Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3144; (P) 1.3168; (R1) 1.3198; More...

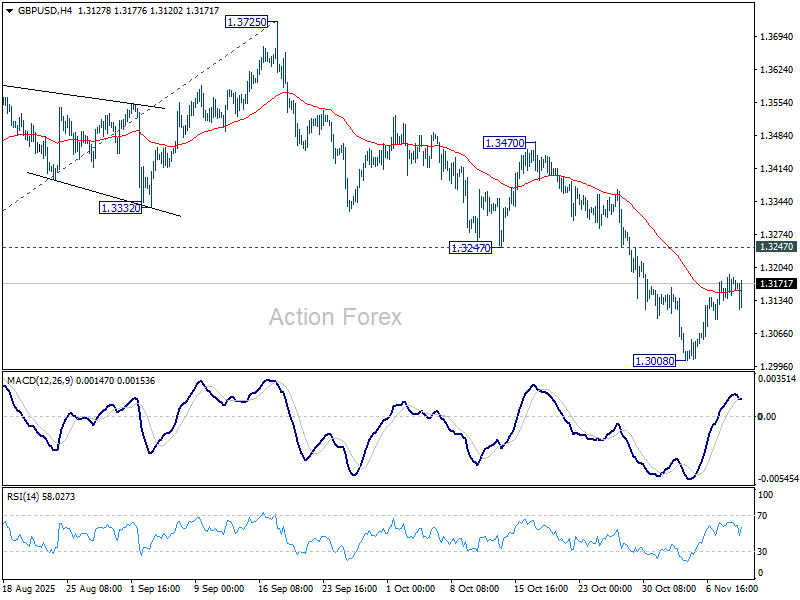

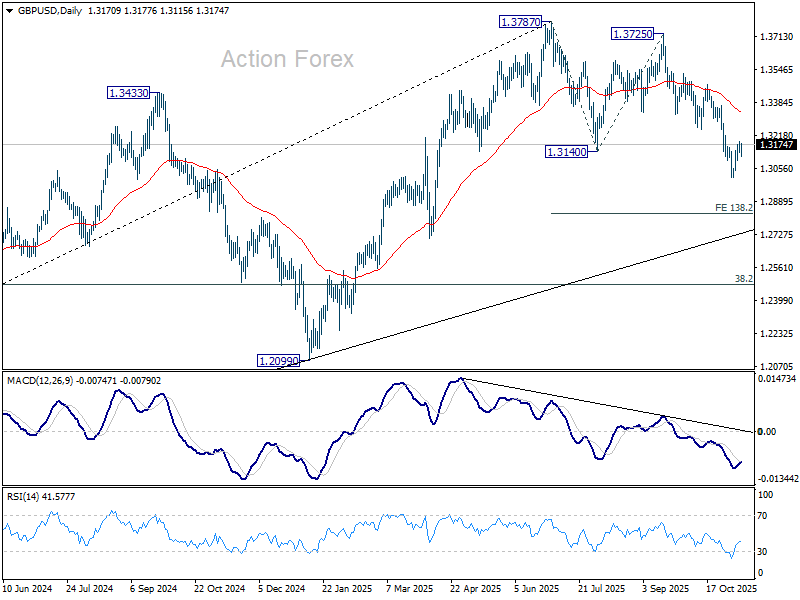

No change in GBP/USD's outlook and intraday bias stays neutral. More consolidations would be seen above 1.3008. Further decline is expected as long as 1.3247 support turned resistance holds. Break of 1.3008 will target 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3185) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2780) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8038; (P) 0.8056; (R1) 0.8067; More…

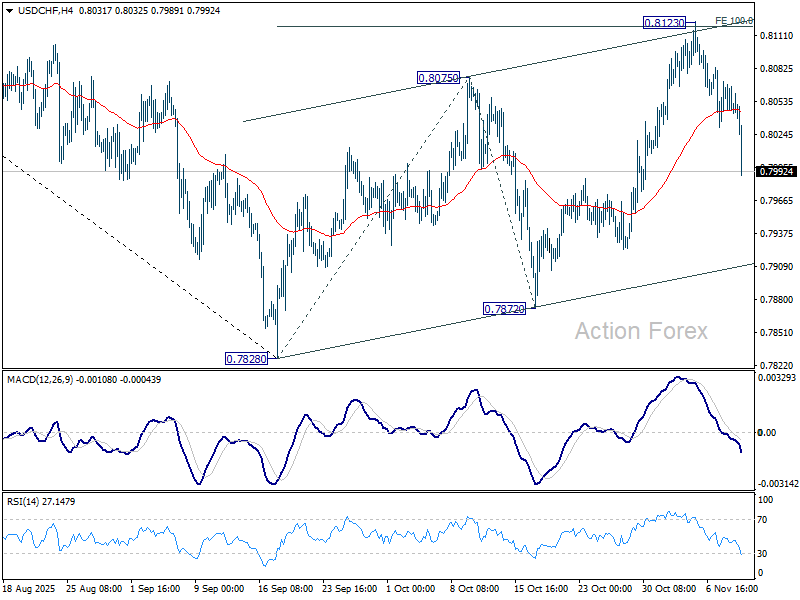

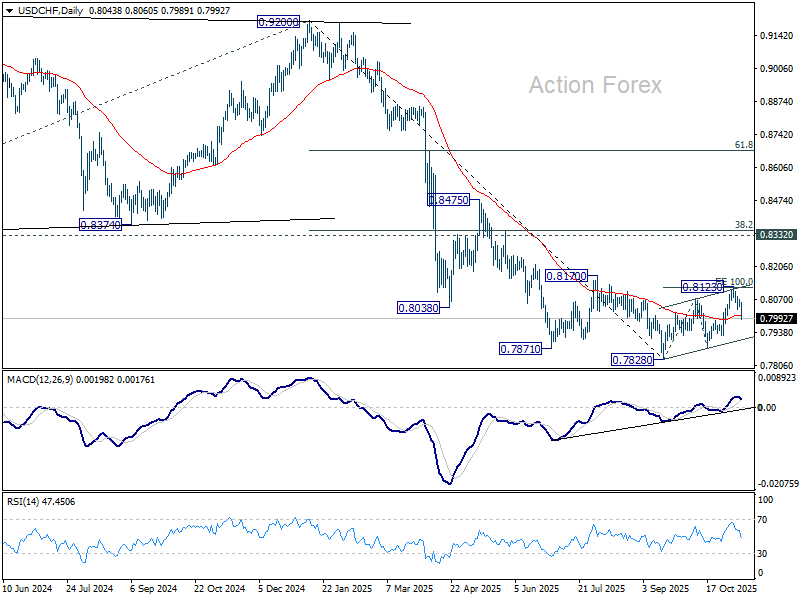

USD/CHF's fall from 0.8123 accelerates lower today. Break of 55 D EMA (now at 0.8008) suggests that corrective rebound from 0.7828 has completed with three waves up to 0.8123. Intraday bias is back on the downside for 0.7872 support. Firm break there will argue that larger down trend is ready to resume 0.7828 low. For now, risk will stay on the downside as long as 0.8123 resistance holds, in case of recovery.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

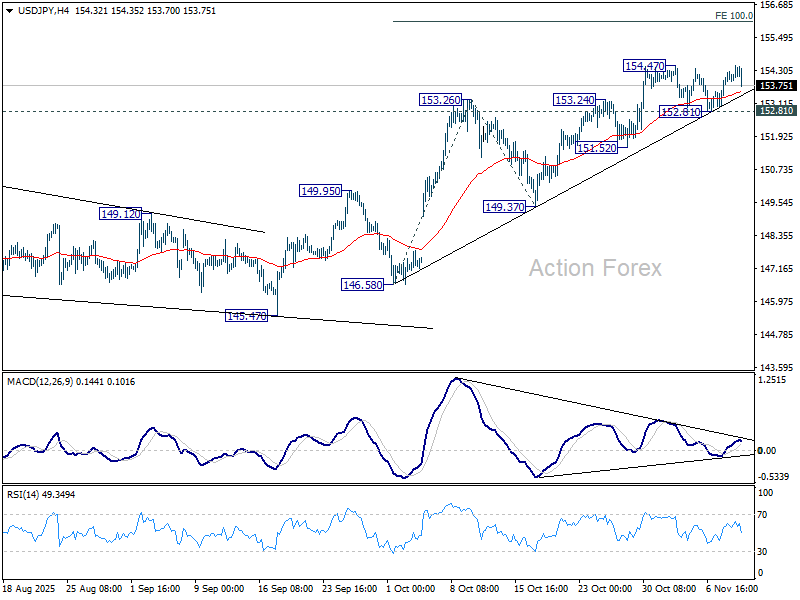

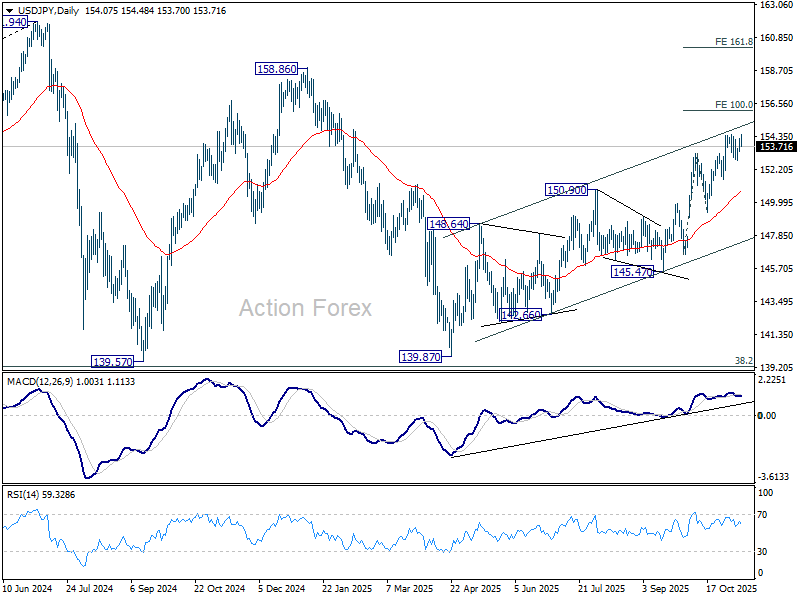

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.64; (P) 153.95; (R1) 154.43; More...

USD/JPY failed to break through 154.47 resistance decisively and retreated. Intraday bias remains neutral for the moment. Further rise is in favor as long as 152.81 support holds. Firm break of 154.47 will confirm resumption of whole up trend from 139.87. Next target is 100% projection of 146.58 to 153.26 from 149.37 at 156.05. However, break of 152.81 support will turn bias back to the downside for 149.37 support for deeper correction.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.

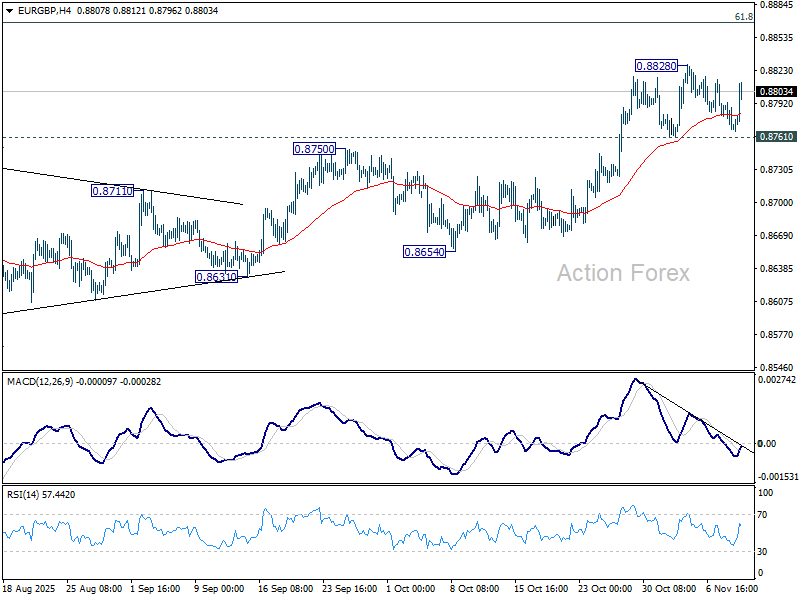

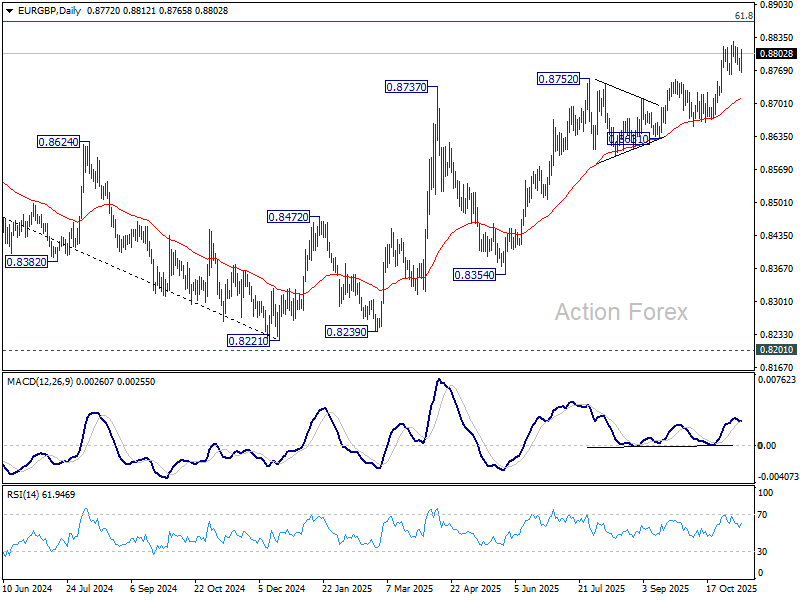

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8762; (P) 0.8779; (R1) 0.8788; More…

EUR/GBP rebounded notably today but stays in range below 0.8828. Intraday bias remains neutral and more consolidations could be seen. Further rally is expected as long as 0.8761 support holds. On the upside, break of 0.8828 will resume the whole rise from 0.8221 and target 0.8867 fibonacci level. Firm break there will carry larger bullish implications. However, considering bearish divergence condition in 4H MACD, decisive break of 0.8761 will confirm short term topping, and bring deeper fall to 55 D EMA (now at 0.8710).

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Firm break of 0.8654 support will be the first sign that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high).

Pound Pressured by Soft Jobs Data, Franc Climbs on Tariff Relief Hopes

Sterling fell mildly across the board today as weak UK labor market data reinforced expectations that the BoE would deliver a rate cut in December. Yet, as seen in comments from MPC member Megan Greene, not all policymakers are convinced, leaving December’s decision finely balanced.

The data comes just days after a closely divided 5–4 MPC vote to hold rates, with Governor Andrew Bailey’s deciding vote narrowly favoring caution. The combination of rising joblessness and easing wage momentum supports the view that inflationary pressures are subsiding faster than expected.

Traders now see the probability of a 25bps cut in December rising sharply, contingent on next week’s Autumn Budget confirming the deflationary tilt hinted at by Chancellor Rachel Reeves. Looking ahead, money markets are now pricing in 65bps of BoE rate cuts by end-2026, up from 55bps yesterday, suggesting investors expect a more extended easing cycle.

While Sterling weakened, Swiss Franc surged on reports that Washington and Bern are close to a deal to cut U.S. tariffs on Swiss exports. Multiple outlets, including Bloomberg, said the current 39% duty could be reduced to 15%, matching the rate applied to European Union goods. A Swiss economy ministry spokesperson declined to confirm details but said Economy Minister Guy Parmelin remains “in regular contact” with U.S. officials, including USTR Jamieson Greer.

In today’s currency rankings so far, Swiss Franc stands as the strongest performer, followed by Euro and New Zealand Dollar. At the other end of the spectrum, Sterling leads the laggards, trailed by Aussie and Loonie. Dollar and Kiwi sit in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.77%. DAX is up 0.08%. CAC is up 0.73%. UK 10-year yield is down -0.085 at 4.383. Germany 10-year yield is down -0.006 at 2.663. Earlier in Asia, Nikkei fell -014%. Hong Kong HSI rose 0.18%. China Shanghai SSE fell -0.39%. Singapore Strait Times rose 1.20%. Japan 10-year JGB yield fell -0.087 to 1.696.

BoE’s Greene wtays hawkish despite rise in UK unemployment

BoC policymaker Megan Greene pushed back against expectations for a December rate cut, saying this morning’s weaker labor data is not enough to change her stance.

Speaking at a conference in London, Greene—one of the five MPC members who voted to hold rates steady last week—argued that the labor market has likely moved past its sharpest adjustment phase.

She pointed to “higher-frequency data” showing early stabilization, adding that many companies still plan to lift wages substantially. Greene said it is “possible that the worst is behind us,” although she acknowledged that the latest 5.0% unemployment rate—the highest in four years—was “not great.”

UK unemployment rate jumps to four year high, wages growth slow

UK labor market data released today showed further cooling, reinforcing expectations that the BoC would deliver another rate cut in December.

In October, Payrolled employment fell -0.1% mom, or -32k, while claimant count rose 29k, exceeding expectations of a 20.3k rise. Wage pressures also eased significantly. Median monthly pay grew just 3.1% yoy, sharply down from 5.9% previously and marking the weakest pace since mid-2020.

In the three months to September, unemployment rate climbed from 4.8% to 5.0%, the highest in four years. Average earnings growth slowed from 5.0% yoy to 4.8% including bonuses, and from 4.7% yoy to 4.6% excluding them. Both readings highlight that the pay cycle is losing momentum as inflation falls and labor slack builds.

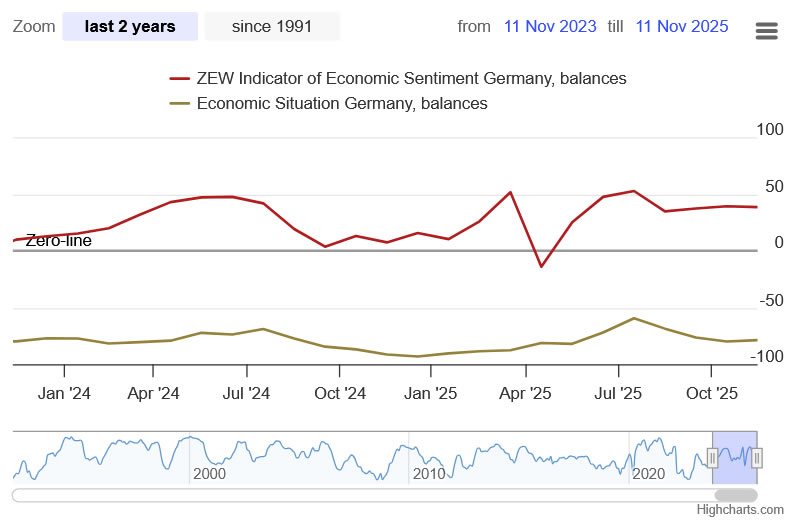

German ZEW falls to 38.5, but Eurozone improves

Investor confidence in Germany softened slightly in November, signaling continued caution about Europe’s largest economy despite signs of broader regional improvement. German ZEW Economic Sentiment Index slipped to 38.5 from 39.3, missing expectations of 42.5. Current Situation Index improved modestly from -80.0 to -78.7.

In contrast, Eurozone-wide ZEW Sentiment Index rose to 25.0 from 22.7, beating forecasts of 23.5. Current Situation Index improved to -27.3, up 4.5 points.

ZEW President Achim Wambach noted that while sentiment remains broadly stable, investors’ trust in Germany’s economic policy response has weakened. He said the government’s investment initiatives may deliver short-term stimulus, but "structural problems continue to exist”.

Australia Westpac consumer confidence surges to 103.8, marking end of prolonged pessimism

Australian consumer confidence jumped sharply in November, marking a clear break from years of pessimism. The Westpac Consumer Sentiment Index rose 12.8% mom to 103.8, its first positive reading since early 2022 and the highest in seven years, excluding the brief COVID-era spike. The surge was underpinned by a sharp improvement in views on the economy, with the 12-month and five-year outlook sub-indexes rising 16.6% and 15.3%, respectively—both now well above long-run averages.

Westpac said the result “draws a clearer line” under the prolonged period of consumer strain caused by high inflation, elevated interest rates, and rising tax burdens. The rebound likely reflects stronger domestic momentum, particularly in housing and consumer demand, as well as a more stable external backdrop. The recent de-escalation in U.S.–China trade tensions and a new Australia–U.S. deal on critical minerals have also buoyed sentiment.

The real surprise, according to Westpac, is how decisively these positive forces outweighed lingering worries about inflation and future rate settings. The data suggest households are regaining confidence in Australia’s recovery prospects even as monetary policy remains tight—offering a fresh signal that consumer resilience could help underpin growth heading into 2026.

RBNZ survey points to one more cut, then extended hold through 2026

New Zealand’s inflation expectations remain well anchored, while rate projections signal the RBNZ’s easing cycle is nearing its end.

The latest RBNZ Survey of Expectations showed the mean one-year-ahead inflation expectation edging up slightly to 2.39% from 2.37%. Two-year expectation stayed unchanged at 2.28%. Longer-term views were broadly steady, with the five-year expectation easing to 2.22% and the ten-year measure rising modestly to 2.18%—all consistent with the Bank’s 1–3% target midpoint.

Respondents now see the Official Cash Rate, currently at 2.50% following October’s 50bps cut, at 2.25% by year-end, implying just one more 25bps reduction before policy stabilizes. The one-year-ahead OCR expectation fell sharply to 2.31% from 2.86%, indicating that market participants expect the RBNZ to remain on hold through much of 2026 as inflation trends near target and growth moderates.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8762; (P) 0.8779; (R1) 0.8788; More…

EUR/GBP rebounded notably today but stays in range below 0.8828. Intraday bias remains neutral and more consolidations could be seen. Further rally is expected as long as 0.8761 support holds. On the upside, break of 0.8828 will resume the whole rise from 0.8221 and target 0.8867 fibonacci level. Firm break there will carry larger bullish implications. However, considering bearish divergence condition in 4H MACD, decisive break of 0.8761 will confirm short term topping, and bring deeper fall to 55 D EMA (now at 0.8710).

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Firm break of 0.8654 support will be the first sign that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high).

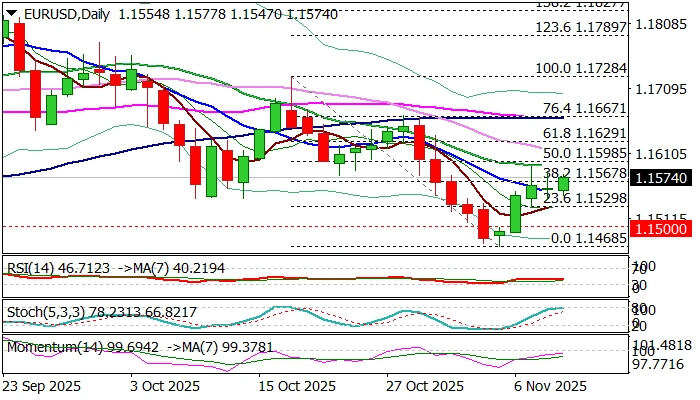

EUR/USD: Attempts Again Through Important Fibo Barrier

The Euro remains constructive and probes again through cracked Fibo resistance at 1.1570 (38.2% of 1.1728/1.1468 descend), as recovery leg from 1.1468 was boosted by formation of bear-trap on weekly chart (under Kijun-sen).

Repeated failure here in last two sessions (upticks were capped by 20 DMA and repeatedly failed to register close above this level) point to significance of the barrier.

Mixed technical signals (55/200DMA death-cross is forming at the upside and weighs along with still negative momentum and stochastic about to enter overbought territory) while formation of 5/10 bull-cross partially counters negative signals.

The dollar remains at the back foot against its major counterparts on fresh expectations of Fed rate cut (economists are optimistic about the condition of the US economy and inflation) though a series of delayed economic data are to be released as soon as the US government reopens, that would provide clearer picture.

We look for initial signal on reaction at 1.1570 pivot, with close above to brighten outlook and open way for attack at next significant barriers at 1.1590/98 (20DMA/Fibo 50%), violation of which to signal bullish continuation and expose targets at 1.1630 (Fibo 61.8%) and 1.1655 (daily cloud base.

Caution on repeated failure at 1.1570 Fibo level, though bullish bias expected to remain while the price holds above 10DMA (1.1543).

Better than expected results from Eurozone November ZEW economic sentiment likely to provide some support to the single currency.

Res: 1.1590; 1.1611; 1.1630; 1.1667.

Sup: 1.1543; 1.1500; 1.1446; 1.1391.

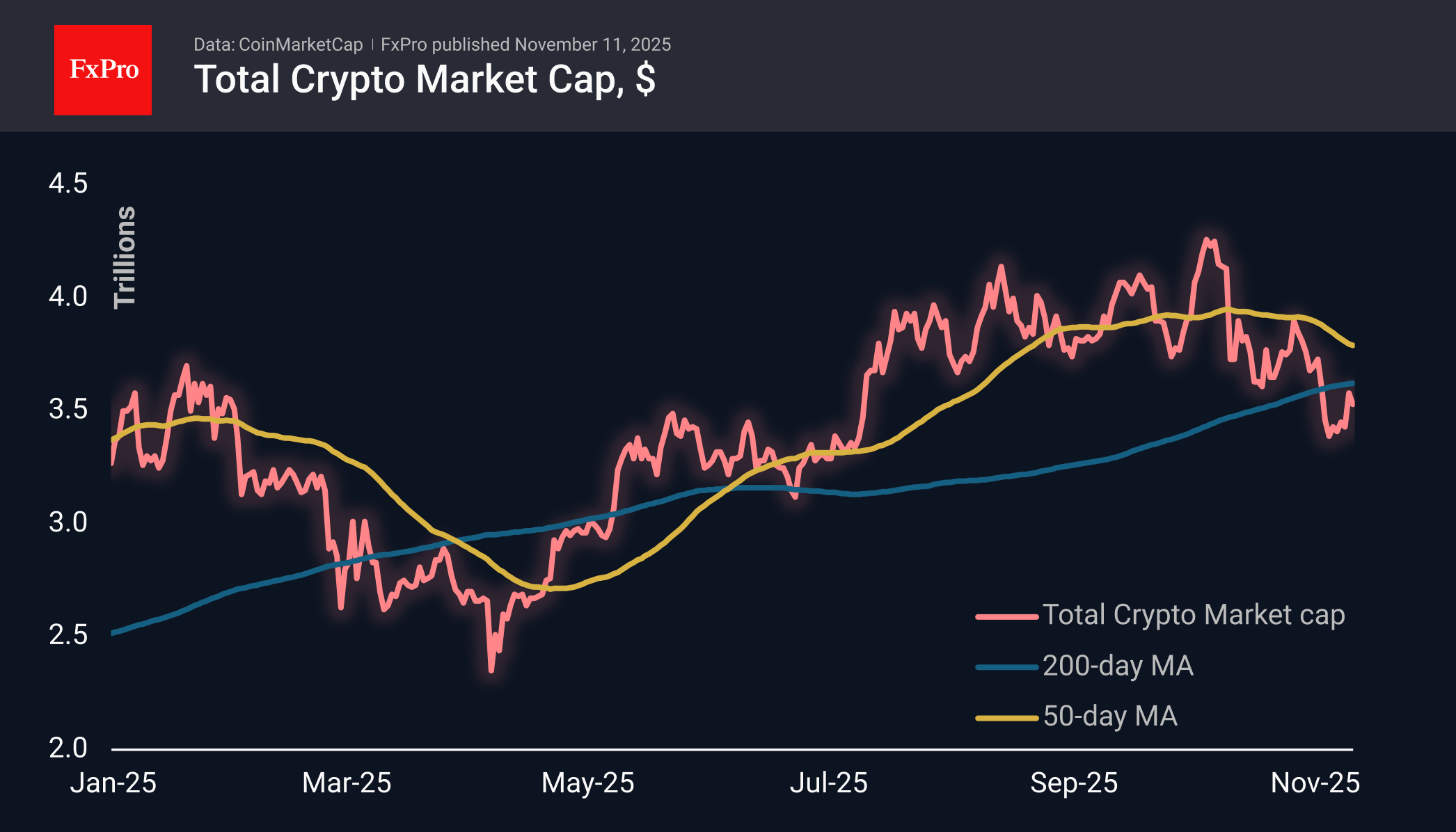

Is Ageing Crypto Bull Market Getting Tired?

Market Overview

The crypto market capitalisation fell by 1.1%, cooling off after an impressive surge in the first half of Monday. The 50-day moving average near $3.62 trillion acted as technical resistance, and the market’s climb stalled at $3.6 trillion. Despite Monday’s impressive surge, the market may be forming a new, lower local maximum, continuing the downward trend that began just over a month ago.

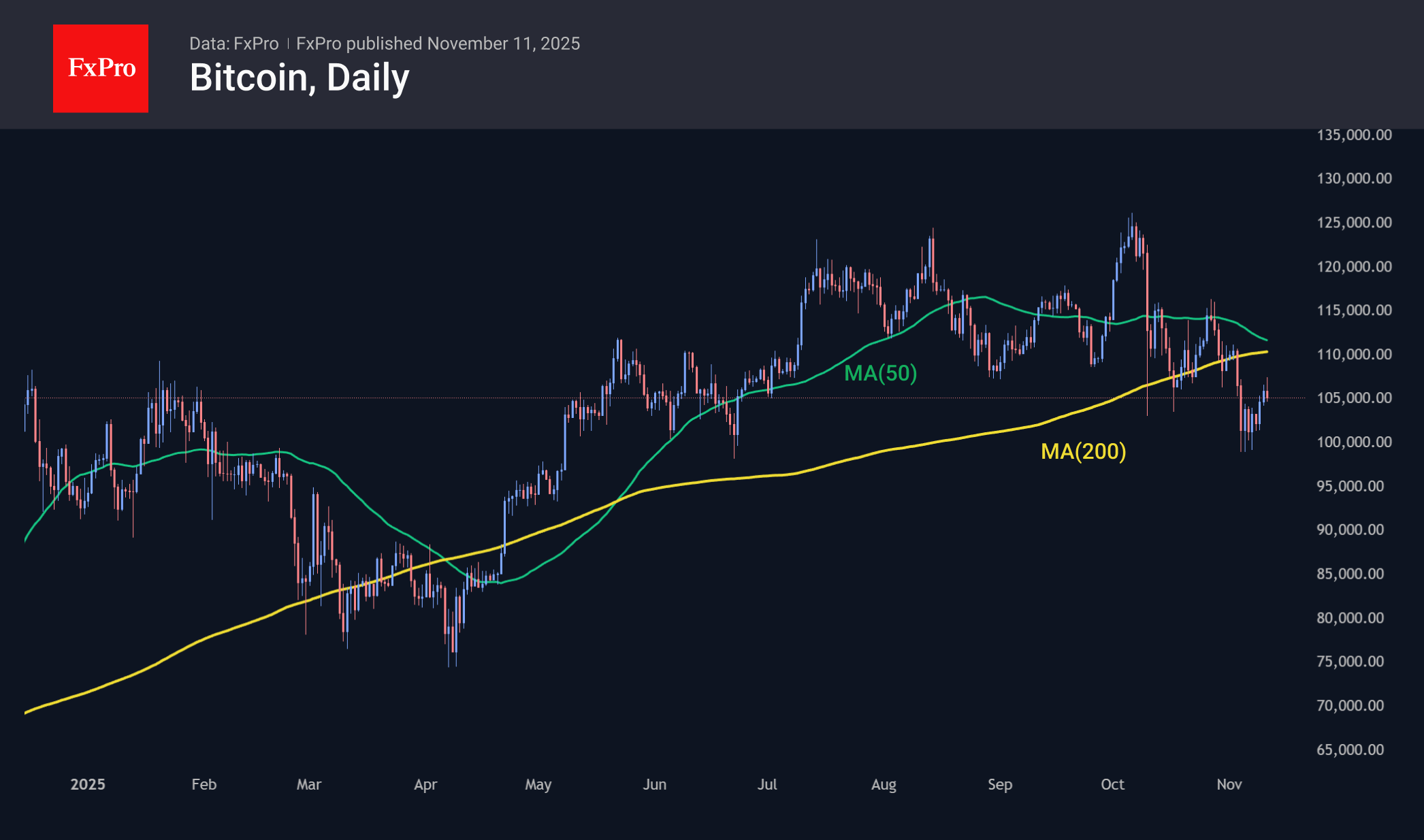

Bitcoin fell back below $105K, after briefly touching $107K this morning. The market is clearly not ready to switch to a mode of frenzied optimism, continuing to take profits after growth impulses have been realised. The reduction in support from corporate buyers is having an impact.

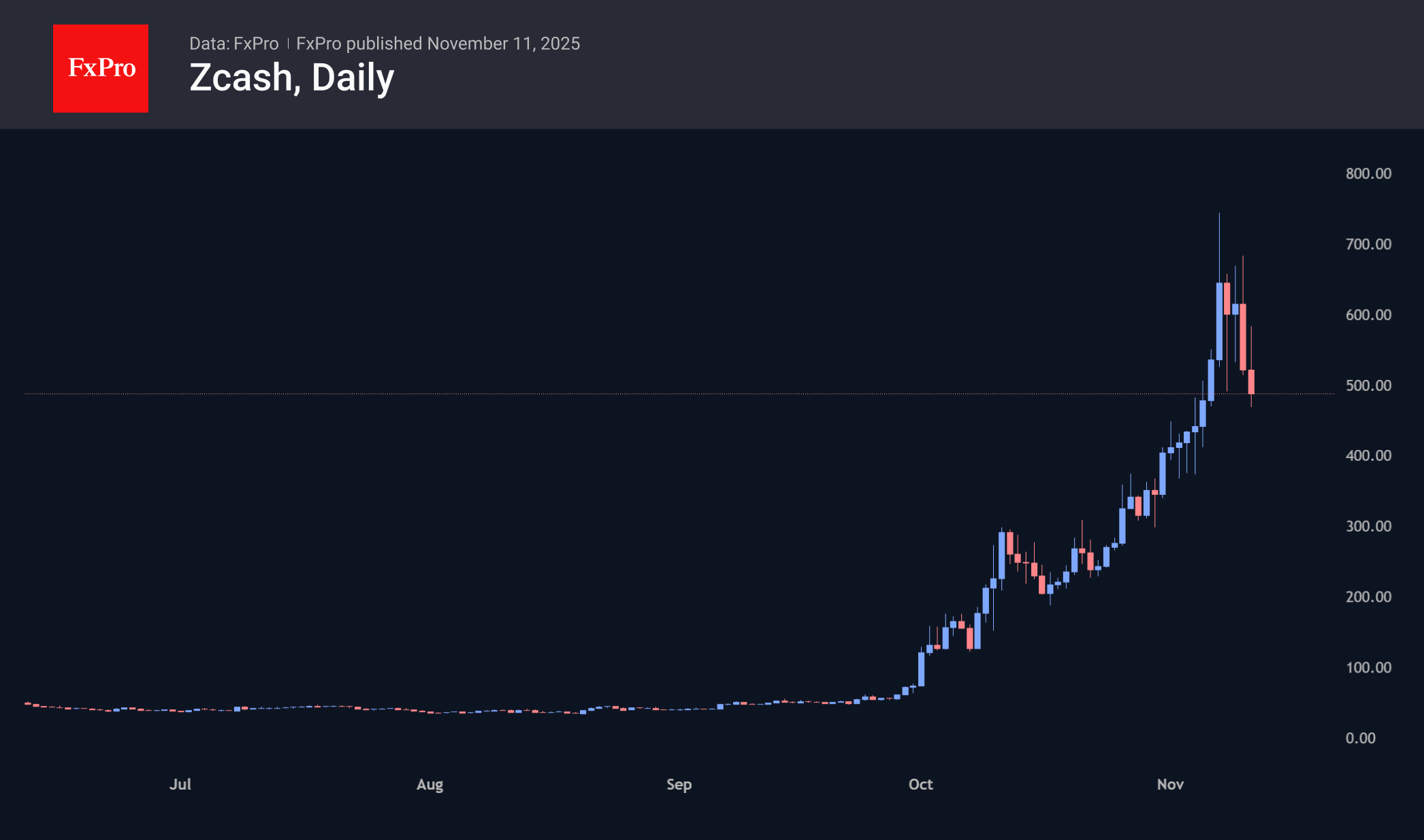

Zcash has fallen back to $477, losing almost 40% from its peak at the end of last week. Current developments continue to fuel our fears that we are witnessing nothing more than a repeat of the dynamics of previous years, when the sharp acceleration of altcoins, and ZEC in particular, occurred as the market was already in decline.

News Background

According to CoinShares, global crypto funds experienced an outflow of $1.172 billion last week, the highest in nearly three months. Investments in Bitcoin fell by $932 million, in Ethereum by $438 million, and in Sui by $4 million. Investments in Solana grew by $118 million, in XRP by $28 million, in HBAR by $27 million, and in Hyperliquid by $4 million.

The options market is not confident that Bitcoin will be able to renew its record highs by the end of the year, according to QCP Capital. The situation is exacerbated by continued selling by long-term holders and outflows from Bitcoin ETFs.

Artificial intelligence, quantum technologies, and gold have reduced investor interest in Bitcoin this year, according to Galaxy Digital, but the firm hopes that interest in BTC will return later.

Five XRP-based spot ETFs have appeared on the list of assets of the Depository Trust & Clearing Corporation (DTCC). This may indicate imminent approval of the products by the SEC. Market participants expect the launch of XRP ETFs as early as this month.

BoE’s Greene stays hawkish despite rise in UK unemployment

BoC policymaker Megan Greene pushed back against expectations for a December rate cut, saying this morning’s weaker labor data is not enough to change her stance.

Speaking at a conference in London, Greene—one of the five MPC members who voted to hold rates steady last week—argued that the labor market has likely moved past its sharpest adjustment phase.

She pointed to “higher-frequency data” showing early stabilization, adding that many companies still plan to lift wages substantially. Greene said it is “possible that the worst is behind us,” although she acknowledged that the latest 5.0% unemployment rate—the highest in four years—was “not great.”

German ZEW falls to 38.5, but Eurozone improves

Investor confidence in Germany softened slightly in November, signaling continued caution about Europe’s largest economy despite signs of broader regional improvement. German ZEW Economic Sentiment Index slipped to 38.5 from 39.3, missing expectations of 42.5. Current Situation Index improved modestly from -80.0 to -78.7.

In contrast, Eurozone-wide ZEW Sentiment Index rose to 25.0 from 22.7, beating forecasts of 23.5. Current Situation Index improved to -27.3, up 4.5 points.

ZEW President Achim Wambach noted that while sentiment remains broadly stable, investors’ trust in Germany’s economic policy response has weakened. He said the government’s investment initiatives may deliver short-term stimulus, but "structural problems continue to exist”.

USD/JPY Climbs to Fresh Nine-Month High

The USD/JPY pair advanced to 154.36 on Tuesday, edging closer to a new ten-month peak. The rally was driven by growing market optimism that the protracted US government shutdown may soon conclude, dampening demand for traditional safe-haven assets like the Japanese yen.

In Japan, Economic Recovery Minister Minoru Kiuchi highlighted the domestic challenges posed by the currency's weakness, warning that a soft yen risks amplifying inflationary pressures by increasing the cost of imports. He called for vigilant monitoring of the situation.

Concurrently, a draft of the government's new economic stimulus plan—scheduled for approval on 21st November—reveals that Prime Minister Sanae Takaichi's cabinet will urge the Bank of Japan to prioritise economic growth alongside price stability. The programme is also set to feature tax breaks and investment incentives targeting 17 key industries.

This comes as the Bank of Japan's October report reaffirmed its close watch on wage growth to determine the timing of its next potential rate hike. In a positive economic sign, the country registered a record current account surplus of ¥4.5 trillion in September, bolstered by robust export growth.

Technical Analysis: USD/JPY

H4 Chart:

On the H4 chart, USD/JPY has formed a consolidation range around 153.80. We anticipate an upward expansion of this range towards 154.80. Following this, a pullback to retest the 153.80 level from above is expected. This would likely set the stage for the next leg of the uptrend, targeting 155.70. This bullish scenario is technically confirmed by the MACD indicator, whose signal line is firmly above zero and pointing upwards, indicating sustained positive momentum.

H1 Chart:

On the H1 chart, the pair has completed an initial growth impulse to 154.48. A near-term correction towards 153.65 is now expected. Once this corrective phase concludes, we anticipate the resumption of the broader upward trend, with the next primary target at 155.70. The Stochastic oscillator corroborates this view. Its signal line is below 50 and trending downwards towards 20, suggesting that short-term downward pressure (the expected correction) is building before the next potential upward wave.

Conclusion

USD/JPY continues its ascent, propelled by renewed risk appetite and domestic Japanese policy that implicitly favours a weaker yen. While minor corrective dips are anticipated in the short term, the overall technical and fundamental backdrop remains bullish. The path of least resistance points towards a test of 155.70, provided the pair maintains its footing above key support near 153.80.

Disclaimer:

Any forecasts contained herein are based on the author’s particular opinion. This analysis may not be treated as trading advice. RoboForex bears no responsibility for trading results based on trading recommendations and reviews contained herein.