Sample Category Title

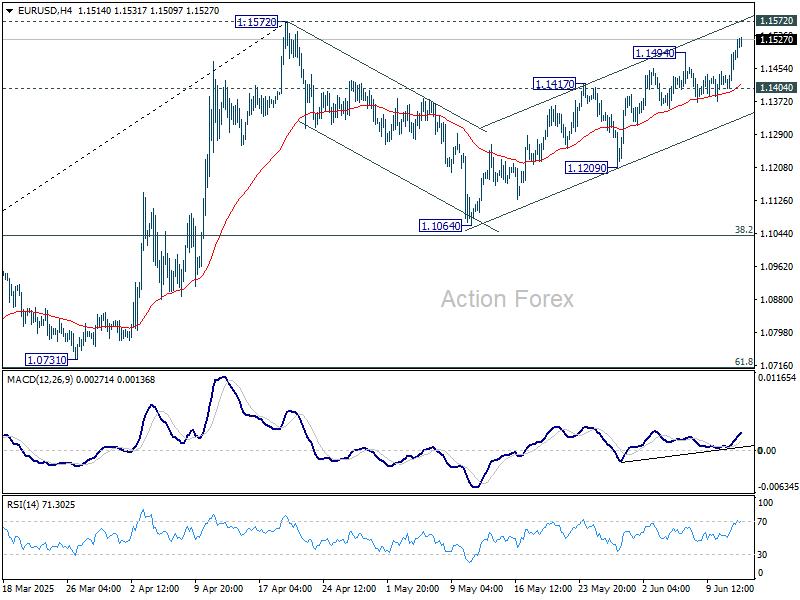

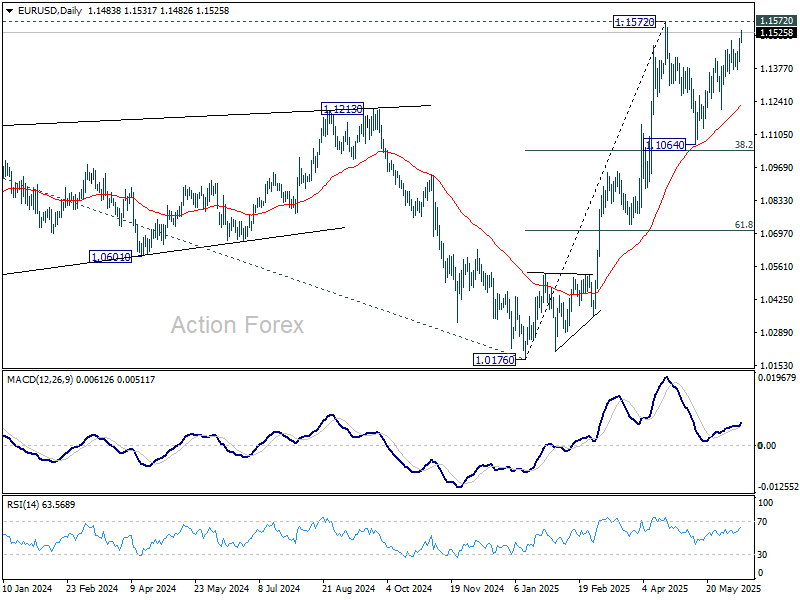

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1429; (P) 1.1465; (R1) 1.1524; More...

EUR/USD's rise from 1.1064 resumed by breaking through 1.1494 and intraday bias is back on the upside for 1.1572 high. Strong resistance could be seen there to bring another fall, to extend the near term consolidation pattern. Firm break of 1.1404 support will turn intraday bias back to the downside for 1.1209 first. However, decisive break of 1.1572 will resume whole rise from 1.0176.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0894) holds.

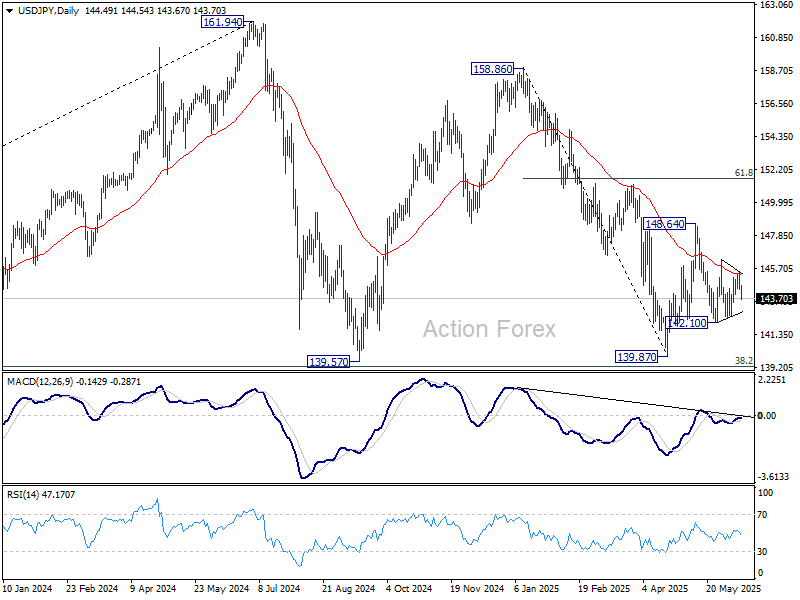

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.13; (P) 144.80; (R1) 145.27; More...

Intraday bias in USD/JPY stays neutral as range trading continues. On the upside, above 146.27 resistance will argue that price actions from 148.64 has completed as a corrective pattern. Intraday bias will be back on the upside for 148.64 resistance and above to resume the rebound from 139.87 low. However, firm break of 142.10 will bring retest of 139.87 instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

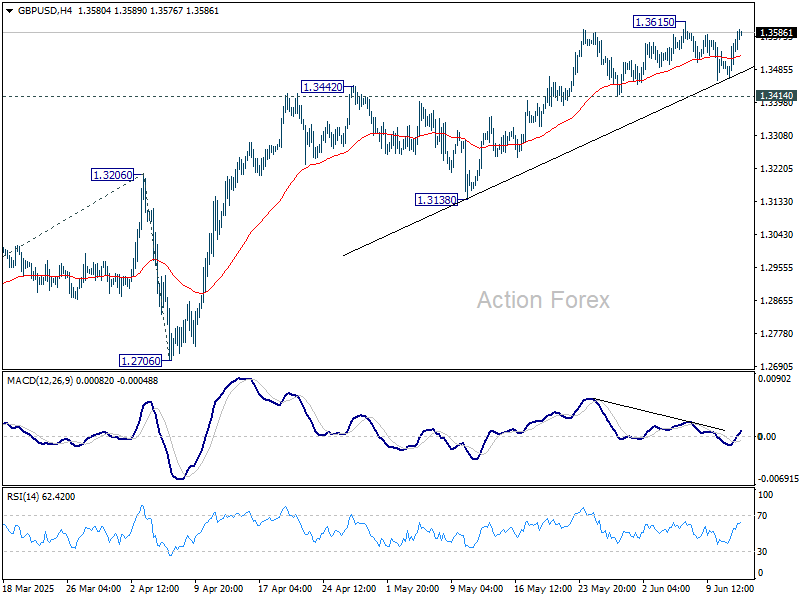

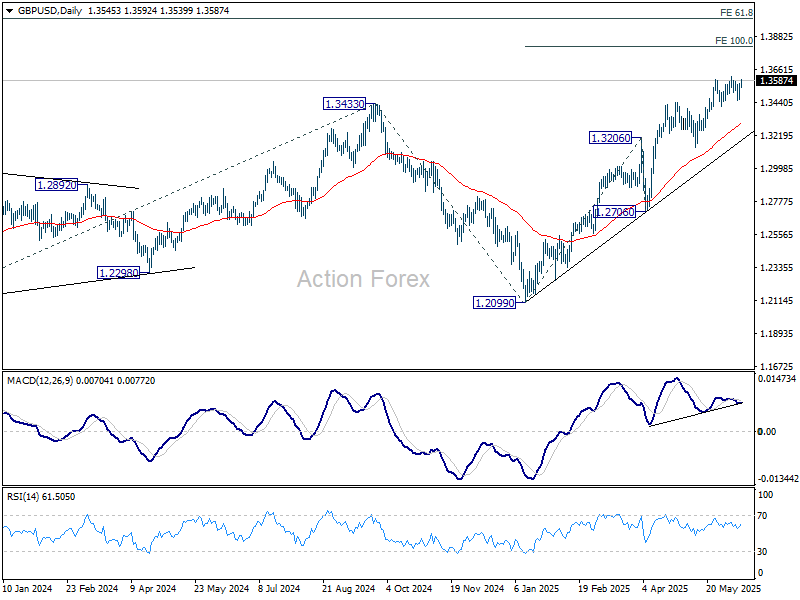

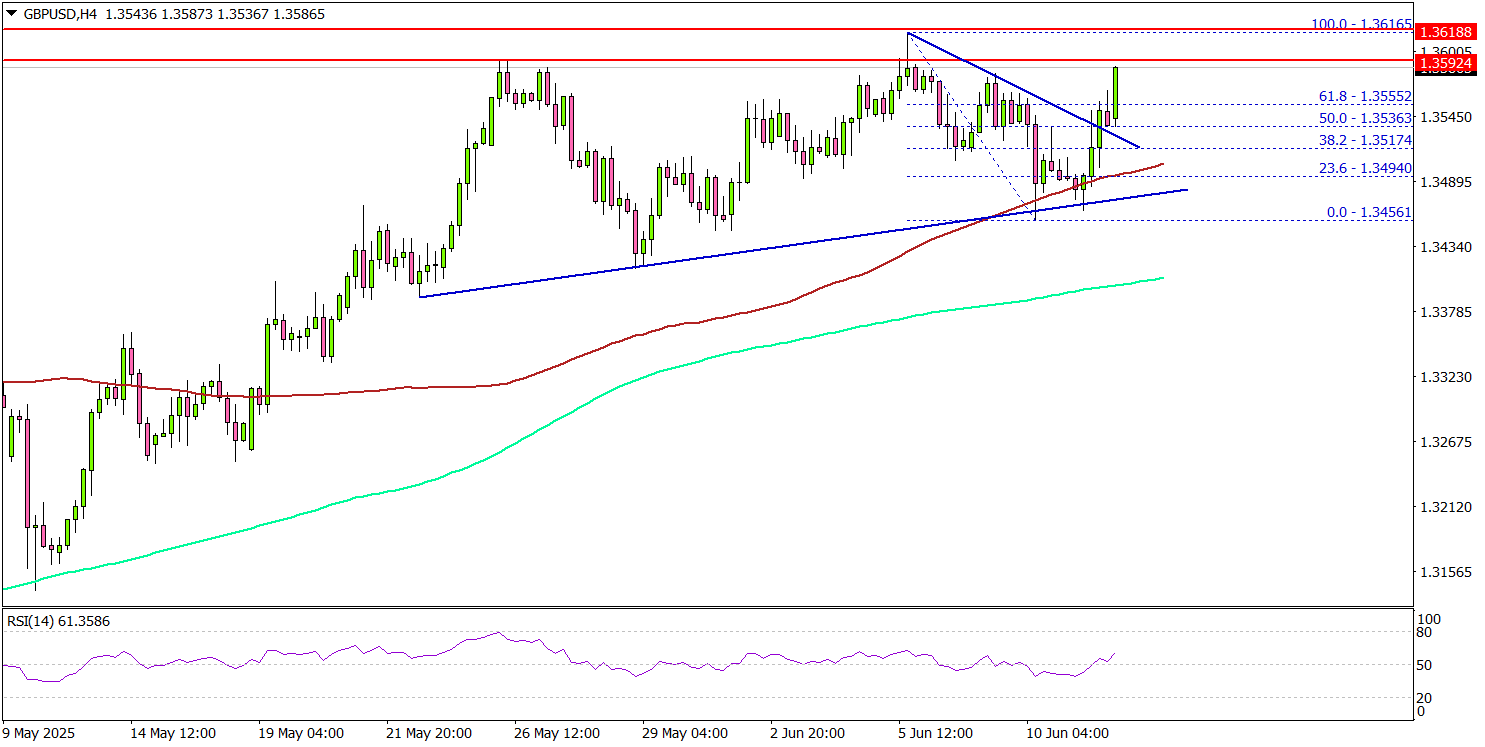

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3486; (P) 1.3526; (R1) 1.3589; More...

GBP/USD is still bounded in range below 1.3615 and intraday bias remains neutral. With 1.3414 support intact, further rally remains in favor. On the upside, break of 1.3615 will resume the rally from 1.2099 and target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. On the downside, break of 1.3414 support should confirm short term topping, and bring deeper correction to 55 D EMA (now at 1.3300) instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2913) holds, even in case of deep pullback.

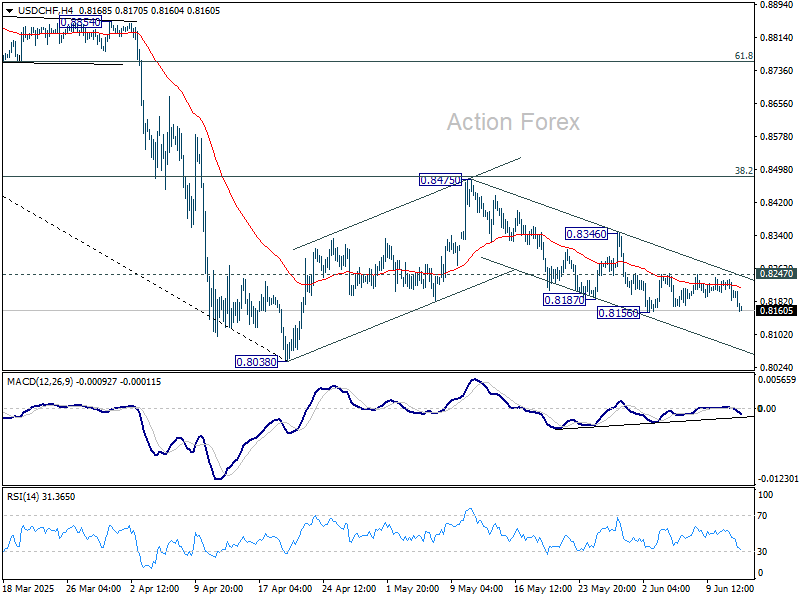

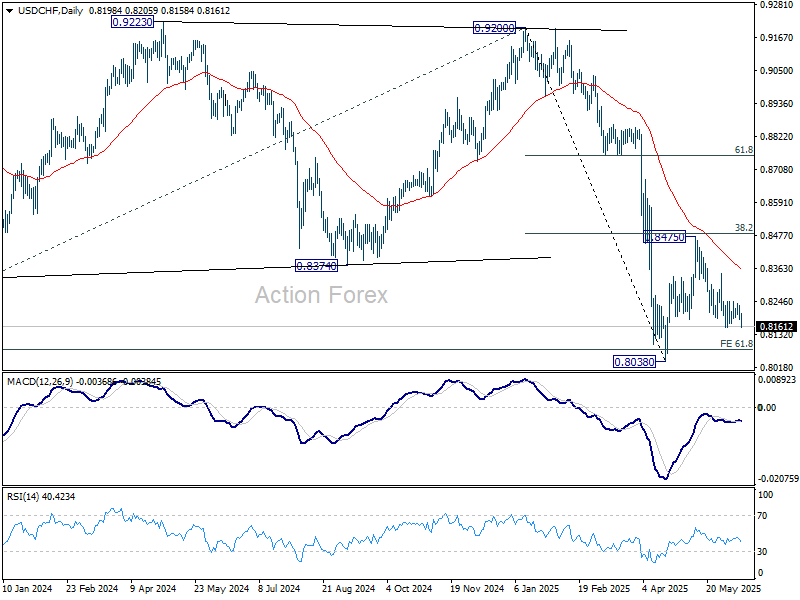

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8180; (P) 0.8209; (R1) 0.8234; More….

Immediate focus is now on 0.8156 support in USD/CHF with current fall. Firm break there would resume the decline from 0.8475 to retest 0.8038 low. Strong support could be seen there to bring rebound to extend the near term consolidation pattern. On the upside, above 0.8247 resistance will turn bias to the upside for 0.8346 resistance first.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8696) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

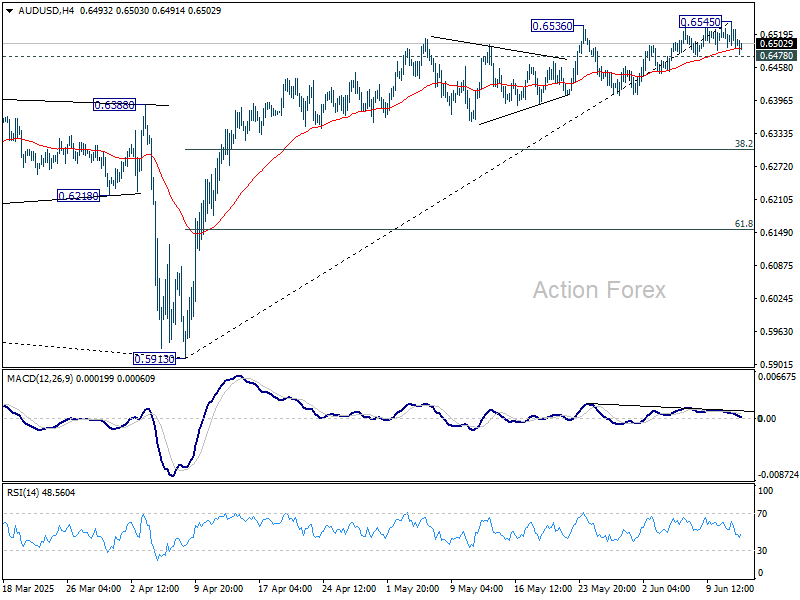

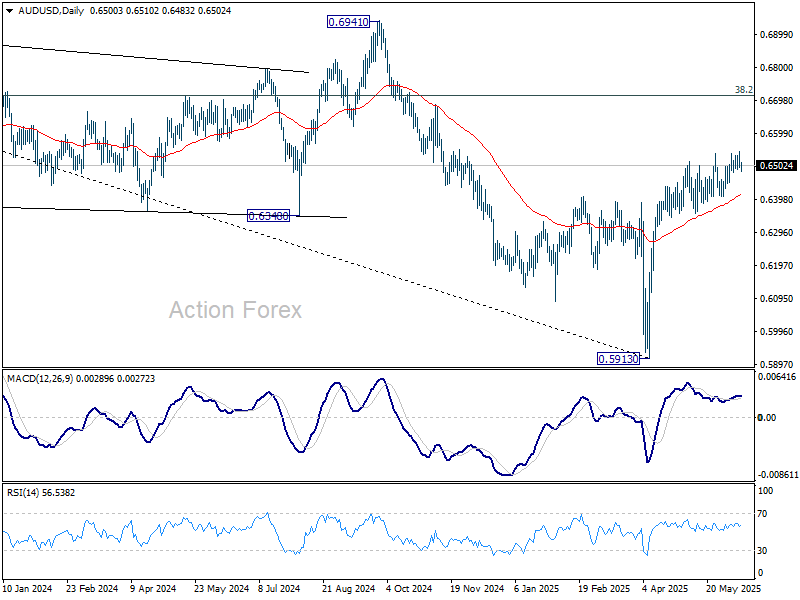

AUD/USD Daily Report

Daily Pivots: (S1) 0.6483; (P) 0.6514; (R1) 0.6533; More...

AUD/USD quickly lost momentum after edging higher to 0.6545 and intraday bias is turned neutral again. Considering bearish divergence condition in 4H MACD, break of 0.6478 support will turn bias back to the downside for 55 D EMA (now at 0.6413) and possibly below. On the upside, firm break of 0.6545 will resume larger rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548.

In the bigger picture, AUD/USD is still struggling to sustain above 55 W EMA (now at 0.6443) cleanly, and outlook is mixed. Sustained trading above 55 W EMA will indicate that rise from 0.5913 is at least correcting the down trend from 0.8006 (2021 high), with risk of trend reversal. Further rise should be seen to 38.2% retracement of 0.8006 to 0.5913 at 0.6713. However, rejection by 55 W EMA will revive medium term bearishness for another fall through 0.5913 at a later stage.

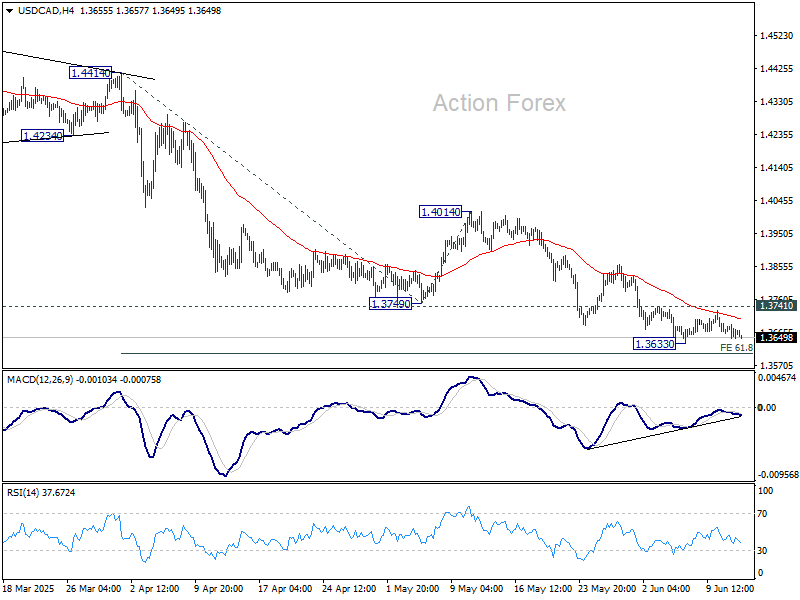

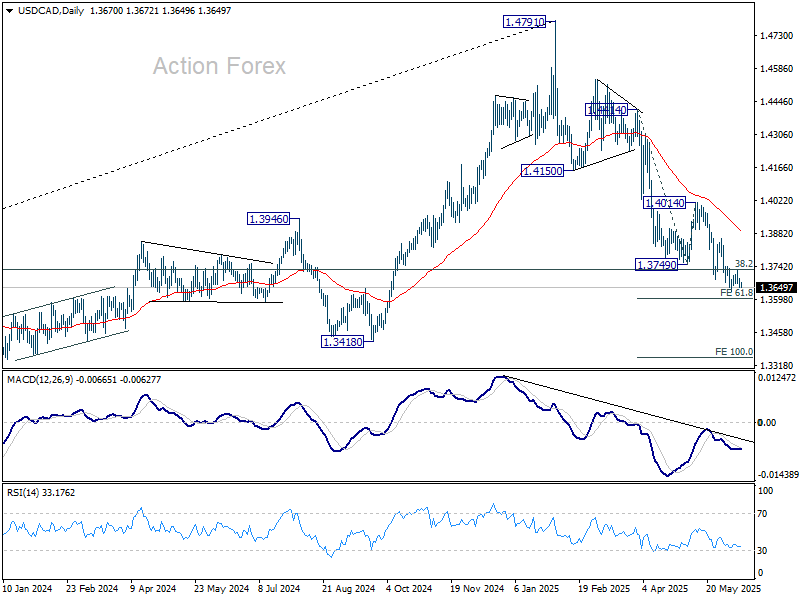

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3651; (P) 1.3671; (R1) 1.3691; More...

USD/CAD is still bounded in established range above 1.3633 and intraday bias stays neutral. Considering bullish convergence condition in 4H MACD, firm break of 1.3741 will indicate short term bottoming at 1.3633. Intraday bias will turn back to the upside for stronger rebound to 1.4014 resistance, as a correction to fall from 1.4791. Nevertheless, decisive break of 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603 will pave the way to 100% projection at 1.3349.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

Japanese business confidence sours amid tariff fears and profit warnings

Business sentiment in Japan deteriorated sharply in Q2, with the Ministry of Finance’s survey revealing a broad-based loss of confidence across industries.

The overall index for large firms slipped into negative territory at -1.09, down from Q1’s modest 2.0. Large manufacturers saw sentiment weaken further from -2.4 to -4.8, while large non-manufacturers experienced a steep drop from 5.2 to -5.7, suggesting that economic uncertainty is spreading beyond export-heavy sectors.

The survey also highlighted a growing sense of earnings pessimism. Large manufacturers now expect recurring profits to decline -1.2% in the fiscal year ending March 2026, a downgrade from the -0.6% fall seen in the previous survey. Particularly alarming is the auto sector's outlook, with automakers and parts suppliers projecting a severe -19.8% drop in profits.

This highlights the mounting concern over the impact of steep US tariffs, which threaten to hit Japan’s flagship export industry hard and weigh on broader economic momentum.

RBA Won’t Rush, But Will Cut More Next Year

We continue to expect RBA to hold in July and cut in August and November. A lower inflation outlook now makes two further cuts in early 2026 likely.

We have retained our current expectations for the near-term path for the RBA cash rate: a 25bp cut in August – not July – and another in November. We have added two more 25bp cuts in early 2026 (February and May), though they could be earlier (December and February or February and March) if inflation and the labour market turn out weaker late in 2025 than we currently expect. That would mean RBA cash rate will bottom out at 2.85%, from a peak of 4.35%, and 3.85% currently. We regard the cash rate at 2.85% as being at the lower end of the ‘neutral range’.

A few months ago, in February, the RBA was sceptical that it would cut rates at all, beyond removing the ‘insurance’ against upside risks that it had taken out in November 2023. At its latest (May) meeting it was confident enough in the disinflation so far that it was comfortable with the market pricing for the cash rate.

Let’s not get ahead of ourselves, though. The Board described itself as having a preference to move cautiously and predictably. This is code for not wanting to do back-to-back cuts. It also made it clear in the minutes that this was about reducing restrictiveness, not moving quickly back to neutral in the style of the Federal Reserve last year. And the Board is not in the habit of changing policy just because the market is pricing it in.

Nothing that has happened since, including a disappointing GDP number, has been enough to tip the RBA into changing its mind in the near term. Neither is the data flow between now and the next meeting likely to shift the dial on the near-term outlook. The May labour force data out next week is likely to show a labour market that still looks tighter than the RBA’s view of full employment. And while the May monthly CPI indicator, to be published on 25 June, is likely to be a low one, the steer from April and May suggests that June quarter CPI is likely to be a bit above what the RBA is forecasting. Given this, the overall data flow will be enough to convince the Board that further reduction in policy restrictiveness is warranted. It will not, however, be enough to induce it to rush that withdrawal of restrictiveness.

Looking forward, though, the arguments in favour of doing more than 50bps more (two cuts) are building. In particular, the outlook for inflation is shifting in the face of slowing population growth and a handover from public to private sector demand growth that is looking shakier.

Recent data has made it clear that population growth is unwinding a bit faster than previously thought. We have assessed that this is enough to have implications for housing costs, particularly rents. Over time, this puts a little more downside into measures of underlying inflation. We are also seeing a bit more downside in some parts of services inflation.

In our view, these and other shifts are enough to take trimmed mean inflation below the midpoint of the target range for a time, starting around the end of this year. We believe that would tip the RBA in favour of cutting the cash rate further. Our previous forecasts did not have trimmed mean inflation going below the 2.5% midpoint of the RBA’s 2–3% inflation target. Such a forecast would not have comported with a policy stance involving the real (inflation-adjusted) cash rate as low as a 2.85% nominal cash rate implies. But our current forecasts, as released by Westpac Senior Economic Justin Smirk this morning, are enough to change the policy calculus.

Indeed, if we are right, the RBA might be in for a bit of an ‘oh crikey!’ moment late this year. A ‘shaky handover’ from the post-expansion normalisation in the care economy and the completion of a raft of state government infrastructure projects could weigh on both output and employment. The parallels with the late 2010s we have previously highlighted could become even clearer. Consumer spending is tracking weakly, as we expected. We are now starting to see this weigh on business activity. The result is likely to be soggy growth and surprisingly weak wages growth despite apparently low unemployment (and despite the RBA’s beliefs about the implications of below-par measured productivity growth). In that case, what at first looked like an inflation trajectory solidly anchored at or above the 2.5% midpoint of the target range will instead look more like our forecasts, drifting below 2.5% for a time.

(We also cannot rule out that the forthcoming update to the Statement on the Conduct of Monetary Policy refines the language on how assiduous the RBA needs to be about hitting the 2.5% midpoint of the target range exactly. When the Governor flagged at last month’s media conference that a new agreement was in the works, it did raise the question of why the current agreement needed revision, less than 18 months after it was published. If a new agreement is finalised soon, the current one will be the shortest-lived of any of them other than the 2006 agreement superseded by the change of government in 2007. This could just be an update now that the new Monetary Policy Board is in place. But perhaps the February episode also spurred a ‘no, not like that!’ reaction in the Government. We will know soon enough.)

As we have previously noted, the risks remain on the downside. It is possible that some of these cuts come a bit faster than the ‘cautious’ path we currently have pencilled in. This will depend on the evolving data flow, particularly for the labour market and inflation, as well as the RBA’s evolving beliefs about what constitutes full employment.

GBP/USD Rises Further—Bulls Tighten Grip as Rally Accelerates

Key Highlights

- GBP/USD started a fresh increase above the 1.3520 resistance.

- It cleared a contracting triangle with resistance at 1.3535 on the 4-hour chart.

- EUR/USD is gaining pace and might clear the 1.1550 resistance.

- Bitcoin price struggled to clear the $110,500 resistance zone.

GBP/USD Technical Analysis

The British Pound remained well-bid above 1.3350 against the US Dollar. GBP/USD climbed above the 1.3450 and 1.3500 resistance levels.

Looking at the 4-hour chart, the pair settled above the 1.3520 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). It cleared a contracting triangle with resistance at 1.3535.

On the downside, immediate support is near the 1.3550 level. The next key support sits near 1.3520. Any more losses could send the pair toward the 1.3500 pivot level and the 100 simple moving average (red, 4-hour) in the near term. The main support could be near 1.3440.

On the upside, the pair could face resistance near the 1.3620 level. The next key resistance sits near the 1.3650 level. The first major resistance sits at 1.3700. A close above the 1.3700 level could set the pace for another increase.

In the stated case, the pair could even clear the 1.380 resistance. The next major stop for the bulls could be near the 1.4000 resistance.

Looking at EUR/USD, the pair started another increase, but the bulls seem to be facing hurdles near the 1.1550 level.

Upcoming Economic Events:

- US Initial Jobless Claims - Forecast 240K, versus 247K previous.

- US Producer Price Index for May 2025 (YoY) – Forecast +0.2%, versus -0.5% previous.

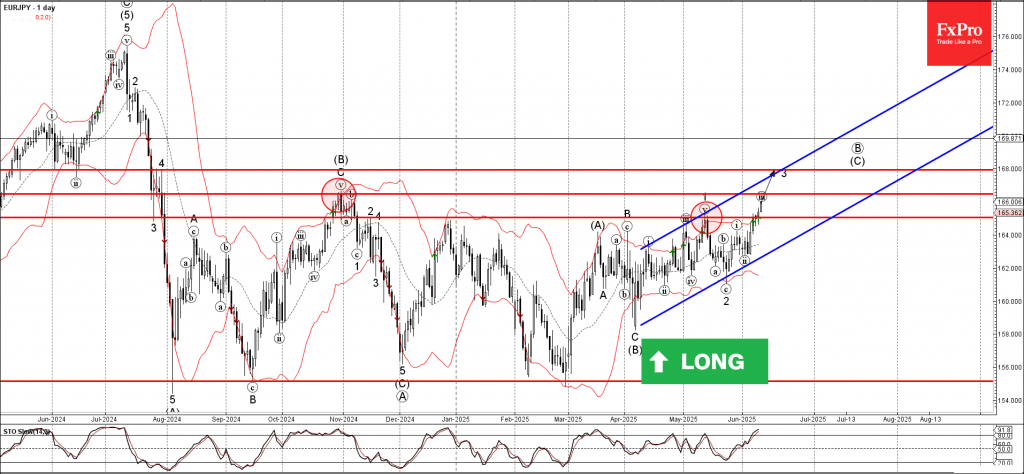

EURJPY Wave Analysis

EURJPY: ⬆️ Buy

- EURJPY broke the key resistance level 165.00

- Likely to rise to the resistance level 168.00

EURJPY currency pair recently broke the key resistance level 165.00 (which has been steadily reversing the pair from the start of November, as can be seen from the daily EURJPY chart below).

The breakout of the resistance level at 165.00 accelerated the active sub-impulse wave 3 of the higher-order impulse wave (C) from April.

EURJPY currency pair can be expected to rise to the next resistance level 166.50 (former multi-month high from November) – the breakout of which can lead to further gains toward 168.00.