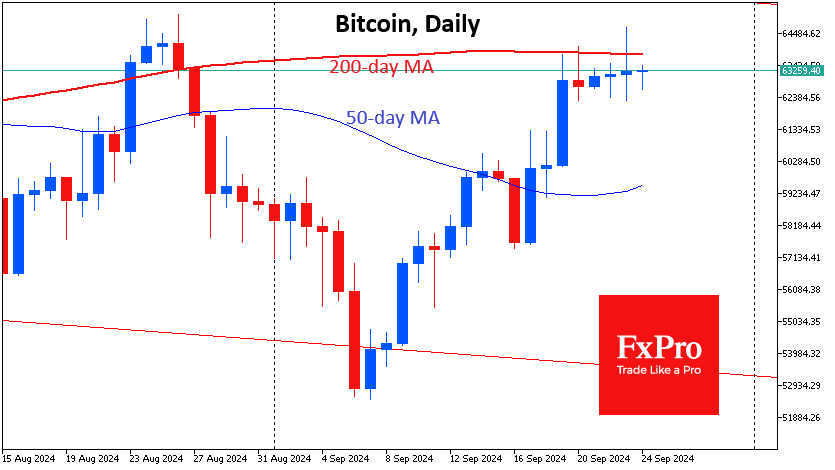

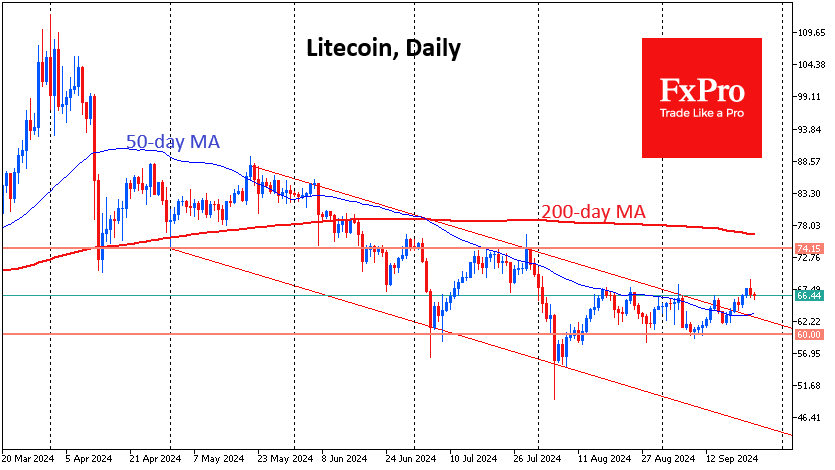

Bitcoin Keeps at Heights, Litecoin Pushes Back from Resistance

Market Picture

The cryptocurrency market corrected 0.5% to levels from a day earlier to $2.22 trillion, continuing to settle at the top near the previous month’s peak. As expected, cryptocurrency selling intensified near the previous peak. The cryptocurrency market will need to rise another nearly 3% to validate the breaking of the multi-month downtrend.

Bitcoin’s previous four daily candles and today’s candles show a very moderate end-of-day trend with relatively impressive intraday swings. The battle for the 200-day moving average continues. In this case, the former cryptocurrency is moving up more cautiously than the stock market.

Last week, Litecoin overcame the resistance of the descending channel, inside which it has been trading since May. However, selling intensified as it approached the horizontal resistance level just above $67, which turned the price downward for the fourth time in the last five weeks. A return of risk appetite in global markets will help validate the break of the downtrend, sending the price to $74 (+12%). Intensifying selloffs will force the price to look for support at $60 (-10%) as soon as possible.

News Background

According to CoinShares, investments in crypto funds rose by $321 million last week after inflows of $436 million a week earlier. Bitcoin investments were up $284 million, while Solana was up $3 million; Ethereum was down $29 million. Investments in funds with multiple crypto assets were up $54 million.

The inflow of funds last week was probably caused by the US Federal Reserve’s decision to cut the interest rate by 50 basis points at once. As a result, total assets under management (AUM) rose 9% to $9.5bn. Ethereum remains the exception, with outflows for the fifth week in a row. This is due to persistent outflows from Grayscale Trust and meagre inflows into the recently launched Ethereum-ETFs, CoinShares noted.

Larry Fink, CEO of BlackRock, said Bitcoin is a legitimate financial instrument that can diversify risk. In his view, it is an instrument that ‘people invest in as soon as they become fearful of the market.’

The average transaction fee on the Ethereum network rose to $3.98, almost fivefold from $0.85 in early September. Uniswap tops the ranking of the most gas-consuming apps.

AUD/USD Reaches Yearly High Amid Positive Stimulus News from China

The AUD/USD pair tested the 0.6860 mark on Tuesday, reaching its highest point in 2024, bolstered by supportive economic news from China. The People's Bank of China (PBoC) announced stimulus measures to boost the Chinese economy. These measures positively influence the Australian dollar due to the close economic ties between Australia and China.

The Reserve Bank of Australia (RBA) is expected to maintain its interest rate, reflecting mixed sentiment among market participants regarding the future rate trajectory. According to a recent Reuters poll of 44 economists, only four anticipate a rate cut by year-end. However, investors assign a 60% probability of a rate reduction in December.

So far, the RBA has maintained a conservative stance regarding inflation and economic activity, believing that the economy can self-adjust without intervention. Nonetheless, the global trend towards rate cuts initiated by central banks, such as the Fed and the ECB, may influence the RBA's perspective in the future.

AUD/USD technical analysis

The AUD/USD has completed the fifth wave of growth, reaching a target of 0.6864. Currently, a potential initial wave of decline to 0.6740 is being considered. After reaching this level, a corrective move to 0.6803 could occur, marking the upper limits of a new consolidation range. A downward exit from this range might lead to further declines towards 0.6740, with a potential continuation down to 0.6677 and possibly extending to 0.6616. The MACD indicator, currently at its peak, suggests an impending decline, supporting this bearish outlook.

On the H1 chart, the AUD/USD is forming a downward structure targeting 0.6805. Subsequently, a narrow consolidation range may develop, with a potential downward breakout leading to further declines towards 0.6744. This scenario is corroborated by the Stochastic oscillator. Its signal line currently above 80 but poised to move downward sharply.

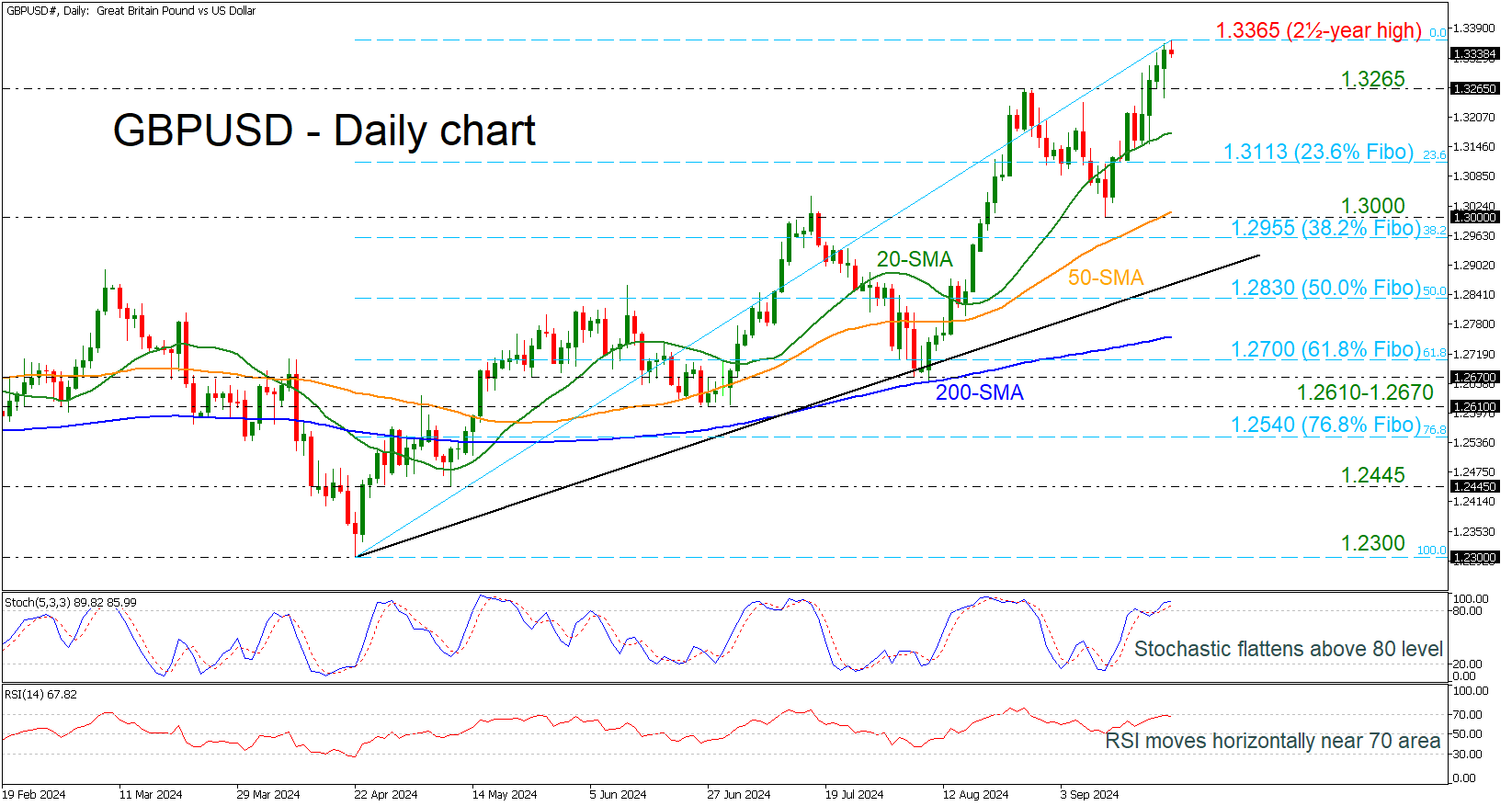

GBPUSD Unlocks Another New 2½-Year High

- GBPUSD eases a bit after strong rally

- Technical oscillators move slightly down

GBPUSD skyrocketed to a fresh two-and-a-half-year high of 1.3365 earlier today, adding almost 3% after the bounce off the 1.3000 round mark. The technical oscillators indicate an overstretched market. The stochastic is turning slightly lower in the overbought territory, while the RSI is pointing down following the pullback at the 70 level. Moreover, the 20-day simple moving average is losing its positive momentum, showing some downside pressure.

If the market retreats, then the pair could open the door for the immediate 1.3265 support level before meeting the 20-day SMA at 1.3170. Moving lower, the 23.6% Fibonacci retracement level of the upward wave from 1.2300 to 1.3365 at 1.3113 could come next before plunging to 1.3000, which coincides with the 50-day SMA.

On the other hand, in case of an upside pressure again, the price could enter the 1.3400 territory ahead of the 1.3640 resistance, achieved back in February 2022.

All in all, GBPUSD has been in a significant bullish tendency since April and only a dive beneath the uptrend line and more importantly below the 200-day SMA may change the current outlook.

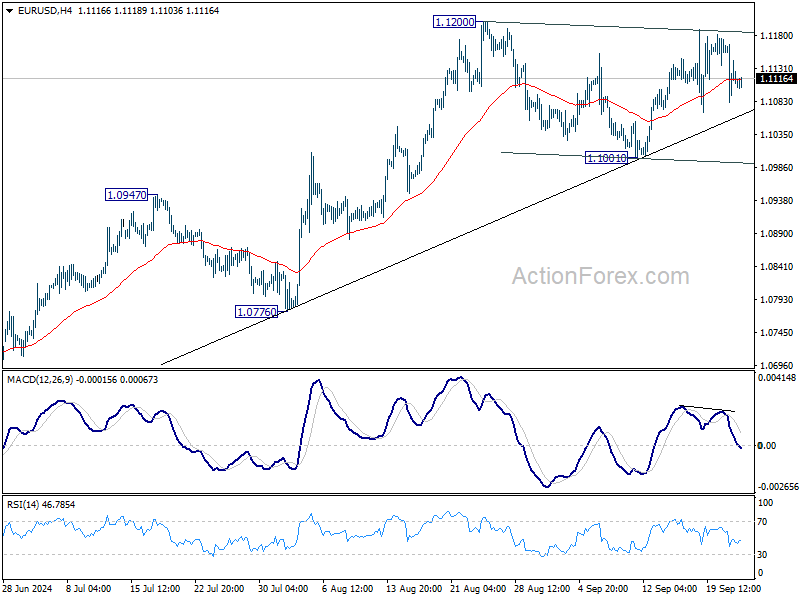

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1073; (P) 1.1121; (R1) 1.1158; More....

Intraday bias in EUR/USD remains neutral as consolidations continues below 1.1200. Further rally is expected as long as 1.1001 support holds. On the upside, above 1.1200 will target 1.1274 high. Firm break there will resume larger up trend. However, firm break of 1.1001 will indicate near term bearish reversal.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

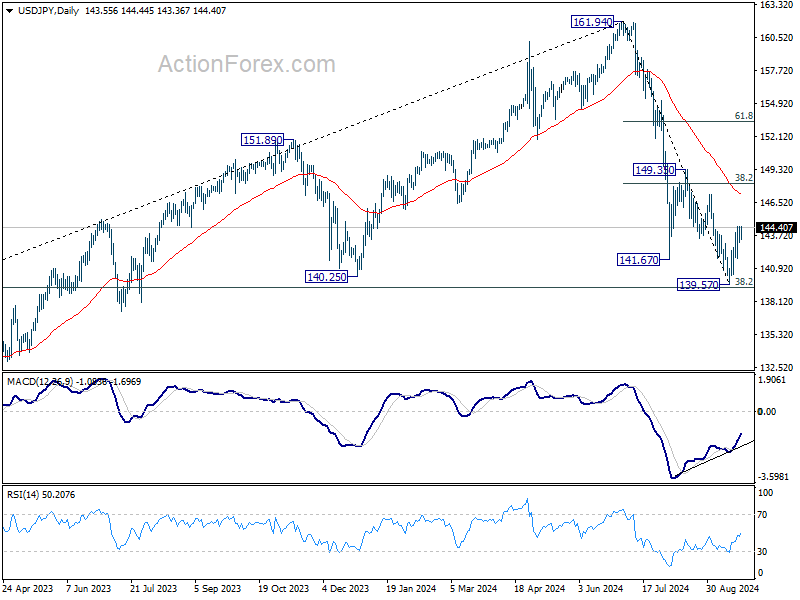

USD/JPY Daily Outlook

Daily Pivots: (S1) 143.02; (P) 143.74; (R1) 144.32; More...

Further rally is still expected in USD/JPY. Rebound from 139.57 short term bottom should extend to 38.2% retracement of 161.94 to 139.57 at 148.11. On the downside, below 141.73 minor support will turn bias to the downside for retesting 139.57 instead.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.