Sample Category Title

Eurozone CPI finalized at 2.2% in Aug, core CPI at 2.8%

Eurozone CPI was finalized at 2.2% yoy in August, down from July's 2.6% yoy. Core CPI (ex-energy, food, alcohol & tobacco) was finalized at 2.8% yoy, down from prior month's 2.9% yoy.

The highest contribution to the annual Eurozone inflation rate came from services (+1.88 percentage points, pp), followed by food, alcohol & tobacco (+0.46 pp), non-energy industrial goods (+0.11 pp) and energy (-0.29 pp).

EU CPI was finalized at 2.4% yoy. The lowest annual rates were registered in Lithuania (0.8%), Latvia (0.9%), Ireland, Slovenia and Finland (all 1.1%). The highest annual rates were recorded in Romania (5.3%), Belgium (4.3%) and Poland (4.0%). Compared with July 2024, annual inflation fell in twenty Member States, remained stable in one and rose in six.

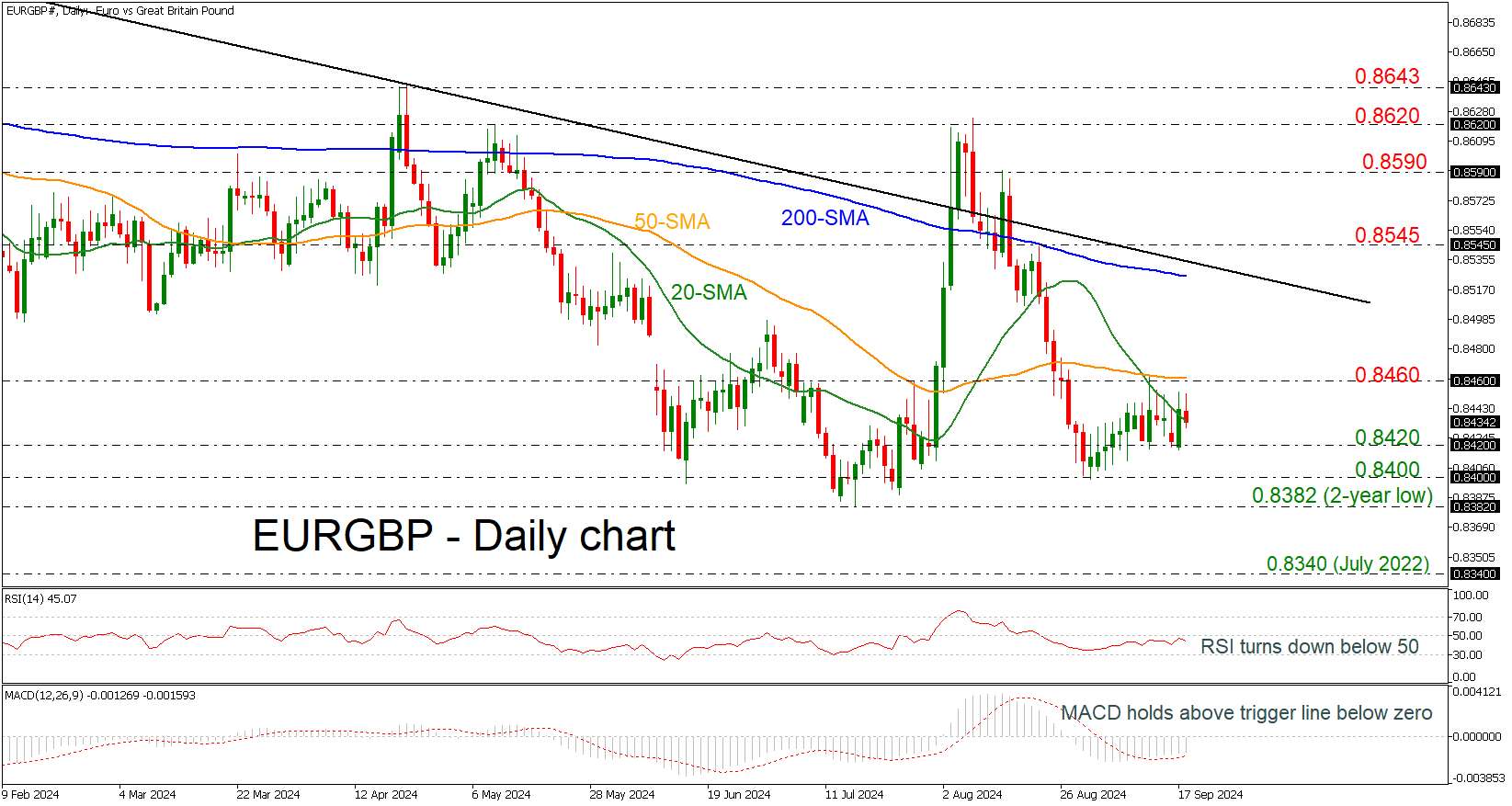

EURGBP Trades Within Tight Channel

- EURGBP finds strong resistance at 50-day SMA

- Momentum oscillators hold below their mid-levels

EURGBP is trading within a narrow range of 0.8420-0.8460 over the last couple of weeks, remaining capped by the flat 50-day simple moving average (SMA) around the 0.8460 resistance.

Technically, the RSI indicator is pointing south marginally beneath the 50 level; however, the MACD oscillator is holding above its trigger line beneath the zero line with weak momentum.

More downside pressures and a successful dive below the 0.8420 support as well as a break beneath the 0.8400 round number, the door would open for the two-year low of 0.8382. If there are steeper decreases the bulls may head towards the July 2022 bottom at 0.8340.

On the flipside, a rally beyond the 50-day SMA could take the market until the 200-day SMA at 0.8525 before testing the long-term downtrend line and the 0.8545 resistance. Moving higher, the 0.8590 and the 0.8620 levels are coming next to switch the outlook to a more positive one.

All in all, EURGBP has been neutral in the very short-term, but the broader picture remains bearish.

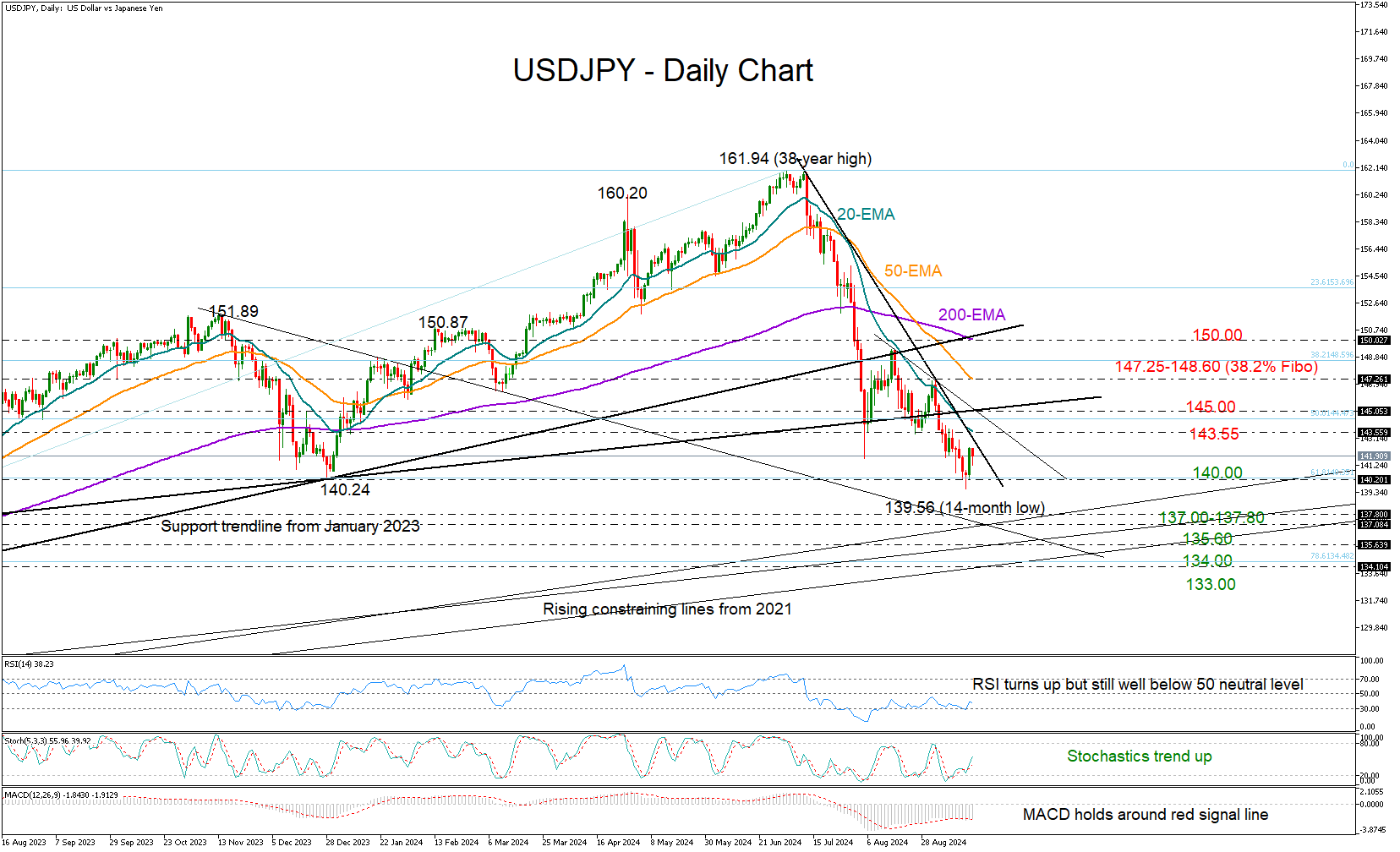

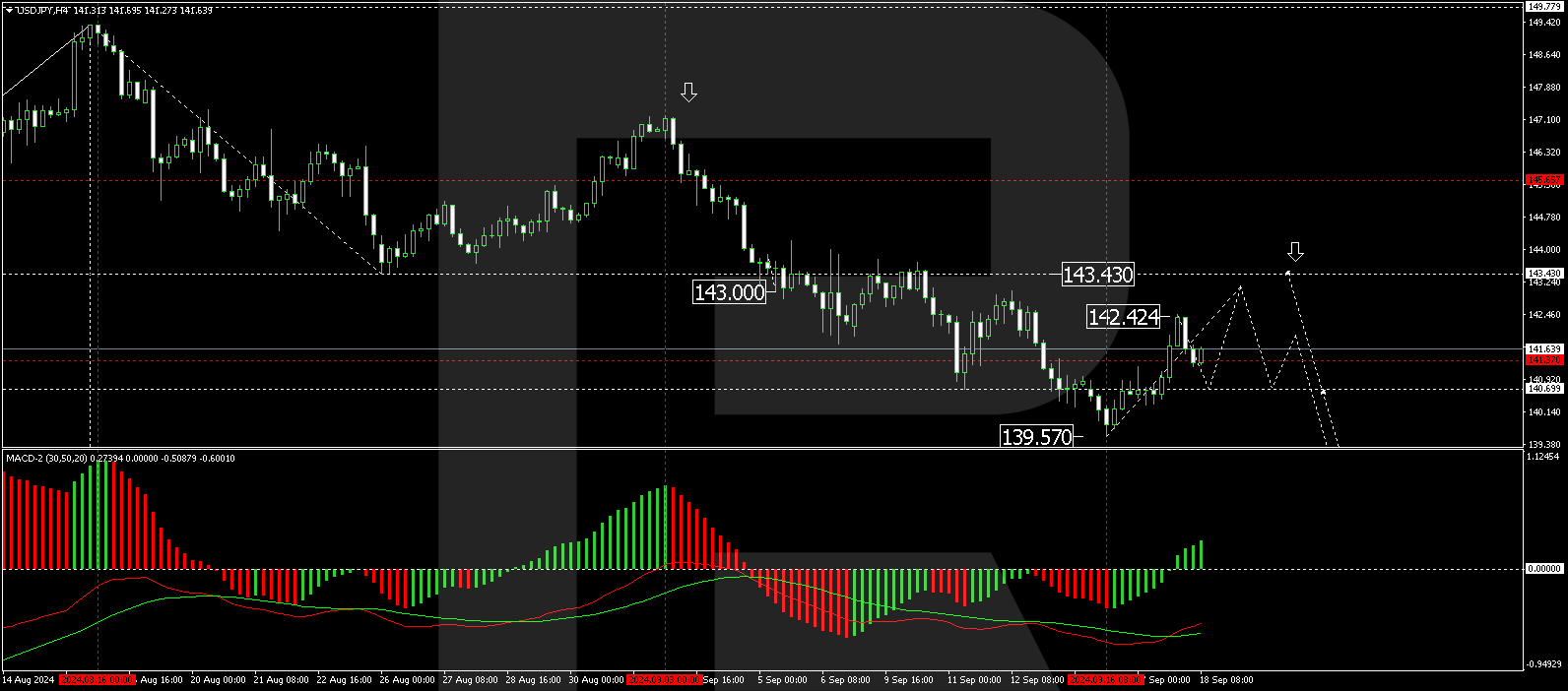

USDJPY Poised for a New Bullish Wave; Will It Succeed?

- USDJPY sets the ground for a bullish reversal, but it's still trapped below key resistance

- Technical signals cannot rule out more bearish actions; sellers wait below 140

- Fed to deliver its first rate cut in four years at 18:00 GMT

USDJPY turned green on Tuesday, marking its best daily session in a month after securing a solid base around the 140 number.

The time has finally come for the Fed to make a crucial decision between a 25bps or a 50bps rate cut today at 18:00 GMT and the pair seems to have completed a bullish dragonfly candlestick pattern. Following a steep downward trend from a 38-year high of 161.94, the price might again push for some recovery, especially if the central bank announces a normal 25bps reduction.

Nevertheless, previous bullish endeavors were unable to surpass the 20-day exponential moving average (EMA) at 143.55, and additional obstacles may arise at the 145.00 trendline region prior to the 50-day EMA at 147.25.

Despite a slight improvement in technical indicators, downside risks persist as the RSI remains deep in bearish territory. Nonetheless, only a close below the 140.00 floor could bolster selling forces towards the 137.00-137.80 trendline zone. There are two more constraining lines to the downside, passing through 135.60 and 134.00. Falling lower, the pair might next stop near 133.00.

In short, USDJPY may be preparing for its next consolidation or bullish phase, but it’s unknown if it will successfully break above the 20-day EMA and exceed 145.00.

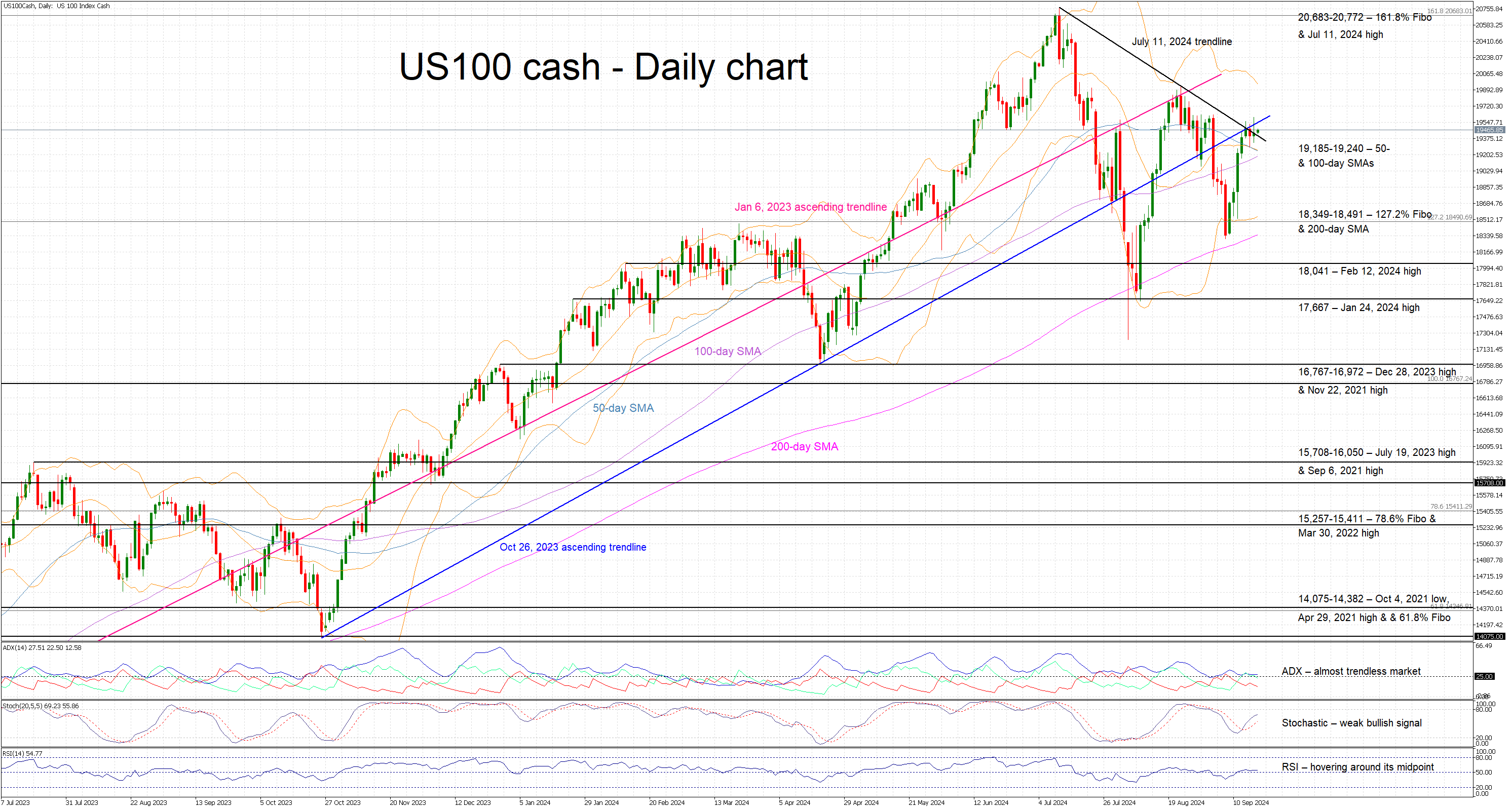

US 100 Index in Anticipation Mode Ahead of Fed

- US 100 index trades sideways ahead of the Fed meeting

- It battles with the July 11, 2024 descending trendline

- Momentum indicators are tentatively bullish

The US 100 cash index is moving sideways today, continuing its low volatility sessions, as market participants are staying on the sidelines ahead of the crucial Fed meeting. The first Fed rate cut since March 2020 will most likely be announced later today with speculation being rife about a 50bps rate cut, with arguable impact on stock markets. Interestingly, a series of lower highs indicates that the bearish trend that commenced on July 11, 2024 is still firmly in place.

In the meantime, the momentum indicators are slightly bullish. More specifically, the Average Directional Movement Index (ADX) is trading sideways and hence signalling a weak bullish trend in the US 100 index. Similarly, the RSI is hovering around its midpoint, confirming a lower volatility period. More importantly, the stochastic oscillator is edging higher, above its moving average. If this move picks up pace towards its overbought area, it would be seen as a very strong bullish signal.

Should the bulls feel confident, they could try to keep the US 100 index above the July 11, 2024 trendline and then overcome the October 26, 2023 long-term trendline. Their next aim could be to break the recent series of lower highs by staging a move above the 19,936 level.

If the bears regain the market reins, they could face strong support at the July 11, 2024 trendline and the 19,185-19,240 area, which is populated by the 50- and 100-day simple moving averages (SMAs). If successful, they could then have a go at pushing the US 100 index towards the key 18,349-18,491 region.

To sum up, market participants are in waiting mode for the Fed meeting that could result in increased volatility and potentially reverse the current bearish trend.

USDJPY Experiences Renewed Decline as Market Adjusts Expectations

The USDJPY pair is currently stabilising around 141.44 on Wednesday, following a brief strengthening of the US dollar which impacted the yen negatively the previous day. Despite this, the overarching downward trend for the pair persists.

Tuesday witnessed strong US retail sales data, bolstering the dollar's strength temporarily and leading to a correction in the JPY. However, as the week progresses, attention is also turning towards the Bank of Japan (BoJ), which is holding its policy meeting alongside the Federal Reserve's gathering.

The baseline expectation is that the BoJ will maintain its interest rate unchanged. Nevertheless, signals might emerge from the meeting indicating a readiness to tighten monetary policy later in the year. With two more meetings scheduled before year-end, in October and December, investor anticipation is growing for a potential rate hike in December, although expectations for October remain very low.

Today's focus is heavily on the Fed, which is widely anticipated to cut rates by 50 basis points, marking the first rate reduction in four years. This significant move could impact global currency dynamics, including the USDJPY pair.

Recent statistics from Japan showed only a minimal rise in imports over the past five months and subdued growth in exports for August, adding to the complex economic landscape.

Overall sentiment towards the yen remains positive, bolstered by the BoJ's cautious approach to gradually tightening monetary conditions.

Technical analysis of USDJPY

The USDJPY market has previously formed a consolidation range just below the level of 141.26, and with an upward breach of this range, the target at 142.42 was achieved. A corrective move to 141.22 has been established, and a further rise to 143.20 is anticipated. Upon reaching this peak, the potential for a new decline towards 137.77 will be considered. The MACD indicator supports this view, with the signal line below zero but pointing upwards, suggesting upward momentum in the short term.

On the H1 chart, following the completion of the corrective wave to 141.22, the market is expected to continue its upward trajectory towards 143.20. After achieving this level, a new decline to 141.20 is anticipated, with a breach below this level potentially signalling a continuation of the downward trend towards 137.77. The Stochastic oscillator, with its signal line above 20 and directed upwards, corroborates the likelihood of further upward movement before a potential reversal.

Market Analysis: EUR/USD Strengthens While USD/CHF Faces Hurdles

EUR/USD started a fresh increase above the 1.1050 resistance. USD/CHF declined and now struggling below the 0.8500 resistance.

Important Takeaways for EUR/USD and USD/CHF Analysis Today

- The Euro surged after it broke the 1.1050 resistance against the US Dollar.

- There is a connecting bullish trend line forming with support near 1.1125 on the hourly chart of EUR/USD at FXOpen.

- USD/CHF declined below the 0.8500 and 0.8460 support levels.

- There is a major bearish trend line forming with resistance near 0.8460 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair started a fresh increase from the 1.1000 zone. The Euro cleared the 1.1050 resistance to move into a bullish zone against the US Dollar, as mentioned in the last analysis.

The bulls pushed the pair above the 50-hour simple moving average and 1.1100. Finally, the pair tested the 1.1145 resistance. A high was formed near 1.1146 and the pair is now consolidating gains above the 23.6% Fib retracement level of the upward wave from the 1.1001 swing low to the 1.1146 high.

Immediate support on the downside is near a connecting bullish trend line at 1.1125. The next major support is the 1.1110 level. A downside break below the 1.1110 support could send the pair toward the 1.1075 level.

The 50% Fib retracement level of the upward wave from the 1.1001 swing low to the 1.1146 high is also at 1.1075. Any more losses might send the pair into a bearish zone toward 1.1050.

Immediate resistance on the EUR/USD chart is near the 1.1145 zone. The first major resistance is near the 1.1165 level. An upside break above the 1.1165 level might send the pair toward the 1.1200 resistance.

The next major resistance is near the 1.1250 level. Any more gains might open the doors for a move toward the 1.1285 level.

USD/CHF Technical Analysis

On the hourly chart of USD/CHF at FXOpen, the pair started a fresh decline from well above the 0.8520 zone. The US Dollar dropped below the 0.8490 support to move into a negative zone against the Swiss Franc.

The bears pushed the pair below the 50-hour simple moving average and 0.8475. Finally, the bulls appeared near the 0.8430 level. A low was formed near 0.8429 and the pair is now consolidating losses.

There was a minor increase above the 23.6% Fib retracement level of the downward move from the 0.8549 swing high to the 0.8429 low. However, the pair struggled to stay above 0.8460. On the upside, the pair could face resistance near the 0.8460 level and a major bearish trend line.

The next major resistance is near the 0.8475 level, above which the pair could test the 50% Fib retracement level of the downward move from the 0.8549 swing high to the 0.8429 low at 0.8490.

If there is a clear break above the 0.8490 resistance zone, the pair could start another increase. In the stated case, it could even surpass 0.8550.

On the downside, immediate support on the USD/CHF chart is 0.8430. The first major support is near the 0.8400 level. The next major support is near 0.8380. Any more losses may possibly open the doors for a move toward the 0.8350 level in the coming days.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

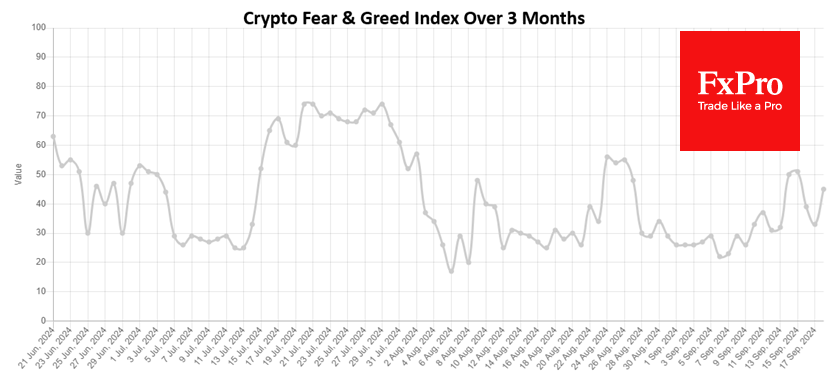

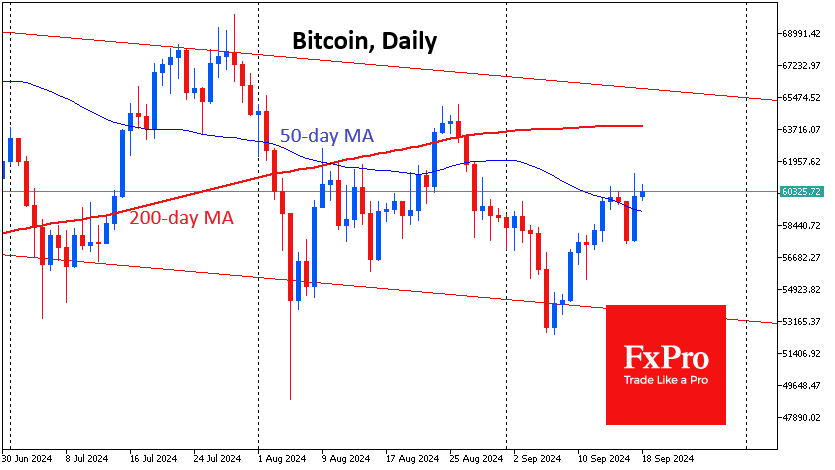

Crypto Market Gets a Boost from Stocks

Market Picture

The crypto market has gained 2.1% in the last 24 hours to reach $2.08 trillion. The rise in the stock market has brought buyers back to Bitcoin, which has positively impacted cryptocurrencies. The sentiment index is still in the fear zone, but at 45, it is already close to neutral territory. This shows that it is lagging stocks where sentiment has shifted to ‘greed’.

Bitcoin surpassed $60K, accelerating sharply at the start of the US session. The price peaked at $61.3K before retreating to $60.4K at the time of writing. Despite some pullback, bitcoin has broken above its 50-day moving average, suggesting significant upside potential. However, it isn’t easy to rely on today’s technical picture ahead of the Fed’s interest rate decision on Wednesday evening. The next important level is likely to be around the $64K, where the late August high and the 200-day average are located.

News Background

JPMorgan sees bitcoin hash rate growth slowing as miner revenues remain at historic lows. Meanwhile, US Bitcoin miners’ share of the network hash rate rose for the fifth consecutive month to 26.7%, an all-time high.

MicroStrategy will place $700 million in four-year unsecured convertible notes to acquire additional bitcoins and fund general corporate purposes.

According to Arkham, the Bhutanese government’s bitcoin holdings amount to 13,036 BTC ($770 million), almost three times El Salvador’s reserves. The country has the world’s fourth-largest stockpile of BTCs, derived from mining by a sovereign wealth fund.

The crypto industry is no longer able to provide ‘dopamine’ to either developers or traders. That is why it is in crisis, said CryptoQuant CEO Ki Young Ju. According to him, the crypto industry is gradually turning into a ‘gambling den’.

Developers Curve Finance and TON Foundation will create a platform for trading stablecoins on the TON blockchain. The new initiative will meet the growing demand for stablecoins and increase the liquidity and popularity of the network’s Web3 ecosystem.

Markets Will Finally Get the Fed Verdict Today

Markets

August US retail sales were supposed to provide final input yesterday as investors concluded their positioning going into today’s Fed policy decision. Overall the report was marginally stronger than expected (headline sales +0.1% vs -0.2% expected after a strong upwardly revised 1.1% in July, core control group sales 0.3% M/M as expected but July upwardly revised to 0.4%). It is very unlikely that it will have a material impact on the Fed’s decision making. Still, the report provided somewhat of a trigger for some investors to take profit on Fed-easing bets after the recent protracted rally. US yields rebounded between 5.4 bps (5 2-y) and 2.8 bps (10-y). Markets still see a 60% chance for the Fed to start with a 50 bps step this evening. German yields in sympathy followed a similar trajectory (2-y +4.4 bps, 30-y -0.2 bps). The Dow (-0.04%) and the S&P 500 (+0.03%) touched new intraday record levels early in the session, but gains could not be sustained. Intraday dynamics in yields (modest rebound) and equities (correcting off the highs) also kept the dollar away from nearby support levels. DXY closed at 100.89 (vs key support at 100.51). EUR/USD stalled ahead of the 1.1155 intermediate resistance (close 1.1114). USD/JPY rebounded from 140.6 to 142.4. Oil still tries to develop a bottoming out process of the sharp decline earlier this month (Brent $73.25 p/b).

Markets will finally get the Fed verdict today. We prefer a scenario of Powell and co starting with a substantial reduction of policy restriction (50 bps) to avoid an unnecessary weakening of the labour market. Current high policy yield levels allow to do so. It still leaves the Fed the option to make a revaluation on both inflation and growth with the policy rate above neutral (end this year/early next year). In this scenario, an assumed additional cumulative 75 bps of easing signaled in the median dot plot for the remainder of the year might still support recent dynamics of markets staying asymmetrically sensitive to softer than expected activity/labour market data. The message from the dots for 2025 might be much less aggressive than what markets are currently discounting, but it’s probably too early as a driver for markets in the near term. In this context we also stay cautious on the dollar.

This morning’s UK August CPI data also brought tomorrow’s BoE policy decision back in the spotlights. The report was perfectly in line with expectations. Headline inflation printed at 0.3% M/M and 2.2% Y/Y (unchanged from July). Core inflation rose 0.5% M/M and 3.6% Y/Y (from 3.3%). Services inflation also stays elevated at 0.4% M/M and 5.6% Y/Y (from 5.2%). Especially the monthly dynamics in core and services inflation indicates that there is little reason for the BoE already to take another advance on easing inflation after the August 01 in augural rate cut. Sterling strengthens from EUR/GBP 0.845 to 0.844 in a first reaction after the release.

News & Views

Andrius Kubilius, former prime minister of Lithuania and the EU’s first-ever defense chief, said that the EU can’t wait until the next 7-yr budget in 2028 to increase its defense spending. While that’s still a national authority, he wants to support the fragmented industrial military base. He suggested exploring the option of issuing joint bonds to raise an additional €500bn or to tap the bloc’s bailout fund or use unspent money from the Recovery and Resilience Facility. The debate on issuing more mutual (EU) debt is gaining again more and more momentum since Mario Draghi published his report on competitiveness.

The Bank of France left its growth forecast for next year unchanged at 1.2% and slightly lowered the 2025 prognosis to 1.5% from 1.6%. Governor Villeroy said that the French economy is recovering from the acute illness of the last two years: inflation. Now we must treat our two chronic illnesses of too much debt and not enough growth, he added. The national bank lowered its average inflation forecast for next year from 1.7% in June to 1.5%, mainly due to weaker electricity prices. Inflation is set to average 2.5% this year.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) make follow-up moves less evident. We expect the central bank to stick with the quarterly reduction pace. Disappointing US and unconvincing EMU activity data dragged the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed in its July meeting paved the way for a first cut in September. It turned attentive to risks to the both sides of its dual mandate as the economy is moving to a better in to balance. The pivot weakened the technical picture in US yields. A string of weak eco data and a risk-off market climate pushed and kept the 10-yr sub 4%. We think we could be up to three 50 bps rate cuts this year.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large rate cuts trumped traditional safe haven flows into USD. EUR/USD 1.1276 (2023 top) serves as next technical references.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Recent better UK activity data and a cautious assessment of BoE’s Bailey at Jackson Hole are pushing EUR/GBP lower in the 0.84/0.086 range.

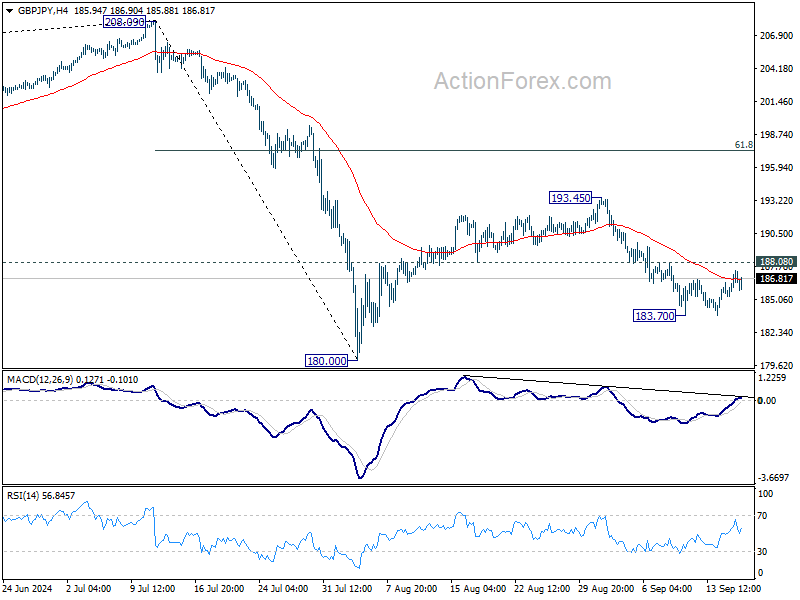

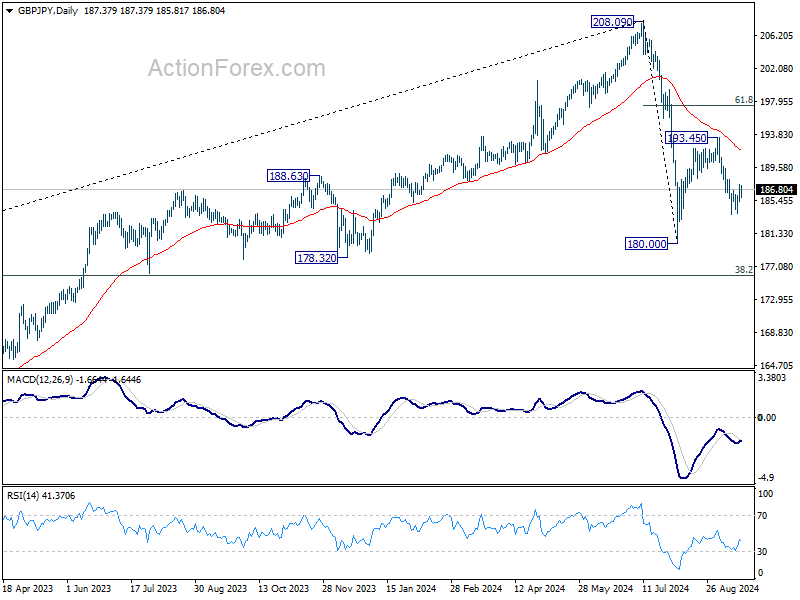

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.00; (P) 186.73; (R1) 188.17; More...

Intraday bias in GBP/JPY remains neutral at this point. Further decline is in favor with 188.08 minor resistance intact. Below 183.70 will resume the fall from 193.45 to retest 180.00 low. Firm break there will extend whole decline from 208.09 to 175.94 fibonacci level. However, break of 188.08 will argue that fall from 193.45 has completed already, and turn bias back to the upside for this resistance.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

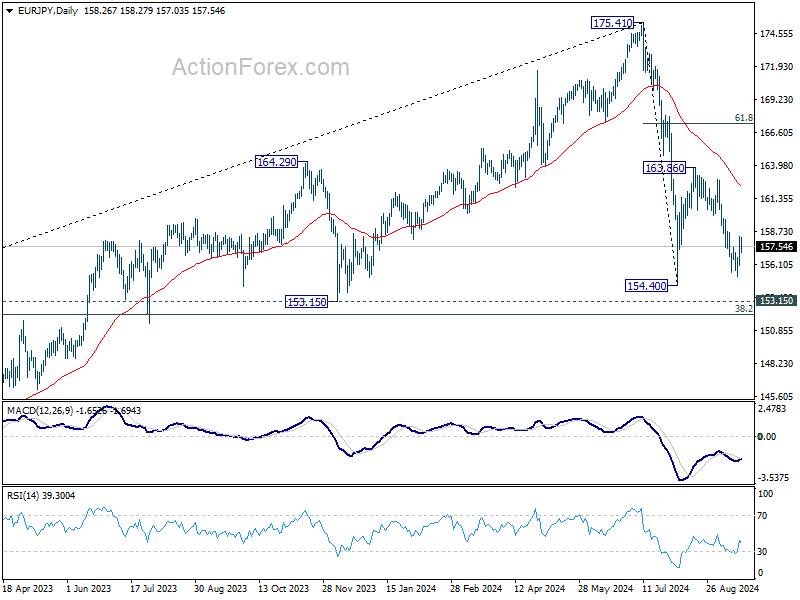

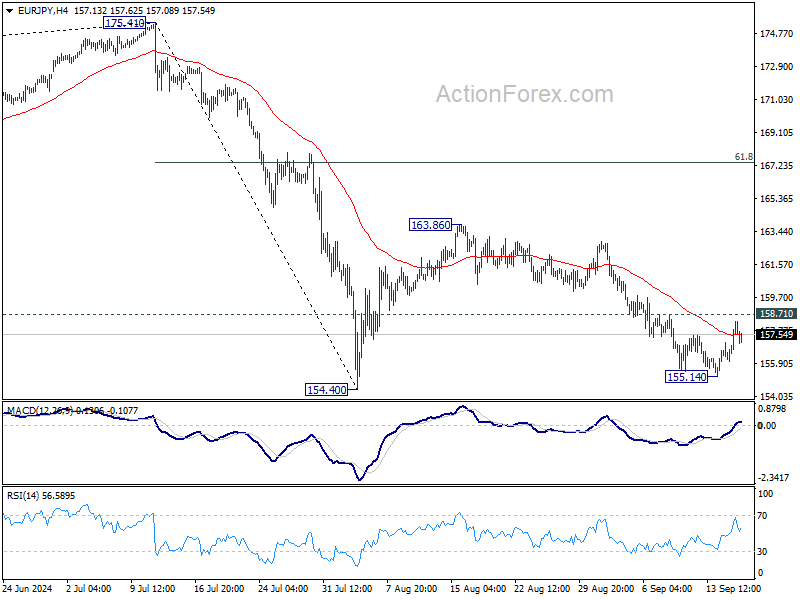

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.78; (P) 157.55; (R1) 159.06; More....

Intraday bias in EUR/JPY remains neutral for the moment. Further decline is expected as long as 158.71 resistance holds. Decisive break of 154.40 low will resume whole decline from 175.41 to 153.15 support, and possibly further to 152.11 fibonacci level. However, firm break of 158.71 will suggests that choppy fall from 163.86 has completed, and turn bias back to the upside for this resistance, as the third leg of the pattern from 154.40.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.