Sample Category Title

Stagflation test begins: PMIs to reveal growth shock and rising costs

The final full week of March opens with markets transitioning from pricing an energy shock to testing its real economic impact. With Persian Gulf exports largely halted, oil prices remains elevated and the inflation impulse is now firmly embedded. The focus shifts to whether this shock is beginning to translate into slower growth, setting up a stagflation backdrop.

Last week’s dominant theme—monetary policy divergence—remains intact, but the emphasis is now on validation. Markets have already repriced central banks toward a more hawkish stance in response to energy-driven inflation. The key question this week is whether incoming data will justify that shift or challenge it by revealing early signs of demand destruction.

The "High Stakes": UK & AU CPI

UK February CPI stands out as one of the week’s most important releases. Headline inflation is expected to hold at 3.0% yoy, with core at 3.1%. Even though the data largely reflects pre-war conditions, it will be interpreted as a "floor" for where inflation is heading under the new energy regime.

An upside surprise in UK CPI would reinforce expectations that Bank of England would need to tighten sooner or more aggressively. That would likely support Sterling, particularly against Euro and Swiss Franc. A softer print, however, may have limited impact, as markets are likely to look through backward-looking data in light of rising energy costs.

Australia’s monthly CPI will play a similar role for the Australian Dollar. Inflation is expected to hold at 3.8% yoy in February. Even though RBA has already delivered consecutive hikes, markets are leaning toward another move in May, after getting Q1 CPI report.

An upside surprise could raise expectations that RBA’s tightening cycle is not yet complete even after May, boosting AUD, particularly against Dollar.

The "Silent Movers": Flash PMIs from JPY, AU, EZ, UK, and US.

Flash March PMI releases from Japan, Australia, Eurozone, UK, and the US will be where the real stagflation test begins. Unlike CPI, which largely reflects pre-escalation conditions, PMIs offer the first timely read on how the Iran war and oil shock are feeding through to both activity and pricing dynamics. This makes them the most forward-looking indicators of whether the macro regime is shifting.

The key focus on the growth side will be new orders and business expectations. Deterioration in these components would signal that elevated energy costs and geopolitical uncertainty are already weighing on demand. If businesses start to scale back orders and turn more cautious on outlook, it would confirm that the shock is not just inflationary, but also growth-destructive.

At the same time, input price indexes will be critical in assessing the inflation channel. With supply disruptions and transport costs rising, firms are likely facing a sharp increase in production costs. If PMIs show accelerating input prices alongside weakening output, it would provide clear evidence that stagflation dynamics are taking hold.

Crucially, the data could also highlight divergence across regions. Economies more exposed to energy imports, particularly in Europe, may show a sharper deterioration in growth alongside stronger cost pressures. In contrast, more insulated economies could display greater resilience. This divergence would reinforce the current split in monetary policy expectations, with some central banks forced toward tightening while others retain room to wait, further shaping FX dynamics.

Here are some highlights for the week:

United States:

The US calendar is relatively light on top-tier data, but focus remains on growth momentum and consumer resilience amid rising energy costs.

- Flash S&P Global PMIs (Tuesday).

Eurozone:

The Eurozone is particularly sensitive to energy market disruptions, and this week's data will highlight the extent of the economic "pinch."

- Flash PMIs (Tuesday).

- German Ifo Business Climate & GfK Consumer Sentiment (Tuesday/Wednesday).

Japan:

The focus is on whether inflation is becoming sticky enough to warrant further BoJ normalization.

- National CPI (Tuesday).

- BoJ Monetary Policy Meeting Minutes (Wednesday).

- Flash PMIs (Tuesday).

United Kingdom:

The UK faces a high-impact week with a focus on whether the BoE will need to pivot to a more hawkish stance.

- Consumer Price Index (Wednesday).

- Flash PMIs (Tuesday).

- Retail Sales (Friday).

Australia:

Aussie is caught between hawkish RBA and global risk-off sentiment.

- AU Consumer Price Index (Wednesday).

- AU Flash PMIs (Monday).

Eco Data 3/23/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 14:00 | USD | Construction Spending M/M Jan | -0.30% | 0.10% | 0.30% | 0.80% |

| 15:00 | EUR | Eurozone Consumer Confidence Mar P | -16 | -15 | -12 |

| 14:00 | USD |

| Construction Spending M/M Jan | |

| Actual | -0.30% |

| Consensus | 0.10% |

| Previous | 0.30% |

| Revised | 0.80% |

| 15:00 | EUR |

| Eurozone Consumer Confidence Mar P | |

| Actual | -16 |

| Consensus | -15 |

| Previous | -12 |

EUR/USD Weekly Outlook

EUR/USD recovered last week but upside is capped below 1.1666 cluster resistance (38.2% retracement of 1.2081 to 1.1408 at 1.1665). Initial bias remains neutral this week, and further decline is in favor. On the downside, below 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. However, decisive break of 1.1666 will argue that the fall from 1.2081 has completed, and turn bias back to the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824.

In the bigger picture, prior break of 55 W EMA (now at 1.1495) should confirm rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. Deeper fall is expected to long term channel support (now at 1.0528). Meanwhile, risk will stay on the downside as long as 1.2081 holds, even in case of strong rebound.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

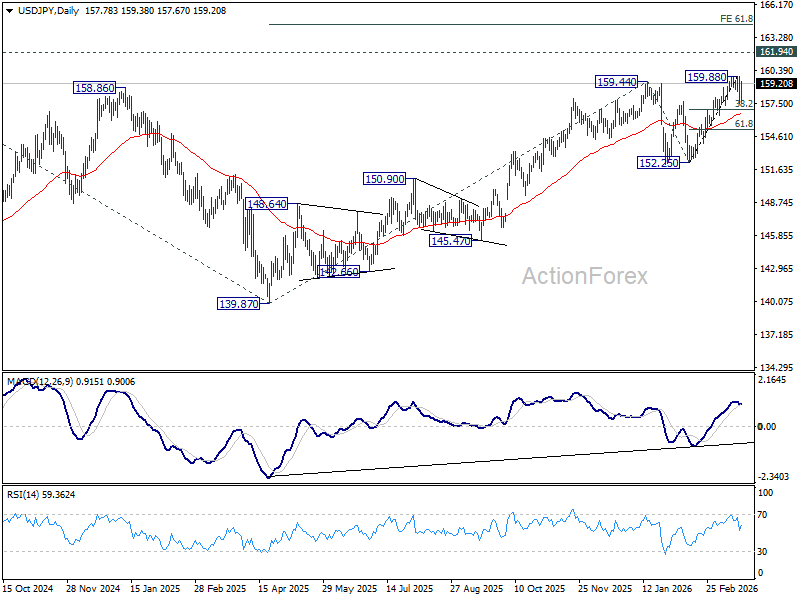

USD/JPY Weekly Outlook

Last week's development suggests that a short term top was in place at 159.88. Price actions from there is correcting the rally from 152.25. Initial bias is neutral this week and more sideway trading could be seen. In case of another dip, downside should be contained by 38.2% retracement of 152.25 to 159.88 at 156.96. On the upside, break of 159.88 will target a test on 161.94 high.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.70) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

www.actionforex.com/wp-content/uploads/2026/03/usdjpy2060321w2-600x450.png" alt="" width="600" height="450" class="aligncenter size-medium wp-image-634212" />

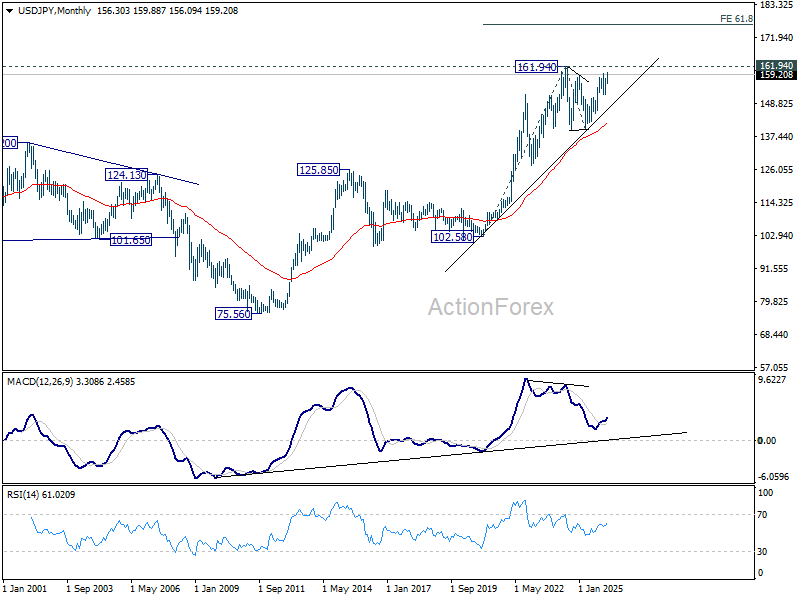

In the long term picture, up trend from 75.56 (2011 low) is still in progress and might be ready to resume. Firm break of 161.94 will target 61.8% projection of 102.58 (2020 low) to 161.94 (2024 high) from 139.87 at 176.55 in the medium term. Long term outlook will stay bullish as long as 139.87 support holds, even in case of deep pullback.

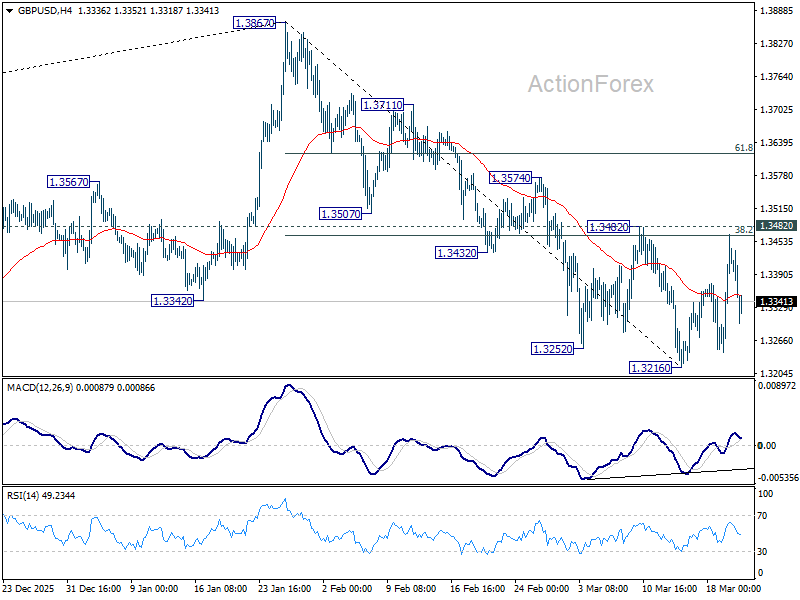

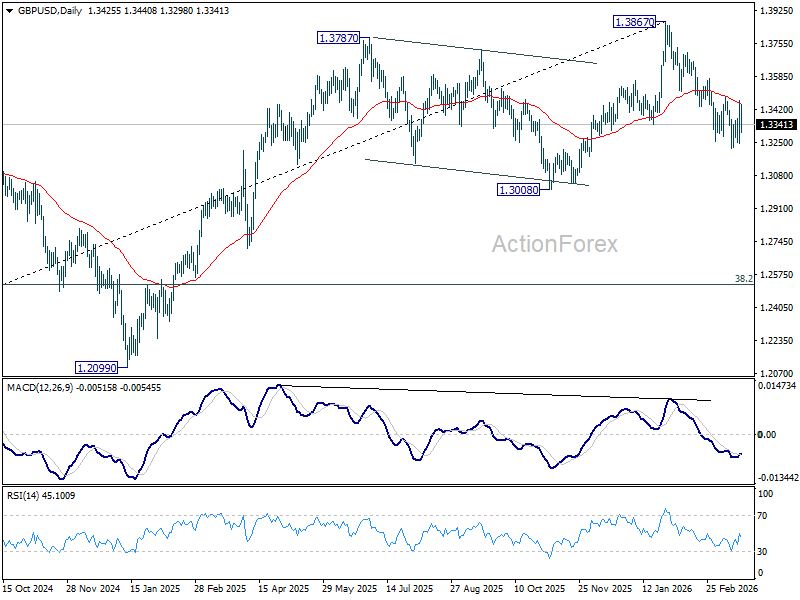

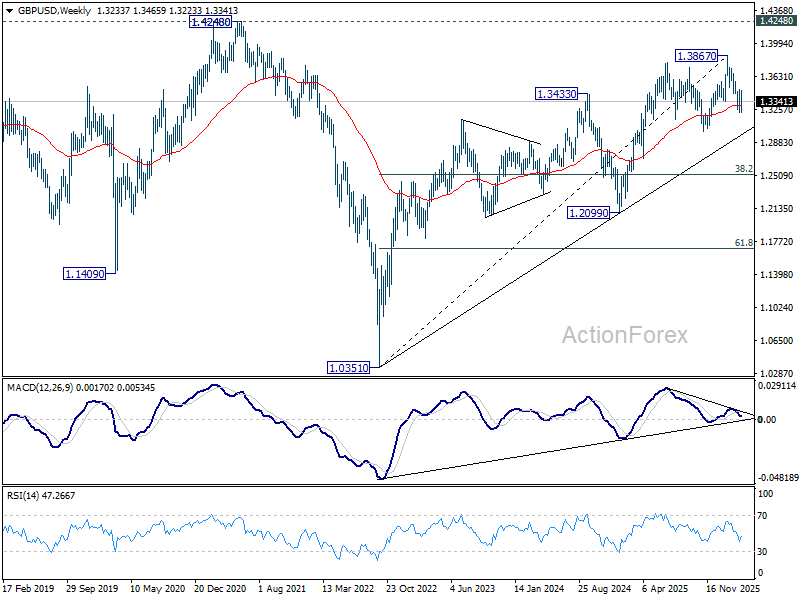

GBP/USD Weekly Outlook

GBP/USD's rebound was capped below 1.3482 resistance last week and reversed. Initial bias stays neutral this week and further decline remains in favor. On the downside, below 1.3216 will resume the fall from 1.3867 to 1.3008 structural support. However, decisive break of 1.3482 will argue that the fall from 1.3867 has completed, and turn bias back to the upside for 61.8% retracement of 1.3867 to 1.3216 at 1.3618.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place at 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or until further development.

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.0351 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.

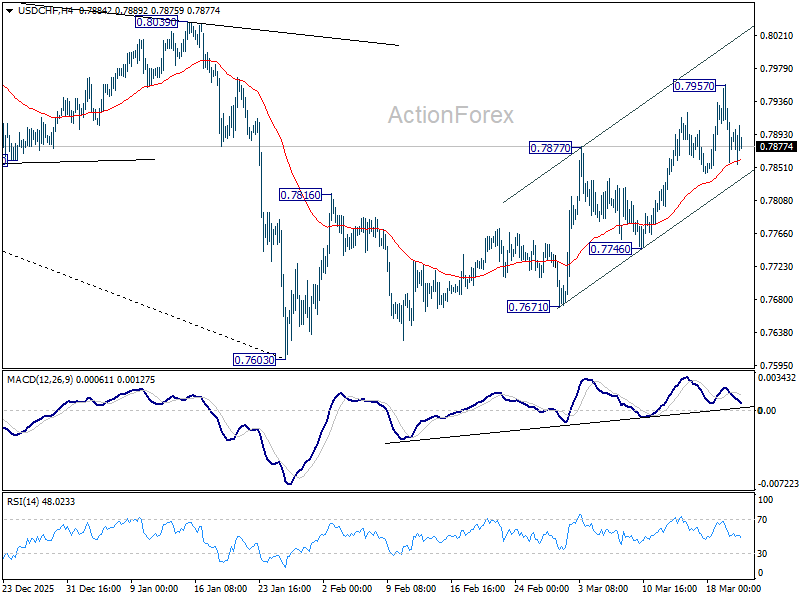

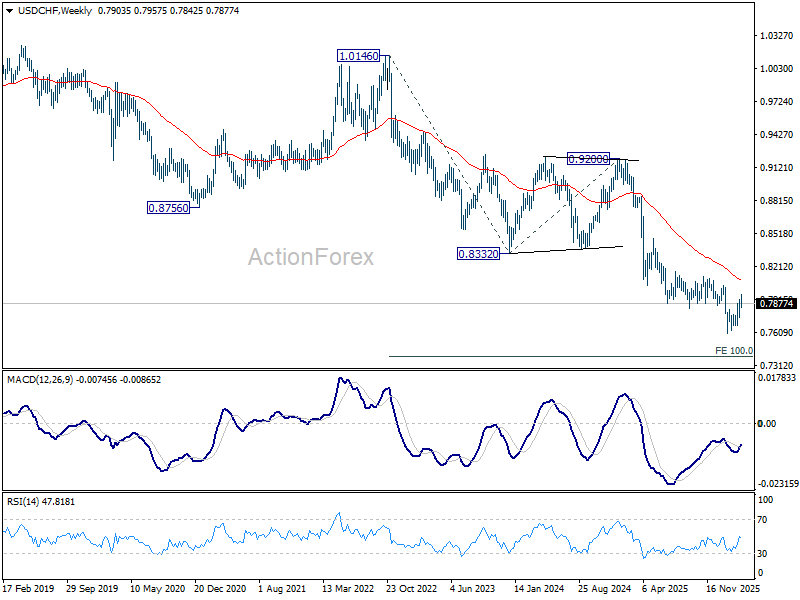

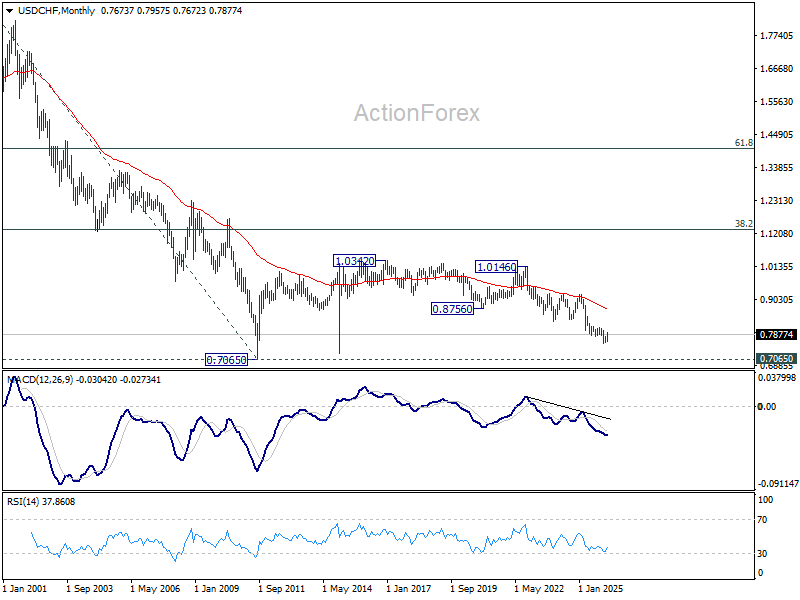

USD/CHF Weekly Outlook

USD/CHF edged higher to 0.7957 last week but retreated. Initial bias remains neutral this week first. As noted before, rise from 0.7603 should be corrective whole decline from 0.9200. Above 0.7957 will target 38.2% retracement of 0.9200 to 0.7603 at 0.8213. This will remain the favored case as long as 0.7746 support holds.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8091) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

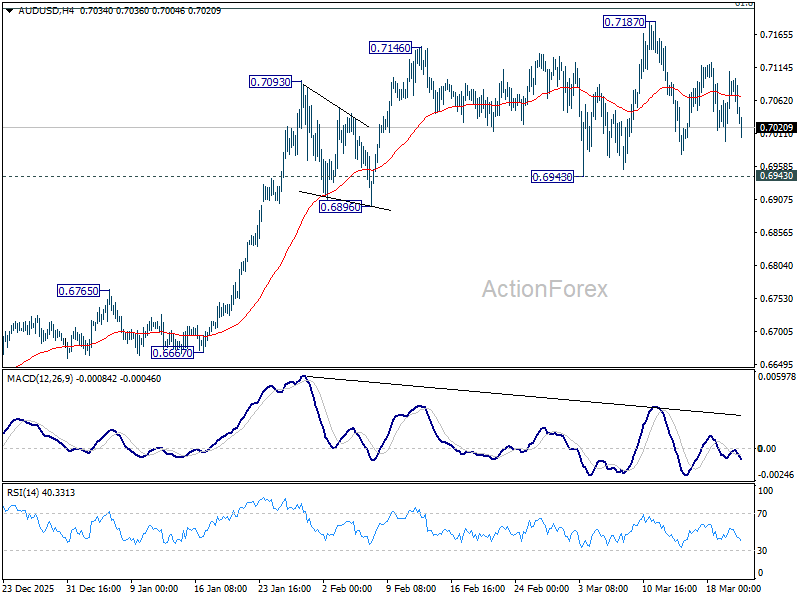

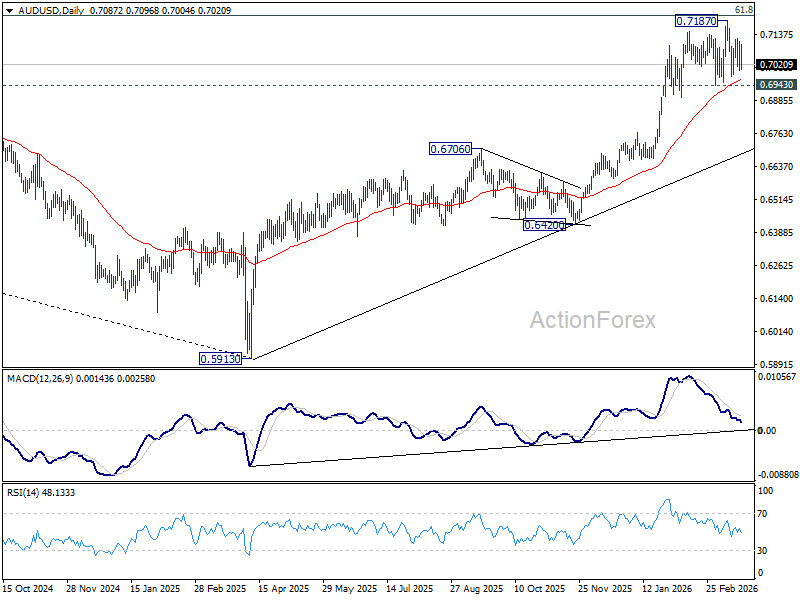

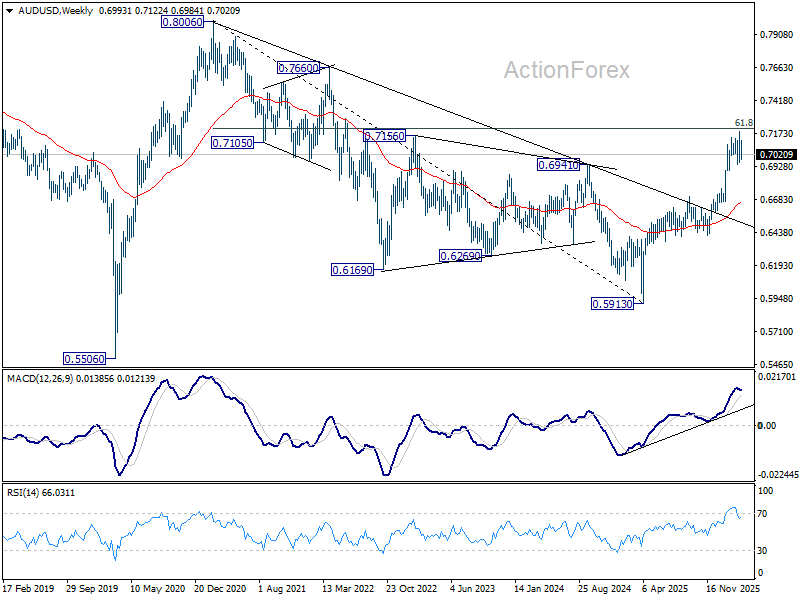

AUD/USD Weekly Report

AUD/USD remained bounded in established range last week and outlook is unchanged. Initial bias stays neutral this week. With 0.6943 support intact, further rally is still expected. On the upside, firm break of 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 could prompt upside acceleration to 161.8% projection at 0.7703. However, firm break of 0.6943 will indicate that a larger scale correction is already underway.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will pave the way back to 0.8006. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

In the long term picture, rise from 0.5913 is seen as the third leg of the whole pattern from 0.5506 (2020 low). It's still early to judge if this is an impulsive or corrective pattern. But in either case, further rise should be seen back to 0.8006 and possibly above.

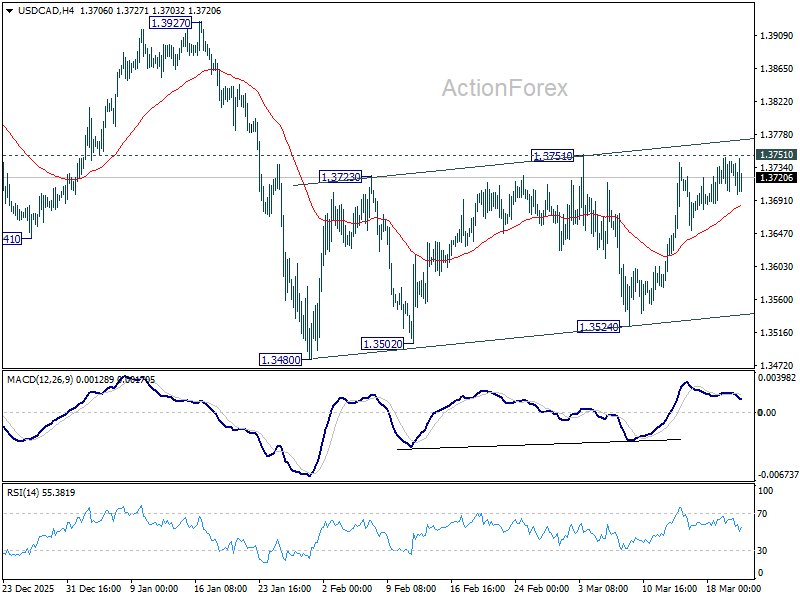

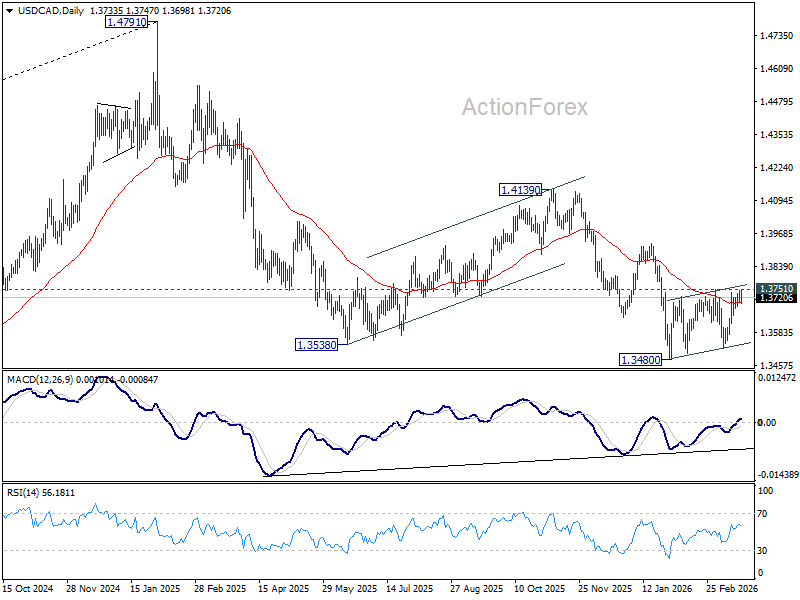

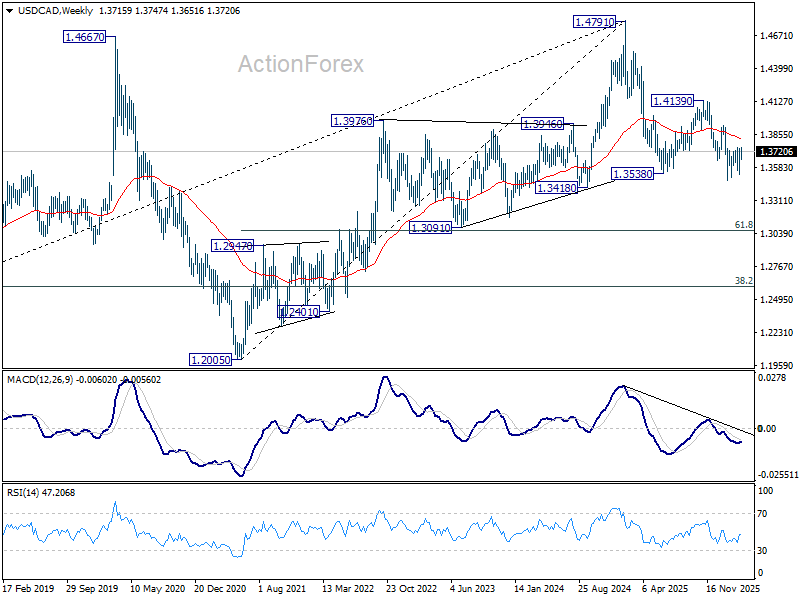

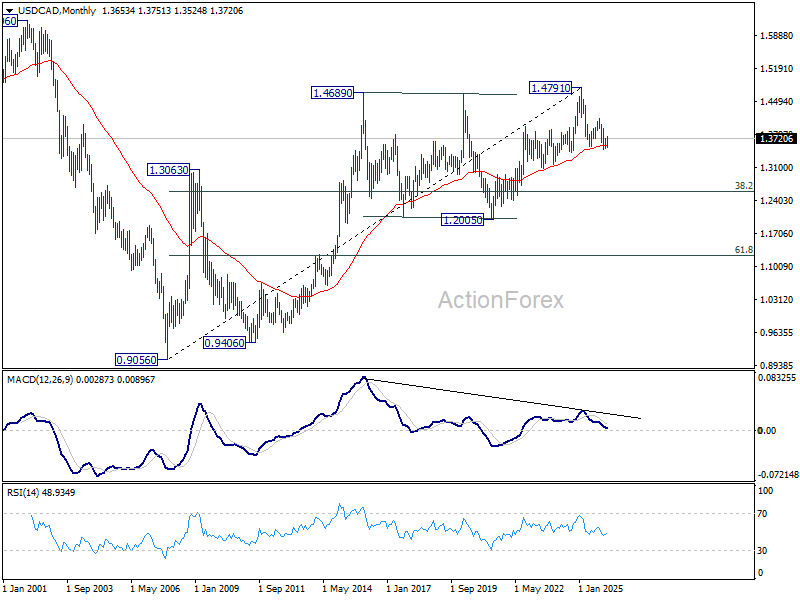

USD/CAD Weekly Outlook

USD/CAD failed to break through 1.3751 resistance last week and retreated. Initial bias remains neutral this week first. On the upside, firm break of 1.3751 resistance will suggest that stronger rebound is underway, and target 1.3927 resistance first. Meanwhile, break of 1.3524 support will bring resumption of whole down trend from 1.4791 through 1.3480 low.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, break of 1.3927 resistance will argue that the correction has completed with three waves down to 1.3480 already.

In the long term picture, rising 55 M EMA (now at 1.3574) remains intact. Thus, up trend from 0.9056 (2007 low) could still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

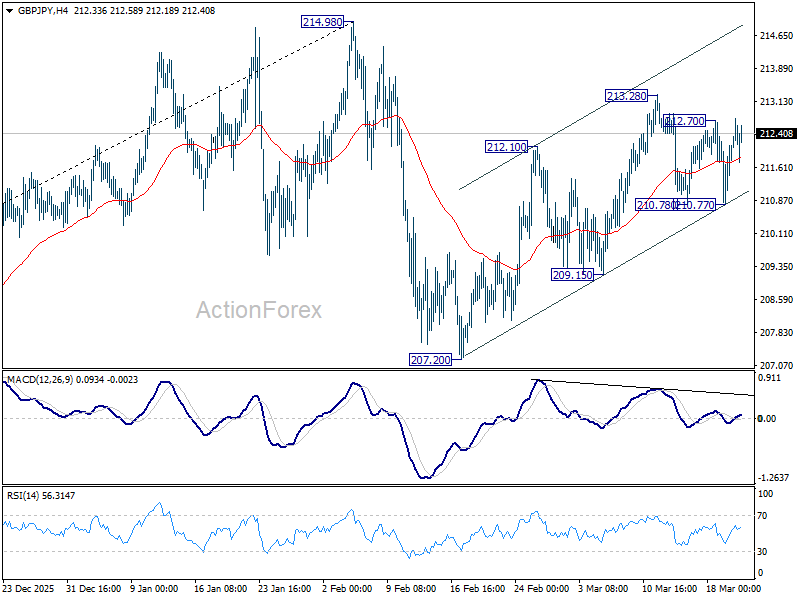

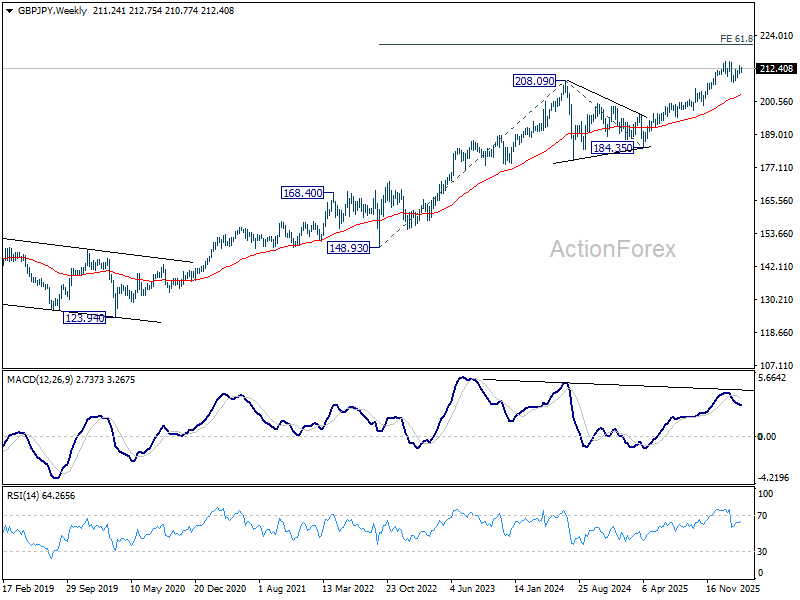

GBP/JPY Weekly Outlook

GBP/JPY's late breach of 212.70 resistance argues that rebound from 207.20 might be resuming. Initial bias is mildly on the upside this week for 213.28 first. Firm break there will target a retest on 214.98 high. For now, risk will stay mildly on the upside as long as 210.77 support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.13) holds, even in case of another deep pullback.

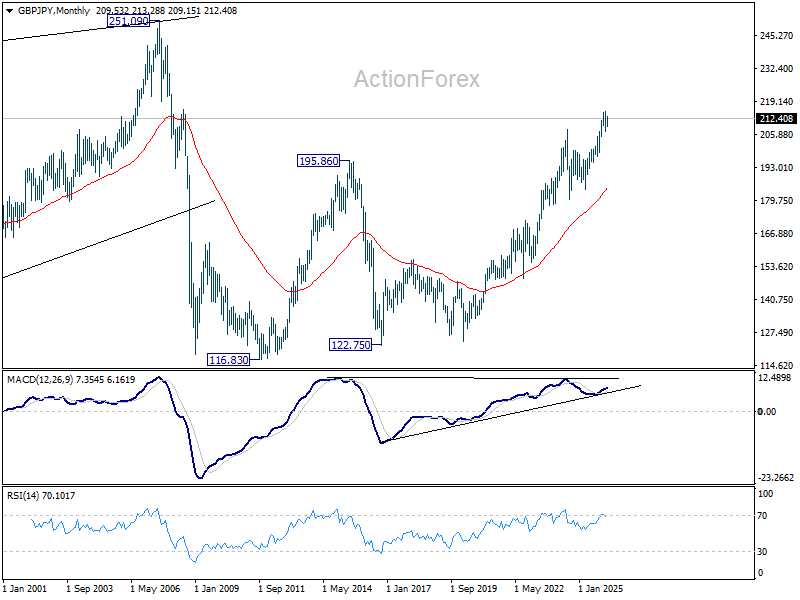

In the long term picture, up trend from 116.83 (2011 low) is in progress. Next target is 251.09 (2007 high). This will remain the favored case as long as 55 M EMA (now at 184.02) holds.

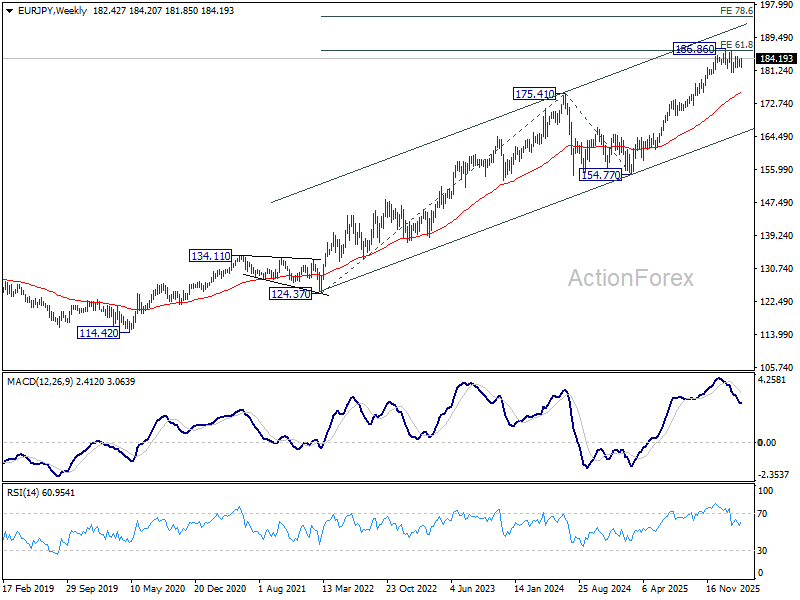

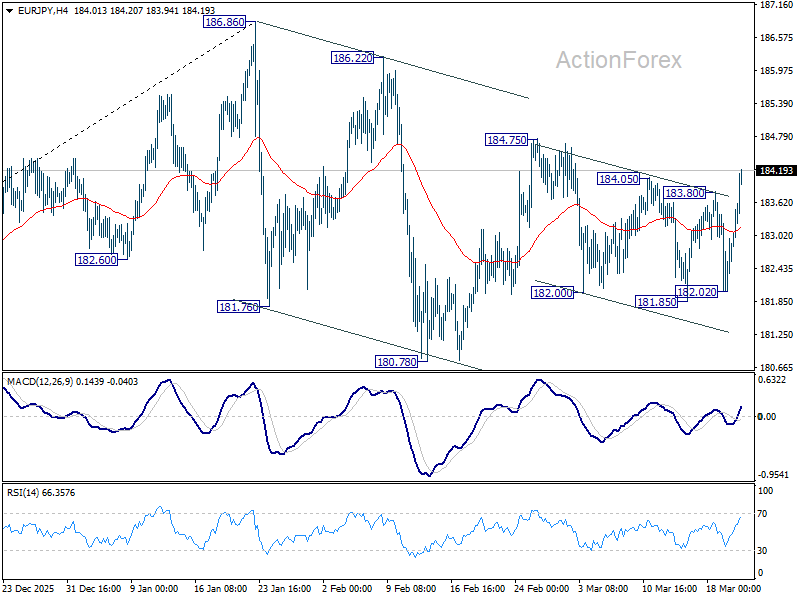

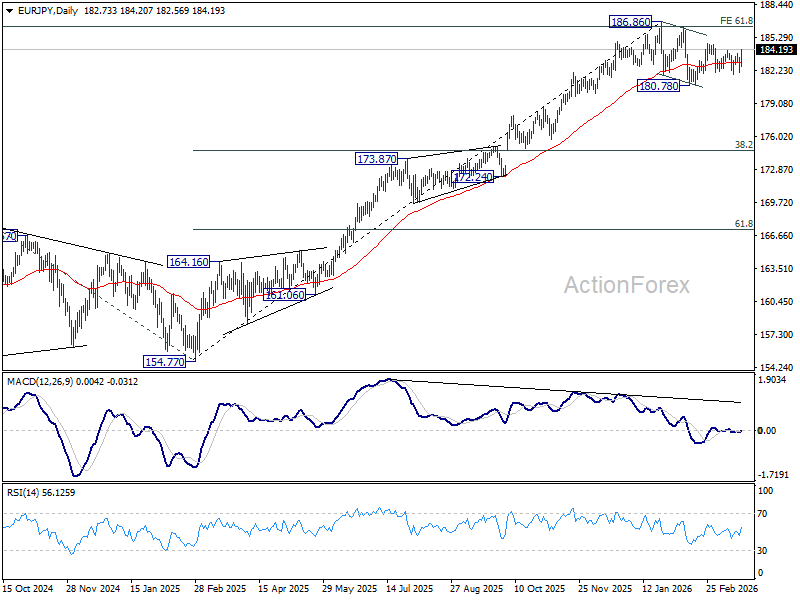

EUR/JPY Weekly Outlook

EUR/JPY's late rally and break of 183.80 resistance suggests that rebound from 180.78 is resuming. Initial bias is now on the upside this week. Firm break of 184.75 will confirm and target a retest on 186.86 high. For now, risk will stay mildly on the upside a long as 182.02 support holds, in case of retreat.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 175.61) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.